ACCA F6 FA09 Study Text 2010

Подождите немного. Документ загружается.

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 385

Paper F6 (UK)

Taxation FA2009

CHAPTER

22

Self assessment and PAYE

Contents

1 Notification of chargeability

2 Filing returns

3 Amendments, enquiries and appeals

4 Payment of tax

5 The PAYE system

Paper F6 (UK): Taxation FA2009

386 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Notification of chargeability

Notification by companies

Notification by individuals

Penalties for failure to notify chargeability

1 Notification of chargeability

1.1 Notification by companies

When a company first comes within the scope of corporation tax (i.e. when it first

has profits that are chargeable to corporation tax), it must notify HMRC of its

chargeability to tax within three months after the start of its first accounting period.

Companies that have been trading for a while usually receive a notice (reminder), a

few weeks before the end of their regular accounting end date, of their self

assessment obligation to file a corporation tax return. If a company with taxable

profits does not receive a return, it must notify HMRC within 12 months of the end

of its accounting period.

1.2 Notification by individuals

Where an individual first comes within the scope of income tax or capital gains tax,

or acquires a new source of income, he must notify HMRC of his chargeability to tax

by 5 October following the end of the tax year in which the new source of income or

gain arose. For example, for 2009/10, HMRC must be notified by 5 October 2010.

1.3 Penalties for failure to notify chargeability

Failure to notify chargeability can result in a penalty. This is determined according

to the new single penalty regime that applies to income tax, capital gains tax,

corporation tax and VAT.

The amount of penalty is based on the ‘potential lost revenue’. This is the amount of

tax due but unpaid by 31 January following the tax year (or 12 months following the

end of the accounting period for companies) as a result of the late notification. The

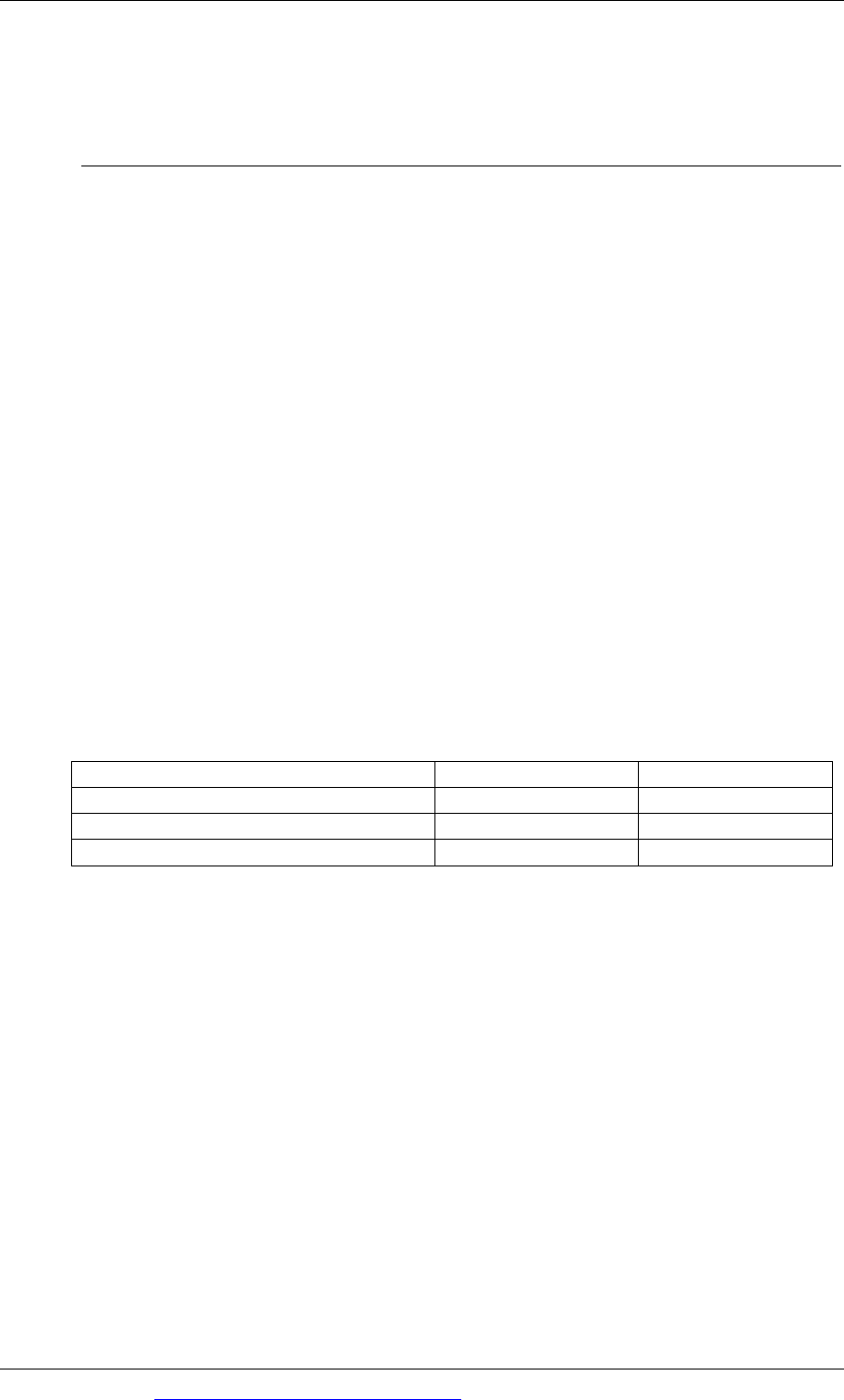

taxpayer’s behaviour also affects the amount of penalty payable:

Type of behaviour Maximum penalty Minimum penalty

Deliberate and concealed 100% 30%

Deliberate but not concealed 70% 20%

Any other case 30% Nil

The minimum penalties apply only where the taxpayer makes an unprompted

disclosure to HMRC. To avoid a penalty entirely the unprompted disclosure must

be made within 12 months of the date notification was due.

Chapter 22: Self assessment and PAYE

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 387

Filing returns

Filing a corporation tax return

Penalties for late filing of a corporation tax return

Filing an income tax return

Penalties for late filing of an income tax return

Penalties for incorrect returns

2 Filing returns

2.1 Filing a corporation tax return

A company must complete a corporation tax return (Form CT600) and submit it to

HMRC within 12 months of the end of its period of account, or three months from

the date on which the notice to complete a return was issued, if later.

The return contains all the information required to calculate the company’s PCTCT

for the accounting period. It also enables the company to claim reliefs and

allowances (e.g. loss reliefs and capital allowances).

The company must also calculate its own corporation tax liability and submit a copy

of its financial accounts with its self assessment form.

2.2 Penalties for late filing of a corporation tax return

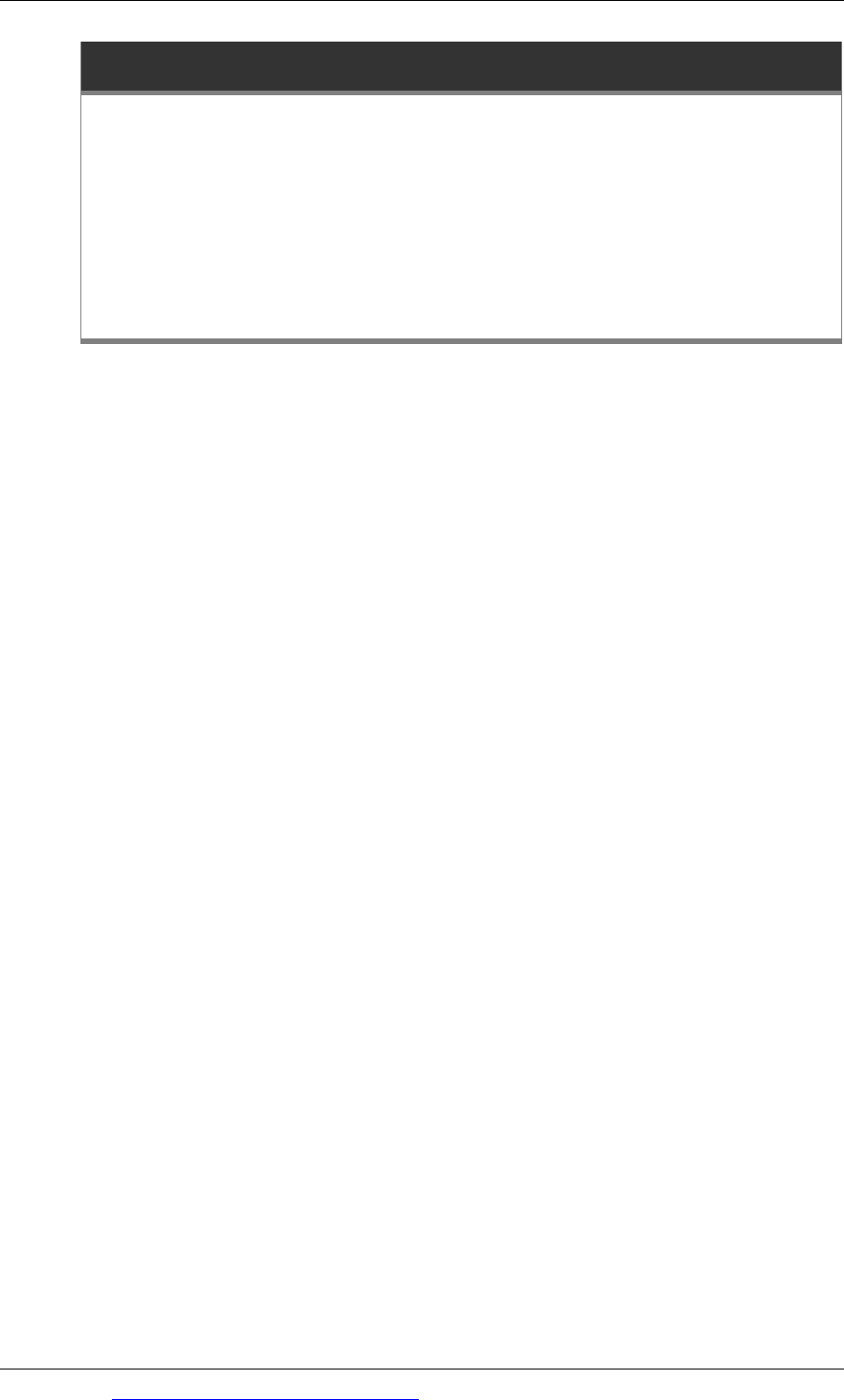

Penalties are levied if the corporation tax return is filed late, as follows:

Filed within Maximum penalty

3 months of filing date £100 fixed penalty.

Increased to £500 if the company becomes liable

to the fixed penalty for three consecutive years.

3 to 6 months of the filing

date

£200 fixed penalty.

Increased to £1,000 if the company becomes liable

to the fixed penalty for three consecutive years.

18 to 24 months after the

end of the accounting period

£200 fixed penalty

plus 10% of the tax outstanding 18 months after

the end of the accounting period

More than 24 months after

the end of the accounting

period

£200 fixed penalty

plus 20% of the tax outstanding 18 months after

the end of the accounting period

Paper F6 (UK): Taxation FA2009

388 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

2.3 Filing an income tax return

The self assessment system for individuals covers:

income tax

Class 4 NICs, and

capital gains tax.

Individuals whose liability to income tax is not settled in full by deduction of tax at

source (for example, through the PAYE system) are required to submit a self

assessment return to HMRC.

Individuals who are likely to need to submit a tax return usually receive a blank

return automatically from HMRC around the end of the tax year (i.e. March/April).

An individual must complete the relevant sections of the tax return and submit it to

HMRC.

The full income tax return consists of a summary form, supplementary pages and a

tax calculation section.

The individual is required to complete the summary form and the appropriate

supplementary pages in full. As regards the completion of the tax calculation

section:

If the return is filed on-line, the tax calculation section is automatically

completed as part of the filing process.

If a paper return is filed, HMRC will do the tax calculation for the individual if

he so wishes, provided the return is filed on time.

If the taxpayer wishes to submit his return on-line, the normal due date for filing the

return is the later of:

31 January following the end of the tax year (i.e. for 2009/10, by 31 January

2011), or

3 months after the issue of the return.

If the taxpayer wishes to submit a traditional paper return, he must do so by the

later of:

31 October following the end of the tax year (i.e. for 2009/10, by 31 October

2010), or

3 months after the issue of the return.

Chapter 22: Self assessment and PAYE

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 389

2.4 Penalties for late filing of an income tax return

Penalties are levied on individuals for late submission of a tax return, as follows:

Filed Maximum penalty

Within 6 months of filing date £100 fixed penalty

Within 6 to 12 months of the filing date £200 fixed penalty

More than 12 months after the filing date £200 fixed penalty plus up to 100%

of the tax liability for the year

If the fixed penalty of £100 is seen to be insignificant to the individual, HMRC may

apply to the tribunal for a penalty of up to £60 per day to apply instead.

The penalties (excluding the daily penalty) cannot exceed the amount of tax

outstanding at the date the return was due.

2.5 Penalties for incorrect returns

A single penalty regime for incorrect returns applies:

to incorrect income tax returns

to incorrect corporation tax returns and

where a misdeclaration has been made on a VAT return.

The penalty will be based on the amount of tax understated and the taxpayer’s

behaviour. The penalty will be:

Type of behaviour Maximum penalty Minimum penalty

Deliberate and concealed 100% 30%

Deliberate but not concealed 70% 20%

Careless 30% Nil

Any penalty will be substantially reduced where a taxpayer makes disclosure,

especially when this is unprompted by HMRC. For example, if a taxpayer makes an

unprompted disclosure of an incorrect return following a failure to take reasonable

care, the penalty could be reduced to nil.

Paper F6 (UK): Taxation FA2009

390 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Amendments, enquiries and appeals

Deadlines for amendments

Enquiries

HMRC’s information and inspection powers

Appeals

Determination assessments

Discovery assessments

Record keeping

3 Amendments, enquiries and appeals

3.1 Deadlines for amendments

HMRC’s right to repair

HMRC have the right to repair (i.e. correct) a taxpayer’s return within 9 months of

the date of receipt, if there are obvious errors or omissions (such as arithmetical

errors and missing pages).

The taxpayer’s right to amend

The taxpayer has the right to amend their return within 12 months of the due filing

date.

For example, for 2009/10, an individual has the right to amend until 31 January

2012, regardless of whether the return is paper-based or filed on-line.

Claims for recovery of overpaid tax

If a taxpayer believes he has overpaid tax, he may make a claim for repayment after

the amendment deadline but within four years of the end of the tax year (accounting

period for companies). However, a mistake is ineligible for relief if the return was

made in accordance with the generally prevailing practice at the time.

3.2 Enquiries

HMRC have the right to enquire into a return to check for completeness and

accuracy.

A return may be investigated:

because information is received by HMRC that does not tie up with the return,

or

as a result of HMRC’s random selection process, whereby it selects a small

percentage of returns to check.

Chapter 22: Self assessment and PAYE

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 391

HMRC are not obliged to disclose the reason for the enquiry to the company.

However, they must give written notice before commencing an enquiry, within 12

months of the date of receipt of the return.

Normally, if HMRC does not issue an enquiry notice within the appropriate time

limit, the self assessment may be regarded as agreed and finalised.

On the completion of an enquiry, HMRC must issue a written notice stating:

that the enquiry has been completed, and

the outcome of the enquiry.

Within 30 days of the completion of the enquiry, the taxpayer must amend their self

assessment as required by HMRC.

If the taxpayer refuses to amend their self assessment, or does not amend the return

according to HMRC’s request, HMRC have the right to impose their assessment

within 30 days of the refusal or inadequate amendment.

The taxpayer can appeal against HMRC’s amendment, in writing, within 30 days of

the amendment.

3.3 HMRC’s information and inspection powers

HMRC can request information and documents from taxpayers by issuing a written

information notice. This power is for the purpose of checking the taxpayer’s tax

position and applies irrespective of whether HMRC has opened an enquiry.

HMRC can also request information from third parties provided the request is

either agreed by the taxpayer or approved by a First-tier Tribunal (see later).

The taxpayer must comply with the information notice within such time as is

reasonably requested by HMRC. If the taxpayer does not wish to comply, they must

appeal to the First-tier Tribunal against the information notice within 30 days.

A standard penalty of £300 can be imposed for failure to comply with an

information notice, unless the taxpayer can satisfy the tribunal that he has a

reasonable excuse for the failure.

HMRC also has powers to enter a taxpayer’s business premises and inspect their

business assets and records if the inspection is reasonably required for the purpose

of checking the taxpayer’s tax liability. Note, however, that the power does not

extend to entering and inspecting premises used solely as a dwelling.

3.4 Appeals

The taxpayer has the right to appeal against:

an amendment to a return

an information notice

the imposition of a penalty or surcharge

Paper F6 (UK): Taxation FA2009

392 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

a discovery assessment (see below).

An appeal should be in writing, and must be made within 30 days of the relevant

event. It must also state the grounds for the appeal.

Appeals may initially be made to HMRC. An officer unconnected with the case will

undertake a review. This review must normally be carried out within 45 days. The

taxpayer then has 30 days in which to appeal to the Tribunal.

The tribunal system consists of a First-tier Tribunal and an Upper Tribunal. The

First-tier Tribunal deals with all but the most complex cases. The Upper Tribunal

deals with the more complex cases and appeals against decisions of the First-tier

Tribunal.

Cases are allocated to one of four tracks:

The paper track hears simple appeals, e.g. appeals against the imposition of a

fixed penalty. This is the default track and cases are normally decided without a

hearing.

The basic track involves a hearing but the exchange of documents beforehand is

kept to a minimum.

The standard track involves cases that are subject to more detailed case

management and formality.

The complex track is for long or complex cases, or those involving an important

principle or a large financial sum.

If the decision of the First-tier Tribunal is based on:

a matter of fact, the decision is binding and final

a point of law, the case can be referred to the Upper Tribunal, but only with the

permission of either the First-tier or Upper Tribunal.

A decision of the Upper Tribunal can be referred to the Court of Appeal.

3.5 Determination assessments

When a taxpayer does not file their return by the filing date, HMRC may estimate

the amount of tax due. A determination assessment may be made at any time within

four years of the end of the taxable period concerned. (The taxable period will be a

tax year for income tax/capital gains tax, and an accounting period for corporation

tax.)

There is no right of appeal against a determination. However the determination

notice will be set aside and replaced with the taxpayer’s own self assessment when

it is submitted.

3.6 Discovery assessments

Where a taxpayer did file their return on time but HMRC did not enquire into the

return within the permitted 12 months, HMRC can raise a discovery assessment

where they suspect that full disclosure has not been made.

Chapter 22: Self assessment and PAYE

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 393

The time limits for making a discovery assessment depend on the circumstances of

the case:

.

Situation Time limit

Ordinary time limit 4 years from the end of the taxable period

Careless omission 6 years from the end of the taxable period

Deliberate omission 20 years from the end of the taxable period

3.7 Record keeping

A company must keep its records for at least six years from the end of the relevant

accounting period.

An individual must retain:

personal records for at least 1 year after the annual filing date (i.e. for a 2009/10

return, personal records must be kept until 31 January 2012), and

business records for at least 5 years after the annual filing date (i.e. for a 2009/10

return, business records must be kept until 31 January 2016).

The above dates for both individuals and companies are replaced by:

the date on which HMRC have completed any enquiry, or

the date on which HMRC no longer have the power to enquire into a return, if

later.

A penalty of up to £3,000 per accounting period/tax year can be levied for failure to

keep records.

The records to be retained by companies include records of:

All receipts and expenses

All sales and purchases

Supporting documents including accounts, books, deeds, contracts, vouchers

and receipts.

Individuals are simply required to keep adequate records to support their tax

return.

The obligation to preserve records may be satisfied by preserving the information

contained in the records, rather than the actual records themselves. It is therefore

permissible to preserve the information in electronic form.

Paper F6 (UK): Taxation FA2009

394 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Payment of tax

Payment dates for corporation tax

Payment dates for income tax, Class 4 NICs and capital gains tax

Surcharges

Interest on underpaid and overpaid tax

4 Payment of tax

4.1 Payment dates for corporation tax

A company that does not pay corporation tax at the full rate of 28% is liable to pay

its corporation tax liability 9 months and one day after the end of the chargeable

accounting period (CAP).

A large company must pay its corporation tax liability in four quarterly instalments.

The definition of a large company in this context is a company that pays tax at the

full rate of 28% (for example, because it has profits for a 12-month period in excess

of the statutory upper limit of £1,500,000).

However, a large company does not have to pay by instalments if it:

was not large in the preceding 12 months and does not have PCTCT in excess of

£10 million in the current accounting period, or

has a corporation tax liability of less than £10,000 and pays corporation tax at the

full rate because it has substantial FII and/or a large number of associated

companies.

The procedure for payments by large companies

If a company has a 12 month accounting period, the following procedure is adopted:

First instalment - 14 days after the end of the 6

th

month from the start of the

accounting period.

Second instalment - 14 days after the end of the 9

th

month.

Third instalment - 14 days after the end of the 12

th

month.

Fourth (i.e. final) instalment - 14 days after the end of the 15

th

month.

The instalments are based on the estimated corporation tax liability for the current

accounting period. The company should revise its estimates, if necessary,

throughout the year and pay any shortfall in respect of the previous quarterly

payments.