Whittenburg Gerald E., Altus-Buller Martha. Income Tax Fundamentals

Подождите немного. Документ загружается.

Questions and Problems 9-57

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

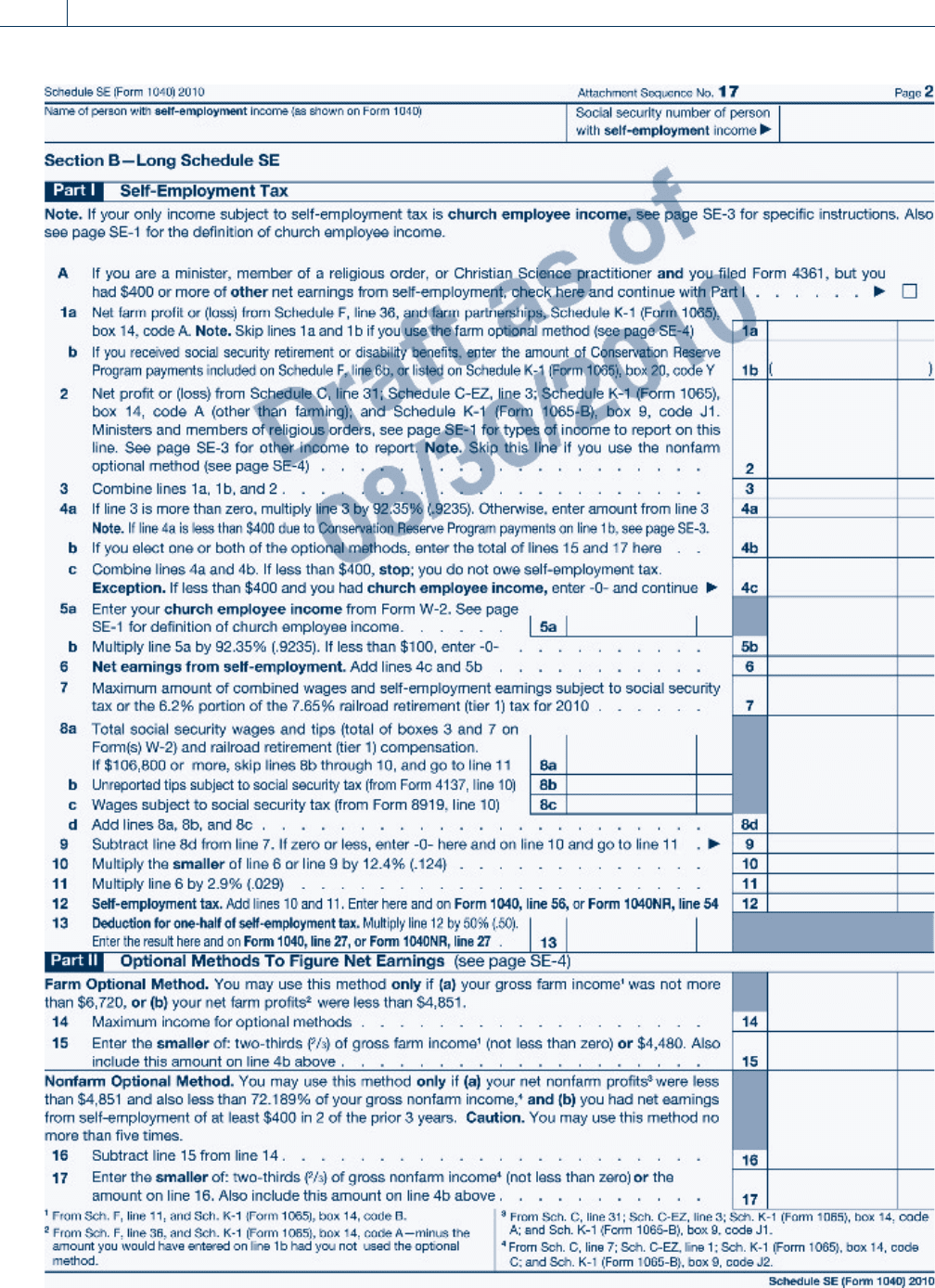

106,800

4,480 00

9-58 Chapter 9

Withholding, Estimated Payments, and Payroll Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Questions and Problems 9-59

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

9-60 Chapter 9

Withholding, Estimated Payments, and Payroll Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Student Name

Class/Section

Date

KEY NUMBER TAX RETURN SUMMARY

Chapter 9

Comprehensive Problem 1

Adjusted Gross Income (Line 37) ________________

Profit or Loss from Business (Line 12) ________________

Total Self-Employment Tax, Schedule SE (Line 5) ________________

Tax Liability (Line 60) ________________

Tax Overpaid (Line 73) ________________

Questions and Problems 9-61

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

c

Dmitriy Shironosov/Shutterstock

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Chapter 10

Partnership Taxation

LEARNING OBJECTIVES

.............................................. .........................

After completing this chapter, you should be able to:

LO 10.1 Define a partnership for tax purposes.

LO 10.2 Understand the basic tax rules for partnership formation

and operation.

LO 10.3 Describe the tax treatment of partnership distributions.

LO 10.4 Determine partnership tax years.

LO 10.5 Identify the tax treatment of transactions between

partners and their partnerships.

LO 10.6 Understand the application of the at-risk rule to

partnerships.

LO 10.7 Analyze the advantages and disadvantages of limited

liability companies (LLCs).

Overview

In recent yea rs, partnerships have been used increasingly as an organizational form. The

partnership form allows taxpayers considerable flexibility in terms of contributions, income

and loss allocations, and distributions. One of the primary benefits of the partnership is

that partnership income is only taxed at the partner level. Corporate taxpayers (other

than ‘‘S’’ corporation s) pay tax at the corporate level and often again at the shareholder

level (see Chapter 11), which results in corporate ‘‘double taxation.’’ Since a partnership’s

income passes through to the partners, there is no tax at the entity level, only at the partner

level.

One of the disadvantages of partnerships over corporations has been the lack of limited

liability for partners while corporate shareholders enjoy protection from liability to third

parties (e.g., creditors of the corporation). In recent years, however, the advent of the lim-

ited liability company (LLC) and the limited liability partnership (LLP) has provided part-

ners this important legal benefit. Because LLCs and LLPs are taxed like partnerships, they

are included in this chapter on partnership taxation.

This chapter will provide an understanding of the tax treatment of partnerships and the

tax forms (Form 1065 and Schedule K-1) related to reporting partnership income or loss.

10-1

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 10.1

NATURE OF PARTNERSHIP TAXATION

Partnership tax returns are information returns only. Returns show the amount of income

by type and the allocation of the income to the partners. Partnership income and other

items are passed through to the partners, and each partner is taxed on his or her distributive

share of partnership income. Partnership income is taxable to the partner even if he or she

does not actually receive it in cash.

Even though the return is only informational, partnerships do have to make various

elections and select accounting methods and periods. For example, partnerships must select

depreciation and inventory methods. In addition, partnerships are legal entities under civil

law, and in most states have rights under the Uniform Partnership Act.

What Is a Partnership?

The tax law defines a partnership as a syndicate, group, pool, joint venture, or other unin-

corporated organization through or by means of which any business, financial operation, or

venture is carried on, and which is not classified as a corporation, trust, or estate. The mere

co-ownership of property does not co nstitute a partnership; the partners must engage in

some type of business or financial activity.

Ordinary partnerships, or general partnerships as they are often called, may be formed

by a simple verbal agreement or ‘‘ha ndshake’’ between partners. In contrast, the forma-

tion of corporations, limited partnerships, limited liability companies (LLCs), and lim-

ited liability partnerships (LLPs) must be documented in writing and the entity must be

legally registered in the state in which it is formed. Even though general partnerships

may be formed by verbal agreement between partners, partners usually document their

agreement in writing with the help of lawyers in case disagreements arise in the course

of operations. General partners usually take on the risk of legal liability for certain

actions of the partnership or debts of the partnership, as specified under state law. To

limit some of the liability exposure of operating a joint business, many partnerships

are created formally as limited partnerships, LLCs, or LLPs for licensed professionals

such as attorneys and accountants.

Entities generally treated as partnerships for tax law purposes include limited partner-

ships, limited liability companies (LLCs), and LLPs. Limited partnerships have one or

more general partners and one or more limited partners. General par tners participate in

management and have unlimited liability for partnership obligations. Limited partners

may not participate in management and have no liability for partnership obligations

beyond their capital contributions. Many partnerships are formed as limited partnerships

because the limited liability helps to attract passive investors. LLCs and LLPs are relatively

new legal entities which co mbine t he limited liability of corporations with the tax treat-

ment of partnerships. LLCs and LLPs are discussed later in this chapter.

EXAMPLE Avery and Roberta buy a rental house which they hold jointly.

The house is rented and they share the income and expenses for

the year. Avery and Roberta have not formed a partnership.

However, if they had bought and operated a store together, a

partnership would have been formed. Although the ownership

of real estate may not rise to the level of a business requiring

a partnership return, co-owners of real estate frequently do

choose to operate in partnership, limited partnership, or LLC

form. N

10-2 Chapter 10

Partnership Taxation

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 10.2PARTNERSHIP FORMATION

Generally, there is no gain or loss recognized by a partnership or any of its partners when

property is contributed to a partnership in exchange for an interest in the partnership. This

rule applies to the formation of a partnership as well as any subsequent contributions to the

partnership. However, there are exceptions to the nonrecognition rule. On formation, income

may be recognized when a partnership interest is received in exchange for services performed

by the partner for the partnership or when a partner transfers to a partnership property subject

to a liability exceeding that partner’s basis in the property transferred. In this situation, gain is

recognized to the extent that the portion of the liability allocable to the other partners exceeds

the basis of the property contributed. If a partner receives money or other property from the

partnership, in addition to an interest in the partnership, the transaction may be considered in

part a sale or exchange, and a gain or loss may be recognized.

EXAMPLE Dunn and Church form the Dunn & Church Partnership. Dunn contrib-

utes a building with a fair market value of $90,000 and an adjusted

basis of $55,000 for a 50 percent interest in the partnership. Dunn

does not recognize a gain on the transfer of the building to the part-

nership. Church performs services for the partnership for his 50 per-

cent interest which is worth $90,000. Church must report $90,000 in

ordinary income for the receipt of an interest in the partnership in

exchange for services provided to the partnership. N

EXAMPLE Ann and Keith form the A&K Partnership. Ann contributes a building

with a fair market value of $200,000 and an adjusted basis of $45,000

for a 50 percent interest in the partnership. The building is subject to

a liability of $130,000. Keith contributes cash of $70,000 for a 50 per-

cent interest in the partnership. Ann must recognize a gain on the

transfer of the building to the partnership equal to $20,000, the

amount by which the liability allocable to Keith, $65,000 (50%

$130,000), exceeds the basis of the building, $45,000. Keith does not

recognize a gain on the contribution of cash to the partnership. N

Self-Study Problem 10.1

Indicate, by placing a check in the appropriate blank, whether each of the

following is or is not required to file a partnership return.

Yes No

1. Duncan and Clyde purchase and operate a plumbing

business together.

________ ________

2. Ellen and Walter form a corporation to operate a

plumbing business.

________ ________

3. George and Marty buy a duplex to hold as rental

property, which is not considered an active business.

________ ________

4. Howard and Sally form a joint venture to drill for and

sell oil.

________ ________

5. Ted and Joyce purchase and operate a candy store. ________ ________

Section 10.2

Partnership Formation 10-3

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

A partner’s original basis in a partnership interest is equal to the basis of the property

transferred plus cash contributed to the partnership. If gain is recognized on the transfer,

the partner’s basis in the partnership interest is increased by the gain recognized. In addi-

tion, the basis is reduced by any liabilities of the contributing partner assumed by the other

partners through the partnership. For example, if a one-third partner is relieved of a

$90,000 liability by the partnership, he or she would reduce by $60,000 (

2

/

3 of $90,000)

his or her partnership interest basis. After the original basis in the partnership interest is

established, the basis is adjusted for future earnings, losses, and distributions from the

partnership.

EXAMPLE Prentice contributes cash of $50,000 and property with a fair

market value of $110,000 (adjusted basis of $30,000) to the P&H

Partnership. Prentice’s basis in the partnership interest is $80,000

($50,000 þ $30,000). N

EXAMPLE Assume that Prentice, in the above example, also received a partner-

ship interest worth $15,000 for services provided to the partnership.

She must recognize $15,000 in ordinary income, and her basis in the

partnership interest is $95,000 ($80,000 þ $15,000). N

EXAMPLE Darnell contributes property with a fair market value of $110,000 and

an adjusted basis of $30,000, subject to a liability of $20,000, to a

partnership in exchange for a 25 percent interest in the partnership.

Darnell’s basis in his partnership interest is $15,000 [$30,000

($20,000 75%)]. N

The basis of a partner’s interest in a p artnership changes due to partnership activities.

A partner’s basis in his or her partnership interest is increased by the partner’s share of

(1) additional contributions to the pa rtnership, (2) net ordinary taxable income of the

partnership, and (3) capital gains and other income of the partnership. Alternatively, a

partner’s basis is reduced (but not below zero) by the partner’s share of (1) distributions

of partnership property, (2) losses from operations of the partnership, and (3) capital

losses and other deductions of the partnership. In addition, changes in partnership liabil-

ities will affect the basis of a partner’s partnership interest.

EXAMPLE Reid has a 50 percent interest in the Reid Partnership. Her basis in her

partnership interest at the beginning of 2010 is $12,000. For 2010, the

partnership reports ordinary income of $15,000, a capital gain of

$3,000, and charitable contributions of $700. The basis of Reid’s part-

nership interest, after considering the above items, would be $20,650

($12,000 beginning basis þ $7,500 share of partnership ordinary

income þ $1,500 share of partnership capital gain $350 share of

partnership charitable contributions). N

The partnership’s basis in property contrib uted by a partner is equal to the partner’s

adjusted basis in the property at the time of the contribution plus any gain recognized

by the partner. The transfer of liabilities to the partnership by the partner does not impact

the basis of the property to the partnership. The partnership’s holding period for the prop-

erty contributed to the partnership includes the partner’s holding period. For example,

long-term capital gain property may be transferred to a partnership by a partner and

10-4 Chapter 10

Partnership Taxation

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.