Gardiner V., Matthews H. The changing geography of the United Kingdom

Подождите немного. Документ загружается.

KEITH CHAPMAN

36

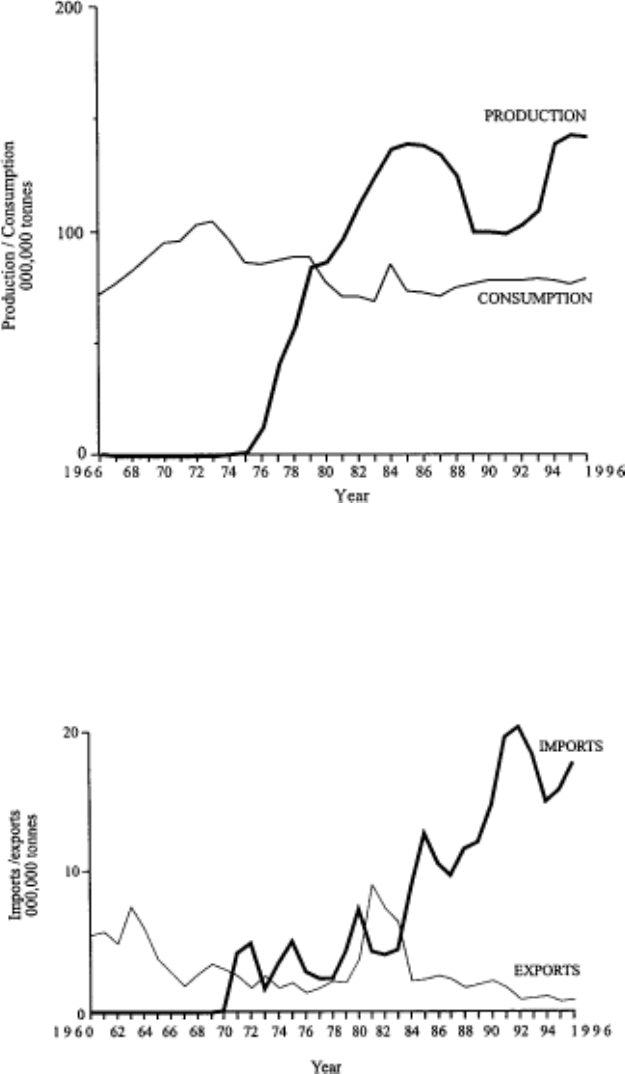

FIGURE 3.4 Oil production and consumption, 1966–96

FIGURE 3.5 Coal exports and imports, 1960–96

ENERGY

37

and the Arab-Israeli war of 1967 emphasised these risks, which were confirmed by

the success of the OPEC countries in harnessing their latent power as suppliers of

energy to Western Europe, Japan and the United States. Although supplies were

generally maintained, the first and second price shocks stimulated interest in

indigenous energy sources in all the major oil-consuming countries. In the case of

the UK, an explicit and overwhelming policy commitment to encourage the rapid

exploitation of the oil and gas resources of the North Sea was the most obvious

expression of this interest. The international oil price has a continuing significance

for events in the North Sea because it is the yardstick against which commercial

decisions are made. The desire of successive governments to maintain the momentum

of development has required periodic adjustments of the fiscal terms and conditions

under which the oil companies operate. Many factors enter into these negotiations,

but one of the most important is the international oil price.

Resource availabilities

Although energy developments in the UK have been strongly influenced by political

and economic circumstances on the world stage, the country has been very fortunate in

its endowment of fossil fuels. It is ironic that the UK’s return to a position of energy

surplus in 1980 coincided with the decline of coal which, in geological terms, is much

more abundant than either oil or natural gas. Volumetric estimates in 1976 suggested

the existence of around 190 billion tonnes (190·10

9

) of coal-in-place in the UK. Defining

the recoverable portion of this gross figure is very difficult given the many variables

which determine the economics of coal production. In the publicity surrounding the

announcement of Plan for Coal in 1974, the NCB estimated recoverable reserves at 45

billion tonnes, which represented approximately 300 years supply at prevailing rates of

consumption. By the end of 1996, the corresponding figure had fallen to only fifty

years. This dramatic decline is, at first sight, hard to explain bearing in mind that coal

consumption has fallen steadily in the UK since 1974 (Figures 3.2 and 3.3). The UK

has obviously not removed the equivalent of 250 years’ supply from its coal resource

base in just over twenty years. The contradiction lies in the factors influencing the

apparent elimination of reserves. Various economic, technical and geological

assumptions are incorporated in the definition of proved reserves.

1

These assumptions

interact with prevailing policies in the sense that colliery closures can effectively sterilise

the resource by making it either technically impossible or prohibitively expensive to

return to abandoned workings. This accounts for the continuous decline in the proved

reserves of coal in the UK from 10,750 million tonnes in 1986 to 2,500 million tonnes

in 1996.

2

This counter-intuitive relationship between falling production and shrinking

reserves demonstrates, in a sense, how the demise of the coal industry has become a

self-fulfilling prophecy.

As the proved reserves of coal have declined, so the equivalent projections for

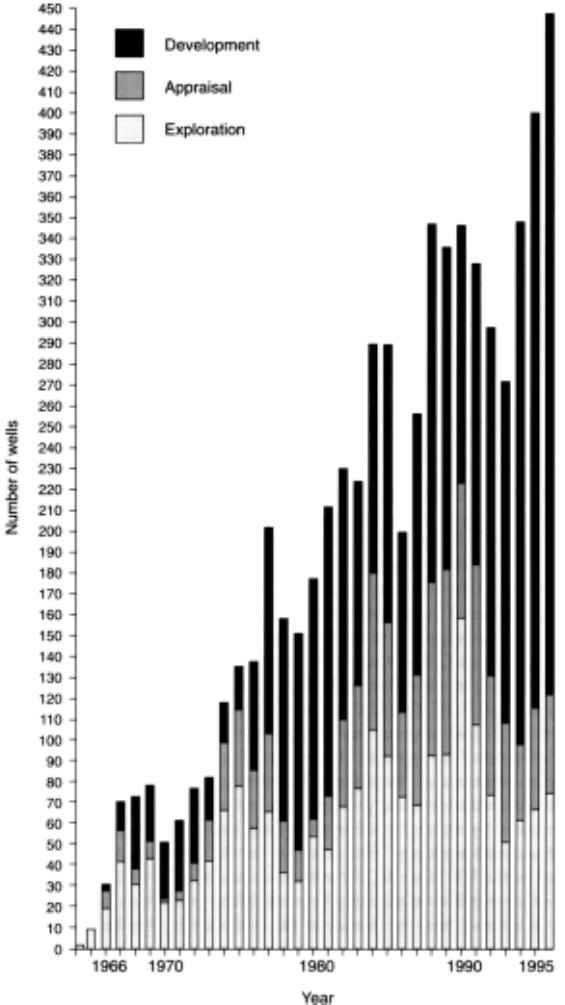

North Sea oil and gas have moved in the opposite direction. Almost 2,000 exploration

wells had been drilled in British waters

3

by the end of 1996, plus a very much larger

number of appraisal and development wells (Figure 3.6). This activity has established

substantial reserves of oil and gas. Commercial interest in the hydrocarbon potential of

the North Sea was initially focused upon natural gas as a result of the discovery of the

KEITH CHAPMAN

38

FIGURE 3.6 Offshore drilling activity, 1964–96

ENERGY

39

massive Groningen gas field in the Netherlands in 1959. This discovery drew attention

to the possible existence of similar geological structures offshore. The validity of this

inference has been confirmed by subsequent events, and estimates of natural gas reserves

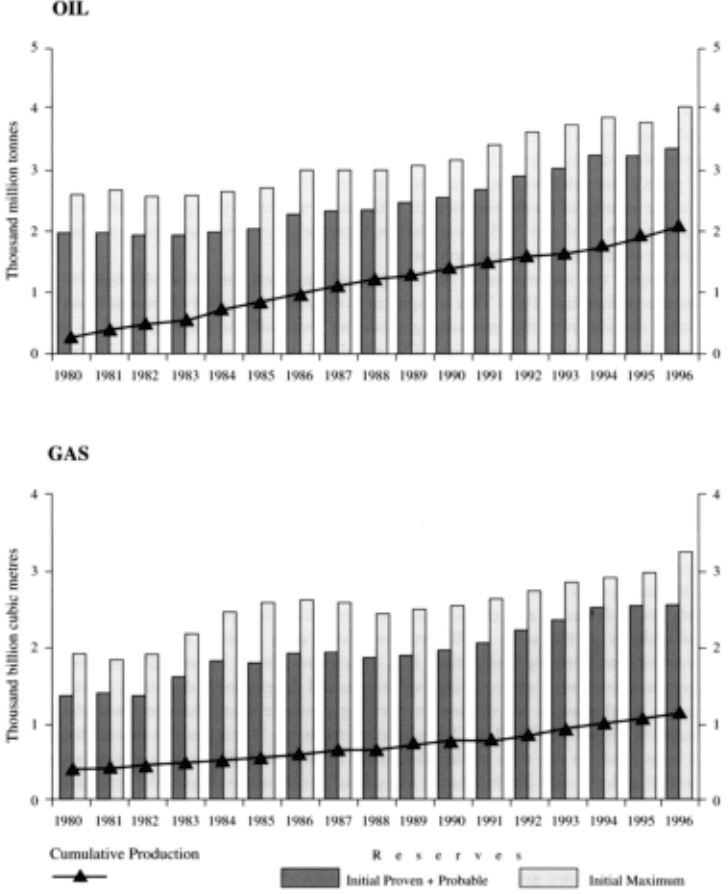

on the UK Continental Shelf (UKCS) have increased steadily since 1980. Total

cumulative production of natural gas over the last thirty years represents approximately

one-third of the current estimate of maximum recoverable reserves (Figure 3.7)

4

The

inference that UKCS natural gas will last for another sixty years is not valid because it

cannot be assumed that there will be no further discoveries or that the volume of

production in each of the next two thirty-year periods will be the same as that between

1965 and 1995. Nevertheless, it can be concluded that there is no prospect of imminent

exhaustion of the resource base.

Despite the importance of natural gas, oil has been the principal objective in the

exploration effort since 1970. This is apparent in the northward shift of interest in successive

licensing rounds from the primarily gas-bearing areas off the English coast to the

predominantly oil-producing territories off Scotland and the Shetlands. The UK has been

a net exporter of oil since 1980 (Figure 3.4) and, following a period of relative stagnation

in the late 1980s/early 1990s, production reached its highest ever level in 1996. It is

projected to remain at around this level to 2001. The immediate control upon output

beyond this date is the timing of decisions to develop known fields. These decisions will

be influenced by the interactions between the prevailing fiscal regime, which is controlled

by government, the international oil price (see p. 34) and technical changes affecting the

economics of exploiting small and/or inaccessible fields (see pp. 42–3). Taking a longer-

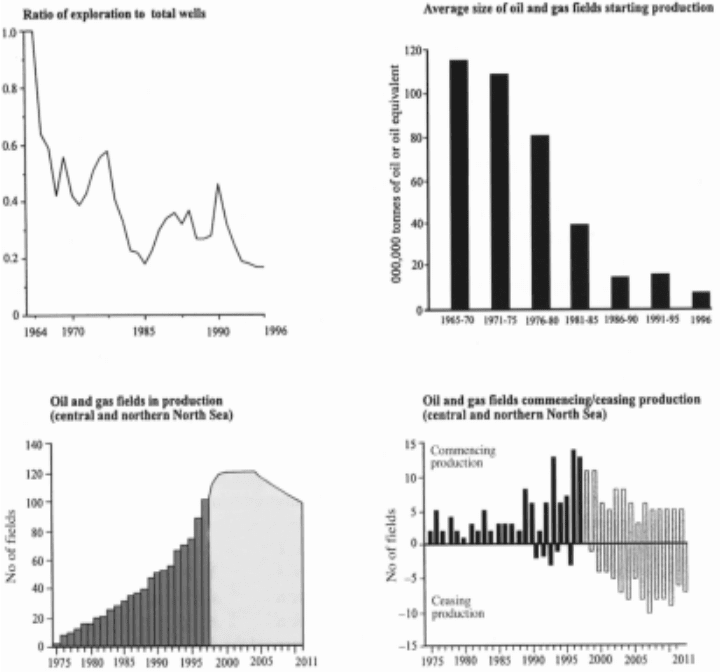

term perspective, there are several indicators suggesting that the North Sea oil and gas

province is at a mature phase in its life cycle (Figure 3.8). The declining average size of

field is consistent with the expectation that the best prospects are targeted first, and the

declining ratio of exploration to total wells drilled is also characteristic of a maturing

hydrocarbon province. Similarly, abandonments in the early 1990s are precursors of a

shifting balance between fields commencing and ceasing production. It is difficult to

predict beyond 2010 because of the numerous uncertainties surrounding exploration and

development decisions. Nevertheless, there are good reasons for caution in deriving

pessimistic conclusions from the trends indicated in Figure 3.8. The UKCS is not restricted

to the North Sea and several discoveries have been made to the west of the Shetlands. If

the North Sea is at a mature stage, the Atlantic frontier is only just beginning its cycle of

development. Figure 3.7 emphasises that the progressive enhancement of reserve estimates

has more or less kept pace with the growth in cumulative oil production since 1980.

Department of Trade and Industry (DTI) estimates in 1996 placed the total remaining

reserves within the range 1,080–5,075 million tonnes. These figures acquire greater

meaning when matched to the United Kingdom’s annual consumption of approximately

78 million tonnes in the same year. A combination of simple arithmetic and heroic

assumptions thus makes it possible to project fourteen to sixty-five years of self-sufficiency

in oil. However, this calculation does not take account of the rapid build-up and subsequent

long decline which is characteristic of the production history of any oil province, nor

does it acknowledge the possibility of changes in demand. The definition of ‘recoverable’

adopted by the DTI is also no guarantee that oil-in-place will actually be extracted under

future technical and economic conditions. On the other hand, historical precedent suggests

that government agencies err on the side of caution when coping with the substantial

KEITH CHAPMAN

40

margins of error involved in making reserve estimates, and some observers believe that

the DTI’s upper figure should be at least doubled to obtain a truer indication of the oil

potential of the North Sea. The picture will only become clear when the final well runs

dry, but it is probable that this resource will remain a major national asset, even if much

of it is not necessarily used directly within the UK, well beyond 2030.

FIGURE 3.7 Discovered recoverable oil and gas reserves and cumulative production, 1980–96

ENERGY

41

Technical change

Technical change influences energy consumption, production and transportation. The

significance of changes in the technology of moving or transporting energy, which

have directly affected the geography of the UK energy industries, will be addressed

later in the chapter, and immediate attention is focused on some of the principal

developments affecting the consumption and production of specific fuels and the

competition between fuels.

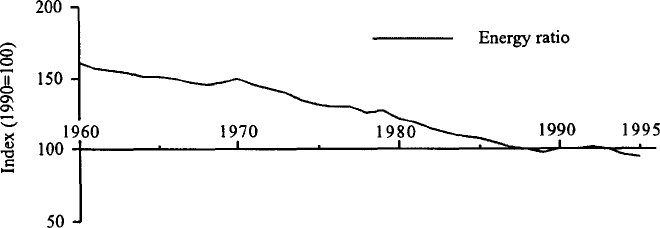

One of the most obvious impacts of technical change has been upon the overall level

of energy consumption. Figure 3.9 plots trends in the ratio of energy consumption to gross

domestic product (GDP) since 1970. It indicates a declining energy ratio, suggesting that

less energy is being consumed per unit (by value) of economic output. This trend is usually

interpreted as an indicator of more efficient energy use. The full explanation is more complex,

but technical change is a common theme. In addition to improvements in the efficiency of

end-users such as individual motor vehicles, the ratio also includes improvements in the

FIGURE 3.8 Life-cycle indicators for UK Continental Shelf oil and gas

KEITH CHAPMAN

42

efficiency of energy producers, most notably in electricity generation. Another important

influence upon the energy ratio has been the changing structure of the economy and, in

particular, the greater importance of services relative to energy-intensive manufacturing

such as iron and steel. Attempts to disentangle the relative contributions of these various

influences upon the energy ratio have suggested that improvements in energy efficiency,

especially in manufacturing, were especially important between 1973 and 1989, but that

the structural effect has been more significant in recent years. Although technical change,

broadly conceived, has been responsible for a long-term downward trend in the energy

ratio, the gradient has been steeper than anticipated twenty or thirty years ago and current

UK energy consumption is well below the levels assumed in prudent strategic planning in

the 1960s.

The aggregate demand-side effect of technical change is composed of impacts upon

specific sectors such as coal. The decline of coal in the 1950s and 1960s was, as noted

above, mainly due to a widening price differential in favour of imported oil. The problems

of the industry were, however, compounded by certain technical changes which reduced

the level of demand. Not only were the major coal-using industries heavily represented in

the slow-growing and declining sectors of the economy, but also these large consumers

were successfully developing more efficient methods of fuel use. Furthermore, several

major markets were lost altogether. In 1950, the railways accounted for 7 per cent of

domestic coal consumption: by 1965, the corresponding figure had fallen to 1.5 per cent

as a result of the changeover to diesel and electric traction. A similar situation arose in the

early 1960s as petroleum fractions replaced coal as the basic feedstock in town gas

manufacture. The trend was repeated in the electricity industry as oil, natural gas and

nuclear power challenged the monopoly position of coal as fuel for thermal power stations.

In 1950, coal represented over 90 per cent of the fuel used for electricity generation in

terms of energy content; by 1996 it accounted for only 20.1 per cent (i.e. approximately

46 million tonnes of oil equivalent).

Whereas technical change has primarily influenced the demand side of the equation

in the case of coal, it has been more significant in affecting the supply of certain other fuels.

For example, the exploitation of the oil and gas resources of the North Sea depends upon

the ability to operate in such a difficult marine environment, and the necessary exploration

—and, more especially, production technology—has been developed in response to this

challenge. Future developments to the west of the Shetlands will depend upon continuing

the record of innovation which has been a feature of the North Sea experience. This record

FIGURE 3.9 Energy ratio, 1960–95

ENERGY

43

is reflected in the Cost Reduction Initiative for the New Era (CRINE) launched in 1993.

This is a scheme, supported by government and the oil industry, aimed at reducing capital

and operating costs, by a combination of technical and managerial innovations, with the

overall objective of extending the economic life of the North Sea oil and gas province.

The history of nuclear power in the UK emphasises that technical change is often

both complex and controversial. There was considerable optimism during the early 1950s

regarding the future contribution of nuclear power to energy supply in the UK. This was

encouraged when, in 1956, Calder Hall became the first nuclear plant in the world to supply

power on a commercial rather than on an experimental basis. Similarly, the ten-year nuclear

power programme announced in 1955 was the first national endorsement of this technology

as a major source of energy supply. Projections made by the Department of Energy in 1978

and 1979 suggested that nuclear power would account for 17 to 22 per cent of primary

energy demand by the year 2000. The actual figure in 1996 was 9.5 per cent and it seems

likely that the late 1990s will witness the zenith of nuclear power in the UK as Sizewell B,

commissioned in 1995, could be the only remaining operational nuclear power station in

the UK by 2020. Some of the first generation Magnox stations have already been

decommissioned and others are already beyond their original design lives. Thus the prognosis

is poor and contrasts sharply with the enthusiasm surrounding the UK’s perceived technical

leadership forty years earlier at ‘the dawn of the atomic age’.

Many factors have contributed to the fading of this vision, but there is no doubt that

the technology has proved more difficult than anticipated. This is reflected in construction

costs, which have been much higher than projected in both the Magnox and, especially,

the Advanced Gas-Cooled Reactor (AGR) programmes. Site work at Dungeness B, for

example, began in 1966 and the station only became fully operational in 1989. Operating

experience was also disappointing for many years as individual stations failed to achieve

their design output. Performance has improved in the 1990s, but there have consistently

been serious doubts about the economics of nuclear power, which was originally justified

in terms of its low cost relative to other fuels. These doubts have been reinforced by a lack

of agreement on the average cost per unit of nuclear electricity. The complexity of

assumptions underpinning these calculations has provided ample opportunity for creative

accounting and the manipulation of figures to suit political agendas (see pp. 44–5). The

Chernobyl incident in 1986 contributed to the collective loss of confidence in nuclear

power and, at the same time, drew attention to the fundamental, unsolved technical problem

of dealing with the radioactive waste products, especially at the decommissioning stage.

The magnitude of this problem was acknowledged in 1990 with the introduction of the

Fossil Fuel Levy which accounts for approximately 10 per cent of electricity prices paid

by consumers in England and Wales. This tax is designed to create a fund ‘to meet the

higher than anticipated backend costs of nuclear power’ (Department of Trade and Industry

1995:15).

Public policy

Government has been a major influence upon the evolution of the UK energy market since

the Second World War. Until comparatively recently only oil, of the major energy supply

industries, was not in public ownership. For more than thirty years there was a political

consensus that these industries should remain in the public sector because of their central

KEITH CHAPMAN

44

role in the national economy. Fiscal measures, such as taxation and subsidies, have also

been frequently employed to manipulate the energy market. These measures have not,

however, been incorporated within a coherent and consistent strategy despite a long history

of energy policy reviews culminating in yet another appraisal initiated by the new government

in 1997 and due for completion in 1998.

The Department of Trade and Industry (1995:3) states that ‘The aim of the

Government’s energy policy is to ensure secure, diverse and sustainable supplies of energy

in the forms that people and businesses want, and at competitive prices.’ This statement

provides clues to some of the problems which have faced successive governments in

regulating the energy market. In the absence of a clearly defined time-scale for their

achievement, several of the aims are contradictory. ‘Competitive’ presumably means ‘low’

prices. However, cheap energy is not consistent with the promotion of efficiency and

sustainability. Thus fossil fuels such as coal and oil may currently be available at more

‘competitive prices’ than renewables such as wind or wave power, but the latter will certainly

need to be developed in the longer term. Such development requires investment which may

be inhibited by a preoccupation with the short-term price relativities of the various energy

sources. Similarly price-driven consumer choices may conflict with wider, strategic concerns

such as the diversification of sources of energy supply. The dramatic decline of the coal

industry has, for example, narrowed future options by making large quantities of coal in

flooded pits inaccessible.

The changing priorities of energy policy in general and attitudes towards the coal

industry in particular illustrate the essentially ad hoc approach. Successive White Papers on

fuel policy in 1965 and 1967 made it clear that the principal objective was ‘to make possible

the supply of energy at the lowest total cost to the community’. The priorities changed after

the first oil price jump in 1972/3, which resulted in a greater awareness of the political and

economic implications of dependence upon external sources of supply. Accordingly policy

statements published by the Department of Energy in 1977 and 1978 demonstrated a greater

commitment to indigenous resources in the support for the expansion plans of the NCB, the

accelerated development of nuclear power, and the promotion of research into renewable

sources of energy. By the 1990s, environmental objectives had become more prominent,

reflecting a prevailing public interest in the concept of sustainable development and the

requirements of international treaty obligations to reduce atmospheric emissions from

combustion processes.

The long-term decline of the coal industry has ultimately been determined by

the preference of consumers for other fuels, but government policy has also been

important. Apart from a relatively brief revival in the 1970s, stimulated by events in

international oil markets (see pp. 34–5), public policy towards the coal industry since

1950 has largely been concerned with the management of decline. In the 1960s, several

steps were taken to slow down the rate of pit closures to ameliorate the adverse

economic and social consequences for coalfield communities. The most important

measures were designed to sustain the demand for coal in its principal market—the

power stations. A completely different agenda emerged in the 1980s when, influenced

by the memory of the miners’ strike in 1973/4 which effectively paralysed the country

and brought down an earlier Conservative government, the Conservative Prime

Minister, Mrs Thatcher, pursued policies intended to break the power of the National

Union of Mineworkers (NUM) and to undermine the position of coal as the dominant

ENERGY

45

fuel in electricity generation. These policies were motivated primarily by political

considerations. These considerations found expression in the imposition of severe

public expenditure controls upon the NCB, which accelerated pit closures and forced

a confrontation with the NUM. They were also evident in a pro-nuclear policy which

resulted in the approval in 1979 of Sizewell B, which is the most recent nuclear power

station in the UK. Mrs Thatcher’s governments imposed less demanding financial

targets in the appraisal of nuclear investment proposals than applied to the operations

of the NCB. This disparity of treatment did not convince commercial interests to bid

for nuclear power at the privatisation of the electricity supply industry in 1989, but it

did reverse the policies of previous governments by accelerating rather than retarding

the decline of coal. The privatisation policies, which became a central feature of the

Thatcher period, were not explicitly directed towards the energy industries.

Nevertheless, the successive transfers of gas, a substantial proportion of the electricity

supply industry and coal from public to private ownership between 1986 and 1994

collectively represented a significant element of the privatisation project. This project,

which is linked to the promotion of competition (i.e. liberalisation), has radically

altered the context of energy production and consumption in the UK.

The structure of the energy sectors following privatisation varies. In the case of

coal, the bulk of British Coal’s

5

assets, amounting to approximately 70 per cent of

UK output in 1994, were sold to RJB Mining (UK) Ltd with smaller companies

assuming responsibility for operations in Scotland and Wales. British Gas plc initially

inherited the monopoly position of its state-owned predecessor at privatisation.

However, various steps designed to create ‘managed competition’ were taken. These

allowed new suppliers to deliver gas from the North Sea and obliged the transportation

and storage arm of British Gas plc (i.e. Transco) to operate as a ‘common carrier’ and

make its on-shore pipeline distribution system available to other companies. British

Gas was itself ‘de-merged’ in 1997 to create two independent companies—BG plc,

responsible for exploration, production and UK pipeline distribution, and Centrica

plc, which is primarily involved in retailing and gas trading activities. The privatisation

of the electricity supply industry has created the most complex structure, partly because

of differences between England and Wales relative to Scotland, and partly because

the nuclear sector remains in public ownership. In England and Wales, the system has

been fragmented into generation, national transmission and regional distribution

(Figure 3.10). The system remains vertically integrated in Scotland, where two area-

based companies are responsible for generation, transmission, distribution and supply

to final consumers. The Scottish generators also contribute electricity to ‘the Pool’ in

England and Wales, which is a wholesale electricity market operated by the National

Grid Company.

There is no doubt that privatisation has contributed to declining real energy prices

in the UK since 1986, but there remain doubts about the ability of the new utility

regulators, OFGAS and OFFER, to fulfil their responsibilities of protecting the interests

of consumers whilst restraining and guiding the activities of the gas and electricity

supply industries respectively. On a strategic level, there is a danger that the

preoccupation with costs and prices will obscure the wider issues implicit in the concept

of energy policy which rests upon the premise that the market mechanism does not

necessarily guarantee an outcome consistent with the national interest, broadly