Skiadas C.H., Dimotikalis I. (editors) Chaotic Systems: Theory and Applications

Подождите немного. Документ загружается.

298 T Sapsis and G. Haller

I

I

\

'\

I

"

'\.

.......

-

"",'"

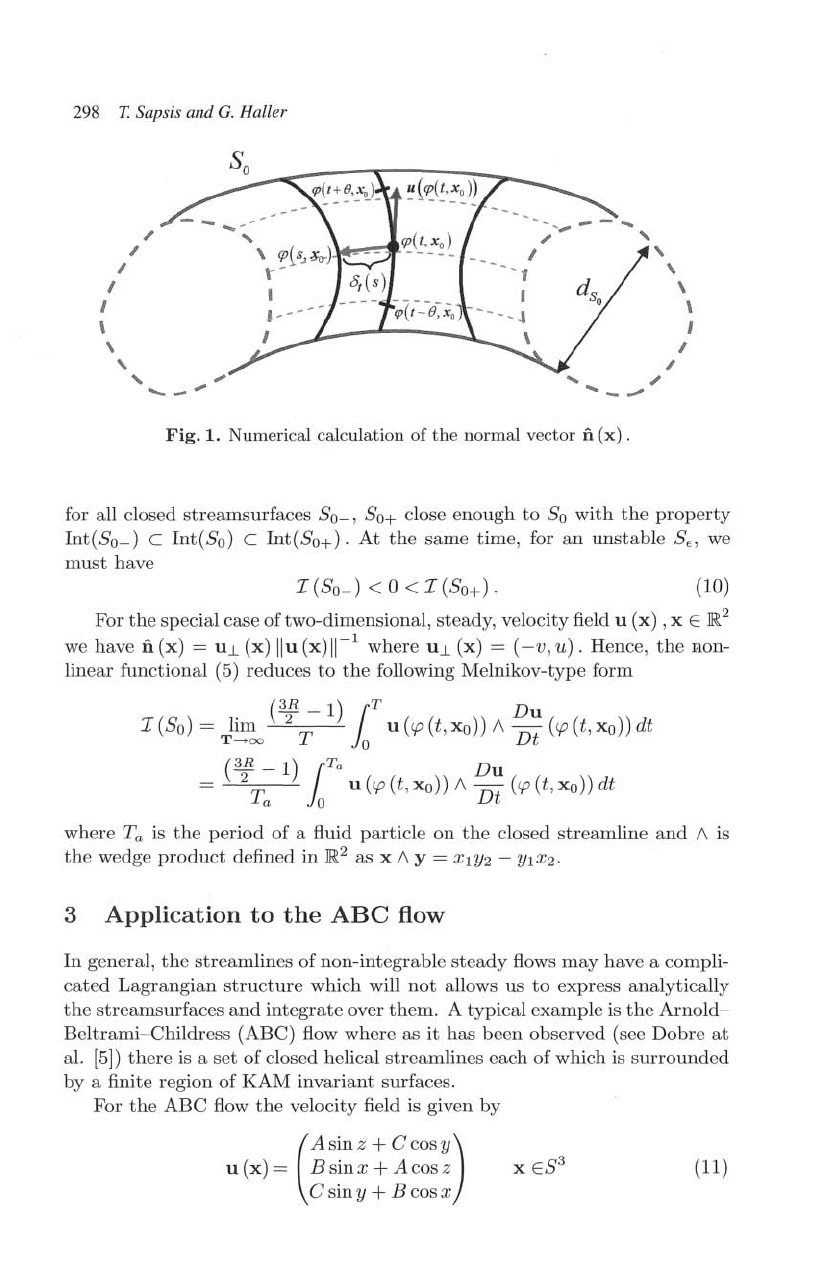

Fig.

1.

Numerical

calculation

of

the

normal

vector

fi

(x)

.

\

\

\

I

I

/

for all closed streamsurfaces

50~

,

5

0

+ close enough

to

50

with

the

property

Int(50~)

C

Int(5

0

)

C

Int(5

0

+

}.

At

the

same

time

, for

an

unstable

5

e

,

we

must

have

(10)

For

the

special case

oftwo

-dimcusional,

ste

ady, velocity field u (x) ,x E

]R2

we have flex) =

U..L

(x)

lI

u(x)

l

l~l

where U

..L

(x) = (- v,

u).

Hence,

the

non-

linear functional

(5)

reduces

to

the

following Melnikov-type form

e

R

-

1)

r

T

Du

I

(So)

=

}~~

2 T

.fa

u(cp(t,xo)) A

Dt

(cp(t,xo))dt

=

(¥T~

1)

laT

a U(cp(t,

XO))

A

~~

(cp

(t,XO)) dt

where

Ta

is

the

period of a fluid particle on

the

closed

st

reamline

and

A is

the

wedge

product

defined in

]R2

as x A y = :rl1/2 -

:t)lX2.

3

Application

to

the

ABC

flow

In

general,

the

streamlines of non-integrable

steady

flows

may

have a compli-

cate

d

Lagran

g

ian

structur

e which will

not

allows us

to

express analytically

the

streamsurfaces

and

integrate

over

them.

A typical example is

th

e Arnold-

Beltrami

- Childress (ABC)

flow

where as

it

has been observed (see Dobre

at

al.

[5])

there

is a set of closed helical streamlines each of which is surrounded

by

a finite region of

KAM

invariant surfaces.

For

the

ABC flow

the

velocity field is given

by

(

ASin Z

+

CCOS

Y)

u (x) =

Bsinx

+

Acos

z

C sin y + B cos x

(11)

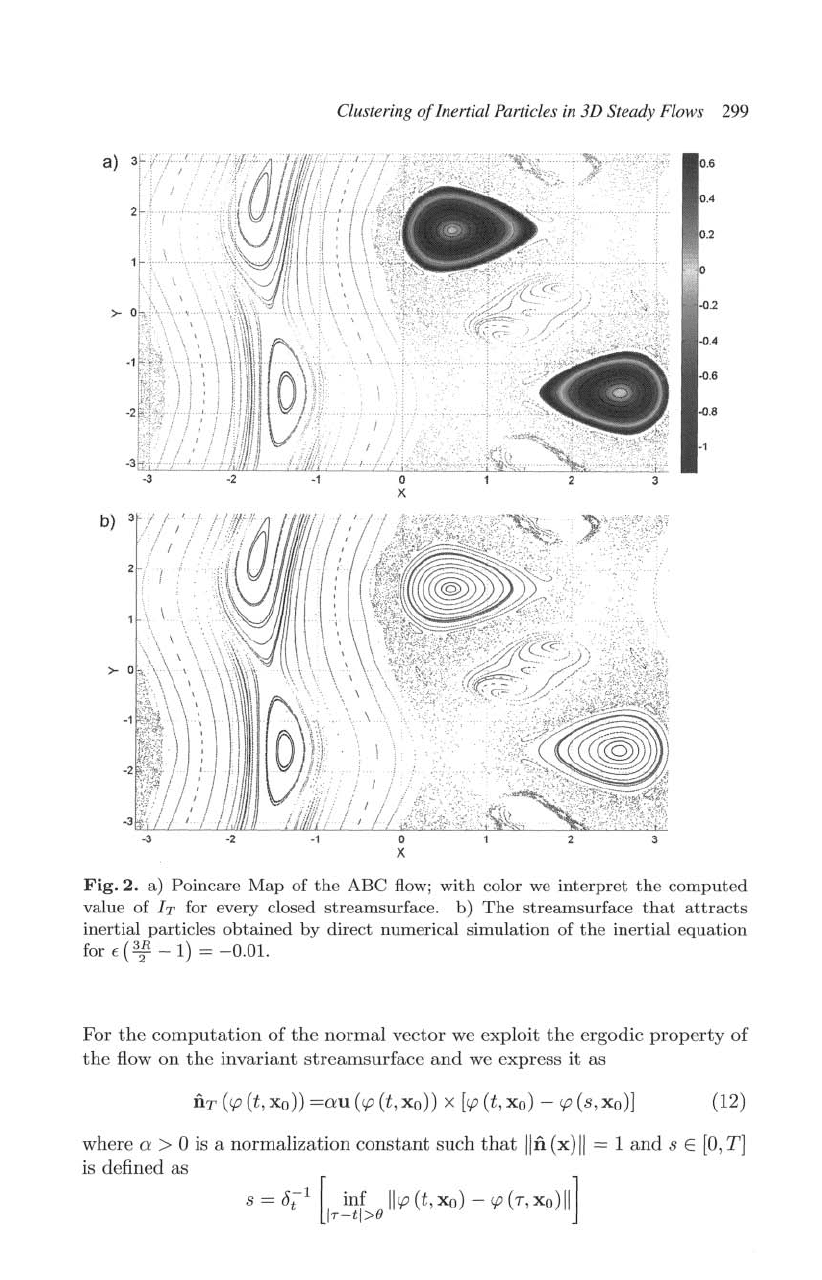

Clustering

of

Inertial Particles in 3D Steady Flows 299

a)

>-

x

Fig.

2.

a)

Poincare

Map

of

the

ABC

flow;

with

col

or

we

interpret

the

comp

uted

value

of

IT for every closed

streams

urfac

e.

b)

The

streamsurface

that

attracts

in

ertia

l

particles

obtained

by direct

numerical

simu

lation

of

the

inerti

al

equation

for

t(

3:

-

1)

=

-0.01.

For

the

computation

of

the

normal vector

we

exploit

the

ergodic

property

of

the

flow

on

the

invariant streamsurface

and

we express

it

as

nT(ip(i,xo))

=O:

U(ip(t,xo)) x

[rp

(t,x

o)

- ip(s,xo)]

(12

)

where

0:

> a

is

a normalization

constant

such

that

lin

(x)11

= 1

and

8 E

[0,

T]

is defined as

8=0;-1

[ inf Ilip(t,XO)-ip(T,

Xo)ll]

I.,.-tl>f)

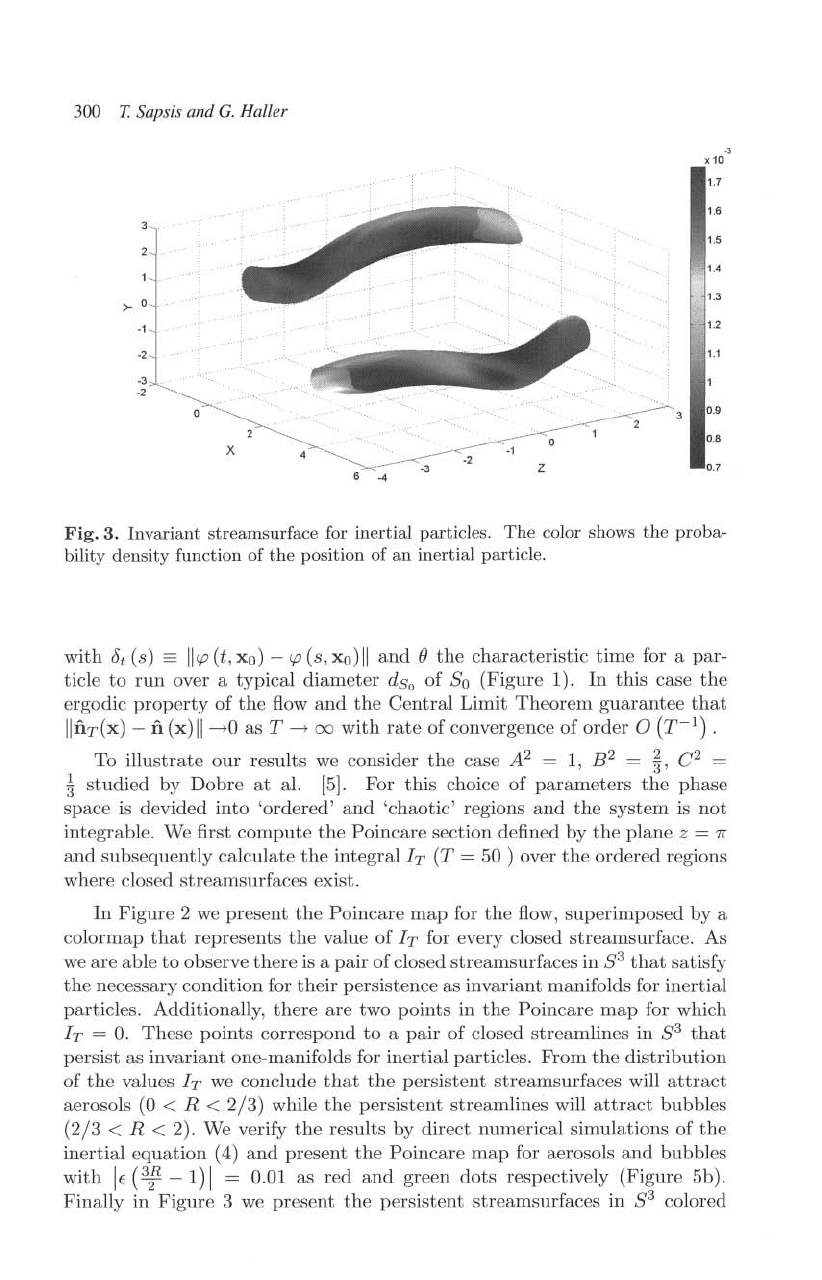

300

T.

Sapsis and

U.

Haller

x

-2

-3

-4

-,

,.

x 10"

I

::

'1.5

~~

f;~~11A

I::

1

:~1'1

'1

'0.9

0,8

0,(

Fig.

3.

Invariant

streamsllrface for

inertial

particles.

The

color

shO\vs

the

proba-,

bility

density

function

of

the

position

of

an

inertial

particle.

with

Ot

(s)

==

11'P(t,xo) - 'P(s,xo)11

and

()

the

characteristic

time

for a

par-

ticle

to

run

over a typical

diameter

ds

o

of

8

0

(Figure 1). In

this

ease

the

ergodic

property

of

the

flow

and

the

Central

Limit

Theorem

gua.rantee

that

IlnT'(x)

-

11

(x)

II~'O

as

T-.,

00

with

rate

of

convergence

of

order

0

(r-l)

.

To

illustrate

our

results

we

consider

the

ease A

2

1, 8

2

=

~)

C

2

=

~

studied

by

Dobre

at

aL

[5].

For this choice

of

parameters

the

phase

space is devided

into

'ordered'

and

'chaotic' regions

and

the

system

is

not

integrable.

vVe

first

compute

the

Poincare

section defined by

the

plane z =

1\

and

sub"equently calculate

the

integral IT' (1' =

50

) over

the

ordered regions

where closed streamsurfaces

exist.

In

Figure 2

we

present

the

F)oincare

map

for

the

flow, superimposed by a

colornlap

that

represents

the

value

of

h· for every closed streamsurface. As

we

are

able

to

observe

there

is a

pair

of

dosed

streamsurfaces

in

S<l

that

satisl:v

the necessary condition for

their

persistence as invariant manifolds for inertial

particles. AdditionaHy.

there

are

two

points

in

the

Poincare

map

for which

IT

O.

These

points

correspond

to

a

pair

of

dosed

streamlines

in

8

3

that

persist as invariant one-manifolds for inertial particles,

From

the

distribution

of

the

valuesTy·

we

conclude

that

the

persistent streamsurfaees will

attract

aerosols

(0

< R < 2/;3) while

the

persistent

streamlines ,\fill

attract

bubbles

(2/;5

< R < 2).

vVe

verify

the

results by direct numerical simulations of

the

inertia.l

equation

(4)

and

present

the

Poincare

map

for aerosols

and

bubbles

with

IE

e2R-l)1

=

(Un

as red

and

green dots respectively (Figure 5b).

Finally in

Figure

:3

we

present

the

persistent

streamsurfaces

in

8

3

colored

Clustering

of

Inertial Particles in

3D

Steady Flows

301

according

to

the

probability

density

function

calculated

through

equation

(6).

4

Conclusions

We have

studied

clustering

properties

of

inertial

particles

in

three-dimensional,

steady

flow fields. Using results

of

Ergodic

theory

we have derived a nec-

essary condition for

the

persistence

of

any

closed

invariant

manifold as a

two-dimensional

invariant

manifold for

inertial

particles.

This

condition

has

the

form

of

a nonlinear functional

that

acts

on

the

unitary

normal

bundle

of

the

streamsurface

and

any

non-resonant

trajectory

that

lies

on

it. We have

illustrated

our

theoretical

findings

through

a

non-integrable

case,

the

ABC

flow,

and

we have

determined

clustering regions for

non-neutrally

buoyant

particles.

Acknowledgements

This

research was

supported

by

NSF

Grant

DMS-04-04845,

AFOSR

Grant

AFOSR

FA 9550-06-0092,

and

an

MIT

Presidential

Fellowship.

References

1.A.

Babiano,

J.

H. E.

Cartwright,

O.

Piro,

and

A.

Provenzale.

Dynamics

of

a

small

neutrally

buoyant

sphere

in a fluid

and

targeting

in

hamiltonian

systems.

Phys.

Rev. Lett., 84:5764, 2000.

2.1.

J.

Benczik,

Z.

Toroczkai,

and

T.

Tel. Selective

sensitivity

of

open

chaotic

flows

on

inertial

tracer

advection:

Catching

particles

with

a stick. Phys. Rev. Lett.,

89:164501,

2002.

3.T.

Burns,

R. Davis,

and

E. Moore. A

perturbation

study

of

particle

dynamics

in

a

plane

wake

flow.

J.

Fluid

Mech., 384:1, 1999.

4.R.

Burton

and

M.

Denker.

On

the

central

limit

theorem

for

dynamical

systems.

Trans.

Amer.

Math. Soc., 302:715, 1987.

5.T.

Dombre,

U. Frisch,

J.

M.

Greene,

M.

Hinon,

A.

Mehr,

and

A. M. Soward.

Chaotic

streamlines

in

the

abc

flows.

J.

Fluid

Mech., 167:353, 1986.

6.G.

Haller

and

T.

Sapsis.

Where

do

inertial

particles

go

in

fluid flows?

Physica

D, 237:573, 2008.

7.A. N. Kolmogorov.

On

dynamical

systems

with

an

integral

invariant

on

the

torus.

Dokl.

Akad.

Nauk, 93:763, 1953.

8.M.

Maxey

and

J.

Riley.

Equation

of

motion

for a

small

rigid

sphere

in a

nonuni-

form

flow. Phys. Fluids, 26:883, 1983.

9.J.

Rubin,

C.

K.

R.

T.

Jones,

and

M. Maxey.

Settling

and

asymptotic

motion

of

aerosol

particles

in a cellular flow field.

J.

Nonlinear

Sci., 5:337, 1995.

W.YA.

G. Sinai.

Introduction

to

ergodic

theory.

Princeton

University Press, 1976.

11.A. N.

Yannacopoulos,

G.

Rowlands,

and

G. P. King.

Influence

of

particle

inertia

and

basset

force

on

tracer

dynamics:

Analytic

results

in

the

small-inertia

limit.

Phys. Rev. E, 55:4148, 1997.

302

A Two Population Model for the

Stock Market Problem

Christos

H.

Skiadas

Technical University

of

Crete, Chania, Crete, Greece

(e-mail:

skiadas@asmda.net)

Abstract: The development

of

the last year disaster in the Stock Markets all over the

world gave rise to reconsidering the previous models used. It is clear that, even in an

organized international or national context, large fluctuations and sudden losses may

occur. This paper explores a two populations' model. The populations are conflicting into

the same environment (a Stock Market) by following the main rules present, that

is

mutual interaction between adopters, potential adopters, word-of-mouth communication

and

of

course by taking into consideration the innovation diffusion process. The

proposed model has special futures expressed by third order terms providing

characteristic stationary points.

Keywords: chaotic modeling, the stock market problem, stock market, innovation

diffusion modeling, Lotka-Volterra, simulation, chaotic simulation.

1.

Introduction

Several attempts to model the stock-market problem can be found in the

literature. Between these models the Lotka-Volterra modeling approach is

of

considerable interest. The model can be used

if

we

assume two interacting

populations and can be generalized to more than two. The case

of

two

interacting populations

is

explored by using two coupled differential equations

and the results found give rise to a limit cycle and the corresponding oscillating

graphs over time, Skiadas,

2009 [7]. However, the Lotka-Volterra system

of

differential equations, a non-linear system

of

the second order, fails to explain

the sudden growth and decline resulting into the stock-market environment and

even more the stability to high or low values (capital gains or losses).

In

view

of

the last year losses in the stock markets globally

it

would be very important to

reconsider the classical Lotka-Volterra theory by introducing into the

corresponding equations terms having to do with the diffusion aspect

of

the

communication process. The proposed model has special futures expressed

by

third order terms providing characteristic stationary points.

It

should be noted

that a seminal paper was published by Harold Hotteling

[1]

during March 1929

few months before the big crash in the New York stock exchange. Hotelling, in

this paper explored the "stability

in

competition" problem. The analysis

proposed was based in a simplification

of

the problem. Only two markets where

competing; however, the results where extremely important and clarified the

situation.

In

this paper

we

accept the same methodology supposing that there is

a stock market with two interacting populations and we explore the arising case.

That is new is the introduction

of

the theories

of

the last decades on the

A

Two

Populatiol1 Model

for

the Stock Market Problem 303

adoption-diffusion

of

innovations in developing the equations

of

the proposed

model.

2. The Model and Simulations

To model the specific situation

we

take into account that two populations x and

yare

present into the stock market and interact each other. Even more to

simplify the case we suppose that the variables

XI

and y, stand for the number

of

players or for the number

of

transactions or for the values

of

the stocks

belonging to each part

of

the players at a specific time period

t.

The aim is to

explore the behavior

of

the two populations during time and especially in the

limits.

A model including the main characteristics

of

two interrelating or even

conflicting popUlations into a stock market can be expressed by the following

set

of

differential equations:

i = a

j

Y + a

2

xy

+ a

3

x(l-

y)

+ a

4

yx(k

-

x)

y

=b

j

x+b

2

xy+b

3

y(k

-x)+b

4

xy(l-

y),

where aj,

a2,

a3,

a4

and bj,

bz,

b

3

,

b

4

are parameters expressing the mutual

interaction

of

the populations X and y. The parameters k and I express the upper

limit

of

the popUlations x and y respectively.

The first term to the right stands for the flows from the one part to the other

whereas the second term expresses the mutual interaction between the active

parts

of

the populations x and

y.

If

we

retain the first two terms to the right the

proposed model is

of

the Lotka-Volterra type.

The non active parts

of

the populations are

(k

-

x)

for x and (l - y) for the

population

y. The interaction

of

these parts with the active popUlations y and x is

expressed with the third terms to the right

of

the above differential equations

(see

[2,

3,4,

5,

6]).

The fourth terms to the right include the terms

x(k

-

x)

and

y(l

-

y)

multiplied by

y and x respectively. These terms account to the rates

of

adoption-diffusion that

is

extremely important in order to express the word-of-mouth communication

between adopters (the active part

of

the players) and potential adopters (the non-

active part

of

the players).

Looking back to the set

of

the two differential equations above we see that

we

have two third degree equations for x and

y.

In the following we check the

influence

of

the third order term to the stock-market model. To this end the

above model is simplified to the following form:

• 2

X =

-ay

+ cyx

. b

2

Y =

x-cxy

,

304

C.

H.

Skiadas

Where

a,

band

c are parameters

of

interaction. Especially the parameter c is

selected to be the same

in

both equations expressing the coupling

of

both

populations

x and y.

The set

of

the last equations takes the form:

i =

-ay

+ cyx

2

=

-cyra;;(.Ja/

c -

x)-

c.xy(Ja/ c - x)

y = bx -

cxy2

=

cx~(.Jb/

c - y)+

c.xy(~

-

y),

The last equations include in the right part side two basic parts

of

the interaction

and the diffusion process where

x = ra;; and y = .J b / c are the upper limit

or the maximum for

x and y respectively.

There

is

a fixed point at (0,

0)

and four other characteristic points at

(x

= ra;; , y = .J b /

c),

(x

= ra;; , y =

-~

)

(x=-ra;;

,y

=~),

(x=-ra;;

,y

=-~)

The last differential equations give the following differential equation for x and

y:

dy

bx-cxy2

dx

-ax+cyx

2

The solution

is

(l-b/c)(X2

-a/c)=h

Where h

is

the integration constant.

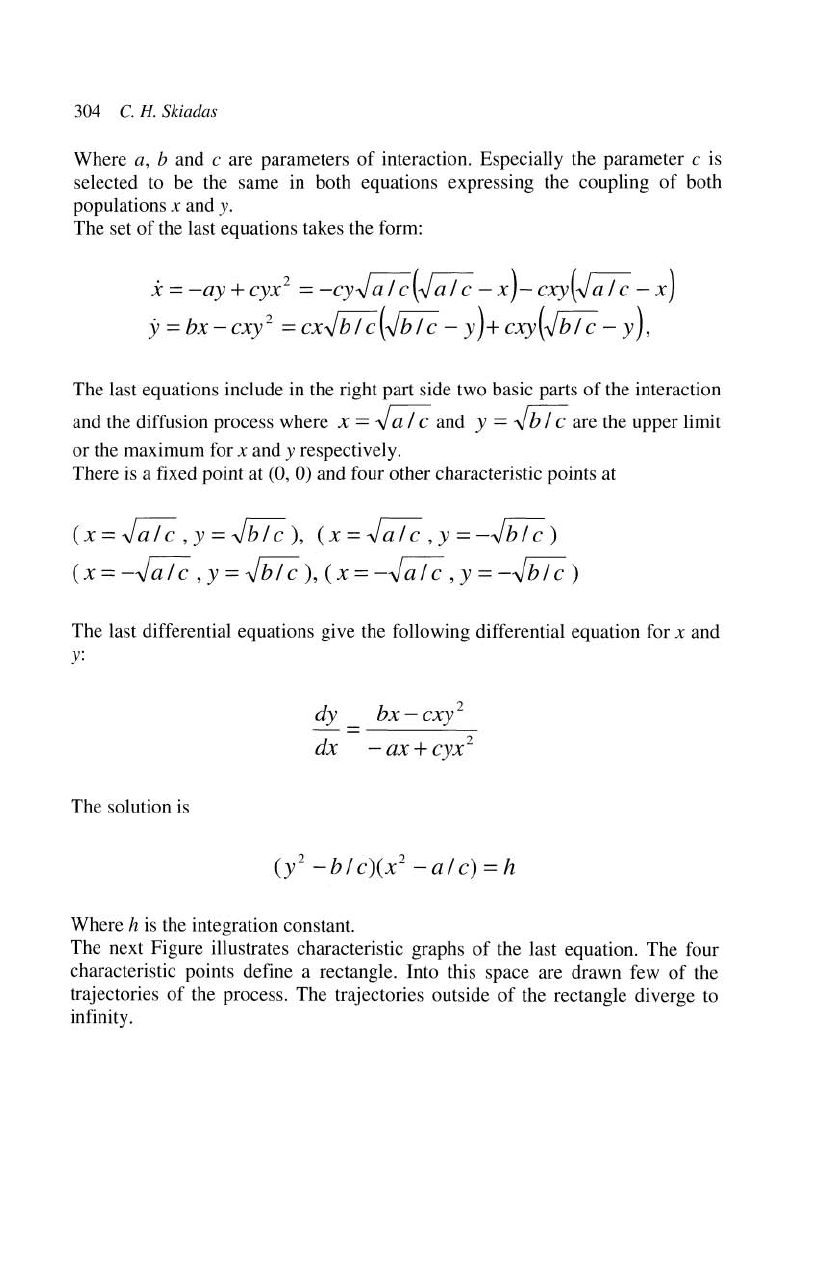

The next Figure illustrates characteristic graphs

of

the last equation. The four

characteristic points define a rectangle. Into this space are drawn few

of

the

trajectories

of

the process. The trajectories outside

of

the rectangle diverge

to

infinity.

A

Two

Population Model

for

the Stock Market Problem 305

)

---~.

-

~

--

----

Figure

1.

Characteristic Trajectories for various

h.

As

it is presented in Figure 1 there appear to be positive and negative values for

the stock-market process. To be realistic

we

will move the main part, that is the

rectangle space, inside the first quarter (the positive space)

of

the Cartesian

Coordinates. This

is

achieved by introducing the transformation x*=x-el and

y*=y-

e

2·

The resulting set

of

differential equations is:

x =

-a(y

- e

2

)

+

c(y

- e

2

)(x

- e

j

)2

y =

b(x

- e

j

) -

c(x

- e

j

)(Y - e

2

)2

,

Where x stands for x* and y for y*.

We can also find the corresponding difference equation form for this system by

observing that

.

dx

Lix

x

t

+

1

-

x

t

X = -

""

- = =

Xt+1

-

xr

dt

M

(t

+

1)

- t

. dy

i1y

Yr+l

- Y

r

Y

=

dt

""

---;; =

(t

+

1)

- t =

Yt+j

- Y

r

The resulting difference equations set

is:

X

t

+

1

=xr

-a(Yr

-e

2

)+C(Yr

-e

2

)(x

r

_e

j

)2

Yr+l

= Y

r

+b(xr

-el)-c(x

r

-ej)(Yr

-e

2

)2,

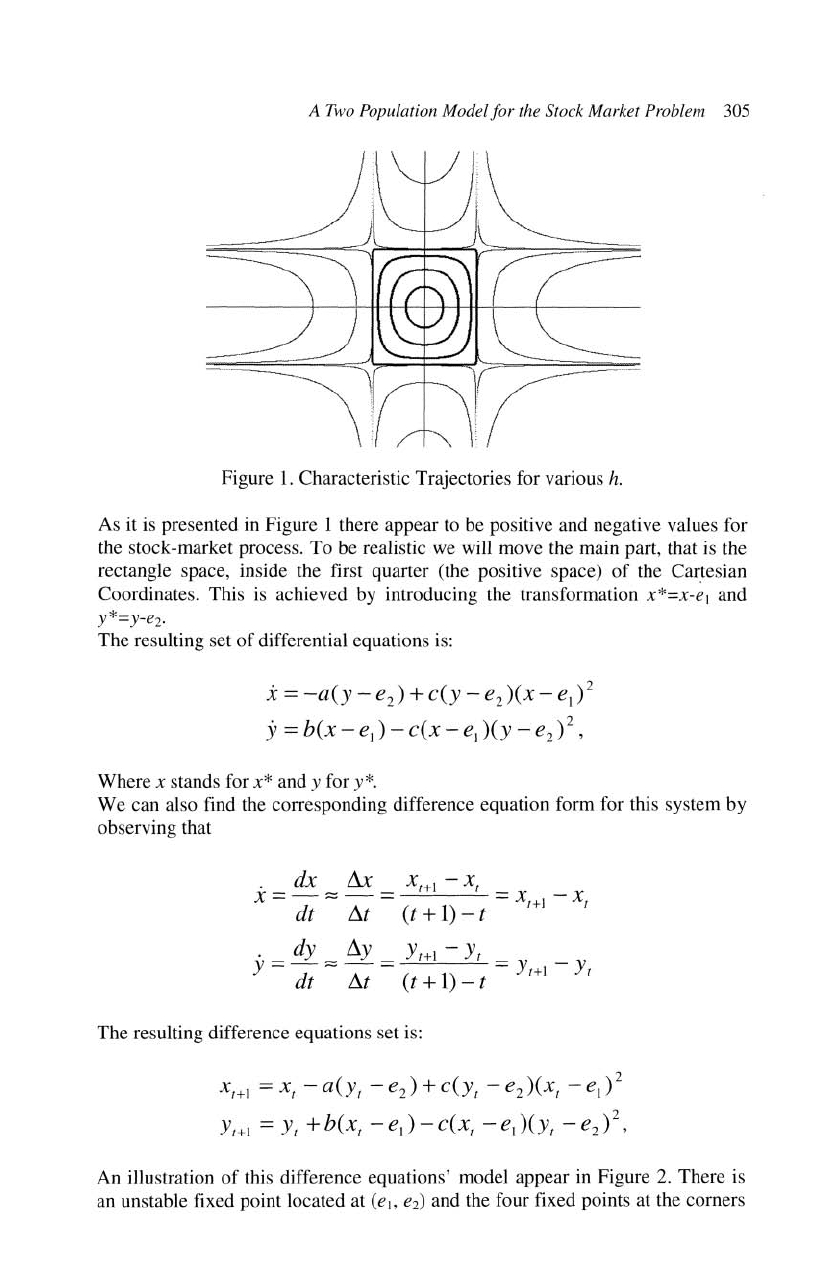

An illustration

of

this difference equations' model appear

in

Figure

2.

There is

an unstable fixed point located at

(e"

e2) and the four fixed points at the corners

306

C.

H.

Skiadas

of

the rectangle. The process can stabilized at any

of

the four points depending

on the starting values

or

on values

of

the parameters. That is extremely

important is that we may have four specific cases when

aJter some time the

process

is stabilized in which:

I.

(x

= e

1

-+;;;t;. y:::: e

2

-+

-Jb/

c);

both gains

2. (x:::: e

J

+

-Ja/

c,)'::::; e

2

-

-Jb/

c

);x

gains,y losses

3. ( X ::: e

J

--

J;;iz,

. y = e

2

+,J

b / c

);

x losses, y gains

4.

(x

= e

j

-,J a / c

,y

::-..:

e

2

-.J

b / c

);

both losses

In Figure

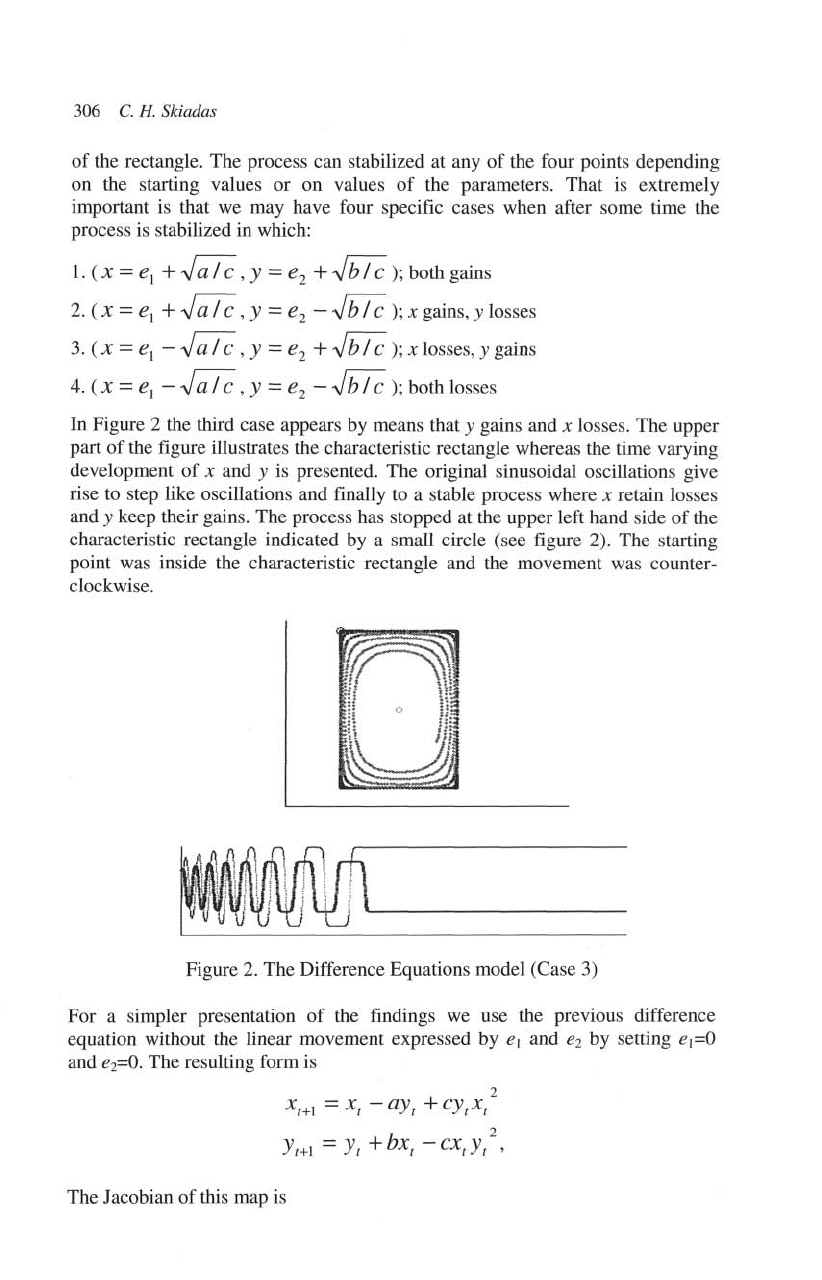

2 the third case appears by means that y gains and x losses. The upper

part

of

the figure illustrates the charactelistic rectangle whereas the time varying

development

of

x and y is presented. The original sinusoidal oscillations give

rise to step

like oscillations and finally to a stable process where x retain losses

and y keep their gains. The process has stopped at the upper left hand side

of

the

charactclistic rectangle indicated

by a small circle (see fjgure 2). The starting

point was inside the characteristic

rectangle and the movement was counter-

clockwise.

-~-----

V U

(-.J

'-------------

Figure 2. The Difference Equations model (Case 3)

For

a simpler presentation

of

the findings

we

use the previous difference

equation without the linear movement expressed

by ej and

ez

by

setting

el=O

and

ez=O.

The resulting form is

J

x

r

+]

:::::

XI

-

aY

t

-+

eytx

t

-

2

Yt+l

==)'/

+bX

t

-ext)'t

'

The Jacobian

of

this map

is

A

7\1'0

Population Modelfor the Stock

Marker

Problem 307

] +2cxy

l(x,),)

= 1

b-cy~

The value

of

the Jacobian at the characteristic point (0, 0) is:

J (0,0)

=:

1 + ab . Assuming positive parameters a and h the point (0,0) is

unstable.

The Jacobian

at the other 4 characteristic points

(±,j

a / c

,±,jb

/

c)

is

J (0,0)

=:

1-

4ab, and for appropriate positive values

of

the parameters the 4

points are stable (attracting).

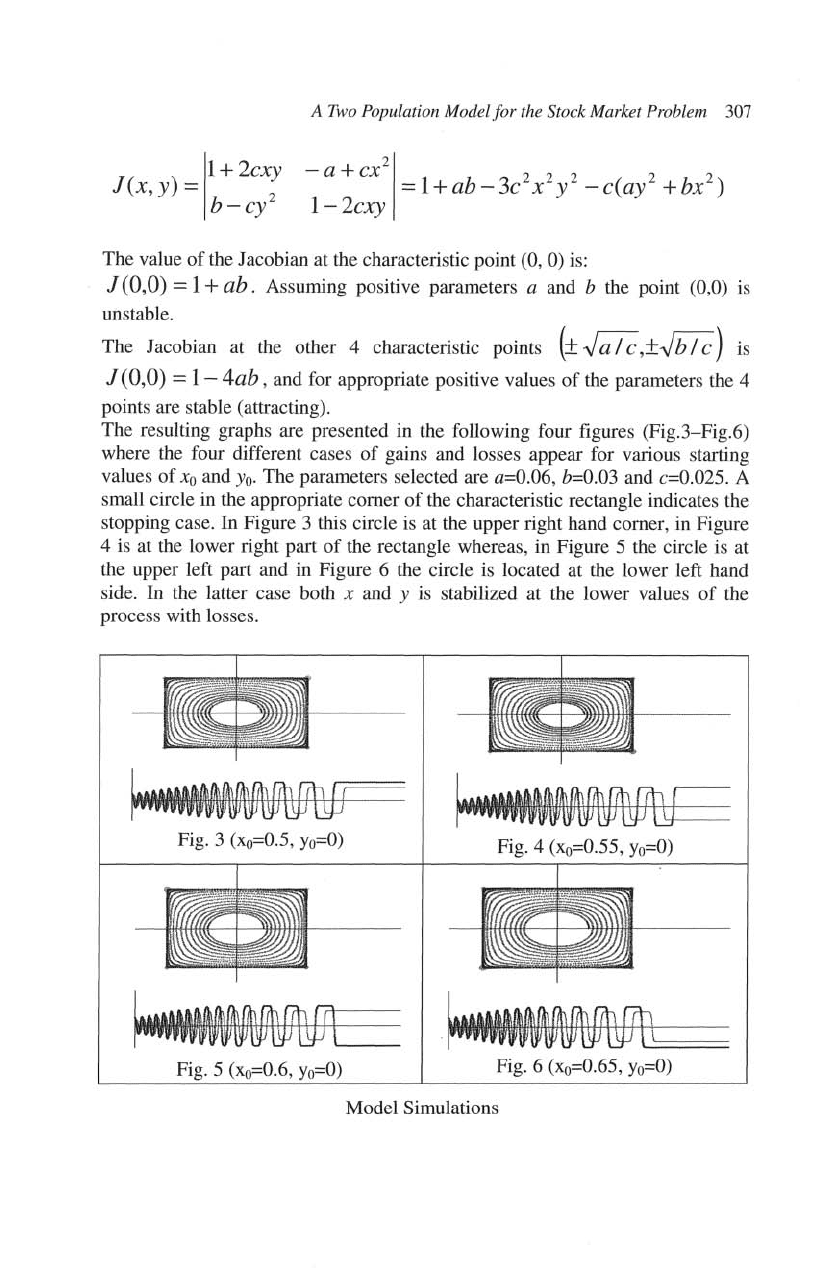

The resulting graphs are presented in the following four figures (Fig.3-Fig.6)

where the four different cases

of

gains and losses appear for various statiing

values

of

Xo and

Yo.

The parameters selected are a=0.06,

h=O.03

and c=0.025. A

small circle in the appropriate comer

of

the charactetistic rectangle indicates the

stopping case. In Figure 3 this circle

is at the upper light hand comer, in Figure

4

is at the lower right part

of

the rectangle whereas, in Figure 5 the circle is at

the upper left part and in Figure 6 the

circle is located at the lower left hand

side.

In

the latter case both x and y is stabilized at the lower values

of

the

process with losses.

lih

frt,

(T--===

¥@Tl1tj-------

tt~fJt\-m:\-t==

1].1

l::t'

L':t------

Fig. 3

(xo=O.5,

Yo=O)

Fig. 4

(xo=O.55,

Yo=O)

5

(xo=O.6,

Yo=O)

Fig. 6

(xo==O.65,

Yo=O)

Model Simulations