Blank L., Tarquin A. Engineering Economy (McGraw-Hill Series in Industrial Engineering and Management)

Подождите немного. Документ загружается.

SECTION

5.3

Present Worth Analysis

of

Different-Life Alternatives

The assumptions of a

PW

analysis

of

different-life alternatives for

the

LCM

method

are

as follows:

1.

The

service provided by the alternatives will be needed for

the

LCM

of years

or

more.

2. The selected alternative will be repeated over each life cycle

of

the

LCM

in exactly the same manner.

3. The cash flow estimates will be

the

same in every life cycle.

As will be shown in Chapter

14

, the third assumption is valid only when the cash

flows are expected to change by exactly the inflation (or deflation) rate that is ap-

plicable through the LCM time period.

If

the cash flows are expected to change

by any other rate, then the

PW analysis must be conducted using constant-value

dollars, which considers inflation (Chapter 14). A study period analysis is neces-

sary if the first assumption about the length

of

time the alternatives are needed

cannot be made. A present worth analysis over the

LCM

requires that the esti-

mated salvage values be included in each life cycle.

For the study period approach, a time horizon

is

chosen over which the eco-

nomic analysis

is

conducted, and only those cash flows which occur during that

time period are considered relevant to the analysis. All cash flows occurring

beyond the study period are ignored. An estimated market value at the end

of

the

study period must be made. The time horizon chosen might

be

relatively short,

especially when short-term business goals are very important. The study period

approach

is

often used in replacement analysis. It is also useful when the

LCM

of

alternatives yields an unrealistic evaluation period, for example, 5 and 9 years.

Example 5.2 includes evaluations based on the

LCM

and study period

approaches. Also, Example 5.12 in Section 5.9 illustrates the use

of

spreadsheets

in

PW

analysis for both different lives and a study period.

EXAMPLE 5.2 '

A project engineer with EnvironCare is assigned to start

up

a new office

in

a city where

a 6-year contract has been finalized to take and

to analyze ozone-level readings. Two

lease options are available, each with a first cost, annual lease cost, and deposit-return

estimates shown below.

First cost,

$

Annual lease cost, $ per year

Deposit return, $

Lease term, years

Location

A

-15,000

-3,500

1,000

6

Location

B

-18,000

-3,100

2,000

9

(a) Determine which lease option should be selected on the basis

of

a present worth

comparison, if the MARR

is

15% per year.

(b) EnvironCare has a standard practice

of

evaluating all projects over

as-year

period.

If

a study period

of

5 years

is

used and the deposit returns are not

expected to change, which location should be selected?

175

176 CHAPTER 5 Present Worth A

nal

ys

is

(c) Which location should be selected over a 6-year study period if the deposit

return at location B

is

estimated to be $6000 after 6 years?

Solution

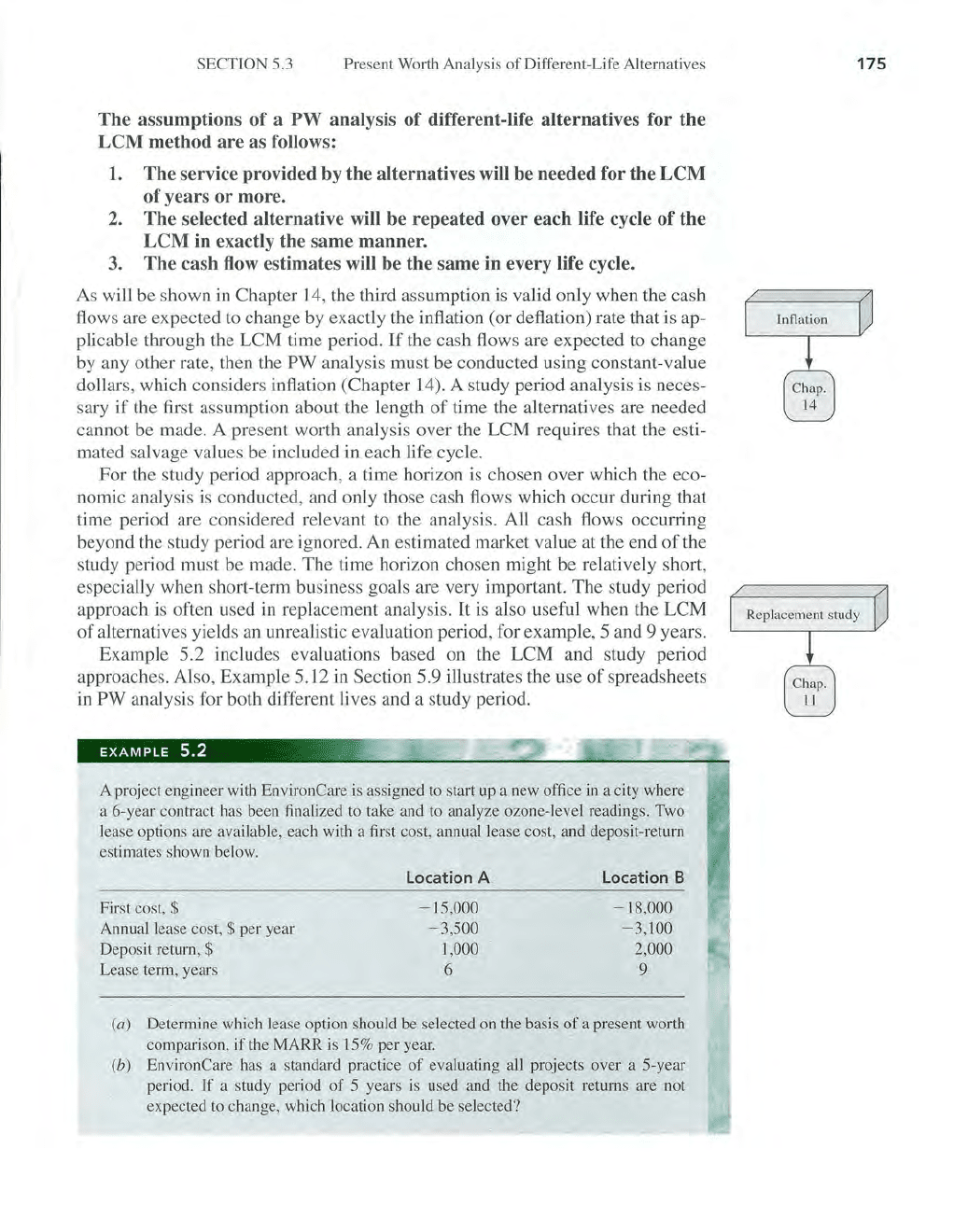

(a) Since the leases have different terms (lives), compare them over the LCM

of

IS years. For life cycles after the first, the first cost

is

repeated

in

year 0 of each

new cycle, which

is

the last year

of

the previous cycle. These are years 6 and

12

for location A a

nd

year 9 for B. The cash

flow

diagram is

in

Figure 5-

2.

Calcu-

late

PW at

15

% over IS years.

$

15

,000

PW/J= ?

$

18

,000

PW

A

= -

15

,000 -

15

,000(P/ F,15%,6) + 1000(P/ F,

15

%,6)

-

15

,000(P/ F,

15

%

,l2

) +

LOOO

(P/ F,

l5

%,

12

) + 1000(P/ F,15%

,I

S)

- 3500(P / A,

15

%,

IS)

= $- 45,036

PW

s

= - IS,

OOO

-

IS

,

000(P/F,15%,9)

+

2000(P/F,15

%,9)

+

2000(P/F

,

15

%, lS) - 3100(P/A,

15

%,

IS)

= $- 41,3S4

Location B is selected, since it costs less

in

PW terms; that

is,

the PW B value is

numerically larger than

PW A '

2

2

$1000

6

~

$

15

,000

$3500

Locat.ionA

$2000

9

$18,000

Location B

$1000

$1000

12

16

J7

18

~

$

15

,000

$2000

16

17 18

Figure

5-2

Cash flow diagram for different-life alternatives, Example 5.2(a).

SECTlON 5.4 Future Worth Analysis

(b) For a 5-year study period

no

cycle repeats are necessary. The PW analysis

is

PW A = - 15,000 - 3500(P/A,

J5

%,5) + 1000(P/ F,15%,5)

= $- 26,236

PW

B

= - 18,000 - 3100(P/A,15%,5) + 2000(P/F,15%,5)

= $- 27,397

Location A

is

now the better choice.

(c) For a 6-year study period, the deposit return for B

is

$6000 in year

6.

PW

A

= -

15

,000 - 3500(P/A,

15

%,6) + 1000(P/ F,

l5

%,6) =

$-27

,

813

PW

B

= -

18

,000 - 3100(P/A,

15

%,

6) + 6000(P/ F,

15

%,6) =

$-27

,138

Location B now has a small economic advantage. Noneconomic factors are

likely

to

enter into the final decision.

Comments

In

part (a) and Figure 5-

2,

the deposit return for each lease

is

recovered after each life

cycle, that

is

,

in

years

6,

12,

and

18

for A and

in

years 9 and

18

for

B.

In

part (c), the

increase

of

the deposit return from $2000

to

$6000 (one year later), switches the

selected location from A

to

B.

The project engineer should reexamine these estimates

before making a final decision.

5.4 FUTURE WORTH ANALYSIS

The future worth (FW)

of

an

alternative may be determined directly from the

cash flows

by

determining the future worth value, or by multiplying the

PW

value by

th

e F / P factor, at the established MARR. Therefore, it is an extension

of

present worth analysis.

The

n value in the F / P factor depends upon which

time period has been used to determine

PW-the

LCM

value or a specified study

period. Analysis

of

one alternative, or the comparison

of

two or more alterna-

tives, using FW values is especially applicable to large capital investment deci-

sions when a prime goal

is

to maximize the

futur

e wealth

of

a corporation's

stockholders.

Future worth analysis

is

often utilized if the asset (equipment, a corporation, a

building, etc.) might be sold or traded at some time after its start-

up

or

acquisi-

tion, but before the expected life is reached. An

FW

value at an intermediate year

estimates the alternative's worth at the time

of

sale

or

disposal. Suppose an en-

trepreneur is planning to buy a company and expects to trade it within 3 years.

FW

analysis is the best method to help with the decision to sell or keep

it

3 years

hence. Example 5.3 illustrates this use

of

FW

analysis. Another excellent appli-

cation

of

FW analysis is for projects that will not come online until the end

of

the

investment period. Alternatives such

as

electric generation facilities, toll roads,

hotels, and the like can be analyzed using the

FW

value

of

investment commit-

ments made during construction.

177

178

CHAPTER 5

Present Worth Analysis

Once the FW value

is

determined, the selection guidelines are the same

as

with PW analysis; FW

:::=:

0 means the MARR is met or exceeded (one alterna-

tive). For two (or more) mutually exclusive alternatives, select the one with the

numerically larger (largest) FW value.

EXAMPLE

5.3

A British food distribution conglomerate purchased a Canadian food store chain for $75

million

(U.S

.)

three years ago. There was a net loss

of

$10 million at

th

e e

nd

of

year 1

of

ownership. Net cash

flow

is increasing with

an

arithmetic gradient

of

$+

5 million

per year starting the second year, and this pattern

is

expected to continue for the fore-

seeable future. This means that breakeven net cash flow was achieved

thi

s year.

Because

of

the heavy debt

fin

ancing used to purchase

th

e Canadian chain, the interna-

tional board

of

directors expects a MARR

of

25% per year from any sale.

(a)

The

British conglomerate has just been offered $159.5 million (U.S.)

by

a

French compa

ny

wishing to get a foothold in Canada. Use FW analysis

to

deter-

mine if the

MARR

will be realized at this selling price.

(b)

If

th

e British conglomerate continues

to

own the chain, what selling price

mu

st

be obtained at the end

of

5 years

of

ownership to make

th

e MARR?

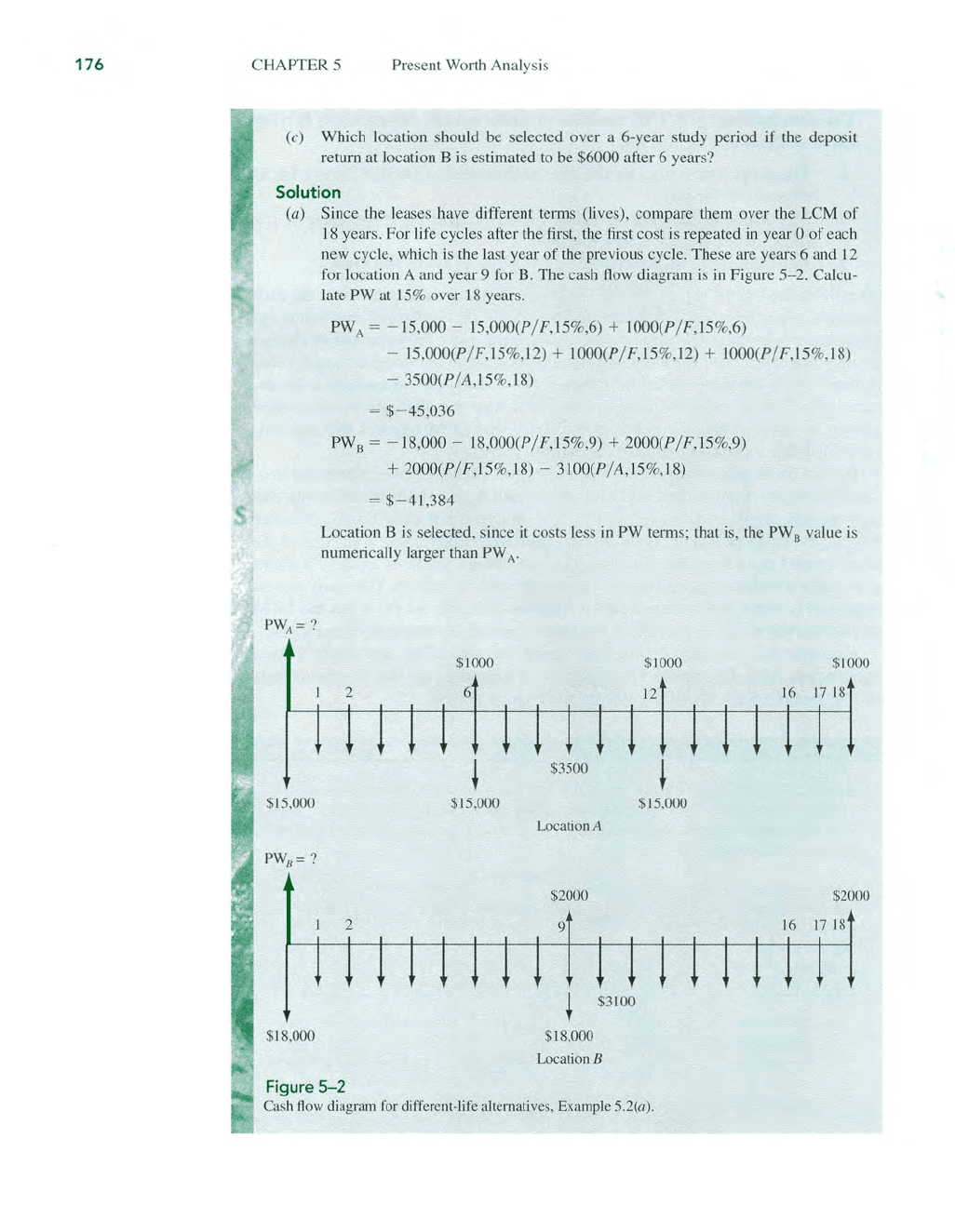

Solution

(a) Set up the future worth

rel

ation

in

year 3 (FW

3

)

at i = 25% per year a

nd

an

offer

price

of

$159.5 million. Figure 5

-3a

prese

nt

s the cash flow diagram

in

million $

unit

s.

o

$75

FW

3

=

-75(F/

P,25%,3) -

IO

(F/

P

,2

5%,2) -

5(F/P,25%,I)

+ 159.5

= - 168.36 + 159.5 =

$-8.86

million

No,

th

e MARR

of

25% will not

be

rea

li

zed if the $159

.5

million offer is

accepted.

$159.5

FW=?

i

~

25

'70

?

i=25

%

2

3

o

2

3

$75

(a)

(b)

Figure

5-3

Cash

fl

ow diagrams for Example 5.3. (a) Is MARR = 25% realized? (b) What

is

FW

in

year

5?

Amounts are

in

million $ units.

SECTION S.S Capitalized Cost Calculation a

nd

Analysis

(b) Determine the future worth S years from now at 2S% per year. Figure S

-3

b pre-

sents the cash flow diagram. The

A/G

and

F/A

factors are applied

to

the arith-

metic gradient.

FW

s = - 7S

(F

/ P,2S%,S) -

1O

(F/A,2S%,S) + S(A/ G,2S%,S)(F

/A,2

S%,S)

=

$-2

46.81 miUion

The offer must be for

at

least $246.81 million

to

make the MARR. This

i.s

approximately 3.3 times the purchase price only S years earlier,

in

large part

based on the required MARR

of

2S%.

Comment

If the 'rule of

72'

in

Equation

[l.9]

is applied at 2S% per year, the sales price must

double approximately eve

ry

72

/ 2S% = 2.9 years. This does not consider any annual

net positive or negative cash

flows during the years

of

ownership.

5.5 CAPITALIZED COST CALCULATION

AND

ANALYSIS

Capitaliz

ed

cost (CC) is the present worth

of

an alternative

th

at will last "for-

ever." Public

sector projects such as bridges, dams, irrigation systems, and rail-

roads fall into this category. In addition, permanent and charitable orgartization

endowments are evaluated using the capitalized cost methods.

The formula to calculate CC

is

derived from the relation P =

A(P

/ A,i,n),

where

n =

00

.

The

equation for P using the P

/;1

factor formula is

P = Al(1 + it -

1]

i(1 + i)"

Divide the numerator and denominator by

(1

+ i)".

r

1 -

(1

~

i)" l

P

=A

i

As n approaches

00

, the bracketed term becomes 1/

i,

and the symbol

CC

replaces

PW and

P.

cc=

~

[5.1]

l

If

the A value

is

an annual worth

(A

W) determined through equivalence calcula-

tions

of

cash flows over n years, the CC value

is

cc=

A~

[5.2]

t

The

validity

of

Equation [5.1] can be illustrated by considering the time value

of

money.

If

$10,000

ea

rns 20% per year, compounded annually, the maximum

179

180

CHAPTER 5

Present Worth Analysis

amount

of

money that can be withdrawn at the end

of

every year for eternity

is

$2000, or the interest accumulated each year. This leaves the original $10,000 to

earn interest so that another

$2000 will be accumulated the next year. Mathe-

matically, the amount

A

of

new money generated each consecutive interest

period for an infinite number

of

periods is

A =

Pi

=

CC(i)

[5.3]

The capitalized cost calculation

in

Equation [5.1]

is

Equation [5.3] solved for

P and renamed

Cc.

For a public sector alternative with an infinite or very long life, the A value

determined by Equation [5.3] is used when the benefit/cost (B/C) ratio is the

comparison basis for public projects. This method

is

covered in Chapter 9.

The cash flows (costs or receipts) in a capitalized cost calculation are usually

of

two types: recurring, also called periodic, and nonrecurring. An annual oper-

ating cost

of

$50,000 and a rework cost estimated at $40,000 every 12 years are

examples

of

recurring cash flows. Examples

of

nonrecurring cash flows are the

initial investment amount in year

0 and one-time cash flow estimates at future

times, for example,

$500,000

in

royalty fees 2 years hence.

The

following pro-

cedure assists

in

calculating the CC for an infinite sequence

of

cash flows.

I. Draw a cash flow diagram showing all nonrecurring (one-time) cash flows

and at least two cycles

of

all recurring (periodic) cash flows.

2.

Find the present worth

of

all nonrecurring amounts. This is their CC value.

3. Find the equivalent uniform annual worth

(A

value) through one

lif

e cy

cl

e

of

all recurring amounts. This is the same value

in

all succeeding life

cycles, as explained in Chapter

6.

Add this to all other uniform amounts

occurring in years 1 through infinity and the result

is

the total equivalent

uniform annual worth (AW).

4. Divide the

AW

obtained in step 3 by the interest rate i to obtain a CC value.

This is an application

of

Equation [5.2].

5.

Add the CC values obtained in steps 2 and 4.

Drawing the cash flow diagram (step

1)

is

more important in CC calculations

than elsewhere, because it helps separate nonrecurring and recurring amounts.

In

step 5 the present worths

of

all component cash flows have been obtained; the

total capitalized cost

is

simply their sum.

EXAMPLE

5.4

: .

The

property appraisal district for Marin Coun

ty

has

just

installed new software to track

residential market values for property tax computations.

The

manager wants

to

know the

total equivalent cost

of

a

ll

future costs incurred when the three county judges agreed to pur-

chase the software system.

If

the new system will be used for

d1e

indefinite future, find the

equivalent va

lu

e (a) now and (b) for each year hereafter.

The

system has an installed cost

of

$150,000 and an additional cost

of

$50,000 after

10

years.

The

annual software maintenance contract cost is $5000 for the first 4 years and

SECTION 5.5 Capitalized Cost Calculation and Analysis

$8000 thereafter.

In

addition, there

is

expected to be a recurring major upgrade cost

of

$15,000 every

13

years. Assume that i = 5% per year for county funds.

Solution

(a) The five-step procedure

is

applied.

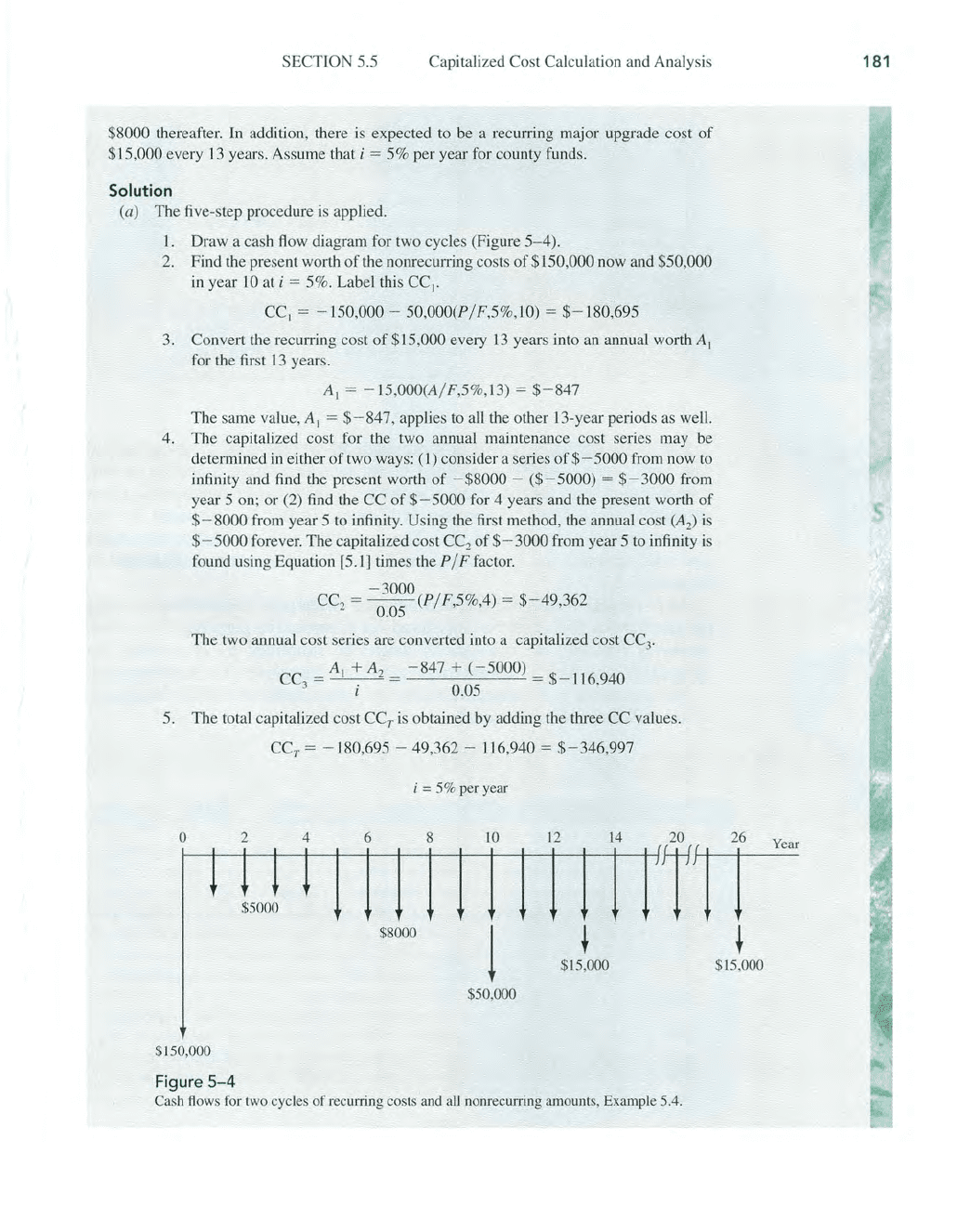

1. Draw a cash flow diagram for two cycles (Figure

5-4)

.

2.

Find the present worth

of

the nonrecurring costs

of

$150,000 now and $50,000

in

year

10

at i = 5%. Label this CCI'

CC

I

= - 150,000 - 50,000(P/F,5%,1O) =

$-180,695

3.

Convert the recurring cost

of

$15,000 every

13

years into

an

annual worth

AI

for the first

13

years.

AI = -

15

,000(A/

F,5

%,

13)

=

$-847

The same value,

AI

= $- 847, applies

to

all the other 13-year periods as well.

4.

The capitalized cost for the two annual maintenance cost selies may be

determined

in

either

of

two ways:

(I)

consider a series

of

$- 5000 from now to

infinity and

find

the present worth

of

-$8000

-

($-5000)

=

$-3000

from

year

5 on;

or

(2) find the CC

of

$-5000

for 4 years and the present worth

of

$-8000

from year 5 to infinity. Using the first method, the annual cost (Az)

is

$- 5000 forever. The capitalized cost CC

2

of

$- 3000 from year 5 to infinity

is

found using Equation [5.1] times the P / F factor.

-3000

CC

2

= - - (P/F,5%,4) =

$-49,362

0.05

The two annual cost series are converted into a capitalized cost CC

3

.

CC

=A

I

+A

2

=

-847+(-5000)=$

_ 116940

3 i 0.05 '

5.

The total capitalized cost CC

T

is

obtained

by

adding the three CC values.

CC

T

= - 180,695 - 49,362 - 116,940 = $- 346,997

i = 5% per year

o

2 4

6 8 10

12 14

TTl

$5000

$150,000

Figure

5-4

$8000

j

$50,000

t

$15,000

Cash flows for two cycles

of

recutTing costs and

all

nonrecurring amount

s,

Example 5.4.

t

$

15

,000

181

182

CHAPTER 5 Present Worth Analysis

(b) Equation [5.3] determines the A value forever.

A =

Pi

= CCT(i) = $346,997(0.05) = $17,350

Correctly interpreted, this means Marin County officials have committed the

equivalent

of

$17,350 forever

to

operate and maintain the property appraisal

software.

Comment

The CC

2

value

is

calculated using

n.

= 4

in

the P / F factor because the present worth

of

the

annual

$3000 cost

is

located

in

year 4, since P is always one period ahead

of

the first A.

Rework the problem using the second method suggested for calculating CC

2

.

For the comparison

of

two or more alternatives on the basis

of

capitalized

cost, use the procedure above

to

find CC

T

for each alternative. Since the capital-

ized cost represents the total present worth

of

financing and maintaining a given

alternative forever, the alternatives will automatically be compared for the

same number

of

years (i.e., infinity). The alternative with the smaller capitalized

cost will represent the more economical one. This evaluation is illustrated in

Example

5.5.

As

in

present worth analysis, it is only the differences in cash

flow

between

the alternatives that must

be

considered for comparative purposes. Therefore,

whenever possible, the calculations should be simplified by eliminating the

elements

of

cash flow which are common to both alternatives. On the other hand,

if true capitalized cost values are needed to reflect actual financial obligations,

actual cash flows should be used.

EXAMPLE

5.5

..

~;

Two sites are currently under consideration for a blidge to cross a river

in

New York.

The north site, which connects a major state highway with

an

interstate loop around the

city, would alleviate much

of

the local through traffic.

The

disadvantages

of

this site are

that the bridge would do little to ease local traffic congestion during rush hours, and the

bridge would have

to

stretch from one hill to another to span the widest part

of

the river,

railroad tracks, and local highways below. This bridge would therefore be a suspension

bridge. The south site would require a much shorter span, allowing for

consu·uction

of

a truss bridge, but

it

would require new road construction.

The suspension bridge will cost

$50 million with annual inspection and maintenance

costs

of

$35,000.

In

addition, the concrete deck would have to

be

resurfaced every 10

years at a cost

of

$100,000. The truss bridge and approach roads are expected to cost

$25 million and have annual maintenance costs

of

$20,000. The bridge would have to

SECTION 5.5 Capitalized Cost Calculation and Analysis

be painted every

3 years at a cost

of

$40,000.

In

addition, the bridge would have to be

sandblasted every

10

years at a cost

of

$190,000. The cost

of

purchasing right-of-way

is

expected to be $2 million for the suspension bridge and $15 million for the truss

bridge. Compare the alternatives on the basis

of

their capitalized cost if the interest rate

is

6% per year.

Solution

Construct the cash

flow

diagrams over two cycles (20 years).

Capitalized cost

of

suspension bridge (CC

s

):

CC

I

= capitalized cost

of

initial cost

= - 50.0 - 2.0 =

$-52.0

milljon

The recurring operating cost

is

A I =

$-35,

000, and the annual equivalent

of

the resur-

face cost

is

A2

= - JOO,000(A/F,6%,

IO)

=

$-7587

CC

2

= capitalized cost

of

recurring costs = A I + A2

I

=

-35,000

+

(-

7587) =

$-709

,

783

0.06

The total capitalized cost

is

CC

s

= CC

I

+ CC

2

=

$-52.71

million

Capitalized cost

of

truss bridge (CC

r

):

CC

I

= - 25.0 +

(-15.0)

=

$-40.0

million

AI =

$-20,000

A2

= annual cost

of

painting = - 40,00

0(A/

F,6%,3) =

$-12,564

A3 = annual cost

of

sandblasting = - 190,000(A/ F,6%,1

0)

= $-

14

,415

CC = AI + A2 + A3 =

$-46,979

=

$-782983

2 i 0.06 '

CC

r

= CC

I

+ CC

2

=

$-40.78

million

Conclusion: Build the truss

bJidge, since its capitalized cost is lower.

If

a finite-life alternative (e.g., 5 years) is compared to one with an indefinite

or very long life, capitalized costs can be used for the evaluation. To determine

capitalized cost for the alternative with a finite life, calculate the equivalent

A

value for one

li

fe cycle and divide by the interest rate (Equation [5.1]). This pro-

cedure is illustrated

in

the next example.

183

184

CHAPTERS Present Worth Analys

is

EXAMPLE

5.6

'.~

~

E-Solve

APSco, a large electronics subcontractor for the Air Force, needs to immediately acquire

10

so

ld

er

in

g machines with specially prepared ji

gs

for assembling components onto

printed circuit

boards, More machines may

be

needed

in

the future. The lead production en-

gineer has outlined below two simplified, but viable, alternatives. The company's MARR

is

15

% per year.

Alternative LT (long-term). For $8 million now, a contractor will provide the necessary

number

of

machines (up

to

a maximum

of

20), now and

in

the future, for

as

long

as

APSco needs them. The annual contract fee is a total

of

$25,000 with no additional

per-machine annual cost. There

is

no time limit placed

on

the contract, and the cos

ts

do not escalate.

Alternative

ST

(short-term). APSco buys its own machines for $275,000 each and ex-

pends

an

est

im

ated $12,000 per machine

in

annual operating cost (AOC). The use-

fu

l

li

fe

of

a soldering system

is

5 years.

Perform a capitalized cost evaluation

by

hand and

by

computer. Once the eva

lu

ation

is

complete, use the spreadsheet for sensitivity anaJysis

to

determine the maximum number

of

so

ld

ering machines that can be purchased now and still have a capitalized cost less than

that

of

the long-term alternative.

Solution

by

Hand

For the

LT

alternative,

find

the CC

of

the AOC using Equation [5.1], CC =

A/i.

Add this

aJTIount

to

the initial contract fee, which is already a capitalized cost (present worth)

amount.

CCLT

= CC

of

contract fee + CC

of

AOC

= - 8 million - 25,000/ 0.15 =

$-8

,166,667

For the

ST

alternative, first calculate the equivalent annual amount for the purchase cost

over the 5-year life, and add the

AOC values for all

10

machines. Then determine the total

CC using Equation [5.2].

AW

sT

=

AW

for purchase + AOC

= - 2.75 million(A/ P,

15

%,

5) - 120,000 = $- 940,380

CC

ST

= - 940,380/0.15 = $- 6,269,200

The

ST alternative has a lower capitalized cost by approximately $1.9 million present

va

lu

e dollars.

Solution

by

Computer

Figure 5- 5 contains the solution for

10

machines

in

column

B.

Cell B8 uses the same rela-

tion as

in

the so

lu

tion by hand. Cell B

15

uses the PMT function to detelmine the equiva-

lent annual amount

A for the purchase

of

10

machines,

to

which the AOC

is

added. Cell

B

16

uses Equation

[5

.

2]

to

find

the total CC for tbe ST alternative. As expected, alternative

ST

is

selected. (Compare CC

ST

for the hand and computer solutions to note that the round-

off

eITor

using the tabulated interest factors gets larger for large P

va

lu

es.)

The type

of

sensitivity analysis requested here is easy to perform once a spreadsheet

is

developed. The PMT function

in

B

15

is

expressed generally in terms

of

cell B

12,

the