Blank L., Tarquin A. Engineering Economy (McGraw-Hill Series in Industrial Engineering and Management)

Подождите немного. Документ загружается.

,

SECTION 4.6 Equ

iv

alence Relations: Series w

ith

PP

2:

CP

Solution

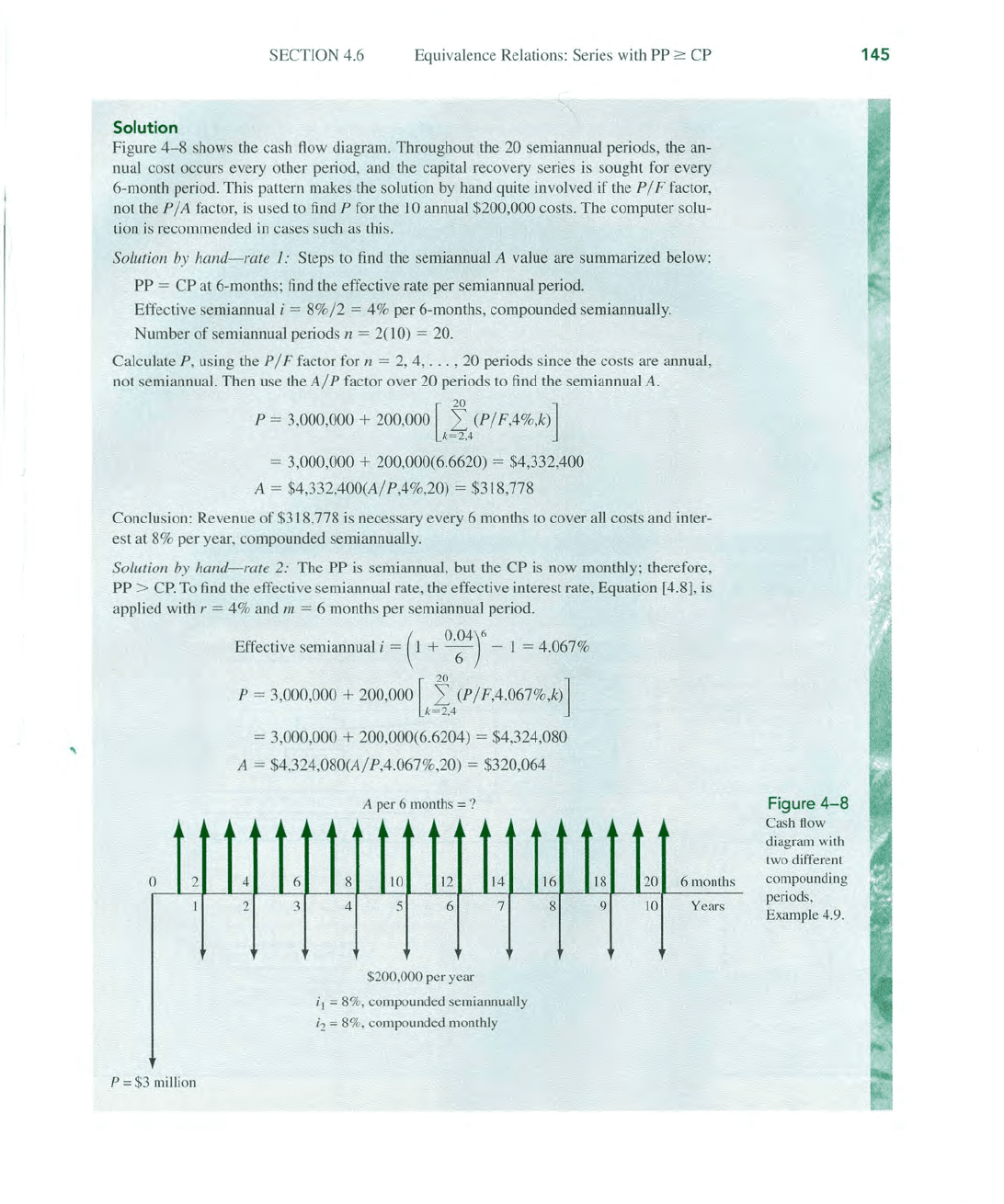

Figure 4

-8

shows the cash

flow

diagram. Throughout the 20 semiannual periods, the an-

nu

al cost occurs every other period, and the capital recovery series

is

sought for every

6-month period. This pattern makes the solution by hand quite involved if

th

e P / F factor,

not the

P / A factor,

is

used to

find

P for the

10

annual $200,000 costs. The computer solu-

tion

is

recommended

in

cases such as this.

Solution

by hand- rate

I:

Steps to

find

the

semjarUJUal

A value are summarized below:

PP = CP at 6-months;

find

the effective rate per semiannual period.

Effective semiannual

i =

8%/2

= 4% per 6-months, compounded semiannually.

Number

of

semiannual periods n = 2(J 0) = 20.

Calculate P, using the P / F factor for n =

2,4,

...

, 20 periods since the costs are annual,

not semiannual. Then use

th

e

A/

P factor over 20 periods to

find

the semiannual A.

P = 3,000,000 + 200,000

[

k~4

(P /

F,4%,k)]

= 3,000,000 + 200,000(6.6620) = $4,332,400

A = $4,332,400(A / P,4%,20) = $318,778

Conclusion: Reve

nu

e

of

$3

18

,778

is

nec

essa

ry

every 6 months to cover all costs and inter-

est at 8% per year, compounded semiannually.

Solution

by

hand-rat

e 2: The PP is se

mi

annual, bot the CP is now monthl

y;

therefore,

PP >

CP.

To

find

th

e effec

ti

ve semiannual rate, the effective interest rate, Equation [4.8], is

applied with

r = 4% and

In

= 6 months per semiannual period.

Effective semiannual

i =

(I

+

0.~4r

- I = 4.067%

P = 3,000,000 + 200,000

[k

~4

(P / F,4.067%,k)]

= 3,000,000 + 200,000(6.6204) = $4,324,080

A = $4,324,080

(A/

P

,4

.067%,20) = $320,064

A per 6 months = ?

0

2

4

6

8

10

12

J4

16

18

20

6 months

I 2

3

4

5 6

7

8

9

10

Years

$200,000 p

er

year

i

l

= 8%,

compo

unded semiannua

ll

y

i2 = 8%,

compo

unded monthly

P = $3 million

Figure

4-8

Cash flow

diagram with

two different

compounding

periods,

Example 4.9.

145

146

CHAPTER 4 Nominal and Effective Interest Rates

Now, $320,064, or $1286 more semiannually,

is

required to cover the more frequent com-

pounding

of

the 8% per year interest. Note that all PI F and AI P factors must be calculated

with factor formulas at 4.067%. This method

is

usually more calculation-intensive and

error-prone than with a spreadsheet solution.

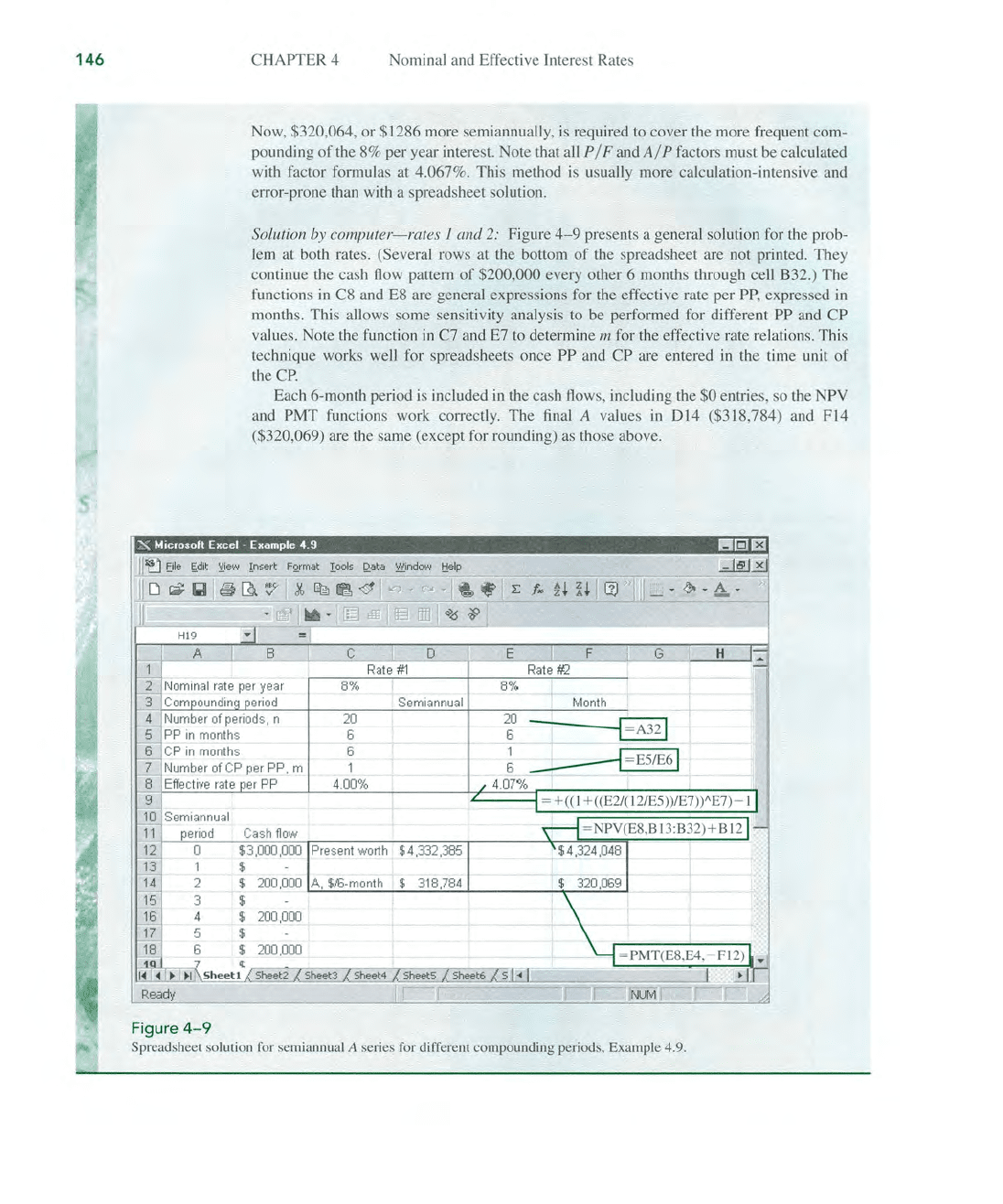

Solution by

computer-rates

1 and 2: Figure

4-9

presents a general solution for the prob-

lem

at both rates. (Several rows at the bottom

of

the spreadsheet are not printed. They

continue the cash flow pattern

of

$200,000 every other 6 months through cell B32.)

The

functions

in

C8 and

E8

are general expressions for the effective rate per PP, expressed

in

months. This allows some sensitivity analysis to be performed for different PP and

CP

values. Note the function

in

C7 and E7 to determine m for the effective rate relations. This

technique works well for spreadsheets once

PP and CP are entered

in

the time unit

of

the

CP.

Each 6-month period

is

included

in

the cash flows, including the $0 entrie

s,

so the NPV

a

nd

PMT functions work con·ectly. The final A values

in

014

($318,784) and F14

($320,069) are the same (except for rounding)

as

those above.

X I.hcrosoft

Excel·

Example 4.9

I!lIiIEf

Semiannual

period

o

1

2

3

Figure 4- 9

0 E

8%

8~~

Semiannual Month

20 20

----sill

6 6

6

1

~

=

ES

/

E6

1

1 6

4.00% 4.07%

= +

«(1

+

«E2/(12/ES

))/E7

))A

E7

)-

1

Cash

fi

ow

= N

PV

(E

S,

8 13

:8

32)+ B

12

$3,000,000

Prese

nt

worth

$4.

332,385

$

A, $!l3·month $ 318,784

$

200 ,000 L:...:!...:;;;:....;;.;.:c.:..:.;..c---'---':..:.:::;.,.:...::...;-L-

____

~==::....r

$

$ 200,000

$

$

=

PMT

(

ES

,E4

,-

FI2

)

I

~~=~~~o;--.,.,-J

I

.l..

1

,

Nur

Vl

,

Spreadsheet solution for semiannual A series for different

compounding

periods,

Ex

ample 4.9.

SECTION 4.7

Equivalence

Relation·

,:

Single Amounts and Series With

PP

<

CP

4.7 EQUIVALENCE RELATIONS: SINGLE

AMOUNTS

AND

SERIES

WITH

PP

<

CP

If

a person deposits money each month into a savings account where interest is

compounded quarterly, do all the monthly deposits earn interest before the next

quarterly compounding time?

If

a person's credit card payment

is

due with inter-

est

on

the 15th

of

the month, and if the full payment is made on the 1 st, does the

financial institution reduce the interest owed, based on early payment?

The

usual

answers are 'No'. However, if a monthly payment on a

$10 million, quarterly-

compounded, bank loan were made early by a large corporation, the corporate

financial officer would likely insist that the bank reduce the amount

of

interest

due, based on early payment. These are examples

of

PP

<

CP.

The

timing

of

cash flow transactions between compounding points introduces the question

of

how interperiod compounding

is

handled. Fundamentally, there are two policies:

interperiod cash flows earn

no interest, or they earn compound interest.

For a no-interperiod-interest policy, deposits (negative cash flows) are all re-

garded

as

deposited at the end

of

the compounding period, and withdrawals are

all regarded as

withdrawn at the beginning. As an illustration, when interest is

compounded quarterly, all monthly deposits are moved to the end

of

the quarter

(no interperiod interest

is

earned), and all withdrawals are moved to the begin-

ning (no interest

is

paid for the entire quarter). This procedure can significantly

alter the distribution

of

cash flows before the effective quarterly rate is applied to

find

P, F, or A. This effectively forces the cash flows into a

PP

=

CP

situation, as

discussed in Sections 4.5 and 4.6. Example

4.10 illustrates this procedure and the

economic fact that, within a one-compounding-period time frame, there is no

interest advantage to making payments early.

Of

course, non-economic factors

may be present.

EXAMPLE 4.10

.~.

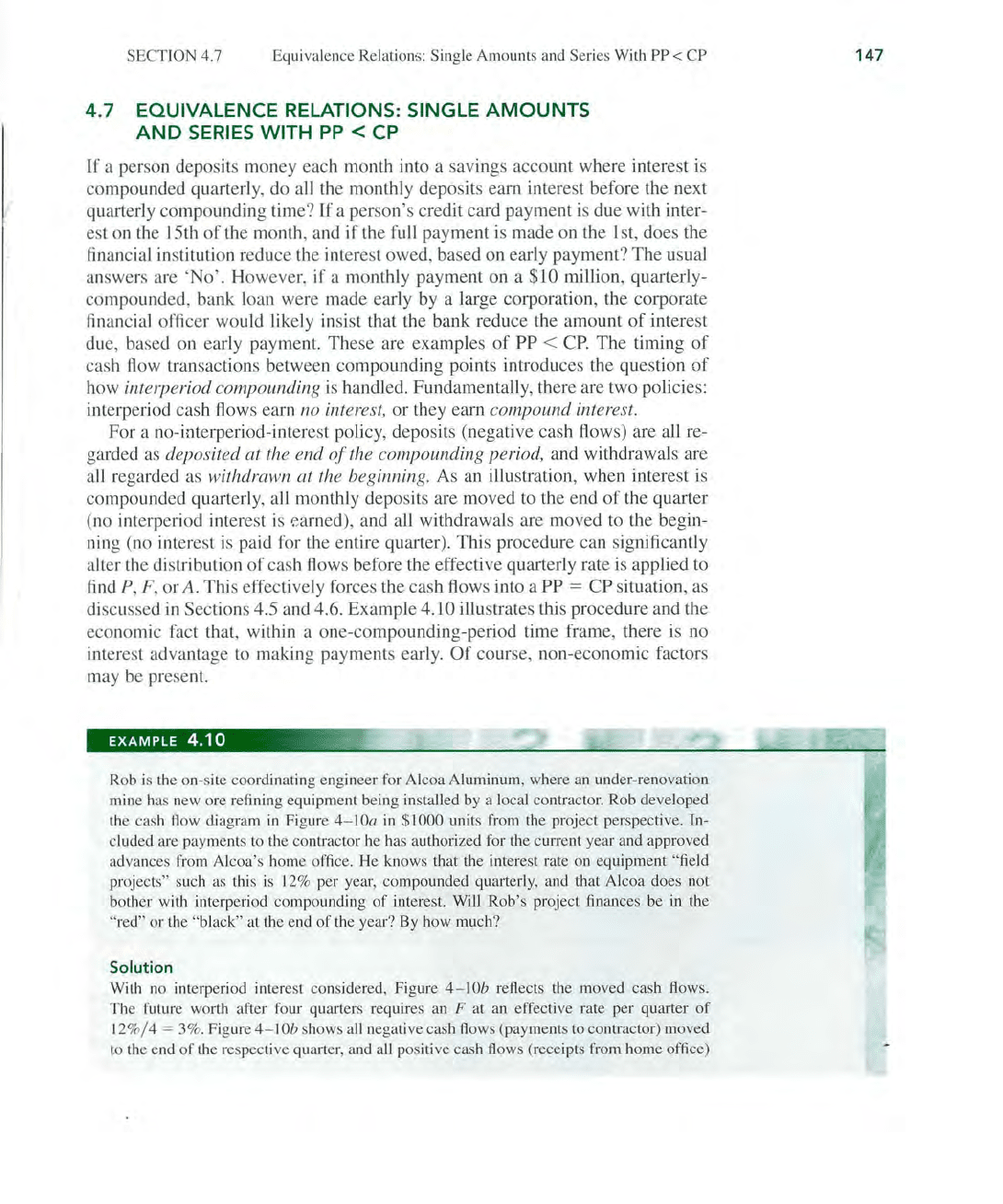

Rob is the on-site coordinating engineer for Alcoa Aluminum, where an under-renovation

mine has new

ore

refining equipment being installed by a local contractor.

Rob

developed

the cash flow diagram

in

Figure 4-

IOa

in

$1000 units from the project perspective. In-

cluded are payments to the contractor he has authorized for the current year and approved

advances

fi

·om Alcoa's home office.

He

knows that the interest rate on equipment "field

projects"

such as this

is

12% per year, compounded quarterly, and that Alcoa does not

bother with interperiod compounding

of

interest. Will Rob's project finances be in the

"red"

or

the "black" at the end

of

the year? By how

much?

Solution

With no interperiod interest considered, Figure

4-10b

reflects the moved cash flows.

The

future worth afler four quarters requires an F at an effective rate per quarter

of

12

%/

4 = 3%. Figure 4- 1

Ob

shows all negative cash flows (payments to contractor)

moved

to the end

of

the respective quarter, and

aU

positive cash flows (receipts from home office)

147

148

CHAPTER 4 Nominal and Effective Interest Rates

Receipts from home office

$

90

$120

0

Year

0

2 3

4

6 7

12

Month

$75

$100

$

150

Payments to contractor

$200

(a)

F=

?

$165

$90

0

2 3

t

Quarter

0

2

3

4

5 6 7 8 9

10

11

J2t

Month

$50

$150

r>

$175

$

200

l

F=

?

(b)

Figure

4-10

(a) Actual and (b) moved cash

Aows

(in

$1000)

for quarterly compounding periods using

no

interperiod

interest, Example 4. J

O.

moved

to

the beginning

of

the respective quarter. Calculate the F value at 3

0/0

.

F = 1000[ -

150(F/P

,3

0/0,

4) -

200(F/

P,3%,3) + (- 175 +

90)(F

/ P,3%,2)

+ 165(F/ P,3%

.l)

- 50]

= $- 357,592

Rob can conclude that the on-site project finances will be

in

the red about $357,600 by the

end

of

the year.

If

PP < CP and interperiod compounding

is

earned, the cash flows are not

moved, and the equivalent

P,

F,

or A values are determined using the effective

interest rate per payment period. The engineering economy relations are deter-

mined in the same way as in the previous two sections for

PP

;:::

CP.

The effec-

tive interest rate formula will have an

m value less than 1, because there is only

a fractional part

of

the

CP

within one

PP.

For

example, weekly cash flows and

SECTION

4.

8 Effective Interest Rate for Continuous Compounding

quarterly compounding require that m =

1/13

of

a quarter.

When

the nominal

rate is 12% per year, compounded quarterly (the

same

as

3%

per quarter, com-

pounded quarterly), the effective rate

per

PP

is

Effective weekly i%

= (1.03)1/13 - 1 = 0.228% per week

4.8

EFFECTIVE INTEREST

RATE

FOR CONTINUOUS

COMPOUNDING

If

we allow compounding to occur more and more frequently, the compounding

period becomes shorter and shorter. Then

m,

the number

of

compounding peri-

ods per payment period, increases. This situation occurs in businesses that have

a very large number

of

cash flows every day, so it is correct to consider interest

as compounded continuous

ly.

As m approaches infinity, the effective interest

rate, Equation

[4.8], must be written in a new form. First, recall the definition

of

the natural logarithm base.

lim 1 +

- = e =

2.71828+

(

1)

11

,,

-'>00

h

[4.11]

The limit

of

Equation [4.8] as m approaches infinity is found by using

r/m

=

l/h

, which makes m = hr.

r)1II

+ -

-1

m

(

1)'11

.

=

Ii

m I + - - 1

Ii

-,>

oo

h

[(

1)"Jr

= lim 1 + - - 1

11.

-'>

00

h

[4.12]

Equation [4.12] is used to compute the effective continuous interest rate, when

the time periods on

i and r are the same. As an illustration,

if

the nominal annual

r =

15

% per year, the effective continuous rate per year is

i%

=

eO.

ls

-

1 = 16.183%

For

convenience, Table

4-3

includes effective continuous rates for the nominal

rates listed.

EXAMPLE 4.11

ff~

(a) For

an

interest rate

of

18% per year, compounded continuously, calculate the ef-

fective monthly and annual interest rates.

(b)

An

investor requires an effective return

of

at least

15

%. What

is

the minimum

annual nominal rate that is acceptable for continuous compounding?

149

150

CHAPTER 4

Nominal and Effective Interest Rates

Solution

(a)

The

nominal monthly rate is r =

18

%/

12 = 1.5%,

or

0.015 per month. By

Equation [4.12], the effective monthly rate is

i% per month

= e

r

- 1 =

eo.O

JS

- 1 = 1.511%

Similarly, the effective annual rate using

r = 0.18 per year is

i% per year

= e

r

- 1 =

eO

ls

- 1 = 19.72%

(b) Solve Equation [4.12] for r by taking the natural

lo

garithm.

e'

- 1 = 0.15

e'

= 1.15

In

e'

=

In

1.15

r% = 13.976%

Therefore, a rate

of

13.976% per year, compounded continuousl

y,

will generate

an effective

15

% per year return.

Comment

The

general fon";ula to find the nominal rate, given the effective continuous rate i, is

r =

In

(1

+ i)

EXAMPLE

4.12

'.

Engineers Marci and Suzanne both invest $5000 for

10

years at 10%

per

yea

r.

Compute

the future worth for both individuals

if

Marci re

ce

ives annual compounding a

nd

Su

za

nne receives continuous compounding.

Solution

Marci: For annual compounding tbe future worth is

F = P

(F/

P,1O

%,lO) = 5000(2.5937) = $12,969

Su

za

nne: Using Equation

[4

.12], first find the effective i per year for use

in

the F / P

factor.

Effective i%

=

eO

J

O - 1 = 10.517%

F =

P(F

/ P,

1O

.517%,

10)

= 5000(2.7183) = $13,

591

Continuous compounding causes a $622 increase

in

earnings. For comparison, daily

compounding yields an

ef

fective rate

of

10.516%

(F

= $13,590), only slightly less than

the I 0.517% for continuous compounding.

SECTION 4.9 Interest Rates That Vary Over Time

For some business activities, cash flows occur throughout the day. Examples

of

costs are energy and water costs, inventory costs, and labor costs. A realistic

model for these activities is to increase the frequency

of

the cash flows to become

continuous. In these cases, the economic analysis can be performed for continu-

ous cash flow (also called continuous

fuRds flow) and the continuous com-

pounding

of

interest as discussed above. Different expressions must be derived

for the factors for these cases. In fact, the monetary differences for continuous

cash flows relative

to

the discrete cash flow and discrete compounding assump-

tions are usually not large. Accordingly, most engineering economy studies do

not require the analyst to utilize these mathematical forms to make a sound eco-

nomic project evaluation and decision.

4.9 INTEREST

RATES

THAT VARY OVER TIME

Real-world interest rates for a corporation vary from year to year, depending upon

the financial health

of

the corporation, its market sector, the national and interna-

tional economies, forces

of

inflation, and many other elements. Loan rates may

increase from one year to another. Home mortgages financed using

ARM

(ad-

justable rate mortgage) interest is a good example.

The

mortgage rate is sljghtly

adjusted annually to reflect the age

of

the loan, the current cost

of

mortgage

money, etc. An example

of

interest rates that rise over time is inflation-protected

bonds that are issued by the U.S. government and other agencies.

The

dividend

rate that the bond pays remains constant over its stated life, but the lump-sum

amount due to the owner when the bond reaches maturity

is

adjusted upward with

the inflation index

of

the Consumer Price Index (CPI). This means the annual rate

of

return will increase annually in accordance with observed inflation. (Bonds and

inflation are visited again

in

Chapters 5 and 14, respectively.)

When

P, F, and A values are calculated using a constant

or

average interest rate

over the life

of

a project, rises and falls in i are neglected.

If

the variation

in

i is

large, the equivalent values will vary considerably from those calculated using

the constant rate. Although an engineering economy study can accommodate

varying

i values mathematically, it

is

more involved computationally to do so.

To determine the

P value for future cash flow values

(F)

at different i values

(i/) for each year t, we will assume annual compounding. Define

i/

= effective annual interest rate for year t

(t

= years 1 to n)

To

determine the present worth, calculate the P

of

each

F/

value, using the applic-

able

i

f'

and sum the results. Using standard notation and the P / F factor,

P =

FI(P

/

F,il,l)

+

FlP

/ F,i

l

,

1)(P/F,i2,l)

+

...

+ F

n

(P/F,i

l

,l)(P/F,i2,l)

...

(P/F,in,l)

[4.13]

When only single amounts are involved, that is, one P and one F in the final year

n, the last term

in

Equation [4.13]

is

the expression for the present worth

of

the

future cash flow.

P = F

II

(P

/

F,i

1

,1)(P/

F,i

2

,1)'"

(P/

F,i

ll

,l)

[4.14]

151

152

EXAMPLE 4.13

o

1

i=

7o/J

p=

?

Figure

4-11

CHAPTER 4 Nominal and Effective Interest Rates

If

the equivalent uniform series A over all n years

is

needed, first find P using ei-

ther

of

the last two equations, then substitute the symbol A for each

F,

symbol.

Since the equivalent

P has been determined numerically using the varying rates,

this new equation will have only one unknown, namely,

A. The following exam-

ple illustrates this procedure.

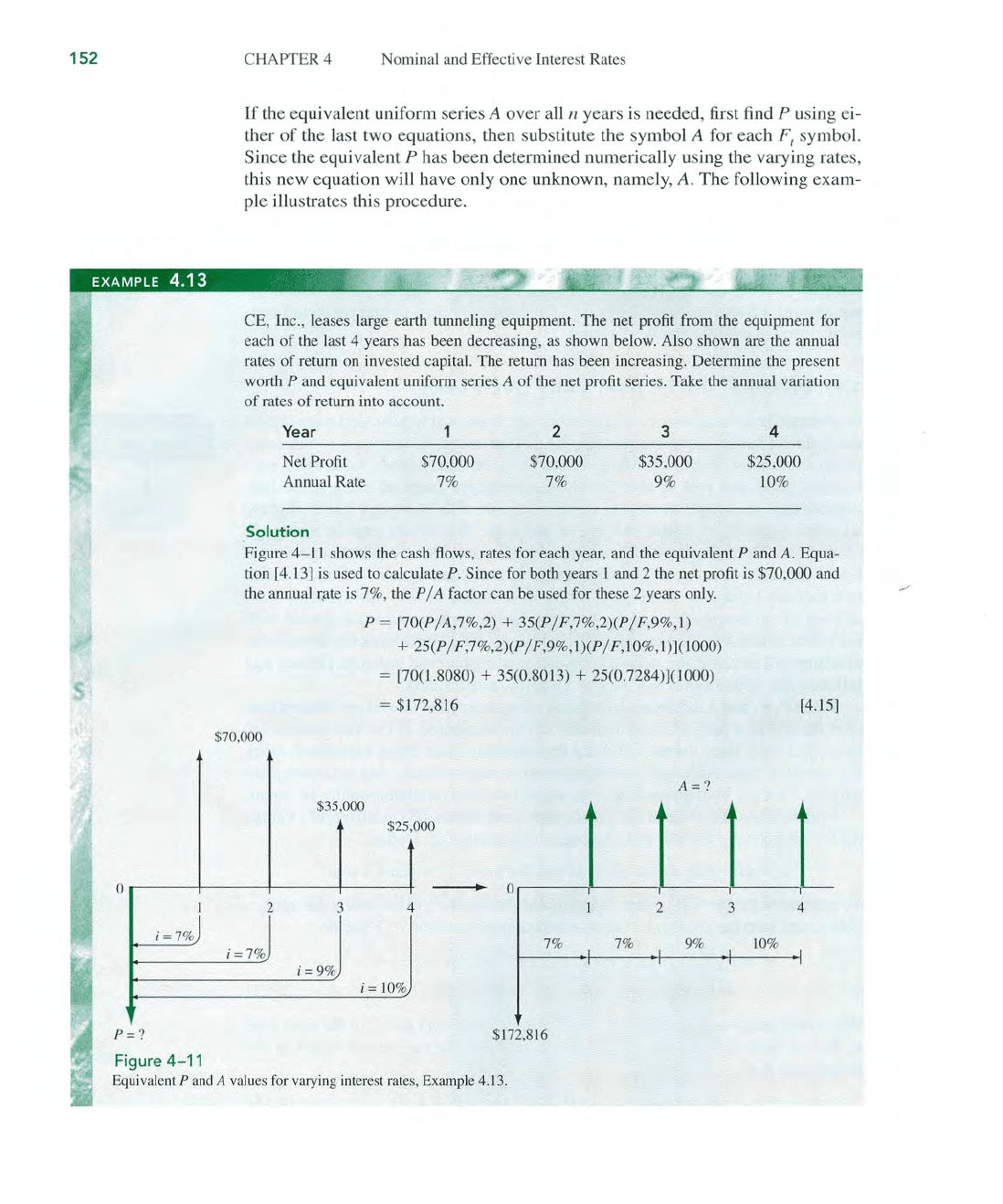

CE, Inc., leases large earth tunneling equipment. The net profit from the equipment for

each

of

the last 4 years has been decreasing, as shown below. Also shown are the annual

rates

of

return on invested capital. The return has been increasing. Determine the present

worth

P and equivalent uniform series A

of

the net profit series. Take the annual variation

of

rates

of

return into account.

Year

Net

Profit

Annual Rate

Solution

1

$70,000

7%

2

$70,000

7%

3

$35,000

9%

4

$25,000

10

%

Figure

4-11 shows the cash flows, rates for each year, and the equivalent P and A. Equa-

tion [4.13]

is

used to calculate

P.

Since for both years 1 and 2 the net profit is $70,000 and

the annual r,ate

is

7%, the P / A factor can be used for these 2 years only.

$70,000

2

i=7

%

$35,000

3

i=9

%

P = [70(P/A,7%,2) +

35(P/F,7%,2)(P/F,9%,l)

+ 25(P/F,7%,2)(P/ F,9

%,

1)(P/

F,

10%,1)](1000)

= [70(1.8080) + 35(0.8013) + 25(0.7284)](1000)

= $172,816

A

=?

$25,

4 2

7% 7% 9%

i=

10%

$172,816

[4.15]

3

4

10%

Eq

uivalent P and A values for varying interest rates, Example 4.13.

CHAPTER SUMMARY

To

determine

an

equivalent annual series, substitute the symbol A for all net profit values

on

the right side

of

Equation [4.15], set it equal to P = $172,816 and solve for

A.

This equa-

tion accounts for the varying

i values each year. See Figure 4-11 for the cash flow diagram

transformation.

$172,816

= A[(1.8080) +

(0

.8013) + (0.7284)] = A [3.3377]

A

=

$51

,777 per year

Comment

If

the average

of

the four annual rates, that is, 8.25

%,

is

used, the result

is

A = $52,467.

This

is

a $690 per year overestimate

of

the required equivalent amount.

When there

is

a cash flow in year 0 and interest rates vary annually, this cash

flow must be included when one

is

determining

P.

In the computation for the

equivalent uniform series

A over all years, including year 0, it

is

important to in-

clude this initial cash flow at

t = O. This is accomplished by inserting the factor

value for

(P

/

F,i

o,

O)

into the relation for A. This factor value is always 1.00.

It

is

equally correct to find the

A value using a future worth relation for F in year

n.

In

this case, the A value is determined using the F / P factor, and the cash flow in

year

n is accounted for by including the factor

(F

/ P,i",O) = 1.00.

CHAPTER SUMMARY

Since many real-world situations involve cash flow frequencies and compound-

ing periods other than 1 year, it is necessary to use nominal and effective interest

rates. When a nomjnal rate

r

is

stated, the effective interest rate per payment

period is determjned

by

using the effective interest rate equation.

(

~

\m

Effective i = 1 + (

iii')

- 1

The m is the number

of

compounding periods (CP) per payment period (PP).

If

interest compounding becomes more and more frequent, the length

of

a

CP

ap-

proaches zero, continuous compounding results, and the effective

i

is

e

r

-1.

All

engineering eco

nom

y factors require the use

of

an

effective interest rat

e.

The i and n values placed in a factor depend upon the type

of

cash flow series.

If

only single amounts (P and

F)

are present, there are several ways to perform

equivalence calculations using the factors. However, when series cash flows

(A, G, and g) are present, only one combination

of

the effective rate i and num-

ber

of

periods n is correct for the factors. This requires that the relative lengths

of

PP and

CP

be considered

as

i and n are determined. The interest rate

and

payment

periods

must

ha

ve the

sam

e time unit for the factors to correctly account for the

time value

of

money.

153

154

CHAPTER 4 Nominal and Effective Interest Rates

From

one

year

(or

interest period) to the next, interest rates will vary. To ac-

curately

perform

equivalence

calculations for P

and

A

when

rates vary signifi-

cantly, the

applicable

interest rate

should

be

used, not

an

average

or

constant

rate

.

Whether

performed

by

hand

or

by

computer

,

the

procedures

and factors

are

the

same

as those for

constant

interest rates;

however

,

the

number

of

calculations

increases.

PROBLEMS

Nominal and Effective Rates

4. 1 Identify

the

compounding

period

for

the

following

interest statements: (a) 1 %

per

month; (b) 2.5%

per

quarter; and (c) 9.3%

per

year

compounded

semiannually.

4.2

Identify the

compounding

period for

the

following interest statements: (a)

Nominal

7% per

year

compounded

quarterly;

(b) effective 6.8%

per

year

compounded

monthly; and (c) effective

3.4

%

per

quar-

ter

compounded

weekly.

4.3

Determine

the

number

of

times interest

would

be

compounded

in 1

year

for the

following intere

st

statements: (a) 1 %

per

month; (b) 2%

per

quarter; and (c) 8%

per

year

compounded

sem

iannually.

4.4

For

an interest rate

of

10%

per

year

com-

pounded

quarterly,

determine

the

number

of

times interest would

be

compounded

(a)

per

quarter

, (b)

per

year, and (c)

per

3 years.

4.5

For

an interest rate

of

0.50%

per

quarter

,

determine

the nominal interest rate

per

(a)

semiann

ual period, (b) year,

and

(c) 2 years.

4.6

For

an interest rate

of

12%

per

year

com-

pounded

every

2

months

,

determine

the

nominal interest rate

per

(a) 4

months

,

(b) 6

months

, and (c) 2 years.

4.7

For

an interest rate

of

10%

per

year,

com-

pounded

quarterly,

determine

the nominal

rate

per

(a) 6

months

and

(b) 2 years.

4.8 Identify the following interest rate state-

ments as either nominal

or

effective:

(a) 1.3%

per

month; (b) 1 %

per

week

,

com-

pounded weekly; (c) nominal

15

%

per

year,

compounded

monthly;

(d)

effective 1.5%

per month,

compounded

daily; and

(e)

15

%

per year,

compounded

semiannually.

4.9

What

effective

interest rate

per

6

months

is

equivalent

to 14%

per

year,

compounded

semiannually?

4.10

An

interest rate

of

16%

per

year,

com-

pounded

quarterly, is

equivalent

to

what

effective interest

rate

per

year?

4.

11

What

nominal interest rate

per

year

is

equivalent

to an effective 16%

per

year

,

compounded

semiannually?

4.12

What

effective interest

rate

per

year is

equivalent

to an effective 18% per year,

compounded

semiannually?

4.13

What

compounding

period is associated

with nominal

and

effective

rates

of

18%

and

18.81 %

per

year,

respectively?

4.14

An

interest

rate

of

1%

per

month

is

equivalent

to

what

effective

rate

per

2

months?