Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 10 Setting the risk premium: the Capital Asset Pricing Model 245

Table 10.3

Possible returns from

Walkley Wagons

State of economy (%) (%)

10 12

20 24

56

15 18

E

4

E

3

E

2

E

1

ER

j

ER

m

expected on the market, It is important to appreciate that ‘returns’ in this context

include both changes in market price and also dividends as we saw in the Pilkington

example. For the overall market, dividend returns may be measured by the average

dividend yield on the market index.

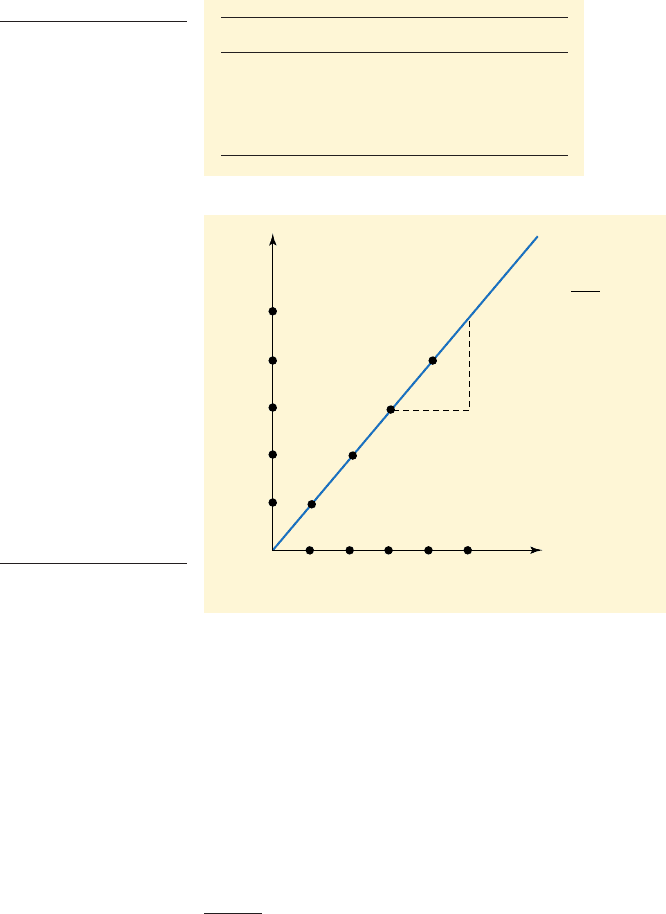

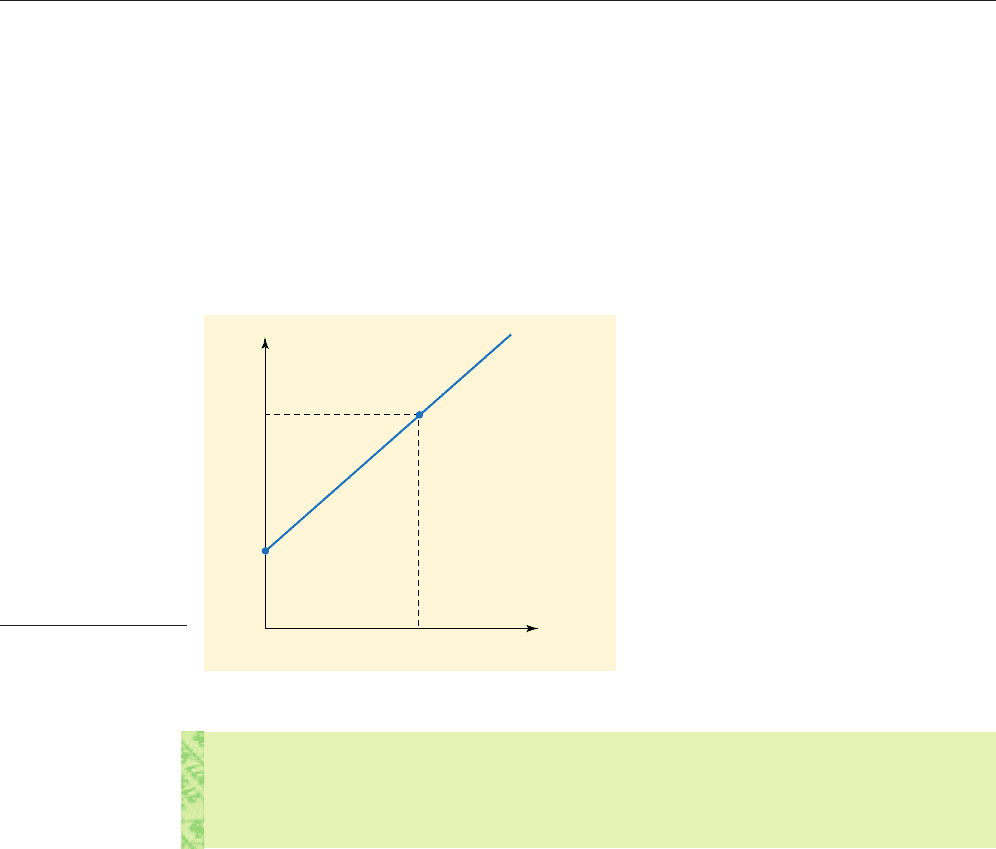

■ Example: Walkley Wagons

The case of Walkley Wagons is shown in Table 10.3. Investors anticipate four possible

future states of the economy. For every percentage point increase in the expected mar-

ket return the expected return on Walkley shares rises by 1.2 percentage

points. Walkley thus outperforms a rising market. The graphical relationship between

and shown in Figure 10.5, is known as the characteristics line. Its slope of 1.2

is the Beta coefficient. Beta indicates how the return on Walkley is expected to vary

alongside given variations in the return on the overall stock market.

ER

m

,ER

j

1ER

j

21ER

m

2,

ER

m

.

30

24

18

12

6

0

510152025

E

3

E

1

E

4

E

2

ER

m

ER

j

Characteristics Line

ER

j

= α + β ER

m

Slope =

= 1.2

ΔER

j

ΔER

m

ΔER

j

ΔER

m

Figure 10.5

The characteristics line:

no specific risk

*Readers unfamiliar with the technique of regression analysis might refer to C. Morris, Quantitative

Approaches in Business statistics (Pearson).

■ The market model

In practice, because it is not easy to record people’s expectations, the measurement of

Beta cannot be done by looking forward. We have to measure Beta using past observa-

tions of the actual values of both the return on the individual company’s shares, and

also for the overall market, i.e. and respectively. So long as the past is accepted as

a reliable indication of likely future events (i.e. people’s expectations are moulded by

examination of the frequency distribution of past recorded outcomes), observed Betas

can be taken to indicate the extent to which may vary for specified variations in

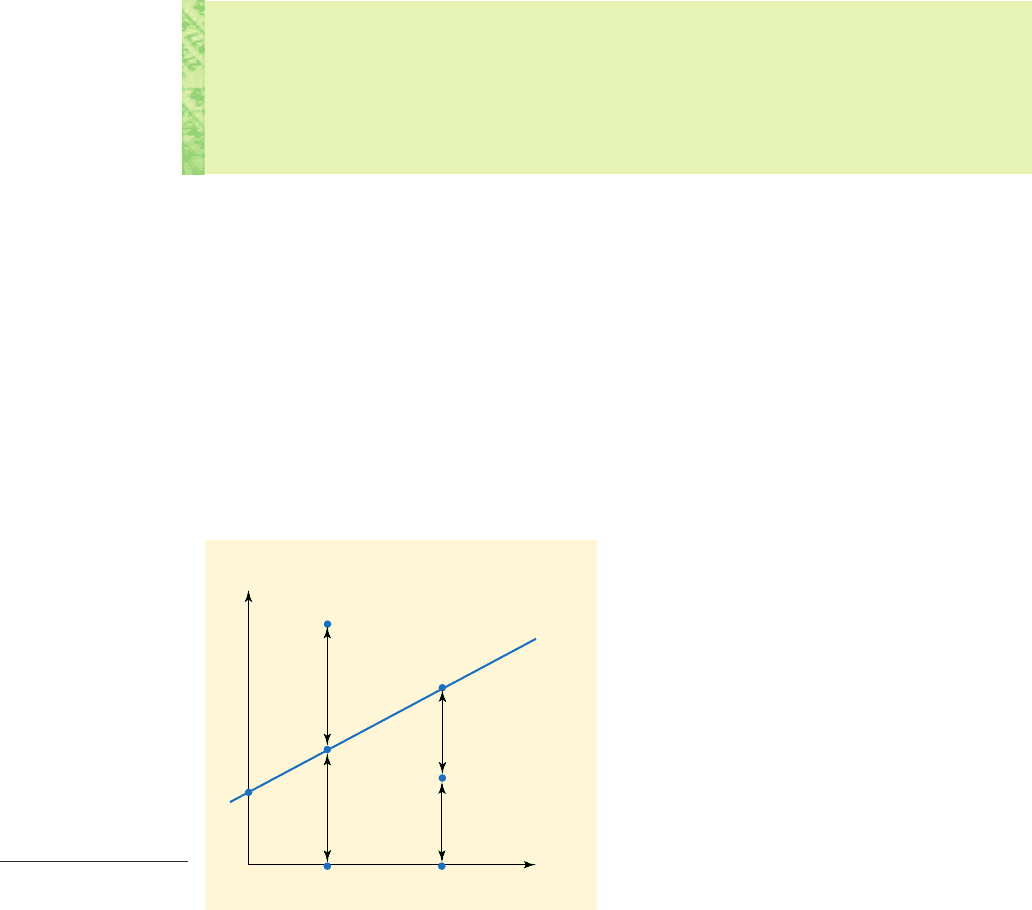

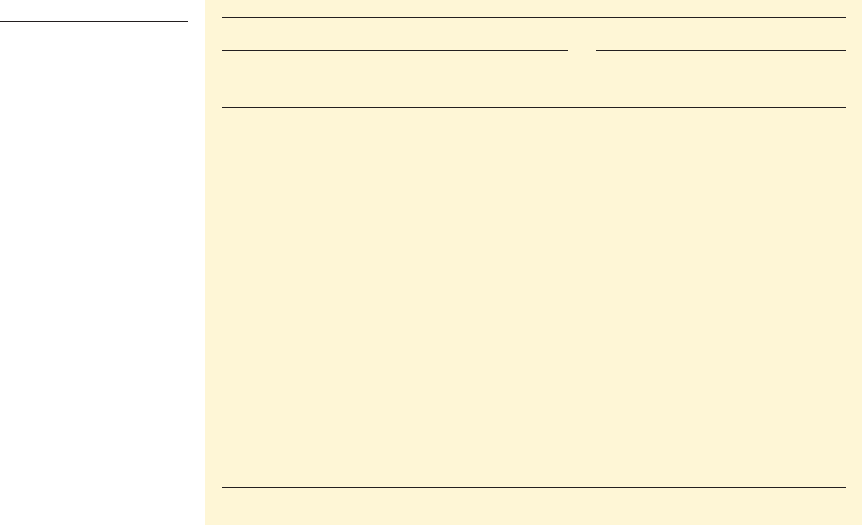

A regression line* is fitted to a set of recorded relationships, as in Figure 10.6. The

R

m

.R

j

R

m

R

j

CFAI_C10.QXD 3/15/07 7:28 AM Page 245

.

246 Part III Investment risk and return

■ Systematic and unsystematic returns

Figure 10.6 shows an imaginary set of monthly observations relating to a given year,

say 2004, to which has been fitted a regression line. Clearly, unlike the expected values

displayed in Figure 10.5, most values actually lie off the line of best fit. These diver-

gences are due to the sort of random, unsystematic factors suggested in Section 10.3.

For example, observation Z relates to the returns in May 2004. The overall return on

security j in this month, XZ, can be broken down into the market-related return, XY, due

to co-movement with the overall market, and the non-market return, or ‘excess return’,

YZ, due to unsystematic factors, which, in this month, have operated favourably. The

opposite appears to have applied in June 2004, indicated by point H. The market-

related return ‘should’ have been FG, but the actual return of GH was dampened by

*

*

*

*

*

*

*

*

*

*

*

*

May 2004

Z

F

H

Y

a

0

XG

R

m

June 2004

R

j

= a + b

R

m

+

u

R

1

Characteristics

line

^^

Figure 10.6

The characteristics line:

with specific risk

Self-assessment activity 10.4

You read in the financial press, that the ‘experts’ are predicting overall stock market

returns of 25 percent next year. What return would you expect from holding Walkley

Wagons ordinary shares?

(Answer in Appendix A at the back of the book)

hypothesized relationship is:

and the fitted line is given by:

where and are estimates of the ‘true’ values of and and u is a term included to

capture random influences, that are assumed to average zero. This regression model is

called the market model.

The intercept term, deserves explanation. This is the return on security j when

the return on the market is zero, i.e. the return with the impact of market or systemat-

ic risk stripped out. Consequently, it indicates what return the security offers for

unsystematic risk. We might expect this to average out at zero over time, given the ran-

dom character of sources of specific risk. However, it is by no means uncommon

empirically to record non-zero values for Notice that in Figure 10.5 is zero.

aa.

a

j

,

b,ab

ˆ

j

a

ˆ

j

R

j

a

ˆ

j

b

ˆ

j

R

m

u

R

j

a

j

b

j

R

m

market model

A device relating the expected

(in practice, actual) return from

individual securities to the

expected/actual return from the

overall stock market

CFAI_C10.QXD 3/15/07 7:28 AM Page 246

.

Chapter 10 Setting the risk premium: the Capital Asset Pricing Model 247

unfavourable random factors represented by FH. This analysis implies that variations in

along the characteristics line stem from market-related factors, which systematically affect all

securities, and that variations around the line represent the impact of factors specific to compa-

ny j. The systematic relationship is captured by b.

R

j

Beta values: the key relationships

Beta is the slope of a regression line. The slope coefficient relating to equals the

covariance of the return on security j with the return on the market divided by

the variance of the market return

Since the covariance is equal to the correlation coefficient times the product of the

respective standard deviations (see Chapter 9), Beta is also equivalent to:

Beta is thus the correlation coefficient multiplied by the ratio of individual security

risk to market risk. If the security concerned has the same total risk as the market, Beta

equals the correlation coefficient. For a given correlation, the greater the security’s sys-

tematic risk in relation to the market, the greater is Beta. Conversely, the lower the

degree of correlation, for a given risk ratio, the lower the Beta. Therefore, while Beta does

not measure risk in absolute terms, it is a risk indicator, reflecting the extent to which the

return on the single asset moves with the return on the market, i.e. it is a measure of relative

risk. To obtain a risk measure in absolute terms, we have to examine the total risk of

the security in more detail, using a statistical technique called analysis of variance. This

is explained in the appendix to this chapter.

■ Systematic risk: Beta measurement in practice

Betas are regularly calculated by several agencies. The Risk Measurement Service (RMS)

operated by the London Business School (LBS) is the best known in the UK. The RMS

is a quarterly updating service, based on monthly observations extending back over

five years, which computes the Betas of all firms listed both on the main market and

also on AIM. For each of the preceding 60 months, is calculated for every security

and regressed against An extract from the RMS showing the components of the FT

30 Index of leading industrial shares is given in Table 10.4.

The Beta values of securities fall into three categories: ‘defensive’, ‘neutral’ and

‘aggressive’. An aggressive security has a Beta greater than 1. Its returns move by a

greater proportion than the market as a whole. In the case of GKN, with a Beta of 1.13,

for every percentage point change in the market’s return, the return on GKN’s shares

changes by 1.13 points. Such stocks are highly desirable in a rising market, although

the excess return is not guaranteed due to the possible impact of company-specific fac-

tors. A defensive share is BOC Group, with a Beta of 0.73, movements in whose returns

tend to understate those of the whole market. The returns on neutral stocks like Royal

Bank of Scotland, with its Beta of 1.01, parallel those on the market portfolio.

R

m

.

R

j

Beta

j

r

jm

s

j

s

m

s

m

2

r

jm

s

j

s

m

1r

jm

s

j

s

m

2

Beta

j

cov

jm

s

m

2

1s

m

2

2:

1cov

jm

2

R

m

R

j

analysis of variance

A statistical technique for

isolating the separate determi-

nants of the fluctuations

recorded in a variable over time

Self-assessment activity 10.5

What is the significance of variations around the characteristics line? Relate this to a

particular company, say, British Airways.

(Answer in Appendix A at the back of the book)

CFAI_C10.QXD 3/15/07 7:28 AM Page 247

.

248 Part III Investment risk and return

Table 10.4

Beta values of the

constituents of the

FT 30 Share Index

Company name FTSE actuaries Varia- Specific Std Err R-

classification Beta bility risk of Beta Squared

Allied Domecq BevDstVn .58 25 23 .16 14

Holdings

BAE Systems Defence 1.19 39 34 .21 23

BG Group Oil Intg .79 26 22 .16 24

BOC Group ChemCom .73 20 17 .13 32

Boots Group Ret Dept .74 25 23 .16 21

BP Oil Intg .83 22 18 .13 34

British Airways

Air

Tran

1.66 49 42 .23 28

British American Tobacco .71 34 32 .20 11

Tobacco

BT Group Telcomfx 1.53 37 29 .19 41

Cadbury-Schweppes FoodProc .53 22 20 .15 15

Compass Group Bus Supp 1.04 32 27 .19 28

Diageo BevDstVn .28 21 21 .15 4

EMI Group PublPrnt 1.14 47 44 .23 14

GKN AutoPrts 1.13 34 29 .19 27

GlaxoSmithKline Pharmact .40 21 20 .15 9

Imperial Chemical ChemSpec 1.36 48 43 .23 20

Industries

Invensys Electrnc 1.36 67 64 .26 10

ITV TVRadFil 1.54 44 37 .21 30

Lloyds TSB group Banks 1.19 30 24 .16 38

LogicaCMG Comp Svs 1.36 64 60 .26 11

Marks & Spencer Ret Dept .66 30 29 .19 12

Group

Peninsular & Shipport 1.14 36 32 .20 24

Oriental ‘Dfd’

Prudential Life Ass 1.50 36 28 .18 42

Reuters Group PublPrnt 1.35 54 50 .24 15

Royal Bank of Banks 1.01 30 26 .17 27

Scotland

Royal & Sun InsNonLf 1.54 50 44 .23 23

Alliance Ins Grp

Scottish Power Electric .44 24 23 .16 8

Tate & Lyle FoodProc .70 35 33 .20 10

Tesco FdrugRet .59 26 24 .17 13

Vodafone Group Telcomob 1.03 35 31 .20 22

Source: Risk Measurement Service, London Business School, Oct.–Dec. 2004.

Notice that the total risk of each security is shown as ‘variability’, e.g. 34 for GKN.

This is a standard deviation. Notice also that this invariably exceeds ‘Specific Risk’,

e.g. 29 for GKN. The difference indicates the market risk that cannot be diversified

away. (See the appendix to this chapter for a fuller explanation.)

Self-assessment activity 10.6

Suggest why the Beta values tend to cluster in a range of roughly 0.70 to 1.30.

(Answer in Appendix A at the back of the book)

CFAI_C10.QXD 3/15/07 7:28 AM Page 248

.

Chapter 10 Setting the risk premium: the Capital Asset Pricing Model 249

10.6 COMPLETING THE MODEL

The CAPM suggests that only systematic risk is relevant in assessing the required risk

premiums for individual securities, and we have established that Beta values reflect the

sensitivity of the returns on securities to movements in the market return. However, the

size of the risk premium on individual securities (or on efficient portfolios) will depend

on the extent to which the return on the investment concerned is correlated with the

return on the market. For a security perfectly correlated with the market, the market

risk premium would be suitable; otherwise the required return depends on the Beta.

The CAPM concludes that when an efficient capital market is in equilibrium, i.e. all

securities are correctly priced, the relationship between risk and return is given by the

security market line (SML), as depicted in Figure 10.7.

■ The security market line

The equation of the SML states that the required return on a share is made up of the

return on a risk-free asset, plus a premium for risk related to the market’s own risk pre-

mium, but which varies according to the Beta of the share in question:

If Beta is 1, the required return is simply the average return for all securities, i.e. the

return on the benchmark market portfolio. Otherwise, the higher the Beta, the higher

are both the risk premium and the total return required. A relatively high Beta does not,

however, guarantee a relatively high return. The actual return depends partly on the

behaviour of the market, which acts as a proxy for general economic factors. Similarly,

expected returns for the individual security hinge on the expected return for the mar-

ket. In a ‘bull’, or rising, market, it is worth holding high Beta (aggressive) securities.

Conversely, defensive securities offer some protection against a ‘bear’, or falling,

ER

j

R

f

b

j

1ER

m

R

f

2

Security market

line (SML)

ER

j

=

R

f

+

b

j

(ER

m

–

R

f

)

Market

portfolio

M

b

= 1

Beta

ER

j

ER

m

R

f

Figure 10.7

The security market

line

Self-assessment activity 10.7

Why is the Beta of the overall market equal to 1.0?

(Answer in Appendix A at the back of the book)

CFAI_C10.QXD 3/15/07 7:28 AM Page 249

.

250 Part III Investment risk and return

market. However, holding a single high Beta security is foolhardy, even on a rising market.

Undiversified investments, whatever their Beta values, are prey to specific risk factors.

Portfolio formation is essential to diversify away the risks unique to individual companies.

10.7 USING THE CAPM: ASSESSING THE REQUIRED RETURN

We may now apply the CAPM formula to derive the rate of return required by share-

holders in a particular company. To do this, we require information on three com-

ponents: the risk-free rate, the risk premium on the market portfolio and the Beta

coefficient.

■ Specifying the risk-free rate

No asset is totally risk-free. Even governments default on loans and defer interest pay-

ments. However, in a stable political and economic environment, government stock is

about the nearest we can get to a risk-free asset. Most governments issue an array of

stock. These range from very short-dated securities, such as Treasury Bills in the UK,

maturing in 1–3 months, to long-dated stock, maturing in 15 years or more and even,

exceptionally, undated stock, such as 3.5 per cent War Loan with no stated redemption

date. It is tempting to try to match up the life of the investment project with the corre-

sponding government stock when assessing the risk-free rate. For example, when deal-

ing with a ten-year project, we might look at the yield on ten-year government stock.

This may be unsatisfactory for several reasons. First, although the nominal yield to

maturity is guaranteed, the real yield may well be undermined by inflation at an

unknown rate. Second, there is an element of risk in holding even government stock.

This is reflected in the ‘yield curve’, which normally rises over time to reflect the

increasing liquidity risk of longer-dated stock. Third, although the yield to maturity is

given, a forced seller of the stock might have to take a capital loss during the inter-

vening period, since bond values fluctuate over time with variations in interest rates.

A better way to specify is to take the shortest-dated government stock available, normal-

ly three-month Treasury Bills, for which these risks are minimised. The current yield

appears in the financial press. This is about the same as LIBOR, the London Interbank

Offered Rate, the rate of interest at which banks lend to each other overnight.

■ Finding the risk premium on the market portfolio

The risk premium on the market portfolio, is an expected premium.

Therefore, having assessed we need to specify by finding a way of capturing the

market’s expectations about future returns. An approximation can be obtained by look-

ing at past returns, which, taken over lengthy periods, are quite stable. The usual

approach with ordinary shares is to analyse the actual total returns on equities as com-

pared with total returns on fixed-interest government stocks over some previous time

period. The results are likely to differ according to the period taken and the type of gov-

ernment stock used as the reference level (e.g. short-term securities such as Treasury Bills

or long-term gilts). However, studies seem to come up with quite stable results. For

example, Dimson and Brealey (1978), Day et al. (1987) and Dimson (1993) for the periods

1918–77, 1919–84 and 1919–92, respectively, showed average annual returns above the

risk-free rate of 9.0, 9.1 and 8.7 per cent (before taxes) for the market index in the UK.

Similar estimates have been obtained in the USA. In 1985, Mehra and Prescott

found that, after adjusting for inflation, equities delivered average real returns of 7 per

cent p.a. over a quarter of a century, compared with 1 per cent for Treasury bonds – a

real risk premium of 6 per cent. Mehra and Prescott found this premium ‘puzzling’ on

ER

m

R

f

,

1ER

m

R

f

2,

R

f

CFAI_C10.QXD 3/15/07 7:28 AM Page 250

.

Chapter 10 Setting the risk premium: the Capital Asset Pricing Model 251

the grounds that it seemed too large a premium for bearing non-diversifiable market

risk, especially given international opportunities for diversification. Fama and French

(2000) found the equity risk premium averaged 8.3 per cent p.a. over 1950–99, this

being well in excess of the 4.1 per cent p.a average for 1872–1949. Ibbotson Associates,

a consulting firm, specifies a risk premium above the US Treasury Bill return at 8.8 per

cent based on long-term research.

Dimson (1993) reported similar premiums in Japan (9.8 per cent, 1970–92), Sweden

(7.7 per cent, 1919–90) and the Netherlands (8.5 per cent, 1947–89), although the last

two estimates were in real terms, i.e. relative to domestic inflation.

A rather lower UK risk premium was recorded by Grubb (1993/4), at 6.2 per cent

for 1960–92. Grubb suggests that returns to equities in the 1970s and 1980s were excep-

tional and that under a ‘modern scenario of moderate growth and moderate inflation’,

a much lower premium on equities of only 2 per cent would be reasonable. This view

is supported by Wilkie (1994), who, after exhaustive study of past trends in dividend

yields and inflation, argues for a risk premium of 3 per cent for longer-term invest-

ment and 2 per cent for the short term. The evidence is inconclusive, but it is unlikely

that many finance directors would contemplate recommending projects with such low

premiums for risk.

However for shorter periods, say five or ten years (more akin to project lifetimes),

returns are highly volatile and sometimes negative. Clearly, people neither require nor

expect negative returns for holding risky assets! It therefore seems more sensible to

take the long-term average, and to accept that, in the short-term, markets exhibit unpre-

dictable variations.

The investment banking arm of Barclays Bank, Barclays Capital (www.barcap.com)

publishes an annual analysis of equity and gilt-edged returns for various time periods

called the ‘Equity–Gilt Study’. Their data show real investment returns on equities and

government stock, and also on cash deposits. The long-term (105 years) equity risk pre-

mium is 4.0 per cent in real terms, and 4.1 per cent above the return on cash deposits.

Like many observers, Barclays Capital suggests that as the world economy moves

from the low growth/high inflation phase of the 1970s and 1980s to the high growth/

low inflation experienced more recently, equity returns were untypically high. One

reason for expecting lower future returns is technological progress, in general, and the

information revolution, in particular, resulting in shorter competitive advantage peri-

ods. Firms typically have less time to exploit a ‘first mover’s advantage’ before com-

petitors arrive i.e. entry barriers are lower. Another likely depressant is the increased

openness of the world economy due to the activities of the World Trade Organisation.

A complicating factor is the ‘unusual demographic outlook of a shrinking population

and an expanding dependent population’. This suggests that the prices of financial

assets will fall relative to prices of goods and services, so that equities may offer a less

effective inflation hedge in the future.

The Barclays Capital website has an interactive facility that allows users to calculate

average annual returns for specified periods for the UK markets for any period over

1919 to date, and from 1925 to date for the USA. Table 10.5 shows some sample calcu-

lations for long periods and a year-by-year analysis for both countries.

In this table, the risk premium is expressed in nominal terms, i.e. before removing

inflation. The data suggest that, recently, equity premia have been high in relation to

longer-term outcomes. Note the remarkable similarity between UK and US premia.

The data are real geometric average annualised returns, i.e. they exclude the effect of

inflation.

One might conclude that, although the early 2000s were poor years, pulling down

the rolling average, there is little solid evidence in these data of a sea-change in the

equity risk premium given its more recent recovery. However, to reflect prevailing

thought, subsequent analysis will build in a risk premium for equities, i.e. the risk pre-

mium of the overall market portfolio, of 5%.

CFAI_C10.QXD 3/15/07 7:28 AM Page 251

.

252 Part III Investment risk and return

Table 10.5

Equity-gilts relative

returns

UK US

Equity Equity

Period Equities Gilts premium Equities Bonds premium

1925–2004 6.0 1.9 4.1 7.1 2.3 4.8

1925–1946 6.0 5.7 0.3 5.0 3.5 1.5

1946–1991 5.9 7.1 7.7 0.7 7.0

–92 6.1 6.9 7.7 0.8 6.9

–93 6.5 6.8 7.7 1.1 6.6

–94 6.2 6.8 7.5 0.9 6.6

–95 6.4 6.7 8.0 1.3 6.7

–96 6.6 0.1 6.7 8.5 1.5 7.0

–97 6.8 0.1 6.7 8.5 1.5 7.0

–98 6.9 0.5 6.4 8.7 1.6 7.1

–99 7.1 0.3 6.8 9.0 1.4 7.6

–2000 6.8 0.4 6.4 8.5 1.6 6.9

–01 6.4 0.5 5.9 8.1 1.7 6.4

–02 5.8 0.6 5.2 7.4 1.9 5.5

–03 5.9 0.5 5.4 7.8 1.9 5.9

–04 6.0 0.6 5.4 7.8 1.9 5.9

Source: Barclays Capital (www.barcap.com)

0.3

0.6

0.3

0.8

1.2

In probably the most thorough analysis to date of the equity risk premium, Dimson,

Marsh and Staunton (2002) updated and largely corroborated these figures in a study

of the equity risk premium for 16 countries, over a full century (1900–2000). They sug-

gested that some earlier studies (including the earlier Dimson Studies!) might have

over-estimated the equity premium by excluding the First World War era, when equi-

ty returns were poor, and by confining the study to the performance of surviving

firms, thus excluding the relatively poor performers that had expired.

They found:

■ The average global real return on equity was 4.6 per cent.

■ Germany had offered the highest risk premium at 6.7 per cent.

■ Denmark offered the lowest risk premium at just 2 per cent.

■ In the US, for every 20-year period examined, equities outperformed bonds.

■ Only four countries – German, Netherlands, Sweden and Switzerland – exhibited

any 20-year periods over which bonds outperformed equities.

■ It is reasonable to expect a real equity premium of no more than 5 per cent or so in

the UK in the future.

The LBS team now offer an annual update of this analysis (www.abn-amro.com).

Their results are beginning to reveal some interesting, even perverse, findings. For

example, contrary to intuition, there appears to be no apparent positive relationship

between equity returns and GDP growth. Moreover, ‘Historically, buying into equity

markets with a high GDP growth rate has given a return that is below the return of

markets with a low GDP growth rate.’ Furthermore, for five years in a row up to 2004,

value investing beat growth investing. Over the period, 1999–2004, high-yield equities

returned per cent compared to low-yield equities that returned per cent.

This, of course, casts some doubt on the wisdom of firms’ re-investment policies. Time

will tell whether this is the beginning of a long-term trend.

Meanwhile, their updates on the real returns on equities and bonds allow us to infer

the following risk premia for equities over 1900–2004 for selected countries:

6285

CFAI_C10.QXD 3/15/07 7:28 AM Page 252

.

Chapter 10 Setting the risk premium: the Capital Asset Pricing Model 253

Country Real risk premium

on equities

Australia 6.4

Sweden 6.4

South Africa 6.2

USA 5.7

UK 4.1

World Average 4.0

Netherlands 3.8

Germany 1.0

Japan 2.8

Italy 0.5

Dimson et al. also discussed the ‘puzzle’ raised by Mehra and Prescott (1985), regard-

ing the size of the equity premium. They suggest that, given the persistent worldwide

out-performance by equities, the risk element in equity investment, at least in devel-

oped, efficient markets, is overplayed. Prescott and McGrattan (2003) have revisited

this puzzle. They found that in the USA, after taking into account certain factors

ignored by Mehra and Prescott, e.g. taxes, regulatory constraints, diversification costs,

and focusing on long-term rather than short-term saving instruments, the puzzle is

solved. Allowing for all these factors, they found that the difference between average

equity and debt returns during peacetime is less than 1 per cent p.a., with the average

real equity return just under 5 per cent, and the average real return on debt instruments

a little under 4 per cent, a far lower premium than other writers have suggested.

■ Finding Beta

Beta values appear to be fairly stable over time, so we can use Beta values based on past

recorded data, such as those provided by the RMS, with a fair degree of confidence.

This is acceptable so long as the company is not expected to alter its risk characteristics

in the future: for example, by a takeover of a company in an unrelated field or a spin-

off of unwanted activities.

■ The required return

We now demonstrate the calculation of the required return for the ‘aggressive’ share

British Airways, using the equation for the SML:

The Beta recorded by the RMS at December 2004 was 1.66 (Table 10.4). At the same date,

the yield on three-month Treasury Bills was about 4.75 per cent. For British Airways, this

results in the following required return, assuming a market risk premium of 5 per cent:

ER 4.75% 1.6615%2 4.75% 8.30% 13.05%.

ER

j

R

f

b

j

1ER

m

R

f

2

Self-assessment activity 10.8

Visit the Barclays Capital website to conduct your own analysis of risk premia, e.g. update

the figures shown on Table 10.5.

CFAI_C10.QXD 3/15/07 7:28 AM Page 253

.

254 Part III Investment risk and return

■ Application to investment projects

As British Airways shareholders appear to require a return of 13.0 per cent, it may seem

reasonable to use this rate as a cut-off for new investments. However, two warnings are

in order.

First, the discount rate applicable to new projects often depends on the nature of the activi-

ty. For example, if a new project takes British Airways away from its present spheres

of activity into, say, mobile telephony, its systematic risk will alter, as suggested by the

Beta for Vodaphone of 1.03. The relevant premium for risk hinges on the systematic

risk of telecommunications rather than of airline operation. This suggests that we ‘tai-

lor’ risk premiums, and thus discount rates, to particular activities. This aspect is

examined in the next chapter.

10.8 THE UNDERPINNINGS OF THE CAPM

All theories rely on assumptions in order to simplify the analysis and expose the impor-

tant relationships between key variables. In economics and related sciences, it is gener-

ally accepted that the validity of a theory depends on the empirical accuracy of its

predictions rather than on the realism of its assumptions (Friedman, 1953). However, if

we find that the predictions fail to correspond with reality, and we are satisfied that this

Self-assessment activity 10.9

What is the implied discount rate for investment by British Airways into retailing?

(Answer in Appendix A at the back of the book)

Second, the appropriate discount rate may depend upon the method of financing used. Until

now, we have implicitly been dealing with an all-equity financed company whose pre-

mium for risk is a reward purely for the business risk inherent in the company’s activ-

ity. In reality, most firms are partially debt-financed, exposing shareholders to financial

risk. Using debt capital increases the risk to shareholders because of the legally-

preferred position of creditors. Defaulting on the conditions of the loan (e.g. failing to

pay interest) can result in liquidation if creditors apply to have the company placed

into receivership. The more volatile the earnings of the firm, the greater the risk of

default.

Financial risk raises the Beta of the equity, as shareholders demand additional returns to

compensate. The Beta of the equity becomes greater than the Beta of the underlying

activity. In Chapter 19, we shall see that observed Betas have two components, one to

reflect business risk and one to allow for financial risk. The Betas recorded by the RMS

are actually equity Betas, so the required return computed for British Airways (a high-

ly geared company) is the shareholders’ required return, part of which is to compensate

for financial risk. However, when a company borrows, only the method of financing

changes; nothing happens to alter the riskiness of the basic activity. The cut-off rate

reflecting the basic risk of physical investment projects is often lower than the share-

holders’ own required return.

In the previous sections, we have concentrated on developing the operational aspects

of the CAPM, without explaining the underlying theoretical relationships. The under-

lying theory is explained in Sections 10.8 and 10.9 and brought together in Section 10.10,

which you may omit at this stage. Section 10.11 discusses some general issues raised

by the CAPM.

CFAI_C10.QXD 3/15/07 7:28 AM Page 254