Blank L., Tarquin A. Engineering Economy (McGraw-Hill Series in Industrial Engineering and Management)

Подождите немного. Документ загружается.

SECTION 4.2

Effective Annual Interest Rates

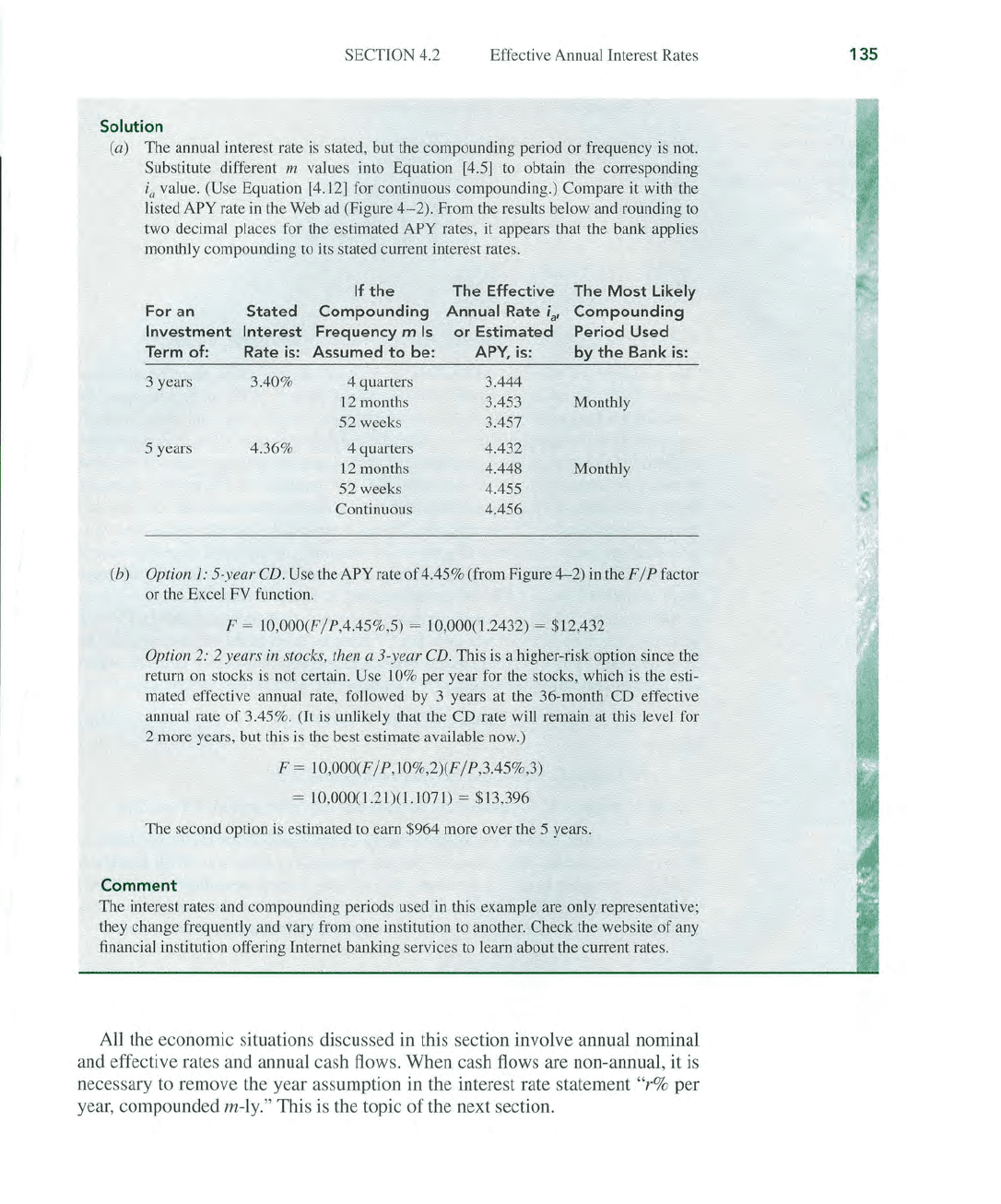

Solution

(a) The annual interest rate

is

stated, but the compounding period or frequency is not.

Substitute different

m values into Equation [4.5] to obtain the corresponding

i"

value. (Use Equation [4.12] for continuous compounding.) Compare

it

with the

listed

APY rate

in

the Web

ad

(Figure

4-2).

From the results below and rounding to

two decimal places for the estimated

APY rates, it appears that the bank applies

monthly compounding

to

its stated current interest rates.

If

the

The Effective

The

Most

Likely

For an

Stated

Compounding

Annual Rate i

a

,

Compounding

Investm

en

t

In

terest

Frequency m

Is

or

Estimated

Period Used

Term of: Rate

is:

Assumed

to

be:

APY,

is:

by

the

Bank

is:

3 years 3.40% 4 quarters 3.444

12 months 3.453 Monthly

52 weeks 3.457

5 years 4.36% 4 quarters 4.432

12

months 4.448 Monthly

52 weeks 4.455

Continuous 4.456

(b)

Option J: 5-year

CD.

Use the APY rate

of

4.45% (from Figure

4-2)

in

the F / P factor

or the Excel FV function.

F = 10,000(F / P,4.45%,5) = 10,000(1.2432) = $12,432

Option 2: 2 years in stocks, then a 3-year

CD.

This

is

a higher-risk option since the

return

on

stocks

is

not certain. Use 10% per year for the stocks, which

is

the esti-

mated effective annual rate, followed

by

3 years at the 36-month CD effective

annual rate

of

3.45%.

(It

is unlikely that the CD rate will remain at this level for

2 more years, but this

is

the best estimate available now.)

F = 1

O,OOO(F

/

P,

1 0%,2)(F / P,3.45%,3)

= 10,000(1.21)(1.1071) = $13,396

The second option is estimated

to

earn $964 more over the 5 years.

Comment

The interest rates and compounding periods used in this example are only representative;

they change frequently and vary from one institution to another. Check the website

of

any

financial institution offering Internet banking services

to

learn about the current rates.

All the economic situations discussed in this section involve annual nominal

and effective rates and annual cash flows. When cash flows are non-annual, it is

necessary

to

remove the year assumption in the interest rate statement "r% per

year, compounded

m-ly." This is the topic

of

the next section.

135

136

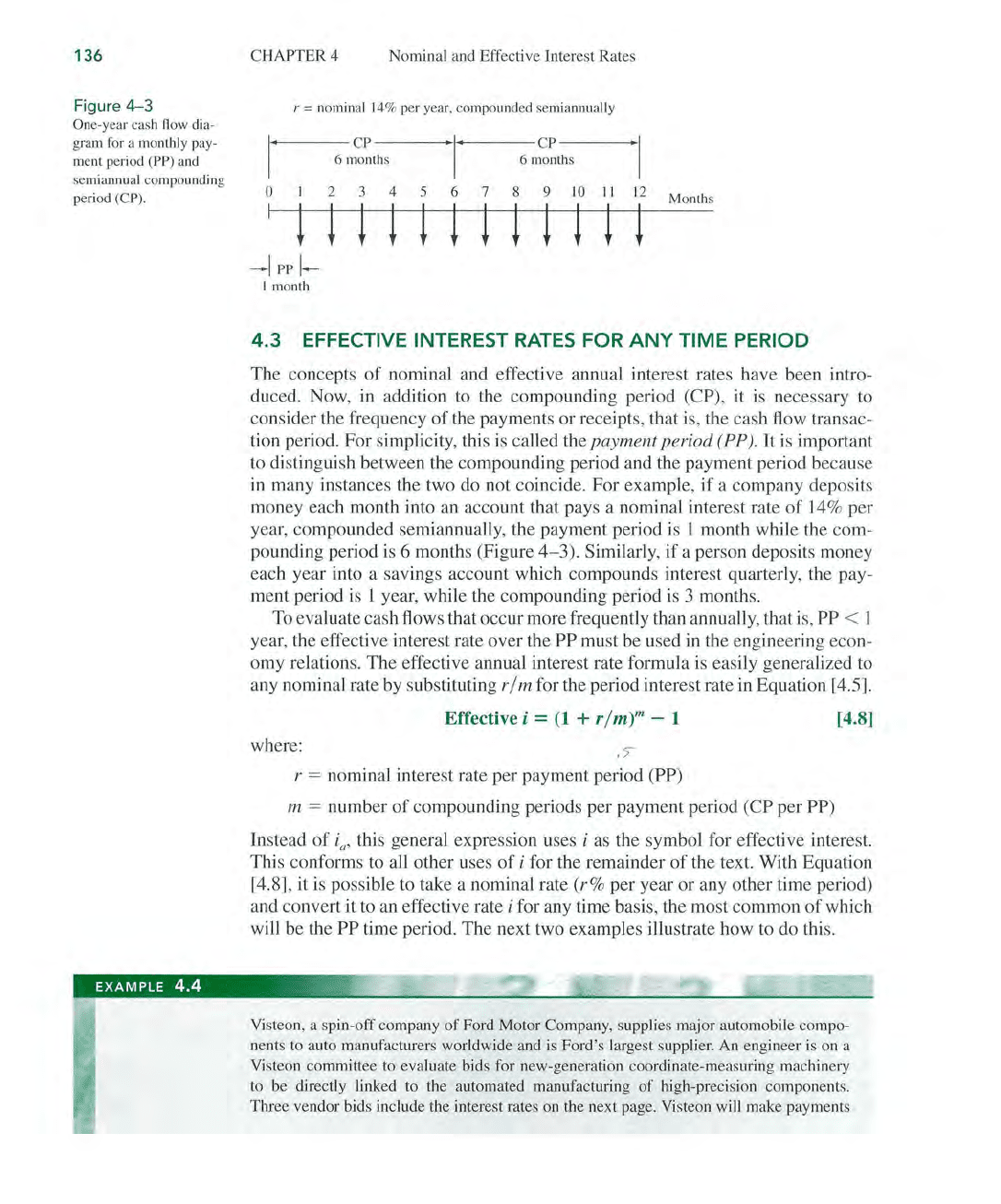

Figure

4-3

One-year cash

flow

dia-

gram for a monthly pay-

ment period (PP) and

semiannual compounding

period

(C

P).

CHAPTER 4 Nominal and Effective Interest Rates

r = nominal 14% per year, compounded semiannually

6

m~~t-h-

S

---'Iom~~ths

'I

2 3 4 5 6 7 8 9 to

11

12

o

I

iii

t t t i

itt

t i

~I

PP

I-

I month

Months

4.3

EFFECTIVE INTEREST

RATES

FOR

ANY

TIME

PERIOD

The concepts

of

nominal and effective annual interest rates have been intro-

duced. Now,

in

addition

to

the compounding period (CP), it

is

necessary to

consider the frequency

of

the payments or receipts, that is, the cash flow transac-

tion period. For simplicity, this is called the

payment

period

(PP). It is important

to

distinguish between the compounding period and the payment period because

in

many instances the two do not coincide. For example, if a company deposits

money each month into

an

account that pays a nominal interest rate

of

14

% per

year, compounded semiannually, the payment period is 1 month while the com-

pounding period is 6 months (Figure

4- 3). Similarly,

if

a person deposits money

each year into a savings account which compounds interest quarterly, the pay-

ment period is 1 year, while the compounding period is 3 months.

To

evaluate cash flows that occur more frequently than annually, that is, PP < ]

year, the effective interest rate over the PP must be used in the engineering econ-

omy relations. The effective annual interest rate formula is easily generalized to

any nominal rate

by

substituting r / m for the period interest rate in Equation [4.5].

Effective

i =

(1

+ r/

m)m

- 1

[4.8]

where:

.7

r = nominal interest rate per payment period (PP)

m = number

of

compounding periods per payment period (CP per PP)

Instead

of

i(f,

this general expression uses i

as

the symbol for effective interest.

This conforms to all other uses

of

i for the remainder

of

the text. With Equation

[4.8], it is possible to take a nominal rate

(r%

per year or any other time period)

and convert it

to

an effective rate i for any time basis, the most common

of

which

will be the

PP time period. The next two examples illustrate how

to

do this.

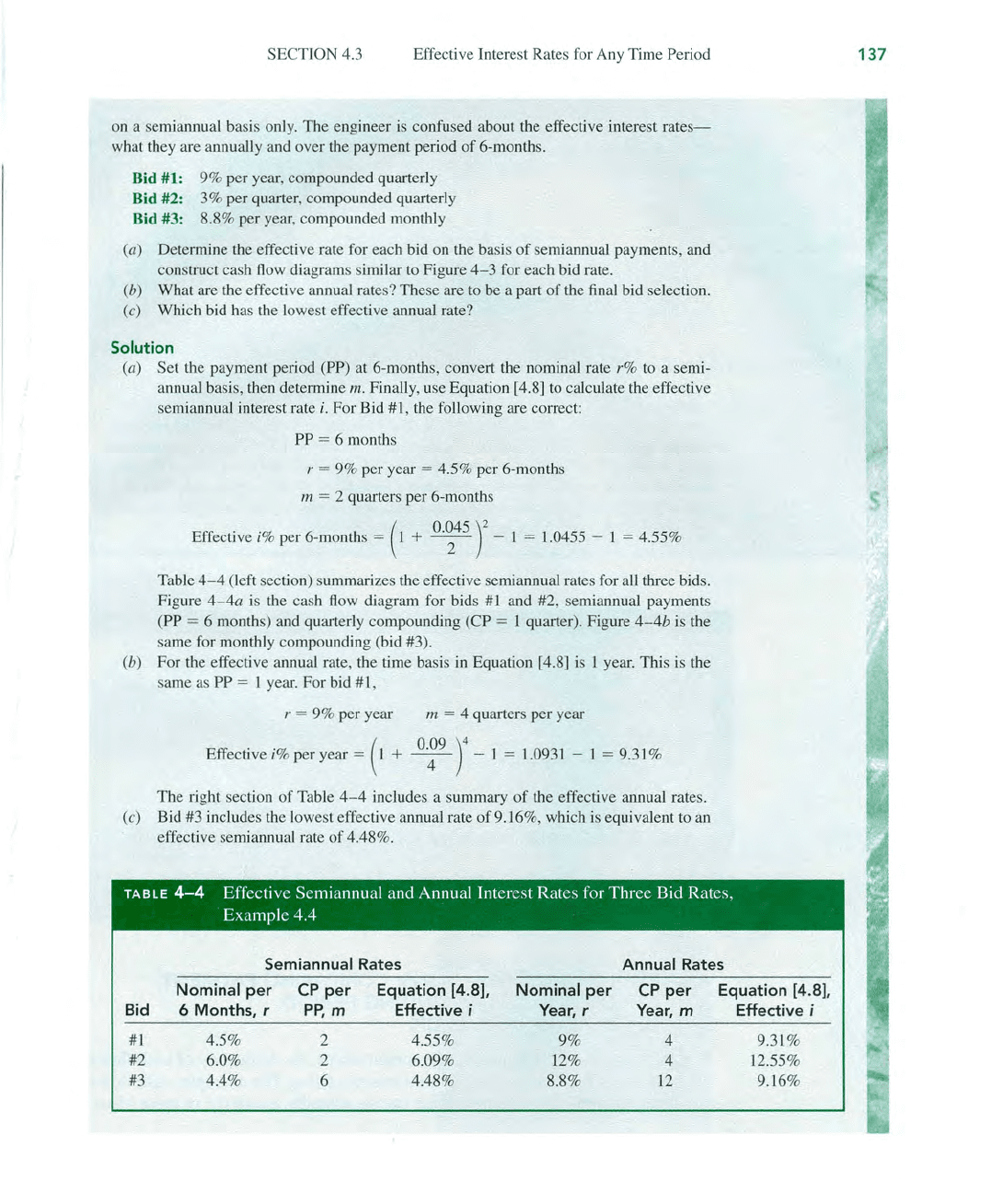

EXAMPLE

4.4

~,'~'

Visteon, a spin-off company

of

Ford Motor Company, supplies major automobile compo-

nents

to

auto manufacturers worldwide and is Ford's largest supplier.

An

engineer

is

on a

Visteon committee to evaluate bids for new-generation coordinate-measuring machinery

to

be directly linked to the automated manufacturing

of

high-precision components.

TIu-ee

vendor bids include the interest rates

011

the next page. Visteon will make payments

SECTION 4.3 Effective Interest Rates for Any Time Period

on a

semiaJU1Ual

basis only. The eng

in

eer is confused about the effective interest rat

es-

what they are annually and over the payment period

of

6-months.

Bid #1: 9% per year, compo

un

ded quarterly

Bid

#2: 3% per quarter, compounded quarterly

Bid #3: 8.8% per year, compounded monthly

(a) Determ

in

e the effective rate for each bid

on

tbe basis

of

semiannual payme

nt

s,

an

d

construct cash

flow

diagrams similar

to

Figure

4-3

for each bid rate.

(b) What are the effective annual rates? These are

to

be a part

of

the

final

bid selec

ti

on.

(c) W

hi

ch bid h

as

the lowest effective annual rate?

Solution

(a) Set the payment peri

od

(PP) at 6-mo

nth

s, convert the nominal rate r%

to

a semi-

annual basis, then determine

m. Fina

ll

y,

use Equation [4.8]

to

calculate

the

effective

semia

nn

ua

l

in

terest rate i. For Bid #1, t

he

fo

ll

owing are correct:

PP

= 6

mo

nths

r = 9% per year = 4.5% per 6-months

m = 2 quarters per 6-months

Effective i% per 6-months

=

(1

+

0.~45

r -1 = 1.0455 - 1 = 4.55%

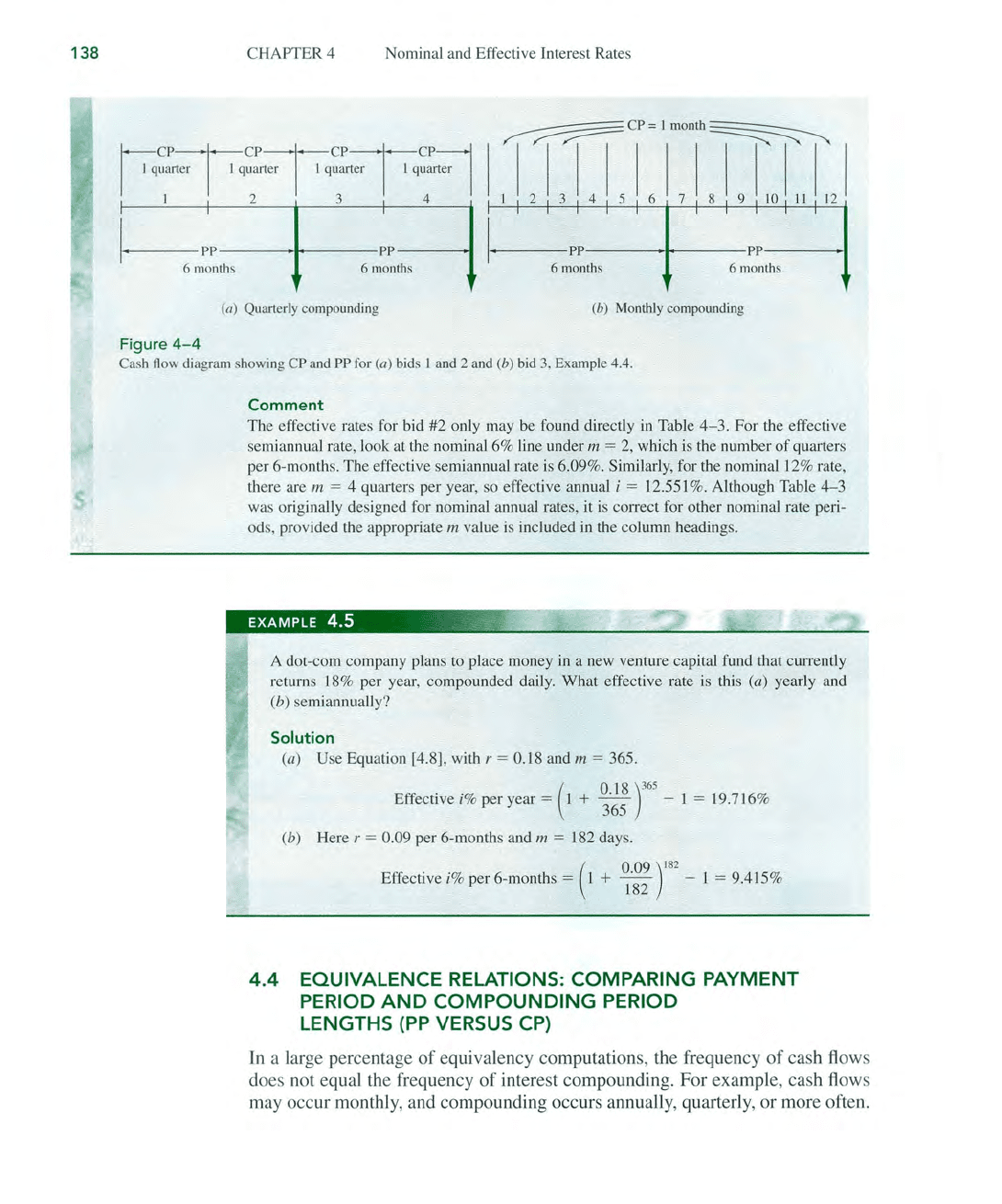

Table 4- 4 (left section) summarizes the effective semiannual rates for all three bids.

Figure

4- 4a

is

the cash

flow

diagram for bids

#1

and #2, semiannual payments

(PP

= 6 months) and quarterly compounding (CP = I quarter). Figure

4-4b

is

the

same for monthly compounding (bid #3).

(b) For the effective annual rate, the time basis in Equation

[4

.

8]

is

1 year. T

hi

s

is

the

same

as

PP = 1 year. For bid

#1

,

r = 9% per year

m = 4 quarters per year

Effective i% per year

=

(1

+

0~9

r -1 = 1.0931 - 1 = 9.31 %

The right secti

on

of

Table

4-4

includes a summary

of

the effective annual rates.

(c) Bid #3 includes the lowest effecti

ve

annual rate

of

9.16%, which

is

equivalent

to

an

effecti

ve

semiannual rate

of

4.48%.

TABLE

4-4

Effec

ti

ve Se

mi

annual and Annual Interest Rates

fo

r Three Bid Rates,

Example 4.4

Semiannual Rates

Annual Rates

Nominal

per

CP

per

Equation

[4.8], Nominal

per

CP

per

Equation

[4

.

8]

,

Bid 6

Months

, r

PP,

m

Effective;

Year, r

Year, m

Effecti

ve

;

#1

4.5% 2 4.55%

9% 4 9.31%

#2

6.0% 2 6.09% 12%

4

12

.

55

%

#3 4.4%

6

4.48%

8.8% 12 9.16%

137

138

CHAPTER 4 Nominal and Effective Interest Rates

~

C

P-~

CP

~CP~CP=1

I I quarter I 1 quarter I I quarter I 1 quarter I

I

mTTf"ihTTril

I 2 3 4 2 3 4 5 6 7 8 9

LO

II 12

1-,----

pp----

.

f+-

----pp---

--+J

6 months 6 months

I

I

-,----PP---~~

~

--

--p

p---~~

,

6 months 6 months

(a) Quarte

rl

y compounding (b) Monthly compounding

Figure

4-4

Cash

fl

ow

diagram

s

howin

g

CP

and

PP

for

(a) bids I

and

2 and (b) bid

3,

Example

4.4.

Comment

The effective rates for bid #2 only may be found direct

ly

in

Table 4

-3

. For the effective

semia

nnu

al rate, look at the nominal

60/0

line under m = 2, which

is

the number

of

quarters

per 6-months. The effective semiannual rate

is

6.09

0/0

. Similarly, for

th

e nominal

120/0

rate,

there are m

= 4 quarters per year, so effective annual i = 12.551

0/0

. Although Table

4-

3

was orig

in

a

ll

y designed for nominal annual rates,

it

is correct for other nominal rate peri-

ods, provided the appropriate

m va

lu

e is included

in

the column headings.

A dot-com company

pl

a

ns

to place money

in

a new venture capital fund that cun·ently

returns

IS0/0

per year, compounded daily. What effective rate

is

th

is (a) yearly and

(b) semiannually?

Solution

(a) Use Equation [4.8], with r = O.IS and m = 365.

Effective

i

O/O

per year = (1 +

~.~;

t

5

- 1 = 19.716

0/0

(b) Here r = 0.09 per 6-months a

nd

m =

IS

2 days.

Effective

i

O/O

per 6-months = (1 +

~.~~

)

182

- 1 =

9.41

5

0/0

4.4

EQUIVALENCE RELATIONS: COMPARING PAYMENT

PERIOD

AND

COMPOUNDING

PERIOD

LENGTHS

(PP

VERSUS

CP)

In

a large

percentage

of

equivale

n

cy

com

put

ations,

the

frequency

of

cash

flows

does not equal the frequency

of

interest

compo

unding.

For

example,

cash

flows

may

occ

ur

monthly

, and

compounding

occur

s annually,

quart

erly,

or

more often.

SECTION 4.5 Equivalence Relation

s:

Single Amounts w

ith

PP ~ CP

TABLE

4-5

Section References for Equivalence Calculations Based

on

Payment Period and Compounding Period Comparison

Involves Involves Uniform

Series

Length

Single

Amounts

or

Gradient

Series

of

Time

(P

and

F Only) (A, G,

or

g)

PP = CP Section 4.5 Section 4.6

PP

> CP Section 4.5

Section 4.6

PP < CP

Section 4.7 Section 4.7

Consider deposits made to a savings account each month, while the earning rate

is

compounded quarterly.

The

length

of

the

CP

is a quarter, while the

PP

is a

month. To correctly perform any equivalence computation, it

is

essential that the

compounding period and payment period be placed on the same time basis, and

that the interest rate be adjusted accordingly.

The next three sections describe procedures to determine correct

i and n val-

ues for engineering economy factors and spreadsheet solutions. First, compare

the length

of

PP

and

CP,

then identify the cash flow series

as

only single amounts

(P and

F)

or as a selies (A, G, or g). Table

4-5

provides the section reference.

When only sing

le

amounts are

in

volved, there is no payment period

PP

per se

defined by the cash flows.

The

length

of

PP

is, therefore, defined

by

the time

period

t

of

the interest rate statement.

If

the rate is 8% per 6-months, com-

pounded quarterly, the

PP

is 6-months, the

CP

is

3 months, and PP >

CPo

Note that the section references in Table

4-5

are the same when PP = CP and

PP >

CPo

The

equations to determine i and n are the same. Additionally, the tech-

nique to account for the time value

of

money

is

the same because it

is

only when

cash flows occur that the effect

of

the interest rate is determined. For example,

assume that cash flows occur every 6 months

(PP is semiannual), and that inter-

est is compou

nd

ed each 3 months (CP is a quarter). After 3 months there is no

cash flow and no need to determine the effect

of

quarterly compounding. How-

ever, at the 6-month time point, it is necessary to consider the interest accrued

during the previous two quarterly compounding periods.

4.5 EQUIVALENCE RELATIONS: SINGLE

AMOUNTS

WITH

PP

2:

CP

When only single-amount cash flows are involved, there are two equally correct

ways

to

determine i and n for P / F and F / P factors. Method 1 is easier to apply,

because the interest tables

in

the back

of

the text can usually provide the factor

value. Method 2 likely requires a factor formula calculation, because the result-

ing effective interest rate is not an integer. For spreadsheets, either method is ac-

ceptable; however, method 1 is usually easier.

Method

1:

Determine the effective interest rate over the compounding period

CP, and set n equal to the number

of

compounding periods between P and F.

The

139

140

"

CHAPTER

4 Nominal and Effective Interest Rates

relations to calculate P and

Fare

P =

F(P

/

F,

effective i%

per

CP,

total

number

of

periods

n)

F =

P(F

/P, effective i%

per

CP

,

total

number

of

periods

n)

[4.9]

[4.10]

For

example, assume that a nominal 15% per year, compounded monthly, is the

stated credit card rate. Here

CP

is

a month.

To

find P or F over a 2-year span, cal-

culate the effective monthly rate

of

15%/12

= 1.25% and the total months

of

2(12) = 24. Then 1.25% and 24 are used in the P / F and F / P factors.

Any time period can be used to determine the effective interest rate; however,

CP

is

the best basis. The

CP

is

best because only over the CP can the effective

rate have the same numerical value as the nominal rate over the same time period

as the

CP.

This was discussed in Section 4.1 and Table

4-1.

This means that the

effective rate over

CP

is usually a whole number. Therefore, the factor tables

in

the back

of

the text can be used.

Method

2: Determine the effective interest rate for the time period t

of

the

nominal rate, and set n equal to the total number

of

periods using this same time

period. The

P and F relations are the same as in Equations [4.9] and [4.10] with

the term

effective i%

per

t substituted for the interest rate.

For a credit card rate

of

15

% per year, compounded monthly, the time period

t is I year.

The

effective rate over 1 year and n values are

Effective

i% per year = (1 +

0~~5)1

2

- 1 = 16.076%

n = 2 years

The

P/F

factor is the same by both methods:

(P/F,1.25%,24)

= 0.7422 using

Table 5; and

(P

/ F, 16.076%,2) = 0.7422 using the P / F factor formula.

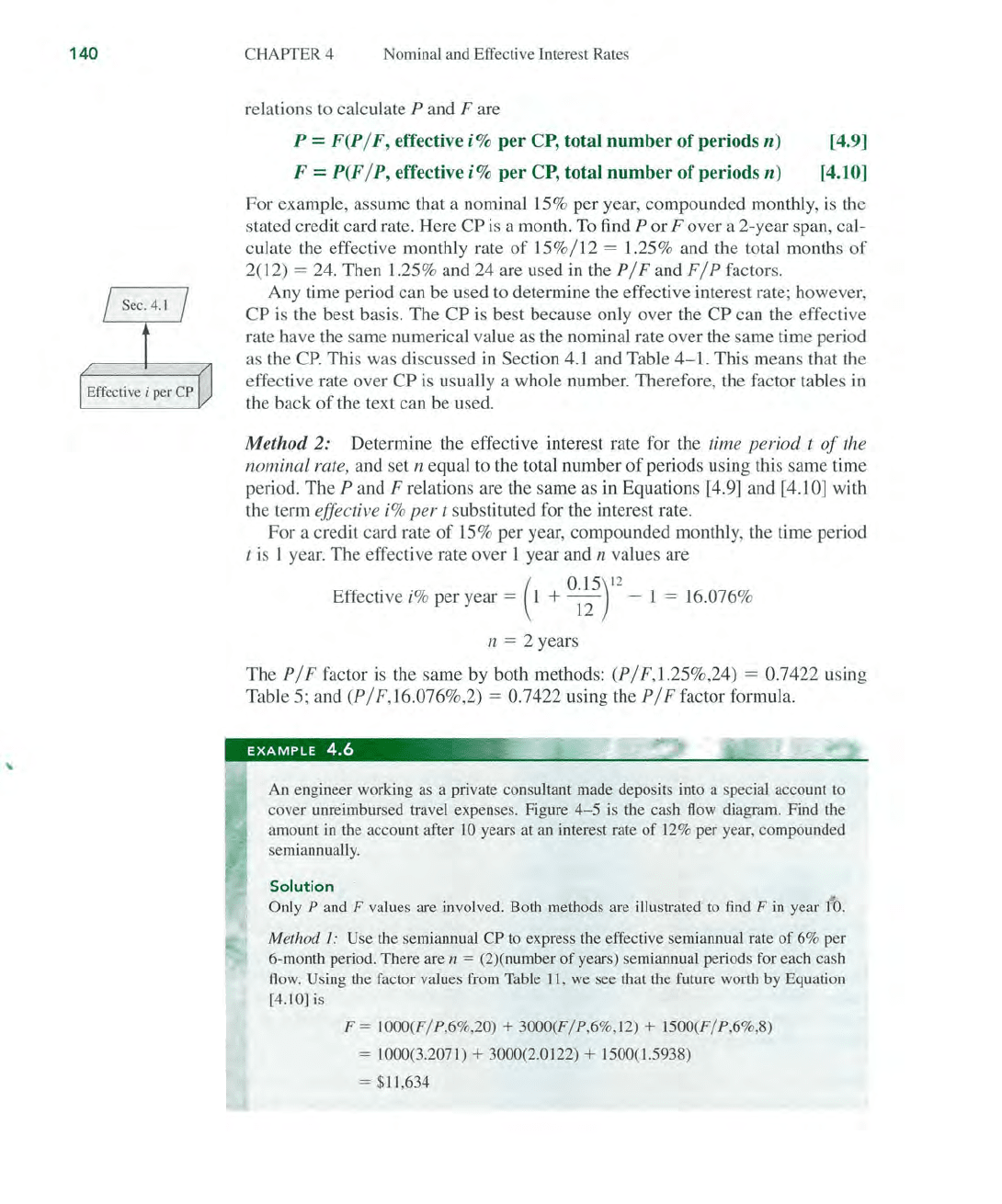

EXAMPLE

4.6

..

An engineer working as a pl;vate consultant

made

deposits into a special account to

cover

unreimbursed travel expenses. Figure

4-5

is

the cash flow diagram. Find the

amount

in the account after

10

years at an interest rate

of

12% per year, compounded

semiannually.

Solution .

Only P and F values are involved. Both methods are illustrated to find

Fin

year It.

Method 1: Use the semiannual CP to express the effective semiannual rate

of

6%

per

6-month period.

There

are n = (2)(number

of

years) semiannual periods for each cash

flow.

Using the factor values from Table 11,

we

see that the future worth by Equation

[4.10]

is

F = 1000(F/P,6%,20) + 3000(F/ P,6

%,

12)

+ 1500(F/P,6

%,

8)

=

LOOO(3.2071)

+ 3000(2.0122) + 1500(1.5938)

=

$11

,634

SECTION 4.5 Equivalence Relations: Single Amounts with PP 2':

CP

F=

?

0

2 3

4

5 6

7

8 9

10

J

!

I I

I

I

I

I I I

$

1000

$1500

$

3000

Figure

4-5

Ca

sh

flow

diagram,

Exampl

e 4.

6.

Method 2: Express the effective annual rate, based on semiannual compounding.

Effective i% per year

=

(I

+

0.~2

r -J = 12.36%

The

n value

is

the actual number

of

years. Use the factor formula (F/ P,i,n) = (1.1236)"

a

nd

Equation [4.10] to obtain the same answer as with method

I.

F =

JOOO

(F/ P,12.

36

%,IO) +

3000(F

/ P,12.36%,6) + 1500(F/ P,12.36%,4)

= J 000(3.2071) + 3000(2.0 J 22) + 1500(1.5938)

=

$11

,634

Comment

For single-amount cash flows, any combination

of

i and n derived from the stated nom-

inal rate can be used

in

the factors, provided they are on the same time basis. Using 12%

per year, compounded monthl

y,

Table

4-6

presents various acceptable combinations

of

i and

n.

Other combinations are

con

'ect, such as the effective weekly rate for i and

weeks for

n.

TABLE

4-6

Various i and

Il

Values for Single-

Amount Equations

Using r =

12

%

per

Year, Compounded Monthly

Effective Rate ;

1% per month

3.03% per quarter

6.15% per 6 months

12.68% per year

26.97% per 2 years

Units for n

Months

Quarters

Serniannual periods

Years

2-year periods

141

142

CHAPTER 4

Nominal and Effective Interest Rates

TABLE

4-7

Examples

of

nand

i Values Where PP = CP or PP > CP

Cash Flow

What

to

Find;

Standard

Series

Interest

Rate

What

Is

Given

Notation

$500 se

mi

annually

16% per year, Find

P; given A

P = 500(P/A,8%,

IO)

for 5 years

compounded

semiannually

$75 monthly for

24% per year,

Find

F; given A F =

75(F

/A,2%,36)

3 years compounded

monthly

$180 quarterly for

5% per quarter Find

F;

given A

F = 180

(F

/ A,5

%,

60)

15

years

$25 per month

1 % per month Find

P; given G P = 25(P/ G,1%,48)

increase for

4 years

$5000 per quarter

J%

per month

Find

A;

given P

A =

5000(A/

P

,3

.03%,24)

for 6 years

4.6

EQUIVALENCE RELATIONS:

SERIES

WITH

PP

2':

CP

When uniform or gradient series are included in the cash flow sequence, the pro-

cedure is basically the same

as

method 2 above, except that PP

is

now defined

by

the frequency

of

the cash flows. This also establishes the time unit

of

the effec-

tive interest rate. For example,

if

cash flows occur

Oi1

a quarterly basis, PP is a

quarter and the effective quart

er

ly rate is necessary. The n value is the total num-

ber

of

quarter

s.

If

PP

is

a quarter, S years translates to an n value

of

20 quarter

s.

This

is

a direct application

of

the following general guideline:

When cash flows involve a series (i.e.,

A,

G, g)

and

the

payment

period

equals

or

exceeds the compounding period in length,

• Find the effective i

per

payment

period.

• Determine n as the total

number

of

payment

periods.

In performing equivalence computations for series, only these values

of

i and n

can be used

in

interest tables, factor formulas, and spreadsheet functions. In other

words, there are no other combinations that give the correct answers, as there are

for single amount cash flows.

Table

4-7

shows the correct formulation for several cash flow series and

interest rate

s.

Note that n is always equal to the total number

of

payment periods

and

i

is

an effective rate expressed over the same time period as n.

EXAMPLE

4.7

'

For the past 7 years, a quality manager has paid $500 every 6 months for the software main-

tenance contract

of

a LAN. What is the equivalent amount after the last payment, if these

funds are taken from a pool

th

at

ha

s been returning 20% per year, compounded quarterly?

SECTION 4.6 Equivalence Relations: Series with PP

2:

CP

Solution

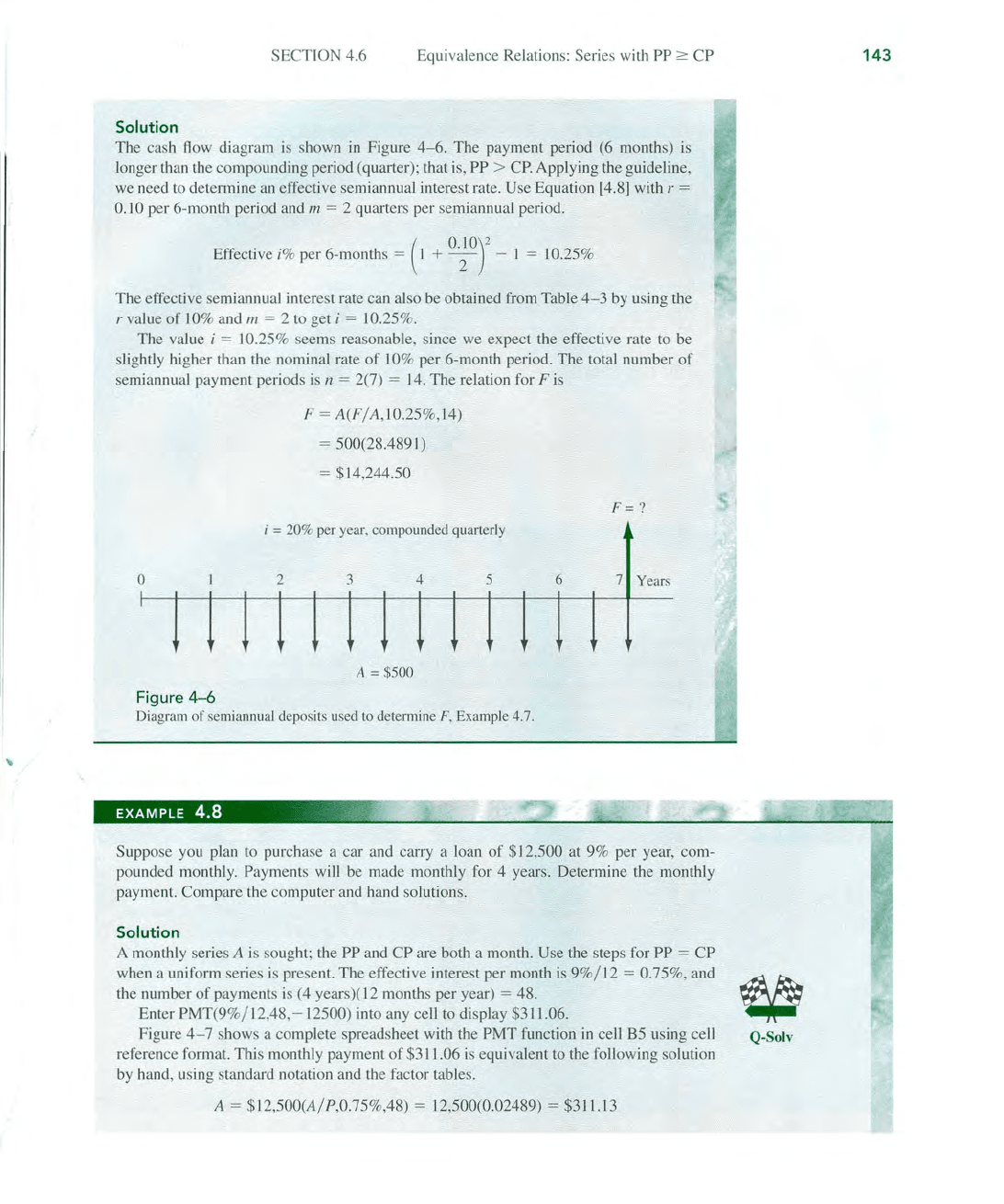

The cash flow diagram is shown

in

Figure

4-6.

The

payment period (6 months) is

longer than the compounding period (quarter); that is,

PP >

CP.

Applying the guideline,

we

need to determine an effective semiannual interest rate. Use Equation [4.8) with r =

0.10 per 6-month period and

/11.

= 2 quarters per semiannual period.

(

0.10)2

Effective i% per 6-months = J + 2 - I = 10.25%

The effect

iv

e semiannual interest rate can also be obtained from Table

4-3

by

using the

r value

of

10

% and

/11.

= 2 to get i =

10

.25%.

The

va

lu

e i = 10.25% see

ms

reasonable, since we expect the effecti ve rate to be

slightly higher than the nominal rate

of

10

% per 6-month period. The total number

of

semiannual payment periods

is

n = 2(7) = J

4.

The relation for F

is

o

I

Figure

4-6

F = A(F/A,10.25%,14)

= 500(28.4891)

= $14,244.50

i = 20% per year. compounded quarterly

2

3

4

5

A = $500

Diagram

of

semiannual deposits used to determine

F,

Example 4.7.

EXAMPLE 4.8

,<.

F=?

6 7

Years

Suppose you plan to purchase a car and carry a loan

of

$12,500

at

9% per year, com-

pounded monthly. Payments will be made monthly for 4 years. Determine the monthly

payment. Compare the computer and hand solution

s.

Solution

A monthly series A

is

sought; the PP and

CP

are both a mon

th

. Use the steps for PP =

CP

when a uniform series is present. The effective interest per month

is

9%/

12

= 0.75%, and

fIJ

the number

of

payments is (4 years)(12 months per year) = 48.

Enter PMT(9

%/

12

,48, - 12500) into any cell to display $3 11.06.

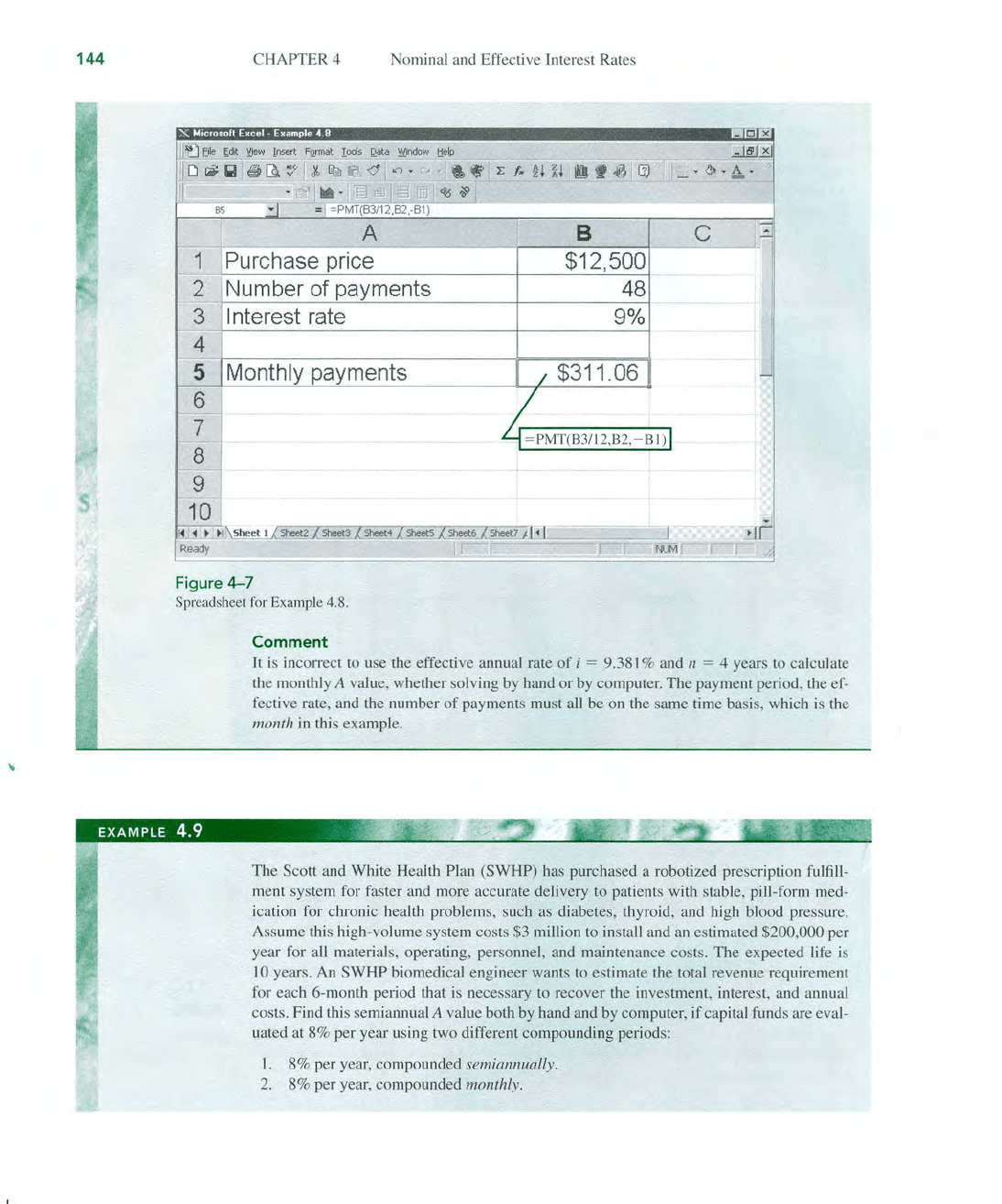

Figure

4-7

shows a complete spreadsheet with the PMT function in cell B5 using ce

ll

Q-

So

lv

reference format. This monthly payment

of

$311.06

is

equivalent to the following solution

by

hand, using standard notation and the factor tables.

A = $12,500(A/ P,0.75%,48) = 12,500(0.02489) =

$31

1.13

143

144

,

CHAPTER 4 No

mi

na

l

an

d Effective Interest Rates

_ 0 x

B

c

Purchase price $12,500

Number of payments

48

I nterest rate 9%

Monthly payments $311 .06

=

PM

T(B31l

2,

B2, - B I)

1

<4

J

<4

~

'

.,

\

Sh

ee

t 1

She~

Sheet5

~

eet

fJ(

Sheet7

.Jl

~

I

J

Re

ady

I

NUM

Fi

gure

4-7

Spreadsheet

fo

r

Ex

ample

4.

8.

Comment

It

is incorrect to use

th

e effective annual rate of i =

9.

3

81

% and n = 4 years to calculate

th

e monthly A value, whether solv

in

g by hand or by

co

mpute

r.

The payment pe

ri

od,

th

e ef-

fective rate, and

th

e number

of

payments must all be on

th

e same time

ba

sis, which is

th

e

month in

thi

s example.

The

Scott a

nd

White Health Plan (SWHP) has purchased a robotized prescription fulfill-

ment system for faster a

nd

more accurate delivery to patients with stable, pill-form med-

ic

ation for chronic health problems, such as diabetes, thyroid, and

hi

gh blood pressur

e.

Assume

thi

s

hi

gh-volume system costs $3 mil lion to

in

sta

ll

and an estimated $200,000 per

year for a

ll

mate

ri

als, operating, personnel, and maintenan

ce

costs. The expected life is

10

years. An SWHP biomedical eng

in

ee

r wants to estimate the total reve

nu

e requirement

for each 6-month pe

ri

od

th

at is necessary

to

recov

er

the investment,

in

terest, a

nd

annual

cost

s.

Find

thi

s semiannual A value bo

th

by hand a

nd

by computer, if capital funds are eval-

uated at 8% per year us

in

g two different compounding periods:

l.

8% per yea

r,

compounded semiannually.

2. 8% per year, compounded monthly.