Hua C., Wong R. Differential Equations and Asymptotic Theory in Mathematical Physics

Подождите немного. Документ загружается.

292

SO

we get,

as

<

+

+m,

where

Also

we know

and

1

4n

A(R)

=

-1S212R

+

o(R),

as

R

+

+co.

C

(qvf),

vf'),

then

aj(R)

is nonnegative and non-

Let

aj(R)

=

decreasing function, we have

$)_<R

aj(R)

I

QjAj(R)

=

O(R),

as

R

-+

+co.

We notice that

aj(R)

=

0

when

0

<

R

<

p?),

and

aj(pkfl)

(j

-

aj(pf))

=

(qv,+,,

(j)

v~+~).

(j)

Therefore, we have

Let

N

-+

co,

we have

293

From Tauberian Theorem, we have

OD

where

I

=

C

Ij

=

J,

q(z,

y)dzdy,

which implies

j=1

The Corollary

4.1

is proved.

0

Finally, if

R

c

R",

n

=

1

or

2,

is

a

fractal

drum,

and

the Minkowski

dimension of

dR

is

6

E

(n

-

1,

n),

then we have

Corollary

4.2.

For the remainder term

r(R),

we have

r(R)

=

o(R~),

as

R

4

+a.

References

Gelfand I.M., Levitan

B.M.,

On

a

simple identity for the characteristic values

of

a differential operator

of

the second order (Russian) D.A.N.

88(1953), 593-

596.

Cao Cewen, On the asymptotic estimation

of

the trace

of

a partial differential

operator,

Scientia Sinica,

Special Issue

11(

1979), 56-68.

Cao Cewen, On the asymptotic trace

of

the second order self-adjoint elliptic

operator, Proceedings

1980

Beijing symposium Diff. Geo. and

Equ.,

vol

3,

1 1707- 1 1 14.

1.

1.

1.

294

4.

Chen Hua, Sleeman

B.D.,

Fractal drums and n-dimensional modified Weyl-

Berry conjecture, Comm. Math. Phys., 168(1995), 581-607.

5. E.C. Titchmarsh, Eigenfunction expansions associated with second order dif-

ferential equations, Part

11,

Oxford, 1958.

LIMITATIONS AND MODIFICATIONS OF

BLACK-SCHOLES MODEL

*

LISHANG JIANG AND XUEMIN REN

Institute

of

Math., Tongji University, Shanghai, China

In this paper we investigate the limitations of Black-Scholes model and provide

some modifications and some applications in pricing of real options and option-like

contracts also.

Our

modifications are based on the following assumptions: jump-

diffusion process, stochastic interest rate, variable volatility and implied volatility.

1.

Introduction

In this paper, we start by a brief review of Black-Scholes model, discuss its

limitations in detail, and show some modifications.

1.1.

Motivation

of

Black-Scholes model

The call(put) option gives the holder the right to buy(sel1)

a

fixed amount

of an asset

S

at a specified time

T

in future for an agreed price

K.

The

key problem is to find a way to determine the fair price of the option in its

whole life, such that

(ST

-

K)+,

call;

(K

-

ST)+,

put.

V(ST,T)

=

There are two different style options: European option can be exercised

only on maturity while American option can be exercised at any time before

maturity.

1.2.

Foundations

of

Black-Scholes model

To derive Black-Scholes formula, we need following assumptions and argu-

ments

*supported by the national natural science foundation

of

china (no.

10171078)

295

296

0

Asset price

st

is governed by a geometric Brownian motion

where

E(dWt)

=

0,

Var(dWt)

=

dt;

0

Interest rate

T

never changes and is same for borrowing or lending;

0

Asset's volatility

o

is

known and never changes for all maturities;

0

There are no transaction costs and taxes for either asset or option;

0

Unlimited short selling is allowed;

0

The underlying asset can be traded continuously and in infinitesi-

mally small numbers of units;

Upon the assumptions above, for European put option, there is an

unique martingale measure

Q

such that

V,

=

e-T(T-t)EQ((K

-

StlFt)),

(1.2)

From the point of view of PDE, there exists a function

V

=

(S,

t)

which

satisfies

where

q

is the dividend rate

of

St.

From the equation

(1.3),

we can obtain

the famous Black-Scholes formula

:

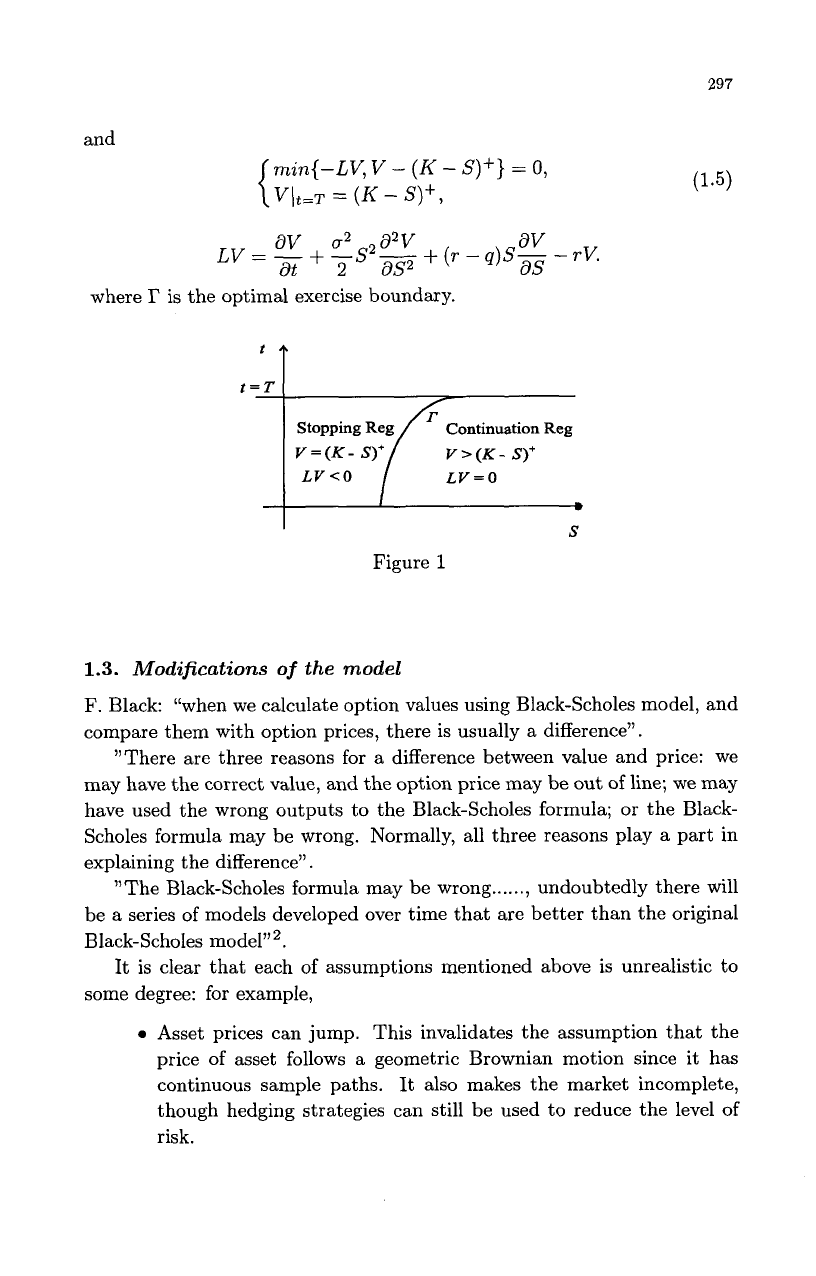

As

for American put option, we can find

a

function

V

=

V(S,t)

which

satisfies

and

min{-LV,

v

-

(K

-

S)+}

=

0,

{

V(t=T

=

(K

-

S)+,

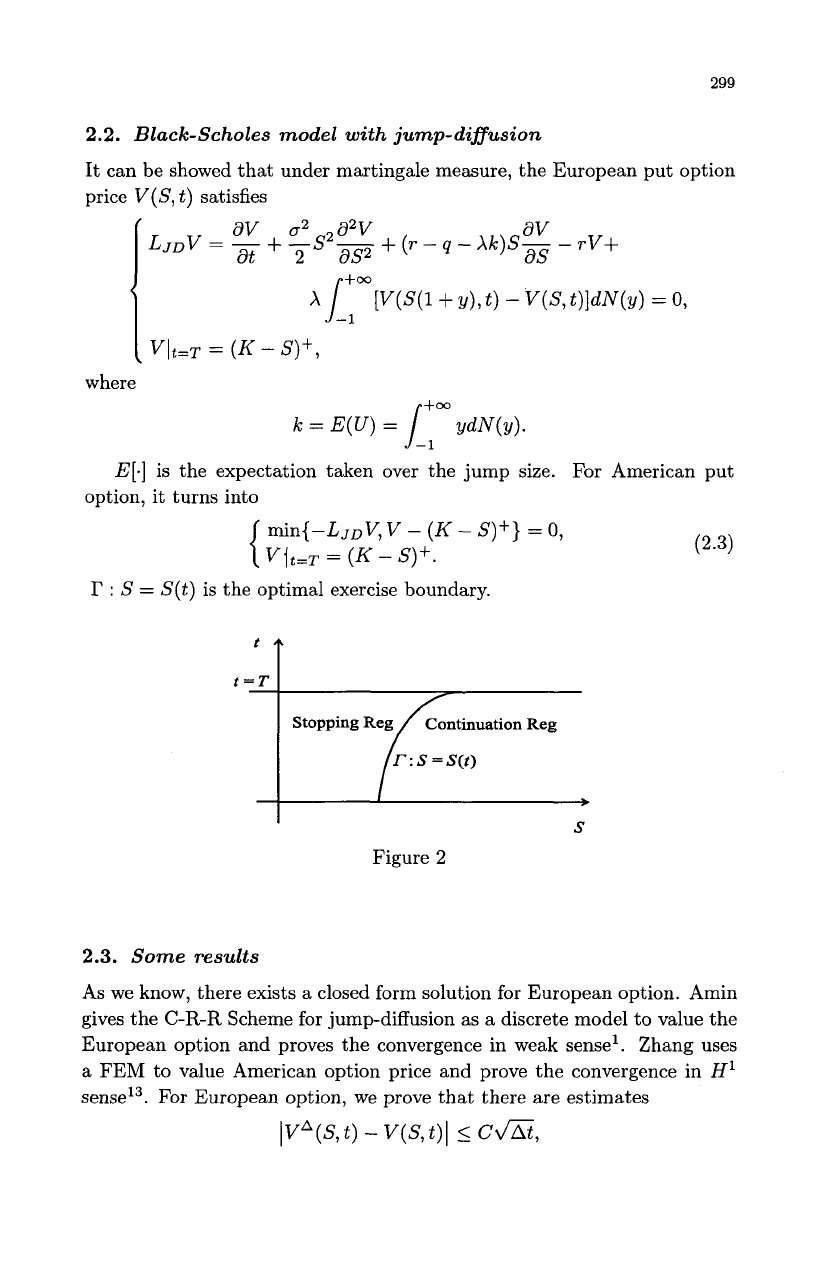

297

(1.5)

av

02

a2v

aV

at

2

as2

as

LV

=

-

+

-s2-

+

(r

-

4)s-

-

rv.

where

I’

is the optimal exercise boundary.

‘T

t=T

Continuation

Reg

V>(K-

S)’

LV=O

S

Figure

1

1.3.

Modifications

of

the

model

F.

Black: “when we calculate option values using Black-Scholes model, and

compare them with option prices, there is usually a difference”.

”There are three reasons for a difference between value and price: we

may have the correct value, and the option price may be out of line; we may

have used the wrong outputs to the Black-Scholes formula; or the Black-

Scholes formula may be wrong. Normally, all three reasons play a part in

explaining the difference”.

”The Black-Scholes formula may be wrong

......,

undoubtedly there will

be

a

series of models developed over time that are better than the original

Black-Scholes model”

’.

It

is clear that each of assumptions mentioned above is unrealistic to

some degree: for example,

0

Asset prices can jump. This invalidates the assumption that the

price of asset follows a geometric Brownian motion since it has

continuous sample paths. It also makes the market incomplete,

though hedging strategies can still be used to reduce the level of

risk.

298

0

The risk-free interest rate does vary and usually in an unpredictable

way. We can adapt some models to allow for

a

stochastic risk-

free rate, especially when we price the option with relatively long

maturity.

Among the inputs for Black-Scholes formula, only the volatility

CJ

can not be observed directly from the market.

If

we derive it from

Black-Scholes formula using quoted option prices, we will find the

assumption that the volatility is a constant

is

not true. The reason

may be that the distributions of asset returns tend to have fatter

tails than suggested by the log-normal model.

Despite

all

of the potential

flaws

in the model assumptions, analysis of

market derivative prices show that the Black-Scholes model does provide a

quite good approximation to the market and an insight into the usefulness

of dynamic hedging. The fact that the assumptions not hold in practice

does not mean that the model has no use. In our opinion, the best way is

to consider some more realistic assumptions.

In the following sections, we will modify Black-Scholes model under the

assumption of jump diffusion process and stochastic interest rate, and find

a robust method to derive the implied volatility.

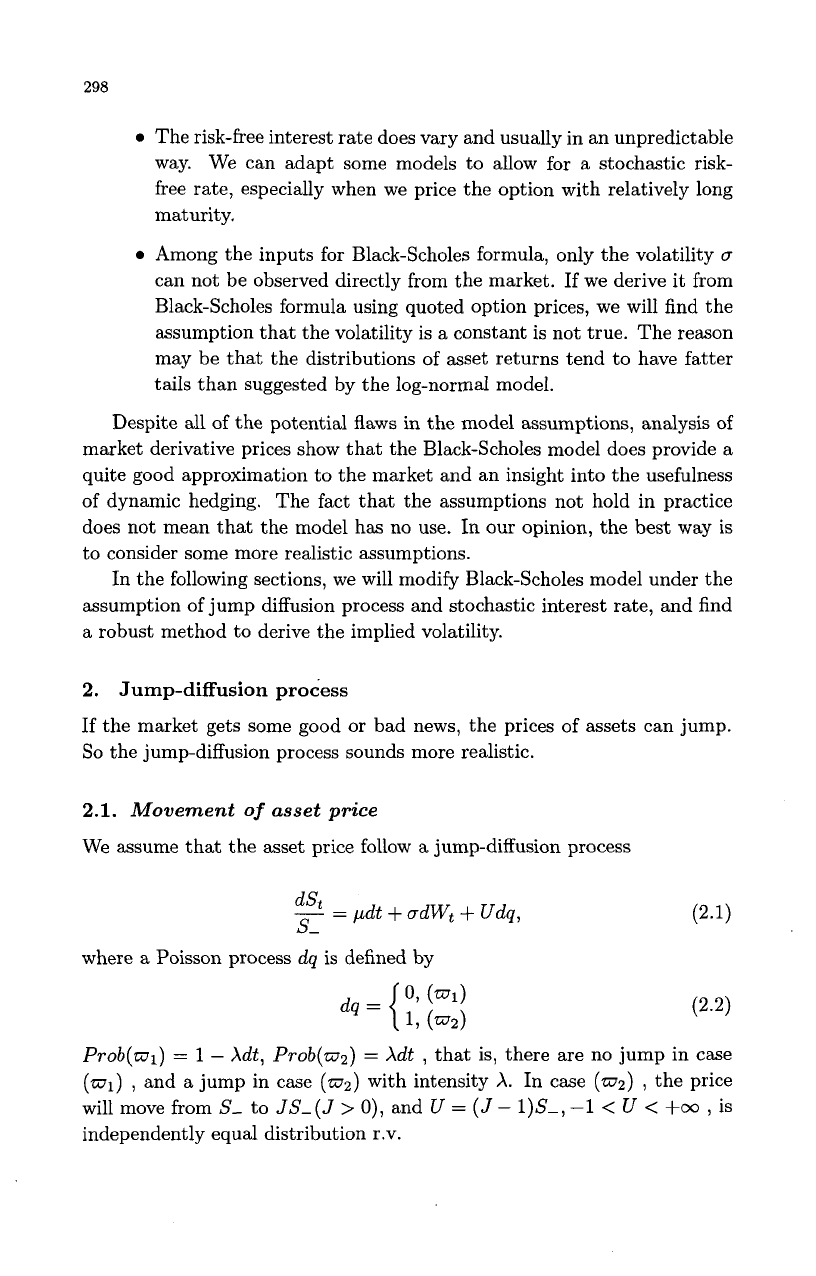

2.

Jump-diffusion

process

If

the market gets some good or bad news, the prices of assets can jump.

So

the jump-diffusion process sounds more realistic.

2.1.

Movement

of

asset price

We assume that the asset price follow

a

jump-diffusion process

_-

dSt

-

pdt

+

adWt

+

Udq,

S-

where a Poisson process

dq

is defined by

Prob(a1)

=

1

-

Xdt,

Prob(az)

=

Xdt

,

that is, there are no jump in case

(wl)

,

and

a

jump in case

(az)

with intensity

A.

In case

(wz)

,

the price

will move from

S-

to

JS-(J

>

0),

and

U

=

(J

-

l)S-,

-1

<

U

<

+cc

,

is

independently equal distribution r.v.

299

2.2.

Black-Scholes model with jump-diffusion

It can be showed that under martingale measure, the European put option

price

V(S,

t) satisfies

av

ff2

,a2v

dV

LJDV

=

-

+

-S

-

+

(T

-

-

M)S-

-

rV+

at

2

as2

dS

where

k

=

E(U)

=

E[.]

is the expectation taken over the jump size. For American put

option, it turns into

(2.3)

min{-LJDV, V

-

(K

-

S)+}

=

0,

{

Vjt=T

=

(K

-

S)+.

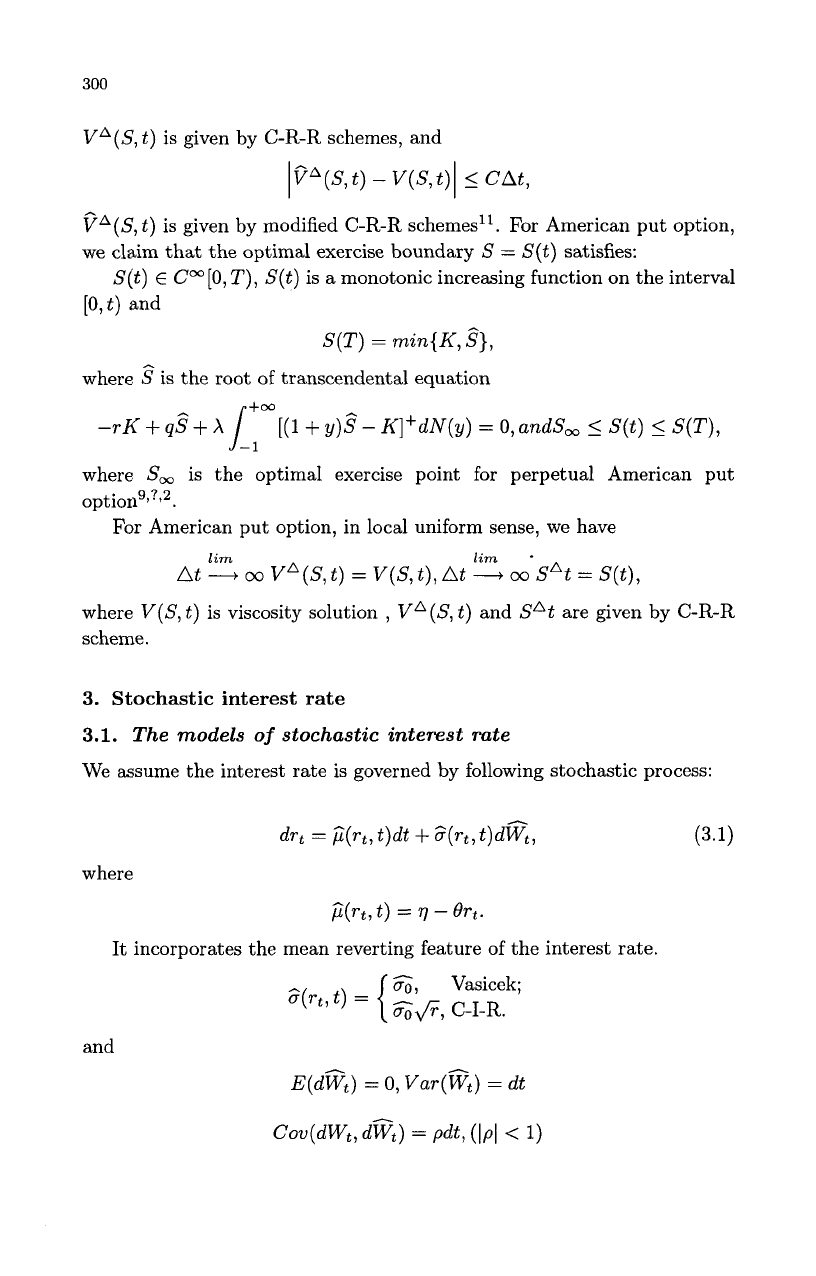

I'

:

S

=

S(t)

is the optimal exercise boundary.

'T

r

:

s

=

s(t)

S

I

Figure

2

2.3.

Some results

As

we know, there exists a closed form solution for European option. Amin

gives the

C-R-R

Scheme for jumpdiffusion as a discrete model to value the

European option and proves the convergence in weak sense'. Zhang uses

a

FEM

to value American option price and prove the convergence in

H1

sense13. For European option, we prove that there are estimates

IVA(S,t) -V(S,t)I

5

CJat,

300

VA(S,

t)

is given by C-R-R schemes, and

IpA(S,t)

-

V(S,t)l

5

Cat,

pA(S,

t)

is given by modified C-R-R schemes'l. For American put option,

we claim that the optimal exercise boundary

S

=

S(t)

satisfies:

S(t)

E

Cm[O,

T),

S(t)

is a monotonic increasing function on the interval

[O,t)

and

S(T)

=

min{K,

S},

where

s^

is the root of transcendental equation

-rK

+

qg

+

X

llw[(l

+

y)s^

-

K]+dlV(y)

=

0,

andS,

5

S(t)

5

S(T),

where

S,

is the optimal exercise point for perpetual American put

opti011~9?*~.

For American put option, in local uniform sense, we have

lim

lim

At

--t

00

VA(S,

t)

=

V(S,t),At

-

00

SAt

=

S(t),

where

V(S,

t)

is viscosity solution

,

VA(S,

t)

and

SAt

are given by C-R-R

scheme.

3.

Stochastic interest rate

3.1.

The models

of

stochastic interest rate

We assume the interest rate is governed by following stochastic process:

where

j2(rt,

t)

=

77

-

Ort.

It incorporates the mean reverting feature

of

the interest rate.

301

Remark

3.1:

the range of

rt

is

Vasicek model

:

-m

<

rt

<

+m

C-I-R

model:if2q>$,O<rt

<+a

3.2

Black-Scholes model with stochastic interest rate

satisfies

Under

a

martingale measure, European put option price

V

=

V(S,

T,

t)

av

u=

2a2v

aV

Lsrv

=

+

TS

+(q-Or)%

-rv

=

O(0

<

s

<

+m,r

E

D,O

5

t

<

t),

+

pcTsz(r,

t)g

+

4~2(T,

t)g

+

rsm

(3.2)

{

V(S,r,T)

=(K-S)+(OIS<+m,rED),

where

D={

R,

Vasicek;

R+,

C-I-R.

Remark: From Fichera theory for second order partial differential equa-

tions with nonnegative characteristic form, we know that European put

option problem is well posed, if

2q

>.

6j2

in C-I-R model, that is, we should

not impose any boundary condition on

r

=

0.

We introduce

a

zero coupon bond with maturity

T

as a numeraire.

P(r,

t)

denotes the value of this zero coupon bond. Under this relative price

system, there exists a martingale measure

Q

such that

2

=

EQ[gIFt].

P(r,

t)

satisfies

+

;z2(r,t)$$

+

(q--Or)%

-rP=

0

,(r

E

D,O

5

t

<

T)

P(r,T)

=

1,

(r

E

0).

(3.3)

~(r,

t)

=

B(t)e-A(t)T, (3.4)

It has affine structure solution