Hull J.C. Risk management and Financial institutions

Подождите немного. Документ загружается.

108

Chapter 4

(with semiannual payments and one having just been made), the yield is

10.4% per annum. What is the bond's price? What is the 18-month zero

rate? All rates are quoted with semiannual compounding.

4.9. Suppose that 6-month, 12-month, 18-month, 24-month, and 30-month

zero rates are 4%, 4.2%, 4.4%, 4.6%, and 4.8% per annum, respectively,

with continuous compounding. Estimate the cash price of a bond with a

face value of 100 that will mature in 30 months and pays a coupon of 4%

per annum semiannually.

4.10. A three-year bond provides a coupon of 8% semiannually and has a cash

price of 104. What is the bond's yield?

4.11. Why are US Treasury rates significantly lower than other rates that are

close to risk free?

4.12. What does duration tell you about the sensitivity of a bond portfolio to

interest rates. What are the limitations of the duration measure?

4.13. A five-year bond with a yield of 11% (continuously compounded) pays an

8% coupon at the end of each year. (a) What is the bond's price? (b) What

is the bond's duration? (c) Use the duration to calculate the effect on the

bond's price of a 0.2% decrease in its yield. (d) Recalculate the bond's

price on the basis of a 10.8% per annum yield and verify that the result is

in agreement with your answer to (c).

4.14. Repeat Problem 4.13 on the assumption that the yield is compounded

annually. Use modified durations.

4.15. A six-year bond with a continuously compounded yield of 4% provides a

5% coupon at the end of each year. Use duration and convexity to

estimate the effect of a 1% increase in the yield on the price of the bond.

How accurate is the estimate?

4.16. Explain three ways in which a vector of deltas can be calculated to manage

nonparallel yield curve shifts.

4.17. Estimate the delta of the portfolio in Table 4.8 with respect to the first two

factors in Table 4.9.

ASSIGNMENT QUESTIONS

4.18. An interest rate is quoted as 5% per annum with semiannual compound-

ing. What is the equivalent rate with (a) annual compounding, (b) monthly

compounding, and (c) continuous compounding.

4.19. Portfolio A consists of a 1-year zero-coupon bond with a face value of

$2,000 and a 10-year zero-coupon bond with a face value of $6,000.

Portfolio B consists of a 5.95-year zero-coupon bond with a face value

of $5,000. The current yield on all bonds is 10% per annum (continuously

Interest Rate Risk 109

compounded). (a) Show that both portfolios have the same duration. (b)

Show that the percentage changes in the values of the two portfolios for a

0.1% per annum increase in yields are the same. (c) What are the

percentage changes in the values of the two portfolios for a 5% per annum

increase in yields?

4.20. What are the convexities of the portfolios in Problem 4.19? To what extent

does (a) duration and (b) convexity explain the difference between the

percentage changes calculated in part (c) of Problem 4.19?

4.21. When the partial durations are as in Table 4.7 estimate the effect of a shift

in the yield curve where the 10-year rate stays the same, the 1-year rate

moves up by 9e and the movements in intermediate rates are calculated by

interpolation between 9e and 0. How could your answer be calculated

from the results for a rotation presented in Section 4.8?

4.22. Suppose that the change in a portfolio value for a 1-basis-point shift in the

3-month, 6-month, 1-year, 2-year, 3-year, 4-year, and 5-year rates are (in

$million) +5, —3, — 1, +2, +5, +7, and +8, respectively. Estimate the delta

of the portfolio with respect to the first three factors in Table 4.9. Quantify

the relative importance of the three factors for this portfolio.

CHAPTER

Volatility

Hedging schemes such as those described in the last two chapters elim-

inate much of the risks from trading activities. This is because traders are

required to ensure that Greek letters such as delta, gamma, and vega are

within certain limits. But trading portfolios are not totally free of risk. At

any given time, a financial institution still has a residual exposure to

changes in hundreds or even thousands of market variables such as

interest rates, exchange rates, equity prices, and commodity prices. The

volatility of a market variable measures uncertainty about the future

value of the variable. It is important for risk managers to monitor the

volatilities of market variables in order to assess potential losses. This

chapter describes the procedures they use to carry out the monitoring.

We begin by defining volatility and then explain how volatility can be

implied from option prices or estimated from historical data. The com-

mon assumption that percentage returns from market variables are

normally distributed is examined and we present the power law as an

alternative. After that we move on to consider models with imposing

names such as exponentially weighted moving average (EWMA), auto-

regressive conditional heteroscedasticity (ARCH), and generalized auto-

regressive conditional heteroscedasticity (GARCH). The distinctive

feature of these models is that they recognize that volatility is not

constant: during some periods it may be relatively low, whereas during

others it may be relatively high. The models attempt to keep track of the

variations in the volatility through time.

112 Chapter 5

5.1 DEFINITION OF VOLATILITY

The volatility of a variable is defined as the standard deviation of the

return provided by the variable per unit of time when the return is

expressed using continuous compounding. When volatility is used for

option pricing, the unit of time is usually one year, so that volatility is the

standard deviation of the continuously compounded return per year.

However, when volatility is used for risk management, the unit of time

is usually one day, so that volatility is the standard deviation of the

continuously compounded return per day.

In general, is equal to the standard deviation of , where

is the value of the market variable at time T and is its value today.

The expression equals the total return (not the return per unit

time) earned in time T expressed with continuous compounding. If is

per day, T is measured in days; if is per year, T is measured in years.

When T is small, the continuously compounded return of a market

variable is close to the percentage change. It follows that, for small T,

is approximately equal to the standard deviation of the percentage

change in the market variable in time T. Suppose, for example, that a

stock price is $50 and its volatility is 30% per year. The standard

deviation of the percentage change in the stock price in one week is

approximately

30 = 4.16%

A one-standard-deviation move in the stock price in one week is therefore

50 0.0416, or $2.08.

When the time horizons considered are short, our uncertainty about a

future stock price, as measured by its standard deviation, increases (at least

approximately) with the square root of how far ahead we are looking. For

example, the standard deviation of the stock price in four weeks is

approximately twice the standard deviation in one week. This corresponds

to the adage "uncertainty increases with the square root of time".

Variance Rate

Risk managers often focus on the variance rate rather than the volatility-

The variance rate is defined as the square of the volatility. The variance

rate per year is the variance of the continuously compounded return in

one year; the variance rate per day is the variance of the continuously

compounded return in one day. Whereas the standard deviation of the

return in time T increases with the square root of time, the variance of

Volatility 113

this return increases linearly with time. If we wanted to be pedantic, we

could say that it is correct to talk about the variance rate per day but that

volatility is "per square root of day".

Trading Days vs. Calendar Days

When volatilities are calculated and used, an issue that crops up is

whether time should be measured in calendar days or trading days. As

shown in Business Snapshot 5.1, research shows that volatility is much

higher when the exchange is open for trading than when it is closed. As a

result, when estimating volatility from historical data, analysts tend to

Business Snapshot 5.1 What Causes Volatility?

It is natural to assume that the volatility of a stock price is caused by new

information reaching the market. This information causes people to revise their

opinions on the value of the stock. The price of the stock changes and volatility

results. However, this view of what causes volatility is not supported by

research. With several years of daily stock price data, researchers can calculate:

1. The variance of stock price returns between the close of trading on one

day and the close of trading on the next day when there are no

intervening nontrading days

2. The variance of the stock price returns between the close of trading on

Friday and the close of trading on Monday

The second variance is the variance of returns over a three-day period. The

first is a variance over a one-day period. We might reasonably expect the

second variance to be three times as great as the first variance. Fama (1965),

French (1980), and French and Roll (1986) show that this is not the case.

These three research studies estimate the second variance to be 22%, 19%, and

10.7% higher than the first variance, respectively.

At this stage you might be tempted to argue that these results are explained

by more news reaching the market when the market is open for trading. But

research by Roll (1984) does not support this explanation. Roll looked at the

prices of orange juice futures. By far the most important news for orange juice

futures prices is news about the weather and news about the weather is equally

likely to arrive at any time. When Roll did a similar analysis to that just

described for stocks, he found that the second (Friday-to-Monday) variance is

only 1.54 times the first variance.

The only reasonable conclusion from all this is that volatility is to a large

extent caused by trading itself. (Traders usually have no difficulty accepting

this conclusion!)

114 Chapter 5

ignore days when the exchange is closed. The usual assumption is that

there are 252 days per year.

Define as the volatility per year of a certain asset, while is the

equivalent volatility per day of the asset. The standard deviation of the

continuously compounded return on the asset in one year is either or

. It follows that

with the result that the daily volatility is about 6% of annual volatility.

5.2 IMPLIED VOLATILITIES

As shown in Appendix C at the end of this book, the one parameter in

option pricing formulas that cannot be directly observed is the volatility

of the asset price. This allows traders to imply a volatility from option

prices.

To illustrate how implied volatilities are calculated, suppose that the

market price of a three-month European call option on a non-dividend-

paying stock is $1.875 when the stock price is $21, the strike price is $20

and the risk-free rate is 10%. The implied volatility is the value of

volatility that, when substituted into the Black-Scholes option pricing

formula, gives an option price of $1.875. Unfortunately, it is not possible

to invert the Black-Scholes formula so that volatility is expressed as a

function of the option price and other variables. However, an iterative

search procedure can be used to find the implied volatility . For example,

we can start by trying =0.20. This gives a value for the option price

equal to $1.76, which is less than the market price of $1.875. Since the

option price is an increasing function of , a higher value of is required.

We can next try =0.3. This gives a value for the option price equal to

$2.10, which is too high and means that must lie between 0.20 and 0.30.

Next, we try a value of 0.25 for . This also proves to be too high,

showing that the implied volatility lies between 0.20 and 0.25. Proceeding

in this way, we can halve the range of values for at each iteration and

calculate its correct value to any required accuracy.

1

In this example, the

1

This method is presented for illustration. Other more powerful search procedures are

used to calculate implied volatilities in practice.

Volatility 115

implied volatility is 0.235, or 23.5% per annum. A similar procedure can

be used in conjunction with binomial trees to find implied volatilities for

American options.

Implied volatilities are used extensively by traders, as we will explain in

Chapter 15. However, risk management is largely based on historical

volatilities. The rest of this chapter will be concerned with developing

procedures for using historical data to monitor volatility.

5.3 ESTIMATING VOLATILITY FROM HISTORICAL

DATA

When the volatility of a variable is estimated using historical data, it is

usually observed at fixed intervals of time (e.g., every day, week, or month).

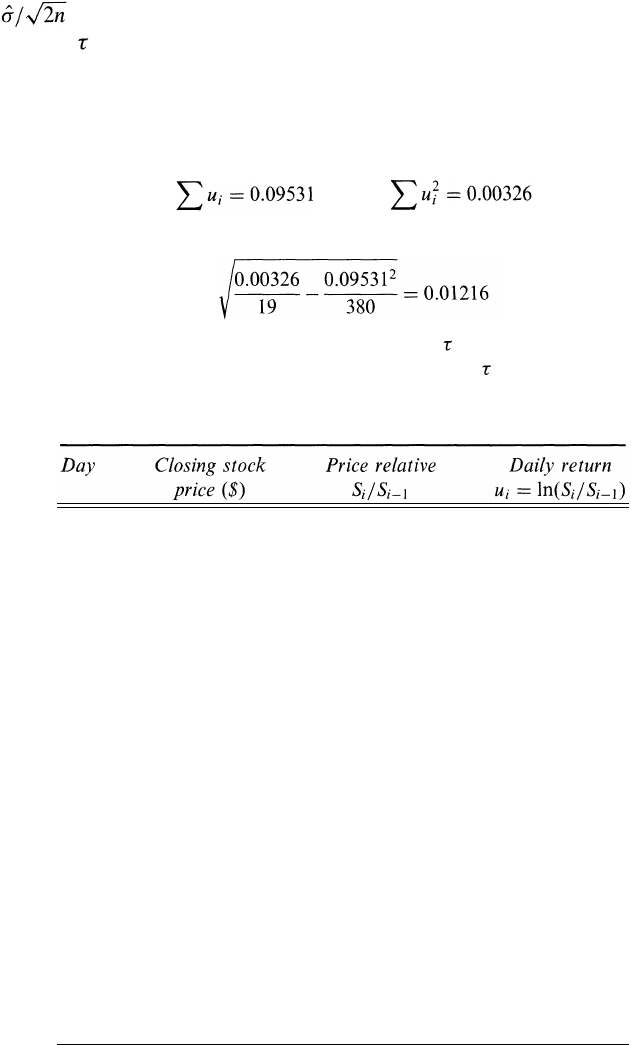

Define:

n + 1: Number of observations

S

i

: Value of variable at end of ith interval, where i = 0, 1,..., n

: Length of time interval

and let

for i = 1,2, ...,n.

The usual estimate s of the standard deviation of the u

i

is given by

where is the mean of the u

i

.

As explained in Section 5.1, the standard deviation of the u

i

is

where is the volatility of the variable. The variable s is, therefore, an

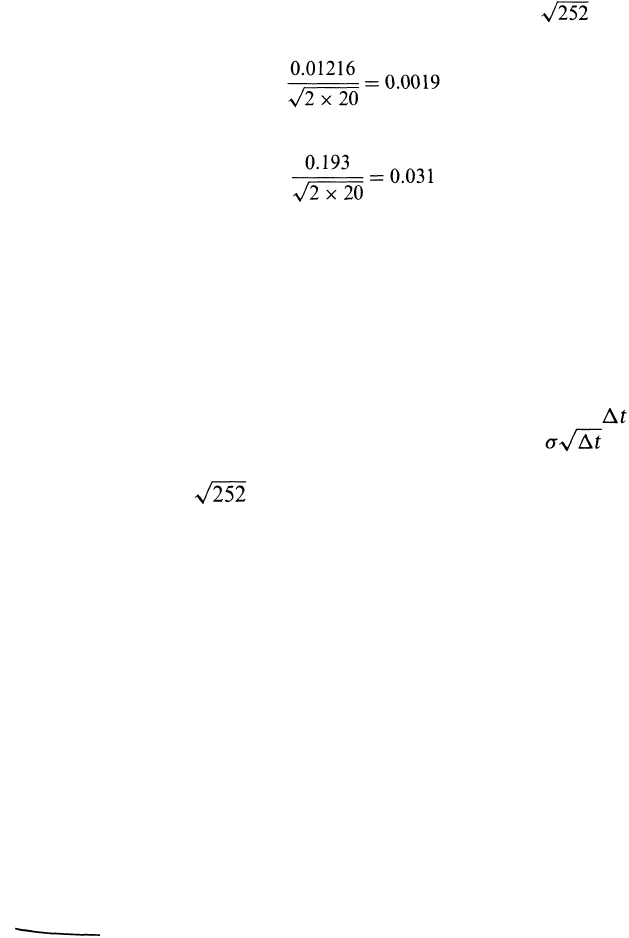

estimate of . It follows that itself can be estimated as , where

The standard error of this estimate can be shown to be approximately

or

116 Chapter 5

. If T is measured in years, the volatility calculated is a volatility per

year; if is measured in days, the volatility that is calculated is a daily

volatility.

Example 5.1

Table 5.1 shows a possible sequence of stock prices during 21 consecutive

trading days. In this case,

or 1.216%. To calculate a daily volatility, we set = 1 and obtain a volatility

of 1.216%. To calculate a volatility per year, we set = 1/252 and the data

Table 5.1 Computation of volatility.

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

20.00

20.10

19.90

20.00

20.50

20.25

20.90

20.90

20.90

20.75

20.75

21.00

21.10

20.90

20.90

21.25

21.40

21.40

21.25

21.75

22.00

1.00500

0.99005

1.00503

1.02500

0.98780

1.03210

1.00000

1.00000

0.99282

1.00000

1.01205

1.00476

0.99052

1.00000

1.01675

1.00706

1.00000

0.99299

1.02353

1.01149

0.00499

-0.01000

0.00501

0.02469

-0.01227

0.03159

0.00000

0.00000

-0.00720

0.00000

0.01198

0.00475

-0.00952

0.00000

0.01661

0.00703

0.00000

-0.00703

0.02326

0.01143

and the estimate of the standard deviation of the daily return is

and

Volatility

117

give an estimate for the volatility per annum of 0.01216 =0.193, or

19.3%. The standard error of the daily volatility estimate is

or 0.19% per day. The standard error of the volatility per year is

or 3.1% per annum.

5.4 ARE DAILY PERCENTAGE CHANGES IN

FINANCIAL VARIABLES NORMAL?

The Black-Scholes model and its extensions (see Appendix C) make the

assumption that asset prices change continuously and have constant

volatility. This means that the return in a short period of time always

has a normal distribution with a standard deviation of . Suppose

that the volatility of an exchange rate is estimated as 12% per year. This

corresponds to 12/ , or 0.756%, per day. Assuming normally dis-

tributed returns, we see from the tables at the end of this book that the

probability of the value of the foreign currency changing by more than

one standard deviation (i.e., by more than 0.756%) in one day is 31.73%;

the probability that the exchange rate will change by more than two

standard deviations (i.e., by more than 1.512%) is 4.55%; the probability

that it will change by more than three standard deviations (i.e., by more

than 2.268%) is 0.27%; and so on.

2

In practice, exchange rates, as well as most other market variables, tend

to have heavier tails than the normal distribution. Table 5.2 illustrates this

by examining the daily movements in 12 different exchange rates over a

ten-year period.

3

The first step in the production of this table is to

calculate the standard deviation of daily percentage changes in each

exchange rate. The next stage is to note how often the actual percentage

changes exceeded one standard deviation, two standard deviations, and

so on. These numbers are then compared with the corresponding num-

bers for the normal distribution.

2

We are making a small approximation here that the one-day continuously compounded

return is the same as the one-week return with daily compounding.

. This table is taken from J. C. Hull and A. White, "Value at Risk When Daily Changes

in Market Variables Are Not Normally Distributed." Journal of Derivatives, 5, No. 3

(Spring 1998): 9-19.

118

Chapter 5

Daily percentage changes exceed three standard deviations on 1.34% of

the days. The normal model for returns predicts that this should happen

on only 0.27% of days. Daily percentage changes exceed four, five, and

six standard deviations on 0.29%, 0.08%, and 0.03% of days, respec-

tively. The normal model predicts that we should hardly ever observe this

happening. The table, therefore, provides evidence to support the exis-

tence of heavy tails. Business Snapshot 5.2 shows how you could have

made money if you had done the analysis in Table 5.2 in 1985!

Table 5.2 Percentage of days when absolute size of daily

exchange rate moves is greater than 1, 2,..., 6 standard deviations.

(SD = standard deviation of daily percentage change.)

>1 SD

>2 SD

>3 SD

>4 SD

>5 SD

>6 SD

Real world

(%)

25.04

5.27

1.34

0.29

0.08

0.03

Normal model

(%)

31.73

4.55

0.27

0.01

0.00

0.00

Business Snapshot 5.2 Making Money from Foreign Currency Options

Suppose that most market participants think that exchange rates are log-

normally distributed. They will be comfortable using the same volatility to

value all options on a particular exchange rate. You have just done the

analysis in Table 5.2 and know that the lognormal assumption is not a good

one for exchange rates. What should you do?

The answer is that you should buy deep-out-of-the-money call and put

options on a variety of different currencies—and wait. These options will be

relatively inexpensive and more of them will close in the money than the

lognormal model predicts. The present value of your payoffs will on average

be much greater than the cost of the options.

In the mid-1980s a few traders knew about the heavy tails of foreign

exchange probability distributions. Everyone else thought that the lognormal

assumption of Black-Scholes was reasonable. The few traders who were well

informed followed the strategy we have described—and made lots of money.

By the late 1980s everyone realized that out-of-the money options should have

a higher implied volatility than at-the-money options and the trading oppor-

tunities disappeared.