Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 9 Relationships between investments: portfolio theory 225

When the covariance is zero, the third term is zero, and portfolio risk reduces to:

With zero covariance, portfolio risk is thus smaller for any portfolio compared to

cases where the covariance is positive. Even better, when the covariance is negative,

the third term becomes negative and risk falls even further. In general, the lowest

achievable portfolio risk declines as the covariance diminishes: if it is negative, all the

better. There is, however, no limit on the covariance value. If we re-express portfolio

risk in terms of the correlation coefficient, we can be more specific about the greatest

achievable degree of risk reduction. The formula relating covariance and correlation

coefficient (Equation 9.3) can be rewritten as:

Substituting into the expression for portfolio risk (Equation 9.2), we derive:

Clearly, when the correlation coefficient is negative, risk is reduced, but since the

limit to negative correlation is minus one, this places a lower limit on As we saw

in the Apple and Pear example, this may fall to zero if the portfolio is appropriately

weighted. Whether one works in terms of the covariance or the correlation coefficient

is generally a matter of preference, but, sometimes, it is dictated by the information

available.

■ The optimal portfolio

An obvious question to ask is: which is the best portfolio to hold? In this example, the

two investments have the same expected values, so any portfolio we construct by com-

bining them will also offer this expected value. The optimal portfolio is simply the one

that offers the lowest level of risk. Although very few decision-makers are outright risk

minimisers, any rational risk-averse manager will adopt the risk-minimising action

where every alternative offers an equal expected payoff.

The minimum risk portfolio with two assets

The expression for finding the weighting required to minimise the risk of a portfolio

comprising two assets, A and B, where proportion invested in asset A is:

(9.4)

Substituting the figures for the AB example into Equation 9.4, we find:

This formula tells us that, to minimise risk, we should place 64 per cent of our funds

in A and 36 per cent in B.

a

A

*

40

2

30

2

40

2

1,600

2,500

0.64

a

A

*

s

B

2

cov

AB

s

A

2

s

B

2

2 cov

AB

a

A

*

the

s

p

.

s

p

23a

2

s

A

2

11 a2

2

s

B

2

2a11 a2r

AB

s

A

s

B

4

cov

AB

1r

AB

s

A

s

B

2

s

p

23a

2

s

A

2

11 a2

2

s

B

2

4

In the next section, we analyse the more likely, and more interesting, case where

both the risks and expected returns of the two components differ.

Self-assessment activity 9.3

Verify that the standard deviation of this portfolio is 24%.

(Answer in Appendix A at the back of the book)

CFAI_C09.QXD 10/28/05 4:28 PM Page 225

.

226 Part III Investment risk and return

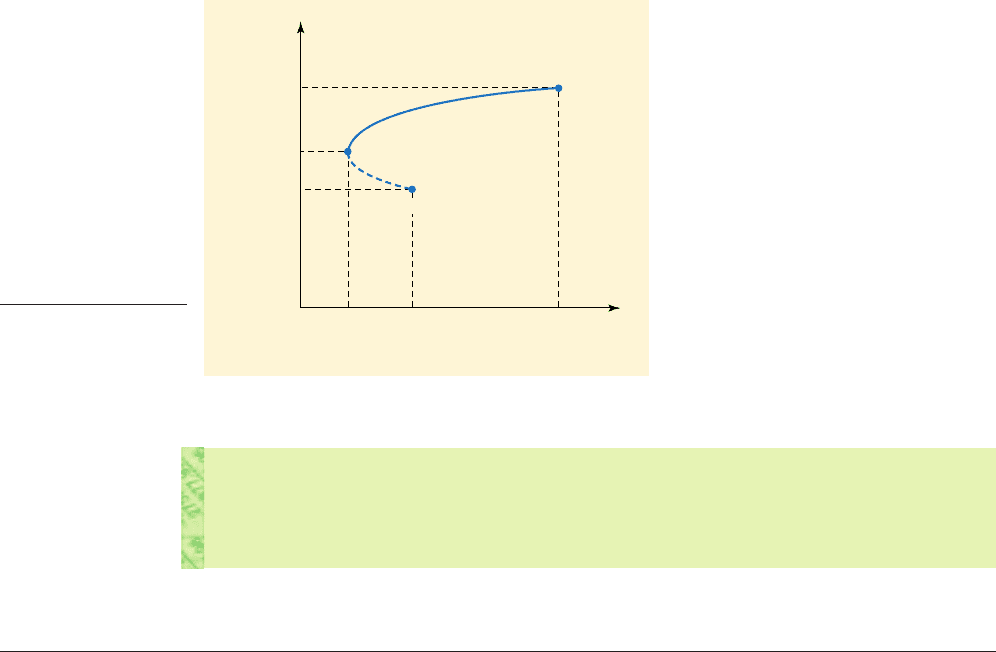

Suppose we are offered the two investments, Z and Y, whose characteristics are shown

in Table 9.3. Which should we undertake? Or should we undertake some combination?

To answer these questions, we need to consider the possible available combinations of

risk and return. Notice that correlation is negative.

Let us assume that the two assets can be combined in any proportions, i.e. the two

assets are perfectly divisible, as with security investments. There is an infinite number

of possible combinations of risk and return. However, for simplicity, we confine our

attention to the restricted range of portfolios whose risk and return characteristics are

shown in Table 9.4.

Not all combinations are of interest to the rational risk-averse manager. Comparing

segment AB with the segment BC, we find that combinations lying along the latter are

inefficient. For any combination along BC, we can achieve a higher return for the same

risk by moving to the combination vertically above it on AB. Point S is clearly superi-

or to T and, applying similar logic to the whole of BC, we are left with the segment AB

summarising all efficient portfolios, i.e. those that maximise return for a given risk. AB

is thus called the efficient frontier. Points along AB are said to dominate correspon-

ding points along BC.

Self-assessment activity 9.4

Verify that the portfolio at B, involving 75 per cent of Z and 25 per cent of Y, is the mini-

mum risk combination.

9.4 PORTFOLIO ANALYSIS WHERE RISK AND RETURN DIFFER

Table 9.3

Differing returns and

risks

Asset Expected return Standard deviation

Z 15% 20%

Y 35% 40%

Covariance

zy

10.252 1202 1402 200Correlation coefficient

ZY

0.25;

Table 9.4

Portfolio risk–return

combinations (%)

Z weighting Y weighting Expected return Standard deviation

100 0 15 20

75 25 20 16

50 50 25 20

25 75 30 29

0 100 35 40

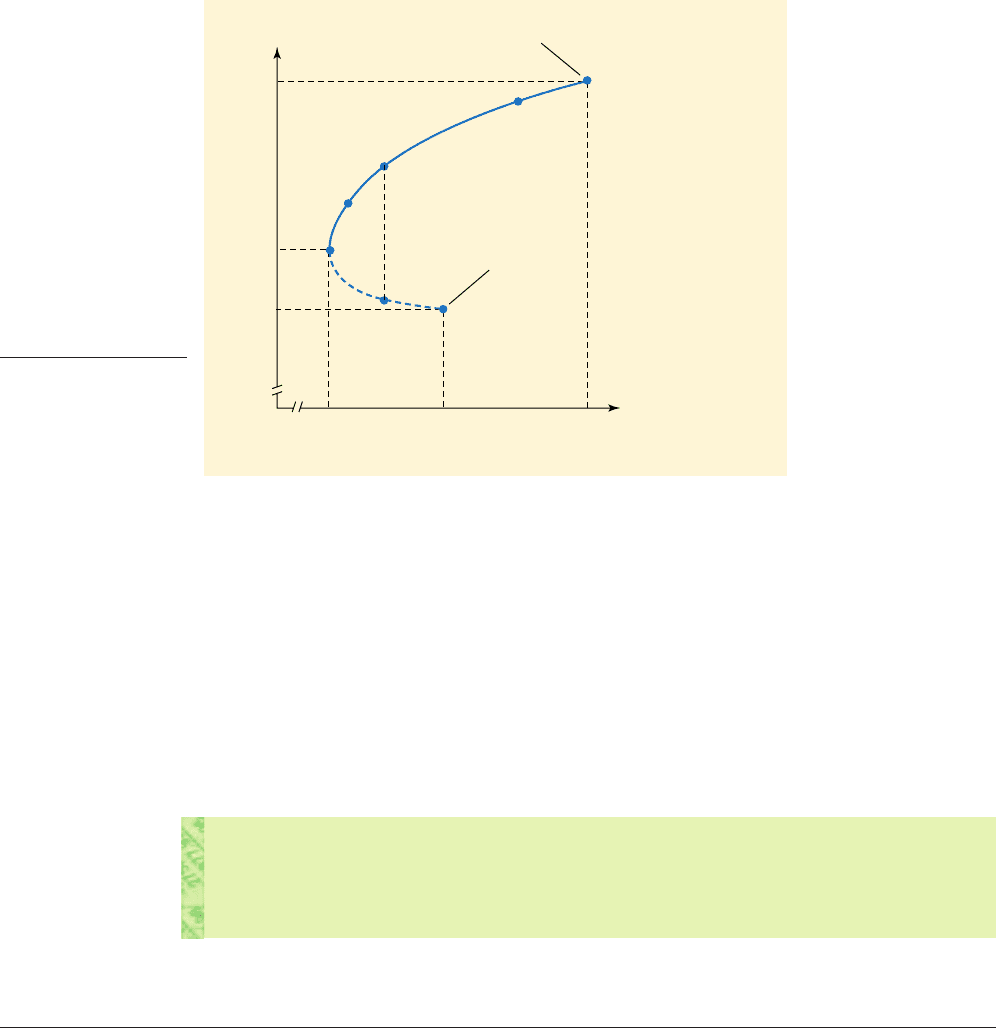

If we wanted to minimise risk, we would invest solely in asset Z, since this has the

lowest standard deviation. However, as we move from the all-Z portfolio to the com-

bination 75 per cent of Z plus 25 per cent of Y the risk of the whole portfolio dimin-

ishes and the expected return increases. Eventually, though, for portfolios more heavily

weighted towards Y, the effect of Y’s higher risk outweighs the beneficial effect of neg-

ative correlation, resulting in rising overall risk.

Figure 9.2 traces the range of available opportunities (or opportunity set), shaped

rather like the nose cone of an aircraft. The profile ranges from point A, representing

total investment in Y, through to point C, representing total investment in Z, having

described a U-turn at B.

opportunity set

The set of investment opportu-

nities (i.e. risk return combina-

tions) available to the investor

to select from

CFAI_C09.QXD 10/28/05 4:28 PM Page 226

.

Chapter 9 Relationships between investments: portfolio theory 227

35

16 20 40

C

all Z

all Y

T

B

P

S

Q

A

ER

p

s

p

AB = Efficient frontier

AC = Opportunity set

75% Z

25% Y

15

20

Figure 9.2

Available portfolio

risk–return combina-

tions when assets, risks

and expected returns

are different

However, we cannot specify an optimal portfolio, except for the outright risk-

minimiser, who would select the portfolio at B, and for the maximiser of expected

return, who would settle at point A (all Y). A risk-averse person might select any

portfolio along AB, depending on his or her degree of risk aversion: that is, what

additional return they would require to compensate for a specified increase in risk.

For example, a highly risk-averse person might locate at point P, while the less cau-

tious person might locate at point Q.

This is a crucial result. The most desirable combination of risky assets depends on the

decision-maker’s attitude towards risk. If we know the extent of their risk-aversion –

that is, how large a premium is required for a given increase in risk – we can specify the

best portfolio.

9.5 DIFFERENT DEGREES OF CORRELATION

Using arbitrary values for the correlation coefficient, we have found that negative cor-

relation offers a handsome portfolio effect, and, to a lesser degree, also zero correlation.

It is useful now to consider more carefully the general relationship between risk, corre-

lation and return. To do this, we look at the full range of possible degrees of correlation,

extending from perfect negative to perfect positive.

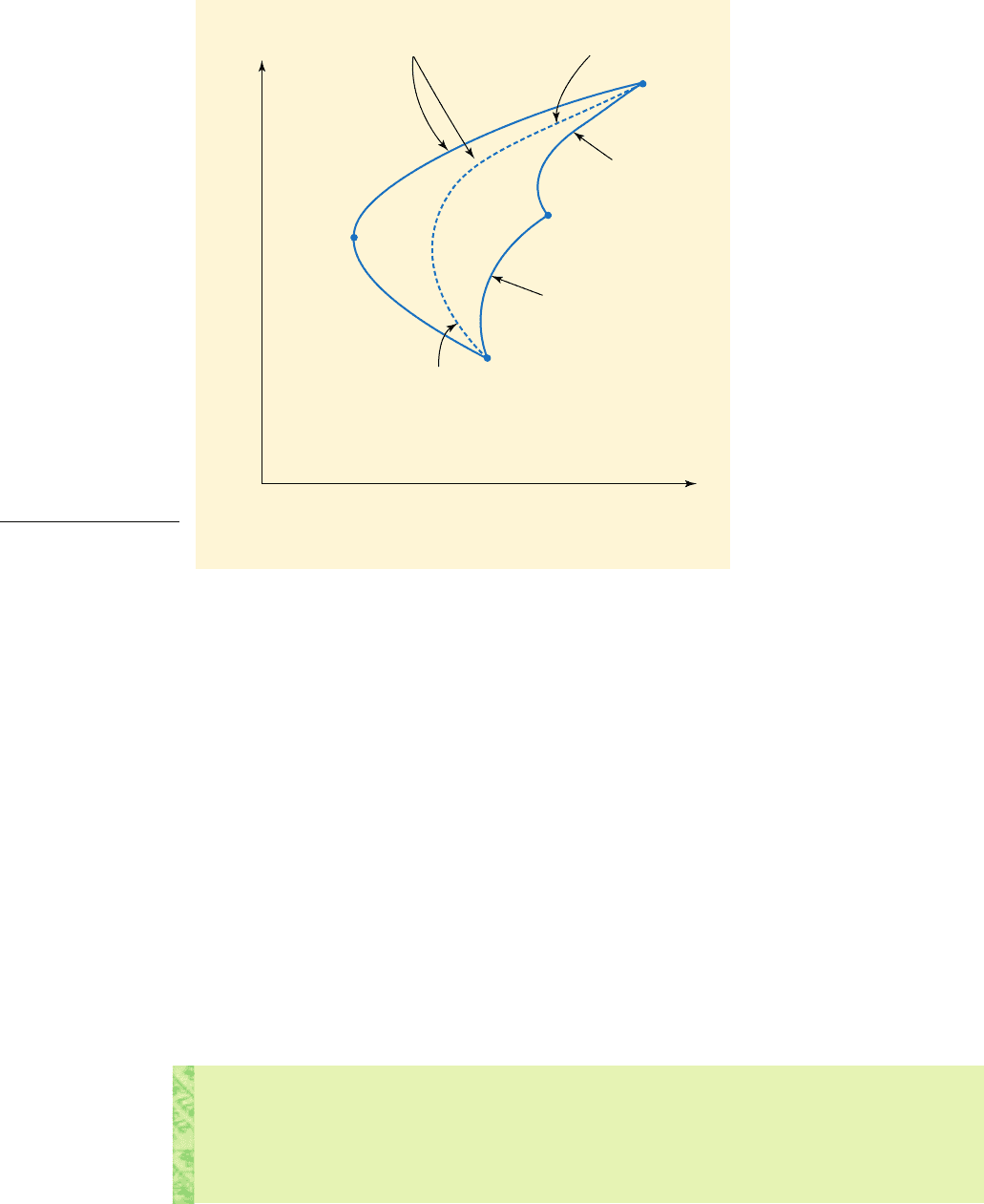

Say we are dealing with two investments, A and B, with Asset A offering the higher

expected return but also carrying greater risk. These are shown in Figure 9.3.

Consider the following degrees of correlation:

1 Perfect positive. In this case, it is not possible to achieve a portfolio effect at all.

Combinations of A and B locate along the straight line AB. To achieve lower risk

Self-assessment activity 9.5

What is meant by an efficient frontier in portfolio analysis?

(Answer in Appendix A at the back of the book)

optimal portfolio

The risk–return combination

that offers maximum satisfac-

tion to the investor, i.e. his/her

most-preferred risk-return

combination

CFAI_C09.QXD 10/28/05 4:28 PM Page 227

.

228 Part III Investment risk and return

A

B

Perfect negative

correlation

Adding B to A

The pull

of reducing

correlation

Too much B

X

0

Expected return on portfolio (ERP)

Perfect positive

correlation

Risk of portfolio

(Standard deviation,

s

p

)

Figure 9.3

The effect on the

efficiency frontier of

changing correlation

levels, we would simply invest more in asset B, while the risk-minimising ‘portfo-

lio’ is simply asset B alone.

2 Perfect negative. With the returns from the two assets moving in perfect opposition

to each other, it is possible to eliminate risk by adding B to A, but only by weight-

ing the portfolio correctly is it possible to fully exploit the beneficial effect of corre-

lation. Maximum risk-reduction is achieved at point X where the portfolio risk is

zero. Combinations along XB are clearly inefficient.

3 Intermediate values. For correlation coefficients between and it is still possi-

ble to generate a portfolio effect. The lower the correlation, i.e. the further away

from the greater the portfolio effect achievable. Two examples are shown in

Figure 9.3 as dotted lines between A and B. The characteristic ‘bow’ shapes result

from progressively lower correlation bending the profile from its original position

until we start observing the ‘nose cones’ identified earlier.

1,

1,1

9.6 WORKED EXAMPLE: GERRYBILD PLC

Gerrybild plc is a firm of speculative housebuilders that builds in advance of firm

orders from customers. It has a given amount of capital to purchase land and raw

materials and to pay labour for development purposes. It is considering two design

types – a small two-bedroomed terraced town house and a large four-bedroomed

‘executive’ residence. The project could last a number of years and its success depends

largely on general economic conditions, which will influence the demand for new

houses. Some information is available on past sales patterns of similar properties in

CFAI_C09.QXD 10/28/05 4:28 PM Page 228

.

Chapter 9 Relationships between investments: portfolio theory 229

Table 9.5

Returns from Gerrybild

Estimated NPV £ per:

State of the economy Probability Large house Small house

0.2 2,000 2,000

0.3 2,000 3,000

0.4 4,000 2,000

0.1 4,000 3,000

E

4

E

3

E

2

E

1

roughly similar locations – the demand is relatively higher for larger properties in

buoyant economic conditions and for smaller properties in relatively depressed states

of the economy. Since there appears to be a degree of inverse correlation between

demand, and, therefore, net cash flows, from the two products, it seems sensible to

consider diversified development. Table 9.5 shows annual net present value estimates

for various economic conditions.

To analyse this decision problem, we need, first, to calculate the risk–return param-

eters of the investment, and, second, to assess the degree of correlation. This informa-

tion may be obtained by performing a number of statistical operations:

1 Calculation of expected values. A shortcut is available, since some outcomes may occur

under more than one state of the economy. Grouping data where possible:

2 Calculation of project risks. We now apply the usual expression for the standard devi-

ation. The calculations for each activity are shown in Table 9.6. Clearly, the relative

money-spinner, the large house project, is also the more risky activity.

3 Calculation of co-variability. Table 9.7 presents the calculation of the covariance in tab-

ular form, following the steps itemised in Section 9.3.

£2,400

EV

S

Expected value of a small house 10.6 £2,0002 10.4 £3,0002

£3,000

EV

L

Expected value of a large house 10.5 £2,0002 10.5 £4,0002

Table 9.6

Calculation of standard

deviations of returns

from each investment

Deviation Squared Weighted squared

Outcome (£) Probability EV (£) (£) deviation (£) deviation (£)

Large houses

2,000 0.5 3,000 1,000,000 500,000

4,000 0.5 3,000 1,000,000 500,000

Small houses

2,000 0.6 2,400 160,000 96,000

3,000 0.4 2,400 360,000 144,000

489

hence s

S

2240,000

s

S

2

Variance 240,000

600

400

1,000

hence s

L

21,000,000

s

L

2

Variance 1,000,000

1,000

1,000

CFAI_C09.QXD 10/28/05 4:28 PM Page 229

.

230 Part III Investment risk and return

Table 9.7

Calculation of the

covariance

Outcomes (£) Weighted

Probability (£) (£) Product (£) product (£)

2,000 2,000 0.2

2,000 3,000 0.3

4,000 2,000 0.4

4,000 3,000 0.1

cov

LS

200,000

60,000

600,0006001,000

160,000400,0004001,000

180,000600,0006001,000

80,000400,0004001,000

1EV

S

R

S

21EV

L

R

L

2R

S

R

L

The covariance of suggests a strong element of inverse association. This

is confirmed by the value of the correlation coefficient:

There are clearly significant portfolio benefits to exploit. To offer concrete advice to

the builder, we would require information on his risk–return preferences, but we can

still specify the available set of portfolio combinations. Rather than compute the full

set of opportunities, we will identify the minimum risk portfolio, to enable construc-

tion of the overall risk–return profile.

■ The minimum risk portfolio

Using Equation (9.4), and defining as the proportion of the portfolio (i.e. proportion

of the available capital) devoted to large houses to minimise risk, we have:

If Gerrybild wanted to minimise risk, it would have to invest 27 per cent of its cap-

ital in developing large houses and 73 per cent in developing small houses.

440,000

1,640,000

0.27

a

L

*

1s

S

2

cov

LS

2

1s

S

2

s

L

2

2 cov

LS

2

240,000 200,000

240,000 1,000,000 400,000

a

L

*

r

LS

cov

LS

s

L

s

S

200,000

11,000214892

0.41

£200,000

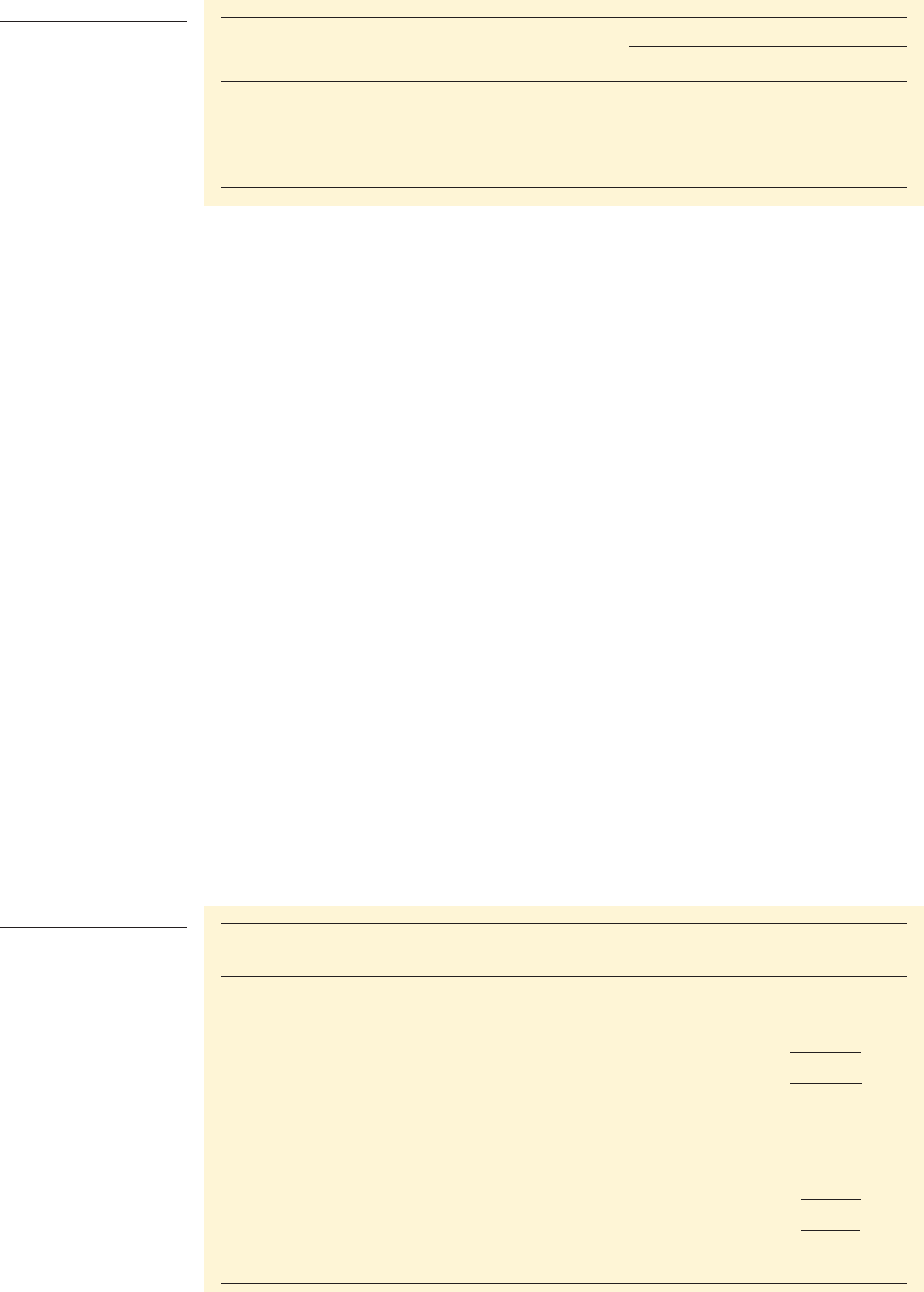

■ The opportunity set

We now have assembled sufficient information to display the full range of opportuni-

ties available to Gerrybild. The opportunity set ABC is shown on Figure 9.4 as the famil-

iar nose cone shape. If Gerrybild risk-averts, only segment AB is of interest, but

precisely where along this segment it will choose to locate depends the attitude towards

risk of its decision-makers.

Self-assessment activity 9.6

Verify that the lowest achievable portfolio standard deviation is £349 and the expected

NPV per house built from the minimum risk portfolio is £2,562.

(Answer in Appendix A at the back of the book)

CFAI_C09.QXD 10/28/05 4:28 PM Page 230

.

Chapter 9 Relationships between investments: portfolio theory 231

Self-assessment activity 9.7

Using Figure 9.4, distinguish between risk minimisation and risk aversion.

(Answer in Appendix A at the back of the book)

349 489 1,000

100% small

100% large

3,000

2,562

2,400

Expected NPV (£)

Risk (standard deviation, £)

B

C

A

Figure 9.4

Gerrybild’s opportunity

set

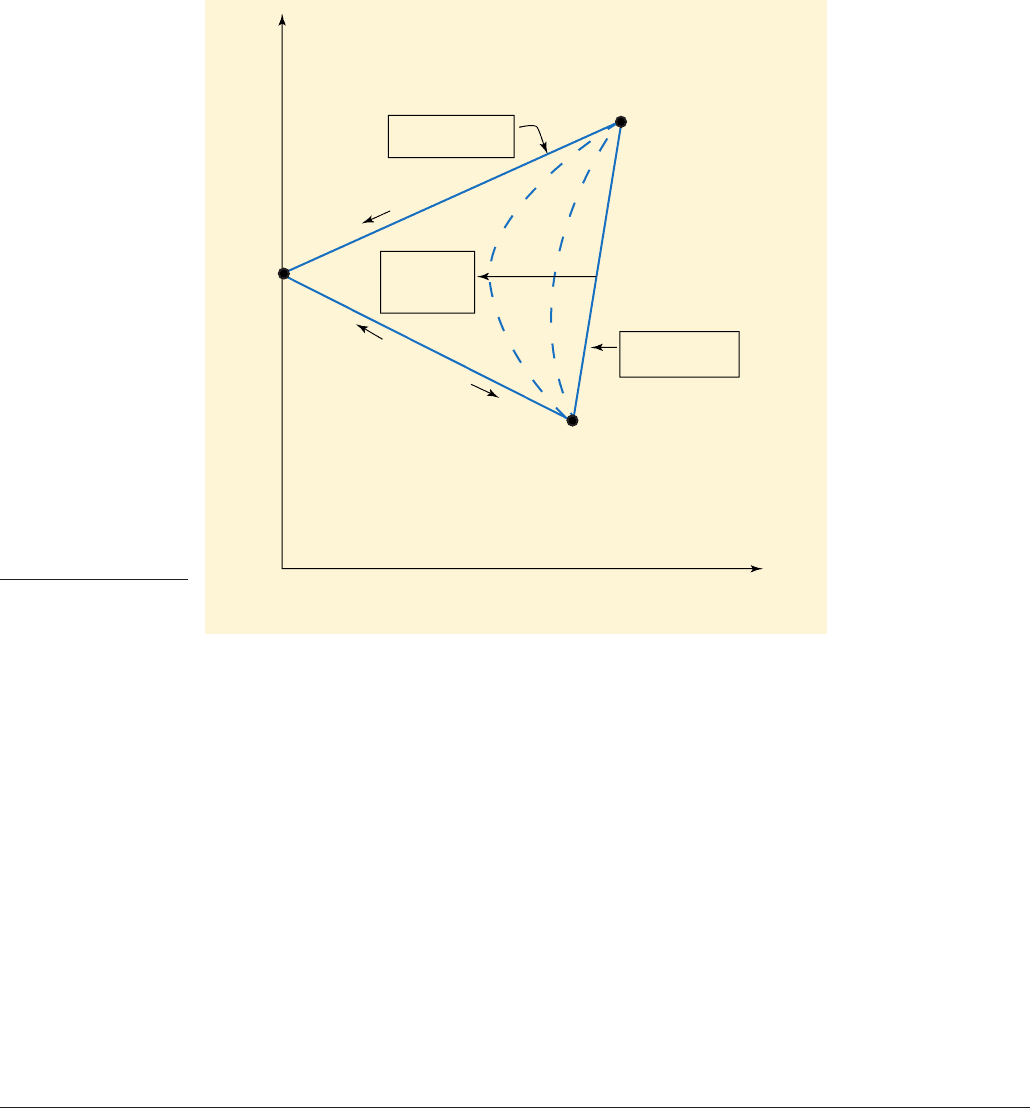

Having so far looked only at simple two-asset portfolios, it is now useful to extend the

analysis to more comprehensive combinations (see Figure 9.5). Imagine three assets are

available, A, B and C, for each of which we have estimates of expected return and stan-

dard deviation, and also the covariance (and hence correlation) between each pair of

assets. Imagine further that, whereas A and B are quite closely correlated, B and C are

less so, and that correlation between A and C is even weaker.

Using a technique called Quadratic Programming, developed by Sharpe (1963), we

can specify all available portfolios comprising one, two or three assets. Although there

are only seven possible combinations of whole investments (A, B and C alone, A plus

B, B plus C, A plus C and all three together), there are myriad combinations if we allow

for divisibility of assets. The full range of available portfolios, i.e. risk–return combi-

nations, is shown by the opportunity set in the form of an envelope, or ‘bat-wing’.

The corners represent individual assets, while two-asset combinations are shown

by the solid lines AB and BC and the dotted profile AC. Notice that by combining A

and C, the investor can exploit their relative lack of correlation by accessing relatively

more attractive portfolios in terms of their respective returns for particular levels of

risk. The opportunity set thus moves inwards as assets with lower correlation are

included. However, he can now access even more attractive combinations of A and C

by combining all three assets. Points inside the envelope, or along the outer boundary,

represent all possible combinations of A, B and C.

Notice that the investor now has access to a far wider range of investment combi-

nations. If he is limited to combinations of only two assets, say A and B, as we saw in

earlier analyses, he is restricted to risk–return combinations along AB or BC, depend-

ing on which two assets are combined. However, if access is opened up to include a

third asset, the expanded range of combinations now available allows him to select far

superior mixes of risk and return. For example, combinations within the envelope and

9.7 PORTFOLIOS WITH MORE THAN TWO COMPONENTS

CFAI_C09.QXD 10/28/05 4:28 PM Page 231

.

232 Part III Investment risk and return

on its upper bound, AEC, are superior to most of the two-asset portfolios available

along AB and BC.

As before, we can differentiate between efficient and inefficient combinations.

Clearly, all points lying beneath the upper edge AE and those along the segment EC are

inefficient. The efficient set is therefore AE, identical in shape to our earlier profile,

except that we are dealing with three-asset combinations (enabling investors to achieve

lower levels of risk for specified returns by diversifying away yet more risk). Similar

principles would apply if we were dealing with 30 or 300 assets, although the informa-

tion requirements would become progressively more formidable.

Generally, we can conclude that the more assets that are available, the wider the

range of choice open to the investor, and the greater his opportunities to achieve more

desirable combinations of risk and return. The more assets under consideration, the

nearer to the vertical axis lies the envelope of portfolios. Hence, the higher is the return

achievable for a given risk, or conversely, the lower is the risk achievable for a speci-

fied expected return.

Notice also that the earlier conclusion about the optimal portfolio remains valid – it

still depends on the particular investor’s risk–return preferences.

Self-assessment activity 9.8

Draw an envelope of portfolios for the case where four assets are available to invest in,

either individually or as portfolios.

(Answer in Appendix A at the back of the book)

A

A and

B combined

A and C combinedA, B and C combined

B

B and C combined

A and C

combined

C

E

Expected return on portfolio (ERP)

Risk of portfolio

(Standard deviation,

s

p

)

Figure 9.5

Portfolio combinations

with three assets

CFAI_C09.QXD 10/28/05 4:28 PM Page 232

.

Chapter 9 Relationships between investments: portfolio theory 233

9.8 CAN WE USE THIS FOR PROJECT APPRAISAL? SOME RESERVATIONS

The Gerrybild example illustrates some drawbacks with the portfolio approach to han-

dling project risk.

1 Most projects can be undertaken only in a very restricted range of sizes or even on

an ‘all-or-nothing’ basis. This does not entirely undermine the portfolio approach –

it simply means that the range of combinations available is much narrower.

Besides, enterprises are often undertaken on a joint venture basis (e.g. in large,

high-risk activities like Eurotunnel and Airbus and many cross-border automobile

operations), where the various parties have some freedom to select the extent of

their participation.

2 A more severe problem is the implication of constant returns to scale. Our analy-

ses imply that if a smaller version of a project is undertaken, the percentage

returns, or the absolute return per pound invested, will remain unchanged. For

example, if the return on a whole project is 20 per cent, the return from doing 30

per cent of the same project is still 20 per cent. This may apply for investment in

securities, but is unlikely for investment projects, where there is often a minimum

size below which there are zero or negative returns, and, thereafter, increasing

returns to scale.

3 We should be wary of any approach that relies on subjective assessments of proba-

bilities, or at least wary of the probabilities themselves. In the case of repetitive

activities, such as replacement of equipment, about which a substantial data bank

of costs and benefits has been compiled, the probabilities may have some basis in

reality. In other cases, such as major new product developments, probabilities are

largely based on inspired guesswork. Different decision analysts may well formu-

late different ‘guesstimates’ about the chances of particular events occurring.

However, the subjective nature of probabilities used in practice need not be a deter-

rent if the estimates are well supported by reasoned argument, and therefore instil

confidence.

4 Since attitudes to risk determine choice, we need to know the decision-maker’s util-

ity function, which summarises his or her preferences for different monetary amounts.

The difficulties of obtaining information about an individual manager’s utility

function (let alone for a group) are formidable, as Swalm (1966) has shown. Besides,

we should really be seeking to apply the risk-return preferences of shareholders

rather than those of managers.

5 The portfolio approach to analysing project risk seems unduly management-oriented.

Managers formulate the assessments of alternative payoffs, assess the relevant

probabilities and determine what combinations of activities the enterprise should

undertake. Managers are considerably less mobile and less well diversified than

shareholders, who can buy and sell securities more or less at will. Managers can

hardly shrug off a poor investment outcome if it jeopardises the future of the enter-

prise or, more pertinently, their job security. Most managers are more risk-averse

than shareholders, resulting in the likelihood of sub-optimal investment decisions.

Here, we see another manifestation of the agency problem – how do we get man-

agers to accept the levels of risk that owners are prepared to tolerate?

These may appear to be highly damaging criticisms of the portfolio approach, espe-

cially as it applies to investment decisions. However, although having limited opera-

tional usefulness for many investment projects, it provides the infrastructure of a more

sophisticated approach to investment decision-making under risk, the Capital Asset

Pricing Model (CAPM). This is based on an examination of the risk–return characteris-

tics and resulting portfolio opportunities of securities, rather than physical investment

opportunities.

Capital Asset Pricing Model

The CAPM is a model designed

to explain how the stock mar-

ket values capital assets, includ-

ing ordinary shares by assessing

their relative risk-return

properties

CFAI_C09.QXD 10/28/05 4:28 PM Page 233

.

234 Part III Investment risk and return

This chapter has examined some reasons why firms diversify their activities, and has

considered the extent to which the theory of portfolio analysis can provide operational

guidelines for diversification decisions.

Key points

■ Both firms and individuals diversify investments – firms build portfolios of busi-

ness activities and individuals build portfolios of securities.

■ An important motive for business diversification is to reduce fluctuations in returns.

■ Variations in returns can be totally eliminated only if the investments concerned

have perfect negative correlation and if the portfolio is weighted so as to minimise

risk.

■ The expected return from a portfolio is a weighted average of the returns expect-

ed from its components, the weights being determined by the proportion of capi-

tal invested in each activity or security. For a portfolio comprising the two assets,

A and B:

■ Portfolio risk, however, is given by a square-root formula:

■ The degree of covariability between the returns expected from the components of

the portfolios can be measured by the covariance, or by the correlation coef-

ficient, The lower the degree of covariability, the lower is the risk of the portfo-

lio (for given weightings).

■ The available risk–return combinations for mixing investments are shown by the

opportunity set.

■ Some combinations can be rejected as inefficient. Rational risk-averting investors

focus only on the efficient set.

■ The optimal portfolio for any investor depends on their attitude to risk: that is, how

risk-averse they are.

■ In practice, there are serious difficulties in applying the portfolio techniques to

physical investment decisions.

r

AB

.

cov

AB

,

s

p

23a

2

s

A

2

11 a2

2

s

B

2

2a11 a2cov

AB

4

ER

p

aER

A

11 a2ER

B

SUMMARY

Further reading

The classic works on portfolio theory are by Markowitz (1952), Sharpe (1964) and Tobin (1958)

(all of whom have won Nobel Prizes for Economics). See also Fama and Miller (1972), Sharpe,

Alexander and Bailey (1996), Levy and Sarnat (1994) and Copeland and Weston (2004) for more

developed analyses, and also proofs and derivations of the formulae used in this chapter. Finally,

Markowitz’s Nobel address (1991) is well worth reading.

The CAPM explains how individual securities are valued, or priced, in efficient capital mar-

kets. Essentially, this involves discounting the future expected returns from holding a security at

a rate that adequately reflects the degree of risk incurred in holding that security. A major con-

tribution of the CAPM is the determination of the premium for risk demanded by the

market from different securities. This provides a clue as to the appropriate discount rate

to apply when evaluating risky projects. The CAPM is analysed in the next chapter.

CFAI_C09.QXD 10/28/05 4:28 PM Page 234