ACCA F6 FA09 Study Text 2010

Подождите немного. Документ загружается.

Chapter 10: Partnerships

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 205

Partnership losses

The allocation of partnership losses

The loss relief options available to each partner

Limited liability partnerships

3 Partnership losses

3.1 The allocation of partnership losses

If a partnership makes a trading loss, it is allocated between the partners in

accordance with the partnership agreement in the accounting period in which it

arises.

The allocation of partnership losses is therefore the same as for profits. Any fixed

salary or interest on partner’s capital must be allocated first. These items are classed

as trading income for the partners. The balance of the loss is then allocated in

accordance with the profit-sharing ratio.

Example

Frank and Gwen are in partnership and have the following partnership agreement:

Frank Gwen

£ £

Salary (per annum) 45,000 25,000

Capital introduced 70,000 70,000

Annual interest on capital

8% 8%

Profit sharing ratio

40% 60%

The adjusted loss of the partnership after capital allowances for the year ended 31

December 2009 was £126,000.

Required

Allocate the partnership profits for the year ended 31 December 2009 between Frank

and Gwen.

Answer

Total

Frank

Gwen

£

£

£

Salary

70,000

45,000

25,000

Interest on capital introduced (8% × £70,000)

11,200

5,600

5,600

81,200

50,600

30,600

Balance of loss (40%: 60%) (207,200)

(82,880)

(124,320)

Allocation of loss

(126,000)

(32,280)

(93,720)

Paper F6 (UK): Taxation FA2009

206 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Note that the balance of the partnership loss is the adjusted loss of the partnership

after capital allowances, plus the partners’ salaries and income on capital. This

balancing loss is shared between the partners in their profit-sharing ratio.

3.2 The loss relief options available to each partner

Each partner can choose to use his share of the loss in the most beneficial way. There

is no requirement for all partners to utilise their losses in the same way.

The options available are the same as those available to a sole trader, and depend on

whether the partner is joining the firm, leaving the firm or is an ongoing partner.

In summary, the options are as follows:

Opening years Ongoing years Closing years

= When the partner joins

the firm, the first four tax

years

The partner is in at least his

fifth tax year and continues

to be a partner

= When the partner

leaves the firm

s64 claim (plus

additional relief if loss

arises in 2009/10)

s64 claim (plus additional

relief if loss arises in 2009/10)

s64 claim (plus

additional relief if loss

arises in 2009/10)

s261B extension claim s261B extension claim s261B extension claim

s83 carry forward s83 carry forward s86 claim if business

incorporated

s72 claim s89 claim

Note that where an individual carries on a trade in a non-active capacity (e.g. is a

‘sleeping’ partner) the loss relief available under s64 and s72 is restricted to a

maximum of £25,000.

An individual is classed as non-active for this purpose if he spends less than 10

hours a week on average on the trading activities of the business.

3.3 Limited liability partnerships

A limited liability partnership (LLP) is a partnership whereby the partners’ liability

to contribute towards the partnership debts and losses is limited in the partnership

agreement.

A partner in an LLP is taxed in the same way as a partner in a normal partnership.

However, the amount of loss that can be relieved against non-partnership income is

restricted to the total contribution to the business by that partner by the end of the

tax year against which a claim for loss relief is being made.

The total contribution of a partner is the total capital introduced to the business by

him plus his share of any profits earned while he has been a partner less any

drawings by him.

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 207

Paper F6 (UK)

Taxation FA2009

CHAPTER

11

Taxation relief for pension

contributions

Contents

1 Overview of taxation relief for pensions

2 The maximum relief available

3 Relief for contributions to occupational pension

schemes

4 Relief for personal pension plan contributions

Paper F6 (UK): Taxation FA2009

208 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Overview of taxation relief for pensions

The choices available for providing a pension for retirement

Overview of the options available for pension contributions

1 Overview of taxation relief for pensions

1.1 The choices available for providing a pension for retirement

A pension scheme is a fund of assets set up with the intention of providing lump

sum benefits and a regular income (pension) for the members of the scheme on their

retirement and/or benefits for dependants after their death.

An individual usually starts to contribute into a pension scheme early in his

working life, with the intention of accumulating sufficient funds to pay for his

retirement years.

The Government wishes to encourage individuals to make tax efficient provision for

their retirement, therefore generous tax relief is given for pension contributions.

In addition to tax relief for the pension contributions, any income or profits earned

by the pension fund itself are exempt from income tax and capital gains tax.

Investments held in a pension fund will therefore grow in value more rapidly than

investments held by an individual personally.

On retirement, an individual can withdraw from the pension fund a lump sum and

regular pension income thereafter. Lump sum payments are tax-free. However,

regular pension income is taxable.

Rules on pension contributions

The choices for providing a pension and the tax relief available for the pension

contributions depend on whether the individual is:

employed, or

self-employed, or

not working.

There are two types of pension scheme that may be available to an employee:

an employer’s occupational pension scheme, or

if the employee opts out of the employer’s scheme, he can set up his own

personal pension plan (PPP).

An occupational pension scheme is a scheme established by an employer solely for

the benefit of the employees of that business. Therefore an occupational pension

Chapter 11: Taxation relief for pension contributions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 209

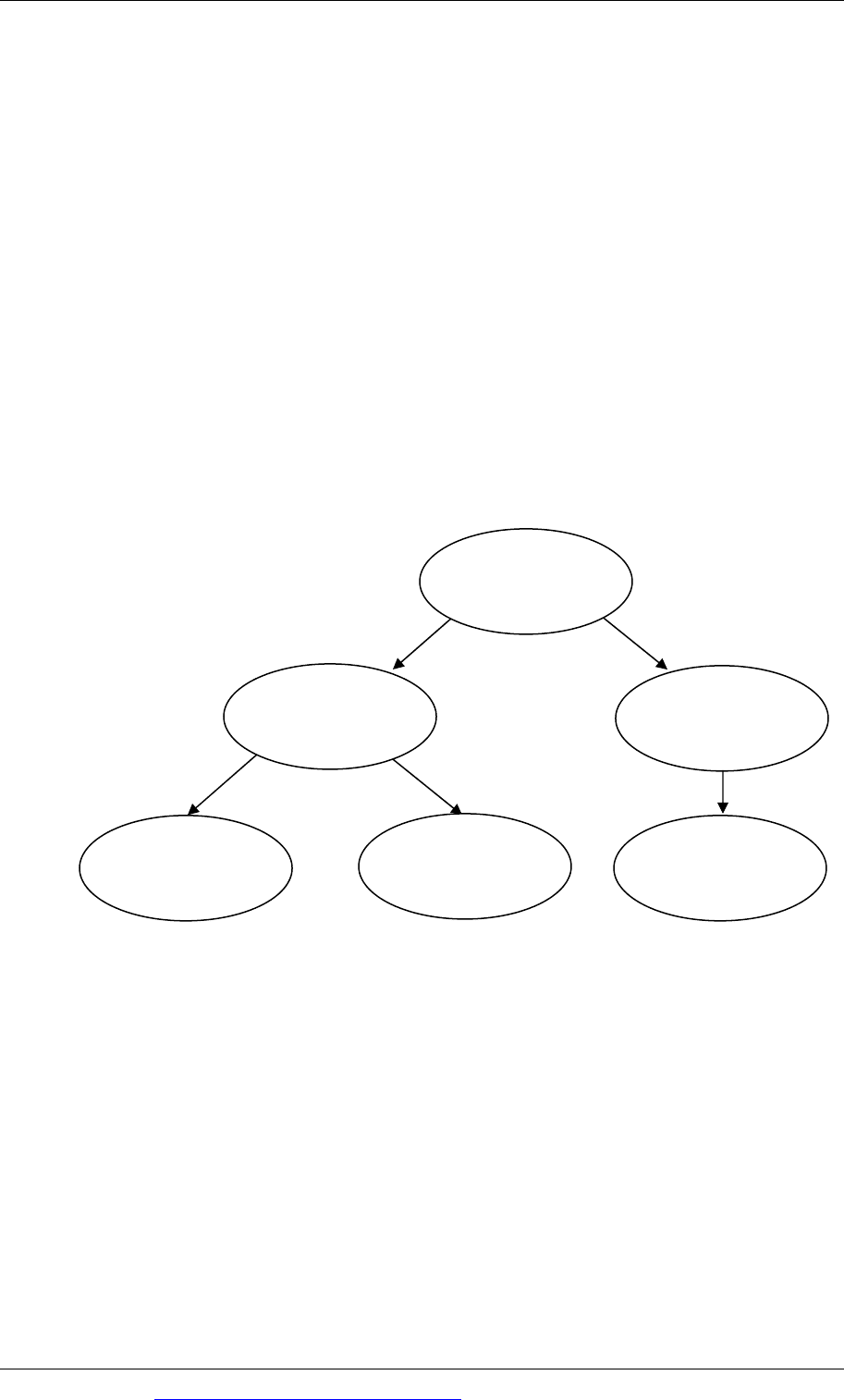

Individual’s status

Self-employed,

employees not in an

occupational scheme

or those not

working

Occupational

scheme relief

Employee in an

occupational

pension scheme

Personal

pension plan (PPP)

relief

Personal

pension plan (PPP)

relief

scheme only relates to that employment. If an individual leaves that employment he

will need to set up new pension arrangements.

A PPP (also sometimes referred to as a stakeholder pension) is a separate fund,

usually established by way of a contract between the individual and an approved

pension provider (a bank or life assurance company).

PPPs do not relate to a particular job, trade or profession. They are personal to that

individual taxpayer and are set up for the duration of his life, regardless of his

employment status.

Unlike an employed individual who has a choice of an occupational pension scheme

and/or a PPP, a self-employed individual and those who are not working can only

set up a PPP.

1.2 Overview of the options available for pension contributions

The options available for pension contributions depend on the status of the

individual as follows:

Paper F6 (UK): Taxation FA2009

210 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

The maximum relief available

The amount of relief available

Net relevant earnings of an individual who is not working

Net relevant earnings of working individuals

Contributions in excess of the annual allowance

The lifetime allowance

2 The maximum relief available

2.1 The amount of relief available

Any amount can be contributed into a pension scheme. However, tax relief is only

available on contributions up to the higher of:

(1) £3,600, and

(2) 100% of net relevant earnings.

2.2 Net relevant earnings of an individual who is not working

If an individual is not working, he will have no net relevant earnings (NRE) and

therefore his maximum (gross) contribution is £3,600. This figure is given in the tax

rates and allowances in the examination.

As contributions are made into a pension scheme net of 20% tax, the maximum

amount of contributions payable into a scheme by a non-working individual is

£2,880 (= £3,600 × 80%).

2.3 Net relevant earnings of working individuals

Where an individual is working, the NRE depends on whether the individual is

employed or self-employed, and is calculated as follows:

Employed individual Self-employed individual

£

£

Employment income X

Trading income X

(including benefits)

= NRE for employee

Minus

Trading losses brought

forward

(X)

NRE for self-employed X

Chapter 11: Taxation relief for pension contributions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 211

2.4 Contributions in excess of the annual allowance

Although an individual can receive tax relief on contributions of up to 100% of his

earnings, there is effectively an upper limit of £245,000 on the amount of

contribution which can qualify for relief. The figure of £245,000 is known as the

annual allowance. Contributions in excess of the annual allowance are taxed at the

rate of 40%. This tax is paid under the self-assessment system. The purpose of this

charge is to cancel out the tax relief that will have been given in respect of the

contribution. Therefore there is no charge where contributions have not qualified for

relief.

Note that all contributions to an individual’s pension scheme(s) during a particular

tax year count towards this annual allowance. This means that you need to take

account of any contributions paid by the individual’s employer in deciding whether

the annual limit has been exceeded.

2.5 The lifetime allowance

The total funds that can be built up within a person’s pension schemes is £1,750,000.

This figure is known as the lifetime allowance. Where it is exceeded, there will be an

additional tax charge when the funds are eventually withdrawn.

Paper F6 (UK): Taxation FA2009

212 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Relief for contributions to occupational pension schemes

Relief for regular contributions into an occupational pension scheme

The treatment of additional voluntary contributions (AVCs)

3 Relief for contibutions to occupational pension

schemes

3.1 Relief for regular contributions into an occupational pension scheme

The tax relief obtained for contributions made into an occupational pension scheme

is as follows:

3.2 The treatment of additional voluntary contributions (AVCs)

The rules of the occupational pension scheme itself usually require an employee to

contribute a certain amount of their salary (e.g. 6% or 7%) to the scheme.

Contributions above those required under the rules of the scheme itself are referred

to as additional voluntary contributions (AVCs). AVCs can be made into the

occupational scheme via the payroll, in which case relief is obtained automatically

under the PAYE system. Alternatively a free-standing AVC scheme can be set up by

the individual. In this case tax relief for the additional contributions will be obtained

in the same way as for PPP relief. (This is explained later.)

Allowable deduction in the

adjustment of profit computation

An exempt benefit for the

employee

Employee in an

occupational pension

scheme

Employee

contributions

Employer

contributions

Amount paid into scheme in the tax

year

= allowable deduction against

employment income

Income tax relief at both the basic

rate (20%) and the higher rate

(40%) is automatically given through

the payroll under the PAYE scheme

Chapter 11: Taxation relief for pension contributions

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 213

Relief for personal pension plan contributions

The scope of personal pension plan relief

The relief for contributions into a PPP

4 Relief for personal pension plan contributions

4.1 The scope of personal pension plan relief

Personal pension plan tax relief (PPP tax relief) is available to:

the self-employed

employees who choose not to join their employer’s occupational pension scheme

individuals who are not working.

Relief is available for contributions made by the individual, the employer and third

parties, as long as the overall contribution limit is not exceeded.

4.2 The relief for contributions into a PPP

Basic rate taxpayers

Basic rate relief (20%) is automatically given at source as pension contributions are

paid net of 20% tax. Therefore pension contributions are ignored in the individual’s

income tax computation. (For example, if an individual pays £200 each month gross

into his pension scheme, he will actually pay only £160. This is the £200 less tax

relief at 20%.)

Higher rate taxpayers

The additional 20% relief is obtained by extending the basic rate band in the same

way as for gift aid contributions. The basic rate band is extended by adding to the

£37,400 threshold, the gross amount of the pension contributions.

Example

Nicholas is aged 49 and is a self-employed electrician who has been trading for

many years. His trading profits have been steadily increasing and his results for the

last two years are as follows:

Yearended

Adjustedprofitafter

capitalallowances

£

31January2009 53,400

31January2010 71,470

Paper F6 (UK): Taxation FA2009

214 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Nicholas has non-trading income of £6,000 each year. He has no trading losses

brought forward.

Required

(a) Calculate the amount of pension contribution Nicholas could make to his PPP

in 2009/10.

(b) Assuming Nicholas decides to make a gross contribution of £20,000, state how

the relief will be obtained.

Answer

(a) Calculate NRE for 2009/10

£

Tradingincome(CYB=y/e31January2010) 71,470

Minus

Tradinglosses (Nil)

NRE 71,470

Maximumrelief=Higherof: £ £

(1) £3,600 3,600

(2) Netrelevantearnings 71,470 71,470

(b) State how the relief will be obtained

Pension contributions are paid net of 20% tax. Therefore to make a gross

contribution of £20,000, Nicholas must pay £16,000 (= £20,000 × 80%) into the

scheme in 2009/10.

Nicholas is clearly a higher rate taxpayer as shown below:

£

Tradingincome 71,470

Non‐tradingincome 6,000

–

––––––––––––––––

–

––––––––––––––

Totalincome 77,470

MinusPA (6,475)

–

–––––––––––––––––––––––––––––––

Taxableincome 70,995

–

–––––––––––––––––––––––––––––––

Relief at 20% is given at source for his payments into the pension scheme.

Higher rate relief is obtained by extending his basic rate band to £57,400, i.e.

by adding the gross pension contribution of £20,000 to the basic rate band

limit of £37,400.