Tan S.T. Finite Mathematics for the Managerial, Life, and Social Sciences

Подождите немного. Документ загружается.

APPLIED EXAMPLE 6

Sinking Fund The proprietor of Carson

Hardware has decided to set up a sinking fund for the purpose of purchasing

a truck in 2 years’ time. It is expected that the truck will cost $30,000. If the fund

earns 10% interest per year compounded quarterly, determine the size of each

(equal) quarterly installment the proprietor should pay into the fund. Verify the

result by displaying the schedule.

Solution

The problem at hand is to find the size of each quarterly payment R

of an annuity given that its future value is S 30,000, the interest earned per

conversion period is , and the number of payments is

n (2)(4) 8. The formula for an annuity,

when solved for R yields

(14)

or, equivalently,

Substituting the appropriate numerical values for i, S, and n into Equation (14), we

obtain the desired quarterly payment

or $3434.02. Table 5 shows the required schedule.

The formula derived in this last example is restated as follows.

R

10.0252130,000 2

11.0252

8

1

⬇ 3434.02

R

S

s

n

|i

R

iS

11 i2

n

1

S R c

11 i2

n

1

i

d

i

r

m

0.1

4

0.025

292 5 MATHEMATICS OF FINANCE

TABLE 5

A Sinking Fund Schedule

End of Deposit Interest Addition Accumulated

Period Made Earned to Fund Amount in Fund

1 $3,434.02 0 $3,434.02 $ 3,434.02

2 3,434.02 $ 85.85 3,519.87 6,953.89

3 3,434.02 173.85 3,607.87 10,561.76

4 3,434.02 264.04 3,698.06 14,259.82

5 3,434.02 356.50 3,790.52 18,050.34

6 3,434.02 451.26 3,885.28 21,935.62

7 3,434.02 548.39 3,982.41 25,918.03

8 3,434.02 647.95 4,081.97 30,000.00

Sinking Fund Payment

The periodic payment R required to accumulate a sum of S dollars over n peri-

ods with interest charged at the rate of i per period is

(15)R

iS

11 i2

n

1

87533_05_ch5_p257-312 1/30/08 9:55 AM Page 292

Here is a summary of the formulas developed thus far in this chapter:

1. Simple and compound interest; annuities

2. Effective rate of interest

3. Amortization

Periodic payment

Amount amortized

4. Sinking fund

Periodic payment taken out

R

iS

11 i2

n

1

P R c

1 11 i2

n

i

d

R

Pi

1 11 i 2

n

r

eff

a1

r

m

b

m

1

5.3 AMORTIZATION AND SINKING FUNDS 293

One deposit Periodic deposits

Simple interest Compound interest Future value of Present value of

an annuity an annuity

Continuous compounding

Continuous compounding

P Ae

rt

A Pe

rt

P A11 i2

n

I Prt

P R c

1 11 i2

n

i

dS R c

11 i2

n

1

i

dA P11 i2

n

A P11 rt2

5.3 Self-Check Exercises

1. The Mendozas wish to borrow $300,000 from a bank to help

finance the purchase of a house. Their banker has offered the

following plans for their consideration. In plan I, the Men-

dozas have 30 yr to repay the loan in monthly installments

with interest on the unpaid balance charged at 6.09%/year

compounded monthly. In plan II, the loan is to be repaid in

monthly installments over 15 yr with interest on the unpaid

balance charged at 5.76%/year compounded monthly.

a. Find the monthly repayment for each plan.

b. What is the difference in total payments made under

each plan?

2. Harris, a self-employed individual who is 46 yr old, is set-

ting up a defined-benefit retirement plan. If he wishes to

have $250,000 in this retirement account by age 65, what

is the size of each yearly installment he will be required to

make into a savings account earning interest at %/year?

Solutions to Self-Check Exercises 5.3 can be found on

page 297.

8

1

4

5.3 Concept Questions

1. Write the amortization formula.

a. If P and i are fixed and n is allowed to increase, what

will happen to R?

b. Interpret the result of part (a).

2. Using the formula for computing a sinking fund payment,

show that if the number of payments into a sinking fund

increases, then the size of the periodic payment into the

sinking fund decreases.

87533_05_ch5_p257-312 1/30/08 9:55 AM Page 293

In Exercises 1–8, find the periodic payment R required to

amortize a loan of P dollars over t yr with interest charged

at the rate of r %/year compounded m times a year.

1. P 100,000, r 8, t 10, m 1

2. P 40,000, r 3, t 15, m 2

3. P 5000, r 4, t 3, m 4

4. P 16,000, r 9, t 4, m 12

5. P 25,000, r 3, t 12, m 4

6. P 80,000, r 10.5, t 15, m 12

7. P 80,000, r 10.5, t 30, m 12

8. P 100,000, r 10.5, t 25,

m 12

In Exercises 9–14, find the periodic payment R required to

accumulate a sum of S dollars over t yr with interest

earned at the rate of r %/year compounded m times a year.

9. S 20,000, r 4, t 6, m 2

10. S 40,000, r 4, t 9, m 4

11. S 100,000, r 4.5, t 20, m 6

12. S 120,000, r 4.5, t 30, m 6

13. S 250,000, r 10.5, t 25, m 12

14. S 350,000, r 7.5, t 10, m 12

15. Suppose payments were made at the end of each quarter

into an ordinary annuity earning interest at the rate of

10%/year compounded quarterly. If the future value of the

annuity after 5 yr is $50,000, what was the size of each

payment?

16. Suppose payments were made at the end of each month

into an ordinary annuity earning interest at the rate of

9%/year compounded monthly. If the future value of the

annuity after 10 yr is $60,000, what was the size of each

payment?

17. Suppose payments will be made for yr at the end of each

semiannual period into an ordinary annuity earning interest

at the rate of 7.5%/year compounded semiannually. If the

present value of the annuity is $35,000, what should be the

size of each payment?

18. Suppose payments will be made for yr at the end of each

month into an ordinary annuity earning interest at the rate

of 6.25%/year compounded monthly. If the present value

of the annuity is $42,000, what should be the size of each

payment?

19. L

OAN

A

MORTIZATION

A sum of $100,000 is to be repaid

over a 10-yr period through equal installments made at the

end of each year. If an interest rate of 10%/year is charged

9

1

4

6

1

2

294 5 MATHEMATICS OF FINANCE

on the unpaid balance and interest calculations are made at

the end of each year, determine the size of each installment

so that the loan (principal plus interest charges) is amor-

tized at the end of 10 yr.

20. L

OAN

A

MORTIZATION

What monthly payment is required to

amortize a loan of $30,000 over 10 yr if interest at the rate

of 12%/year is charged on the unpaid balance and interest

calculations are made at the end of each month?

21. H

OME

M

ORTGAGES

Complete the following table, which

shows the monthly payments on a $100,000, 30-yr mort-

gage at the interest rates shown. Use this information to

answer the following questions.

Amount of Interest Monthly

Mortgage, $ Rate, % Payment, $

100,000 7 665.30

100,000 8

100,000 9

100,000 10

100,000 11

100,000 12 1028.61

a. What is the difference in monthly payments between a

$100,000, 30-yr mortgage secured at 7%/year and one

secured at 10%/year?

b. Use the table to calculate the monthly mortgage pay-

ments on a $150,000 mortgage at 10%/year over 30 yr

and a $50,000 mortgage at 10%/year over 30 yr.

22. F

INANCING A

H

OME

The Flemings secured a bank loan of

$288,000 to help finance the purchase of a house. The bank

charges interest at a rate of 9%/year on the unpaid balance,

and interest computations are made at the end of each

month. The Flemings have agreed to repay the loan in

equal monthly installments over 25 yr. What should be the

size of each repayment if the loan is to be amortized at the

end of the term?

23. F

INANCING A

C

AR

The price of a new car is $16,000.

Assume that an individual makes a down payment of 25%

toward the purchase of the car and secures financing for the

balance at the rate of 10%/year compounded monthly.

a. What monthly payment will she be required to make if

the car is financed over a period of 36 mo? Over a

period of 48 mo?

b. What will the interest charges be if she elects the 36-mo

plan? The 48-mo plan?

24. F

INANCIAL

A

NALYSIS

A group of private investors pur-

chased a condominium complex for $2 million. They made

an initial down payment of 10% and obtained financing for

the balance. If the loan is to be amortized over 15 yr at an

interest rate of 12%/year compounded quarterly, find the

required quarterly payment.

25. F

INANCING A

H

OME

The Taylors have purchased a

$270,000 house. They made an initial down payment of

$30,000 and secured a mortgage with interest charged at

5.3 Exercises

87533_05_ch5_p257-312 1/30/08 9:55 AM Page 294

the rate of 8%/year on the unpaid balance. Interest compu-

tations are made at the end of each month. If the loan is to

be amortized over 30 yr, what monthly payment will the

Taylors be required to make? What is their equity (disre-

garding appreciation) after 5 yr? After 10 yr? After 20 yr?

26. F

INANCIAL

P

LANNING

Jessica wants to accumulate $10,000

by the end of 5 yr in a special bank account, which she had

opened for this purpose. To achieve this goal, Jessica plans

to deposit a fixed sum of money into the account at the end

of each month over the 5-yr period. If the bank pays inter-

est at the rate of 5%/year compounded monthly, how much

does she have to deposit each month into her account?

27. S

INKING

F

UNDS

A city has $2.5 million worth of school

bonds that are due in 20 yr and has established a sinking

fund to retire this debt. If the fund earns interest at the rate

of 7%/year compounded annually, what amount must be

deposited annually in this fund?

28. T

RUST

F

UNDS

Carl is the beneficiary of a $20,000 trust

fund set up for him by his grandparents. Under the terms of

the trust, he is to receive the money over a 5-yr period in

equal installments at the end of each year. If the fund earns

interest at the rate of 9%/year compounded annually, what

amount will he receive each year?

29. S

INKING

F

UNDS

Lowell Corporation wishes to establish a

sinking fund to retire a $200,000 debt that is due in 10 yr. If

the investment will earn interest at the rate of 9%/year com-

pounded quarterly, find the amount of the quarterly deposit

that must be made in order to accumulate the required sum.

30. S

INKING

F

UNDS

The management of Gibraltar Brokerage

Services anticipates a capital expenditure of $20,000 in

3 yr for the purchase of new computers and has decided to

set up a sinking fund to finance this purchase. If the fund

earns interest at the rate of 10%/year compounded quar-

terly, determine the size of each (equal) quarterly install-

ment that should be deposited in the fund.

31. R

ETIREMENT

A

CCOUNTS

Andrea, a self-employed individ-

ual, wishes to accumulate a retirement fund of $250,000.

How much should she deposit each month into her retire-

ment account, which pays interest at the rate of 8.5%/year

compounded monthly, to reach her goal upon retirement

25 yr from now?

32. S

TUDENT

L

OANS

Joe secured a loan of $12,000 3 yr ago from

a bank for use toward his college expenses. The bank

charged interest at the rate of 4%/year compounded monthly

on his loan. Now that he has graduated from college, Joe

wishes to repay the loan by amortizing it through monthly

payments over 10 yr at the same interest rate. Find the size

of the monthly payments he will be required to make.

33. R

ETIREMENT

A

CCOUNTS

Robin wishes to accumulate a sum

of $450,000 in a retirement account by the time of her

retirement 30 yr from now. If she wishes to do this through

monthly payments into the account that earn interest at the

rate of 10%/year compounded monthly, what should be the

size of each payment?

34. F

INANCING

C

OLLEGE

E

XPENSES

Yumi’s grandparents pre-

sented her with a gift of $20,000 when she was 10 yr old to

be used for her college education. Over the next 7 yr, until

she turned 17, Yumi’s parents had invested her money in a

tax-free account that had yielded interest at the rate of

5.5%/year compounded monthly. Upon turning 17, Yumi

now plans to withdraw her funds in equal annual install-

ments over the next 4 yr, starting at age 18. If the college

fund is expected to earn interest at the rate of 6%/year, com-

pounded annually, what will be the size of each installment?

35. IRA

S

Martin has deposited $375 in his IRA at the end of

each quarter for the past 20 yr. His investment has earned

interest at the rate of 8%/year compounded quarterly over

this period. Now, at age 60, he is considering retirement.

What quarterly payment will he receive over the next

15 yr? (Assume that the money is earning interest at the

same rate and that payments are made at the end of each

quarter.) If he continues working and makes quarterly pay-

ments of the same amount in his IRA until age 65, what

quarterly payment will he receive from his fund upon

retirement over the following 10 yr?

36. F

INANCING A

C

AR

Darla purchased a new car during a spe-

cial sales promotion by the manufacturer. She secured a

loan from the manufacturer in the amount of $16,000 at a

rate of 7.9%/year compounded monthly. Her bank is now

charging 11.5%/year compounded monthly for new car

loans. Assuming that each loan would be amortized by

36 equal monthly installments, determine the amount of

interest she would have paid at the end of 3 yr for each

loan. How much less will she have paid in interest pay-

ments over the life of the loan by borrowing from the man-

ufacturer instead of her bank?

37. A

UTO

F

INANCING

Dan is contemplating trading in his car

for a new one. He can afford a monthly payment of at most

$400. If the prevailing interest rate is 7.2%/year com-

pounded monthly for a 48-mo loan, what is the most

expensive car that Dan can afford, assuming that he will

receive $8000 for the trade-in?

38. A

UTO

F

INANCING

Paula is considering the purchase of a new

car. She has narrowed her search to two cars that are equally

appealing to her. Car A costs $28,000, and car B costs

$28,200. The manufacturer of car A is offering 0% financing

for 48 months with zero down, while the manufacturer of car

B is offering a rebate of $2000 at the time of purchase plus

financing at the rate of 3%/year compounded monthly over

48 mo with zero down. If Paula has decided to buy the car

with the lower net cost to her, which car should she purchase?

39. F

INANCING A

H

OME

The Sandersons are planning to refi-

nance their home. The outstanding principal on their orig-

inal loan is $100,000 and was to be amortized in 240 equal

monthly installments at an interest rate of 10%/year com-

pounded monthly. The new loan they expect to secure is to

be amortized over the same period at an interest rate of

7.8%/year compounded monthly. How much less can they

expect to pay over the life of the loan in interest payments

by refinancing the loan at this time?

5.3 AMORTIZATION AND SINKING FUNDS 295

87533_05_ch5_p257-312 1/30/08 9:55 AM Page 295

40. I

NVESTMENT

A

NALYSIS

Since he was 22 years old, Ben has

been depositing $200 at the end of each month into a tax-

free retirement account earning interest at the rate of

6.5%/year compounded monthly. Larry, who is the same

age as Ben, decided to open a tax-free retirement account

5 yr after Ben opened his. If Larry’s account earns inter-

est at the same rate as Ben’s, determine how much Larry

should deposit each month into his account so that both

men will have the same amount of money in their accounts

at age 65.

41. P

ERSONAL

L

OANS

Two years ago, Paul borrowed $10,000

from his sister Gerri to start a business. Paul agreed to pay

Gerri interest for the loan at the rate of 6%/year, com-

pounded continuously. Paul will now begin repaying the

amount he owes by amortizing the loan (plus the interest

that has accrued over the past 2 yr) through monthly pay-

ments over the next 5 yr at an interest rate of 5%/year com-

pounded monthly. Find the size of the monthly payments

Paul will be required to make.

42. R

EFINANCING A

H

OME

Josh purchased a condominium 5 yr

ago for $180,000. He made a down payment of 20% and

financed the balance with a 30-yr conventional mortgage

to be amortized through monthly payments with an interest

rate of 7%/year compounded monthly on the unpaid bal-

ance. The condominium is now appraised at $250,000.

Josh plans to start his own business and wishes to tap into

the equity that he has in the condominium. If Josh can

secure a new mortgage to refinance his condominium

based on a loan of 80% of the appraised value, how much

cash can Josh muster for his business? (Disregard taxes.)

43. F

INANCING A

H

OME

Eight years ago, Kim secured a bank

loan of $180,000 to help finance the purchase of a house.

The mortgage was for a term of 30 yr, with an interest rate

of 9.5%/year compounded monthly on the unpaid balance

to be amortized through monthly payments. What is the

outstanding principal on Kim’s house now?

44. B

ALLOON

P

AYMENT

M

ORTGAGES

Olivia plans to secure a

5-yr balloon mortgage of $200,000 toward the purchase of

a condominium. Her monthly payment for the 5 yr is cal-

culated on the basis of a 30-yr conventional mortgage at

the rate of 6%/year compounded monthly. At the end of the

5 yr, Olivia is required to pay the balance owed (the “bal-

loon” payment). What will be her monthly payment, and

what will be her balloon payment?

45. B

ALLOON

P

AYMENT

M

ORTGAGES

Emilio is securing a 7-yr

Fannie Mae “balloon” mortgage for $280,000 to finance

the purchase of his first home. The monthly payments are

based on a 30-yr amortization. If the prevailing interest rate

is 7.5%/year compounded monthly, what will be Emilio’s

monthly payment? What will be his “balloon” payment at

the end of 7 yr?

46. F

INANCING A

H

OME

Sarah secured a bank loan of $200,000

for the purchase of a house. The mortgage is to be amor-

tized through monthly payments for a term of 15 yr, with

an interest rate of 6%/year compounded monthly on the

unpaid balance. She plans to sell her house in 5 yr. How

much will Sarah still owe on her house?

47. H

OME

R

EFINANCING

Four years ago, Emily secured a bank

loan of $200,000 to help finance the purchase of an apart-

ment in Boston. The term of the mortgage is 30 yr, and the

interest rate is 9.5%/year compounded monthly. Because

the interest rate for a conventional 30-yr home mortgage

has now dropped to 6.75%/year compounded monthly,

Emily is thinking of refinancing her property.

a. What is Emily’s current monthly mortgage payment?

b. What is Emily’s current outstanding principal?

c. If Emily decides to refinance her property by securing a

30-yr home mortgage loan in the amount of the current

outstanding principal at the prevailing interest rate of

6.75%/year compounded monthly, what will be her

monthly mortgage payment?

d. How much less would Emily’s monthly mortgage pay-

ment be if she refinances?

48. H

OME

R

EFINANCING

Five years ago, Diane secured a bank

loan of $300,000 to help finance the purchase of a loft in

the San Francisco Bay area. The term of the mortgage was

30 yr, and the interest rate was 9%/year compounded

monthly on the unpaid balance. Because the interest rate

for a conventional 30-yr home mortgage has now dropped

to 7%/year compounded monthly, Diane is thinking of refi-

nancing her property.

a. What is Diane’s current monthly mortgage payment?

b. What is Diane’s current outstanding principal?

c. If Diane decides to refinance her property by securing a

30-yr home mortgage loan in the amount of the current

outstanding principal at the prevailing interest rate of

7%/year compounded monthly, what will be her monthly

mortgage payment?

d. How much less would Diane’s monthly mortgage pay-

ment be if she refinances?

49. A

DJUSTABLE

-R

ATE

M

ORTGAGES

Three years ago, Samantha

secured an adjustable-rate mortgage (ARM) loan to help fi-

nance the purchase of a house. The amount of the original

loan was $150,000 for a term of 30 yr, with interest at the

rate of 7.5%/year compounded monthly. Currently the

interest rate is 7%/year compounded monthly, and Saman-

tha’s monthly payments are due to be recalculated. What

will be her new monthly payment?

Hint: Calculate her current outstanding principal. Then, to amor-

tize the loan in the next 27 yr, determine the monthly payment

based on the current interest rate.

50. A

DJUSTABLE

-R

ATE

M

ORTGAGES

George secured an adjustable-

rate mortgage (ARM) loan to help finance the purchase of

his home 5 yr ago. The amount of the loan was $300,000 for

a term of 30 yr, with interest at the rate of 8%/year com-

pounded monthly. Currently, the interest rate for his ARM is

6.5%/year compounded monthly, and George’s monthly pay-

ments are due to be reset. What will be the new monthly

payment?

296

5 MATHEMATICS OF FINANCE

87533_05_ch5_p257-312 1/30/08 9:55 AM Page 296

51. F

INANCING A

H

OME

After making a down payment of

$25,000, the Meyers need to secure a loan of $280,000 to

purchase a certain house. Their bank’s current rate for 25-yr

home loans is 11%/year compounded monthly. The owner

has offered to finance the loan at 9.8%/year compounded

monthly. Assuming that both loans would be amortized over

a 25-yr period by 300 equal monthly installments, determine

the difference in the amount of interest the Meyers would pay

by choosing the seller’s financing rather than their bank’s.

52. R

EFINANCING A

H

OME

The Martinezes are planning to refi-

nance their home. The outstanding balance on their origi-

nal loan is $150,000. Their finance company has offered

them two options:

Option A: A fixed-rate mortgage at an interest rate of

7.5%/year compounded monthly, payable over a 30-yr

period in 360 equal monthly installments.

Option B: A fixed-rate mortgage at an interest rate of

7.25%/year compounded monthly, payable over a 15-yr

period in 180 equal monthly installments.

a. Find the monthly payment required to amortize each of

these loans over the life of the loan.

b. How much interest would the Martinezes save if they

chose the 15-yr mortgage instead of the 30-yr mort-

gage?

5.3 AMORTIZATION AND SINKING FUNDS 297

5.3 Solutions to Self-Check Exercises

1. a. We use Equation (13) in each instance. Under plan I,

Therefore, the size of each monthly repayment under

plan I is

or $1816.05.

Under plan II,

Therefore, the size of each monthly repayment under

plan II is

or $2492.84.

⬇ 2492.84

R

300,00010.00482

1 11.00482

180

n 11521122 180

P 300,000

i

r

m

0.0576

12

0.0048

⬇ 1816.05

R

300,00010.0050752

1 11.0050752

360

n 13021122 360

P 100,000

i

r

m

0.0609

12

0.005075

b. Under plan I, the total amount of repayments will be

(360)(1816.05) 653,778 Number of payments

the size of each installment

or $653,778. Under plan II, the total amount of repay-

ments will be

(180)(2492.84) 448,711.20

or $448,711.20. Therefore, the difference in payments

is

653,778 448,711.20 205,066.80

or $205,066.80.

2. We use Equation (15) with

S 250,000

i r 0.0825

Since

m

1

n 20

giving the required size of each installment as

or $5313.59.

⬇ 5313.59

R

10.082521250,0002

11.08252

20

1

USING

TECHNOLOGY

Amortizing a Loan

Graphing Utility

Here we use the TI-83/84

TVM SOLVER

function to help us solve problems involving

amortization and sinking funds.

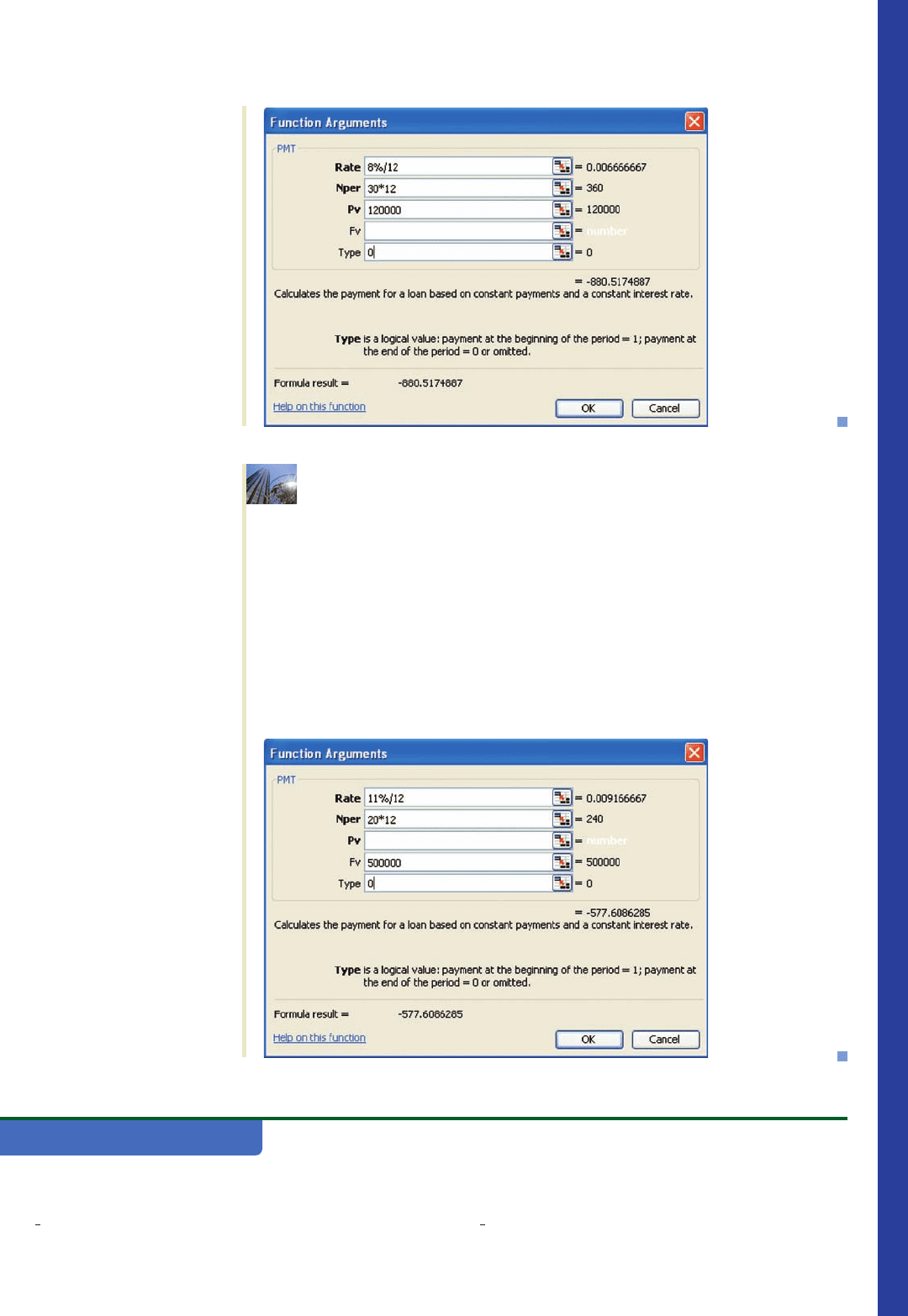

APPLIED EXAMPLE 1

Finding the Payment to Amortize a Loan

The Wongs are considering obtaining a preapproved 30-year loan of

$120,000 to help finance the purchase of a house. The mortgage company

(continued)

87533_05_ch5_p257-312 1/30/08 9:55 AM Page 297

charges interest at the rate of 8% per year on the unpaid balance, with interest

computations made at the end of each month. What will be the monthly install-

ments if the loan is amortized?

Solution

We use the TI-83/84

TVM SOLVER

with the following inputs:

N 360

(30)(12)

I% 8

PV 120000

PMT 0

FV 0

P/Y 12

The number of payments each year

C/Y 12 The number of conversion periods each year

PMT:END BEGIN

From the output shown in Figure T1, we see that the required payment is

$880.52.

APPLIED EXAMPLE 2

Finding the Payment in a Sinking Fund

Heidi wishes to establish a retirement account that will be worth $500,000

in 20 years’ time. She expects that the account will earn interest at the rate of

11% per year compounded monthly. What should be the monthly contribution

into her account each month?

Solution

We use the TI-83/84

TVM SOLVER

with the following inputs:

N 240

(20)(12)

I% 11

PV 0

PMT 0

FV 500000

P/Y 12

The number of payments each year

C/Y 12 The number of conversion periods each year

PMT:END BEGIN

The result is displayed in Figure T2. We see that Heidi’s monthly contribution

should be $577.61. (Note: The display for PMT is negative because it is an out-

flow.)

Excel

Here we use Excel to help us solve problems involving amortization and sinking funds.

APPLIED EXAMPLE 3

Finding the Payment to Amortize a Loan

The Wongs are considering a preapproved 30-year loan of $120,000 to help

finance the purchase of a house. The mortgage company charges interest at the

rate of 8% per year on the unpaid balance, with interest computations made at the

end of each month. What will be the monthly installments if the loan is amortized

at the end of the term?

Solution

We use the PMT function to solve this problem. Accessing this function

from the Insert Function dialog box and making the required entries, we obtain the

Function Arguments dialog box shown in Figure T3. We see that the desired result

is $880.52. (Recall that cash you pay out is represented by a negative number.)

298 5 MATHEMATICS OF FINANCE

N = 360

I% = 8

PV = 120000

PMT = −880.51748...

FV = 0

P/Y = 12

C/Y = 12

PMT : END BEGIN

FIGURE T1

The TI-83/84 screen showing the

monthly installment, PMT

N = 240

I% = 11

PV = 0

PMT = −577.60862...

FV = 500000

P/Y = 12

C/Y = 12

PMT : END BEGIN

FIGURE T2

The TI-83/84 screen showing the

monthly payment, PMT

Note: Words/characters printed blue (for example, Chart sub-type:) indicate words/characters on the screen.

87533_05_ch5_p257-312 1/30/08 9:55 AM Page 298

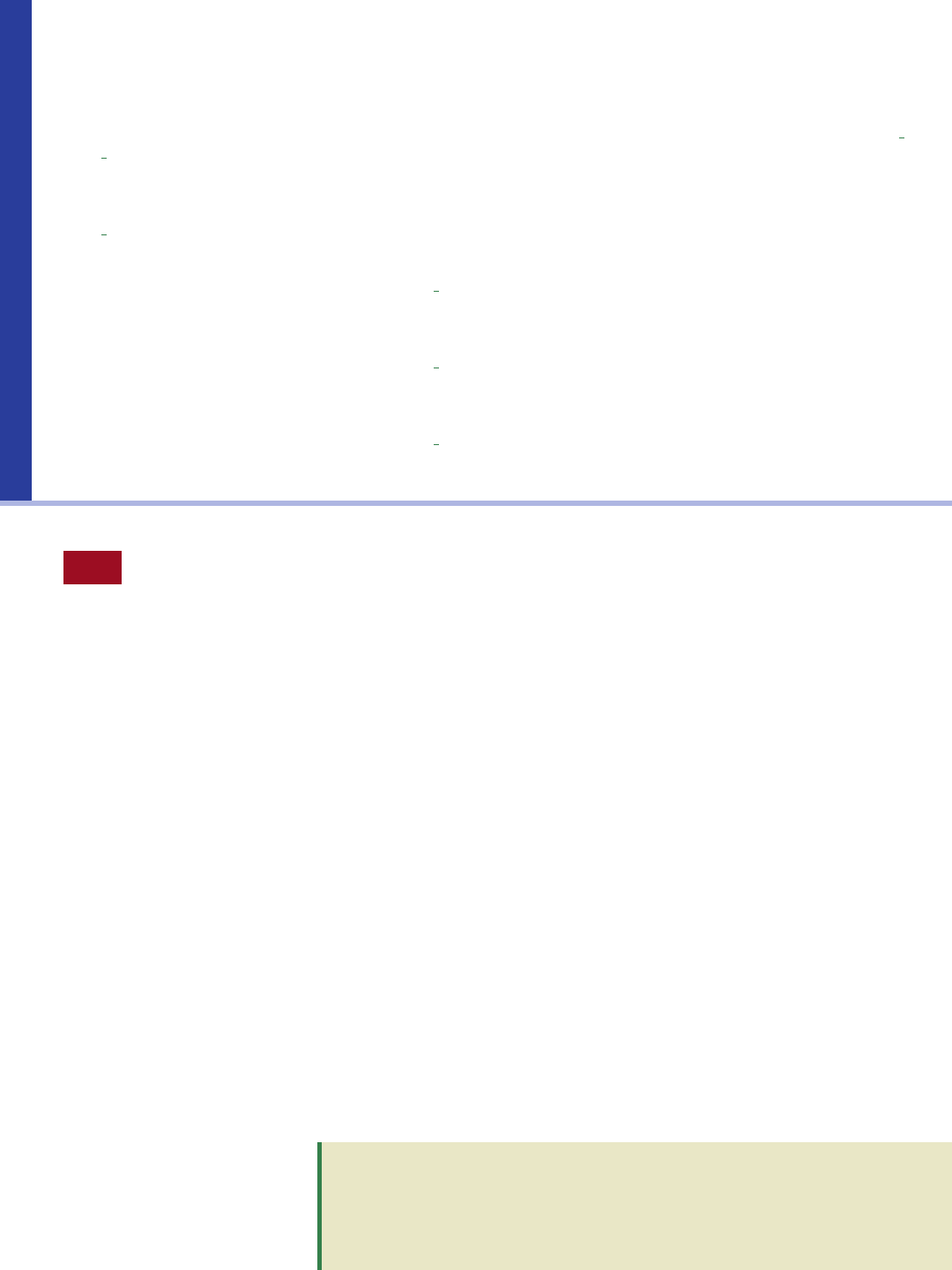

APPLIED EXAMPLE 4

Finding the Payment in a Sinking Fund

Heidi wishes to establish a retirement account that will be worth $500,000

in 20 years’ time. She expects that the account will earn interest at the rate of

11% per year compounded monthly. What should be the monthly contribution

into her account each month?

Solution

As in Example 3, we use the PMT function, but this time we are

given the future value of the investment. Accessing the PMT function from the

Insert Function dialog box and making the required entries, we obtain the Func-

tion Arguments dialog box shown in Figure T4. We see that Heidi’s monthly

contribution should be $577.61. (Note that the value for PMT is negative because

it is an outflow.)

5.3 AMORTIZATION AND SINKING FUNDS 299

FIGURE T3

Excel’s dialog box giving the payment

function, PMT

FIGURE T4

Excel’s dialog box giving the payment

function, PMT

TECHNOLOGY EXERCISES

1. Find the periodic payment required to amortize a loan of

$55,000 over 120 mo with interest charged at the rate of

year compounded monthly.

6

5

8

%/

2. Find the periodic payment required to amortize a loan of

$178,000 over 180 mo with interest charged at the rate of

%/year compounded monthly.7

1

8

(continued)

87533_05_ch5_p257-312 1/30/08 9:55 AM Page 299

3. Find the periodic payment required to amortize a loan of

$227,000 over 360 mo with interest charged at the rate of

%/year compounded monthly.

4. Find the periodic payment required to amortize a loan of

$150,000 over 360 mo with interest charged at the rate of

%/year compounded monthly.

5. Find the periodic payment required to accumulate $25,000

over 12 quarters with interest earned at the rate of %/year

compounded quarterly.

6. Find the periodic payment required to accumulate $50,000

over 36 quarters with interest earned at the rate of %/year

compounded quarterly.

7. Find the periodic payment required to accumulate $137,000

over 120 mo with interest earned at the rate of %/year

compounded monthly.

4

3

4

3

7

8

4

3

8

7

3

8

8

1

8

300 5 MATHEMATICS OF FINANCE

8. Find the periodic payment required to accumulate $144,000

over 120 mo with interest earned at the rate of %/year

compounded monthly.

9. A loan of $120,000 is to be repaid over a 10-yr period

through equal installments made at the end of each year. If

an interest rate of 8.5%/year is charged on the unpaid bal-

ance and interest calculations are made at the end of each

year, determine the size of each installment such that the

loan is amortized at the end of 10 yr. Verify the result by

displaying the amortization schedule.

10. A loan of $265,000 is to be repaid over an 8-yr period

through equal installments made at the end of each year. If

an interest rate of 7.4%/year is charged on the unpaid bal-

ance and interest calculations are made at the end of each

year, determine the size of each installment so that the loan

is amortized at the end of 8 yr. Verify the result by dis-

playing the amortization schedule.

4

5

8

5.4 Arithmetic and Geometric Progressions

Arithmetic Progressions

An arithmetic progression is a sequence of numbers in which each term after the first

is obtained by adding a constant d to the preceding term. The constant d is called the

common difference. For example, the sequence

2, 5, 8, 11, . . .

is an arithmetic progression with common difference equal to 3.

Observe that an arithmetic progression is completely determined if the first term

and the common difference are known. In fact, if

a

1

, a

2

, a

3

, . . . , a

n

, . . .

is an arithmetic progression with the first term given by a and common difference

given by d, then by definition we have

Thus, we have the following formula for finding the nth term of an arithmetic pro-

gression with first term a and common difference:

nth Term of an Arithmetic Progression

The nth term of an arithmetic progression with first term a and common differ-

ence d is given by

a

n

⫽ a ⫹ (n ⫺ 1)d (16)

a

n

⫽ a

n⫺ 1

⫹ d ⫽ a ⫹ 1n ⫺ 22d ⫹ d ⫽ a ⫹ 1n ⫺ 12d

o

a

4

⫽ a

3

⫹ d ⫽ 1a ⫹ 2d2⫹ d ⫽ a ⫹ 3d

a

3

⫽ a

2

⫹ d ⫽ 1a ⫹ d2⫹ d ⫽ a ⫹ 2d

a

2

⫽ a

1

⫹ d ⫽ a ⫹ d

a

1

⫽ a

87533_05_ch5_p257-312 2/19/08 8:41 AM Page 300

EXAMPLE 1

Find the twelfth term of the arithmetic progression

2, 7, 12, 17, 22, . . .

Solution

The first term of the arithmetic progression is a

1

a 2, and the com-

mon difference is d 5; so, upon setting n 12 in Equation (16), we find

a

12

2 (12 1)5 57

EXAMPLE 2

Write the first five terms of an arithmetic progression whose third

and eleventh terms are 21 and 85, respectively.

Solution

Using Equation (16), we obtain

Subtracting the first equation from the second gives 8d 64, or d 8. Substituting

this value of d into the first equation yields a 16 21, or a 5. Thus, the

required arithmetic progression is given by the sequence

5, 13, 21, 29, 37, . . .

Let S

n

denote the sum of the first n terms of an arithmetic progression with first term

a

1

a and common difference d. Then

S

n

a (a d ) (a 2d ) [a (n 1)d] (17)

Rewriting the expression for S

n

with the terms in reverse order gives

S

n

[a (n 1)d] [a (n 2)d] (a d ) a (18)

Adding Equations (17) and (18), we obtain

EXAMPLE 3

Find the sum of the first 20 terms of the arithmetic progression of

Example 1.

Solution

Letting a 2, d 5, and n 20 in Equation (19), we obtain

S

20

20

2

32

#

2 19

#

54 990

S

n

n

2

32a 1n 12d 4

n32a 1n 12d 4

32a 1n 12d4

2S

n

32a 1n 12d 4 32a 1n 1 2d4

a

11

a 10d 85

a

3

a 2d 21

5.4 ARITHMETIC AND GEOMETRIC PROGRESSIONS 301

Sum of Terms in an Arithmetic Progression

The sum of the first n terms of an arithmetic progression with first term a and

common difference d is given by

(19)S

n

n

2

32a 1n 12d 4

87533_05_ch5_p257-312 1/30/08 9:55 AM Page 301