ACCA F5 Performance Management - 2010 - Study text - Emile Woolf Publishing

Подождите немного. Документ загружается.

Chapter 10: Basic variance analysis

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 275

Deciding whether to investigate a variance

Management responses to reported variances

Factors to consider

Interdependence between variances

Statistical control charts

Cost-benefit analysis for variance investigation

11 Deciding whether to investigate a variance

11.1 Management responses to reported variances

When a variance is reported, the manager responsible must decide whether it

should be investigated. The purpose of investigating a variance is to:

find out the cause or causes of the variance

decide whether the variance is ‘controllable’: a variance is controllable if

management control action can be taken that will affect the amount of the

variance in future periods

if the variance is controllable, to decide whether any control action should be

taken to deal with its cause.

Investigating the cause of a variance takes management time and can be costly.

Management should not spend time and money on an investigation if the expected

benefits are unlikely to exceed the costs.

The size of a reported variance can be misleading. For example, if a reported labour

efficiency variance is $4,000 adverse, this does not mean that $4,000 can be saved by

taking action to correct the cause of the adverse variance.

The reported variance is a historical variance, and any control action can only

affect the future, not what has already happened in the past.

The reported variance shows how much actual costs were higher than expected

because actual efficiency was worse than the expected standard of efficiency.

However, this does not mean that control action will enable the entity to achieve

standard efficiency in the future. For example, the standard might be an ideal

standard, which means that the reported efficiency variance will almost certainly

always be adverse.

Control action should affect all periods in the future, so the effect of taking

control action in response to a reported variance in one period could have an

effect that lasts for several periods, or even years, into the future.

11.2 Factors to consider

Before making a decision whether to investigate a variance, the following factors

should be considered:

Paper F5: Performance management

276 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Size of the variance. As a general rule, the cause of a variance is more likely to

be significant when the variance is large. For example, a sales volume variance

that is $40,000 adverse will be considered more significant than a sales volume

variance of $400 adverse. The larger the variance, the greater the potential

benefit from investigation and control measures.

Favourable or adverse variance. Significant controllable favourable variances

should be investigated as well as adverse variances. However, more significance

might be given by management to adverse variances than to favourable

variances. Management might take the view that if a reported variance is

favourable, no action is needed and the variance might continue to be favourable

in future periods – and this is desirable. However, using the same logic, unless

control action is taken to correct the cause of an adverse variance, adverse

variances will continue in the future – and this is undesirable. For this reason, a

fairly small adverse variance might be investigated, but a favourable variance of

the same amount might not be investigated.

Probability that the cause of the variance will be controllable. A decision

whether or not to investigate the cause of a variance will also depend on the

expectation of management that the cause of the variance will be controllable.

For example, management might be aware that there has recently been a

significant increase in the market price of a raw material, or an increase in pay

rates for employees. If so, they might decide that reported adverse material price

and labour rate variances shouldn’t be investigated, because the main cause is

already known and it is unlikely that any control measures can be taken that will

be effective in reducing adverse price and rate variances in the future.

Costs and benefits of control action. Investigating a variance has a cost in terms

of both management time and expenditure. A variance should not be

investigated unless the expected benefits exceed the costs of investigation and

control. The benefits are the cost savings or other benefits that will be obtained

in the future if the variance is found to have a controllable cause and control

action is therefore taken.

Random variations in reported variances. Management might take the view

that a favourable or adverse variance in one month is due to random factors that

will not recur next month. A decision might therefore be taken to do nothing in

the current month about the variance, but to wait and see whether the same

variance occurs again next month. If the variance is due to random factors, it

should not happen again next month, and management can probably ignore it

without risk.

Reliability of budgets and measurement systems. Management might have a

view about whether the variance is caused by poor planning and poor

measurement systems, rather than by operational factors. If so, investigating the

variance would be a waste of time and would be unlikely to lead to any cost

savings.

11.3 Interdependence between variances

In some cases, individual variances should not be considered in isolation. The cause

of one variance might be connected to the cause of another variance. For example:

Chapter 10: Basic variance analysis

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 277

An adverse materials usage variance might be caused by purchasing cheaper-

than-normal materials (favourable price variance). If the quality of the materials

is less than normal, higher rates of wastage or loss in production may occur.

An adverse direct labour rate variance might be caused by using experienced

workers who are more skilled but who are paid a higher rate. The employees

might do the work more efficiently and more quickly (so there would be a

favourable efficiency variance for labour and variable overheads) but there will

be an adverse rate variance.

Using unskilled workers to do a job might result in a favourable rate variance

but an adverse efficiency variance. In addition, unskilled workers may cause

higher wastage of materials, so that there may also be an adverse materials

usage variance.

A favourable sales volume variance might be the result of cutting prices (adverse

sales price variance).

Mix variances are described in the next chapter. However, there may be a

connection between the total material usage variance in production (the material

yield variance) and the mix of different materials used in production. Using a

cheaper mix of materials in production will result in a favourable mix variance,

but the consequence mat be inefficiency in material usage (an adverse yield

variance).

The possibility of interdependence between variances means that if management

decide to investigate one reported variance, they might find that they also have to

investigate or more inter-related variances, to establish the cause of the variance and

the possible benefits from control action.

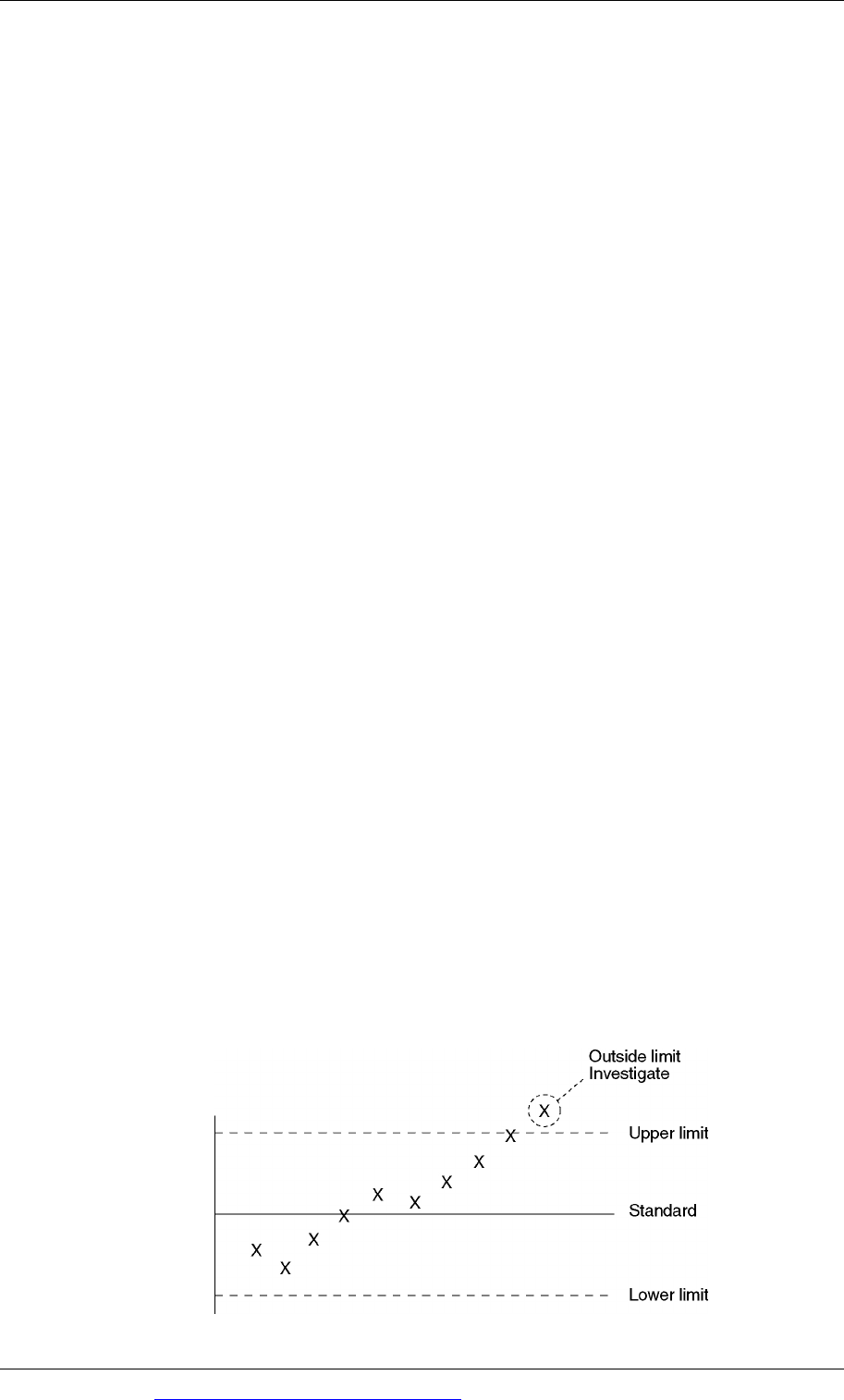

11.4 Statistical control charts

Statistical control charts might be used for the assessment of variances and making a

decision whether or not to investigate a reported variance.

Control limits might be set for each variance, so that only variances that are an

unusually large amount, and exceed the control limit, should be investigated.

This could be plotted on a statistical control chart, with the control limits shown

as ‘trigger limits’ for control action. The control limit for investigating a

favourable variance could be a different size to the control limit for an adverse

variance.

Paper F5: Performance management

278 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

This statistical control chart shows reported variances over time. The variances

recorded on the chart could be:

The variance in each individual control period

A cumulative total of variances, for example a 12-month rolling total for the

variance. The variance should only be investigated if the cumulative total for the

past 12 months exceeds the upper or lower control limit.

11.5 Cost-benefit analysis for variance investigation

The decision about whether or not to investigate a variance might be based on an

assessment of:

the costs of investigating the variance

the probability that the cause of the variance will be a controllable factor

the costs of control action if the cause is controllable

the expected benefits from control action if the cause is controllable.

This method weighs up the expected value of the costs and the expected value of

the benefits of investigating a variance.

The ‘decision rule’ for investigating a variance can be expressed as a formula.

The variance should be investigated if:

I + pC < pB

Where:

I = the cost of investigating the variance

C = the cost of correcting the cause of the variance, if the cause is found to be

controllable

p = the probability that the cause of the variance will be controllable

B = the expected benefits from control action, if the cause of the variance is found to

be controllable

Example

An adverse material usage variance of $1,400 has been reported.

The estimated cost of investigating the cause of a material usage variance is $800.

It is also estimated that if the cause of the variance is found, after investigation, to be

controllable, the cost of taking control action would be $650.

The estimated benefits from control action, if the cause of the variance is found to be

controllable, are $2,500.

The probability that the variance will be caused by a controllable factor is 60%.

Should the variance be investigated?

Chapter 10: Basic variance analysis

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 279

Answer

EV of costs of investigation = I + pC = $800 + 0.60 ($650) = $1,190.

EV of benefits from investigation and control = pB = 0.6 × $2,500 = $1,500.

The EV of benefits exceed the EV of costs by $310; therefore the variance should be

investigated.

Paper F5: Performance management

280 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 281

Paper F5

Performancemanagement

CHAPTER

11

Advanced variance analysis

Contents

1 Materials mix and yield variances

2 Planning and operational variances

3 Market size and market share variances

4 Behavioural aspects of standard costing

Paper F5: Performance management

282 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Materials mix and yield variances

Definition of materials mix and yield variances

Calculating a direct materials mix variance

Calculating a direct materials yield variance

Changing the materials mix: factors to consider

1 Materials mix and yield variances

1.1 Definition of materials mix and yield variances

When standard costing is used for products which contain two or more items of

direct material, the total materials usage variance can be analysed into a materials

mix and a materials yield variance. However, mix and yield variances have a useful

meaning only when the proportions (or ‘mix’) of the different raw materials in the

final product can be varied and so are subject to management control

The total direct materials usage variance is calculated by taking each item of

direct material in turn, and calculating a materials usage variance in the normal

way. The total direct material usage variance is the sum of the direct materials

usage variance for each of the individual materials.

The materials mix variance measures how much of this total variance is

attributable to the fact that the actual combination or mixture of materials that

was used was more expensive or less expensive than the standard mixture for

the materials.

The materials yield variance is a total usage variance for all the materials taken

together, assuming that the materials are in the standard proportions or mix. It is

calculated as a single figure, using the weighted average standard price per unit

of material for the calculation of the variance.

The mix component of the usage variance therefore indicates the effect on costs of

changing the combination (or mix or proportions) of material inputs in the

production process.

The yield component indicates the effect on costs of the total materials inputs

yielding more or less output than expected.

There is possible value for management, for control purposes, in calculating a mix

variance and a yield variance, but only if they are in a position to control the

mixture or proportions of the materials in the manufactured item.

1.2 Calculating a direct materials mix variance

There are two methods of calculating the mix variance. Both should provide exactly

the same variance. You should use the method that you find easier to understand.

Chapter 11: Advanced variance analysis

© EWP Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides 283

Method 1

Take the total quantity of al the materials used and calculate what the quantities

of each material in the mix should be if the total usage had been in the standard

proportions or standard mix.

Compare the actual quantities of each individual material that were used, and

the standard quantities that would have been used (the standard mix) if the total

usage had been in the standard proportions or standard mix.

For each material, take the difference between the quantity in the actual mix

used and the quantity in the standard mix. If actual usage is higher than

standard usage, the variance is adverse. If actual usage is less than standard

usage, the variance is favourable. The total mix variance in material quantities is

always zero.

Convert the mix variance for each individual material into a money value by

multiplying by the standard price per unit of the material. Add the total mix

variances for each material (money values) to obtain the total mix variance.

If the actual mix used is more expensive than the standard mix, the total mix

variance is adverse. If the actual mix used is cheaper than the standard mix, the

total mix variance is adverse.

Example

Product N is produced from three direct materials that are mixed together in a

process, materials A, B and C. The standard materials cost for product N is as

follows:

Material

Quantity

Standard price

per kilo

Standard

cost

kilos

$

$

A 1

20

20

B 1

22

22

C 8

6

48

10

90

Actual output during month 6 amounted to 200 units of product N in total. Actual

usage of each material was as follows:

Material kilos

A 160

B 180

C 1,760

2,100

Required

Calculate the direct materials mix variance for month 6.

Paper F5: Performance management

284 Go to www.emilewoolfpublishing.com for Q/As, Notes & Study Guides © EWP

Answer

The total quantity used was 2,100 kilos. This total usage can be divided into a

standard mix for materials A, B and C and the standard mix and actual mix can be

compared, as follows.

Material

Actual

mix

Standard

mix

Mix variance

in quantities

Standard price

per kilo

Mix variance

in value

kilos kilos

kilos

$ $

A 160 (1) 210

50

(F) 20 1,000

(F)

B 180 (1) 210

30

(F) 22 660

(F)

C 1,760 (8) 1,680

80

(A) 6 480

(A)

2,100 2,100

0

1,180

(F)

For each individual item of material, the mix variance is favourable when the actual

mix is less than the standard mix, and the mix variance is adverse when actual

usage exceeds the standard mix.

The total mix variance is favourable in this example because the actual mix of

materials used is cheaper than the standard mix.

Method 2

Method 2 produces the same value for the mix variance.

Take the total quantity of materials used.

For each material, calculate a mix variance in quantities, the same as for method

1. However, do not decide yet whether the variance is adverse or favourable for

each material.

Next, calculate the weighted average price per unit of materials in the mix. This

is calculated as [the total direct materials cost per unit divided by the total

number of units of materials in one unit of finished product].

For each material, calculate the difference between the standard price for the

material and the weighted average standard price.

A cheap material is a material whose standard price is lower than the weighted

average standard price for materials in the mix.

An expensive material is a material whose standard price is higher than the

weighted average standard price for materials in the mix.

Next, for each material in the mix, multiply the mix variance in quantities by the

difference between its standard price and the weighted average standard price.

Decide whether the variance for each material is favourable or adverse.

− If there is more of a cheap material in the actual mix than in the standard

mix, the variance for the material is favourable.

− If there is less of a cheap material in the actual mix than in the standard mix,

the variance for the material is adverse.

− If there is more of an expensive material in the actual mix than in the

standard mix, the variance for the material is adverse.