Blank L., Tarquin A. Engineering Economy (McGraw-Hill Series in Industrial Engineering and Management)

Подождите немного. Документ загружается.

SECTION 9.3

Alternative Selection

Using Incremental B/C Analysis

There are several special considerations for

B/C

analysis that make it slightly

different from that for

ROR analysis.

As

mentioned earlier, all costs have a pos-

itive sign

in

the

B/C

ratio. Also, the ordering

of

alternatives

is

done on the basis

of

total costs in the denominator

of

the ratio. Thus,

if

two alternatives, A and B,

have equal initial investments and lives, but B has a larger equivalent annual

cost, then B must be incrementally justified against A. (This is illustrated in the

next example.)

If

this convention is not correctly followed, it is possible

to

get a

negative cost value in the denominator, which can incorrectly make

B/C

< 1 and

reject a higher-cost alternative that is actually justified.

Follow these steps to correctly perform a conventional

B/C

ratio analysis

of

two alternatives. Equivalent values can be expressed in

PW,

AW,

or FW terms.

l.

Determine the total equivalent costs for both alternatives.

2.

Order the alternatives by total equivalent cost; smaller first, then larger.

Calculate the incremental cost

(~C)

for the larger-cost alternative. This is

the denominator in

B/C.

3. Calculate the total equivalent benefits and any disbenefits estimated for

both alternatives. Calculate the incremental benefits

(~B)

for the larger-

cost alternative. (This is

~(B

-

D)

if

dis benefits are considered.)

4.

Calculate the incremental

B/C

ratio using Equation [9.2], (B -

D)/

c.

5.

Use the selection guideline

to

select the higher-cost alternative

ifB/C

:::::

1.0.

When the

B/C

ratio

is

determined for the lower-cost alternative, it is a compari-

son with the do-nothing (DN) alternative.

If

B/C

< l.0, then DN should be

selected and compared

to

the second alternative.

If

neither alternative has an

acceptable

B/C

value, the DN alternative must be selected. In public sector

analysis, the DN alternative

is

usually the current condition.

EXAMPLE

9.4

.

The city

of

Garden Ridge, Florida, has received designs for a new patient room wing to

the municipal hospital from two architectural consultants.

One

of

the two designs must

be accepted in order to announce it for construction bids. The costs and benefits are the

same

in

most categories, but the city financial manager decided that the three estimates

below should be considered

to

determine which design to recommend at the city council

meeting next week and to present to the citizenry

in

preparation for an upcoming bond

referendum next month.

Construction cost, $

Building maintenance cost, $/year

Patient usage cost, $/year

Design A

10,000,000

35,000

450,000

Design 8

15,000,000

55,000

200,000

The patient usage cost

is

an estimate

of

the amount paid by patients

over

the insurance

coverage generally allowed for a hospital room. The discount rate is 5%, and the life

of

325

Incremental ROR

326

CHAPTER 9 Benefit/Cost Analysis and Public Sector Economics

the building is estimated at

30 years.

(a) Use conventional BtC ratio analysis to select design A or B.

(b) Once the two designs were publicized, the privately owned hospital in the di-

rectly adjacent city

of

Forest Glen lodged a complaint that design A will reduce

its own municipal hospital's income by an estimated

$500,000 per year because

some

of

the day-surgery features

of

design A duplicate its services. Subsequently,

the Garden Ridge merchants' association argued that design B could reduce its

annual revenue by

an

estimated $400,000, because it will eliminate

an

entire

parking lot used by their patrons for short-term parking. The city financial man-

ager stated that these concerns would be entered into the evaluation

as

disbene-

fits

of

the respective designs. Redo the BtC analysis to determine if the economic

decision

is

still the same

as

when disbenefits were not considered.

Solution

(a) Since most

of

the cash flows are already annualized, the incremental BtC ratio

will use

AW

values. No disbenefit estimates are considered. Follow the steps

of

the procedure above:

1.

The

AW

of

costs is the sum

of

construction and maintenance costs.

A W

A

==

1

O,OOO,OOO(A/

P,5%,30) + 35,000 = $685,500

AWe

=

15,OOO,000(A/P

,

5%

,

30)

+ 55,000 = $1,030,750

2.

Design B has the larger

AW

of costs, so it

is

the alternative to

be

incre-

mentally justified. The incremental cost value is

ilC

=

AWe

-

AW

A = $345,250 per year

3.

The

AW

of

benefits is derived from the patient usage costs, since these are

consequences to the public. The benefits for the

BtC analysis are not the

costs themselves, but the

difference

if

design B is selected. The lower

usage cost each year

is

a positive benefit for design

B-

ilB = usage

A

-

usageB

= $450,000 - $200,000 = $250,000 per year

4.

The incremental BtC ratio

is

calculated by Equation [9.2].

BtC

==

. $250,000 = 0.72

$345,250

5.

The BtC ratio

is

less than 1.0, indicating that the extra costs associated

with design

Bare

not justified. Therefore, design A is selected for the con-

struction bid.

(b) The revenue loss estimates are considered disbenefits. Since the dis benefits of

design

Bare

$100,000 less than those of

A,

this positive difference

is

added to

the

$250,000 benefits

of

B to give it a total benefit of $350,000. Now

BtC = $350,000 = 1

OJ

$345,250 .

Design B

is

slightly favored.

In

this case the inclusion of disbenefits has reversed

the previous economic decision.

Thi.s

has probably made the situation more

di

f-

ficult politically. New disbenefits will surely be claimed in the near future

by

other special-interest groups.

SECTION 9.4 Incremental B/C Analysis

of

Multiple, Mutually Exclusive Alternatives

Like other methods, B/C analysis requires equal-service comparison

of

alter-

natives.

Usually, the expected useful life

of

a public project is long (25 or 30 or

more years), so alternatives generally have equal lives. However, when alterna-

tives do have unequal lives, the use

of

PW to determine the equivalent costs and

benefits requires that the

LCM

of

lives be used. This is an excellent opportunity

to use the A W equivalency

of

costs and benefits,

if

the implied assumption that

the project could be repeated is reasonable. Therefore, use AW-based analysis for

B/C ratios when different-life alternatives are compared.

9.4

INCREMENTAL SIC ANALYSIS

OF

MULTIPLE,

MUTUALLY EXCLUSIVE ALTERNATIVES

The procedure necessary to select one from three or more mutually exclusive

alternatives using incremental B/C analysis is essentially the same

as

that

of

the

last section. The procedure also parallels that for incremental

ROR analysis in

Section 8.6. The selection guideline

is

as

follows:

Choose the largest-cost alternative that is justified with an incremental

B/C

2:: 1.0 when this selected alternative has been compared with another

justified alternative.

There are two types

of

benefit

estimates-estimation

of

direct benefits, and

implied benefits based on usage cost estimates. Example 9.4 is a good illustra-

tion

of

the second type

of

implied benefit estimation. When direct benefits are

estimated, the

B/C

ratio for each alternative may be calculated first as an initial

screening mechanism to eliminate unacceptable alternatives. At least one alter-

native must have B/C

2:: 1.0 to perform the incremental B/C analysis.

If

all alter-

natives are unacceptable, the DN alternative

is

indicated as the choice. (This

is

the same approach as that

of

step 2 for "revenue alternatives only" in the

ROR

procedure

of

Section 8.6. However, the term "revenue alternative"

is

not applic-

able to public sector projects.)

As

in

the previous section comparing two alternatives, selection from multi-

ple alternatives by incremental B/C ratio utilizes total equivalent costs to initially

order alternatives from smallest to largest.

Pairwise comparison

is

then under-

taken. Also, remember that all costs are considered positive in B/C calculations.

The terms defender and challenger alternative are used in this procedure, as

in

a ROR-based analysis. The procedure for incremental B/C analysis

of

multiple

alternatives

is

as follows:

1.

Determine the total equivalent cost for all alternatives. (Use

AW,

PW, or

FW equivalencies for equal lives; use AW for unequal lives.)

2.

Order the alternatives by total equivalent cost, smallest first.

3.

Determine the total equivalent benefits (and any dis benefits estimated) for

each alternative.

4. Direct benefits estimation only: Calculate the

B/C

for the first ordered

alternative. (In effect, this makes

DN

the defender and the first alternative

the challenger.)

If

B/C <

1.0

, eliminate the challenger, and go to the next

327

Incremental

ROR

328

CHAPTER 9

Benefit/Cost Analysis and

Public Sector Economics

challenger. Repeat this until B/C ~ 1.0. The defender is eliminated, and the

next alternative is now the challenger. (For analysis

by

computer, deter-

mine the B/C for all alternatives initially and retain only acceptable ones

.)

5.

Calculate incremental costs

(~C)

and benefits

(~B)

using the relations

~c

= challenger cost - defender cost

~B

= challenger benefits - defender benefits

[9.4]

[9.5]

If

relative usage costs are estimated for each alternative, rather than direct

benefits,

~B

may be found using the relation

~B

= defender usage costs - challenger usage costs [9.6]

6.

Calculate the incremental B/C for the first challenger compared

to

the

defender.

B/C

=

~B/~C

[9.7]

If

incremental B/C

~

1.0 in Equation [9.7], the challenger becomes the

defender and the previous defender is eliminated. Conversely, if incremen-

tal B/C < 1.0, remove the challenger and the defender remains against the

next challenger.

7.

Repeat steps 5 and 6 until only one alternative remains. It is the selected one.

In all the steps above, incremental disbenefits may be considered by replacing

~B

with

~(B

- D),

as

in

the conventional B/C ratio, Equation [9.2].

EXAMPLE

9.5

..

"

The Economic Development Corporation (EDC) for the city

of

Bahia, California, and

Moderna County

is

operated

as

a not-for-profit corporation. It

is

seeking a developer that

wi

ll

place a major water park

in

the city or county area. Financial incentives will

be

awarded. In response to a request for proposal (RFP) to the major water park developers

in

the country, four proposals have been received. Larger and more intricate water rides and

in

creased size

of

the park will attract more customers, thus different levels

of

initial ince

n-

tives are requested

in

the proposals. One

of

these proposals will be accepted by the EDC

and recommended to the Bahia City Council and Moderna County Board

of

Trustees for

approval.

Approved and in-place economic incentive guidelines allow entertainment industry

prospects to receive up to

$500,000 cash as a first-year incentive award and

10

%

of

this

amount each year for 8 years

in

property tax reduction. All the proposals meet the require-

ments for these two incentives. Each proposal includes a provision that residents

of

the city

or county

wi

ll

benefit from reduced entrance (usage) fees when using the park. This fee re-

duction will be in effect

as

long

as

the property tax reduction incentive continues. The EDC

has estimated the annual total entrance fees with the reduction included for local residents.

Also, EDC estimated the extra sales tax revenue expected for the four park designs. These

estimates and the costs for the initial incentive and annual 10% tax reduction are summa-

rized

in

the top section

of

Table 9-1.

SECTION 9.4

Incremental B/C Analysis

of

Multiple, Mutually Exclusive Alternatives

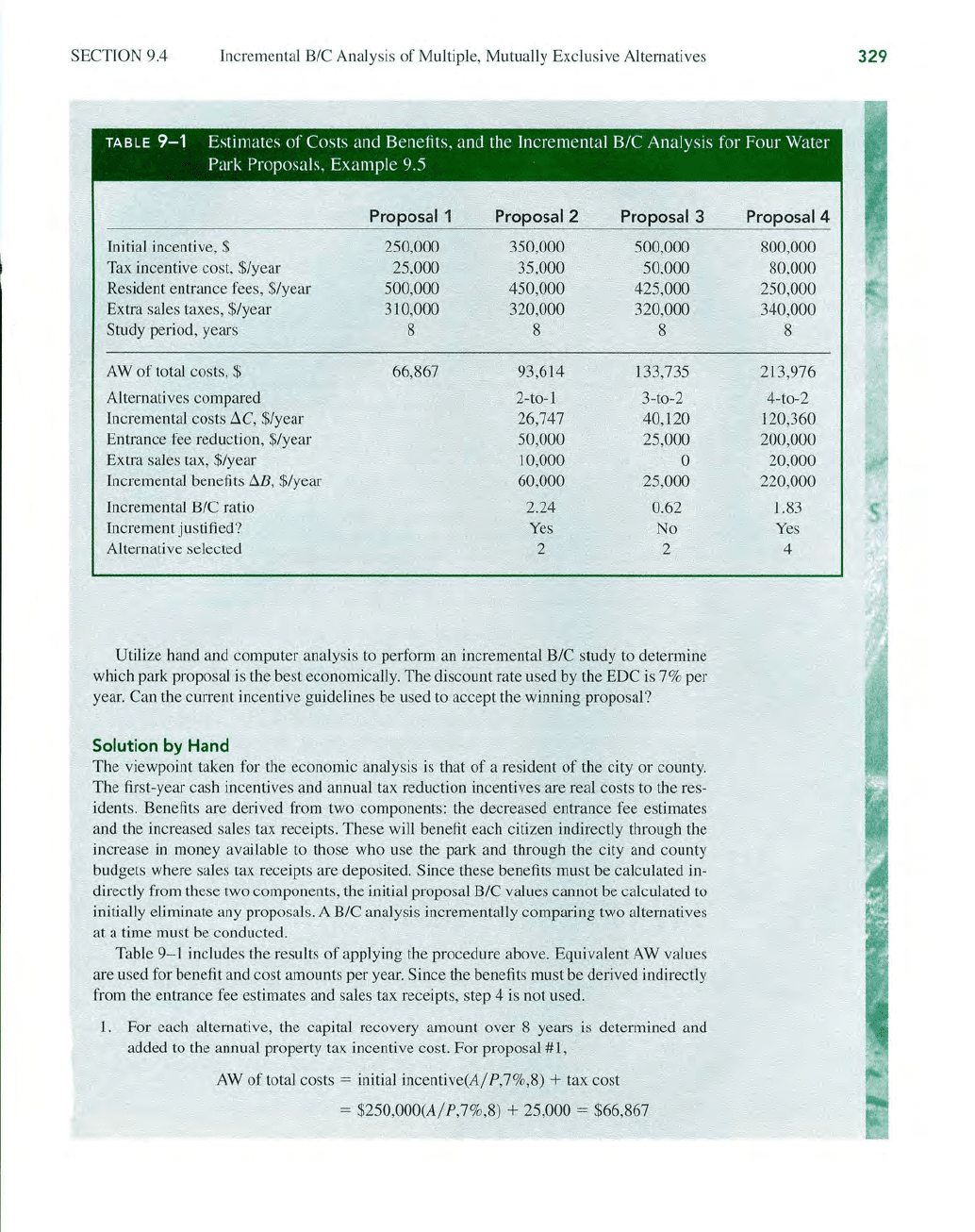

TABLE

9-1

Estimates

of

Costs and Benefits, and the Incremental BIC Analysis for Four Water

Park Proposals, Example 9.5

Proposal 1

Proposal 2 Proposal 3

Initial incentive, $ 250,000 350,000

500,000

Tax incentive cost, $/year 25,000 35,000

50,000

Resident entrance fees, $/year 500,000 450,000 425,000

Extra sales taxes, $/year

310,000 320,000

320,000

Study

period, years

8 8

8

A W of total costs, $

66,867 93,614 l33,735

Alternatives compared

2-to-l 3-to-2

Incremental costs

ilC

, $/year 26,747

40

,1

20

Entrance fee reduction, $/year 50,000

25,000

Extra sales tax, $/year 10,000

0

Incremental benefits ilB, $/year 60,000

25,000

Incremental B/C ratio 2.24

0.62

Increment justified?

Yes

No

Alternative selected 2

2

Utilize hand and computer analysis

to

perform

an

incremental B/C study to determine

which park proposal is the best economically. The discount rate used

by

the EDC

is

7% per

year. Can the

ClUTent

incentive guidelines be used to accept the winning proposal?

Solution

by

Hand

The viewpoint taken for the economic analysis is that

of

a resident

of

the city or county.

The first-year cash incentives and annual tax reduction incentives are real costs to the res-

idents. Benefits are derived from two components: the decreased entrance fee estimates

and the increased sales tax receipts. These will benefit each citizen indirectly through the

increase

in

money available to those who use the park and through the city and county

budgets where sales tax receipts are deposited.

Since these benefits must be calculated

in-

directly from these two components, the initial proposal B/C values cannot be calculated to

initially eliminate any proposals. A B/C analysis incrementally comparing two alternatives

at a time must be conducted.

Table 9- 1 includes the results

of

applying the procedure above. Equivalent

AW

values

are used for benefit and cost amounts per year.

Since the benefits must be derived indirectly

from the entrance fee estimates and sales tax receipts, step 4 is not used.

1.

For each alternative, the capital recovery amount over 8 years

is

determined and

added to the annual property tax incentive cost. For proposal #1,

AW

of

total costs = initial incentive(A/P,7%,8) + tax cost

= $250,000(A/ P,7%,8) + 25,000 = $66,867

Proposal 4

800,000

80,000

250,000

340,000

8

2l3,976

4-to-2

120,360

200,000

20,000

220,000

1.83

Yes

4

329

330

~

E-Solve

CHAPTER 9 Benefit/Cost Analysis and Public Sector Economics

2.

The alternatives are ordered

by

the

AW

of

total costs in Table 9-1.

3.

The annual benefit

of

an

alternative

is

the incremental benefit

of

the entrance fees and

sales tax amounts. These are calculated in step 5.

4.

This step

is

not used.

5.

Table

9-1

shows incremental costs calculated

by

Equation [9.4]. For the 2-to-l

comparison,

~c

= $93,614 - 66,867 = $26,747

Incremental benefits for

an

alternative are the sum

of

the resident entrance fees com-

pared

to

those

of

the next-lower-cost alternative, plus the increase in sales tax receipts

over those

of

the next-lower-cost alternative. Thus, the benefits are determined incre-

mentally for each pair of alternatives. For example, when proposal #2

is

compared

to

proposal #1, the resident entrance fees decrease

by

$50,000 per year and the sales

tax

receipts increase by $10,000. Then the total benefit is the sum

of

these, that is,

~B

= $60,000 per year.

6.

For the 2-to-l comparison, Equation

[9

.

7]

results in

B/C = $60,000/$26,747 = 2.24

Alternative #2 is clearly incrementally justified. Alternative

#1

is eliminated, and

alternative

#3

is the new challenger

to

defender #2.

7.

This process

is

repeated for the 3-to-2 comparison, which has an incremental B/C

of

0.62 because the incremental benefits are substantially less than the increase in costs.

Therefore, proposal #3

is

eliminated, and the 4-to-2 comparison results in

B/C = $220,000/$120,360 = 1.83

Since

B/C > 1.0, proposal #4 is retained. Since proposal #4 is the one remaining

alternative, it

is

selected.

The recommendation for proposal #4 requires an initial incentive

of

$800,000, which

exceeds the

$500,000 limit

of

the approved incentive limits. The EDC will have

to

request

the City Council and County Trustees

to

grant

an

exception to the guidelines.

If

the excep-

tion

is

not approved, proposal #2 is accepted.

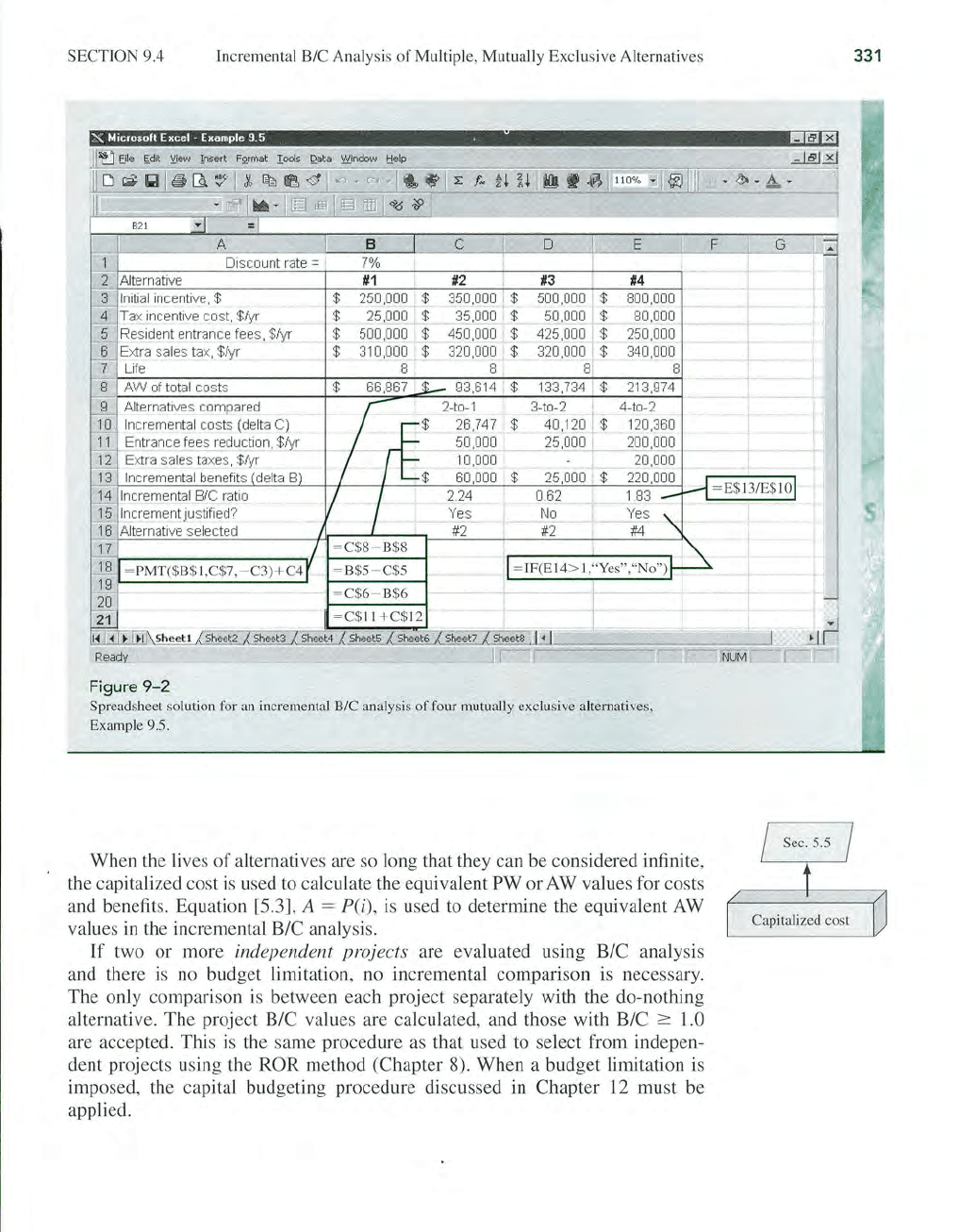

Solution by

Computer

Figure

9-2

presents a spreadsheet using the same calculations

as

those in Table 9-1. Row 8

cells include the function PMT(7%,8,

-initial

incentive) to calculate the capital recovery

for each alternative, plus the annual

tax

cost. These

AW

of

total cost values are used

to

order the alternatives for incremental comparison.

The cell tags for rows 10 through

13

detail the formulas for incremental costs and

benefits used in the incremental

B/C computation (row 14). Note the difference in row

11

and 12 formulas, which find the incremental benefits for entrance fees and sales tax, re-

spectively. The order

of

the subtraction between columns

in

row

11

(e.g., =

B5

- C5, for

the

2-to-1 comparison) must be correct

to

obtain the incremental entrance fees benefit. The

IF operators

in

row

15

accept or reject the challenger, based upon the size

of

B/C. After

the 3-to-2 comparison with

B/C = 0.62

in

cell D14, alternative #3 is eliminated. The final

selection is alternative #4, as in the solution

by

hand.

SECTION 9.4 Incremental B/C Analysis

of

Multiple, Mutually Exclusive Alternatives

X Microsoft

Excel-

Example

9_5

.

I!I~Ei

Figure

9-2

Spreadsheet so

lu

ti

on

for an incremental B/C analysis

of

four mutually exclusive alternatives,

Example 9.5.

When the lives

of

alternatives are so long that they can be considered infinite,

the capitalized cost

is

used to calculate the equivalent PW or

AW

values for costs

and benefits. Equation [5.3], A = P(i), is used to determine the equivalent

AW

values in the incremental

B/C

analysis.

If

two or more independent projects are evaluated using

B/C

analysis

and there is

no

budget limitation,

no

incremental comparison is necessary.

The only comparison is between each project separately with the do-nothing

alternative. The project B/C values are calculated, and those with B/C

:2::

1.0

are accepted. This is the same procedure as that used to select from indepen-

dent projects using the

ROR

method (Chapter 8). When a budget limitation is

imposed, the capital budgeting procedure discussed in Chapter

12

must be

applied.

I

Sec.5.5

I

Capitalized cost

331

332

CHAPTER

9 Benefit/Cost Analysis and Public Sector Economics

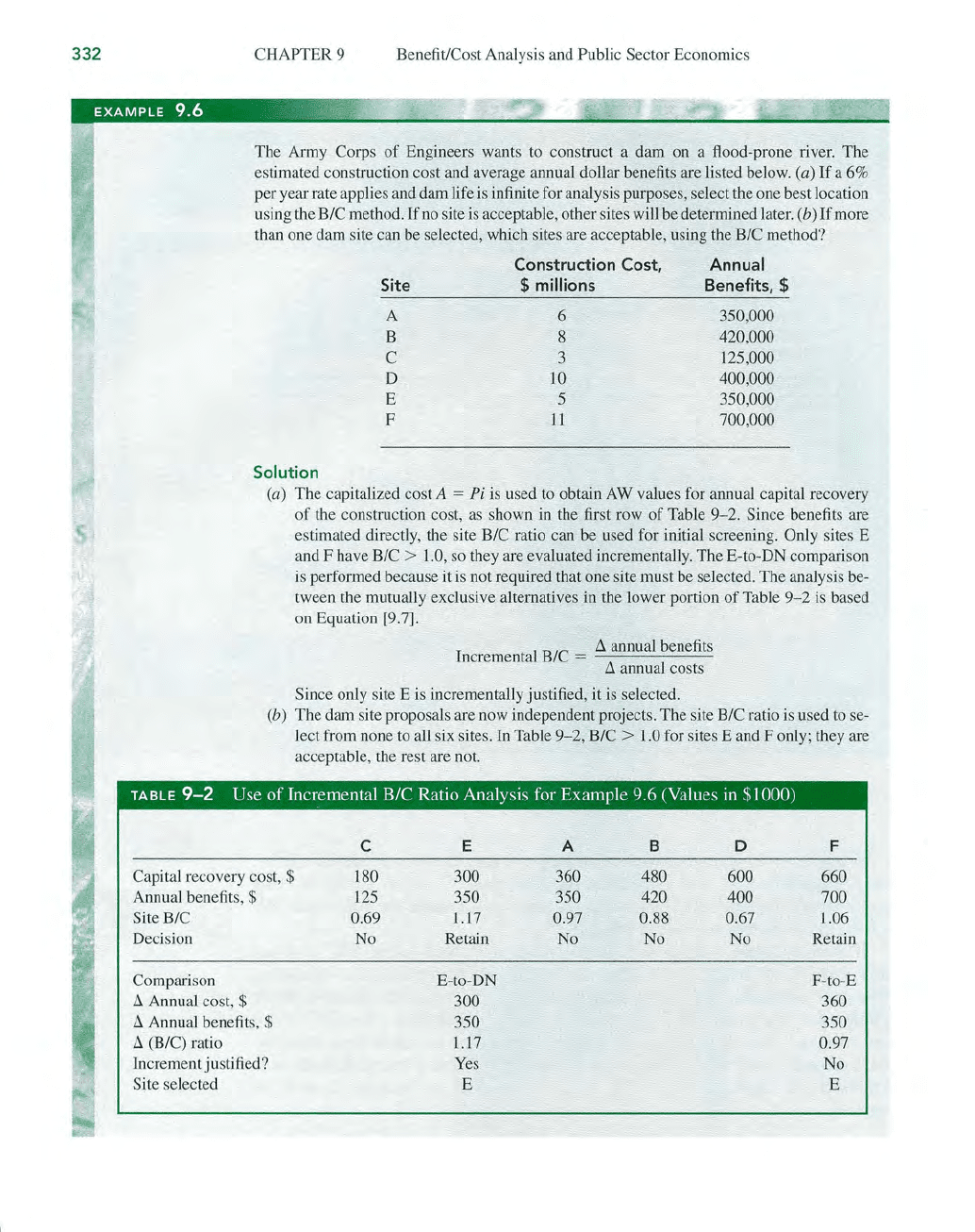

The Army Corps

of

Engineers wants to construct a

dam

on a flood-prone river. The

estimated construction cost and average annual dollar benefits are listed below.

(a)

If

a 6%

per

year rate applies and dam life is infinite for analysis purposes, select the one best location

using the

B/C method.

If

no site is acceptable, other sites will

be

determined later.

(b)

If

more

than one dam site can be selected, which sites are acceptable, using the

B/C method?

Construction Cost,

Annual

Site

$ millions Benefits, $

A 6 350,000

B 8 420,000

C

3

125,000

D

10

400,000

E 5

350,000

F

11

700,000

Solution

(a) The capitalized cost A =

Pi

is used to obtain AW values for annual capital recovery

of

the construction cost, as shown in the first row

of

Table

9-2.

Since benefits are

estimated directly, the site

B/C ratio can

be

used for initial screening. Only sites E

and F have

B/C > 1.0, so they are evaluated incrementally.

The

E-to-DN comparison

is performed because

it is not required that

one

site must be selected. The analysis be-

tween the mutually exclusive alternatives in the lower portion

of

Table

9-2

is based

on Equation [9.7].

Incremental

B/C =

_Ll_a_n_n_ua_l_b_e_n_efi_t_s

Ll

annual costs

Since only site E is incrementally justified, it is selected.

(b) The dam site proposals are now independent projects. The site B/C ratio is used to se-

lect from none to all six sites. In Table

9-2,

B/C > 1.0 for sites E and F only; they are

acceptable, the rest are not.

TABLE

9-2

Use

of

Incremental B/C Ratio Analysis for Example 9.6 (Values

in

$ I 000)

C

E A B D F

Capital recovery cost, $

180 300 360

480

600

660

Annual benefits, $ 125

350

350

420

400

700

Site

B/C

0.69 1.17 0.97 0.88 0.67

l.06

Decision No Retain

No No No

Retain

Comparison E-to-DN F-to-E

L1

Annual cost, $

300

360

L1

Annual benefits, $

350 350

L1

(B/C)

ratio 1.17

0.97

Increment justified? Yes

No

Site selected E E

PROBLEMS

Comment

In part (a), suppose that site G is added with a construction cost

of

$10 million and an

annual benefit

of

$700,000. The site B/C is acceptable at B/C =

700/600

= 1.17. Now, in-

crementally compare

G-to-E; the incremental B/C =

350/300

= 1.17, in favor

of

G.

In this

case, site F must be compared with G. Since the annnal benefits

are the same ($700,000),

the B/C ratio

is

zero and the added investment is not justified. Therefore, site G

is

chosen.

CHAPTER

SUMMARY

The benefit/cost method is used primarily to evaluate projects and to select from

alternatives

in

the public sector. When one

is

comparing mutually exclusive al-

ternatives, the incremental B/C ratio must be greater than or equal to

l.0

for the

incremental equivalent total cost to be economically justified. The

PW,

AW,

or

FW

of the initial costs and estimated benefits can be used to perform an incre-

mental B/C analysis.

If

alternative lives are unequal, the

AW

values should be

used, provided the assumption

of

project repetition is not unreasonable. For inde-

pendent projects, no incremental B/C analysis is necessary. All projects with

B/C

2:

1.0 are selected provided there is no budget limitation.

Public sector economics are substantially different from those

of

the private

sector. For public sector projects, the initial costs are usually large, the expected

life is long (25,

35

, or more years), and the sources for capital are usually a combi-

nation

of

taxes levied on the citizenry, user fees, bond issues, and private lenders.

It is very difficult to make accurate estimates

of

benefits

for

a public sector project.

The interest rates, called the discount rates in the public sector, are lower than

those for corporate capital financing. Although the discount rate is

as

important to

establish as the MARR, it can be difficult

to

establish, because various government

agencies qualify for different rates. Standardized discount rates are established

for some federal agencies.

PROBLEMS

333

Public Sector Economics

9.1

State the difference between public and

private sector alternatives with respect

to

the following characteristics.

9.2 Indicate whether the following character-

istics are primarily associated with public

sector or private sector projects.

(a) Size

of

investment

(b)

Life

of

project

(c) Funding

(d)

MARR

(a) Profits

(b)

Taxes

(c) Disbenefits

(d)

Infinite life

(e)

User fees

(f)

Corporate bonds

334

CHAPTER

9

Benefit/Cost Analysis and

Public Sector Economics

9.3 Identify

each

cash flow as a benefit, dis-

bene

fit

,

or

cost.

(a) $

500

,

000

annual income from

tourism created by a freshwater

reservoir

(b)

$

700,000

per

year

maintenance by

container ship port authority

(c)

Expenditure

of

$45 million for tun-

nel construction

on

an interstate

hi

ghway

(d)

Elimination

of

$1.3 million in

salaries for

co

unty residents based

on reduced international trade

(e) Reduction

of

$375,000 per year in

car

accident repairs

because

of

im-

proved lighting

(f)

$700,000 per year loss

of

revenue

by

farmers because

of

highway

right-of-

way purchases

9.4 During its

20

years

in

business,

Deware

Co

nstruction

Company

has always devel-

oped its contracts under a fixed-fee

or

cost-plus arrangement.

Now

it has been

offered an opportunity to participate in a

proj

ect

to provide cross-country

highway

transportation in an international

se

tting,

speci fically, a

country

in Africa.

If

ac-

ce

pted, D

eware

will

work

as subcontractor

to a lar

ge

r European corporation, and the

BOT

form

of

contracting will

be

used with

the African country government.

Describe

for the president of

Dew

are at least

four

of

the signi ficant

diff

erences that may be ex-

pected when the

BOT

format is utilized in

I ieu

of

its more traditional forms

of

con-

tract maki ng.

9.5

If

a corporation accepts the

BOT

form

of

contracting,

(a)

identify two risks taken by

a corporation and

(b) state how these risks

can be reduced by the

government

partner.

Project

B/C

Value

9.6

The

estimated annual cash flows for a pro-

posed city

gove

rnment

project are costs

of

$450,000

per year, benefits

of

$600,000

per

year, and disbenefits

of

$100,000

per

year.

Determine

the (a) B/C ratio and

(b)

value

of

B -

C.

9.7 Use spreadsheet

software

such as Excel,

PW

analysis, and a

discount

rate

of

5% per

year

to determine

that

the B/C value for

the following estimates is 0.375, making

the project not acceptable us

in

g the ben

efi

t!

cost method. (a)

Enter

the values and

equations on the spreadsheet so they may

be

changed

for the

purpose

of

sensitivity

analysis.

First

cost

= $8 million

Annual

cost

=

$800,000

per year

Benefit

=

$550,000

per

year

Disbenefit =

$100

,

000

per

year

(b)

Do

the following sensitivity analysis

by changing only

two

cells on

your

spreadsheet.

Change

the

discount rate to

3%

per year,

and

adjust

the annual

cost

es-

timate until

B/C =

l.023

.

This

make

s the

project

just

acceptable using benefit!cost

analysis.

9.8 A proposed regulation regarding the re-

moval

of

arsenic

from

drinking water

is

expected to

have

an annual

cost

of

$200

per household

per

year.

If

it

is assumed

that there are

90

million households

in

the

country and that the regulation could save

12

lives per year,

what

would the value

of

a human life have to

be

for the B/C ratio to

be equal to

1.0?

9.9

The

U.S. Environmental Protection Agency

has established that 2.5%

of

the median

household

income

is a

reasonable

amount

to pay for safe drinking water.

The

median

hou

se

hold

income

is

$30,000

per year. For

a regulation that

would

affect the health

of

people in 1 %

of

the households,

what

would the health benefits have to equal

in

dollars per

household

(for that 1 %

of