ACCA F6 FA09 Study Text 2010

Подождите немного. Документ загружается.

Chapter 13: Capital gains tax

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 235

Transfers between spouses

Transfers between spouses

3 Transfers between spouses

3.1 Transfers between spouses

The computation for a disposal to an individual’s spouse (or civil partner) is fixed so

that at the time of the transfer no gain arises on the disposal and there is no

allowable loss.

Inter-spouse transfers are therefore referred to as ‘nil gain/nil loss’ transfers.

Disposal consideration = Allowable Cost (AC)

On the subsequent disposal of the asset by the spouse, a normal computation is

required using a deemed acquisition cost equal to the deemed disposal

consideration at the time of the inter-spouse transfer.

Example

Michelle bought some land in September 1994 for £30,000 as an investment. She

gave the land to Andy, her husband, in December 2006 when it was worth £78,000.

In January 2010 Andy sold the land to an unconnected person for £125,000.

Required

Calculate the chargeable gains arising on the transfer to Andy and on the sale by

Andy.

Answer

£

Deemed disposal consideration (Cost) 30,000

Less: Cost of asset (September 1994) (30,000)

–

–––––

–

––––––––––––––––––––––––––––

Gain / (loss) Nil

–

–––––

–

––––––––––––––––––––––––––––

SubsequentdisposalbyAndyinJanuary2010

£

Sale proceeds 125,000

Less: Deemed acquisition cost (30,000)

–

–––––

–

––––––––––––––––––––––––––––

Gain 95,000

–

–––––

–

––––––––––––––––––––––––––––

Paper F6 (UK): Taxation FA2009

236 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Part disposals

The problem with part disposals

The part disposal formula

4 Part disposals

4.1 The problem with part disposals

Where only part of an asset is disposed of, it is necessary to allocate the allowable

cost of the whole asset between:

the part of the asset that is being disposed of, and

the part of the asset that is being retained.

It is only the allowable costs incurred prior to the sale that need to be allocated.

Costs relating wholly to the part that is sold (for example, incidental selling

expenses) are allowable in full on the part disposal.

4.2 The part disposal formula

When calculating the allowable cost:

Any allowable costs that relate to the whole asset are allocated between the two

parts on the basis of market values at the date of the part disposal as follows:

retainedpartofMV+ofdisposedpartofMV

ofdisposedpartofMV

AC=disposalpart‐reAC ×

of)disposedpart‐reACless(AC=retainedpart‐reAC

The market value of the part disposed of is usually the gross sale proceeds

received. The market value of the part retained will be given in the examination

question and is usually referred to as the market value of the remainder.

Any allowable costs that relate only to the part disposed of can be deducted in

full in the part disposal computation.

Any allowable costs that relate only to the part retained can be deducted in full

in the subsequent disposal computation.

Example

Penelope acquired a non-business asset in July 1985 for £29,600. Incidental costs of

acquisition totalled £530. The asset was enhanced in July 1999 at a cost of £14,200.

Chapter 13: Capital gains tax

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 237

On 11 September 2009 Penelope sold a one-third interest in the asset to an

unconnected person for £48,000. Incidental selling expenses amounted to £900. At

that time the value of the remaining two-thirds was £105,000.

On 31 March 2010 Penelope sold the remaining two-thirds interest for £147,500.

Incidental selling expenses amounted to £2,300.

Required

Calculate the chargeable gains arising in 2009/10.

Answer

Part disposal Sept 2009

£

Gross sale proceeds 48,000

Less Incidental selling expenses (900)

–––––––––––––––––––––––––––––––––

Net sale proceeds 47,100

Less

Allowable cost

Original cost (July 1985):

105,000+48,000

48,000

£530)+(£29,600 ×

(9,453)

Enhancement expenditure (July 1999):

105,000+48,000

48,000

(£14,200)×

(4,455)

–––––––––––––––––––––––––––––––––

Gain 33,192

–––––––––––––––––––––––––––––––––

Subsequent disposal Mar 2010

£

Gross sale proceeds 147,500

Less Incidental selling expenses (2,300)

–––––––––––––––––––––––––––––––––

Net sale proceeds 145,200

Less

Allowable cost

Original cost (July 1985):

((£29,600 + £530) – £9,453) (20,677)

Enhancement expenditure (July 1999):

(£14,200 – £4,455) (9,745)

–––––––––––––––––––––––––––––––––––––

Gain 114,778

–––––––––––––––––––––––––––––––––––––

Paper F6 (UK): Taxation FA2009

238 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Wasting assets and chattels

The definition of wasting assets and chattels

A summary of the consequences of the disposal of chattels

Gains on the disposal of chattels

Losses on the disposal of chattels

The disposal of plant and machinery

A summary of the consequences of the disposal of wasting assets

5 Wasting assets and chattels

5.1 The definition of wasting assets and chattels

A wasting asset is an asset with an expected useful life of 50 years or less.

A chattel is tangible moveable property (for example, most things you would put

into a removal van if you were to move house).

A wasting chattel is therefore tangible moveable property with an expected life of

50 years or less. Examples include a caravan, boat, dishwasher, cooker, greyhound,

horse.

A non-wasting chattel is tangible moveable property with an expected life of more

than 50 years. Examples include antiques, jewellery, paintings.

5.2 A summary of the consequences of the disposal of chattels

Chattels are treated as follows:

Wasting chattels are exempt from capital gains tax.

Non-wasting chattels are chargeable but the treatment depends on the amount

of gross disposal consideration (i.e. sale proceeds or market value) and the

allowable cost.

Gross Disposal Consideration

£6,000 or less

More than £6,000

Cost

£6,000 or less

Exempt

5/3 rule applies

More than £6,000

Deemed disposal for

£6,000

Normal gain

computation

Chapter 13: Capital gains tax

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 239

5.3 Gains on the disposal of chattels

Where a chattel is sold for more than £6,000 but the item cost £6,000 or less, the gain

is restricted to the lower of:

(i) the gain calculated applying the normal rules, and

(ii) (Gross sale proceeds – £6,000) × 5/3

Example

Teresa purchased an antique for £2,200 on 23 March 1987. She sold it for £7,600 on

16 October 2009.

Required

Calculate the chargeable gain arising in 2009/10.

Answer

Gain calculated applying the normal rules:

£

Sale proceeds 7,600

Less Acquisition cost (2,200)

––––––––––––––––––––––––––––––

Gain 5,400

––––––––––––––––––––––––––––––

Marginal gain calculation:

(£7,600 – £6,000) × 5/3 2,667

––––––––––––––––––––––––––––––

Decision:

The lower gain of £2,667 is taken.

5.4 Losses on the disposal of chattels

Where a chattel is sold for less than £6,000 but the item cost more than £6,000, the

actual sale proceeds received are ignored and the allowable loss is calculated

assuming the gross sale proceeds are £6,000.

Example

John purchased an antique for £7,200 on 23 March 1987. He sold it for £4,600 on 16

October 2009 and incurred £540 of incidental selling expenses.

Required

Calculate the allowable loss arising in 2009/10.

Paper F6 (UK): Taxation FA2009

240 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Answer

£

Deemed gross sale proceeds

6,000

Less Incidental selling expenses (540)

––––––––––––––––––––––––––––

Net sale proceeds 5,460

Less Allowable cost (7,200)

––––––––––––––––––––––––––––

Allowable loss (1,740)

––––––––––––––––––––––––––––

5.5 The disposal of plant and machinery

Items of plant and machinery are always deemed to have a life of less than 50 years

and are therefore wasting assets.

As most items of plant and machinery are tangible and moveable, they are classed

as wasting chattels and, following the rules above, would therefore be exempt from

capital gains tax.

However, not all plant and machinery is exempt. Special rules apply as follows:

If the plant and machinery is used in a trade and capital allowances can be

claimed:

− they are chargeable assets and the 5/3 rule applies if sold at a gain

− no allowable loss arises if sold at a loss.

If there are no capital allowances available on the plant and machinery:

− they are exempt if they are chattels (i.e. tangible and moveable), and

− the rules for wasting assets are followed if they are not chattels.

5.6 A summary of the consequences of the disposal of wasting assets

Wasting assets which are chattels (i.e. tangible, moveable property) are exempt

assets as explained above.

Wasting assets which are not chattels are chargeable assets, but special rules apply

in the calculation of the gain.

As wasting assets usually decline in value over time, they are often referred to as

depreciating assets. Wasting assets are deemed to depreciate on a straight line

basis.

When calculating the allowable cost, the net cost of the asset must be depreciated on

a straight line basis as follows:

(months)assettheoflifeExpected

(months)sellerthebyownershipo

f

Length

costNet

×

The net cost of the asset is the original cost of the asset less any anticipated scrap

value at the end of the life of the asset.

Chapter 13: Capital gains tax

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 241

Insurance and compensation

The receipt of a capital sum due to the ownership of an asset

Assets totally destroyed or lost

Damaged assets

6 Insurance and compensation

6.1 The receipt of a capital sum due to the ownership of an asset

The receipt of a capital sum due to the ownership of an asset is a chargeable

disposal for capital gains tax purposes. The receipt of compensation or insurance on

making a claim due to the loss, destruction or damage to a capital asset is therefore

a chargeable event.

The treatment of the receipt depends on whether the asset is:

totally destroyed/lost – i.e. a disposal of the asset, or

damaged but not totally destroyed – i.e. a part disposal of the asset.

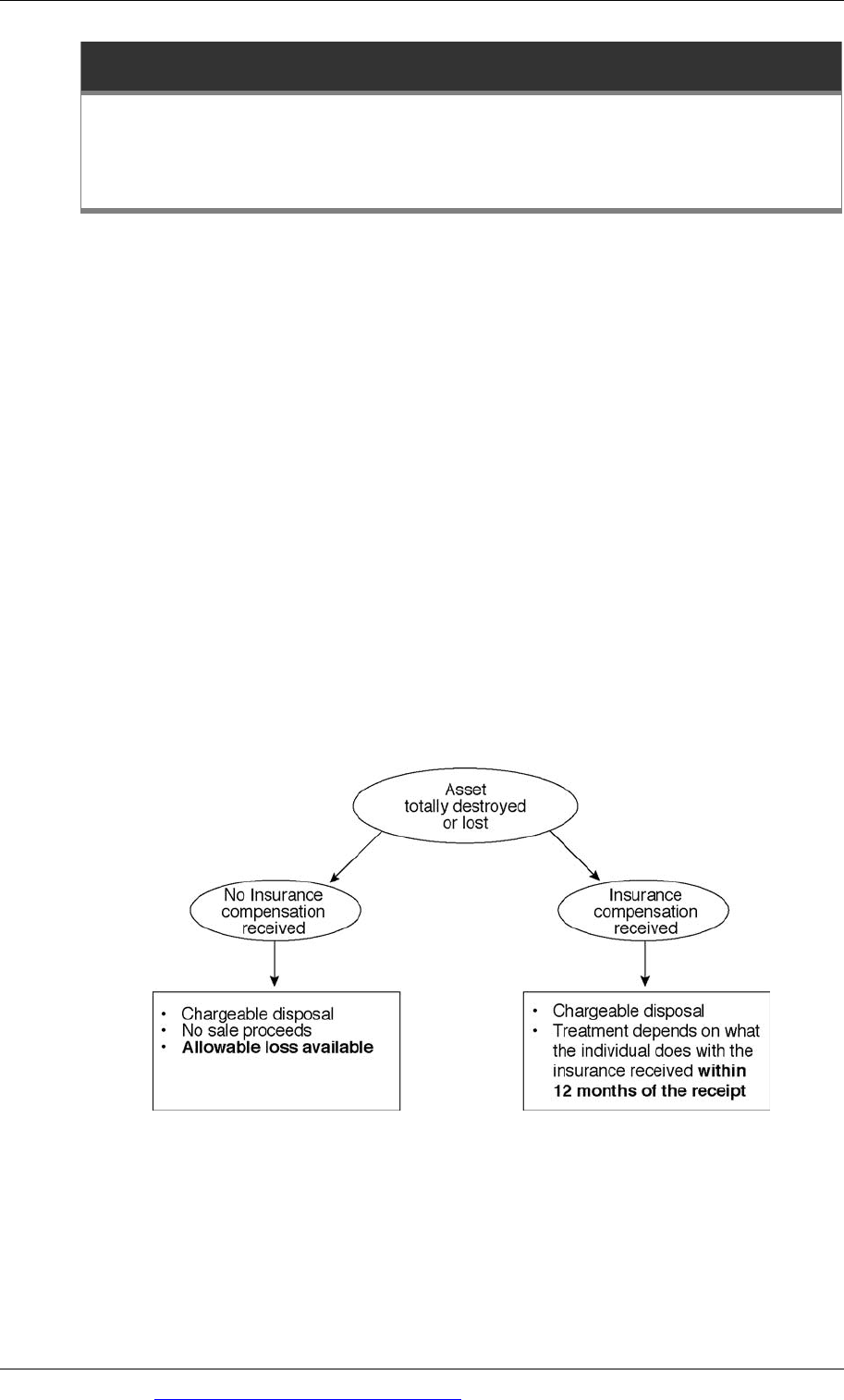

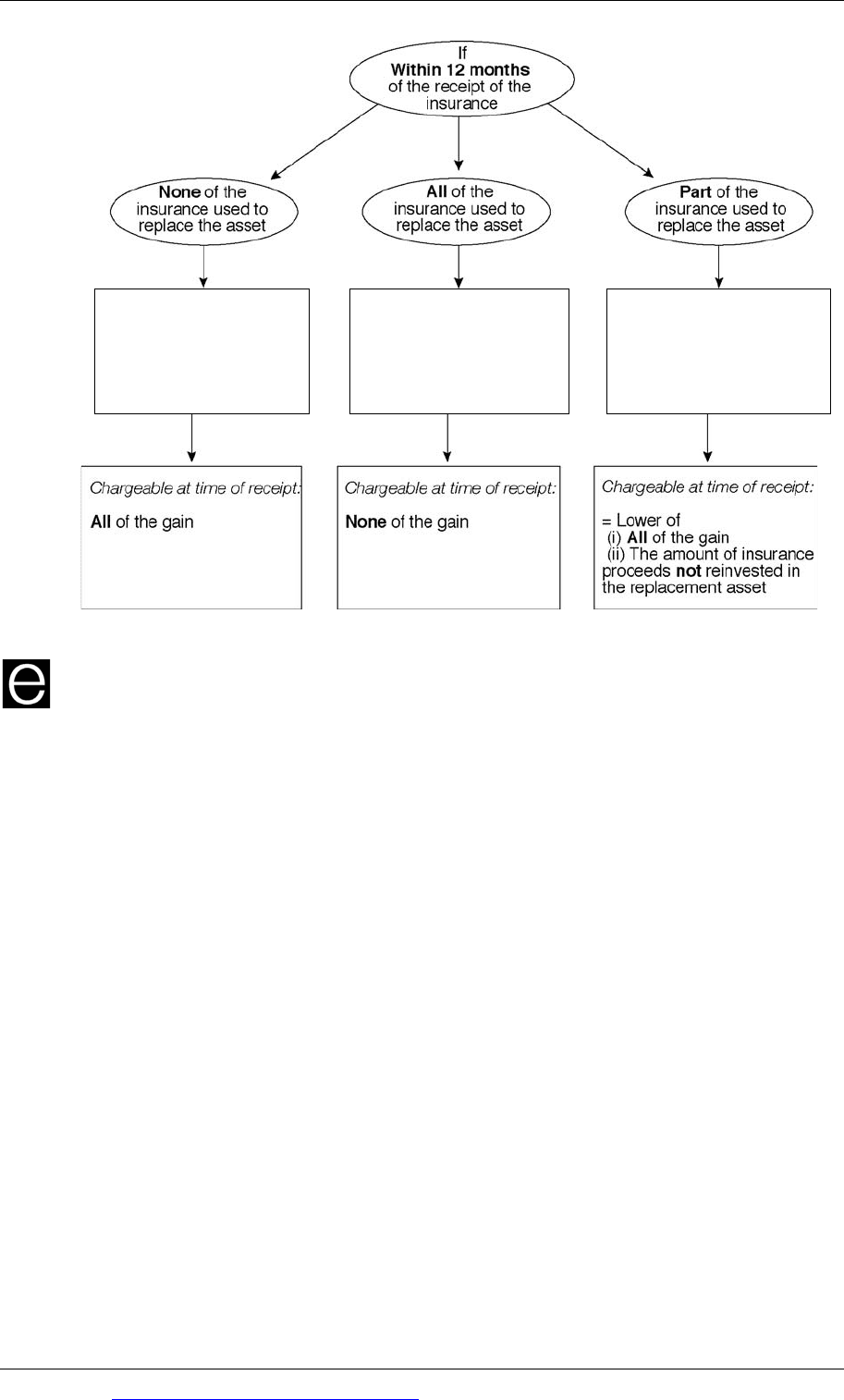

6.2 Assets totally destroyed or lost

Where an asset is totally destroyed or lost, the treatment for capital gains tax can be

summarised as follows:

Paper F6 (UK): Taxation FA2009

242 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

• Calculate gain as

normal using

insurance received as

gross consideration

•

Calculate gain as

normal

•

Claim to defer all of

the gain against the

cost of replacement

asset

•

Calculate gain as

normal

•

Claim to defer some of

the gain against the

cost of the replacement

asset

Example

Diane bought a painting for £280,000 in August 1999. In November 2009 the

painting was destroyed in a fire. The insurance company settled a claim for £600,000

in January 2010. In May 2010 Diane replaced the painting.

Required

Calculate the chargeable gain arising in 2009/10 and the base cost of the

replacement painting assuming the replacement painting cost:

(a) £650,000

(b) £480,000

Chapter 13: Capital gains tax

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 243

Answer

£

Insurance proceeds (January 2010)

600,000

Less Allowable cost (August 1999) (280,000)

–––––––––––––––––––––––––––––––––

–

–

Gain 320,000

–––––––––––––––––––––––––––––––––

–

–

(a) If replacement cost £650,000 (b) If replacement cost £480,000

Gain in 2009/10 £Nil Gain in 2009/10

–

–––––

–

––––––––––––––––––––––––––

–

–

= Lower of

all of the gain

insurance not reinvested

£320,000

£120,000

As all of the insurance proceeds are

reinvested in a replacement painting, the

whole gain can be deferred until the later

disposal of the replacement painting

Note:

The chargeable gain is assessed in

2009/10 (the tax year of the receipt of

the insurance, not the date of the

destruction of the asset)

Base cost of replacement painting:

£

£

Cost 650,000 Cost 480,000

Less Deferred gain (320,000) Less Deferred gain

(£320,000 – £120,000)

(200,000)

–

–––––

–

––––––––––––––––––––––––––

–

–

–––––––––––––––––––––––––––––––––

–

–

Base cost 330,000 Base cost 280,000

–

–––––

–

––––––––––––––––––––––––––

–

–

–––––––––––––––––––––––––––––––––

–

–

Paper F6 (UK): Taxation FA2009

244 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

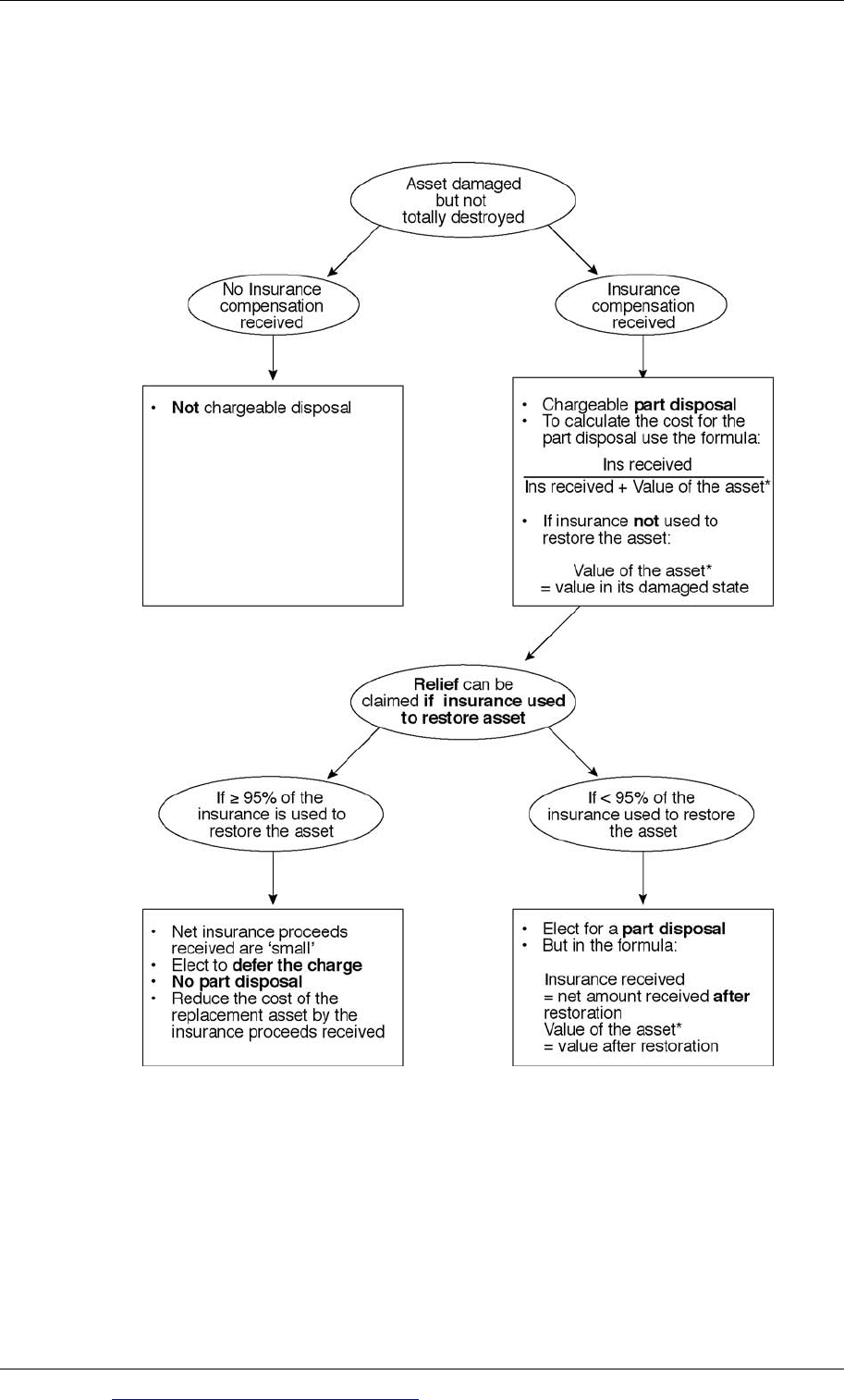

6.3 Damaged assets

Where an asset is damaged but not totally destroyed, the treatment for capital gains

tax can be summarised as follows:

Note

The net insurance proceeds are also deemed to be small if they are < £3,000.