Blank L., Tarquin A. Engineering Economy (McGraw-Hill Series in Industrial Engineering and Management)

Подождите немного. Документ загружается.

SECTION 17.2 Before-Tax and After-Tax Cash Flow

it is time

to

expand our terminology. NCF is replaced by the term cash flow be-

fore taxes (CFBT),

and we introduce the new term

cashflow

after taxes (CFAT).

CFBT and CFAT are actual cash flows; that is, they represent the estimated

actual flow

of

money

in

and out

of

the corporation that will result from the alter-

native. The remainder

of

this section explains how

to

transition from before-tax

to

after-tax cash flows for solutions by hand and by computer, using income tax

rates and other pertinent tax regulations described in the next few sections.

Once the CFAT estimates

are

developed, the economic evaluation is per-

formed using the same methods

and

selection guidelines applied previ-

ously. However, the analysis is

performed

on the CFAT estimates.

The annual CFBT estimate must include the initial capital investment and sal-

vage value for the years in which they occur. Incorporating the definitions

of

gross income and operating expenses, CFBT for any year is defined

as

CFBT = gross income - expenses - initial investment + salvage value

=

GI

-E

- P + S

[17.7]

As

in previous chapters, P is the initial investment (usually in year 0) and S is the

estimated salvage value in year

n.

Once all taxes are estimated, the annual after-

tax cash flow

is

simply

CFAT = CFBT - taxes

[17.8]

where taxes are estimated using the relation

(TI)(T)

or

(TI)(T

e

),

as

discussed

earlier.

We

know from Equation [17.1] that depreciation D is subtracted to obtain TI.

It is very important to understand the different roles

of

depreciation for income

tax computations and in

CFAT

estimation.

Depreciation

is

a noncash

flow.

Depreciation is tax-deductible for deter-

mining the

amount

of

income taxes only,

but

it

does not represent a di-

rect, after-tax cash flow to the corporation. Therefore, the after-tax engi-

neering economy study must be based on actual cash flow estimates,

that

is,

annual

CFAT estimates

that

do not include depreciation as a negative

cash

flow.

Accordingly, if the

CFAT

expression is determined using the TI relation, depre-

ciation must not be included outside

of

the TI component. Equations [17.

7]

and

[17.8] are now combined

as

CFAT =

GI

- E - P + S - (GI - E -

D)(T

e) [17.9]

Suggested table column headings for CFBT and

CFAT

calculations by hand or

by

computer are shown

in

Table 17-3. The equations are shown in column num-

bers, with the effective tax rate

Te

used for income taxes. Expenses E and initial

investment

P will be negative values.

The TI value in some years may be negative due

to

a depreciation amount

that is larger than (GI -

E). It is possible

to

account for this in a detailed after-

tax analysis using carry-forward and carry-back rules for operating losses.

It

is

the exception that the engineering economy study will consider this level

of

575

576

CHAPTER 17 After-Tax Economic Analysis

TABLE

17-3

Table Column H

ead

in

gs

for Calculation

of

(({)

CFBT

and

(Ii)

CFAT

(a)

CFBT

table

head

i

ng

s

Gros

s

Ope

r

at

i

ng

Investment P

Income

Expenses

and

Salvage

Year GI

E

5

CFBT

(4) =

(1

)

(2) (3)

(1) +

(2)

+

(3)

(b)

CFAT

table

headings

Year

Gross

Operating

Investment

P Taxable

Income

GI

(1

)

~

E-Sol

ve

Expenses

and

Salvage

Depreciat

i

on

Income Tax

es

E 5

D

TI

(TI)(T

e

)

C

FAT

(7) =

(5) =

(1

) + (2) +

(2)

(3)

(4)

(1) + (2) - (4)

(6)

(3)

-

(6)

detail. Rather, the associated negative

in

come tax is considered as a

ta

x savings

for the

year.

The assumption is that

th

e negative tax will offset taxes for the same

year in other income-producing areas

of

the corporation.

TransAmerica

In

surance

ex

pects to initiate a new outreach service next yea

r.

Sma

ll

facili-

ties will be constructed

in

about 35 high-risk c

iti

es across the continen

t.

Company person-

nel from

th

e area will offer training and consulting services to the citizens and officials

of

the cities and counties in fire avoidance, theft deterrence, and similar topics. Current a

nd

prospective customers will be invited

to

visit the facility. Each facility is expected

to

cost

$550,000 initially with a resale (sa

lv

age) value

of

$150,000 after 6 year

s-

th

e time period

for which the TransAmerica Board

of

Directors approved this activity. MACRS deprecia-

ti

on allows a 5-year recovery period. A team

of

safety engineers, actuaries, and

fi

nancial

personnel estimate bottom-line results at

an

nu

al net increases to the corporation

of

$200,000

in

revenue and $90,000

in

costs. Us

in

g an effective tax rate

of

35

%,

tabulate the

CFBT and CFAT estimates.

Solution

by

Hand

and

by

Computer

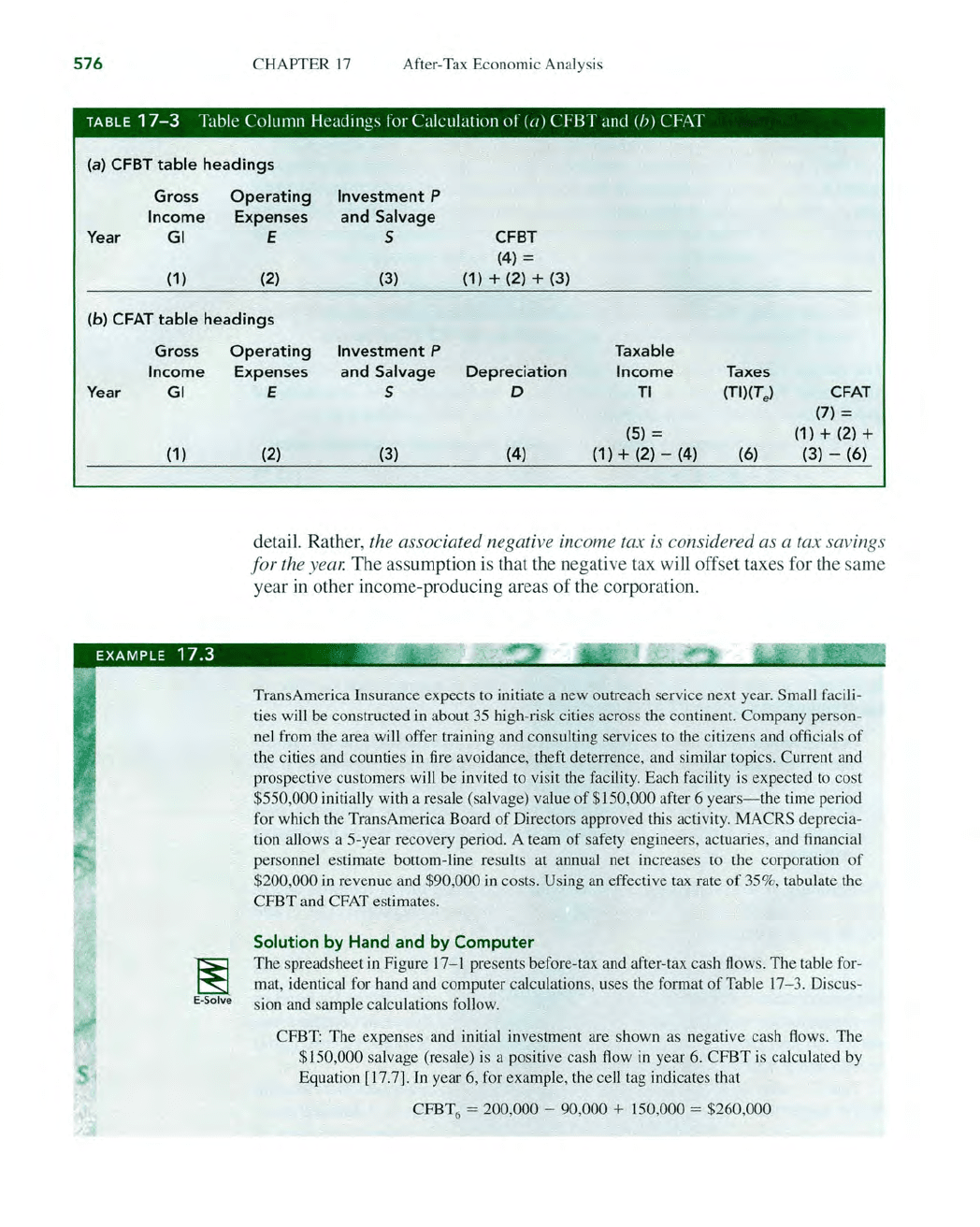

The spreadsheet

in

Figure

17

- 1 presents before-tax and after-tax cash flows. The table for-

ma

t,

id

en

ti

cal for hand and computer calc

ul

ation

s,

uses the format

of

Table

17

-3.

Di

scus-

sion and sample calculations foll

ow.

CFBT: The

ex

penses and initial investment are shown

as

negative cash

flow

s.

The

$150,000 salvage (resale) is a positive cash

flow

in

year

6.

CFBT is calculated

by

Equation [17

.7

].

In

year

6,

for example, the cell tag indicates that

CFBT

6

= 200,000 - 90,000 + 150,000 = $260,000

SECTION 17.2 Before-Tax and After-Tax Cash Flow

X Microsoll EHcel - EHample 17.3

Ii!!III'.ii1D

Ye

ar

o

1

2

3

GI

Figure 17-1

Computation

of

CFBT and CFAT using MACRS depreciation and a 35% effective tax rate, Example

17

.3.

CFAT:

Column E for MACRS depreciation (rates in Table 16-2 for n = 5) over the

6-year period writes off the entire

$550,000 investment. Taxable income, taxes, and

CFAT,

illustrated

in

the cell tags for year 4, are computed

as

TI4 = GI - E - D = 200,000 - 90,000 - 63,360 = $46,640

Taxes

= (TI)(0.35) = (46,640)(0.35) = $16,324

CFAT

4

=

Gl

- E - taxes = 200,000 - 90,000 - 16,324 = $93,676

In

year 2, MACRS depreciation

is

large enough

to

cause TI to

be

negative

($-66,000).

As

mentioned above, the negative tax

($-23,100)

is

considered a tax savings

in

year 2, thus increasing

CFAT.

Comment

MACRS depreciates

to

a salvage value

of

S =

O.

Later we will learn about a

tax

implica-

tion due

to

"recapturing

of

depreciation" when an asset is sold for

an

amount larger than

zero, and

MACRS was applied

to

fully depreciate the asset

to

zero.

577

578

CHAPTER

17

After-Tax Economic Analysis

17.3

EFFECT

ON

TAXES

OF DIFFERENT DEPRECIATION

METHODS

AND

RECOVERY PERIODS

Although MACRS is the required tax depreciation method in the United States, it is

important to understand why accelerated depreciation rates give the corporation a

tax advantage relative to the straight line method with the same recovery period.

Larger rates in earlier years

of

the recovery period require less taxes due to the larger

reductions in taxable income. The criterion

of

minimizing the prese

nt

worth a

/ta

xes

is used to demonstrate the tax effect. That is, for the recovery period n, choose the

depreciation rates that result in the minimum present worth value for taxes.

I=n

PW

tax = I (taxes in

year

t)(P

/ F

,i

,

t)

[17.10]

1=1

This is equivalent to maximizing the present worth

of

total depreciation PW D'

in

Equation [16A.S].

Compare any two different depreciation models. Assume the following:

(1) There is a constant single-value tax rate, (2) CFBT exceeds the annual depre-

ciation amount,

(3) the method reduces book value to the same salvage value,

and (4) the same recovery period is used.

On the basis

of

these assumptions, the

following are correct:

1. The total taxes paid

are

equal for all depreciation models.

2.

The present worth

of

taxes

is

less for accelerated depreciation methods.

As we learned in Chapter 16, MACRS

is

the prescribed tax depreciation model

in the United States, and the only alternative is MACRS straight line depreciation

with an extended recovery period.

The

accelerated write-off

of

MACRS always

provides a smaller

PW

l

ax

compared to less accelerated models.

If

the DDB model

were still allowed directly, rather than embedded in MACRS, DDB would not

fare as well as MACRS. This is because DDB does not reduce the book value to

zero. This is illustrated in Example 17.4.

An

after-tax analysis for a new $50,000 machine proposed for a fiber optics manufac-

turi

ng

line is in process. The CFBT for the machine is estimated at $20,000.

If

a recov-

ery period

of

5 years applies, use the present-worth-of-taxes criterion,

an

effective tax

rate

of

35%, and a return

of

8% per year

to

compare the

fo

ll

owing: classical straight

line, classical DDB, and required MACRS depreciation.

Use a 6-year period for the

comparison to accommodate the half-year convention imposed

by

MACRS.

Solution

Table

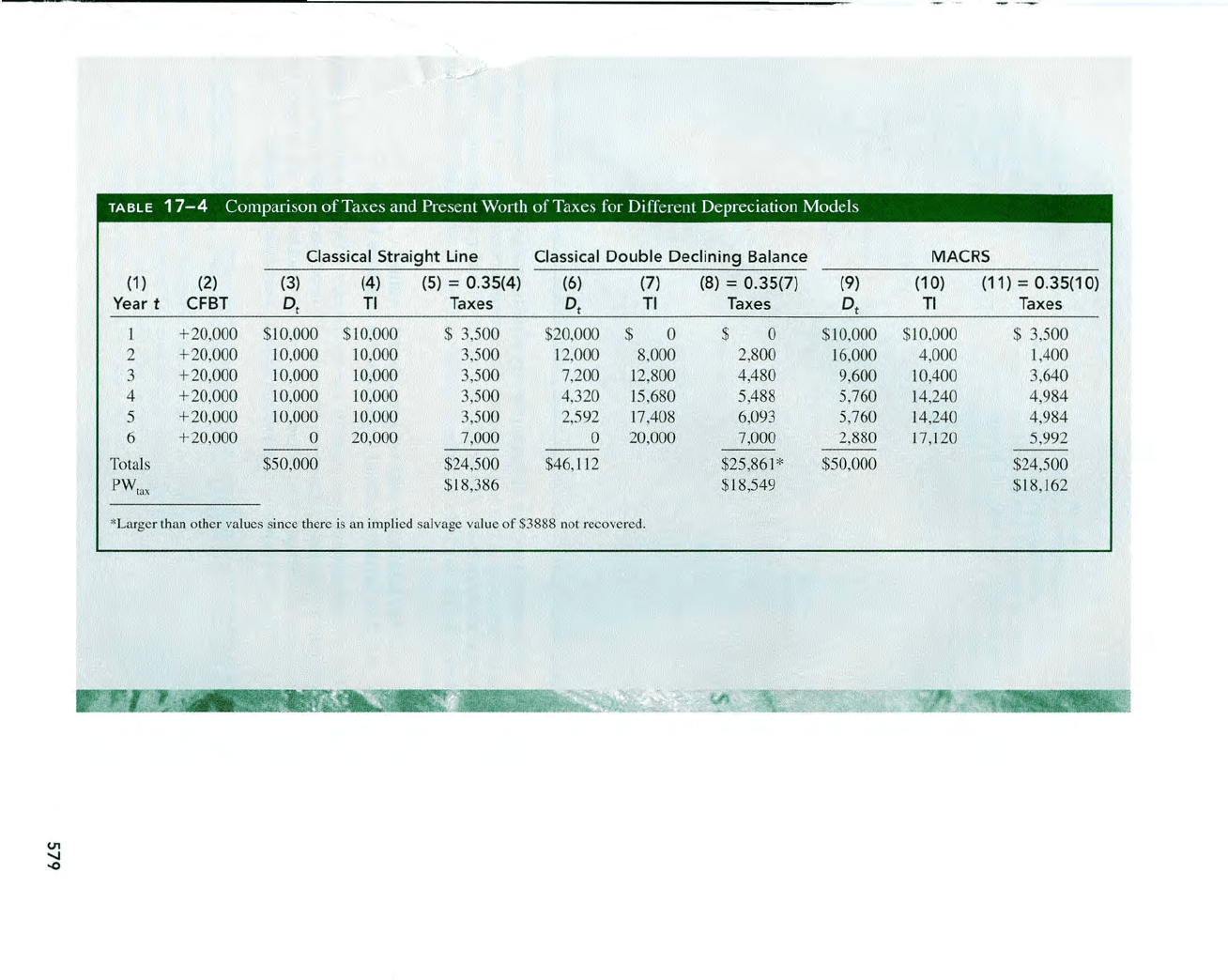

17--4

presents a summary

of

annual depreciation, taxable income, and taxes for

each model. For classical straight line depreciation with

n = 5,

D{

= $10,000 for 5 years

and

D6

= 0 (column 3). The CFBT

of

$20,000

is

fully taxed at 35%

in

year

6.

The classical DDB percentage

of

d = 2/ n = 0.40

is

applied for 5 years. The implied

salvage value

is

$50,000 - 46,112 = $3888, so not all $50,000 is tax deductible. The

taxes using classical DDB would be $3888 (0.35)

= $1361 larger than for the classical

SLmodel.

(J1

'-I

-0

Classi

cal

Straight Line Class

ic

al

Double

Declining

Ba

lan

ce

(1 )

(2)

(3) (4)

(5)

= 0.

35(4

)

(6)

(7)

(8)

=

0.35(7

)

Year t CFBT D

t

TI Taxes

D

t

TI

Taxes

+20,000 $10,000 $10,000 $ 3,500 $20,000

$ 0

$

0

2 + 20,000

10

,000 10,000 3,500

12

,000

8,000

2,800

3

+ 20,000

10

,000

10

,000 3,500 7,200

12

,8

00

4,480

4 + 20,000

10

,000 10,000 3,500 4

,3

20

15

,68

0

5,488

5

+2

0,000 10,000 10,000 3,500

2,592

17

,4

08

6,093

6

+2

0,000

0

20,000

7,000

0

20,000

7,000

Totals $50,000 $24,500 $46,

Jl2

$25,861*

PW,

ax

$18,386

$18,549

*Larger than other values since there is an implied salvage val

ue

of

$3888 not recovered.

MACRS

(

9)

(10)

(11) = 0.

35(10)

D

t

TI Taxes

$10,000

$10,000

$ 3,500

16

,000 4,000

1,400

9,600

10

,400

3,640

5,760 14,240

4,984

5,760 14,240 4,984

2,880

17

,120 5,992

$50,000

$24,500

$]8,162

580

CHAPTER

17

After-Tax Economic Analysis

MACRS writes off the $50,000

in

6 years using the rates

of

Table

16

-

2.

Total taxes

are

$24,500, the same as for classical SL depreciation.

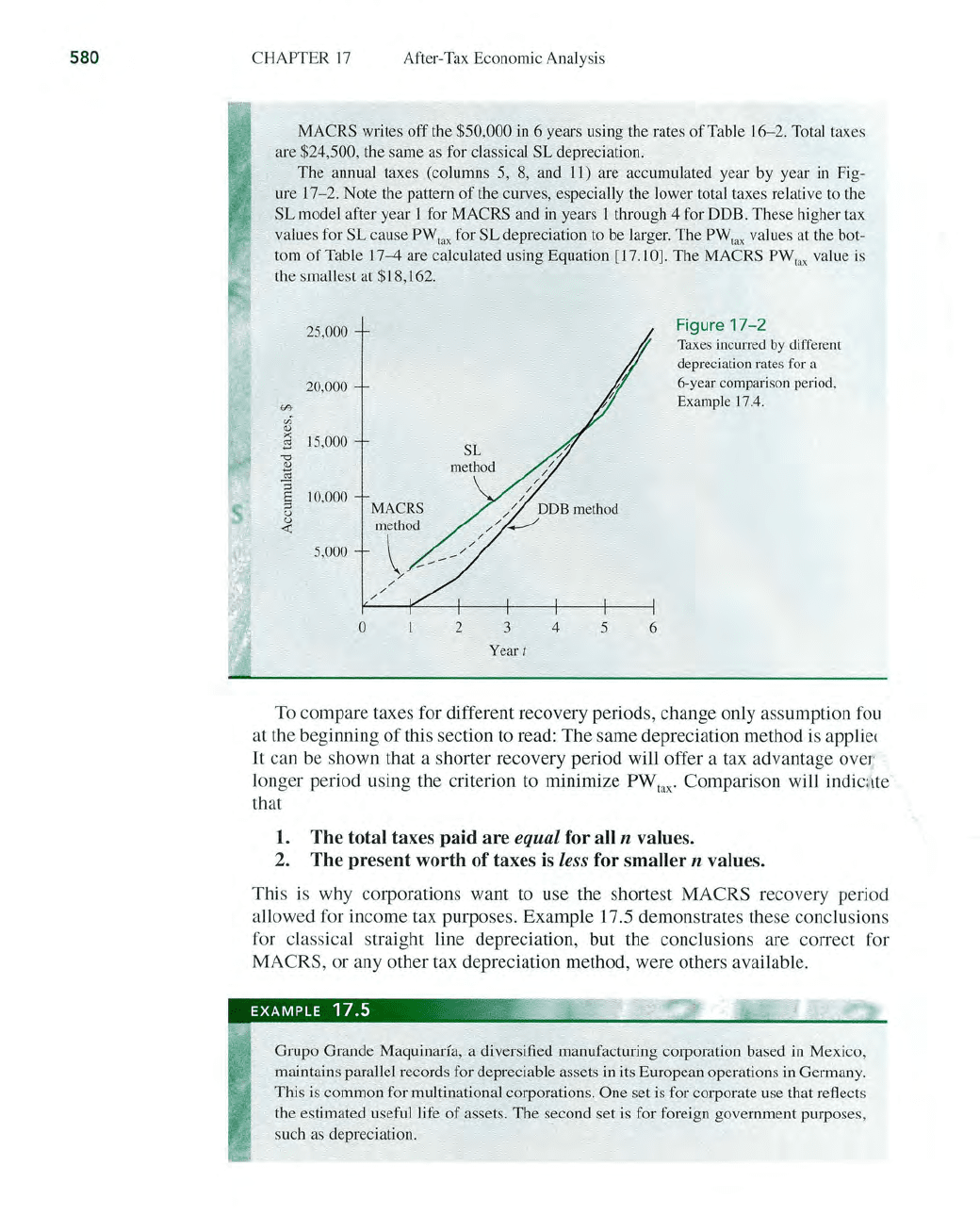

The annual taxes (columns 5,

8,

and

11)

are accumulated year by year

in

Fig-

ure

17

-2.

Note the pattern

of

the curves, especially the lower total taxes relative to

th

e

SL model after year 1 for MACRS and

in

years 1 through 4 for

DDB

. These higher tax

values for SL cause

PW

tax

for SL depreciation to be larger. The PW

tax

values at the bot-

tom

of

Table

17-4

are calculated using Equation [17.10]. The MACRS PW

tax

value

is

the smallest at $18,162.

25,000

20,000

""

vl

<t.)

x

15,000

B

-0

~

OJ

0;

E

10,000

;:t

u

u

-0::

5,000

0

MACRS

method

\

/

/

/

SL

method

2

3

Year t

4

5 6

Figure

17-2

Taxes incurred by different

depreciation rates for a

6-year comparison period,

Example 17.4.

To

compare taxes for different recovery periods, change only assumption

fou

at the beginning

of

this section to read: The same depreciation method is applie(

It

can be shown that a shorter recovery period will offer a tax advantage over

longer period using the criterion to minimize

PW

tax

'

Comparison will indic.

lte

that

1.

The total taxes paid are equal for all n values.

2. The present worth

of

taxes is less for smaller n values.

This is why corporations want

to

use the shortest MACRS recovery period

allowed for income tax purposes. Example 17.5 demonstrates these conclusions

for classical straight line depreciation, but the conclusions are correct for

MACRS, or any other tax depreciation method, were others available.

Grupo Grande Maquinarfa, a diversified manufacturing corporation based

in

Mexico,

maintains parallel records for depreciable assets

in

its European operations

in

Germany.

This

is

common for multinational corporations. One set is for corporate use that reflects

the estimated useful life of assets. The second set is for foreign government purposes,

such as depreciation.

SECTION 17.4 Depreciation Recapture and Capital Gains (Losses)

The company just purchased an asset for

$90,000 with an estimated useful life

of

9 years; however, a shorter recovery period

of

5 years is allowed by German tax law.

Demonstrate the

tax

advantage for the smaller n

if

(GI -

E)

= $30,000 per year, an

effective tax rate

of

35% applies, invested money is returning 5% per year after taxes,

and classical SL depreciation

is

allowed. Neglect the effect

of

any salvage value.

Solution

Determine the annual taxes

by

Equations [17.1] and [17.2], and the present worth

of

taxes using Equation [17.10) for both n values.

Useful life

n = 9 years:

D = 90,000 = $10 000

9 '

TI = 30,000 - 10,000 = $20,000 per year

Taxes

= 20,000(0.35) = $7000 per year

PW

ta

x

= 7000(P/A,5%,9) = $49,755

Total taxes

= 7000(9) = $63,000

Recovery period n = 5 years:

Use the same comparison period

of

9 years, but depreciation occurs only during the first

5 years.

{

90,000

= $18,000

D = 5

I

o

t = 1 to 5

t = 6 to 9

T - {(30,000 -

18

,000)(0.35) = $4200

axes - (30,000)(0.35) = $10,500

t = 1 to 5

t = 6 to 9

PW

tax

= 4200(P / A,5%,5) + 1O,500(P /

A,5%,4)(P/

F,5%,5)

= $47,356

Total taxes

= 4200(5) + 10,500(4) = $63,000

A total

of

$63,000 in taxes

is

paid in both cases. However, the more rapid write-off for

n = 5 results

in

a present worth tax savings

of

nearly $2400 ($49,755 - 47,356).

17.4

DEPRECIATION RECAPTURE

AND

CAPITAL GAINS

(LOSSES):

for

corporations

All the tax implications discussed here are the result

of

disposing

of

a deprecia-

ble asset before, at, or after its recovery period. In an after-tax economic analysis

of

large investment assets, these tax effects should be considered. The key is the

size

of

the selling price (or salvage or market value) relative to the book value at

disposal time, and relative

to

the first cost. There are three relevant terms.

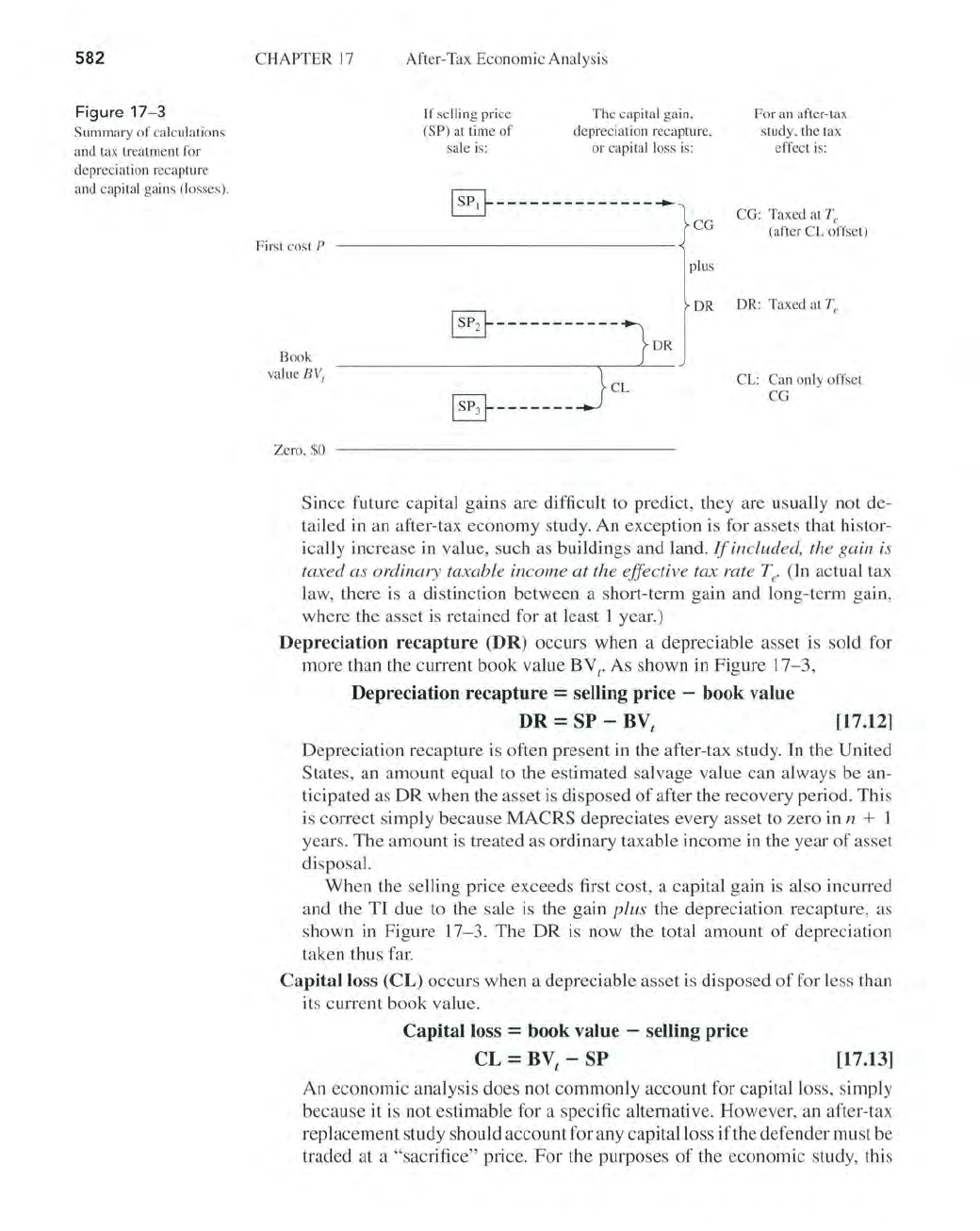

Capital

gain (CG)

is

an amount incurred when the selling price exceeds its

first cost. See Figure

17

- 3. At the time

of

asset disposal,

Capital

gain

= selling

price

- first cost

CG

=

SP

- P

[17.11]

581

582

Fi

gur

e 17

-3

Summ

ary of c

al

culations

and tax treatment for

depr

ec

iation recapture

and capital gains (losses).

CHAPTER

17

First cost P

Book

value

BV,

Ze

ro, $0

After-Tax

Economic

Analysis

If selling pri

ce

(

SP

) at time

of

sale is:

Th

e capital gain,

depr

ec

iation re

capture

,

or

capital loss is:

~--------------~

CG

plus

DR

For an after-tax

study, the tax

effect is:

CG: Taxed

at

Te

(after

CL

off

set)

DR: Taxed at

Te

CL: Can only offset

CG

Since

future capital gains are difficult to predict, they are usually not de-

tailed

in

an after-tax

economy

study. An exception is for assets that histor-

ically increase in value, such as buildings and land.

If

included,

th

e gain is

ta

xe

d as ordinary taxable inc

om

e

at

the effective tax rate Te' (In actual tax

law, there

is

a distinction between a short-term gain and long-term gain,

where the asset

is

retained for at least 1 year.)

Depreciation

recapture

(DR) occurs when a depreciable asset is sold for

more than the current

book

value

BY

r

As

shown

in

Figure

17

- 3,

Depreciation

recapture

= selling price - book value

DR

= SP - BV

t

[17.12]

Depreciation recapture is often present

in

the after-tax study. In the United

States, an

amount

equal to the estimated salvage value can always be an-

ticipated as DR when the asset is disposed

of

after the recovery period. This

is correct simply because

MACRS

depreciates every asset to zero

in

It

+ I

years.

The

amount is treated as ordinary taxable

income

in

the year

of

asset

di

sposal.

When the selling price exceeds first cost, a capital gain is also incurred

and the TI due to the sale is the gain plus the depreciation recapture, as

shown

in

Figure 17-3.

The

DR

is

now the total amount

of

depreciation

taken thus far.

Capital loss (CL) occurs when a depreciable asset is disposed

of

for less than

it

s current book value.

Capital

loss = book value - selling price

CL

= BV

t

-

SP

[17.13]

An economic analysis does not commonly account for capital loss, simply

because it is not estimable for a specific alternative.

However

, an after-tax

replacement study should account for any capital loss

if

the defender must be

traded at a "sacrifice" price.

For

the purposes

of

the economic study, this

SECTION 17.4

Depreciati

on

Recapture and Capital Gains (Losses)

provides a tax savings in the year

of

replacement. Use the effecti ve tax rate to

esti mate

th

e tax savings. These savings are assumed to be offset elsewhere in

th

e corporation

by

other income-producing assets that generate taxes.

Most depreciable corporate assets are retained in use for more than 1 year. When

such an asset is sold, disposed of, or traded after the I-year point, the

U.S. tax con-

sideration is referred to as a

Section 1231 transaction, named after the IRS rules

section

of

the same number.

To

determine the associated TI, all capital losses

of

the

corporation are netted against all capital gains, because losses do not directly re-

duce taxes.

On the other hand, net capital gains are taxed as ordinary TI. Addition-

ally complicating the analysis may be the different tax treatment oflong-term gains

and losses (Section 1231 transaction

s)

compared to short-term dispositions. Addi-

tional considerations are special, time-limited incentives offered by government

agencies to boost capital, and possibly foreign investment, through allowances

of

increased depreciation and reduced taxes. These benefits come and go depending

on the

"health

of

the economy." Only

if

multiple-asset sales and/or exchanges are

involved in

an

alternative's after-tax study may it be necessary to include this level

of

detail. These details are usually left to the accountants and finance personnel.

(Reference to IRS Publications 334 and 544 may be

of

interest.) For most after-tax

studies, it is

sufficient

to

apply the effective tax rate

Te

to

the alternative's

TI

in the

year that the

DR

, CG, or

CL

occurs, with a tax savings generated by the CL.

Finally, it is important to realize that this description and this tax treatment are

for

corporations, not individuals. Individual taxpayers use essentially the same

calculations when they sell investments or depreciated assets, but the tax rates

vary significantly from those for corporations, especially for capital gains. Also,

tax laws and rates for individual taxpayers change more frequently. Refer to the

IRS website and publications for details.

Equation

[17.1] a

nd

the expression for

TI

in Equation [17.9] can now be

expanded to include the additional cash flow estimates for asset disposal.

TI

=

gross

income

-

expenses

-

depreciation

+

depreciation

recapture

+

capital

gain

-

capital

loss

= GI - E - D +

DR

+

CG

- CL [17.14]

EXAMPLE

17.6

'

Biotech, a medical imaging and modeling company, must purchase a bone cell analysis

system for use

by

a team

of

bioengineers and mechanical engineers studying bone density

in athletes. This particular part

of

a 3-year contract with the NBA will provide additional

gross income

of

$100,000 per year. The effective tax rate is 35%. Estimates for two alter-

natives are summarized below.

First cost, $

Operating expenses, $ per year

MACRS recovery, years

Analyzer 1

150,000

30,000

5

An

alyzer 2

225,000

10,000

5

583

584

CHAPTER

17

After-

Tax

Economic Analysis

Answer the following questions, solving by hand and

by

computer.

(a) The Biotech president, who is very tax conscious, wishes to use a criterion

of

mini-

mizing total taxes incurred over the 3 years

of

the contract. Which analyzer should

be

purchased?

(b) Assume that 3 years have now passed, and the company is about to sell the analyzer.

Using the same total tax criterion, did either analyzer have an advantage? Assume

the selling price

is

$130,000 for analyzer

J,

or $225,000 for analyzer 2, the same

as

its first cost.

Solution by Hand

(a) Table

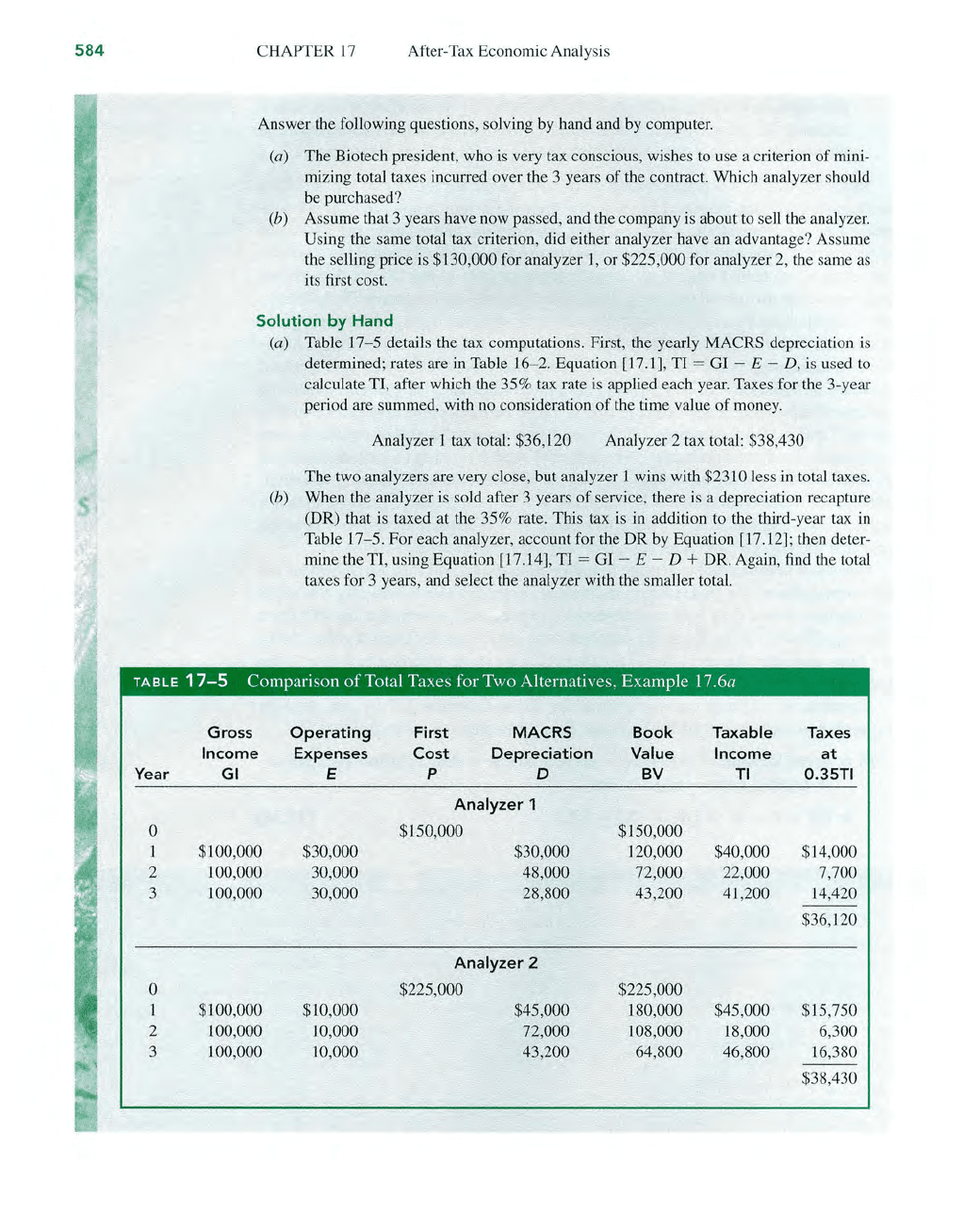

17

- 5 details the tax computations. First, the yearly MACRS depreciation is

determined; rates are in Table 16- 2. Equation [17.1], TI

=

OJ

- E - D, is used

to

calculate TI, after which the 35% tax rate is applied each year. Taxes for the 3-year

period are summed, with

no

consideration

of

the time value

of

money.

Analyzer 1 tax total: $36,120 Analyzer 2 tax total: $38,430

The two analyzers are very close, but analyzer 1 wins with $2310 less

in

total taxes.

(b) When the analyzer is sold after 3 years

of

service, there

is

a depreciation recapture

(DR) that is taxed at the 35% rate. This tax is

in

addition to the third-year tax

in

Table 17-5. For each analyzer, account for the DR by Equation [17.12];

th

en deter-

mine the TI, using Equation [17.14J, TI

=

OJ

- E - D + DR. Again,

find

the total

taxes for 3 year

s,

and select the analyzer with the smaller total.

TABLE

17-5

Comparison

of

Total Taxes for Two Alternatives, Example

17.6a

Gross

Operating

First

MACRS Book Taxable Taxes

Income

Expenses Cost Depreciation Value Income

at

Year GI E

P D

BV

TI

O.35TI

Analyzer 1

0 $150,000 $150,000

1 $100,000

$30,000

$30,000

120,000

$40,000 $14,000

2 100,000

30,000

48,000 72,000 22,000 7,700

3 100,000 30,000 28,800 43,200

41

,200

14

,4

20

$36,120

Analyzer 2

0 $225,000 $225,000

$100,000 $10,000 $45,000 180,000 $45,000

$15,750

2

100,000 10,000 72,000 108,000 18,000 6,300

3

100,000 10,000 43,200 64,800 46,800 16,380

---

$38,430