CIMA CO2 Official Learning System - Fundamentals of Financial Accounting

Подождите немного. Документ загружается.

STUDY MATERIAL C2

340

THE REGULATORY FRAMEWORK OF ACCOUNTING

In Chapter 6, Section 6.8, we looked at the accounting treatment of intangible assets. In

this chapter we look at how the accounting conventions apply to intangible assets.

Intangible assets affect the value of a business and challenge our use of the historical cost

convention. They are all items that cause accountants diffi culty in their valuation, mainly

because of the subjective nature of the value of such items. The general principle on which

all intangibles are valued is whether or not they have the potential to earn profi ts in the

future. In other words, do they have a value in use, and can it be quantifi ed with a reason-

able degree of accuracy?

We shall look at one of the intangibles above in order to appreciate the diffi culties

involved and the approach to be taken in their valuation.

The valuation of research and development costs

S

ome businesses spend money on research and development (R & D), and this giv

es dif-

fi culties for accountants. General R & D costs, which do not lead to a specifi c new product

or method of production, are always written off to the income statement in the period in

which the costs are incurred. However, there is an argument for regarding some develop-

ment costs as capital expenditure if they comply with the following criteria:

●

they are directed towards the development of a specifi c product or production method;

●

the outcome of the research is known with reasonable certainty;

●

the future revenue is likely to exceed the costs.

If these three criteria are met, the expenditure can be included in the statement of fi nancial

position, and is written off when the product or production method commences.

Exercise 10.2

List and briefl y describe as many examples as you can of different methods of valuing

assets.

Solution

●

Original cost/historical cost – as evidenced on invoice.

●

Carrying amount – cost less accumulated depreciation (i.e. original cost, less reduction

due to proportion of asset used up).

●

Fair value – professional or other valuation of asset, often used where asset value has

increased, for example land and buildings, and where the fair value is the amount that

could be obtained on the open market.

●

Replacement cost – of replacing asset with its current equivalent.

●

Current cost accounting – original cost adjusted by an industry-specifi c index, less accu-

mulated depreciation.

●

Current purchasing power accounting – original cost adjusted by a general index, less

accumulated depreciation.

●

Fair value less costs to sell (Net realisable value) – amount expected to be received from

the sale of an asset, less costs of selling.

341

FUNDAMENTALS OF FINANCIAL ACCOUNTING

THE REGULATORY FRAMEWORK OF ACCOUNTING

Exercise 10.3

Make brief notes on the shortcomings of the historical cost convention, and briefl y

describe two alternative methods of accounting that attempt to recognise changing

price levels.

Solution

Shortcomings of historical cost convention . Asset values are out of date, perhaps too low. This

prevents comparison between businesses with newer assets and return on capital employed

is distorted by infl ation. No account is taken of gains that arise until they are realised, even

though they may have occurred during previous periods. Profi t is the increase in net assets

during the period, but this fi gure cannot be fully determined using historical costs.

Current cost accounting applies industry- or asset-specifi c price indices to the costs of

goods sold and assets consumed, to produce values that are based on the cost at the time

of consumption. Because assets consumed are valued at a current value, profi ts are lower

and are said to more accurately represent the increase (or decrease) in the capital of the

organisation.

Current purchasing power accounting applies a general price index to the non-monetary

items in the historical cost fi nancial statements, thus showing the change in the general

purchasing power of money. The value of the net assets is, therefore, restated according to

the index applied; only if this results in an increase in net assets over the previous period is

there said to be a ‘ real ’ profi t for the period.

In a current value system of accounting, assets and liabilities are remeasured regularly so

that changes in value are recorded as they occur; this results in the computation of a profi t

that refl ects the organisation’s ability to continue to operate at the same, or an improved,

level of activity as in the past (or at a reduced level, if a loss occurs).

Exercise 10.4

Explain briefl y what is meant by the term capital maintenance .

Solution

Capital maintenance is the concept that profi t is earned only if the value of the organisation’s

net assets – or alternatively the organisation’s operating capability, that is, its physical pro-

ductive capacity – is greater at the end of the accounting period than it was at the begin-

ning. The amount of profi t earned is the amount of this increase.

One of the criticisms of historical cost fi nancial statements is that they fail to comply

with this concept. Under historical cost accounting (HCA), profi t is measured as the

increase in net assets valued in terms of a monetary unit – say, the dollar – which is not

stable over time. The result is that HCA profi ts often do not represent true increases in the

worth of a business, because apparent increases in asset values may be nothing more than

the effect of infl ation on the unit used to value them.

STUDY MATERIAL C2

342

THE REGULATORY FRAMEWORK OF ACCOUNTING

If fi nancial statements are prepared under the historical cost convention, the profi t

reported may not be suffi cient to support the organisation at the same level of activity in

the future, especially if this profi t is then paid out to the owner(s) of the organisation.

10.5 Regulations in accounting

There is little regulation regarding the preparation of fi nancial statements for sole trad-

ers and partnerships, other than to satisfy the tax authorities of the profi ts made in each

accounting period. However, with regard to the fi nancial statements of limited companies,

charities and so on, there are several types of regulation and guidance to assist the account-

ant in preparing such fi nancial statements, and most of the principles they encompass can

and should be equally applied to other organisations.

10.5.1 Company law

Most countries have legislation applying to companies and this is generally known as ‘ com-

pany law ’ . The amount of detail in company law will vary between countries but in gen-

eral they cover broad issues rather than detailed aspects of accounting. Company law often

states which companies are required to have their fi nancial statements audited by a regis-

tered auditor.

10.5.2 The accountancy profession

Many countries have their own professional accountancy qualifi cation. In the USA, for

example, they are known as Certifi ed Public Accountants (CPA). Some countries do not

have their own professional accountancy qualifi cation in which case trainee accountants

take the qualifi cation of another country. This will also apply if students in a country

believe that the accountancy qualifi cation in another country is more prestigious than their

own domestic qualifi cation. Thus some professional accountancy bodies which were origi-

nally just domestic have become international qualifi cations. Two examples in the UK are:

●

The Chartered Institute of Management Accountants (CIMA),

●

The Association of Chartered Certifi ed Accountants (ACCA).

These bodies insist on their members being properly qualifi ed, not only by passing

examinations but also by obtaining appropriate practical experience, updating their skills

and knowledge on a regular basis, and maintaining certain professional standards based on

an ethical code.

10.5.3 International accounting standards

The Fundamentals of Financial Accounting syllabus states that no knowledge of any spe-

cifi c accounting treatment contained in the international fi nancial reporting standards

(IFRSs) is necessary. This Learning System has not, therefore, made mention of these

343

FUNDAMENTALS OF FINANCIAL ACCOUNTING

THE REGULATORY FRAMEWORK OF ACCOUNTING

IFRSs, but nevertheless this text is based on IFRSs. The infl uence of IFRSs on the text has

three main affects:

1 . Terminology . This text uses the words, phrases, defi nitions and so on found in IFRSs.

2 . Presentation . The presentation of the fi nancial statements and particularly the statement

of fi nancial position and statement of cash fl ows follow the IFRS formats. The syllabus

states that the formats in IAS 1 Presentation of Financial Statements (Revised) and IAS 7

Statement of Cash Flows are to be followed when preparing these fi nancial statements.

3 . Technical . The technical requirements of the IFRS have been followed, for example, in

the discussion above in accounting for goodwill.

These IFRSs are very important and a brief description of how they are issued is given

below.

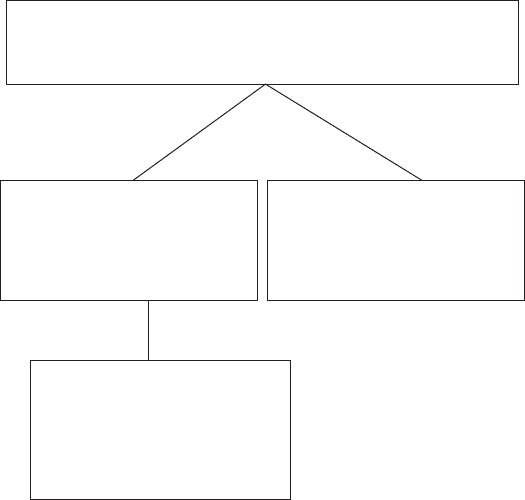

There are four separate but related bodies which control the setting of IFRSs. They are

organised as in the fi gure below.

International Accounting Standards Committee Foundation (IASCF)

responsible for:

• Funding

• Appointment of members of IASB, SAC & IFRIC

International Accounting

Standards Board (IASB)

responsible for:

• Issuing IFRSs

Standards Advisory Council (SAC)

responsible for:

• Advice to IASB on its

priorities

• Information to IASB about

the implications of IFRSs

International Financial Reporting

Interpretations Committee (IFRIC)

responsible for:

• Providing guidance on

problems that have

emerged relating to

IFRSs

Members of these bodies are drawn from preparers of fi nancial statements, (account-

ants) and users of fi nancial statements (banks, analysts, stock exchange, government, etc.),

all from different parts of the world.

The IASB sets IFRSs; a previous body, known as the International Accounting Standards

Committee (IASC) set International Accounting Standards (IAS). When the IASB came

into existence it adopted all of the IAS issued by the IASC. Thus we have in existence two

sets of standards – IFRS and IAS, with the IAS being the older standards. In general, when

reference is made to IFRS, it includes the IASs.

Many countries which previously set their own accounting standards still have their own

standard-setting boards, for example the Financial Accounting Standards Board (FASB) in

the USA, and the Accounting Standards Board (ASB) in the UK. However, these national

boards are working with the IASB and are trying to reach convergence between their own

national standards and the international standards.

STUDY MATERIAL C2

344

THE REGULATORY FRAMEWORK OF ACCOUNTING

Countries in the European Union (EU) – for example Germany, France, Italy and the

UK – are generally required to use IFRSs when preparing the fi nancial statements of com-

panies listed (quoted) on a stock exchange. Once an IFRS has been developed by the IASB

it is scrutinised by the EU to see whether it should be adopted for use by member states. It

takes advice from two committees before adopting an IFRS – the Accounting Regulatory

Committee and the European Financial Reporting Advisory Group (EFRAG). So far all

IFRSs have been adopted, apart from certain sections of one particular standard.

Accountants are obliged to follow accounting standards and the enforcement of IFRSs

is left to each individual country. In the UK, for example, the enforcement agencies are the

Financial Services Authority (FSA) and the Financial Reporting Review Panel (FRRP).

10.5.4 The IASB Framework for the Preparation

and Presentation of Financial Statements

(the ‘Framework’)

Accounting is a social science not a natural science, like physics and chemistry. Whereas

physics and chemistry have natural laws, accounting has to develop its own ‘ laws ’ , which

are the conventions listed above. It is important that the IFRSs produced by the IASB

are consistent with the conventions and that the accounting standards are consistent

with each other. In order to help ensure that this occurs the IASC produced a document

which provides a framework within which all standards are set. This document underpins

all accounting standards and provides the platform from which all future standards will

be developed. This document is the ‘ Framework ’ , which we have already mentioned in

Chapter 1, and which has implicitly been the basis for many of the discussions in the pre-

ceding chapters. The Framework deals with the fundamental issues in fi nancial reporting

and a brief list of its contents is given below.

●

The objective of fi nancial statements – to provide useful information, such as statement

of fi nancial position and income statement to users.

●

Underlying assumptions and qualitative characteristics – these are the conventions

discussed above, for example accruals, going concern, materiality, prudence and

recognition.

●

The elements of fi nancial statements – these are the fi ve main components of an income

statement and statement of fi nancial position – revenue and expense, assets, capital and

liabilities.

●

The measurement of profi t and capital maintenance – different methods of measuring

profi t, for example CPP and CCA, and the concept of capital maintenance, using different

methods of asset valuation, for example value in use and replacement cost.

10.6 The role of the auditor

As we have seen, fi nancial statements are prepared to provide information to a variety of

different user groups. If the statements are to be useful they must be reliable and reasonably

accurate. Accounting systems must therefore be designed to ensure that suffi cient accuracy

exists. In accounting terms we refer to fi nancial statements as giving a fair presentation, or

as being true and fair . It is the role of the auditor to ascertain that the fi nancial statements

are properly prepared in accordance with company law and accounting standards.

345

FUNDAMENTALS OF FINANCIAL ACCOUNTING

THE REGULATORY FRAMEWORK OF ACCOUNTING

It is not, however, the responsibility of the auditor to actually prepare the fi nancial

statements – this is the responsibility of management (the directors in a limited company).

In some cases, the auditors are engaged to prepare the fi nancial statements, but this is in

addition to their audit duties, and is still the responsibility of management. There is more

about this in Section 10.7.

Some organisations are required by law to have their fi nancial statements audited by

an independent, qualifi ed accountant. Others choose to have their fi nancial statements

audited on a voluntary basis, as the existence of an audit report may be benefi cial to them.

10.6.1 Fair presentation or true and fair

Fair presentation or ‘ true and fair ’ means that fi nancial statements prepared for external

publication should fairly refl ect the fi nancial position of the organisation. They should be

free of serious errors arising from negligence or deliberate manipulation. It may not be

economically viable to test every single transaction, or to ensure 100 per cent accuracy, but

fair presentation assumes that the fi nancial statements do not contain any signifi cant errors

that would affect the actions of those reading them. This is based on the materiality con-

vention discussed below. It is the duty of the registered auditor to test the fi nancial state-

ments for material misstatement and to report on whether they are presented fairly.

The materiality convention and the auditor

The purpose of an audit is to allow the auditor to form an opinion and to report accord-

ingly on whether or not the fi

nancial statements fairly pr

esent the company.

In doing this the auditor will perform various tests based on the accounting records and

other information gained from minutes of board meetings and discussions with the direc-

tors. In doing so, the auditor will not be able to check everything in the smallest detail.

Instead, the implications of potential errors will be considered – if they would not affect

the overall fair presentation of the reports they are not signifi cant, that is, not material.

If it were not for the materiality convention, then fi nancial statements would always be

required to be 100 per cent accurate, which would be very expensive and impractical, and

the extra accuracy would be of limited extra benefi t to the users of the fi nancial statements.

There are two main types of tests that the auditor may choose to carry out. The fi rst is

known as compliance testing , which involves assessing the reliability of accounting systems,

procedures and controls. If these appear to be working satisfactorily, the auditors can place

a degree of reliance on them that means that they do not need to test those areas in detail.

If there are areas of doubt, areas of high risk or items of a material nature, the auditors may

choose to carry out more detailed testing, known as substantive testing .

Exercise 10.5

Explain what is meant by the convention of materiality as used by accountants. Give exam-

ples of occasions where materiality might affect the treatment of an item in the fi nancial

statements of an organisation.

Solution

Materiality is concerned with the importance of information to its users. Items that might

affect the decisions made by a user should be clearly stated; items that are insignifi cant

STUDY MATERIAL C2

346

THE REGULATORY FRAMEWORK OF ACCOUNTING

need not be highlighted. Small items of miscellaneous expense can be grouped together

under general headings; larger items should be identifi ed separately.

An example might be to treat sundry stationery items as expenses as soon as they are

purchased, or to value the inventories of stationery remaining at the end of a period and

include it as an asset on the statement of fi nancial position. Another example might be to

regard offi ce staplers as expenses because of their low value, or as non-current assets to be

depreciated because of their long useful life. A third example might be to disclose the sale

of a section of the business, even though the proceeds were small – the amount might be

insignifi cant but the effect on the future of the business might materially affect someone’s

opinion. The degree of materiality of items in the fi nancial statements will affect the level

of testing carried out by the auditor.

Exercise 10.6

Explain what is meant by a fair presentation when applied to the audit of an organisation’s

fi nancial statements.

Solution

Fair presentation exists if the fi nancial statements as presented enable the users and poten-

tial users to gain a picture of the affairs of the organisation that is suffi cient to make proper

judgements. It does not mean that the fi nancial statements are completely accurate, but

that any inaccuracies that exist would not affect the view of the fi nancial statements. The

audit does not guarantee to uncover every error or possible fraud, but does imply that the

systems in use by the organisation would have a reasonable chance of preventing errors

and fraud.

10.6.2 The role of the external auditor

The purpose of the external audit is to form an opinion on the fi nancial statements.

The role of the external auditor will vary depending on the size of the organisation and

whether or not it has its own internal audit department. The work can be divided into two

categories:

1. testing the reliability of the systems and procedures used (compliance testing);

2. testing specifi c transactions to ensure that they have been accounted for accurately (sub-

stantive testing).

On the basis of the above, together with their fi ndings and tests carried out by internal

audit (if appropriate), an opinion will be formed and expressed in an audit report.

Auditors do not check every entry in the ledger accounts. They design their audit pro-

gramme primarily to test that there are proper control systems and procedures in place to

accurately record the fi nancial position of the organisation. Depending on their opinion

of the systems and procedures in place, they will conduct additional, more detailed tests

in some areas, such as tracing particular transactions through the system ( testing the audit

trail , as mentioned in Section 9.2.2). They will also perform tests on the control systems,

347

FUNDAMENTALS OF FINANCIAL ACCOUNTING

THE REGULATORY FRAMEWORK OF ACCOUNTING

such as reconciliations, the segregation of duties, authorisation procedures and documen-

tation, and will check the existence of non-current assets.

They are also concerned to ensure that items are properly valued in accordance with

accepted accounting practice, as discussed earlier in this chapter.

At the conclusion of the audit, an audit report is produced, summarising their fi ndings.

The auditor and fraud

It is not the auditor’s duty to detect fraud . A

uditors should str

ucture their audit tests in such

a way that instances of fraud are likely to be brought to their attention, but the discovery

of fraud has no more importance to them than the discovery of errors and omissions.

10.6.3 The role of the internal auditor

Many larger organisations have their own internal audit department. The work of internal

audit falls into two categories:

●

advising on accounting systems;

●

carrying out tests on the accounting records and internal management reports.

10.6.4 The value-for-money audit

The audit of an organisation does not have to be strictly confi ned to the legal require-

ments. Audits can be carried out on a number of other areas, such as the effi ciency of man-

agement, the design and implementation of computerised systems, and so on. One type of

audit is the value-for-money audit , in which the organisation’s expenditure is scrutinised to

ensure its maximum effectiveness in earning profi ts. Expenditure could include that on

non-current assets, current assets or expenses.

Such audits can be carried out by either internal or external auditors.

10.7 The role of management

In a sole trader’s business it is entirely up to the sole trader to manage his or her business

affairs as she or he wishes. If he or she does not make a good job of it, there is only himself

or herself to suffer as a result, and only himself or herself to answer to.

In a limited company, however (and in other types of organisation, such as charities,

clubs and societies), management are not necessarily the same people who provide its capi-

tal, nor will they be the prime benefi ciaries of the organisation’s continued success. In a

limited company, it is the shareholders who provide the capital, and who expect that capi-

tal to be used properly and wisely, to produce profi ts, or to enable them to sell their shares

successfully in the future. In a charity, club or society, the benefi ciaries are those who enjoy

the rewards of membership or other benefi ts derived from the organisation.

However, the shareholders/members/benefi ciaries often are not involved in the running

of the organisation; they appoint (or elect) others to manage things for them. In a com-

pany, those people are the directors; in a charity, club or society, they are the trustees or the

members of the committee.

STUDY MATERIAL C2

348

THE REGULATORY FRAMEWORK OF ACCOUNTING

It is the responsibility of management , whoever they are, to ensure that the assets of the

organisation are safeguarded. This might involve ensuring that

●

all assets are recorded correctly, exist, and are properly maintained and insured;

●

procedures are in place to prevent misappropriation or misuse of assets;

●

the accounting system is effi cient and effective;

●

no expenditure is undertaken, or liability incurred, without proper procedures for its

authorisation and control;

●

the fi nancial statements are prepared in accordance with current legislation and account-

ing standards.

The term often given to these responsibilities is ‘ the stewardship function ’ . Management

acts as stewards on behalf of shareholders, members and other benefi ciaries, and may be

answerable if they fail in this duty. That is not to say that it is their responsibility to make

as much profi t as possible, or even that they are to blame if losses are made, but they must

take appropriate steps to minimise the risks, within the confi nes of the business world.

10.8 Summary

In this chapter we have looked at:

●

the main accounting conventions underlying the preparation of fi nancial statements;

●

the limitations of the historical cost convention and the methods suggested for

remedying them;

●

the regulatory framework, which includes company law and accounting standards;

●

an outline of the purpose of internal and external audit;

●

the stewardship role of management.

349

Question 1 Multiple choice

1.1 If, at the end of the fi nancial year, a company makes a charge against the profi ts for

stationery consumed but not yet invoiced, this adjustment is in accordance with the

convention of:

(A) materiality.

(B) accruals.

(C) consistency.

(D) objectivity.

1.2 You are the accountant of ABC Ltd and have extracted a trial balance at 31 October

20X4. The sum of the debit column of the trial balance exceeds the sum of the credit

column by $829. A suspense account has been opened to record the difference. After

preliminary investigations failed to locate any errors you have decided to prepare

draft fi nancial statements in accordance with the prudence convention.

The suspense account balance would be treated as:

(A) an expense in the income statement.

(B) additional revenue in the income statement.

(C) an asset in the statement of fi nancial position.

(D) a liability in the statement of fi nancial position.

1.3 A fair presentation is one that

(A) occurs when fi nancial statements have been prepared in accordance with

International Financial Reporting Standards.

(B) occurs when the fi nancial statements have been audited.

(C) shows the fi nancial statements of an organisation in an understandable format.

(D) shows the assets on the statement of fi nancial position at their fair value.

Revision Questions

10