Blank L., Tarquin A. Engineering Economy (McGraw-Hill Series in Industrial Engineering and Management)

Подождите немного. Документ загружается.

SECTION 12.4

Ca

pital Bu

dget

ing Problem

Form

ulation Using

Linear

Programming

X

Mi

cr

os

oft

EKeel

I!II§I

f3

Eile

~

di

t

~je

w

in

sert

FQ.rmat

I

oo

ls

~ata

~indo\N

tielp

A23

iI

E Hample

12

.3

I!lOO

f3

A

Project

s

Year

1

2

3

.

1~

I?

1§

10

17

11

18 12

19

Projects selected

20

f'VV

value

at

MARR

21

Contribution to Z

22

Inves1ment

I~

~

~

~I

She

etl

Ready

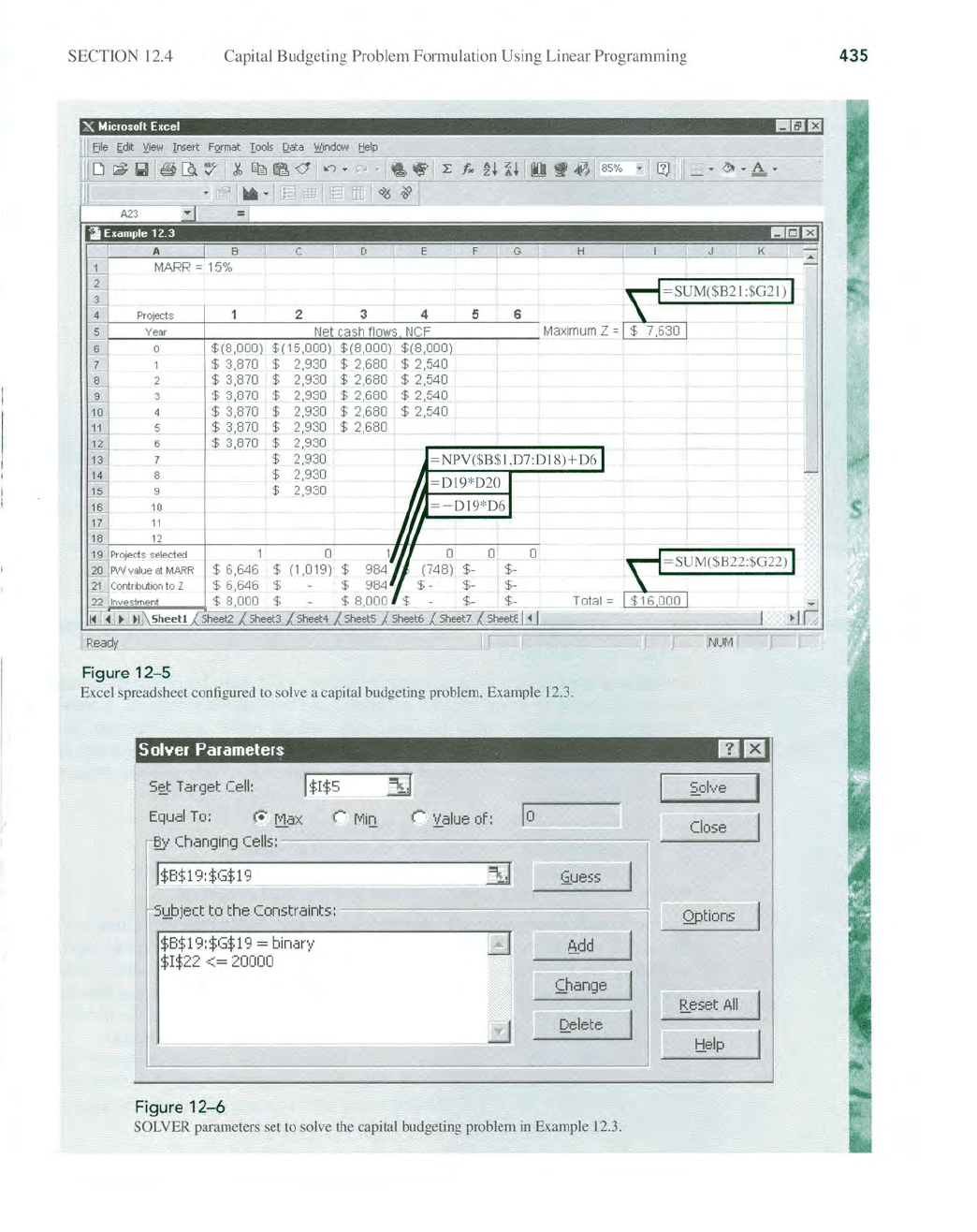

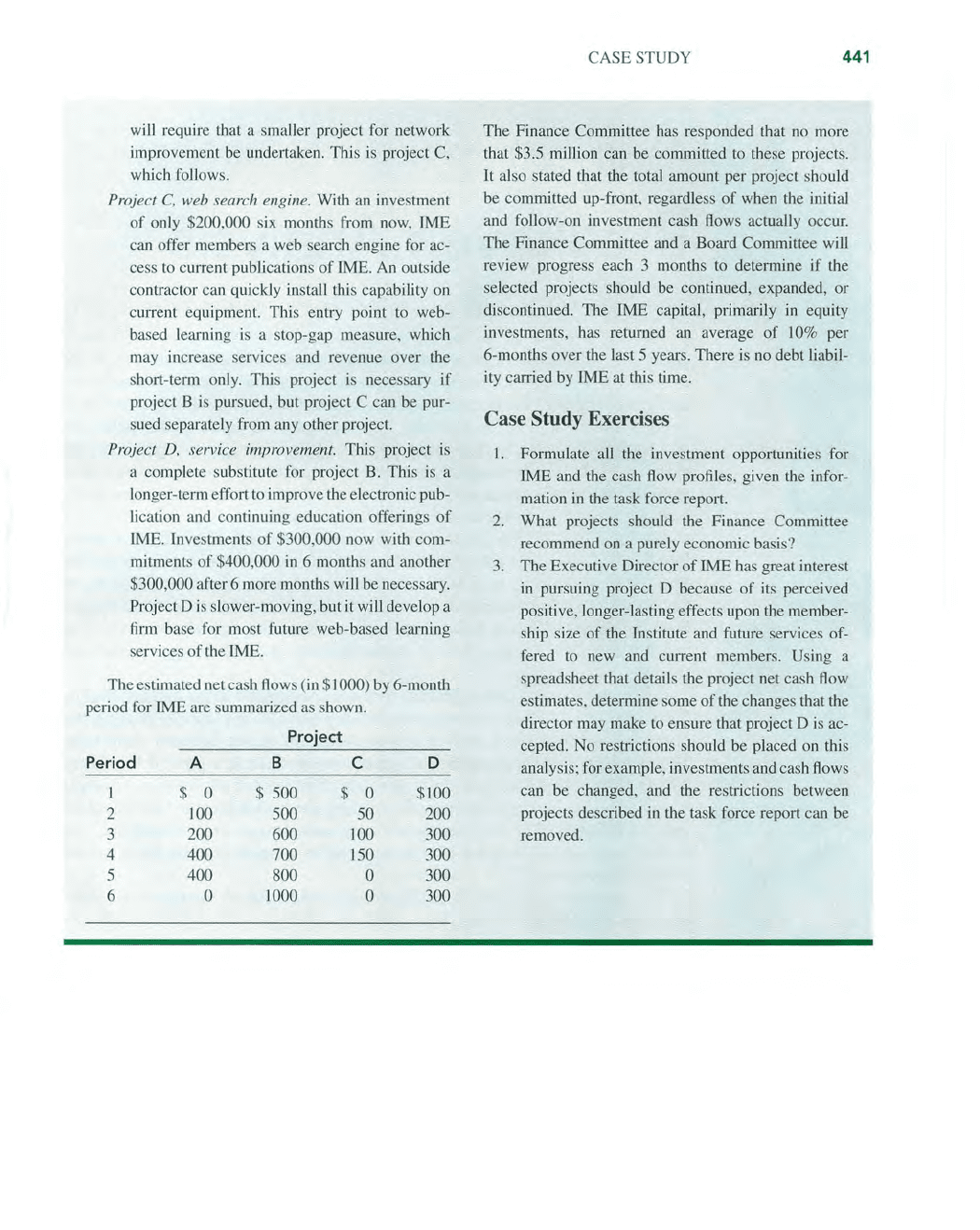

Figure

12-5

$(8

,000)

$ 3,870

$ 3,870

$

3,870

$ 3,870

$ 3,870

$

3,870

2 3 4 5 6

Net cash flows

NCF

$(15,000)

$(8,000) $(8,000)

$ 2,930 $ 2,680 $ 2,540

$ 2,930 $ 2,680 $ 2,540

$ 2,930 $ 2,680 $

2,540

$ 2,930 $ 2,680 $ 2,540

$ 2,930 $ 2,680

$ 2,930

$ 2,930

$ 2,930

$ 2,930

o o

$ (1,019)

$

$ 984 $- $-

$ 984

$-

$-

$ $ 8,000 $- $-

o

~lihilitI

'

l

Total =

Excel spreadsheet co

nfi

gured to solve a capital

bu

dget

in

g pro

bl

em, Example 12.3.

=SUM($B22:$G22)

NUM

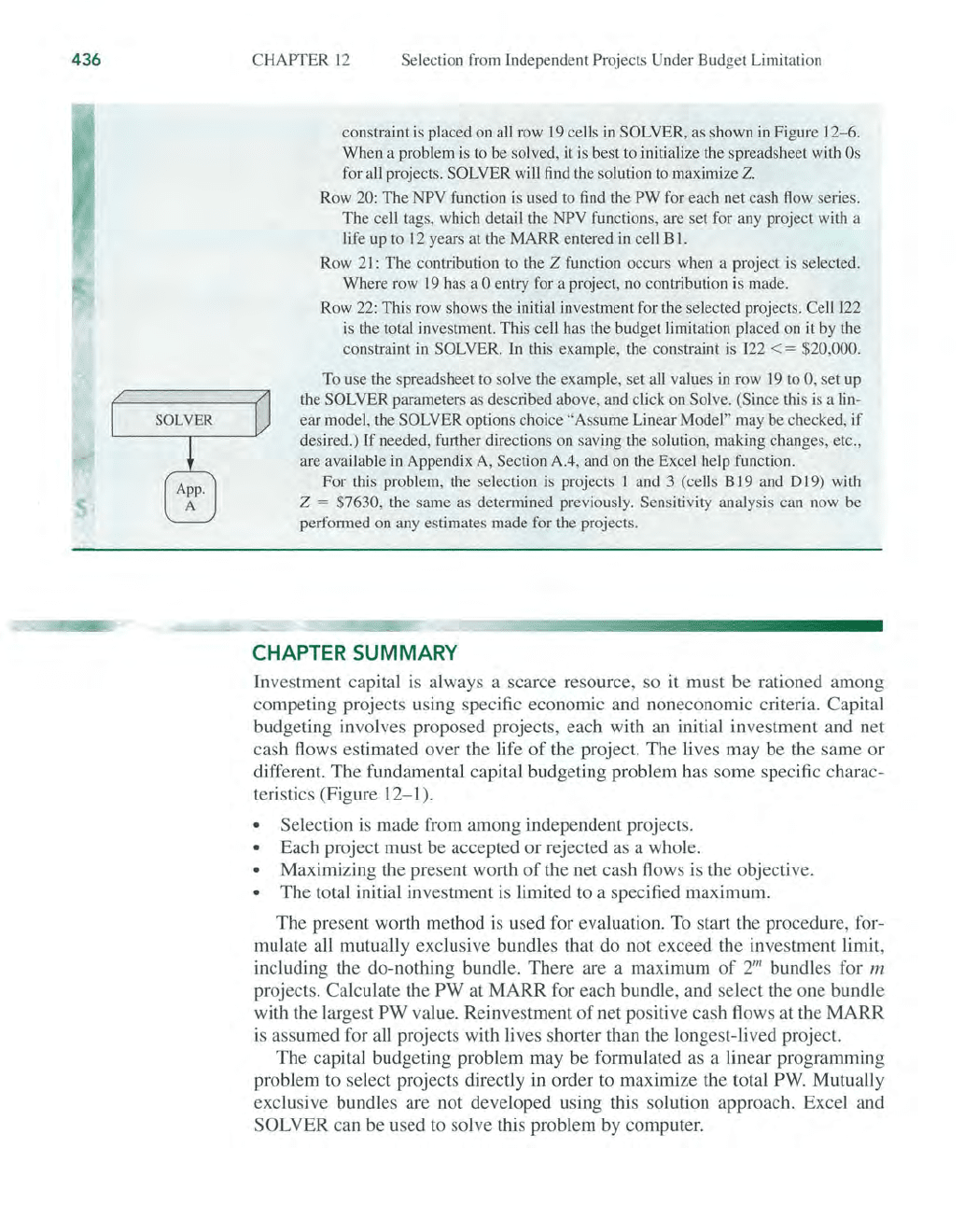

5 olver Parameters

DEI

s~

Target

Cell:

J$I$5

spl

ve

Equal

To:

r.

f:1a

x

r

rv1io.

r

~

alue

of:

]0

Close

j'

Changing

Cells:

------.,..-----,-~"'---'~

......

----

........

~-;-

--~

~--'

I I

. 3ij'

§.ue

ss

5!,lbject

to the Constraints:

~-=-~--~

~~

"=''''''''--

..........

-''''"'~~.

$8$19:$(;'$19 = binary

$I$22 <=

20000

Figure

12-6

8.dd

~hange

Q.elete

SOLVER parameters set to solve

th

e ca

pi

tal budgeting pro

bl

em

in

Example 12.3.

Qptions

&eset

All

tielp

435

436

CHAPTER

12

Selection from Independent Projects Under Budget Limitation

constraint

is

placed

on

all row

19

cells

in

SOLVER, as shown in Figure 12-6.

When a problem is to be solved,

it

is

best to initialize the spreadsheet with

Os

for all projects. SOLVER will find the solution

to

maximize

Z.

Row 20: The NPV fWlction is used to find the PW for each net cash flow selies.

The cell tags, which detail the NPV functions, are set for any project with a

life

up

to

12

years at the MARR entered in cell

Bl.

Row 21: The contribution to the Z function occurs when a project

is

selected.

Where row

19

has a 0 entry for a project, no contribution is made.

Row

22:

This row shows the initial investment for the selected projects. Cell

122

is

the total investment. This cell has the budget limitation placed on

it

by

the

constraint

in

SOLVER. In this example, the constraint is

122

<=

$20,000.

To

use the spreadsheet to solve the example, set all values

in

row

19

to 0, set up

the

SOLVER parameters as described above, and click on Solve. (Since this

is

a lin-

ear model, the

SOLVER options choice "Assume Linear Model" may be checked,

if

desired.)

If

needed, further directions on saving the solution, making changes, etc.,

are available

in

Appendix

A,

Section A.4, and

on

the Excel help function.

For this problem, the selection

is

projects 1 and 3 (cells B19 and D19) with

Z

= $7630, the same

as

determined previously. Sensitivity analysis can now be

performed on any estimates made for the projects.

CHAPTER

SUMMARY

Investment capital

is

always a scarce resource, so

it

must be rationed among

competing projects using specific economic and noneconomic criteria. Capital

budgeting involves proposed projects, each with

an

initial investment and net

cash flows estimated over the life

of

the project. The lives may be the same or

different. The fundamental capital budgeting problem has some specific charac-

teristics (Figure

12-1).

• Selection is made from among independent projects.

• Each project must be accepted or rejected

as

a whole.

• Maximizing the present worth

of

the net cash flows is the objective.

• The total initial investment

is

limited to a specified maximum.

The present worth method

is

used for evaluation.

To

start the procedure, for-

mulate all mutually exclusive bundles that do not exceed the investment limit,

including the do-nothing bundle. There are a maximum

of

2

m

bundles for m

projects. Calculate the PW at MARR for each bundle, and select the one bundle

with the largest

PW

value. Reinvestment

of

net positive cash flows at the MARR

is

assumed for all projects with lives shorter than the longest-lived project.

The capital budgeting problem may be formulated

as

a linear programming

problem

to

select projects directly in order

to

maximize the total

PW.

Mutually

exclusive bundles are not developed using this solution approach. Excel and

SOLVER can be used

to

solve this problem by computer.

PROBLEMS

Understanding the Capital Rationing

Problem

12.1

Write a short paragraph that explains the

problem

of

rationing investment capital

among several projects that are indepen-

dent

of

one another.

12.2 State the reinvestment assumption about

project cash flows that is made when one

is solving the capital budgeting problem.

12.3

12.4

Four independent projects

(1, 2, 3, and 4)

are to be evaluated for investment by

Perfect Manufacturing. Develop all the

acceptable mutually exclusive bundles

based on the following selection restric-

tions developed by the department

of

engineering production:

Project 2 can be selected only if project

3

is

selected.

Projects 1 and 4 should not both

be selected; they are essentially

duplicates.

Develop all acceptable mutually exclu-

sive bundles for the four independent

projects described below

if

the invest-

ment limit

is

$400 and the following pro-

ject

selection restriction applies: Project

I

can be selected only if both projects

3 and 4 are selected.

Project

2

3

4

Initial Investment, $

- 250

- 150

- 75

- 235

Selection from

Independent

Projects

12.5 (a) Determine which

of

the following

independent projects should be se-

lected for investment

if

$325,000

is

available and the MARR

is

10% per

Project

A

B

C

0

E

PROBLEMS

437

year. Use the

PW

method to evalu-

ate mutually exclusive bundles to

make the selection.

Initial Net Cash

Life,

Investment, $

Flow,

$lYear

Years

- 100,000

50,000

8

-125

,000

24,000

8

-

120

,000

75

,000

8

-220

,000

39,000

8

- 200,000 82,000

8

(b)

If

the five projects are mutually ex-

clusive alternatives, perform the

present worth analysis and select

the best alternative.

12.6 Work

Problem 12.5(a), using a spread-

sheet.

12.7 The engineering department at General

Tire has a total

of

$900,000 for no more

than two projects in capital improvement

for the year.

Use a spreadsheet-based

PW

analysis and a minimum 12% per year

return to answer the following.

Project

A

B

C

(a) Which projects are acceptable from

the three described below?

(b) What is the minimum required an-

nual net cash flow necessary to se-

lect the bundle that expends as

much as possible without violating

either the budget limit or the two-

project maximum restriction?

Estimated

Initial

NCF,

Life,

Salvage

Investment,

$ $/year Years

Value, $

-400,000

120,000 4 40,000

- 200,000 90,000

4 30,000

-700,000

200,000 4 20,000

12.8 Jesse wants to choose exactly two inde-

pendent projects from four opportunities.

438

CHAPTER

12

Selection from Independent Projects Under Budget Limitation

Each project has an initial investment

of

$300,000 and a life

of

5 years.

The

an-

nual NCF estimates for the first three

projects are available, but a detailed esti-

mate for the fourth

is

not yet prepared

and time has run out for the selection.

Using MARR = 9% per year, determine

the minimum NCF for the fourth project

(Z) that will guarantee that it

is

part

of

the

selected twosome.

Project

w

X

Y

Z

Annual NCF, $/year

90,000

50,000

130,000

at least 50,000

12.9

The

engineer at Clean Water Engineering

has established a capital investment limit

of

$800,000 for next year for projects

that target improved recovery

of

highly

brackish groundwater.

Select any or all

of

the following projects, using a

MARR

of

10

% per year. Present your solution by

hand calculations, not Excel.

Initial Annual

Life,

Salvage

Project Investment, $ NCF, $/Year Years Value, $

A

B

C

- 250,000

- 300,000

- 550,000

50,000

90,000

150

,000

4 45.000

4 - 10,000

4 100,000

12.

10

Develop an Excel spreadsheet for the

three projects

in

Problem 12.9. Assume

that the engineer wants project C to be

the only one selected. Considering the

viable project options and

b = $800,000,

determine (a) the largest initial invest-

ment for C and

(b) the largest

MARR

allowed to guarantee that C

is

selected.

12.

ll

Eight projects are available for selection

at HumVee Motors.

The

listed

PW

val-

ues are determined at the corporate

MARR

of

10

% per year and rounded to

the nearest

$1000. Project

lives vary

from 5 to

15

years.

Initial

PW

value

Project

Investment,

$

at

10%, $

- 1,500,000

- 50,000

2

-300

,000

+35

,000

. 3

-95,000

- 9,000

4

- 400,000 + 75,000

5

-195

,000 +

125

,000

6

-175,000

-27,000

7

-100,000

+62,000

8

-400,000

+ 110,000

Project selection guidelines:

1.

No

more than $400,000 in invest-

ment capital

is

available.

2.

No

negative

PW

project may be

selected.

3.

At

least one project, but no more

than three, must be selected.

4.

The

following selection restrictions

apply to specific projects:

• Project 4 can be selected only if

project 1

is

selected.

• Projects 1 and 2 are duplicative;

don't

select both.

• Projects 8 and 4 are also

duplicative.

• Project 7 requires that project 2

also be selected.

(a) Identify the viable project bun-

dles and select the best econom-

ically justified projects. What

is

the investment assumption for

any remaining capital funds?

(b)

If

as much

of

the $400,000 as

possible

must

be invested, use

the same restrictions and deter-

mine the project(s) to select. Is

this a viable second choice for

investing the

$400,000? Why?

12.12

Use the analysis below

of

five indepen-

dent projects to select the best, if the cap-

itallimitation is

(a) $30,000, (b) $60,000,

and (c) unlimited.

Initial Life, PW

at

12%

Project

Investment,

$

Years

per

Year, $

S

- 15,000

6

8,540

A

- 25,000

8

12,325

M

- 10,000

6 3,000

E

- 25,000

4

10

H

- 40,000

12

15

,350

1

2.

13 The independent project estimates below

have been developed by the engineering

and finance managers. The corporate

MARR

is

15

% per year, and the capital

investment limit is $4 million.

Project

2

3

4

(a) Use the

PW

method and hand solu-

tion to select the economically best

projects.

(b) Use the

PW

method and computer

solution to select the economically

best projects.

Project

Cost,

Life,

NCF,

$ Millions

Years

$lYear

-

1.5

8

360,000

- 3.0

10

600,000

-

1.8

5 520,000

- 2.0

4

820,000

1

2.

14 The following capital rationing problem

is defined. Three projects are to be evalu-

ated at a MARR

of

12.5% per year. No

more than $3.0 million can be invested.

(a) Use a spreadsheet to select from the

independent projects.

(b) Use SOLVER to determine the

minimum year 1 NCF for project

3 alone to have the same PW as the

best bundle in part (a)

if

project 3

life can be increased to 10 years for

the same

$1

million investment. All

other estimates remain the same.

With this increased NCF and life,

what are the best projects for in-

vestment?

PROBLEMS

439

Estimated

NCF,

$/Year

Investment,

Life,

Gradient

Project

$ Millions Years

Year 1

after

Year 1

-0.9

6

250,000 - 5000

2 -

2.1

10

485,000

+5000

3

-

1.0

5 200,000 +

10

%

1

2.

15

Use the PW method to evaluate four in-

dependent projects. Select as many as

three

of

the four projects. The MARR

is

12

% per year, and an available capital

investment limit is $16,000.

Project

1 2

3 4

Investment,

$

- 5000

-8000

- 9000 - 10,000

Life,

years

5 5 3

4

Year NCF

Estimates,

$

1

1000

500 5000

0

2 1700

500 5000

0

3 2400

500

2000

0

4

3000

500

17,000

5 3800 10,500

12

.

16

Work Problem 12.15, using a spreadsheet.

1

2.

17

Using the NCF estimates

in

Problem

12.15 for projects 3 and 4, demonstrate

the reinvestment assumption made when

the capital budgeting problem is solved

for the four projects by using the

PW

method. (Hint: Refer to Equation [12.2].)

Linear Programming

and

Capital Budgeting

12

.18 Formulate the linear programming model,

develop a spreadsheet, and solve the

capital rationing problem in Example

12.1

(a) as presented and (b) using

an

investment limit

of

$13 million.

12

.

19

For Problem 12.5, use Excel and

SOLVER to (a) answer the question

in

440

CHAPTER

12

Selection from Independent Projects Under Budget Limitation

part (a) and (b) select the projects

if

MARR = 12% per year and the invest-

ment limit

is

increased

to

$500,000.

12

.20 Use SOLVER

to

work Problem 12.10.

12.21

Use SOLVER

to

find the minimum NCF

required for project Z

as

detailed

by

Jesse

in

Problem 12.8.

12.22

Use linear programmjng and a

spreadsheet-based solution technique

to

select from the independent unequal-life

projects

in

Problem 12.13.

CASE STUDY

12.23 Solve the capital budgeting problem

in

Problem 12.14(a), using the linear pro-

gramming model and Excel.

12

.24 Solve the capital budgeting problem

in

Problem 12.15, using the ljnear program-

mjng model and Excel.

12.25

Using the data in Problem 12.15 and

Excel solutions

of

the capital rationing

problem for capital budget limjts ranging

from b = $ 5000

to

b = $25,000, develop

an Excel chart that plots

b versus the

value

of

Z.

LIFELONG ENGINEERING EDUCATION IN A WEB ENVIRONMENT

The Report

IME

is

a not-for-profit engineer

in

g professional society,

headquartered

in

New York City with offices in several

international sites. A task force was established last

year with the charge to recommend ways to improve

services to members

in

the area

of

lifelong learning.

Overall sales

to

individuals, libraries, a

nd

businesses

of

technical journals, magazines, books, monographs,

CDs, and videos have decreased by 35% over the last

3 years. IME,

li

ke virtually a

ll

for-profit corporations,

is

being negatively impacted bye-commerce. The just-

published repOlt

of

the task force contains the following

conclusion and recommendations:

It

is

essential that IME take rapid, proactive steps to

initiate web-based learning materials itself and/or in

conjunction with other organizations. Topically, these

materials should concentrate on areas such as:

Professional engineer certification and licensing.

Leading-edge technical topics.

Retooling topics for mature engineers.

Basic tools for individuals doing engineering

ana

ly

sis with

in

adequate training

or

education.

Projects should be started immediately and evalu-

ated over the next 3 years to determine future direc-

tions

of

electronic learning materials for IME.

The Project Proposals

In

the Action Items section

of

the report, four projects

are identified, along with cost and net revenue estimates

made on a 6-month basis. The project summaries that

follow all require development and marketing

of

online

learning materials.

Project

A,

niche markets.

!ME

identifies several

new technical areas and offers Ieanling materi-

als to members and nonmembers.

An

initial in-

vestment

of

$500,000 and a follow-up invest-

ment

of

another $500,000 after

18

months are

necessary.

Project B, partnering. IME joins with several other

professional societies to offer materials on a rel-

atively wide spectrum. This business strategy

could bring a larger investment to bear on life-

long learning materials.

An

initial investment

by

IME

of

$2 million is necessary. This project

will require that a smaller project for network

improvement

be

undertaken. This

is

project C,

which foHows.

Project C, web search engin

e.

With

an

in

vestment

of

only $200,000 six months from now, 1ME

can offer me

mb

ers a web search engine for ac-

cess

to

current publications

of

IME.

An

outside

contractor can qui

ck

ly

install this capability on

current equipment. This entry point to web-

based learn

in

g is a stop-gap measure, which

may

in

crease services a

nd

revenue over the

short-term only. This project is necessary if

project B is pursued, but project C can be pur-

sued separately from any other project.

Project

D,

service improvement. This project

is

a complete substitute for project B. This

is

a

longer-term effort to improve

th

e electronic pub-

li

cation and continuing education offerings

of

lME. Investments

of

$300,000 now with com-

mitments

of

$400,000

in

6 months and another

$300,000 after 6 more months will be necessary.

Project D

is

slower-moving, but it will develop a

firm

base for most future web-based learning

services

of

the IME.

The estimated net cash flows (in $1

000) by 6-month

period for IME are summarized

as

s

ho

wn.

Project

Period

A B

C

0

$

0

$ 500

$ 0 $100

2

100 500 50 200

3 200 600 100 300

4 400 700 150

300

5 400

800 0 300

6 0 1000 0 300

CASE STUDY

441

The Finance Committee has responded that no more

that $3.5 million can be committed to these projects.

It also stated that the total amount per project should

be committed up-front, regardless

of

when the

in

itial

and follow-on investment cash flows actually occ

ur.

The Finance Committee and a Board Committ

ee

will

review progress each 3 months to determine

if

the

selected projects should be continued, expanded,

or

discontinued. The 1ME capital, primarily in equity

investments, has returned

an

average

of

10% per

6-months over the last 5 years. There is

no

debt liabil-

ity carried by 1ME at this time.

Case Study Exercises

1.

Formulate all the investment opportunities for

1ME and the cash flow profiles, given the infor-

mation

in

the task force report.

2. What projec

ts

should the Finance Committee

recommend on a purely economic basis?

3.

The Executive Director

of

1ME has great interest

in pursuing project D because

of

its perceived

positive, longer-lasting effects upon the member-

ship size

of

the Institute and future services of-

fered to new and current members.

Using a

spreadsheet that details the project net cash flow

estimates, determine some

of

the changes that the

director may make to ensure that project D is ac-

cepted. No restrictions should be placed on this

analysis; for example, investments and cash flows

can be changed, and the restrictions b

et

ween

projects described

in

the task force report can be

removed.

1

UJ

I-

I

u

Breakeven Analysis

Breakeven analysis

is

performed

to

determine

the

value

of

a variable

or

parameter

of

a

project

or

alternative

that

makes

two

elements

equal,

for

example,

the

sales

volume

that

will

equate

revenues

and

costs. A breakeven

study

is

performed

for

two

alternatives

to

determine

when

either

alternative

is

equally

acceptable,

for

example,

the

replacement

value

of

the

defender

in

a

replacement

study

that

makes

the

challenger

an

equally

good

choice

(Section

11

.

3).

Breakeven analysis

is

commonly

applied

in make-or-buy deci-

sions

when

corporations

and

businesses

must

decide

upon

the

source

for

manufactured

components,

services

of

all kinds,

etc

.

We

have

utilized

the

breakeven

approach

previously in

payback

analysis

(Section 5.6)

and

for

breakeven

ROR

analysis

oftwo

alternatives (Section 8.4).

The

Excel

optimizing

tool

SOLVER,

introduced

and

used

most

recently

in

Chapter

12

to

select

from

independent

projects,

is

a

prime

tool

used

to

per-

form

a

compute

r-based breakeven analysis

between

two

alternatives. This

chapter

expands

our

scope

and

understanding

of

performing

a breakeven

study

.

Breakeven studies use estimates

that

are

considered

to

be

certain;

that

is

,

if

the

estimated

values are

expected

to

vary

enough

to

possibly

change

the

outcome

,

another

breakeven

study

is

necessary using

different

estimates.

This

leads

to

the

observation

that

breakeven analysis

is

a

part

of

the

larger

efforts

of

sensitivity analysis.

If

the

variable

of

interest

in a breakeven

study

is

allowed

to

vary,

the

approaches

of

sensitivity analysis

(Chapter

18)

should

be

used.

Additionally,

if

probability

and

risk assessment are

considered,

the

tools

of

sim

ulation

(Chapter

19) can

be

used

to

supplement

the

static

nature

of

a breakeven

study

.

This chapter's case

study

focuses

on

cost

and

efficiency measures in a

pub-

lic

sector

(municipal)

setting

.

LEARNING OBJECTIVES

Purpose: For one or more alternatives, determine the level

of

activity necessary

or

the

value

of

a parameter

to

break even.

Breakeven

point

Two alternative breakeven

Spreadsheets

This

chapter

will

help

you:

1.

Determine

the

breakeven value

for

a single

project

.

2.

Calculate

the

breakeven value

between

two

alternatives and

use

it

to

select

one

alternat

ive.

3.

Develop

a

spreadsheet

that

uses

the

Excel

tool

SOLVER

to

perform

breakeven analysis.

444

CHAPTER

13

Breakeven Analysis

13.1 BREAKEVEN ANALYSIS FOR A SINGLE PROJECT

When one

of

the engineering economy

symbols-P,

F, A,

i,

or

n-is

not known

or not estimated, a breakeven quantity can be determined by setting an equiva-

lence relation for

PW

or

AW

equal to zero. This form

of

breakeven analysis has

been used many times so far. For example, we have solved for the rate

of

return

i*, found the payback period nfl' and determined the P, F, A, or salvage value S

at which a series

of

cash flow estimates return a specific MARR. Methods used

to determine the quantity are

Direct solution by hand

if

only one factor is present (say, P / A)

or

only single

amounts are estimated (for example,

P and

F)

.

Trial and error by hand when multiple factors are present.

Computer spreadsheet when cash flow and other estimates are entered into

spreadsheet cells and used in resident functions, such as

PV,

FV,

RATE,

IRR,

NPV, PMT, and NPER.

We

now concentrate on the determination

of

the breakeven quantity

for

a

decision variable. For example, the variable may be a design element to mini-

mize cost, or the production level needed to realize revenues that exceed costs by

10

%.

This quantity, called the breakeven point

QB

E'

is determined using relations

for revenue and cost at different values

of

the variable

Q.

The size

of

Q may be

expressed

in

units per year, percentage

of

capacity, hours per month, and many

other dimensions.

Figure

13-1a

presents different shapes

of

a revenue relation identified as

R.

A linear revenue relation

is

commonly assumed, but a nonlinear relation

is

often

more realistic. It can model an increasing per unit revenue with larger volumes

(curve J

in

Figure

13-la)

, or a decreasing per unit price that usually prevails at

higher quantities (curve 2).

Costs, which may be linear or nonlinear, usually include two

components-

fixed and

variable-as

indicated in Figure 13-1b.

Fixed costs (FC). Includes costs such as buildings, insurance, fixed over-

head, some minimum level

of

labor, equipment capital recovery, and infor-

mation systems.

Variable costs

(Ve).

Includes costs such as direct labor, materials, indirect

costs, contractors, marketing, advertisement, and warranty.

The fixed cost component is essentially constant for all values

of

the variable, so it

does not vary for a large range

of

operating parameters, such as production level

or workforce size. Even

if

no units are produced, fixed costs are incurred at some

threshold level.

Of

course, this situation cannot last long before the plant must

shut down to reduce fixed costs. Fixed costs are reduced through improved

equipment, information systems and workforce utilization, less costly fringe ben-

efit packages, subcontracting specific functions, and so on.

Variable costs change with production level, workforce size, and other parame-

ters. It is usually possible to decrease variable costs through better product design,

manufacturing efficiency, improved quality and safety, and higher sales volume.