Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 16 Long-term finance 425

■

Equity issues by quoted companies

Once a company has achieved a quotation, it will find it easier to raise further equity,

assuming a successful trading and profit record. The commonest method of raising new

equity is by a rights issue (see below). The Companies Act of 1985 gives existing share-

holders the right to subscribe to new share issues in proportion to their existing holdings.

This generally rules out a public issue although these pre-emption rights can be waived

with the agreement of shareholders at a properly convened meeting. With such agree-

ment, a placing may be arranged whereby shares are sold to participating institutions

provided that the price involves no more than a 10 per cent discount to the market price.

Shares can also be issued as full or partial consideration when acquiring another com-

pany. In some cases, this may be done via a vendor placing, or placing with clawback. In a

vendor placing, the acquiring company places the new shares with a group of institutions,

thus diluting the ownership and earnings of existing shareholders. For sufficiently large

issues, existing shareholders have the right to reclaim the shares they would have been

entitled to, had there been a rights issue. If they do not, they receive no compensation for

the loss in value of their holdings as there are no detachable rights to sell (see below).

In view of their importance, we now give detailed consideration to rights issues.

Salaam Alaykum to the AIM

In August 2004, the first fully Islamic British bank, the Islamic Bank of Britain, but with origins in

the tiny desert state of Qatar, was given permission by the FSA to offer a range of consumer

banking products compliant with Sharia, the code of laws that govern Islam. None of its products

would involve the taking or paying of interest, or investing in haram (prohibited) activities such

as alcohol, tobacco or pornography. Depositors in such banks are offered a share in profit from

the bank’s operations (rather like the Cooperative dividend). Formed with £14 million of seed

capital, raised largely from the Qatari royal family and other wealthy Arabian Gulf investors, the

biggest shareholders were the Emir of Qatar, Sheikh Hamad Khalifa bin Hamad al Thani, and the

Qatar International Islamic Bank, both with around 17 per cent of the equity.

Later that month, it announced details of a floatation to raise £40 million by the issuance

of 160 million shares at 25 pence through a combination of a public issue on the AIM market

and a private placing, with existing investors invited to participate to avoid diluting their hold-

ings. This issue price valued the business at £105 million. The proceeds were to be used to

open new branches in London and other cities with large Muslim populations, such as Leicester

and Bradford, and to develop new products such as mortgages by the end of 2004, and an

internet banking service in 2005.

Source: Based on Financial Times, 9 August 2004, and www.ft.com 27 August 2004.

Reversing the flow: Going private again

The years since the stock market slide of 2000/01 have seen an upsurge in the number of firms

being taken off the stock market by so-called private equity firms, generally specialist funds that

are subsidiaries of banks or syndicates set up by a number of banks. Traditionally, they have spe-

cialised in funding management buy-outs or spin-offs of unwanted divisions of larger firms, but

more recently, they have been active in taking quoted firms off the stock market. For example, in

February 2005, one such firm, Apax Partners, made a bid for the high-street retailer Woolworths.

Continued

pre-emption rights

The right for existing share-

holders to be offered newly

issued shares before making

them available to outside

investors

vendor placing/placing

with clawback

A placing of new shares with

financial institutions where

existing investors have the

right to purchase the shares

from the institutions con-

cerned to protect their rights

CFAI_C16.QXD 10/28/05 4:57 PM Page 425

.

426 Part V Strategic financial decisions

■ Rights issues

In a rights issue, shareholders are granted the right to subscribe for shares (or less com-

monly, for other types of security) in proportion to their existing holdings, thus

enabling them to retain their existing share of voting rights. Apart from the control fac-

tor, rights issues have certain other attractions:

1 They are far cheaper than a public share issue. Provided the issue is for less than 10

per cent of the class of capital, there is no need for a prospectus, although a brochure

must still be made available.

2 They may be made at the discretion of the directors without consent of the share-

holders or the Stock Exchange. At one time, a queuing system for all new issues was

operated by the government broker, acting for the Bank of England, in order to

ensure a measured flow of new securities on to the market. Nowadays, lead insti-

tutions are merely requested to notify the Bank in advance of new issues to enable

the Bank to compile a ‘calendar’ of all forthcoming new issues proposed for mil-

lion or more.

3 When stock market prices are generally high, companies have been known to raise

cash through rights issues and to place it on deposit while seeking suitable candi-

dates for acquisition. This gives a high degree of flexibility in timing a bid, i.e. the

cash is already to hand.

4 The finance is guaranteed, either from existing shareholders or from the under-

writers. Existing shareholders are given an incentive either to take up their rights or

to sell them. It is not a sensible option to do nothing: this effectively reduces their

wealth, as shares are typically offered at a discount of about 20 per cent below the

current market price. If, as is usual, they are underwritten, the company is guaran-

teed to receive the cash, although it is embarrassing to have to call upon the under-

writers to fulfill their obligations.

£20

Sometimes, they are set up specifically to acquire one particular firm. Some observers esti-

mated that by the end of 2004, firms controlled by private equity firms accounted for around

a quarter of private sector employment in the UK.

Not being quoted themselves, they do not face the same public scrutiny or continuous pres-

sure to perform. Their aim is to restructure the acquired firm and sell it on, either in a trade sale

or by a refloatation. Some spectacular successes have been achieved with substantial increases

in the value of firms taken private and then refloated a few years later being recorded.

Among the reasons for the rise in the private equity sector are:

■ The weight of regulation and disclosure that listed firms have to bear, for example, the move

to International Reporting Standards in 2005, the ongoing requirements of the Combined

Code, the introduction of the Sarbanes-Oxley Act affecting firms with a US listing, and the

requirement to provide a detailed Operating and Financial Review (OFR). Regarding the

Combined Code, many firms do not see the need to separate the roles of Chairman and

Chief Executive, arguing that it leads to lack of flexibility, which hampers swift and effective

decision-making.

■ Greater liquidity among financial institutions. Many institutions have curtailed their invest-

ment of new money into the stock market, and others have cut back their exposure, creat-

ing vacuums that they have filled by investing in private equity funds.

■ The ability to tolerate higher gearing. With no public scrutiny, the amount of debt that they

can carry is greater than for an equivalent listed firm. Private equity firms tend to concen-

trate on asset-rich firms with solid cash flows, most notably firms in the retail store sector,

which often need a re-vamp. In the case of Woolworth (see above), the target had little by

way of freehold property assets, although its leasehold property was generally on very

attractive sites. Moreover, it was a very strong cash generator.

prospectus

A document setting out the

existing financial situation of a

firm and its future prospects

that is published to accompa-

ny a share issue

CFAI_C16.QXD 10/28/05 4:57 PM Page 426

.

Chapter 16 Long-term finance 427

■

Shareholders’ choices in a rights issue: Grow-up plc

Grow-up plc decides to make a rights issue of one new share for every three held. The

share price prior to the issue is 200p and the new shares are to be offered at 160p. In

practice, rights issues are made at a discount, partly to make them look attractive and

thus encourage shareholders to subscribe, and partly to safeguard against the risk of a

fall in the market price during the offer period. The theoretical ex-rights price (TERP) is

the price at which shares are expected to trade after the rights issue has been completed.

It is calculated below at 190p:

The underwriting controversy

The size of underwriting fees and the allegedly uncompetitive way in which contracts are

awarded has generated considerable controversy. Typically, companies ‘lose’ 2 per cent of the

monies raised from a new share issue in fees. The lead underwriter, usually the merchant bank

handling the issue, takes 0.5 per cent, and the firm’s stockbroker 0.25 per cent, with the

remaining 1.25 per cent split among the institutional sub-underwriters (who are in many cases

shareholders!). Critics of the system argue that costs are higher than they would be if a sys-

tem of open tender applied. Indeed, rights issues which have involved tendering for the sub-

underwriting business have produced lower fees. For example, the construction company

Berkeley plc made a rights issue in 1997 incurring sub-underwriting fees of just 0.2 per cent.

In 1997, the Office of Fair Trading instructed the Monopolies and Mergers Commission

(MMC) to investigate the fee structure and system of awarding sub-underwriting contracts. In

May 1998, the MMC reported that a ‘complex monopoly’ existed in these areas and identified

28 ways in which it could operate against the public interest. Following the final report of the

MMC in 1999, and instructions issued by the Secretary of State for Trade and Industry, the fol-

lowing measures were implemented:

■ Stock Exchange listing rules were amended to instruct firms to explain fully to shareholders

why a share issue is made with less than two-thirds of the sub-underwriting offered for ten-

der.

■ The Bank of England published a ‘best practice’ guide which focused on the use of tendering

for sub-underwriting, and on the circumstances in which deep discounts might be advanta-

geous.

■ The SFA was instructed to remind its members that they should give client firms all infor-

mation necessary to make balanced judgements including the alternatives to underwriting

at standard fees.

Effect of a 1-for-3 rights issue

Before 3 old shares prior to rights issue at 200p each: 600p

1 new share at 160p: 160p

After 4 shares worth: 760p

1 share is therefore worth 190p1760p 42 TERP

The value of the rights is the difference between the pre-rights share price and the

TERP. In the case of Grow-up plc, this is for every existing share

held. This 30p is termed the ’nil paid price of rights’. The first option for shareholders

is to sell their rights, obtaining 10p per share, less any dealing costs. A shareholder

with 3,000 shares in the company would have a holding with market value prior

1200p 190p2 10p

theoretical ex-rights price

(TERP)

The share price that should in

theory be established, other

things being equal, after a

rights issue is completed

nil paid price of rights

The market value of the right

to subscribe for new shares

offered in a rights issue

CFAI_C16.QXD 10/28/05 4:57 PM Page 427

.

428 Part V Strategic financial decisions

to the rights issue of After the issue, the value will fall to

a decline of which is the amount he or she would

receive for the rights sold.

The formula for the TERP is thus:

where base number of shares held (i.e. number of rights required to buy one

share).

In this example, TERP is thus:

Similarly, the value of a

.

In the example, this is:

The nil paid price can be expressed per existing share, (10p) or more usually, per

block of shares required to acquire one new share

,

i.e. the difference

between the TERP and the issue price.

The second option is to subscribe for the new shares by taking up the rights. This

should happen only if the shareholder has the resources to acquire the additional

shares and believes this is the best way to invest such money. Additional reasons for

taking up the rights are the fact that no stamp duty or broker’s commission is payable,

and the desire to maintain one’s existing share of voting power.

A third option is to sell sufficient of the rights to provide the cash to take up the balance.

This option, known as ‘tail-swallowing’, makes sense for shareholders who want to

maintain their existing investment in the company in value terms.

The formula for calculating the number of shares is:

As noted, the nil paid price is the difference between the TERP and the subscription

price, i.e. The number of new shares to which our investor with

3,000 existing shares retains acquisition rights is:

To buy 157 shares at 160p will cost funded from (843/1,000) rights sold at

The total investment is now worth which

(when rounded) is equivalent to the original investment of

The final option is to let the rights lapse by doing nothing. In this case, the company

may sell the new shares in the market and, reimburse the shareholder net of dealing

fees. Alternatively, the issuer may conduct an auction of rights not taken up to avoid

the need to appoint underwriters.

The real message from rights issues is that shareholders cannot expect to receive

something for nothing. The apparent gain from the invitation to purchase new shares

at a discount on the existing price is more illusory than real.

To some, a rights issue may look damaging because the share price (in theory) has

to fall due to the sale of shares at a discount, but again this apparent damage is illusory.

Of course, the EPS, based on the last reported profits, will fall, as there are more shares

in issue. But if people are bullish about the firm’s prospects then the post-issue price

may exceed the TERP (and vice versa). In this case, the market would be pricing in the

£6,000.

13,157 190p2 £5,998,30p £252.90.

£251.20,

30p

190p

1,000 157 shares

1190p 160p2 30p.

Nil paid price

Ex-rights price

Number of shares allotted

13 10p 30p2

1190p 160p2 30p

right 1TERP issue price2

13 200p2 160p

13 12

760p

4

190p

N the

TERP

1N cum rights price2 issue price

N l

£300,1£3,000 £1.902 £5,700,

13,000 £22 £6,000.

CFAI_C16.QXD 10/28/05 4:57 PM Page 428

.

Chapter 16 Long-term finance 429

expected returns from new investment, i.e. adding in the NPV of the new project (and

v.v.). In effect, investors are saying that the cash raised is worth more than its nominal

value as it brings with it the promise of positive investment returns (and v.v.); similar-

ly, if the post-issue price is equal to the TERP, investors are assessing the NPV of the

investment project at zero.

■ Open offers

An open offer, or ‘entitlement offer’, may also be made by a quoted company to its

existing shareholders. Like a rights issue, it invites shareholders to buy new shares at a

specified price, normally lower than the going market price. The investor’s entitlement

to buy is also based on his/her existing holdings. However, there is one important dif-

ference – an open offer cannot be traded on the market – if the offer is not taken up it

lapses. An additional difference is that the firm may invite investors to apply for more

than their strict entitlement – a so-called ‘excess application’, although there is no guar-

antee that this excess will be satisfied, as demand for shares may exceed the amount the

firm wishes to issue.

An open offer was made by Corus plc in November 2003 to raise money to finance

its ongoing restructuring programme. New ordinary shares were offered at 23.5p, a 10

per cent discount to the market price, on the basis of five new shares for 12 existing

ordinary shares, although no excess application was offered. The offer was well

received as the supporting information was extensive and convincing, and the Corus

shares began a long bull run.

Self-assessment activity 16.3

What is the TERP in the following case?

■ pre-announcement share price £5.

■ rights issue of 1-for-6 at £3.50 issue price

(Answer in Appendix A at the back of the book)

Powering ahead

International Power plc, the electricity firm formed out of the privatisation of the UK power

generation industry, announced its first ever rights issue on 30 July 2004, when its opening

share price was 143p. The funds involved, about £290 million net of issue expenses, were

intended to help finance two acquisitions with ‘the potential to improve shareholder returns,

and enhance the quality of International Power’s earnings from income that is largely con-

tracted.’ One acquisition was the purchase from RWE Power AG of Germany of a 75% stake in

the 990MW combined cycle gas turbine Turbogas power station in Portugal for Euros 205 mil-

lion in order to strengthen IP’s position in the Iberian market. The other was the acquisition, in

a 70/30 partnership with Mitsui of Japan, of a portfolio of 13 power generation projects, locat-

ed in 9 different countries, 11 of which were operating under long-term power contracts. IP’s

investment in the joint venture amounted to US$677 million.

IP offered existing shareholders 33 new shares per 100 existing ordinary shares at a price of

82 pence, representing a 43% discount to the closing price of 143p on the day prior to the

announcement. The news of the issue and the intended use of the funds pushed the share

price up 3% to 147.5p. By the ex-rights day, the share price stood at 144.25. On the first day

Continued

CFAI_C16.QXD 10/28/05 4:57 PM Page 429

.

430 Part V Strategic financial decisions

■ Scrip issues and bonus issues

Whereas a rights issue raises new finance, a scrip issue simply gives shareholders more

shares in proportion to their existing holdings. As a result, the value of their total hold-

ings is unchanged, but the share price will fall due to earnings dilution. Scrip issues are

often used by companies whose unit share price is ‘high’ – a high or ‘heavyweight’

share price (usually or above) is regarded as a deterrent to trading. This was the rea-

son given by the airport operator, BAA plc, in 1994, when it made a ‘one-for-one’ scrip

issue. For every share held, owners were given a free share. According to BAA, ‘this

will improve the marketability of the company’s shares as the increased number of

shares in issue should result in a corresponding reduction in share price’.

Companies like BAA have built up substantial reserves by retention of earnings,

making their issued share capital look relatively small. In the case of BAA, the issued

share capital was million and the revenue reserve was million. The effect

of the scrip issue was to double the issued share capital and to reduce the revenue

reserve by million to million. In other words, BAA converted, or ‘capi-

talised’, its reserves into issued share capital, hence the common use of the synonym

‘capitalisation issue’.

Scrip issues do not always involve such a drastic reorganisation of shareholder

funds. They are often given as ‘bonus issues’ in addition to cash dividends, and are

often taken by the market as a signal of higher future dividends. If a company makes,

say, a one-for-ten scrip and maintains the dividend per share, this is tantamount to a

future increase in dividends of 10 per cent (the new shares do not normally qualify for

the dividend immediately). This signifies the company’s expectation of greater capac-

ity to pay dividends in the future, i.e. higher future earnings. In such cases, the share

price may not fall quite so far as the simple arithmetic may suggest, i.e. by 1/11th, but

may even increase as the market responds to the ‘signals’ emitted by the company.

■ Share splits (‘stock splits’ in the USA)

An alternative way of addressing the heavyweight status of a share is to split the ordi-

nary shares into a larger number with lower par value. For example, one additional

share may be given for every existing share in a ‘2-for-1’ split. In theory, this has no

effect on the accounting numbers, i.e. the book value of the share capital. Nor should it

affect the share price since no additional funds are raised and each shareholder’s inter-

est in future profits is unchanged.

Microsoft Inc. has made nine stock splits since its IPO in March 1986, the most

recent being in February 2003, as shown in Table 16.1, when 5.4 billion shares were

multiplied into a total of 10.8 billion in a 2-for-1 split.

£837£511

£1,348£511

£10

of trading ex-rights, when investors could begin to trade the rights separately from the shares

themselves, the shares opened at 136p, but receded to close at 131p. The nil paid rights price

opened at 53p, but fell back to 48p, in line with the ordinary share price.

The theoretical ex-rights price (TERP), based on the share price ruling just prior to

announcement was:

100 shares @ 143p £143.00

Cash: 33 shares @ 82p £27.06

Total £170.36

TERP (£170.06/133 shares) 128p

With the market price above the TERP, this suggested people viewed the issue favourably,

(although the market as a whole had risen over this period).

Source: Circular sent to International Power shareholders, August 2004 (Details used with permission).

CFAI_C16.QXD 10/28/05 4:57 PM Page 430

.

Chapter 16 Long-term finance 431

Table 16.1

History of Microsoft

common stock splits

Split Payable date Type of split Closing price before/after

First Sept. 18, 1987 2 for 1 Sept. 18–$114.50/

Sept. 21–$53.50

Second April 12, 1990 2 for 1 April 12–$120.75/

April 16–$60.75

Third June 26, 1991 3 for 2 June 26–$100.75/

June 27–$68.00

Fourth June 12, 1992 3 for 2 June 12–$112.50/

June 15–$75.75

Fifth May 20, 1994 2 for 1 May 20–$97.75/

May 23–$50.63

Sixth Dec. 6, 1996 2 for 1 Dec. 6–$152.875/

Dec. 9–$81.75

Seventh Feb. 20, 1998 2 for 1 Feb. 20–$155.13/

Feb. 23–$81.63

Eighth March 26, 1999 2 for 1 March 26–$178.13/

March 29–$92.38

Ninth Feb. 14, 2003 2 for 1 Feb. 14–$48.30

Feb. 18–$24.96

Source: www.microsoft.com

Self-assessment activity 16.4

In a share split, e.g. ‘2-for-1’, what is the effect on:

■ the number of shares issued?

■ the shareholders’ capital in the balance sheet?

■ the firm’s assets?

■ its market value – per share? in total?

(Answer in Appendix A at the back of the book)

Equity capital: checklist of key features

For

■ No fixed charges (e.g. interest payments). Dividends are paid if the company generates suf-

ficient cash, the level being decided by the directors.

■ No repayment is required. It is truly permanent capital.

■ In the case of retained profits and rights issues, directors have greater control over the

amount and timing, with minimal paperwork or issuing costs.

■ It carries a higher return than loan finance and acts as a better hedge against inflation for

investors.

■ Shares in most listed companies can be easily disposed of at a fair value.

Against

■ Issuing equity finance can be cost-effective (as in the case of retained profits or a rights

issue), but it is expensive in the case of a public issue (often 5 per cent or more of the

finance raised).

■ Issuing ordinary shares to new shareholders dilutes the degree of control of existing members.

■ Dividends are not tax-deductible, making equity relatively more expensive than borrowing.

■ A higher proportion of equity can increase the overall cost of capital for the company (see

Chapter 18).

■ Shares in unlisted companies are difficult both to value and to dispose of.

CFAI_C16.QXD 10/28/05 4:57 PM Page 431

.

432 Part V Strategic financial decisions

16.6 DEBT INSTRUMENTS: DEBENTURES, BONDS AND NOTES

The array of instruments for raising debt finance is even greater than for equity finance.

Firms can raise long-term debt via the banking system, e.g. by a term-loan, or via the

money and bond markets, by issuing a security that can be traded rather than held to

maturity. The money markets supply short-term borrowing while the bond markets

supply medium-to-long term finance.

The word ‘bond’ is a general term used to describe a variety of longer-term loans to

companies. In some markets, they are described as ‘loan stock’, or, especially where

the interest payable is variable, as ’notes’. A bond is simply a receipt or promise to

repay money on a loan, usually with interest i.e. it binds the borrower to a commit-

ment that can range between one and 30 years.

Characteristics of a bond are:

■ the nominal or par value in the currency of denomination.

■ the redemption value – usually the par value, but other possibilities include a stat-

ed premium or index-linking.

■ the rate of interest payable – known as the coupon – expressed as a percentage of

the nominal value.

■ the redemption date.

For example, BAA plc, the UK airports operator, is committed to the following bond:

BAA plc 7.875% 2007 million

The million will be repaid in full in 2007; and interest is payable per

of stock each year in two stages.

■ Debentures

In strict legal terms, a debenture is a document acknowledging that the firm has bor-

rowed money, whether or not any security has been given to back the loan. However, in

normal business usage, this term is used to describe a loan which is secured on the assets

of the company by mortgage deeds – a secured debenture is often called a mortgage

debenture. If the issuer goes into liquidation, or defaults on interest or capital payments,

the holders can apply for a court ruling to order the sale of either specified assets (called

a fixed charge) or any of the firm’s assets (a floating charge). The firm cannot dispose

of assets subject to a fixed charge without the permission of the creditors.

As regards priority for payment, debts rank in order of issue – holders of the earli-

est issued debentures must be paid interest before the later comers. Where a firm has

issued a series of bonds, a pari passu clause is inserted into the document acknowl-

edging the debt. Debentures that rank lower down the priority list are called ‘junior’

or ‘subordinated’ stock.

The BAA stock referred to above is unsecured, and thus ranks behind its secured bor-

rowing, but ahead of a number of subsequently-issued unsecured bonds. Unsecured

stock is riskier than secured stock and investors thus require a higher coupon rate.

The pejorative term ‘junk bond’ is applied to the unsecured loan stock of a bor-

rower that merits sub-investment grade by a bond-rating agency. Standard & Poor’s

investment grade is BBB or above – any security rated below this ‘is regarded as hav-

ing predominantly speculative characteristics with respect to capacity to pay interest

and repay principal’. Obviously, junk carries much higher than average yields, hence

the euphemism ‘high yield bonds’.

Loan agreements usually specify restrictive covenants. Such conditions might include

the following:

1 Dividend restrictions – limitations on the level of dividends a company is permitted

to pay. This is designed to prevent excessive dividend payments, which may

£100

£7.875£200

£200

notes

Loan securities in general, but

often referred to securities

that carry a floating rate of

interest

restrictive covenants

Limitations on managerial

freedom of action, stipulated

as conditions of making a loan

mortgage debenture

A loan instrument under which

the ownership of selected

assets is mortgaged to the

lender – in a default, the title

passes to the lender

CFAI_C16.QXD 10/28/05 4:57 PM Page 432

.

Chapter 16 Long-term finance 433

seriously weaken the company’s future cash flows and thereby place the lender at

greater risk.

2 Financial ratios – specified levels below which certain ratios may not fall, e.g. debt-

to-net-assets ratio, current ratio.

3 Financial reports – regular accounts and financial reports to be provided to the lender

to monitor progress.

4 Issue of further debt – the amount and type of debt that can be issued may be restrict-

ed. Subordinated loan stock (i.e. stock ranking below the existing unsecured loan

stock) can usually still be issued.

5 Asset backing – a specified minimum level of tangible fixed assets.

Debentures and unsecured loan stock: checklist of key features

For

■ Most corporate loan stocks give ten or more years before repayment is due. A ‘bullet’ loan is

where there is just one final repayment, and a ‘balloon’ loan is where increasing amounts of

capital are repaid towards the end of the period of the loan. Bullet and balloon loans give

attractive cash flow benefits in the early years, where little or no interest is payable.

■ A successful company may eventually be able to redeem the loan stock through a new

issue, without drawing upon operating cash flows (although the company is exposed to the

risk of higher interest rates).

■ Interest is tax-deductible.

Against

■ Restrictions are placed on the company in terms of either the charge over assets or the

restrictive covenants imposed.

■ Unsecured loan stock may impose demanding performance requirements.

■ Greater monitoring and control takes place over a public issue such as a debenture than

with, say, a term loan with a bank.

■ Deep-discount bonds

Some debt instruments are sold at a price well below the par value, with a so-called

deep-discount. An extreme case of this is Zero-coupon bonds, e.g. a bond issued at

with a five-year life to maturity when it will be repaid at par of Such bonds carry

no entitlement to interest as such, thus appealing to investors who would normally pay

Income or Corporation Tax on interest income, but who may not be liable to Capital

Gains Tax, or who wish to defer it. In this example, the annualised rate of return from

the capital gain if held to maturity for the full five years is represented by the rate r in

the following compound interest expression:

This can be written as:

The discount tables (PVIF) can be used to find r (about 10.75 per cent p.a.).

1

11 r2

5

£70

£100

0.700

£7011 r2

5

£100

£100.

£70

CFAI_C16.QXD 10/28/05 4:57 PM Page 433

.

434 Part V Strategic financial decisions

Self-assessment activity 16.5

What is the yield to maturity on a zero-coupon bond issued at £50, repayable at par of

£100, in ten years’ time?

(Answer in Appendix A at the back of the book)

■ Asset-Backed Securities (ABSs)

In recent years, some companies – and even certain individuals – have issued a new

breed of securities, backed not by physical assets but by a reliable long-term stream of

future earnings. A category of assets commonly utilised has been intellectual property

represented by patents and copyrights. Like most security issues, ABSs are sold essen-

tially to raise cash for investing in other activities.

Organisations effectively capitalise their future income into a single lump sum and

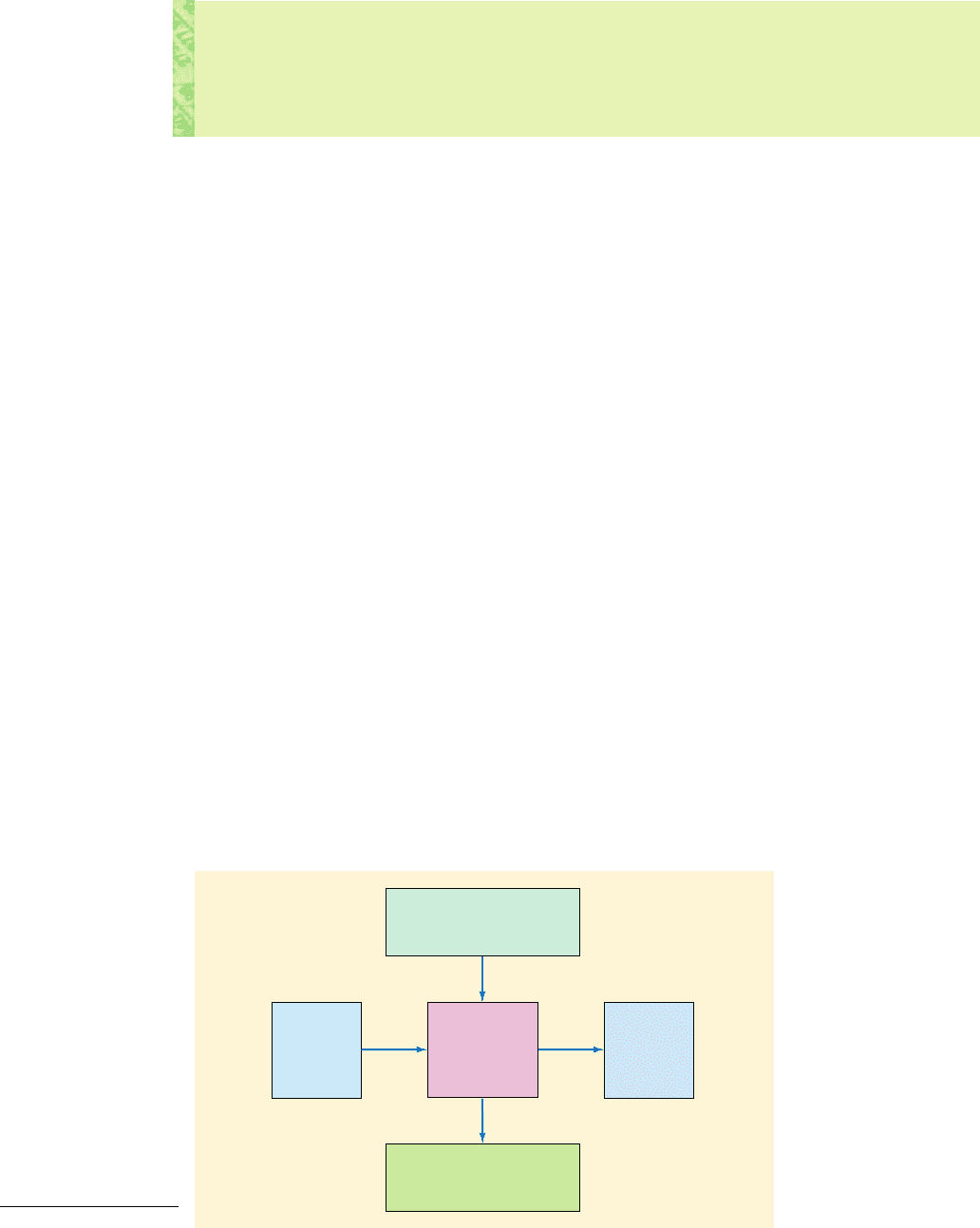

sell it on the financial markets to generate immediate cash. The firm’s financial advis-

ers set up a Special Purpose Vehicle (SPV), as shown in Figure 16.1. This is effectively

a ‘bank’ which handles the bond issue and into which the designated income stream

is paid and from which is paid the stream of interest payments needed to service the

borrowing.

This process of converting non-tradable claims into tradable ones is called securiti-

sation. Like most financial innovations, securitisation originated in the USA. Banks

parcelled up mortgage commitments made by house purchasers into bundles of mort-

gages to sell as interest-bearing securities, originally known as collateralised mortgage

obligations (CMOs). Having both liquidity and a bank’s guarantee, these could be

offered at a lower interest rate than that charged on the underlying mortgages, the dif-

ference representing profit for the bank. This practice is now widespread in Europe,

where it is increasingly seen as a cheaper alternative to unsecured bond issues.

The following examples of the ABS principle (not all of which involved SPVs) demon-

strate its flexibility and versatility:

■ In 1992, the Disney Corporation issued $400 million in seven-year notes with a vari-

able rate of interest to be paid from royalties receivable from its portfolio of film

copyrights, a path followed also by News Corporation in 1996.

■ In 1997, David Bowie raised $55 million by selling bonds backed by his music copy-

right portfolio, with an average bond life of ten years. This tactic was also adopted

by Rod Stewart and Michael Jackson, using similar security.

Income from

specified asset

e.g. recording royalties

Interest and

principal paid to

investors

Capital

raised

for

originator

Proceeds

of

sale of

bonds

SPECIAL

PURPOSE

VEHICLE

Figure 16.1

How an SPV works

Special Purpose Vehicle

(SPV)

A financial vehicle set up to

manage the issue of Asset-

Based Securities and arrange

for payment of interest and

eventual redemption

CFAI_C16.QXD 10/28/05 4:57 PM Page 434