Whittenburg Gerald E., Altus-Buller Martha. Income Tax Fundamentals

Подождите немного. Документ загружается.

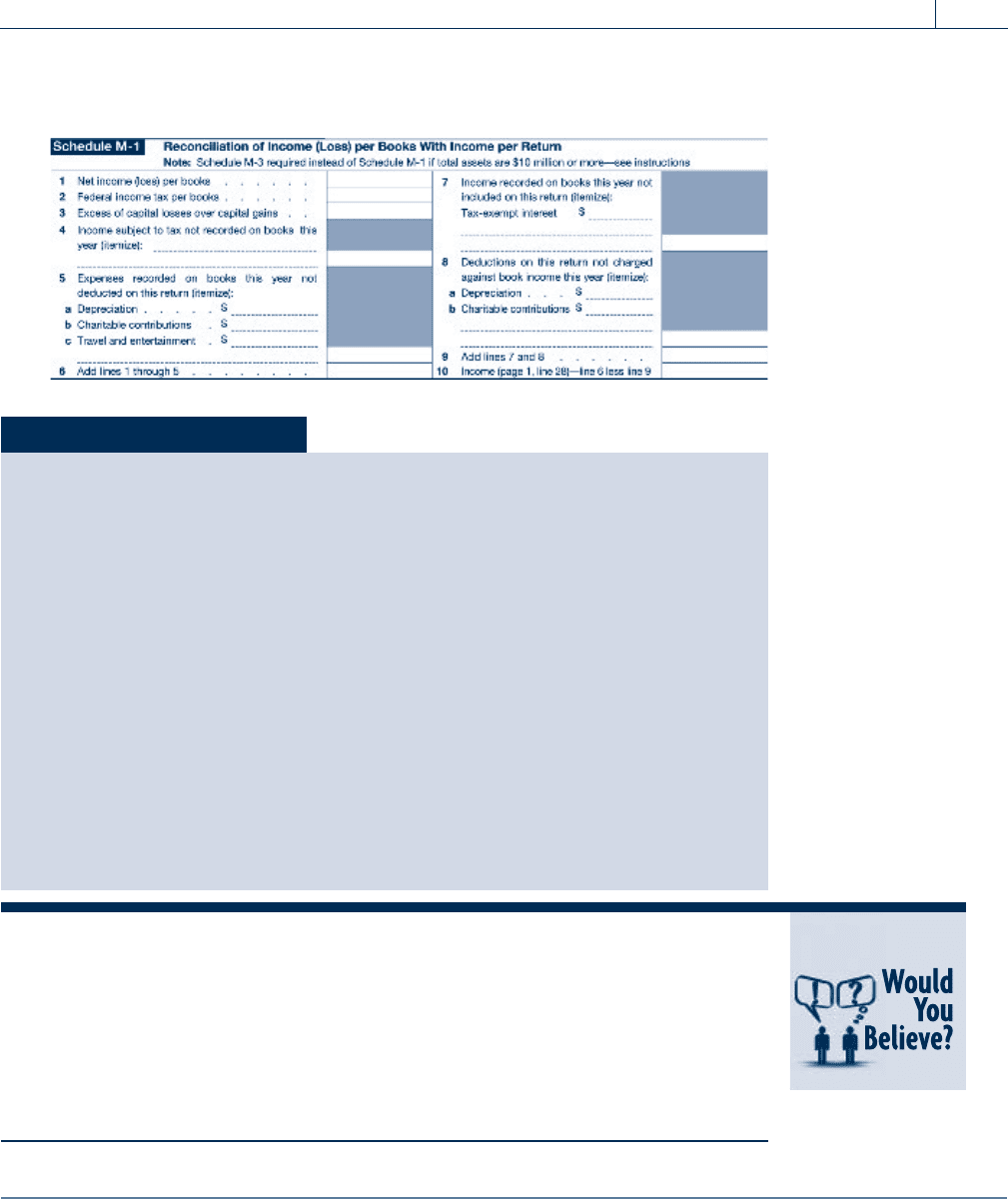

Wisteria Corporation’s Schedule M-1, Form 1120, is illustrated below.

40,000

4,000

65,000

interest

16,000

5,000

9,000

9,000

3,500

12,500

52,500

3,500

In 2010, a new tax form will be required for certain large corporations: Schedule

UTP, Uncertain Tax Position Statement. This form has rattled the accounting

world, since it requires corporations to disclose the uncertain tax positions taken

on corporate tax returns directly to the IRS. The IRS is expected to use Schedule

UTP to make audits of corporations more pointed and efficient and to generate

more tax revenue. However, corporations will likely fight back through the

courts, and they may win the right to keep ‘‘privileged’’ information private.

Only time will tell how Schedule UTP will affect IRS audits of large corporations.

SECTION 11.5

FILING REQUIREMENTS AND ESTIMATED TAX

The tax return form for a regular corporation is Form 1120; for an S corporation, the tax

return form is Form 1120S. Corporate tax returns are due on or before the fifteenth day of

the third month following the close of the corporation’s tax year, but corporations may

receive an automatic 6-month extension by filing Form 7004. A corporation must pay

any tax liability by the original due date of the return.

Corporations must make estimated tax payments in a m anner similar to those made by

self-employed individual taxpayers. The payments are made in four installments due on the

fifteenth day of the fourth, sixth, ninth, and twelfth months of the corporation’s tax year.

Self-Study Problem 11.4

Redwood Corporation has net income from its books of $104,0 00. For the cur-

rent year, the corporation had federal income tax expense of $41,000, a net

capital loss of $9,100, and tax-exempt interest income of $4,700. The company

deducted depreciation of $17,000 on its tax return and $13,000 on its books.

Using Schedule M-1 below, calculate Redwood Corporation’s taxable income,

before any net operating loss or special deductions, for the current year.

N

Section 11.5

Filing Requirements and Estimated Tax 11-7

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Small corporations with less than $250,000 in gross receipts and less than

$250,000 in assets do not have to complete Schedule L (Balance Sheet) or Sched-

ules M-1 and M-2. The rule applies to both S and C corporations, and allows

small businesses to keep records based on their checkbook or cash receipts and

disbursements journal. This makes the reporting requirements for a small corpo-

ration similar to the reporting requirements for a Schedule C sole proprietorship.

Self-Study Problem 11.5

Aspen Corporation was formed and began operations on January 1, 2010.

Aspen Corporation

Income Statement

For the Year Ended December 31, 2010

Gross income from operations $285,000

Qualified dividends received from a 10 percent

owned domestic corporation

10,000

Total gross income $295,000

Cost of goods sold

(80,000)

Total income $215,000

Other expenses:

Compensation of officers $ 90,000

Salaries and wages 82,000

Repairs 8,000

Depreciation expense 5,000

Payroll taxes

11,000

Total other expenses

(196,000)

Net income (before federal income tax expense)

$ 19,000

Aspen Corporation

Balance Sheet

as of December 31, 2010

Assets:

Cash $ 35,000

Accounts receivable 10,000

Land 18,000

Building 125,000

Less: accumulated depreciation

(5,000)

Total assets

$183,000

Liabilities and owners’ equity:

Accounts payable $ 25,800

Common stock 140,000

Retained earnings

17,200

Total liabilities and owners’ equity

$183,000

Aspen Corporation made estimated tax payments of $2,000.

Based on the above information, complete Form 1120 on pages 11-9

through 11-13. Assume the corporation’s federal income tax expense is equal

to its 2010 federal income tax liability and that any tax overpayment is to be

applied to the next year’s estimated tax. Schedule UTP is not required.

11-8 Chapter 11

The Corporate Income Tax

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Section 11.5

Filing Requirements and Estimated Tax 11-9

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

11-10 Chapter 11

The Corporate Income Tax

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Section 11.5

Filing Requirements and Estimated Tax 11-11

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

11-12 Chapter 11

The Corporate Income Tax

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Section 11.5

Filing Requirements and Estimated Tax 11-13

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

11-14 Chapter 11

The Corporate Income Tax

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 11.6

S CORPORATIONS

Certain qualified small business corporations (S corporations) may elect to be taxed in a manner

similar to partnerships. An S corporation does not generally pay tax, and each shareholder

reports his or her share of corporate income. The S corporation election is designed to relieve

small corporations of certain corporate tax disadvantages, such as the double taxation of income.

To elect S corporation status, a corporation must be a small business corporation with

the following characteristics:

1. The corporation must be a domestic corporation;

2. The corporation must have 100 or fewer shareholders who are all either individuals,

estates, certain trusts, certain financial institutions, or certain exempt organizations;

3. The corporation must have only one class of stock; and

4. All shareholders m ust be U.S. citizens or resident aliens.

The S corporation election must be made during the prior year or the first two and one-

half months of the current tax year to obtain the status for the current year.

EXAMPLE Laurel Corporation is a calendar year corporation that makes an S cor-

poration election on April 2, 2010. The corporation is not an S corpo-

ration until the 2011 tax year; it is a regular corporation for 2010. N

After electing S corporation status, the corporation retains the status until the election is

voluntarily revoked or statutorily terminated. If the corporation ceases to be a small busi-

ness corporation (for exam ple, it has 102 sharehol ders in 2010), the election is statutorily

terminated. Also, the election is terminated when a corporation receives 25 percent

or more of its gross income from passive investments for 3 consecutive tax years and the

corporation has accumulated earnings and profits at the end of each of those years. If a cor-

poration experiences an involuntary termination of S corporation status, the election is ter-

minated on the day the status changes. For example, the loss of S corporation status on

June 1, 2010, causes the corporation to be a regul ar corporation from that day on.

Upon consent of shareholders owning a majority of the voting stock, an S corporation

election can be voluntarily revoked. If the consent to revoke the election is made during

the first two and one-half months of the tax year, the S corporation status will be considered

voluntarily terminated effective at the beginning of that year. Shareholders may specify a date

on or after the date of the revocation as the effective date for the voluntary termination of the

S corporation election. If a prospective revocation date is not specified, and the consent to

revoke the election is made after the fifteenth day of the third month of the tax year, the ear-

liest that the S corporation status can be terminated is the first day of the following tax year.

EXAMPLE On January 20, 2010, Juniper Corporation, a calendar year corpora-

tion, files a consent to revoke its S corporation election. No date is

specified in the consent as the effective date of the revocation. The

corporation is no longer an S corporation effective January 1, 2010.

If the election were made after March 15, the corporation would not

become a regular corporation until the 2011 tax year. N

Reporting Income

Each shareholder of an S corporation reports his or her share of corporate income based on

his or her stock ownership during the year. The taxable income of an S corporation is com-

puted in the same manner as for a partnership.

Each shareholder of an S corporation takes into account separately his or her share of

items of income, deductions, and credits on a per share per day basis. Schedule K-1 of

Section 11.6

S Corporations 11-15

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Form 1120S is used to report the allocation of ordinary income or loss, plus all separately

stated items of income or loss, to each of the shareholders. Each shareholder’s share of

these items is included in the shareholder’s computation of taxable income for the tax

year during which or with which the corporation’s year ends. In the case of the death of

a shareholder, the shareholder’s portion of S corporation items will be taken into account

on the shareholder’s final tax return.

EXAMPLE Freda is the sole shareholder of the Freda Corporation, which has an

S corpo ration election in effect. During calendar year 2010, the corpo-

ration has ordinary taxable income of $100,000. Freda must report

$100,000 on her individual income tax return for 2010 as income from

the Freda Corporation. N

S Corporation Losses

Losses from an S corporation also pass through to the shareholders. However, the amount of

loss from an S corporation that a shareholder may report is limited to his or her adjusted

basis in the corporation’s stock plus the amount of any loans from the shareholder to the cor-

poration. Any loss in excess of the shareholder’s basis in the stock of the corporation plus

loans is a carryforward. If a shareholder was not a shareholder for the entire tax year, losses

must be allocated to the shareholder on a daily basis. This prevents a shareholder from sell-

ing losses late in the year to another taxpayer by selling the stock of an S corporation.

EXAMPLE Lawson and Mary are equal shareholders in L&M Corporation, an

S corporation. On December 1, 20XX, Mary sells her interest to

Connley for $15,000. Lawson’s basis in his L&M Corporation stock

is $10,000. For the 20XX tax year, the corporation has a loss of

$24,000. Lawson can deduct only $10,000 of his half of the loss

($12,000), since that is the amount of his stock basis. Even though

she is not a sha reholde r at yea r end, Mary may deduct $1 0,981 of

the loss, which is 334/365 of $12,000, assuming her basis w as at least

that amount. Connley may deduct $1,019, 31/365 of $12,000. In leap

years, the amounts would be $10,984 (335/366 $12,000) and

$1,016 (31/366 $12,000), respectively. N

Pass-through Items

Certain items pass through from an S corporation to the shareholders and retain their tax

attributes on the shareholders’ tax returns. The following are examples of pass-through items:

1. Capital gains and losses

2. Section 1231 gains and losses

3. Dividend income

4. Charitable contributions

5. Tax-exempt interest

6. Most credits

Special Taxes

S corporations are not subject to the corporate income tax on their regular taxable income.

Under certain circumstances, an S corporation may be liable for tax at the corporate level. An

S corporation may be subject to a tax on gains attributable to appreciation in the value of

assets held by the corporation prior to the S corporation electi on, the built-in gains tax.

In addition, a tax may be imposed on certain S corporations that have large amounts of pas-

sive investment income, such as income from dividends and interest. The rules for the appli-

cation of these taxes are complex.

11-16 Chapter 11

The Corporate Income Tax

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.