McConnell Campbell R., Brue Stanley L., Barbiero Thomas P. Microeconomics. Ninth Edition

Подождите немного. Документ загружается.

300 Part Two • Microeconomics of Product Markets

may now constitute a significant

barrier to entry.

Blindfold taste tests confirm

that most mass-produced Cana-

dian beers taste alike, so, brew-

ers greatly emphasize advertis-

ing. Here, Labatt and Molson,

who sell national brands, enjoy

major cost advantages over pro-

ducers that have regional brands

(for example, Creemore Springs,

Upper Canada, and Okanagan

Spring). The reason is because

national television advertising is

less costly per viewer than local

spot TV advertising.

Mergers in the brewing in-

dustry have been a fundamental

cause of the rising concentra-

tion. Dominant firms have ex-

panded by heavily advertising

their main brands such as Labatt

Blue, Molson Canadian, Blue

Light, Canadian Light, and Mol-

son Special Dry, sustaining sig-

nificant product differentiation

despite the declining number of

major brewers.

Two factors dominate the

Canadian beer industry: high

transportation costs and provin-

cial policies and practices. High

transportation costs have trans-

lated into a regional structure of

production compared with the

brewing industry in the United

States. As a consequence, a large

number of breweries exist in

Canada relative to the size of the

domestic market. Especially out-

side the larger breweries in On-

tario and Quebec, unit costs are

markedly higher because of the

inability to achieve economies of

scale.

Even more important than

transportation costs, provincial

policies and practices in the past

had a dominant impact on the

Canadian brewing industry; until

recently, brewers were not al-

lowed to transport beer produced

in one province to be sold in an-

other. This restriction has now

been relaxed, and brewers will

centralize operations in the future

to capture economies of scale.

Imported beers such as Beck,

Corona, Foster’s, and Guinness

constitute over 10 percent of the

Canadian market, with individ-

ual brands seeming to wax and

wane in popularity. Some local

or regional microbreweries such

as Upper Canada (purchased re-

cently by Sleeman), which brew

specialty beers and charge pre-

mium prices, have whittled into

the sales of the major brewers.

Labatt and Molson have taken

notice, responding with spe-

cialty brands of their own (for

example, John Labatt Classic

and Molson Signature Spring

Bock). Overall, however, it ap-

pears that imports such as

Heineken and Budweiser may

pose more of a threat to the ma-

jors than the microbreweries do.

Sources: Based on Kenneth G.

Elzinga, “Beer,” in Walter Adams

and James Brock (eds.), The Struc-

ture of American Industry, 9th ed.

(Englewood Cliffs, NJ: Prentice-Hall,

1995), pp. 119–151; Douglas F. Greer,

“Beer: Causes of Structural Change,”

in Larry Duetsch (ed.), Industry

Studies, 2nd ed. (New York: M. E.

Sharpe, 1998), pp. 28–64; authors’

updates; the Conference Board of

Canada, The Canadian Brewing

Industry: Historical Evolution and

Competitive Structure (Toronto: Inter-

national Studies and Development

Group, 1989).

chapter summary

1. The distinguishing features of monopolistic

competition are (a) enough firms are in the

industry to ensure that each firm has only

limited control over price, mutual interde-

pendence is absent, and collusion is nearly

impossible; (b) products are characterized by

real or perceived differences so that eco-

nomic rivalry entails both price and nonprice

competition; and (c) entry to the industry is

relatively easy. Many aspects of retailing,

and some manufacturing industries in which

economies of scale are few, approximate

monopolistic competition.

2. Monopolistically competitive firms may earn

economic profits or incur losses in the short

run. The easy entry and exit of firms result in

only normal profits in the long run.

3. The long-run equilibrium position of the

monopolistically competitive producer is

less socially desirable than that of the pure

competitor. Under monopolistic competition,

chapter eleven • monopolistic competition and oligopoly 301

price exceeds marginal cost, suggesting an

underallocation of resources to the product,

and price exceeds minimum average total

cost, indicating that consumers do not get

the product at the lowest price that cost con-

ditions might allow.

4. Nonprice competition provides a means by

which monopolistically competitive firms

can offset the long-run tendency for eco-

nomic profit to fall to zero. Through product

differentiation, product development, and

advertising, a firm may strive to increase the

demand for its product more than enough to

cover the added cost of such nonprice com-

petition. Consumers benefit from the wide

diversity of product choice that monopolistic

competition provides.

5. In practice, the monopolistic competitor

seeks the specific combination of price, prod-

uct, and advertising that will maximize profit.

6. Oligopolistic industries are characterized by

the presence of few firms, each having a sig-

nificant fraction of the market. Firms thus

situated are mutually interdependent: the

behaviour of any one firm directly affects,

and is affected by, the actions of rivals. Prod-

ucts may be either virtually uniform or sig-

nificantly differentiated. Various barriers to

entry, including economies of scale, underlie

and maintain oligopoly.

7. Concentration ratios are a measure of oli-

gopoly (monopoly) power. By giving more

weight to larger firms, the Herfindahl index

is designed to measure market dominance in

an industry.

8. Game theory (a) shows the interdependence

of oligopolists’ pricing policies; (b) reveals

the tendency of oligopolists to collude; and

(c) explains the temptation of oligopolists to

cheat on collusive arrangements.

9. Noncollusive oligopolists may face a kinked-

demand curve. This curve and the accompa-

nying marginal-revenue curve help explain

the price rigidity that often characterizes

oligopolies; they do not, however, explain

how the actual prices of products are first

established.

10. The uncertainties inherent in oligopoly pro-

mote collusion. Collusive oligopolists such

as cartels maximize joint profits—that is,

they behave like pure monopolists. Demand

and cost differences, a large number of

firms, cheating through secret price conces-

sions, recessions, and the anti-combines

laws are all obstacles to collusive oligopoly.

11. Price leadership is an informal means of col-

lusion whereby one firm, usually the largest

or most efficient, initiates price changes and

the other firms in the industry follow the

leader.

12. Market shares in oligopolistic industries are

usually determined based on product de-

velopment and advertising. Oligopolists

emphasize nonprice competition because

(a) advertising and product variations are

harder for rivals to match and (b) oligopo-

lists frequently have ample resources to

finance nonprice competition.

13. Advertising may affect prices, competition,

and efficiency either positively or negatively.

Positive: It can provide consumers with low-

cost information about competing products,

help introduce new competing products

into concentrated industries, and generally

reduce monopoly power and its attendant

inefficiencies. Negative: It can promote

monopoly power via persuasion and the cre-

ation of entry barriers. Moreover, it can be

self-cancelling when engaged in by rivals

by boosting costs and increasing economic

inefficiency while accomplishing little else.

14. Neither productive nor allocative efficiency

is realized in oligopolistic markets, but oli-

gopoly may be superior to pure competition

in promoting research and development and

technological progress.

terms and concepts

monopolistic competition,

p. 274

product differentiation, p. 274

nonprice competition, p. 276

excess capacity, p. 281

oligopoly, p. 282

homogeneous oligopoly, p. 283

differentiated oligopoly, p. 283

mutual interdependence, p. 283

concentration ratio, p. 284

interindustry competition,

p. 285

import competition, p. 285

Herfindahl index, p. 285

game theory model, p. 286

collusion, p. 287

kinked-demand curve, p. 288

price war, p. 291

cartel, p. 292

tacit understandings, p. 293

price leadership, p. 295

302 Part Two • Microeconomics of Product Markets

study questions

1. How does monopolistic competition differ

from pure competition in its basic character-

istics? from pure monopoly? Explain fully

what product differentiation may involve.

Explain how the entry of firms into its in-

dustry affects the demand curve facing a

monopolistic competitor and how that, in

turn, affects its economic profit.

2.

KEY QUESTION Compare the elastic-

ity of the monopolistic competitor’s demand

with that of a pure competitor and a pure

monopolist. Assuming identical long-run

costs, compare graphically the prices and out-

puts that would result in the long run under

pure competition and under monopolistic

competition. Contrast the two market struc-

tures in terms of productive and allocative

efficiency. Explain: “Monopolistically compet-

itive industries are characterized by too many

firms, each of which produces too little.”

3. “Monopolistic competition is monopolistic

up to the point at which consumers become

willing to buy close-substitute products and

competitive beyond that point.” Explain.

4. “Competition in quality and service may be

just as effective as price competition in giv-

ing buyers more for their money.” Do you

agree? Why? Explain why monopolistically

competitive firms frequently prefer nonprice

competition to price competition.

5. Critically evaluate and explain:

a. “In monopolistically competitive indus-

tries, economic profits are competed

away in the long run; hence, there is no

valid reason to criticize the performance

and efficiency of such industries.”

b. “In the long run, monopolistic competi-

tion leads to a monopolistic price but not

to monopolistic profits.”

6. Why do oligopolies exist? List five or six oli-

gopolists whose products you own or regu-

larly purchase. What distinguishes oligopoly

from monopolistic competition?

7.

KEY QUESTION Answer the follow-

ing questions, which relate to measures of

concentration:

a. What is the meaning of a four-firm con-

centration ratio of 60 percent? 90 percent?

What are the shortcomings of concen-

tration ratios as measures of monopoly

power?

b. Suppose that the five firms in industry A

have annual sales of 30, 30, 20, 10, and 10

percent of total industry sales. For the

five firms in industry B the figures are

60, 25, 5, 5, and 5 percent. Calculate the

Herfindahl index for each industry and

compare their likely competitiveness.

8.

KEY QUESTION Explain the general

meaning of the following payoff matrix for

oligopolists C and D. All profit figures are in

thousands.

a. Use the payoff matrix to explain the

mutual interdependence that character-

izes oligopolistic industries.

b. Assuming no collusion between C and D,

what is the likely pricing outcome?

c. In view of your answer to 8b, explain why

price collusion is mutually profitable.

Why might a temptation to cheat on the

collusive agreement exist?

9.

KEY QUESTION What assumptions

about a rival’s response to price changes

underlie the kinked-demand curve for oli-

gopolists? Why is there a gap in the oligop-

olist’s marginal-revenue curve? How does

the kinked-demand curve explain price rigid-

ity in oligopoly? What are the shortcomings

of the kinked-demand model?

10. Why might price collusion occur in oligopo-

listic industries? Assess the economic desir-

ability of collusive pricing. What are the

main obstacles to collusion? Discuss the

weakening of OPEC in the 1980s in terms of

those obstacles.

11.

KEY QUESTION Why is there so

much advertising in monopolistic competi-

tion and oligopoly? How does such advertis-

ing help consumers and promote efficiency?

Why might it be excessive at times?

High

$60

Low

$57

$55

$59

$69

$50

$58

$55

High Low

C's possible prices

D's possible prices

chapter eleven • monopolistic competition and oligopoly 303

internet application questions

1. Indigo at <www.indigo.ca> is Canada’s

largest online bookseller, but it still has to

compete with the very popular Amazon at

<www.amazon.com>. Search both sites for

Viktor Frankl’s Man’s Search for Meaning (in

paperback). Find the price and determine

which company sells the book at a lower

price (convert Amazon’s price into Canadian

dollars using the current exchange rate at

Yahoo’s financial site, <finance.yahoo.com/

m3?u>. Identify the nonprice competition

that might lead you to order from one com-

pany rather than the other.

2. Advertising Age at <adageglobal.com/cgi-bin/

pages.pl?link=428> compiles statistics on

the large advertisers and advertisements

categories. Go to Ad Age Data Base to find

information on Canadian advertising. Which

ad category has the largest spending? What

is the biggest circulation magazine? How

much does an entire black and white page

advertisement cost in that magazine?

12. (Advanced analysis) Construct a game the-

ory matrix involving two firms and their

decisions on high versus low advertising

budgets and the effects of each on profits.

Show a circumstance in which both firms

select high advertising budgets even though

both would be more profitable with low

advertising budgets. Why won’t they unilat-

erally cut their advertising budget?

13. (The Last Word) What firm(s) dominate the

beer industry? What demand and supply fac-

tors have contributed to the small number of

firms in this industry?

IN THIS CHAPTER

IN THIS CHAPTER

Y

Y

OU WILL LEARN:

OU WILL LEARN:

To distinguish among an

invention, an innovation,

and technological diffusion.

•

About the role of entrepreneurs

and other innovators.

•

A firm’s optimal amount of R&D.

•

About the role of market

structure on technological change.

•

How technological advance

enhances both productive

and allocative efficiency.

•

About consumer surplus

and producer surplus.

Technology,

R&D, and

Efficiency

J

ust do it! In 1968 two entrepreneurs

in Oregon developed a lightweight

sport shoe and formed a new company

called Nike, incorporating a “swoosh” logo

(designed by a graduate student for $35).

Today, Nike employs more than 20,000 work-

ers and sells more than U.S.$9 billion worth

of athletic shoes, hiking boots, and sports

apparel annually.

“Intel inside.” Intel? In 1967 neither this

company nor its product existed. Today, it is

the world’s largest producer of microproces-

sors for personal computers, with 67,500

employees and more than U.S.$29 billion in

annual sales.

TWELVE

Nortel Networks, headquartered in Brampton, Ontario, has become the largest

optical fibre manufacturer in the world. Optical fibres allow much faster transmis-

sion of electronic data, which increases the speed of Internet connections.

In 1996 Palm introduced its Palm Pilot, a palm-sized personal computer that now

also has wireless Internet capabilities. A novel idea? Apparently, so: Microsoft, Hand-

spring, OmniSky, and others have followed with similar products, and cell phone

makers are incorporating Internet functionality into some of their new phones.

Each of these brief descriptions entails some elements of technological advance,

broadly defined as new and better goods and services and new and better ways of

producing or distributing them. In this chapter, we want to look at some of the

microeconomics of technological advance. Who motivates and implements techno-

logical advance? What determines a firm’s optimal amount of research and devel-

opment (R&D)? What is the extent and implications of the imitation problem that

innovators face? Are certain market structures more conducive to technological

advance than others? How does technological advance relate to efficiency? These

are some of the questions we address in this chapter. We also take another look at

allocative and productive efficiency and investigate another way to measure them.

For economists, technological advance occurs over a theoretical time period called

the very long run, which can be as short as a few months or as long as many years.

Recall that in our four market models (pure competition, monopolistic competition,

oligopoly, and pure monopoly), the short run is a period in which technology, plant,

and equipment are fixed; in the long run, technology is constant but firms can

change their plant sizes and are free to enter or exit industries. In contrast, the very

long run is a period in which technology can change and in which firms can develop

and offer entirely new products.

In Chapter 2 we saw that technological advance shifts an economy’s produc-

tion possibilities curve outward, enabling the economy to obtain more goods and

services. Technological advance is a three-step process of invention, innovation, and

diffusion.

Invention

The basis of technological advance is invention: the discovery of a product or process

through the use of imagination, ingenious thinking, and experimentation and the first proof

that it will work. Invention is a process, and the result of the process is also called an

invention. The prototypes (basic working models) of the telephone, the automobile,

and the microchip are inventions. Invention usually is based on scientific knowl-

edge and is the product of individuals, either working on their own or as members

of corporate R&D staffs. Later on you will see how governments encourage inven-

tion by providing the inventor with a patent, an exclusive right to sell any new and

useful process, machine, or product for a set time.

Innovation

Innovation draws directly on invention. While invention is the “discovery and first

proof of workability,” innovation is the first successful commercial introduction

of a new product, the first use of a new method, or the creation of a new form of

chapter twelve • technology, r&d, and efficiency 305

techno-

logical

advance

New

and better goods

and services and

new and better

ways of producing

or distributing them.

very long

run

A period in

which technology

can change and

in which firms

can develop and

offer entirely new

products.

invention

The discovery of a

product or process

through the use of

imagination, ingen-

ious thinking, and

experimentation

and the first proof

that it will work.

patent An

exclusive right to

sell any new and

useful process,

machine, or product

for a set time.

innovation

The first successful

commercial intro-

duction of a new

product, the first use

of a new method of

production, or the

creation of a new

form of business

organization.

Technological Advance: Invention,

Innovation, and Diffusion

business organization. Innovation is of two types: product innovation, which refers

to new and improved products or services; and process innovation, which refers to

new and improved methods of production or distribution.

Unlike inventions, innovations cannot be patented. Nevertheless, innovation is a

major factor in competition, since it sometimes enables a firm to leapfrog competi-

tors by rendering their products or processes obsolete. For example, personal com-

puters coupled with software for word processing pushed some major typewriter

manufacturers into obscurity. More recently, innovations in hardware retailing

(large warehouse stores such as Home Depot) have threatened the existence of

smaller, more traditional hardware stores.

Innovation need not weaken or destroy existing firms. Aware that new products

and processes may threaten their survival, existing firms have a powerful incentive

to engage continually in R&D of their own. Innovative products and processes often

enable such firms to maintain or increase their profits. The introduction of alu-

minum cans by Reynolds, disposable contact lenses by Johnson & Johnson, and sci-

entific calculators by Hewlett-Packard are good examples. Thus, innovation can

either diminish or strengthen market power.

Diffusion

Diffusion is the spread of an innovation through imitation or copying. To take

advantage of new profit opportunities or to slow the erosion of profit, both new and

existing firms emulate the successful innovations of others. Years ago McDonald’s

successfully introduced the fast-food hamburger; Burger King, Swiss Chalet, and

other firms soon copied that idea. Hertz greatly increased its auto rentals by offer-

ing customers unlimited mileage, and Avis, Budget, and others eventually fol-

lowed. DaimlerChrysler profitably introduced a luxury version of its Jeep Grand

Cherokee; other manufacturers, including Acura, Mercedes, and Lexus, countered

with luxury sport-utility vehicles of their own. In each of these cases, innovation has

led eventually to widespread imitation—that is, to diffusion.

R&D Expenditures

As related to businesses, the term “research and development” is used loosely to

include direct efforts toward invention, innovation, and diffusion. However, gov-

ernment also engages in R&D, particularly R&D having to do national defence. In

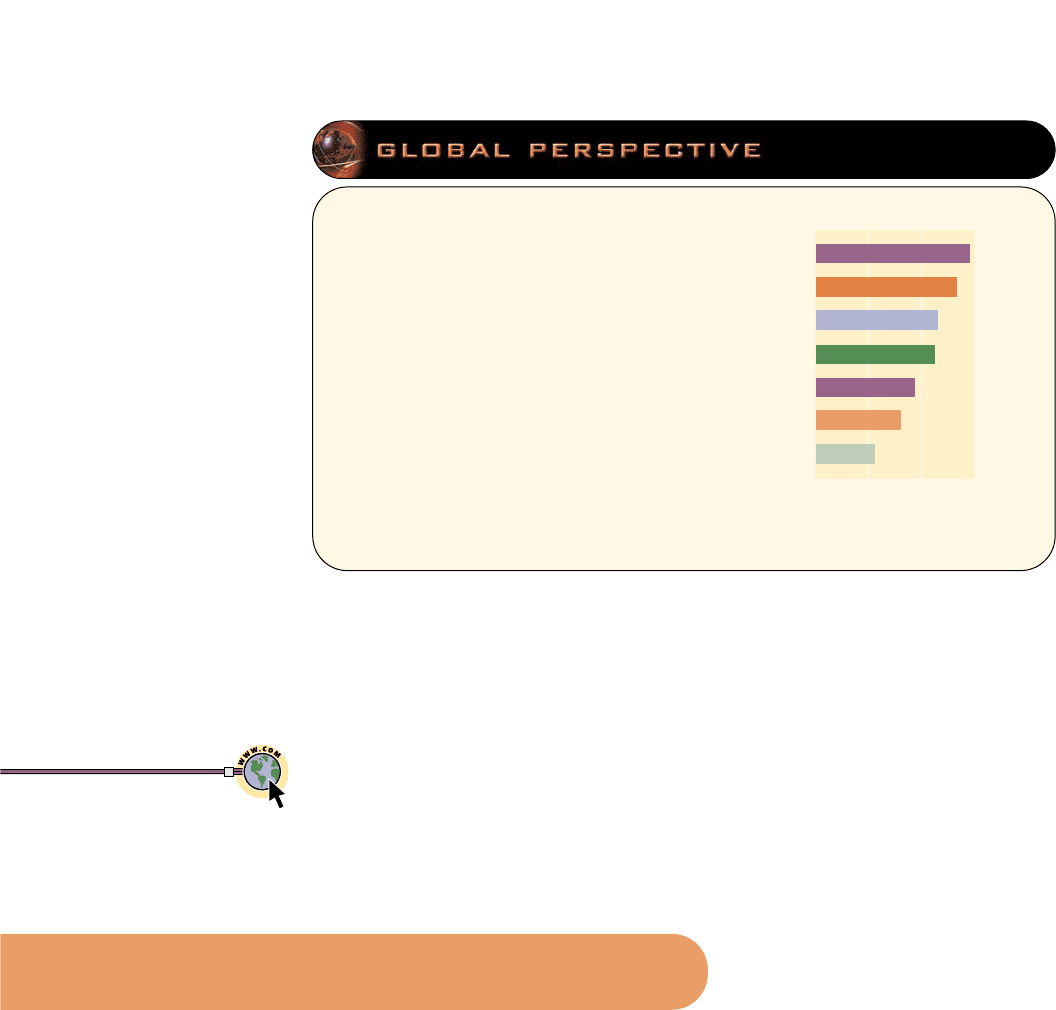

1999 total Canadian R&D expenditures (business plus government) were $12 billion.

Relative to GDP, that amount was 1.6 percent, which is a reasonable measure of the

emphasis the Canadian economy puts on technological advance. As shown in

Global Perspective 12.1, this is a relatively low percentage of GDP compared to sev-

eral other nations.

Modern View of Technological Advance

For decades most economists regarded technological advance as being external to

the economy—a random outside force to which the economy adjusted. Periodically

fortuitous advances in scientific and technological knowledge occurred, paving the

way for major new products (automobiles, airplanes) and new production processes

(assembly lines). Firms and industries, each at its own pace, then incorporated the

new technology into their products or processes to enhance or maintain their profit.

Then after making the appropriate adjustments, they settled back into new long-run

equilibrium positions. Although technological advance has been vitally important

306 Part Two • Microeconomics of Product Markets

product

innovation

The development

and sale of a new or

improved product

or service.

process

innovation

The development

and use of new or

improved produc-

tion or distribution

methods.

diffusion

The widespread

imitation of an

innovation.

to the economy, economists believed it was rooted in the independent advance of

science, which is largely external to the market system.

Most contemporary economists have a different view. They see capitalism itself

as the driving force of technological advance. In their view, invention, innovation,

and diffusion occur in response to incentives within the economy, meaning that

technological advance is internal to capitalism. Specifically, technological advance

arises from intense rivalry among individuals and firms that motivates them to seek

and exploit new profit opportunities or to expand existing opportunities. That

rivalry occurs both among existing firms and between existing firms and new firms.

Moreover, many advances in pure scientific knowledge are motivated, at least in

part, by the prospect of commercial applicability and eventual profit. In the modern

view, entrepreneurs and other innovators are at the heart of technological advance.

It will be helpful to distinguish between entrepreneurs and other innovators:

● Entrepreneurs Recall that the entrepreneur is an initiator, innovator, and risk

bearer—the catalyst who combines land, labour, and capital resources in new

and unique ways to produce new goods and services. In the past a single indi-

vidual, for example, Hart Massey in farm machinery, Henry Ford in automo-

biles, and Levi Strauss in blue jeans, carried out the entrepreneurial role. Such

advances as air conditioning, the ballpoint pen, cellophane, the jet engine,

insulin, xerography, and the helicopter all have an individualistic heritage. But

in today’s more technologically complex economy, entrepreneurship is just as

likely to be carried out by entrepreneurial teams. Such teams may include only

two or three people working as their own bosses on some new product or idea,

or it may consist of larger groups of entrepreneurs who have pooled their

financial resources.

chapter twelve • technology, r&d, and efficiency 307

Total R&D expenditures

as a percentage of GDP,

selected nations 1999

Relative R&D spending varies

among the seven leading

industrial nations. From a

microeconomic perspective,

R&D helps promote economic

efficiency; from a macroeco-

nomic perspective, R&D helps

promote economic growth.

12.1

0123

Japan

United States

Canada

Germany

France

United Kingdom

Italy

Source: National Science Foundation, <www.nsf.gov>.

<www.interlog.com/

~womenip/>

Women inventors

project

Role of Entrepreneurs and

Other Innovators

● Other innovators This designation includes other key people involved in the

pursuit of innovation who do not bear personal financial risk. Among them are

key executives, scientists, and other salaried employees engaged in commer-

cial R&D activities. (They are sometimes referred to as intrapreneurs, since they

provide the spirit of entrepreneurship within existing firms.)

Forming Start-Ups

Entrepreneurs often form small new companies called start-ups that focus on cre-

ating and introducing a new product or employing a new production or distribu-

tion technique. Two people, working out of their garages, formed such a start-up in

the mid-1970s. Since neither of their employers—Hewlett-Packard and Atari, the

developer of Pong (the first video game)—was interested in their prototype per-

sonal computer, they founded their own company: Apple Computers. Other exam-

ples of successful start-ups are Amgen, a biotechnology firm specializing in new

medical treatments; Second Cup, a seller of gourmet coffee; and Corel, which devel-

ops innovative graphics software.

Innovating within Existing Firms

Innovators are also at work within existing corporations, large and small. Such inno-

vators are salaried workers, though many firms have pay systems that provide them

with substantial bonuses or shares of the profit. Examples of firms known for their

skillful internal innovators are the 3M Corporation, the U.S. developer of Scotch

tape, Post-it Notes, and Thinsulate insulation; and Canon, the Japanese developer

of the laser engine for personal copiers and printers. R&D work in major corpora-

tions has produced significant technological improvements in such products as tel-

evision sets, telephones, home appliances, automobiles, automobile tires, and

sporting equipment.

Some large firms, aware that excessive bureaucracy can stifle creative thinking and

technological advance, have split part of their R&D and manufacturing divisions to

form new, more flexible, innovative firms. One significant example of such a spinoff

firm is Nortel, a telephone equipment and R&D firm created by Bell Canada.

Anticipating the Future

Some 50 years ago a writer for Popular Mechanics magazine boldly predicted, “Com-

puters in the future may weigh no more than 1.5 tons.” Today’s notebook comput-

ers weigh less than two kilograms. It is difficult to anticipate the future, but that is

what innovators try to do. Those with strong anticipatory ability and determination

have a knack for introducing new and improved products or services at just the

right time. The rewards are both monetary and nonmonetary. Product innovation

and development are creative endeavours, with such intangible rewards as personal

satisfaction. Also, many people simply enjoy participating in the competitive con-

test. Of course, the winners can reap huge monetary rewards in the form of eco-

nomic profits, stock appreciation, or large bonuses. Extreme examples are Bill Gates

and Paul Allen, who founded Microsoft in 1975 and had a net worth in 2000 of U.S.$85

billion and U.S.$40 billion, respectively, mainly in the form of Microsoft stock.

Past successes often give entrepreneurs and innovative firms access to resources

for further innovations that anticipate consumer wants. Although they may not suc-

ceed a second time, the market tends to entrust the production of goods and serv-

308 Part Two • Microeconomics of Product Markets

start-ups

Small new com-

panies that focus

on creating and

introducing a new

product or employ-

ing a new produc-

tion or distribution

technique.

ices to businesses that have consistently succeeded in filling consumer wants. And

the market does not care whether these winning entrepreneurs and innovative firms

are Canadian, American, Brazilian, Japanese, German, or Swiss. Entrepreneurship

and innovation are global in scope.

Exploiting University and Government Scientific Research

Only a small percentage of R&D spending goes to basic scientific research. The rea-

son that percentage is so small is that scientific principles, as such, cannot be

patented, nor do they usually have immediate commercial uses. Yet new scientific

knowledge is highly important to technological advance. For that reason, entrepre-

neurs study the scientific output of university and government laboratories to iden-

tify discoveries with commercial applicability.

Government and university labs have been the scene of many technological

breakthroughs. Entire high-tech industries such as computers and biotechnology,

for example, have their roots in major research universities and government labo-

ratories, and nations with strong scientific communities tend to have the most tech-

nologically progressive firms and industries.

Also, firms increasingly help to fund university research that relates to their prod-

ucts. Business funding of R&D at universities has grown rapidly. Today, the sepa-

ration between university scientists and innovators is narrowing; scientists and

universities increasingly realize that their work may have commercial value and are

teaming up with innovators to share in the potential profit. A few firms, of course,

find it profitable to conduct basic scientific research on their own. New scientific

knowledge can give them a head start in creating an invention or a new product.

This is particularly true in the pharmaceutical industry, where it is not uncommon

for firms to parlay new scientific knowledge generated in their corporate labs into

new, patentable drugs.

How does a firm decide on its optimal amount of research and development? That

amount depends on the firm’s perception of the marginal benefit and marginal cost

of R&D activity. The decision rule here flows from basic economics: To earn the

greatest profit, expand a particular activity until its marginal benefit (MB) equals

its marginal cost (MC). A firm that sees the marginal benefit of a particular R&D

chapter twelve • technology, r&d, and efficiency 309

A Firm’s Optimal Amount of R&D

● Broadly defined, technological advance means

new or improved products and services and

new or improved production and distribution

processes.

● Invention is the discovery of a new product or

method; innovation is the successful commer-

cial application of some invention; and diffusion

is the widespread imitation of the innovation.

● Many economists view technological advance

as mainly a response to profit opportunities

arising within a capitalist economy.

● Technological advance is fostered by entrepre-

neurs and other innovators and is supported

by the scientific research of universities and

government-sponsored laboratories.