Blank L., Tarquin A. Engineering Economy (McGraw-Hill Series in Industrial Engineering and Management)

Подождите немного. Документ загружается.

SECT

ION 17.7

Af

ter-Tax Re

pl

acement Study

The proce

dur

e to

co

mpare a

lt

e

rn

a

ti

ves outlined

in

Se

ct

ion 8.6 is applie

d.

These are

r

eve

nu

e alterna

ti

ves, so

th

e overa

ll

i* values (ce

ll

s ]9 and I19) indic

at

e

th

at both CFAT

se

ri

es are accepta

bl

e. The va

lu

e

t::.i

* = 23.6% (ce

ll

J I 9)

al

so exceeds

MARR

=

1O

%, so

analyzer 2 is selecte

d.

This d

ec

ision applies the ROR method guideline:

Select

the a

lt

e

rn

a-

tive that requires

th

e largest, incrementally

ju

stified investment.

Comment

In

Sec

ti

on 8.4, Figure

8-

5b demonstrated

th

e fallacy of sel

ec

ting an alternative based

solely upon

th

e ROR.

Th

e

in

cremental ROR must be used. The same fa

ct

is demon

st

rated

in

this example.

If

the lar

ge

r i* alternative is chosen, analyzer I is

in

co

rr

ec

tl

y sel

ec

ted.

When

t::.i

* exceeds

th

e MA

RR

,

th

e larg

er

in

vestment is

conectl

y

cho

se

n

-ana

lyzer 2

in

this case. For ve

ri

fica

ti

on,

th

e PW at

10

% is

ca

lculated for

ea

ch analyzer (110 and l20).

Aga

in

, analyzer 2 is

th

e winner, based on its larger PW of $93,905.

17.7 AFTER-TAX REPLACEMENT STUDY

When a currently

in

sta

ll

ed asset (the defender) is challenged with possible re-

placement,

th

e effect of taxes can have an impact upon the decision of the

re

pl

acement stud

y.

The final decision may not be reversed by taxes, but the dif-

ference between before-tax A W va

lu

es may be significantly different from the

af

ter-tax

di

fference. There may be tax considera

ti

ons

in

the year

of

the possible

re

pl

acement due to depreciation recapture or capital gain,

or

th

ere may be tax

sav

in

gs due to a siza

bl

e capital loss, if

it

is necessary to trade the

def

ender at a

sac

rifi

ce pric

e.

Additionall

y,

th

e after-tax re

pl

acement study cons

id

ers tax-de-

ductible

de

pr

eciation and operating expenses not accounted for in a before-tax

ana

ly

si

s.

The

ef

fective tax rate Te is used to estimate the amount

of

annual taxes

(or tax sav

in

gs) from TI. The same procedure as the b

ef

or

e-tax replacement

study

in

Chapter II is applied here, but for CF

AT

estimates. The

pr

ocedure

sho

ul

d be thoroug

hl

y underst

oo

d b

ef

or

e proceedin

g.

Special attention to Sec-

tions

11

.3

and

11

.5

is recommended.

Example

17.1

2 presents a solution by hand

of

an after-tax replacement study

us

in

g a simplify

in

g assumption

of

classical

SL

(s

traight line) deprecia

ti

on. Ex-

ample

17.1

3 solves

th

e same problem by computer, but includes the deta

il

of

MACRS depreciation. This provides an opportunity to

ob

serve the differe

nc

e in

th

e AW values between

th

e two deprecia

ti

on assumptions.

EXAMPLE

17.12 "

Mid

cont

in

ent

Powe

r Autho

ri

ty purchased coal extraction equipment 3 years ago for

$600,000. Manageme

nt

has

di

scovered that it is t

ec

hn

ol

og

i

ca

ll

y outdated n

ow

. New equip-

ment has b

ee

n

id

ent

ifi

ed.

If

th

e market va

lu

e

of

$4

00

,

000

is offered as the b'ade-

in

for the

current equipment, perf

Olm

a repla

ce

ment study us

in

g (a) a before-t

ax

MARR

of 10% per

yea

r and (b) a 7% per year after-tax MARR. Assume an eff

ec

tive t

ax

rate of 34%. As a

simplify

in

g assumption, u

se

classical straight line depreciation with S = 0 for bo

th

alter-

natives.

595

Before-t

ax

replaceme

nt

596

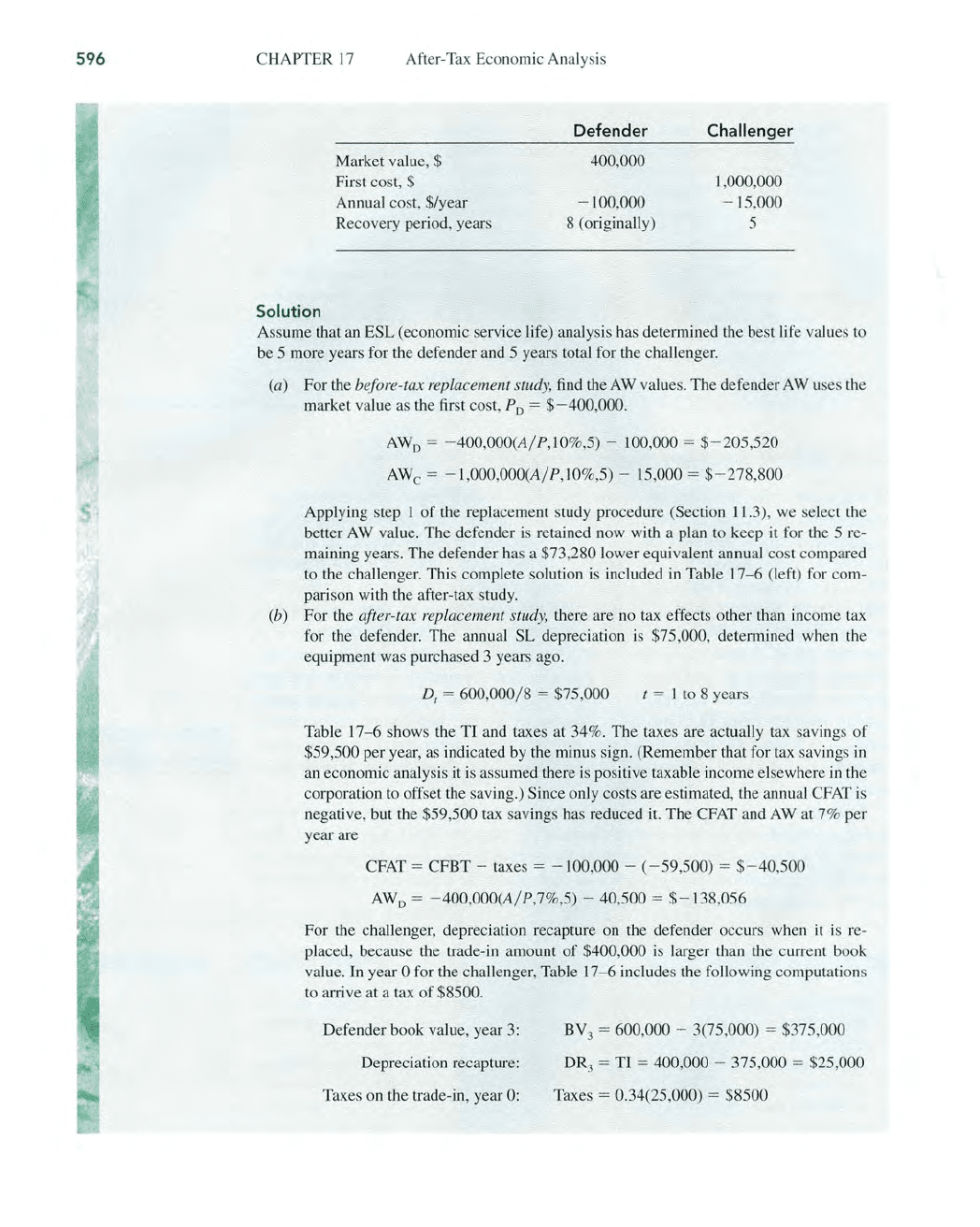

CHAPTER 17 After-Tax Econo

mi

c Analysis

Defender

Chall

enger

Market value, $

400,000

First cost, $

1,000,000

Annual cost, $/year - 100,000

-

15

,000

Recovery pe

ri

od, years 8 (originally)

5

Solution

Assume that an ESL (economic se

rvi

ce life) analysis

ha

s determined

th

e best

li

fe va

lu

es to

be 5 more years for

th

e defender and 5 years total for

th

e challenge

r.

(a) For

th

e before-tax replacement study,

find

th

e

AW

va

lu

es. The defe

nd

er AW uses

th

e

market va

lu

e as

th

e

fir

st cost, Po = $- 400,000.

AWo = - 400,

000

(A/

P,IO%,5) - 100,000 = $- 205,520

AW

e = - 1,

000

,

000

(A/P,

IO

%

,5)

-

15

,000 = $- 278,800

Apply

in

g step I of

th

e re

pl

acement study procedure (Section 11.3), we sel

ec

t

th

e

better

AW

valu

e.

The defe

nd

er

is

reta

in

ed now with a plan to keep it

fo

r the 5 re-

maining year

s.

The defender h

as

a $73,280

lo

wer equivalent annual cost co

mp

ar

ed

to th

e cha

ll

enge

r.

This complete solution is included

in

Ta

bl

e

17

-6

(left) for com-

parison with

th

e after-tax study.

(b

) For

th

e a

ft

er-tax replacement study,

th

ere are no tax effects other than income t

ax

for

th

e defende

r.

The annual SL depreciation is $

75

,000, determined

wh

en

th

e

equipment was purchased 3 years ago.

D, = 600,000/ 8 = $75,000

t = I

to

8 years

Table

17

- 6 sho

ws

th

e TI and taxes at 34%. The taxes are actua

ll

y t

ax

sav

in

gs of

$59,500 per year,

as

indicated

by

the minus sign. (Remember that for t

ax

sav

in

gs

in

an

economic analysis

iti

s assumed there is positive taxable income else

wh

ere

in

th

e

corpora

ti

on to offset the saving.) Since only costs are estimated, the annual CFAT is

nega

ti

ve, but

th

e $5

9,

500 t

ax

savings h

as

reduced

it.

The CFAT and AW at 7% per

year are

CF

AT

= CFBT - taxes = - 100,000 -

(-

59,500) =

$-

40,500

AW

o = -

400

,

000

(A/P,7

%,

5) - 40,500 =

$-

13

8,056

For

th

e challenger, deprecia

ti

on recapture

on

th

e defender occurs

wh

en

it

is re-

placed, bec

au

se

th

e trade-in amount of $400,000 is larger than

th

e current book

va

lu

e. In year 0 for the cha

ll

enger, Table

17

-6

in

cl

ud

es

th

e fo

ll

ow

in

g computations

to a

rri

ve at a tax

of

$8500.

Defender book va

lu

e, year

3:

Depreciation recapture:

Taxes on

th

e trade-

in

, year 0:

BY

3

= 600,000 - 3(75,000) = $375,000

DR3 = TI = 400,000 - 375,000 = $25,000

Taxes = 0.34(25,000) = $8500

SECTION 17.7

After-Tax Re

pl

acement Study

TABLE

17-6

Before-Tax and After-Tax Re

pl

acement Analyses, Example 1

7.

12

Before Taxes

After

Taxes

Depre-

Taxable Taxes*

Defender

Expenses

dation

Income

at

Age

Year

E

Pand

5 CFBT 0

TI

O.34TI

DEFENDER

3

0

$- 400,000 $- 400,000

4

$-

100

,000 -

100

,000

$75

,000 $- 175,000

$-59,500

5 2

-

100

,000

-

100

,000

75

,000 -

175

,000 -

59

,500

6 3 -

100

,000

-

100

,000

75

,000 - 175,000 - 59,500

7 4 - 100,000 -

100

,000

75

,000

-

175

,000

-

59

,500

8 5

-

100

,000

0

- 100,000

75,000

-

175

,000

- 59,500

AW

at

10%

$- 205,520

AWat7%

CHALLENGER

0

$- 1,000,000 $- 1,000,000

$+25,000t

$

8,500

$- 15,000 -

15

,000

$200,000

-

215

,000

-73

,

100

2

-

15

,000 -

15

,000

200,000 - 215,000

-73,

100

3

- 15,000 - 15,000 200,000 - 215,000 - 73,100

4

-

15

,000 - 15,000

200,000 - 215,000 - 73,100

5

- 15,000

0

- 15,000

200,000

- 215,000'

-7

3,100

AWat

10

% $-

278

,800

AWat7

%

•

Minu

s

sign

indi

cate

s a

tax

s

aving

s

for

the

year.

t

Depreciation

recapture

on defender

trade-in.

j;

Assumes

c

hall

en

ge

r's s

alvage

actua

ll

y r

ea

li

zed

is

S =

0;

no

tax.

The SL depreciation

is

$1

,000,000/ 5 = $200,000 per year. This results

in

tax sav-

ing and CFAT as follows:

Taxes

= (-

15

,000 - 200,000)(0.34) = $- 73,100

CFAT

= CFBT - taxes = -

15

,000 -

(-73,100)

= $+ 58,100

In year 5, it

is

ass

um

ed the

cha

ll

enger

is

sold for $0; there

is

no depreciation recap-

ture. The

AW

for the cha

ll

enger at the 7% after-tax MARR is

AW

e = - 1,000,000(A/ P

,7

%,5) + 58,100 =

$-187,863

The defender

is

again selected; however, the equivalent annual advantage has de-

creased from $73,280 before

ta

xes to $49,807 after taxes.

Conclusion:

By

either analysis, retain the defender now and plan

to

keep it for

5 more years. Additionally, pl

an

to

eva

lu

ate the estimates for both alternatives

I year hence.

If

a

nd

when cash flow estimates change significantl

y,

perform another

replacement analysis.

597

CFAT

$- 400,000

-

40

,500

-40

,500

- 40,500

-40

,500

-40,5

00

$-

138

,056

$-

1,008

,500

+58,

100

+58,

100

+58,

100

+58,

100

+58,

100

$-187

,

863

598

CHAPTER

17

After-Tax Economic Analysis

Comment

lfth

e market value (trade-in) had been less than the cun'ent defender book value of$375,000,

a capital

lo

ss, rather than depreciation recapture, would occur in year O. The

re

su

lting tax

savin

gs

would decrease the

CFAT

(which is

to

reduce costs if CFAT

is

negative). For ex-

ample, a trade-in amount

of

$350,000 would r

es

ult

in

a

TI

of

$350,000 - 375,000 =

$-

25

,000 and a tax sav

in

gs

of

$-8500

in

year

O.

The CFAT

is

then

$-1,000,000

-

(- 8500) = $- 991,500.

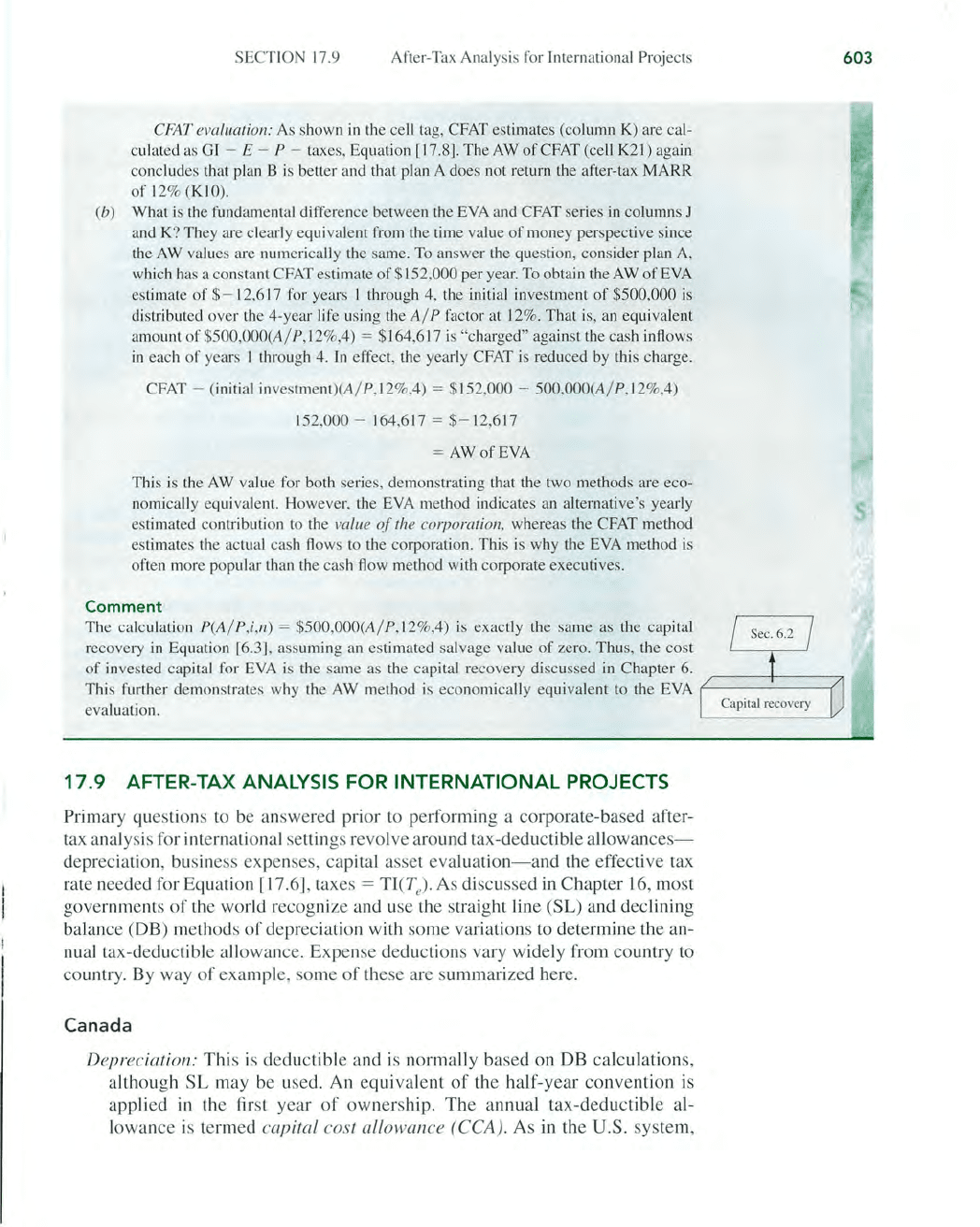

EXAMPLE

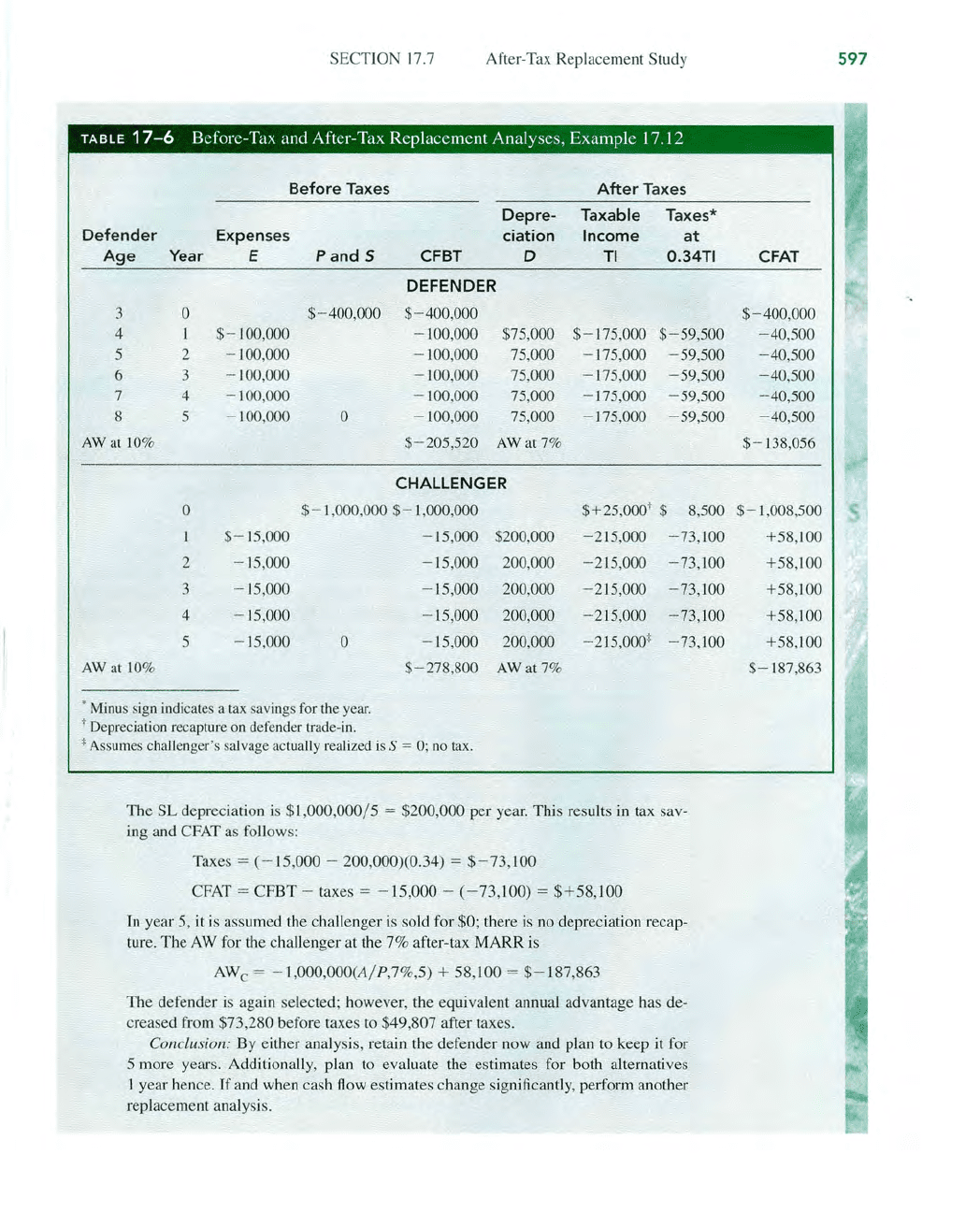

17.13

;

Repeat the after-tax replacement study of the previous example (17.12b) using 7-year

MACRS depreciation for the defender and 5-year MACRS depreciation for the challenger.

Assume either asset is sold after the 5 years for exactly its book value. Determine if the an-

swers are significantly different from those obtained when the simpliJying assumption

of

classical SL depreciation was made.

Solution

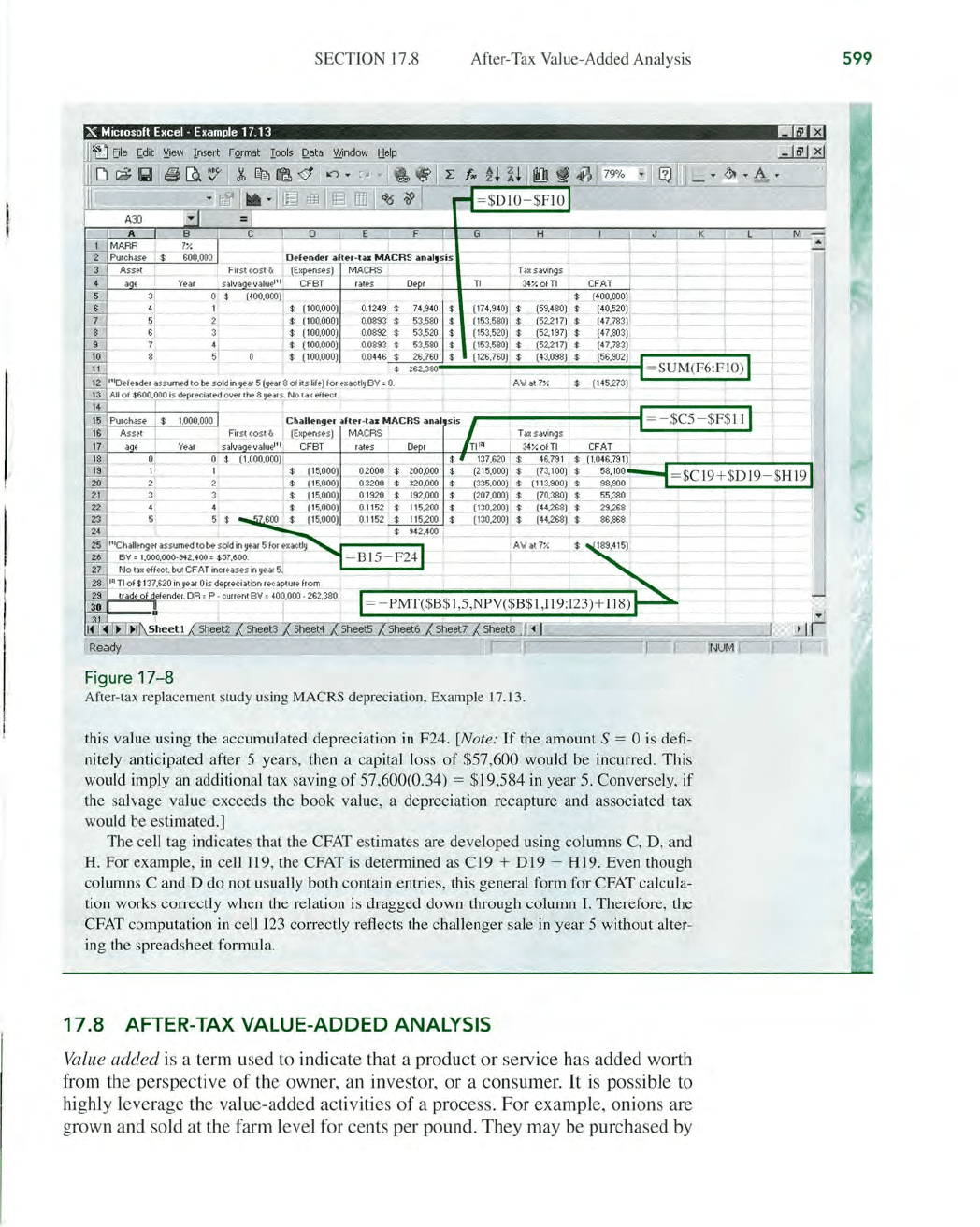

Figure

17

- 8 shows the complete analysis. Refer to the cell tags for det

ai

ls

of

the comput

a-

tions. MACRS requires substantially more computation than SL depreciation, but this

effort is easi

ly

reduced

by

the use of a

sp

re

adsheet. Again the defender is selected

for

retention, but now by an advantage of$44,142 annually. This compares to the $49,807 ad-

van

tage using classical SL depreciation and the $73,280 before-t

ax

advantage

of

the

defender. Therefore, taxes

an

d MACRS have both reduced the defender's economic ad-

va

nt

age, but not enough

to

reverse the decisi

on

to

retain i

t.

Several other differences

in

the results between SL and MACRS depreciation are worth

noting. There is depreciation recapture

in

year 0

of

the challenger due

to

trade

in

of

the de-

fender at

$400,000, a value larger than

th

e book value

of

the 3-year-old defender. This

amount, $137,620

in

cell

GI8,

is

treated as ordinary taxable incom

e.

The calculations for

th

e DR and associated tax,

by

hand, are

as

follows:

BY

3 = first cost - MACRS depreciation for 3 years

= total MACRS depreciation for years 4 through 8

= $262,380

DR

=

TIo

= trade

in

- BV

3

= 400,000 - 262,380 = $137,620

Taxes

=

137

,620(0.34) = $46,790

(cell

Fll)

(cell G18)

(cell

HI

8)

See the ce

ll

tags for the spreadsheet relations

th

at duplicate this logic.

The assumption

th

at the challenger is sold after 5 years at its book

va

lu

e implies

a positive cash

flow

in

year

5.

The enu'y $57,600

in

cell C23

of

Figure 17-8 reflects

this

as

sumption, s

in

ce the foregone MACRS depreciation in year 6 would be

1,000,000(0.0576) = $57,600. The spreadsheet relation BJ5-F24 in cell C23 determines

SECTION

17

.8 After-Tax Va

lu

e-Added

An

alysis

}(

Microsoft EHcel - EHample 17

13

I!I~

t3

E F K M

Tdx

s.av

ings

C

FAT

-t

TI

3

4XofTI

D@fen

de

r a

ft

@r-t

aa

MACR

S ana

l,

s is

s

alv

a e va

lu

el

'l

(

E~;~

S;5

)

~

:

t

~~

S

r Oe r

(5

9.

~

80)

J

:

(400.oo0J

(174.9

40

J

(

4O.

520J

1'

~3.58

0J

_

(5

2.

217) $ (47.783)

o $ (400.00

0)

I $

(1

00

.

00

0)

0.1249

1'

-$

74,

940

(100.

00

0) 0.089} $ 53.

58

0

(100.000) 0.0892

$ 53.520 $ (153.5

20

) (

52

.197) $

(4

7.8

03J

(10

0.000) 0.0893 $ 5

3.

58

0 $ (

15

3.

580) (

52

.217) $

(4

7.783J

(126

.7

60) l 43.098) $ (56.902)

I = S U M

(F

6 :

FIO

) 1

pOO.OOO)

O.OH S $

26,760

$

$

2&2,380

A'I,/at

7X

$ (

14

5.273)

Cha

ll

en

ger

a

li

ef-tali

MA

CRS anal s is

= - $

C5

-$

F $

11

Fir

st cost & (Expenses) MACRS

Tax

s

av

in

gs

CFST rates 34%

ofTl

CFAT

137.620 $

is

.

79

1 $ (1.046

.7

91) 1

(215.000)

$ (

73.1

00) $

5

8:io

O

~

=

$C

I

9

+$

DI9

-

$H

I

9

1

20

21

22

23

24

4

5 $

(1

5.0

00)

(15.00

0)

(1

5.000)

(1

5.

00

0)

(15.000)

0.

32

00

32

0.

0

00

(335.0

00

) $ (

11

3.

90

0) $

98.9

00

. ! _

0.1

92

0 (

20

7

.0

0

0)

$

(7

0.380) $ 5

5.

380

0.1152 (130.20

Q)

$

(44

.268) $ 29

.2

68

0.

115

2

(1

30.200) $ (

44.

268) $ 86

.8

68

25

II'Chalien

ge

r assum

ed

to be

so

ld in

year

5 for

e~actly

A'oJ

at

7x

26 B

V.

1

.0

0

0.

000·94

2.

40

0 . $57.600.

27

No (.all

e-

ff

ect.

bu

t CF AT inc

re

ases in y

;;>a

r 5.

Sh

eet6 SheetZ

Fi

gu

re

17-8

After-tax replacement s

tu

dy using MACRS deprecia

ti

on

, Example

17.

13.

thi

s

va

lu

e us

in

g

th

e accumulated deprecia

ti

on in F24. [Note:

If

the amount S = 0 is de

fi-

nite

ly

anti.cipated after 5 year

s,

then a capital loss

of

$57

,6

00 would be incurre

d.

This

would imply an additional tax sav

in

g

of

57,600(0.34) = $19,584

in

year 5. Conversel

y,

if

th

e salvage va

lu

e exceeds the book

va

lu

e, a deprecia

ti

on recapture and associated tax

would be estimated.]

The ce

ll

tag indicates that

th

e CFAT estimates are developed using columns C, D,

an

d

H. For example, in cell

Jl

9, the CFAT is determined as C19 + D19 -

H1

9. Even though

columns C and D do not usua

ll

y bo

th

conta

in

entries, this general

fo

rm

fo

r C

FAT

calcula-

ti

on wo

rk

s correctly

wh

en the rela

ti

on is dragged down

th

ro

ugh column

1.

Therefore, the

CFAT computa

ti

on

in

ce

ll

1

23

correctly reflects the challenger sale

in

year 5 without alter-

ing

th

e spreadsheet formula.

17

.8 AFTER-TAX VALUE-ADDED ANALYSIS

Val

ue added is a term used to indicate that a product or service has added worth

from

th

e perspec

ti

ve

of

the o

wn

er, an invest

or

, or a consumer. It is possible to

hig

hl

y leverage

th

e value-added activities

of

a process. For example, o

ni

ons are

grown and sold at the

fa

rm level for cents per pound. They may be purchased by

&

599

600

CHAPTER

17

After-Tax Economic Analysis

the shopper in a store at 25 to

50

cents

per

pound.

But

when onions are cut and

coated with a special batter, they may be fried in hot oil and sold as onion rings

for dollars per pound. Thus, from the perspe

ct

ive

of

the

co

nsu

mer

, there has been

a large amount

of

va

lu

e added by the processing from raw onions in the ground

into onion rings sold at a restaurant

or

fast-food shop.

The

value added measure was briefly introduced in conjunction with AW

analysis before taxes. When value added analysis is performed after taxes, the

approach is

somew

hat different from that

of

CFAT analysis developed previously

in

this

cha

pte

r.

How

ever, as shown below,

The

decision

about

an

alternative will be the same for both the value

added

and

CFAT methods, because the

AW

of

economic value

added

esti-

mates

is

the same as the

AW

of

CFAT estimates.

Va

lue

added analysis starts with Equation [17.3], net profit

af

t

er

taxes (NPAT),

which includes the depreciation for year 1 through year

n.

T

hi

s is different from

CFAT, where the

depr

eciation has been specifically removed so that only actual

cash

fl

ow

estimates are used for year 0 through year

n.

The

term economic value added (EVA) indicates the monetary worth added by

an alternative to the corporation's bottom line.

Th

e technique discussed below

was first publicized in several

articles';'

in

the mid-1990s, and it has since b

ecome

very popular as a

me

ans to

eva

luate the ability

of

a corporation to increase its

economic

worth, especially from the shareholder

s'

viewpoint.

The

annual

EVA

is

the

amount

of

the NPAT remaining on

corporate

books

after

removing the cost

of

invested capital

during

the year.

That

is,

EVA

indicates

the

project's contribution to the

net

profit

of

the corpora-

tion

after

taxes.

Th

e cost

of

invested capital is the

af

ter-tax rate

of

return (usually the

MARR

value) multiplied by the book value

of

the asset during the year. This is the inter-

est

incurred by the current l

eve

l

of

capital

in

vested

in

the asse

t.

(If

different tax

and book depreciation methods

ar

e used, the book depreciation

va

lue is used

here, because it more closely represents the remaining capital invested

in

th

e

asset from the corporation's perspective.) Computationally,

EVA

= NPAT - cost

of

invested capital

= NPAT - (after-tax interest rate)(book value

in

year

t - 1)

=

TI(l

- Te) - (i)(BV

t

_

1

)

[17.18]

Since bo

th

TI

and the book value

co

nsid

er

depreciation, EVA is a measure

of

worth that mingles actual cash flow with noncash

fl

ows to determine the esti-

mated financial worth

co

ntribution to the corporation. This financial

wor

th

is

th

e

amount

used

in

public documents

of

the corporation (balance sheet,

in

come

statement, stock reports, etc.).

Because

corporations want to present the largest

*A. Blair. "EVA F

eve

r

,"

Manageme

l1l

Toda

y,

Jan. 1997,

pp.

42-45

;

W.

Freedman,

"H

ow

Do You Add Up?"

Che

mi

cal Week,

Oc

t.

9, 1996,

pp.

31

-3

4.

SECT

ION

17.

8

Af

ter-Tax Va

lu

e-Added Analysis

va

lu

e possible to the stockholders and other

owner

s,

the EVA method may

be

more appealing from the financial perspective than the AW method.

The

result

of

an EVA analysis is a series

of

annual EVA estimates. Two

or

more a

lt

erna

tives are compared by calculating the AW

of

EVA

est

imat

es and

selecting the alternative with the larger AW value.

If

only

one

project is evalu-

ated, A W > 0 means the after-tax

MARR

is exceeded, thus making the project

value addin

g.

Sullivan and Needy* have demonstrated that the AW

of

EVA and the AW

of

CFAT are identical

in

amount. Thu

s,

either method can be used to make a

decision.

The

annual EVA

est

imates indicate added worth to the corporation

generated by the alternative,

willIe the annual CFAT estimates describe

how

cash

will flow. This

co

mpa

ri

son is made

in

Example 17.14.

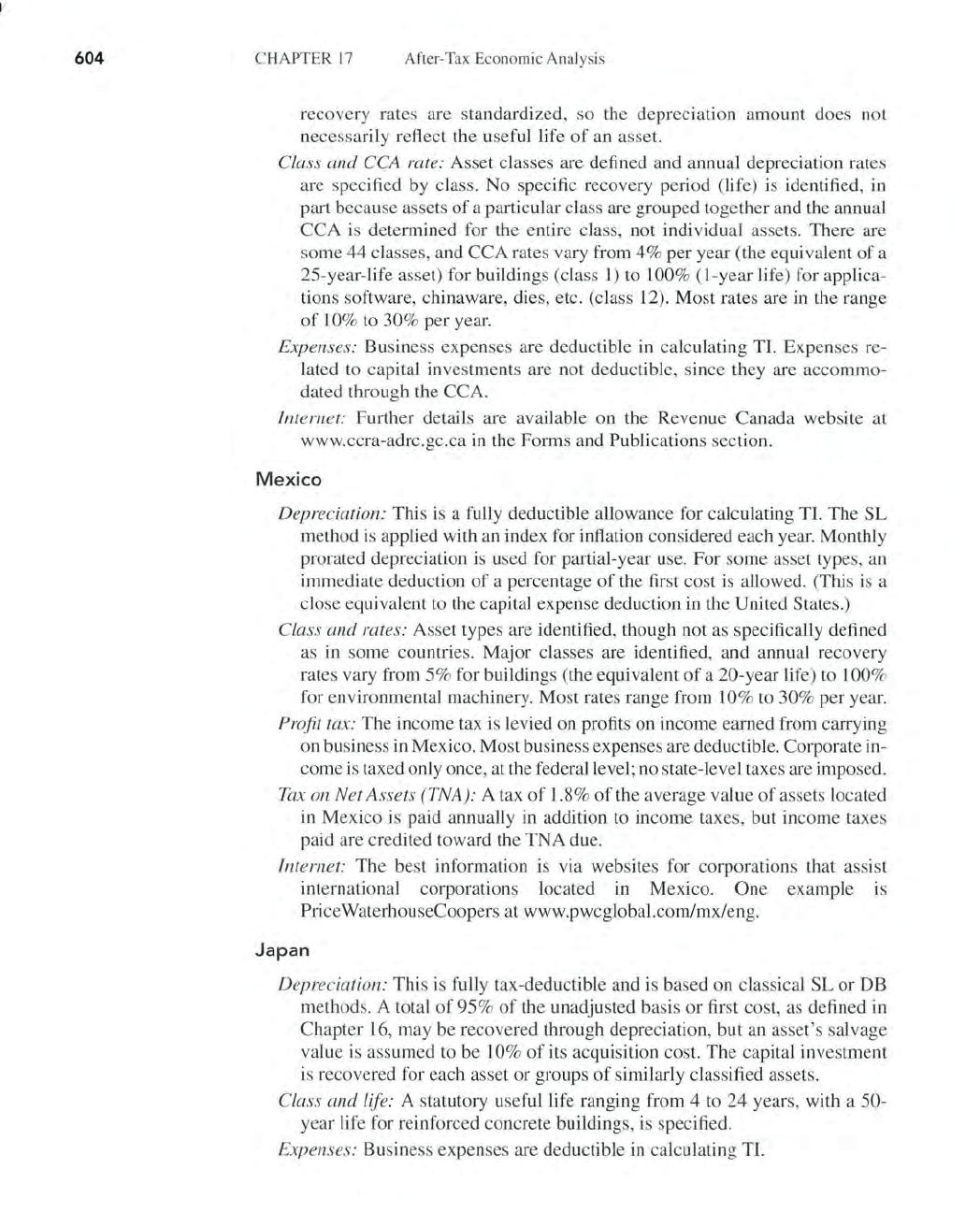

EXAMPLE

17.14

.

:"

Biotechnics Engineering has developed two mutually exclusive plans for investing in new

cap

it

al equipment with the expectation

of

increased revenue from its medical diagnostic

services to cancer patients.

The

estimates are summarized below. (

0)

Use classical straight

line depreci

at

ion, an after-tax MARR

of

12%, an effective tax rate

of

40%, and solution by

computer to perform two annual worth after-tax analyses: EVA and

CFAT.

(b) Explain the

fundamental difference betw

ee

n the results

of

the two analyses.

Plan A

Initial investment

$500,000

Gross income - expenses $170,000 per year

Estimated

li

fe 4 years

Salvage va

lu

e None

Solution by Computer

Plan B

$1,200,000

$600,000

in year I, decreasing

by

$50,0

00

per

year thereafter

4 years

None

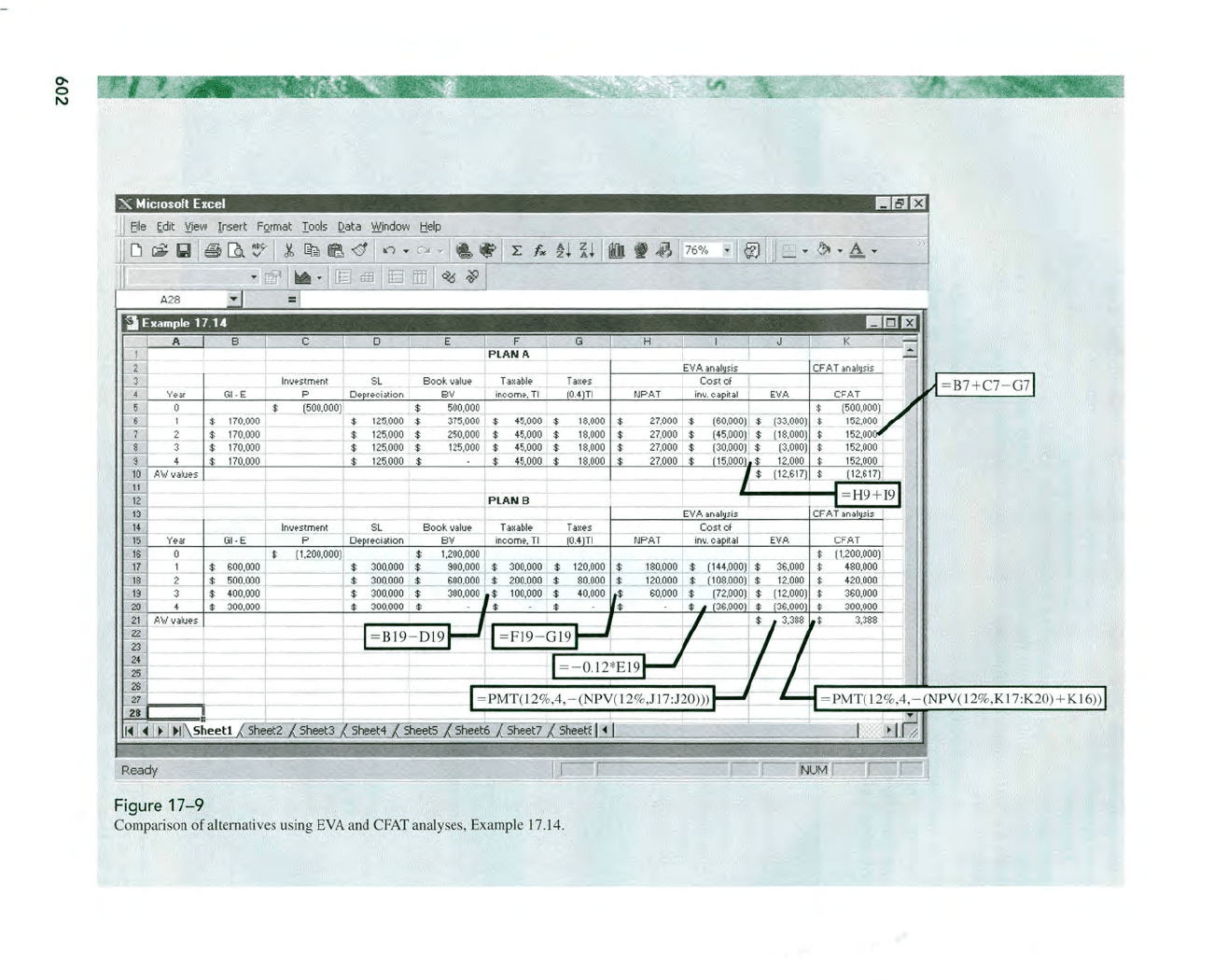

(a) Refer to the spreadsheet and ce

ll

tags

in

Figure

17

- 9.

EVA

eva

lu

ation: All the nec

essa

ry

inf

ormation for EVA estimation is determined

in

columns B through G.

The

net profit after taxes (NPAT)

in

column H is calculated

by Equation

[17.3], TI - taxes.

The

book values (column

E)

are used to determine

the cost

of

invested capital

i.n

column I, us

in

g the second term

in

Equation [17.18],

that i

s,

i(B V,_

I)

' where i

is

the J 2% after-tax MARR. This represents the amount

of

interest at 12%

per

year, after taxes, for the currently invested capital as reflected by

the book va

lu

e at the beginni.ng

of

the year.

The

annual EVA estimate is the sum

of

columns H a

nd

I (Equation [17.18]) for years 1 through 4. Notice there

is

no EVA es-

timate

for

year

0,

since NPAT and the cost

of

invested capital are estimated for

years

I through n. Finally, the larger

AW

of

the EVA value is selected (121), which

indicates

th

at plan B is better, a

nd

that plan A does not make the

12

% return (JlO).

*

W.

G. Sulli van and

K.

L.

Needy, "Determ

in

ation of Economic Value Added for a Proposed Inves

Ull

ent

in

ew Manufac

tu

ring

."

Th

e

Ell

g

in

eer

in

g Economist, vo

l.

45, no. 2 (2000), pp. 1

66-

18

1.

601

~

E-Solve

0-

o

I\.)

X Microsoft Excel

I!I~Ef

Eile

~dit

Jljew

insert

FQI'mat

10015

Q.ata

:0Lindow

t!elp

.

~

.

A.

.

)I

Example n 14 !Iii!

Ef

I-"LAN

A

E

VA

anahJsis

I CF

AT

anahlsis

lnlJestment

SL

Book

valuE'

Tal!able

Ta

xes

Cost

of

Y

ear

GiI·E

P

De

reciation

8V

income,

TI

0,4

TI

NPAT

in

...

.

ca

ital

E

VA

0

(500,000)

$

500.000

$

27,000

$

(60,000) $

$

27,000

$

(

45

,00~

$

$

27,000

$

(30,000) $

27,000

$

$

170,000

$

125,000

$

375,000

$

45,000

$

18,000 I $

$

170,000

$

125.000

$

_-

250.000

$ 45,00

0...

$

18,000 $

$

170,000

$

125,000

$

125.000

$

45,000

$

18,000 $

$

170,000

I $

125,000

$ $

45,000

$

18,000 $

A'W'

..

alu~

I

11

12

PLANS

.-

---

_

13

14

I

n'''E':s:t

me

~

SL

.§:~Qk

v.a

l

ue

Ta:-lab

le

Ta!!!?

s

1~

Year

GiI·E P Oe leciation 8V

income.

TI

rO

.

4lT1

NPAT

16

0

(1,200,000)

.L

1,

200,000

17

$

600,000

$

300,000 . $ 900.000 $

30Q,QQIl....

$

18

I

$

500,000 I $

300,00

01$

--

600.000 J $

200,000 • t.

,

~

19

$

400,000

$

300,000' 1-.1.

__

- 300,000 i $

1

00,0OQ.

~

$

20

300,000

$

300,000 $ $

$

21

A'W

lJalu~s

..,?2.

23

E

25

2G

=

Sheetl

f Sheet2 f Sheet3

Ready

Figure

17-9

Comparison

of

alternatives using

EVA

a

nd

CFAT analyses, Example 17.14.

SECTION

17

.9

After-Tax Analys

is

for International Projects

CFAT evaluation:

As

shown

in

the cell tag, CFAT estimates (column

K)

are cal-

culated as GI -

E - P - taxes, Equation

I:

17.8].

The

AW

ofCFAT

(cell K21) again

concludes that plan

B

is

better and that pl

an

A does not return the after-tax

MARR

of

12% (K I

O).

(b)

What

is

the fundamental difference between the EVA and CFAT series

in

columns J

and K? They are clearly equivalent

From

the time value

of

money perspective since

the

AW

va

lu

es are numerically the same. To answer the question, consider pl

an

A,

wh

ic

h has a constant CFATestimate oF$152,

000

per year. To obta

in

the

AW

of

EVA

estimate

of

$- 12,617 for years I through 4, the initial investment

of

$500,000 is

di

st

ri

buted over the 4-year life

us

i

ng

the

A/

P factor at 1

2%

.

That

is,

an

equivalent

amount

of

$5

00,OOO(A

/ P,

l2

%,4) = $164,617

is

"c

harged" against the cash inflows

in

each

of

years I through 4. In effect, the yearly CFAT is reduced by this charge.

CFAT - (initial

in

vestmenl

)(A

/ P,

12

%,

4)

= $152,

000

- 500

,000(A/

P,

12

%,4)

J 52,000 - 164,6

17

=

$-12,617

=

AWofEVA

This is the A W value for both series, demonstrating that the two methods are eco-

nomica

ll

y equivalent. However, the EVA method indicates an alternative's yearly

estimated

co

ntribution to the

va

/u

e

of

(he corporation, whereas the CFAT method

estimates

th

e actual cash flows to the corporation. This

is

why the EVA method is

often more popular than the cash flow method with corporate executives.

Comment

The

calculation

P(A/P

,i,n) = $500,OOO(A/P,12%,4) is exactly the same as the capital

recovery

in

Equation [6.3], assuming an estimated salvage value

of

zero.

Thus

, the

cost

of

invested capital for EVA is the same as the

cap

ital

re

cove

ry discus

se

d

in

Chapter

6.

This further demonstrates why the AW method is economically equivalent to the EVA

1'-------("

evaluation.

17.9

AFTER-TAX ANALYSIS FOR INTERNATIONAL PROJECTS

Primary questions to be answered prior to performing a corporate-based after-

tax analysis for international settings revolve around tax-deductible

allowances-

depreciation, business expenses, capital asset evalua

tion-and

the effective tax

rate needed for Equation [17.6], taxes =

TI(T

e)' As discussed

in

Chapter 16, most

governments

of

the world recognize and use the straight line (SL) and declining

balance (DB) methods

of

depreciation with some variations to determine the an-

nual tax-deductible allowance.

Expense

deductions vary widely from country to

country. By way

of

example, some

of

these are s

umm

arized here.

Canada

De

pr

eciation: This is

deductib

le and

is

normally based on DB calculations,

although

SL

may be used. An

equivalent

of

the half-year

convention

is

applied in the first

year

of

ownership

.

The

annual

tax-deductible

al-

lowance

is termed capital cost allowance (CCA). As

in

the U.S. system,

603

604

CHAPTER

17

After-Tax Economic Analys

is

recovery rates are standardized,

so

the depreciation amount does not

necessarily reflect the u

sef

ul life

of

an asset.

Class

and

CCA rate: Asset classes are defined and annual depreciation rates

are specified by class.

No

specific recovery period (life) is identified,

in

part because assets

of

a particular class are grouped together and the annual

CCA

is determined for the entire class, not individual assets. There are

some

44

classes, and

CCA

rates vary from 4% per year (the equivalent

of

a

25-year-life asset) for buildings (class 1) to 100%

(I-year

life) for applica-

tions software, chinaware, dies, etc. (class 12). Most rates are

in

the range

of

10% to 30% per year.

Expenses: Business expenses are deductible in calculating TI. Expenses re-

lated to capital investments are not deductible, since they are accommo-

dated through the CCA.

In

ternet

: Further details are available on the Revenue

Ca

nada website at

www.ccra-adrc.gc.

cain

the Forms and Publications section.

Mexico

Depreciation: This is a

fu

ll

y deductible allowance for calculating TI.

The

SL

method is app

li

ed with an index for infla

ti

on considered each year. Monthly

prorated depreciation

is

used for partial-year use.

For

some

asset types, an

immediate deduction

of

a percentage

of

the first cost is allowed. (This

is

a

close equivalent to the cap

it

al

expense deduction

in

the United States.)

Class

and

rates: Asset types are identified, though not as specifically defined

as

in

some countries. Major classes are identified, and annu

al

recovery

rates vary from 5% for buildings (the equivalent

of

a 20-year

li

fe) to 100%

for environmental machinery.

Most

rates range from

10

% to

30

% per year.

Profit tax: The income tax is levied on profits on income earned from carrying

on business in Mexico.

Most

business expenses are deductible. Corporate in-

come

is

taxed only once, at the federal level; no state-level taxes are imposed.

Tax

on

Net

Assets

(TNA): A tax

of

1.8%

of

the average va

lu

e

of

assets located

in

Mexico is paid annua

ll

y

in

addition to income taxes, but income taxes

paid are credited toward the

TNA

due.

Internet:

The

best information is via websites for corporations that assist

international corporations located in Mexico.

One

example

is

Price WaterhouseCoopers at www.pwcglobal.com/rnx/eng.

Japan

De

pr

eciation: This

is

fully tax-deductible and is based on classical

SL

or

DB

methods. A total

of

95%

of

the unadjusted basis

or

first cost, as defined

in

Chapter

16,

may be recovered through depreciation, but an asset's salvage

value is assumed to

be

10

%

of

its acquisition cost.

The

capital

in

vestment

is

recovered for each asset

or

groups

of

similarly classified assets.

Class

and

life: A statutory useful

li

fe ranging from 4 to

24

years, with a 50-

year life for reinforced concrete buildings,

is

specified.

Expe

ns

es: Business expenses are deductible

in

calculating TI.