White R.E. Computational Mathematics: Models, Methods, and Analysis with MATLAB and MPI

Подождите немного. Документ загружается.

220 CHAPTER 5. EPIDEMICS, IMAGES AND MONEY

5.5.2 Application

We will focus on a particular option contract called an American put option.

This option contract obligates the writer of the contract to buy an underlying

asset from the holder of the contract at a particular price, called the exercise

or strike price,

H. This must be done within a given time, called an expiration

date,

W . The holder of the option contract may or may not sell the underlying

asset whose market value,

V, will vary with time. The value of the American

put option contract to the holder will vary with time, w> and V. If V gets large

or if w gets close to W , then the value of the American put option contract,

S (V> w), will decrease. On the other hand, if V gets small, then the value of the

American put option contract will increase towards the exercise price, that is,

S (V> w) will approach H as V goes to zero. If time exceeds expiration date, then

the American put option will be worthless, that is,

S (V> w) = 0 for w A W=

The objective is to determine the value of the American put option contract

as a function of

V, w and the other parameters H, W , u ( the interest rate) and

(the market volatility), which will be described later. In particular, the holder

of the contract would like to know when is the "best" time to exercise the

American put option contract. If the market value of the underlying contract

is well above the exercise price, then the holder may want to sell on the open

market and not to the writer of the American put option contract. If the market

price of the underlying asset continues to fall below the exercise price, then at

some "point" the holder will want to sell to the writer of the contract for the

larger exercise price. Since the exercise price is fixed, the holder will sell as

soon as this "point" is reached so that the money can be used for additional

investment. This "point" refers to a particular market value V = V

i

(w)> which

is also unknown and is called the optimal exercise price.

The writers and the holders of American put option contracts are motivated

to enter into such contracts by speculation of the future value of the underlying

asset and by the need to minimize risk to a portfolio of investments. If an

investor feels a particular asset has an under-valued market price, then entering

into American put option contracts has a p ossible value if the speculation is

that the market value of the underlying asset may increase. However, if an

investor feels the underlying asset has an over-priced market value, then the

investor may speculate that the underlying asset will decrease in value and may

be tempted to become holder of an American put option contract.

The need to minimize risk in a portfolio is also very important. For example,

suppose a portfolio has a number of investments in one sector of the economy.

If this sector expands, then the portfolio increases in value. If this sector con-

tracts, then this could cause some significant loss in value of the portfolio. If

the investor becomes a holder of American put option contracts with some of

the portfolio’s assets as underlying assets, then as the market values of the

assets decrease, the value of the American put option will increase. A proper

distribution of underlying investments and option contracts can minimize risk

to a portfolio.

© 2004 by Chapman & Hall/CRC

5.5. OPTION CONTRACT MODELS 221

5.5.3 Model

The value of the payo from exercising the American put option is either the

exercise price minus the market value of the underlying asset, or zero, that is,

the payo is max(H V> 0). The value of the American put option must almost

always be greater than or equal to the payo

. This follows from the following

risk free scheme: buy the underlying asset for

V, buy the American put option

contract for

S (V> w) ? max(H V> 0)> and then immediately exercise this option

contract for

H, which would result in a profit H S V A 0= As this scheme is

very attractive to investors, it does not exist for a very long time, and so one

simply requires

S (V> w) max(H V> 0)= In summary, the following conditions

are placed on the value of the American put option contract for w W . The

boundary conditions and condition at time equal to

W are

S (0> w) = H (5.5.1)

S (O> w) = 0 for O AA H (5.5.2)

S (V> W ) = max(H V> 0)= (5.5.3)

The inequality constraints are

S (V> w) max(H V> 0)

(5.5.4)

S

w

(V> w) 0 and S

w

(V

i

+> w) = 0 (5.5.5)

S (V

i

(w)> w) = H V

i

(w) (5.5.6)

S (V> w) = H V for V ? V

i

(w) (5.5.7)

g

gw

V

i

(w) A 0 exists. (5.5.8)

The graph of

S (V> w

The partial derivative of S (V> w) with respect to V needs to be continuous

at

V

i

so that the left and right derivatives must both be equal to -1. This

needs some justification. From (5.5.7) S

V

(V

i

> w) = 1 so we need to show

S

V

(V

i

+> w) = 1= Since S (V

i

(w)> w) = H V

i

(w)>

g

gw

S

(V

i

(w)> w) = 0

g

gw

V

i

(w)

S

V

(V

i

+> w)

g

gw

V

i

(w) + S

w

(V

i

+> w) =

g

gw

V

i

(w)

S

w

(V

i

+> w) = (1 + S

V

(V

i

+> w))

g

gw

V

i

(w)=

Since S

w

(V

i

+> w) = 0 and

g

gw

V

i

(w) A 0> 1 + S

V

(V

i

+> w) = 0.

In the region in Figure 5.5.1 where

S (V> w) A max(H V> 0)> the value of

the option contract must satisfy the celebrated Black-Scholes partial dierential

equation where

u is the interest rate and is the volatility of the market for a

particular underlying asset

S

w

+

2

2

V

2

S

VV

+ uVS

V

uS = 0= (5.5.9)

© 2004 by Chapman & Hall/CRC

) for fixed time should have the form giv en in Figure 5.5.1.

222 CHAPTER 5. EPIDEMICS, IMAGES AND MONEY

Figure 5.5.1: Value of American Put Option

The derivation of this equation is beyond the scope of this brief intro duction to

option contracts. The Black-Scholes equation di

ers from the partial dierential

equation for heat di

usion in three very important ways. First, it has variable

co e

!cients. Second, it is a backward time problem where S (V> w) is given at a

future time

w = W as S (V> W ) = max(H V> 0)= Third, the left boundary where

V = V

i

(w) is unknown and varies with time.

Black-Scholes Model for the American Put Option Contract.

S (V> W ) = max(H V> 0) (5.5.10)

S (0> w) = H (5.5.11)

S (O> w) = 0 for O AA H (5.5.12)

S (V

i

(w)> w) = H V

i

(w) (5.5.13)

S

V

(V

i

±> w) = 1 (5.5.14)

S (V> w) max(H V> 0) (5.5.15)

S = H V for V V

i

(w) (5.5.16)

S

w

+

2

2

V

2

S

VV

+ uVS

V

uS = 0 for V A V

i

(w)= (5.5.17)

The volatility

is an important parameter that can change with time and

can be di

!cult to approximate. If the volatility is high, then there is more

uncertainty in the market and the value of an American put option contract

should increase. Generally, the market value of an asset will increase with time

according to

g

gw

V

= V=

© 2004 by Chapman & Hall/CRC

5.5. OPTION CONTRACT MODELS 223

The parameter

can be approximated by using past data for V

n

= V(nw)

V

n+1

V

n

w

=

n

V

n

=

The approximation for is given by an average of all the

n

=

1

N

N1

X

n=0

n

=

1

Nw

N1

X

n=0

V

n+1

V

n

V

n

= (5.5.18)

The volatility is the square root of the unbiased variance of the above data

2

=

1

(N 1)w

N1

X

n=0

µ

V

n+1

V

n

V

n

w

¶

2

= (5.5.19)

Thus, if

2

is large, then one may expect in the future large variations in the

market values of the underlying asset. Volatilities often range from near 0=05

for government bonds to near 0

=40 for venture stocks.

5.5.4 Method

The numerical approximation to the Black-Scholes model in (5.5.10)-(5.5.17)

is similar to the explicit method for heat diusion in one space variable. Here

we replace the space variable by the value of the underlying asset and the

temperature by the value of the American put option contract. In order to

obtain an initial condition, we replace the time variable by

W w= (5.5.20)

Now abuse notation a little and write S(V> ) in place of S (V> w) = S (V> W )

so that

S

replaces S

w

in (5.5.17). Then the condition at the exercise date in

(5.5.10) becomes the initial condition. With the boundary conditions in (5.5.11)

and (5.5.12) one may apply the explicit finite dierence method as used for the

heat di

usion model to obtain S

n+1

l

approximations for S (lV> (n + 1))=

But, the condition in (5.5.15) presents an obstacle to the value of the option.

Here we simply choose the

S

n+1

l

= max(H V

l

> 0) if S

n+1

l

? max(H V

l

> 0)=

© 2004 by Chapman & Hall/CRC

224 CHAPTER 5. EPIDEMICS, IMAGES AND MONEY

Explicit Method with Projection for (5.5.10)-(5.5.17).

Let

(@(V)

2

)(

2

@2)=

S

n+1

l

= S

n

l

+ V

2

l

(S

n

l

1

2S

n

l

+ S

n

l

+1

)

+ (

@V) uV

l

(S

n

l

+1

S

n

l

) uS

n

l

= V

2

l

S

n

l

1

+ (1 2V

2

l

(@V) uV

l

u)S

n

l

+(V

2

l

+ (@V) uV

l

)S

n

l

+1

S

n+1

l

= max(S

n+1

l

> max(H V

l

> 0))=

The conditions (5.5.13) and (5.5.14) at V = V

i

do not have to be explicitly

implemented provided the time step is suitably small. This is another

version of a stability condition.

Stability Condition.

(@(V)

2

)(

2

@2)

1

2V

2

l

(@V) uV

l

u A 0=

5.5.5 Implementation

The MATLA B code bs1d.m is an implementation of the explicit method for the

American put option contract model. In the code the array

{ corresponds to

the value of the underlying asset, and the array x corresponds to the value of

the American put option contract. The time step,

gw, is for the backward time

step with initial condition corresponding to the exercise payo

of the option.

Lines 1-14 define the parameters of the model with exercise price

H = 1=0. The

payo obstacle is defined in lines 15-20, and the boundary conditions are given

in lines 21 and 22. Lines 23 -37 are the implementation of the explicit scheme

with projection to payo

obstacle given in lines 30-32. The approximate times

when market prices correspond to the optimal exercise times are recorded in

lines 33-35. These are the approximate points in asset space and time when

(5.5.13) and (5.5.14) hold, and the output for time versus asset space is given

in figure(1) by lines 38 and 39. Figure(2) generates the value of the American

put option contract for four di

erent times.

MATLAB Code bs1d.m

1. % Black-Scholes Equation

2. % One underlying asset

3. % Explicit time with projection

4. sig = .4

5. r = .08;

6. n = 100 ;

7. maxk = 1000;

8. f = 0.0;

9. T = .5;

10. dt = T/maxk;

© 2004 by Chapman & Hall/CRC

5.5. OPTION CONTRACT MODELS 225

11. L = 2.;

12. dx = L/n;

13. alpha =.5*sig*sig*dt/(dx*dx);

14. sur = zeros(maxk+1,1);

15. % Define the payo

obstacle

16. for i = 1:n+1

17. x(i) = dx*(i-1);

18. u(i,1) = max(1.0 - x(i),0.0);

19. suro(i) = u(i,1);

20. end

21. u(1,1:maxk+1) = 1.0; % left BC

22. u(n+1,1:maxk+1) = 0.0; % right BC

23. % Use the explicit discretization

24. for k = 1:maxk

25. for i = 2:n

26. u(i,k+1) = dt*f+...

27. x(i)*x(i)*alpha*(u(i-1,k)+ u(i+1,k)-2.*u(i,k))...

28. + u(i,k)*(1 -r*dt) ...

29. -r*x(i)*dt/dx*(u(i,k)-u(i+1,k));

30. if (u(i,k+1)

?suro(i)) % projection step

31. u(i,k+1) = suro(i);

32. end

33. if ((u(i,k+1)

Asuro(i)) & (u(i,k)==suro(i)))

34. sur(i) = (k+.5)*dt;

35. end

36. end

37. end

38. figure(1)

39. plot(20*dx:dx:60*dx,sur(20:60))

40. figure(2)

41. %mesh(u)

42. plot(x,u(:,201),x,u(:,401),x,u(:,601),x,u(:,maxk+1))

43. xlabel(’underlying asset’)

44. ylab el(’value of option’)

45. title(’American Put Option’)

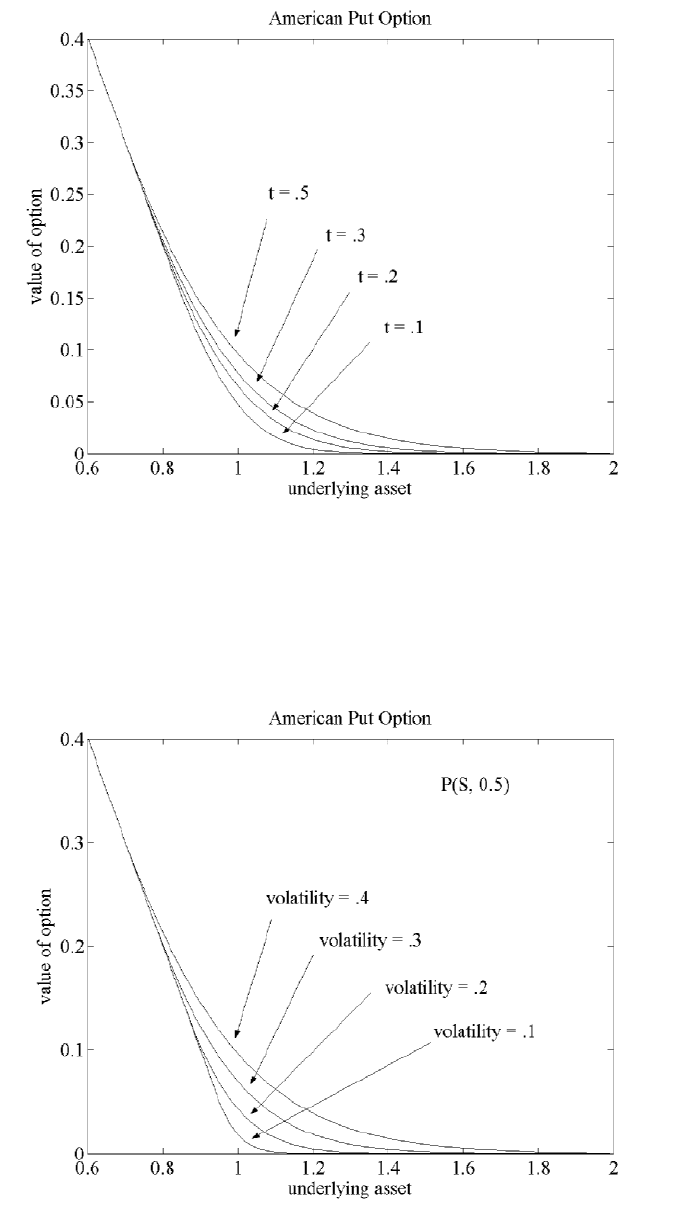

values of the American put option contracts are increasing with respect to

(decreasing with respect to time w). Careful inspection of the curves will verify

that the conditions at

V

i

in (5.5.13) and (5.5.14) are approximately satisfied.

at time

w = 0=5 and variable volatilities = 0=4> 0=3> 0=2 and 0=1= Note as the

volatility decreases, the value of the option contract decreases towards the payo

value. This monotonicity prop erty can be used to imply volatility parameters

based on past market data.

© 2004 by Chapman & Hall/CRC

Figure 5.5.2 contains the output for the above code where the curves for the

Figure 5.5.3 has the curves for the value of the American put option contracts

226 CHAPTER 5. EPIDEMICS, IMAGES AND MONEY

Figure 5.5.2: P(S,T-t) for Variable Times

Figure 5.5.3: Option Values for Variable Volatilities

© 2004 by Chapman & Hall/CRC

5.5. OPTION CONTRACT MODELS 227

Figure 5.5.4: Optimal Exercise of an American Put

Figure 5.5.4 was generated in part by figure(1) in bs1d.m where the smooth

curve represents the time when

V equals the optimal exercise of the American

put option contract. The vertical axis is

= W w> and the horizontal axis

is the value of the underlying asset. The non smooth curve is a simulation of

the daily market values of the underlying asset. As long as the market values

are above

V

i

(w)> the value of the American put option contract will be worth

more than the value of the payo

, max(H V> 0)> of the American put option

contract. As soon as the market value is equal to

V

i

(w)> then the American

put option contract should be exercised This will generate revenue H = 1=0

where the

w is about 0.06 before the expiration date and the market value

is about

V

i

(w) = 0=86= Since the holder of the American put option contract

will give up the underlying asset, the value of the payo

at this time is about

max(H V> 0) = max(1=0 0=86> 0) = 0=14=

5.5.6 Assessment

As usual the parameters in the Black-Scholes model may depend on time and

may be di

!cult to estimate. The precise assumptions under which the Black-

Scholes equation models option contracts should be carefully studied. There are

a numb er of other option contracts, which are di

erent from the American put

option contract. Furthermore, there may be more than one underlying asset,

and this is analogous to heat di

usion in more than one direction.

The question of convergence of the discrete model to the continuous model

needs to be examined. These concepts are closely related to a well studied

© 2004 by Chapman & Hall/CRC

228 CHAPTER 5. EPIDEMICS, IMAGES AND MONEY

applied area on "free boundary value" problems, which have models in the

form of variational inequalities and linear complementarity problems. Other

applications include mechanical obstacle problems, heat transfer with a change

in phase and fluid flow in earthen dams.

5.5.7 Exercises

1. Experiment with variable time and asset space steps.

2.

3. Experiment with variable interest rates

u.

4. Experiment with variable exercise values

H=

5. Experiment with variable expiration time W> and examine figure(1) gen-

erated by bs1d.m.

5.6 Black-Scholes Model for Two Assets

5.6.1 Introduction

A portfolio of investments can have a number of assets as well as a variety of

option contracts. Option contracts can have more than one underlying asset

and di

erent types of payo

The Black-Scholes two assets model is similar to the heat diusion model in

two space variables, and the explicit time discretization will also be used to

approximate the s olution.

5.6.2 Application

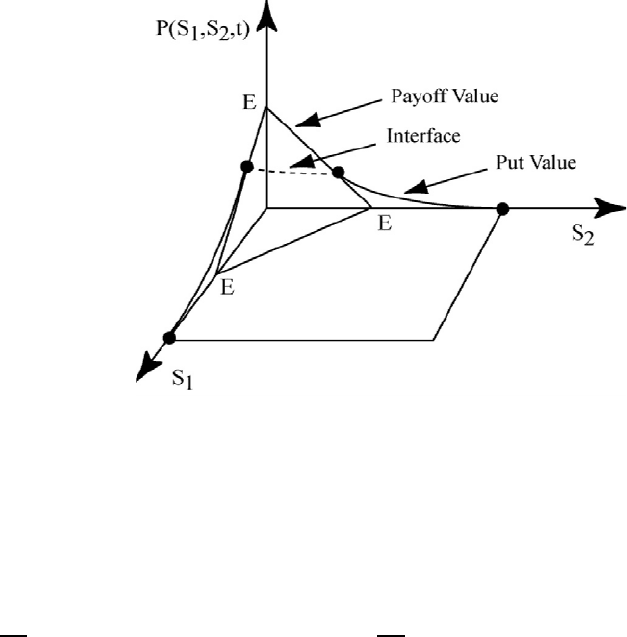

Consider an American put option contract with two underlying assets and a

payo

function max(H V

1

V

2

> 0) where H is the exercise price and V

1

and

V

2

are the values of the underlying assets. This is depicted in Figure 5.6.1

where the tilted plane is the positive part of the payo

function. The value of

the put contract must be ab ove or equal to the payo

function. The dotted

curve indicates where the put value separates from the payo

function; this

is analogous to the

V

i

(w) in the one asset case. The dotted line will change

with time so that as time approaches the expiration date the dotted line will

move toward the line

H V

1

V

2

= 0 = S . If the market values for the two

underlying assets at a particular time are on the dotted line for this time, then

the option should be exercised so as to optimize any profits.

5.6.3 Model

Along the two axes where one of the assets is zero, the model is just the

Black-Scholes one asset model. So the boundary conditions for the two as-

set mo del must come from the solution of the one asset Black-Scholes model.

© 2004 by Chapman & Hall/CRC

Duplicate the calculations in Figures 5.5.2 and 5.5.3.

functions such as illustrated in Figures 5.6.1-5.6.3.

5.6. BLACK-SCHOLES MODEL FOR TWO ASSETS 229

Figure 5.6.1: American Put with Two Assets

Let

S (V

1

> V

2

> w) be the value of the American put option contract. For positive

values of the underlying assets the Black-Scholes equation is

S

w

+

2

1

2

V

2

1

S

V

1

V

1

+

1

1

12

V

1

V

2

S

V

1

V

2

+

2

2

2

V

2

2

S

V

2

V

2

+uV

1

S

V

1

+uV

2

S

V

2

uS = 0=

(5.6.1)

The following initial and boundary conditions are required:

S (V

1

> V

2

> W ) = max(H V

1

V

2

> 0) (5.6.2)

S (0> 0> w) = H (5.6.3)

S (O> V

2

> w) = 0 for O AA H (5.6.4)

S (V

1

> O> w) = 0 (5.6.5)

S (V

1

> 0> w) = from the one asset model (5.6.6)

S (0> V

2

> w) = from the one asset model. (5.6.7)

The put contract value must be at least the value of the payo

function

S (V

1

> V

2

> w) max(H V

1

V

2

> 0)= (5.6.8)

Other payo

functions can be used, and these will result in more complicated

boundary conditions. For example, if the payo

function is pd{(H

1

V

1

> 0=0)+

pd{(H

2

V

2

> 0=0)> then S (O> V

2

> w) and S (V

1

> O> w) will be nonzero solutions of

two additional one asset models.

Black Scholes Model of an American Put with Two Assets.

Let the payo function be max(H V

1

V

2

> 0)=

Require the inequality in (5.6.8) to hold.

The initial and boundary condition are in equations (5.6.2)-(5.6.7).

Either

S (V

1

> V

2

> w) = H V

1

V

2

or S (V

1

> V

2

> w) satisfies (5.6.1).

© 2004 by Chapman & Hall/CRC