Blank L., Tarquin A. Engineering Economy (McGraw-Hill Series in Industrial Engineering and Management)

Подождите немного. Документ загружается.

Case Study Exercises

1.

For

an interest rate

of

8% and a toilet life

of

5 years, what would the participant's payback

period be?

2.

Is the participant's payback period more sensi-

tive

to

the interest rate used or to the

li

fe

of

the

toilet?

3. What would the cost to the city be

if

an inter-

est rate

of

6% per year were used with a toi-

let life

of

5 years? Compare the cost

in

$ICCF

CASE STUDY

215

and

$/1

000 gallons to those determined at 0%

interest.

4.

From

the city's standpoint,

is

the Sllccess

of

the

program sensitive to

(a) the percentage

of

toilet

cost rebated,

(b) the interest rate,

if

rates

of

4%

to 15% are used, or

(c) the toilet life, if lives

of

2

to

20 years are used?

5.

What

other factors might be important to (a) the

participants and

(b) the city

in

evaluating whether

the program is a sllccess?

UJ

u

Annual Worth Analysis

In

this chapter,

we

add

to

our

repertoire

of

alternative

comparison

tools.

In

the

last

chapter

we

learned

the

PW

method.

Here

we

learn

the

equivalent

annual

worth,

or

AW,

method.

AW

analysis

is

commonly

considered

the

more

desirable

of

the

two

methods

because

the

AW

value

is

easy

to

calcu-

late;

the

measure

of

worth-AW

in dollars

per

year-is

understood

by

most

individuals;

and

its assumptions are essentially identical

to

those

of

the

PW

method

.

Annual

worth

is

also

known

by

other

titles

. Some are

equivalent

annual

worth

(EAW),

equivalent

annual

cost

(EAC), annual

equivalent

(AE), and

EUAC

(equivalent

uniform

annual cost).

The

resulting

equivalent

annual

worth

amount

is

the

same

for

all

name

variations.

The

alternative

selected

by

the

AW

method

will always

be

the

same

as

that

selected

by

the

PW

method,

and all

other

alternative

evaluation

methods,

provided

they

are

performed

correctly.

In

the

case study,

the

estimates

made

when

an

AW

analysis was

per-

formed

are

found

to

be

substantially

different

after

the

equipment

is

in-

stalled.

Spreadsheets, sensitivity analysis,

and

annual

worth

analysis

work

together

to

evaluate

the

situation.

LEARNING OBJECTIVES

r Purpose: Make annual worth calculations and compare alternatives using the annual

worth method.

This

chapter

wi

ll

help

you:

,

One life cycle

J

1.

D

emons

trate that

AW

needs to

be

calculated

over

on

ly

one

life cy

cl

e.

I

AW

calculation

·1

2.

Ca

lculate capit

al

recovery

(C

R) and

AW

using

two

methods.

Alternative selection

by

AW

I

3. Select

the

best

alternative

on

the

basis

of

an

AW

analysis.

,

Permanent investment

AW

4.

Ca

lculate the

AW

of a permanent

in

vest

me

nt.

I

218

L

Sec. 5.3

1

t

PW

method

assumptions

EXAMPLE 6.1

Sec. 5.3

CHAPTER 6 Annual Worth Analysis

6.1

ADVANTAGES

AND

USES

OF

ANNUAL

WORTH ANALYSIS

For many engineering economic studies, the A W method is the best to use, when

compared to

PW, FW, and rate

of

return (next two chapters). Since the AW value

is

the equivalent uniform annual worth

of

all estimated receipts and disburse-

ments during the life cycle

of

the project or alternative,

AW

is

easy to understand

by any individual acquainted with annual amounts, that is, dollars per year. The

AW

value, which has the same economic interpretation as A used thus far,

is

equivalent to the

PW

and FW values at the

MARR

for n years. All three can be

easily determined from each other by the relation

AW

= PW(AjP,i,n) =

FW(A

jF,i,n) [6.1]

The

n

in

the factors is the number

of

years for equal-service comparison. This

is

the

LCM

or the stated study period

of

the

PW

or

FW

analysis.

When all cash flow estimates are converted to an

AW

value, this value applies

for every year

of

the life cycle, and for each additional life cycle. In fact, a prime

computational and interpretation advantage

is

that

The

A W value has to be calculated for only one life cycle. Therefore, it is

not necessary to use the

LCM

of

lives, as

it

is for

PW

and

FW

analyses.

Therefore, determining the

AW

over one life cycle

of

an alternative determines

the

AW

for all future life cycles. As with the

PW

method, there are three funda-

mental assumptions

of

the A W method that should be understood.

When alternatives being compared have different lives, the

AW

method

makes the assumptions

that

1.

The

services provided

are

needed for

at

least the

LCM

of the lives of

the alternatives.

2.

The

selected alternative will be repeated for succeeding life cycles in

exactly the same

manner

as for the first life cycle.

3. All cash flows

will have the same estimated values in every life cycle.

In practice, no assumption is precisely correct.

If,

in

a particular evaluation, the

first two assumptions are not reasonable, a study period must be established for the

analysis. Note that for assumption

1,

the length

of

time may be the indefinite future

(forever). In the third assumption, all cash flows are expected to change exactly

with the inflation (or deflation) rate.

If

this

is

not a reasonable assumption, new

cash flow estimates must be made for each life cycle, and, again, a study period

must be used. AW analysis for a stated study period

is

discussed

in

Section 6.3.

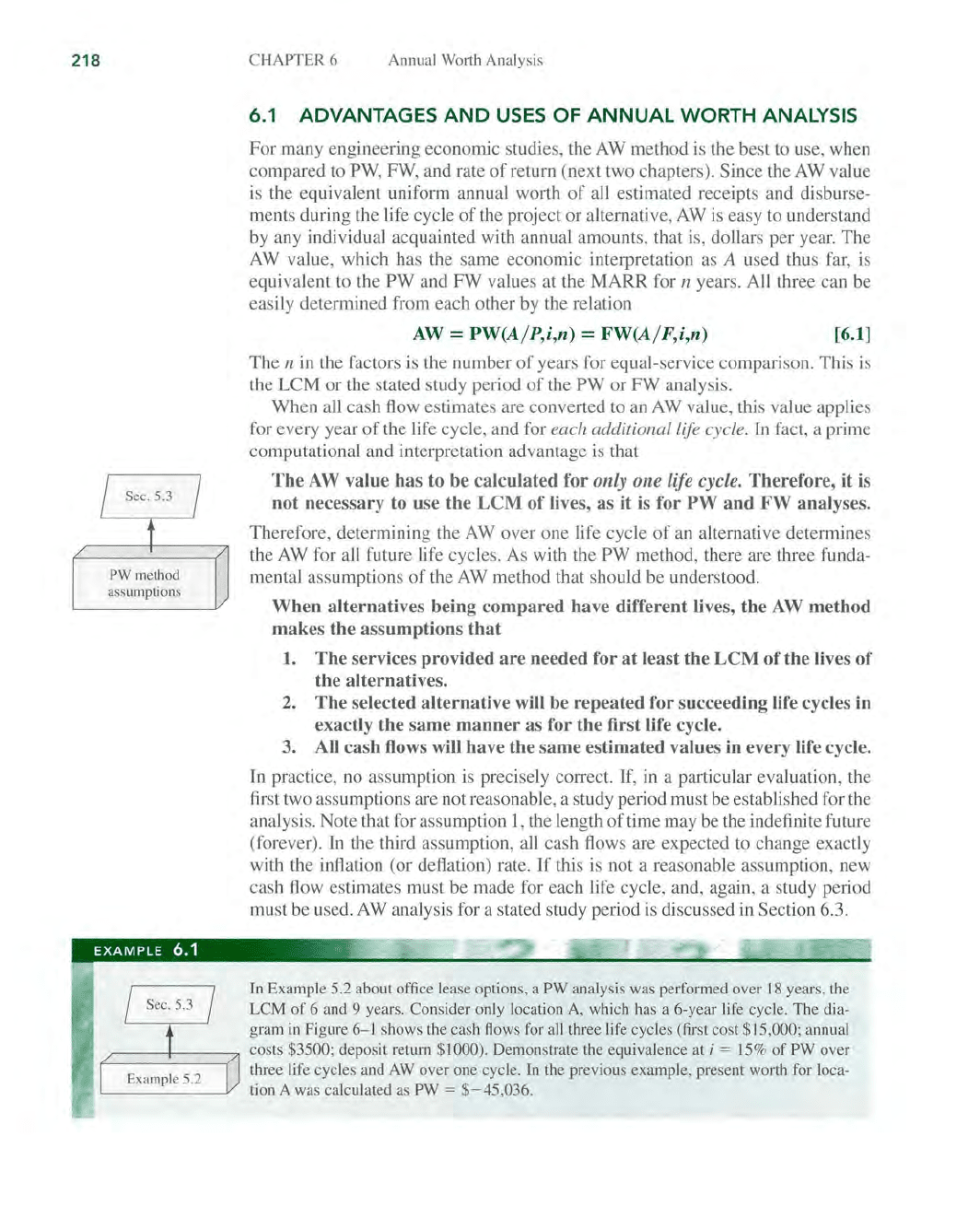

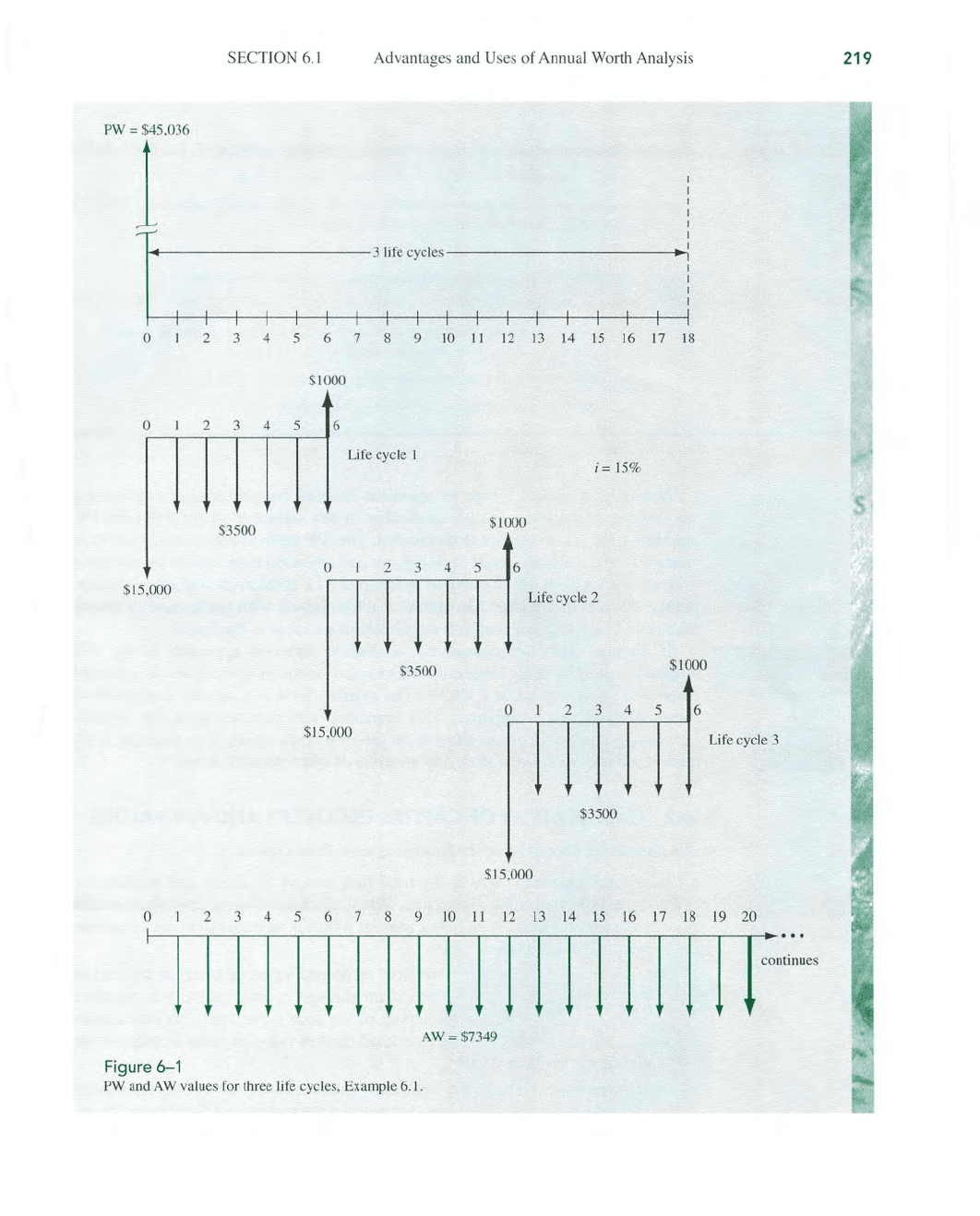

In

Example 5.2 about office lease options, a PW analysis was performed over

18

years, the

LCM

of

6 and 9 years. Consider only location

A,

which has a 6-year life cycle. The di

a-

gram

in

Figure

6-

1 shows the cash flows for

all

three life cy

cl

es

(fi

rst cost $15,000; annual

costs

$3500; deposit return $1000). Demonstrate the equivalence at i = 15%

of

PW over

three life cycles and

AW

over one cycle. In the previous example, present worth for loca-

tion A was calculated

as

PW =

$-45,036.

SECTION

6.1

Advantages and Uses

of

Annual Worth Analysis

PW = $45,036

1

I

I

I

I

I

1 t-ot--

----------3Iife

cycles -

----------

-.;

I

..

:

I

I

I

I

I

o 2 3 4 5 6 7 8 9 10

II

12 13 14

15

16

17 18

$1000

0

I 2

3

4

5 6

Li

fe

cycle 1

i=

15%

$3500

$1000

0

23456

$15,000

Li

fe

cycle 2

$3500

$1000

o

2 3 4 5

6

$15,000

Li

fe

cy

cl

e 3

$3500

$15,000

o

I

2 3 4 5 6 7 8 9

10

II

12 13

14

15

16

17

18 19 20

11111

11111

11111

III

II

:"~;:

"

AW

= $7349

Figure 6- 1

PW

and

AW

va

lu

es for three

li

fe cycle

s,

Example

6.

1.

219

220

CHAPTER

6 Annual Worth Analysis

Solution

Calculate the equivalent uniform annual worth value for all cash flows

in

the first life cycle.

AW

= -15,000(A/P,15%,6) + 1000(A/F,I5%,6) - 3500 =

$-7349

When the same computation is performed on each life cycle, the AW value is $- 7349.

Now, Equation [6.1] is applied to the

PW

value for

18

years.

AW

=

-45

,

036(A/P

,

15

%,18) =

$-7349

The

one-life-cycle

AW

value and the

PW

value based

on

18

years are equal.

Comment

If

the

FW

and AW equivalence relation is used, first find the FW from the PW over the

LCM, then calculate the

AW

value. (There are small round-off errors.)

FW

=

PW(F

/ P,

15

%,

18)

=

-45

,036(12.3755) =

$-557

,343

AW = FW(A/F,15%,18) = -557,343(0.01319) = $-

7351

Not only

is

annual worth an excellent method for performing

engineering

economy

studies,

but

it is also applicable in any situation where

PW

(and

FW

and Benefit/Cost) analysis can

be

utilized.

The

AW method is especially useful

in

certain types

of

studies: asset replacement and retention time studies to minimize

overall annual costs (both covered in

Chapter

II),

breakeven studies and make-

or-buy decisions (Chapter 13), and all studies dealing with production

or

manu-

facturing costs where a cost/unit

or

profit/unit

measure

is

the focus.

If

income

taxes are considered, a slightly different approach to the A W

method is used by

some

large corporations and financial institutions. It

is

termed

economic value added

or

EVA.TM

(The

symbol

EVA is a current trademark

of

Stern Stewart

and

Company.) This approach concentrates upon the wealth-

increasing potential that an alternative offers a corporation.

The

resulting EVA

values are the equivalent

of

an AW analysis

of

after-tax cash flows.

6.2 CALCULATION OF CAPITAL RECOVERY

AND

AW

VALUES

An alternative should

have

the following cash flow estimates:

Initial investment

P.

This

is

the total first

cost

of

all assets and services re-

quired to initiate the alternative.

When

portions

of

these investments take

place

over

several years, their

present

worth is an equivalent initial invest-

ment.

Use

this

amount

as

P.

Salvage value

S.

This

is the terminal estimated value

of

assets at the end

of

their useful life.

The

S

is

zero

if

no salvage is anticipated; S

is

negative

when it will

cost

money

to dispose

of

the assets.

For

study periods

shorter

than the useful life, S

is

the estimated market value

or

trade-in value at the

end

of

the study period.

Annual amount

A.

This is the equivalent annual

amount

(costs only for service

alternatives; costs and receipts for revenue alternatives).

Often this

is

the an-

nual operating cost

(AOC)

, so the estimate is already an

equivalent

A value.

SECTION 6.2 Calculation

of

Capital Recovery and

AW

Values

The

annual worth (AW) value for an alternative is comprised

of

two compo-

nents: capital recovery for the initial investment P at a stated interest rate (usu-

ally the

MARR)

and the equivalent annual amount

A.

The

symbol

CR

is

used for

the capital recovery component. In equation form,

AW=

-CR-A

[6.2]

Both CR and A have minus signs because they represent costs.

The

total annual

amount A is determined from uniform recurring costs (and possibly receipts) and

nonrecurring amounts.

The

PIA and pi F factors may be necessary to first obtain

a present worth

amount

, then

the

AI P factor converts this

amount

to the A value

in

Equation [6.2].

(If

the alternative

is

a revenue project, there will be positive

cash flow estimates present

in

the calculation

of

the A value.)

The

recovery

of

an

amount

of

capital P committed to an asset, plus the time

value

of

the capital at a particular interest rate, is a very fundamental principle

of

economic analysis.

Capital

recovery

is

the

equivalent

annual

cost

of

owning

the

asset

plus

the return

on

the initial investment.

The

AI

P factor is used to convert

P to an equivalent annual cost.

If

there

is

some anticipated positive salvage value

S at the end

of

the asset's useful life, its equivalent annual value is removed using

the AI F factor. This action reduces the equivalent annual

cost

of

owning the

asset. Accordingly,

CR

is

CR

=

-[P

(A

I P,i,n) - S(AI

F,i,n)]

The

computation

of

CR

and AW is illustrated in Example 6.2.

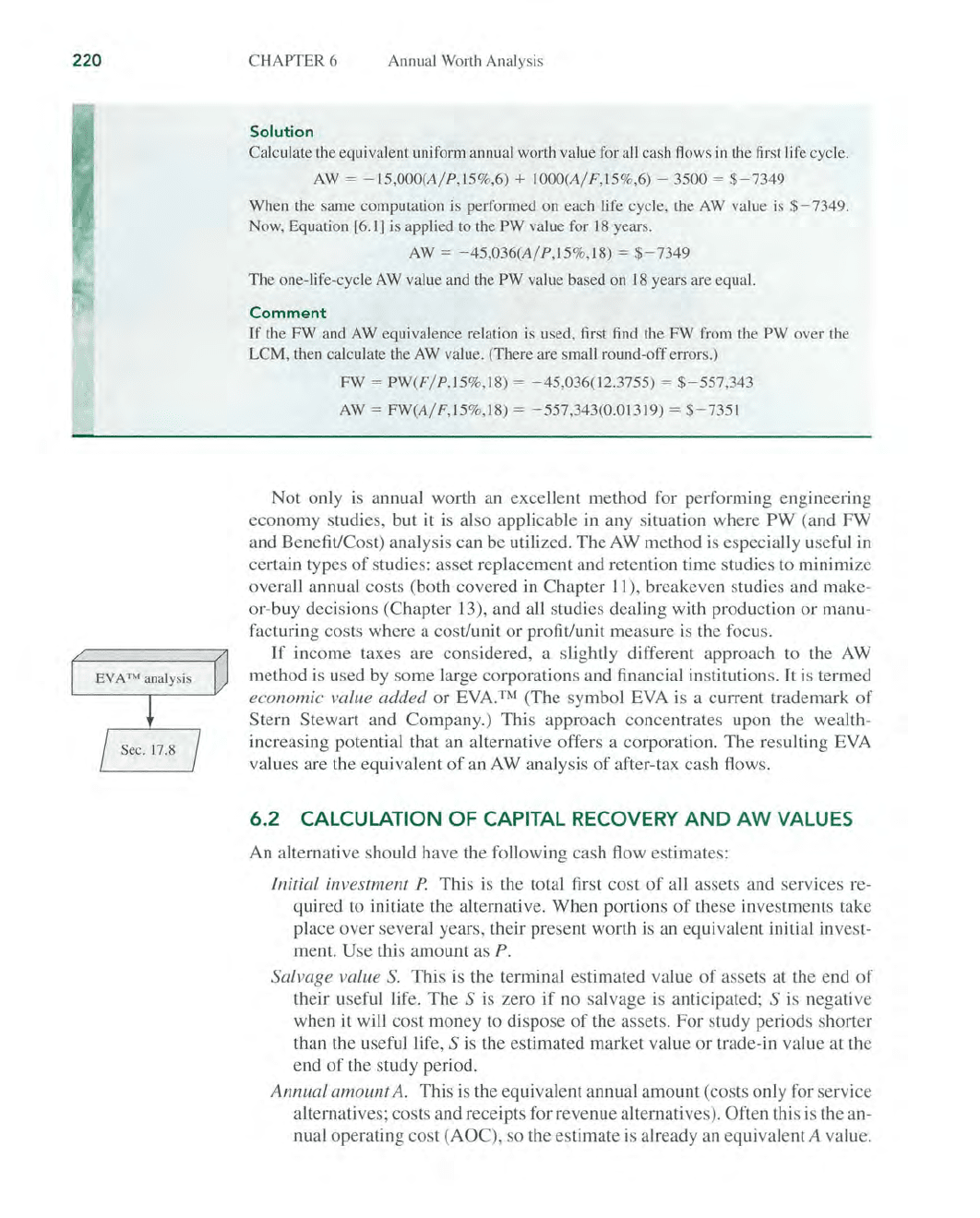

EXAMPLE

6.2

."

[6.3]

Lockheed Martin

is

increasing its booster thrust power

in

order to win more satellite

launch contracts from European companies interested in opening up new global

com-

munications markets. A piece

of

earth-based tracking equipment

is

expected to require

an

investment of$1 3 million, with $8 million committed now and the remaining $5 mil-

lion expended at the end

of

year 1

of

the project. Annual operating costs for the system

are expected to sta

rt

the first year and continue at

$0

.9 million

per

year.

The

useful life

of

the tracker

is

8 years with a salvage value

of

$0.5 million. Calculate the

AW

value for

the system, if the corporate

MARR

is currently

12

% per year.

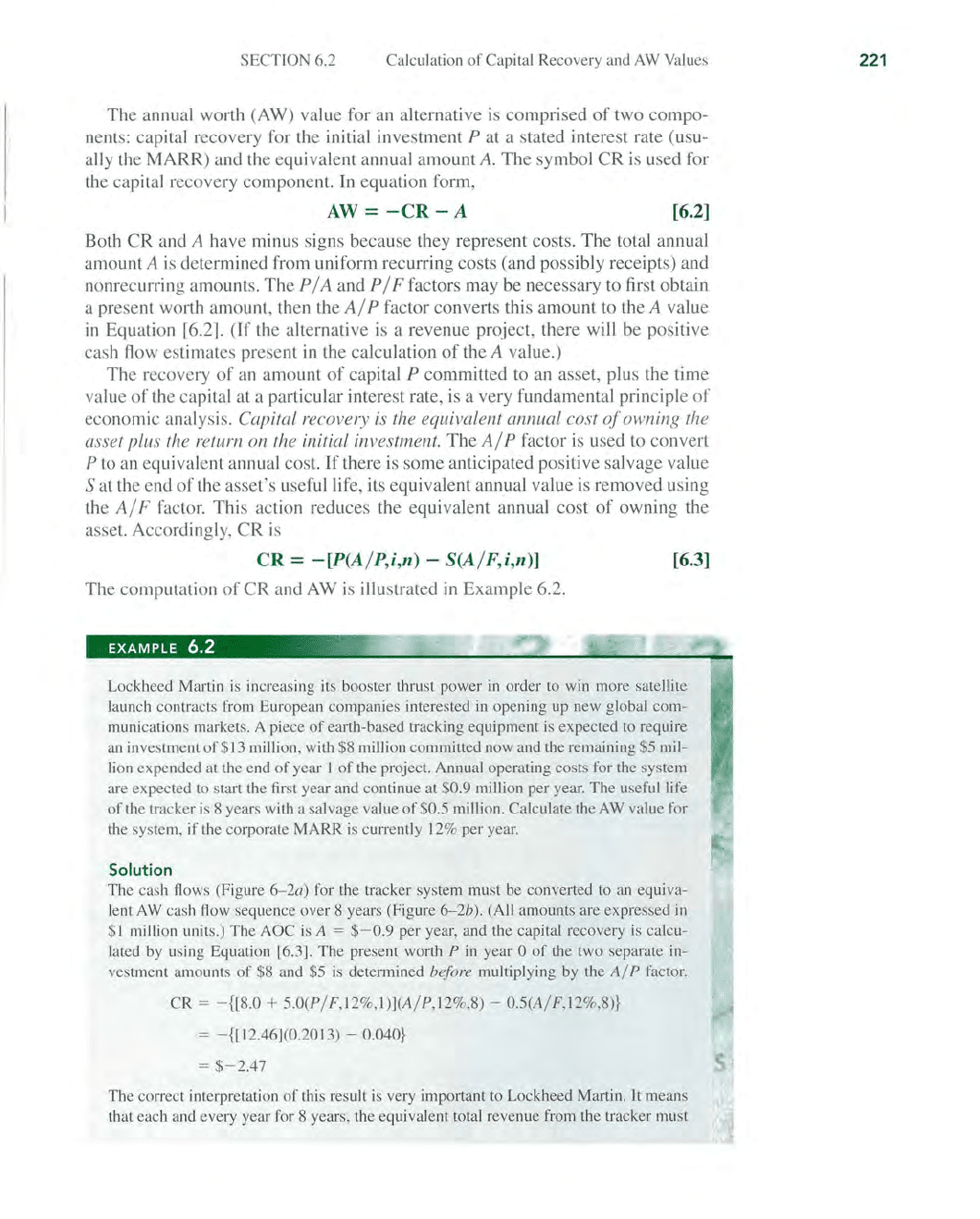

Solution

The ca

sh

flows (Figure 6-2a) for the tracker system must be converted to

an

equiva-

lent

AW

cash flow sequence over S years (Figure 6-2b). (All amounts are expressed in

$1

million units.)

The

AOC

is

A = $- 0.9 per year, and the capital recovery is calcu-

lated by using Equation l6.3].

The

present worth P in year 0

of

the two separate in-

vestment amounts

of

$8 and $5 is determined before mUltiplying by the A/ P factor.

CR

= -

([S.O

+ 5.0(P/

F,l2

%

,1)JCA

/P,12%,8) - 0.5(A/ F,

12

%,8)}

= -

([J

2.46](0.20 13) - 0.040}

= $- 2.47

The correct interpretation

of

this result

is

very important to Lockheed Martin. It means

that each and every year for 8 years, the equivalent total revenue from the tracker must

221

222

I

Sec. 2.3

I

t

/

AlP

and

AlF

factors

/

CHAPTER 6

Annual Worth Analysis

$0.5

0

I 2 3 4 5 6 7 8

1

$0.9

AW

=?

$5.0

$8.0

(a) (b)

Figure

6-2

(a) Cash flow diagram for satellite tracker costs, and (b) conversion

to

an

eq

ui

va

lent

AW

(in

$1 million), Example 6.

2.

be at least

$2

,470,000 just to

re

cover the initial present worth investment plus the

re-

quired return

of

12

% per ye

ar.

This does not include the AOC

of

$0.9 million each yea

r.

Since this amount,

CR

=

$-2.47

million,

is

an

equi

va

lent annual cost, as indicated

by

the minus sign, total A W is found

by

Equation [6.2].

AW

=

-2.47

- 0.9 =

$-3.37

million per year

This is the

AW

for all future life cycles

of

8 years, provided the costs rise at the same

rate

as

inflation, and the same costs and services are expected to apply for each suc-

ceeding life cycle.

There is a second, equally correct way to determine CR. Either method results

in

the same value. In Section 2.3, a relation between the

A/

P and

A/

F factors

was stated as

(A/F,i,n)

=

(A/P,i,n)

- i

Both factors are present

in

the

CR

Equation

[6

.3]. Substitute for the

A/

F factor

to obtain

CR

=

-{

P

(A/

P,i,n) -

S[(A/

P,i,n) -

i]}

= - [(P -

S)(A/P,i,n)

+

SCi)]

[6.4]

There

is

a basic logic to this formula. Subtracting S from the initial investment P

before applying the

A/

P factor recognizes that the salvage value will be recov-

ered. This reduces

CR

, the annual cost

of

asset ownership. However,

th

e fact that

S is not recovered until year

n

of

ownership is compensated for by charging the

annual interest

SCi)

against the CR.

In Example

6.2, the use

of

this second way to calculate

CR

results in

th

e same

value.

CR

= -([S.O + 5.0(P

/F,

12

%,

l)

- 0.5]

(A/

P,

12

%,S) + 0.5(0.12)}

=

-{[

12.46 - 0.5](0.2013) + 0.06} =

$-2.47

SECTION

6.3 Eva

lu

ating Alternatives by Annual Worth Analysis

Although either

CR

relation results in the sa

me

amount, it is better to consistently

use the same method.

The

first method, Equation

[6

.

3]

, will be used in this text.

For solution by computer, use the

PMT

function to determine

CR

only in a

single spreadsheet cell. The

ge

neral function

PMT(i

%,n,P,

F)

is rewritten using

the initi

al

investment as P a

nd

-S

for the

sa

lvage value. The format is

PM T(i % ,n,P,

-5

)

As an illustration, determine the

CR

only in Example 6.2 above. Since the ini-

tial investment is distributed

over

2

years-$8

million in year 0 and $5 million

in year

I-embed

the PV function into

PMT

to find the equivalent P in year

O.

The

co

mplete function for only the

CR

amount (in

$1

million units) is

PMT(l2%

,8,

8+PV(l2%

,1

,-5),-O.

5

),

where the embedded PV function

is

in

italic. The answer

of

$-2.4

7 (million) will be displayed

in

the spreadsheet

cell.

6.3 EVALUATING ALTERNATIVES

BY

ANNUAL

WORTH

ANALYSIS

The annual worth method is typically the easiest

of

the evaluation techniques to

perform, when the

MARR

is specified.

The

alternative selected has the lowest

eq

ui

valent annual cost (service alternatives), or highest equivalent income (rev-

enue alternatives). This means

th

at the selection guidelines are the sa

me

as for

the PW method, but u

si

ng the

AW

value.

For

mutually exclusive alternatives, calculate

AW

at

the MARR.

One

alternative: A W

?:

0,

MARR

is met

or

exceeded.

Two

or

more alternatives: Choose the lowest cost

or

highest income

(numerically largest)

AW

value.

If

an assumption in Section

6.1

is not acceptable for an alternative, a study period

analysis

mu

st be used. Then the cash flow estimates over the study period are

converted to AW amounts. This is illustrated later in Example 6.4.

EXAMPLE

6.3

PizzaRush, which

is

located

in

the general

Los

Angeles area, fares very well with its com-

petition

in

offering fast delivery.

Many

students

at

the area universities and

community

col-

leges work part-time delivering orders made via the web

at

PizzaRush.com.

The

owner, a

sof

tware engineering graduate

of

USC,

plans to purchase and install five portable, in-car

systems to increase delivery speed and accurac

y.

The

systems provide a link between the

web order-place

ment

software and the

On-Star

© system for satellite-generated directions to

any address

in

the

Lo

s Angeles area.

The

expected result is faster, friendlier servi

ce

to cus-

tomers, and

mor

e

income

for PizzaRush.

Each system costs

$46

00

, has a

5-year

u

sef

ul life, and may be

sa

lvaged for an estimated

$300

. Total operating cost for all systems is $

650

for the first year, increasing by

$50

per

year thereafter.

The

MARR

is 10%.

Per

form an

annua

l worth evaluation for the

owner

that

223

Q-Solv

224

CHAPTER 6 Annual Worth Analysis

answers the following questions.

Perform the solution

by

hand and by computer,

as

re-

quested below.

(a) How much new annual income

is

necessary to recover the investment at the MARR

of

10

% per year? Generate this value

by

hand and

by

computer.

(b) The owner conservatively estimates increased income

of

$1200 per year for

aJl

five

systems.

Is

this project financially viable at the MARR? Solve by hand and

by

com-

puter.

(c) Based on the answer

in

part (b), use the computer to determine how much new

income

PizzaRush must have to economically justify the project. Operating costs

remain

as

estimated.

Solution by Hand

(a and b) The

CR

and

AW

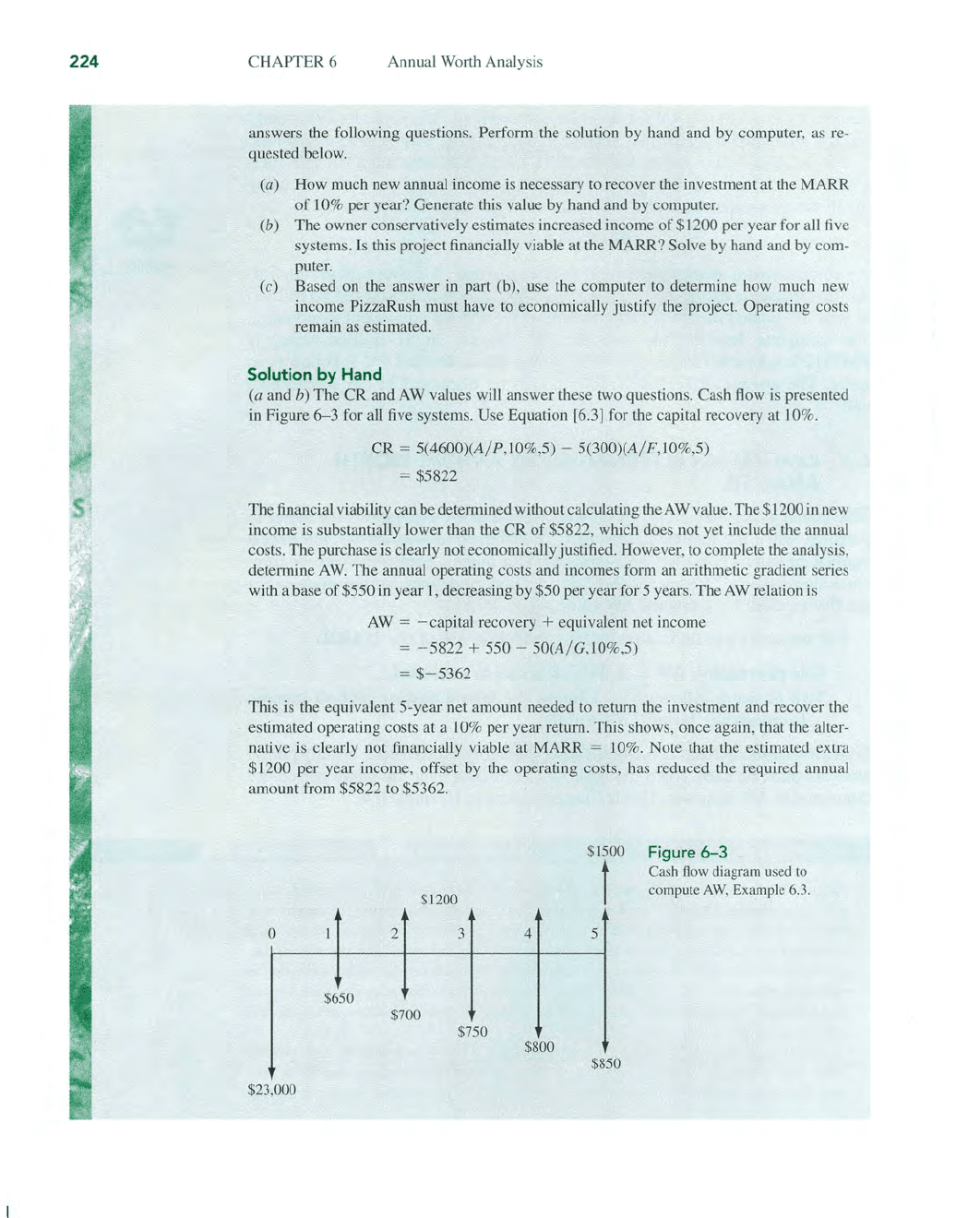

values will answer these two questions. Cash flow is presented

in

Figure

6-3

for all five systems. Use Equation [6.3) for the capital recovery at 10%.

CR =

5(4600)(A/P,lO%,5)

-

5(300)(A/F,lO%,5)

= $5822

The financial viability can be determined without calculating theAW value. The

$1200

in

new

income

is

substantially low

er

than the CR

of

$5822, which does not yet include the annual

costs. The purchase

is

clearly not economically justified. However, to complete the analysis,

determine

AW.

The annual operating costs and incomes form an arithmetic gradient series

with a base

of

$550 in year I, decreasing by $50 per yearfor 5 years. The A W relation

is

AW

=

-cap

ital recovery + equivalent net income

=

-5822

+ 550 - 50(A/G,1O%,5)

=

$-5362

This

is

the equivalent 5-year net amount needed to return the investment and recover the

estimated operating costs at a

10% per year return. This shows, once again, that the alter-

native is clearly not financially viable at MARR

= 10%. Note that the estimated extra

$1200 per year income, offset by the operating costs, has reduced the required annual

amount from $5822 to $5362.

$1500

Figure

6-3

t

Cash flow diagram used to

$1200

compute

AW,

Example 6.3.

0

2 3 4 5

$650

$700

$750

$800

$850

$23,000