Tracy John A. Accounting for Dummies

Подождите немного. Документ загружается.

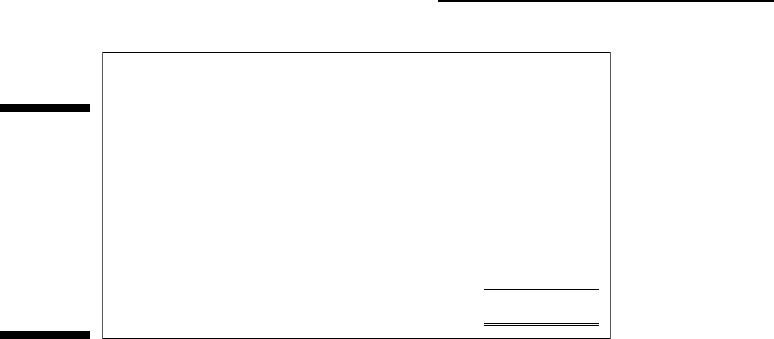

You submit this budgeted cash flow from operating activities (see Figure 10-3)

to headquarters. Top management expects you to control the increases in your

operating assets and liabilities so that the actual cash flow generated by your

division next year comes in on target. The cash flow of your division (minus,

perhaps, a small amount needed to increase the working cash balance held by

your division) will be transferred to the central treasury of the business.

Headquarters will be planning on you generating about $3.2 million cash flow

during the coming year.

Considering Capital Expenditures

and Other Cash Needs

This chapter focuses on profit budgeting for the coming year and budgeting

the cash flow from that profit. These are the two hardcore components of busi-

ness budgeting, but not the whole story. Another key element of the budgeting

process is to prepare a capital expenditures budget for your division that goes

to top management for review and approval. A business has to take a hard look

at its long-term operating assets — in particular, the capacity, condition, and

efficiency of these resources — and decide whether it needs to expand and

modernize its property, plant, and equipment.

In most cases, a business needs to invest substantial sums of money in pur-

chasing new fixed assets or retrofitting and upgrading its old fixed assets.

These long-term investments require major cash outlays. So, each division of

a business prepares a formal list of the fixed assets to be purchased, con-

structed, and upgraded. The money for these major outlays comes from the

central treasury of the business. Accordingly, the overall capital expenditures

Budgeted profit (See Figure 10-2) $2,856,000

Accounts receivable increase (195,574

Inventory increase (317,095

Prepaid expenses increase (26,226

Depreciation expense 835,000

Accounts payable increase 34,968

Accrued expenses payable increase 52,453

Budgeted cash flow from operating profit $3,239,526

)

)

)

Figure 10-3:

Budgeted

cash flow

from

operating

activities

for the

coming

year.

220

Part III: Accounting in Managing a Business

16_246009 ch10.qxp 4/17/08 12:02 AM Page 220

budget goes to the highest levels in the organization for review and final

approval. The chief financial officer, the CEO, and the board of directors of

the business go over a capital expenditure budget request with a fine-toothed

comb (or at least they should).

At the company-wide level, the financial officers merge the profit and cash

flow budgets of all profit centers and cost centers of the business. (A cost

center is an organizational unit that does not generate revenue, such as the

legal and accounting departments.) The budgets submitted by one or more of

the divisions may be returned for revision before final approval is given. One

main concern is whether the collective cash flow total from all the units pro-

vides enough money for the capital expenditures that will be made during the

coming year — and to meet the other demands for cash, such as for cash dis-

tributions from profit. The business may have to raise more capital from debt

or equity sources during the coming year to close the gap between cash flow

from operating activities and its needs for cash. This is a central topic in the

field of business finance and beyond the coverage of this book.

221

Chapter 10: Financial Planning, Budgeting, and Control

Business budgeting versus government budgeting:

Only the name is the same

Business and government budgeting are more

different than alike. Government budgeting is

preoccupied with allocating scarce resources

among many competing demands. From federal

agencies down to local school districts, govern-

ment entities have only so much revenue avail-

able. They have to make very difficult choices

regarding how to spend their limited tax revenue.

Formal budgeting is legally required for almost

all government entities. First, a budget request

is submitted. After money is appropriated, the

budget document becomes legally binding on

the government agency. Government budgets

are legal straitjackets; the government entity

has to stay within the amounts appropriated for

each expenditure category. Any changes from

the established budgets need formal approval

and are difficult to get through the system.

A business is not legally required to use budget-

ing. A business can implement and use its budget

as it pleases, and it can even abandon its budget

in midstream. Unlike the government, the revenue

of a business is not constrained; a business can

do many things to increase sales revenue. A busi-

ness can pass its costs to its customers in the

sales prices it charges. In contrast, government

has to raise taxes to spend more (except for fed-

eral deficit spending, of course).

16_246009 ch10.qxp 4/17/08 12:02 AM Page 221

222

Part III: Accounting in Managing a Business

16_246009 ch10.qxp 4/17/08 12:02 AM Page 222

Chapter 11

Cost Concepts and Conundrums

In This Chapter

Determining costs: The second most important thing accountants do

Appreciating the different needs for cost information

Contrasting costs for understanding them better

Determining product cost for manufacturers

Padding profit by manufacturing too many products

M

easuring costs is the second most important thing accountants do,

right after measuring profit. (Well, the Internal Revenue Service might

think that measuring taxable income is the most important.) But really, can

measuring a cost be very complicated? You just take numbers off a purchase

invoice and call it a day, right? Not if your business manufactures the products

you sell — that’s for sure! In this chapter, I demonstrate that a cost, any cost,

is not as obvious and clear-cut as you may think. Yet, obviously, costs are

extremely important to businesses and other organizations.

Consider an example close to home: Suppose you just returned from the gro-

cery store with several items in the bag. What’s the cost of the loaf of bread you

bought? Should you include the sales tax? Should you include the cost of gas

you used driving to the store? Should you include some amount of depreciation

expense on your car? Suppose you returned some aluminum cans for recycling

while you were at the grocery store, and you were paid a small amount for the

cans. Should you subtract this amount against the total cost of your purchases?

Or should you subtract the amount directly against the cost of only the sodas in

aluminum cans that you bought? And, is cost the before-tax cost? In other

words, is your cost equal to the amount of income you had to earn before

income tax so that you had enough after-tax income to buy the items?

These questions about the cost of your groceries are interesting (well, to me

at least). But you don’t really have to come up with definite answers for such

questions in managing your personal financial affairs. Individuals don’t have

to keep cost records of their personal expenditures, other than what’s needed

for their annual income tax returns. In contrast, businesses must carefully record

all their costs correctly so that profit can be determined each period, and so that

managers have the information they need to make decisions and to make a

profit.

17_246009 ch11.qxp 4/17/08 12:50 AM Page 223

224

Part III: Accounting in Managing a Business

Looking down the Road to

the Destination of Costs

All businesses that sell products must know their product costs — in other

words, the costs of each and every item they sell. Companies that manufac-

ture the products they sell — as opposed to distributors and retailers of

products — have many problems in figuring out their product costs. Two

examples of manufactured products are a new Cadillac just rolling off the

assembly line at General Motors and a copy of my book, Accounting For

Dummies, 4th Edition, hot off the printing presses.

Most production (manufacturing) processes are fairly complex, so product cost

accounting for manufacturers is fairly complex; every step in the production

process has to be tracked carefully from start to finish. Many manufacturing

costs cannot be directly matched with particular products; these are called indi-

rect costs. To arrive at the full cost of each product manufactured, accountants

devise methods for allocating indirect production costs to specific products.

Surprisingly, generally accepted accounting principles (GAAP) provide very

little authoritative guidance for measuring product cost. Therefore, manufactur-

ing businesses have more than a little leeway regarding how to determine their

product costs. Even businesses in the same industry — Ford versus General

Motors, for example — may use different product cost accounting methods.

Accountants determine many other costs, in addition to product costs:

The costs of departments, regional distribution centers, and other

organizational units of the business

The cost of the retirement plan for the company’s employees

The cost of marketing programs and advertising campaigns

The cost of restructuring the business or the cost of a major recall of

products sold by the business, when necessary

A common refrain among accountants is “different costs for different purposes.”

True enough, but at its core, cost accounting serves two broad purposes: mea-

suring profit and providing relevant information to managers for planning,

control, and decision-making.

In my experience, people are inclined to take cost numbers for granted, as if

they were handed down on stone tablets. The phrase actual cost often gets

tossed around without a clear definition. An actual cost depends entirely on

the particular methods used to measure the cost. I can assure you that these

cost measurement methods have more in common with the scores from

judges in an ice skating competition than the times clocked in a Formula One

auto race. Many arbitrary choices are behind every cost number you see.

17_246009 ch11.qxp 4/17/08 12:50 AM Page 224

There’s no one-size-fits-all definition of cost, and there’s no one correct and

“best-in-all-circumstances” method of measuring cost.

The conundrum is that, in spite of the inherent ambiguity in determining

costs, we need exact amounts for costs. In order to understand the income

statement and balance sheet that managers use in making their decisions, they

need to understand a little bit about the choices an accountant has to make in

measuring costs. Some cost accounting methods result in conservative profit

numbers; other methods boost profit, at least in the short run.

This chapter covers cost concepts and cost measurement methods that apply to

all businesses, as well as basic product cost accounting of manufacturers. I dis-

cuss how a manufacturer could be fooling around with its production output to

manipulate product cost for the purpose of artificially boosting its profit figure.

(Service businesses encounter their own problems in allocating their operating

costs for assessing the profitability of their separate sales revenue sources.)

Are Costs Really That Important?

Without good cost information, a business operates in the dark. Cost data is

needed for the following purposes:

Setting sales prices: The common method for setting sales prices (known

as cost-plus or markup on cost) starts with cost and then adds a certain

percentage. If you don’t know exactly how much a product costs, you

can’t be as shrewd and competitive in your pricing as you need to be.

Even if sales prices are dictated by other forces and not set by managers,

managers need to compare sales prices against product costs and other

costs that should be matched against each sales revenue source.

Formulating a legal defense against charges of predatory pricing prac-

tices: Many states have laws prohibiting businesses from selling below

cost except in certain circumstances. And a business can be sued under

federal law for charging artificially low prices intended to drive its com-

petitors out of business. Be prepared to prove that your lower pricing is

based on lower costs and not on some illegitimate purpose.

Measuring gross margin: Investors and managers judge business perfor-

mance by the bottom-line profit figure. This profit figure depends on the

gross margin figure you get when you subtract your cost of goods sold

expense from your sales revenue. Gross margin (also called gross profit) is

the first profit line in the income statement (see Figures 4-1 and 9-1, as

well as Figure 11-1 later in this chapter, for examples). If gross margin is

wrong, bottom-line net income is wrong — no two ways about it. The cost

of goods sold expense depends on having correct product costs (see

“Assembling the Product Cost of Manufacturers” later in this chapter).

225

Chapter 11: Cost Concepts and Conundrums

17_246009 ch11.qxp 4/17/08 12:50 AM Page 225

Valuing assets: The balance sheet reports cost values for many (though

not all) assets. To understand the balance sheet you should understand

the cost basis of its inventory and certain other assets. See Chapter 5 for

more about assets and how asset values are reported in the balance

sheet (also called the statement of financial condition).

Making optimal choices: You often must choose one alternative over

others in making business decisions. The best alternative depends heav-

ily on cost factors, and you have to be careful to distinguish relevant

costs from irrelevant costs, as I describe in the section “Relevant versus

irrelevant costs,” later in this chapter.

In most situations, the book value of a fixed asset is an irrelevant cost. Say

book value is $35,000 for a machine used in the manufacturing operations

of the business. This is the amount of original cost that has not yet been

charged to depreciation expense since it was acquired, and it may seem

quite relevant. However, in deciding between keeping the old machine or

replacing it with a newer, more efficient machine, the disposable value of

the old machine is the relevant amount, not the undepreciated cost bal-

ance of the asset. Suppose the old machine has only a $20,000 salvage

value at this time; this is the relevant cost for the alternative of keeping it

for use in the future — not the $35,000 that hasn’t been depreciated yet. In

order to keep using it, the business forgoes the $20,000 it could get by sell-

ing the asset, and this $20,000 is the relevant cost in this decision situation.

Making decisions involves looking forward at the future cash flows of each

alternative — not looking backward at historical-based cost values.

Becoming More Familiar with Costs

The following sections explain important cost distinctions that managers

should understand in making decisions and exercising control. Also, these cost

distinctions help managers better appreciate the cost figures that accountants

attach to products that are manufactured or purchased by the business.

Retailers (such as Wal-Mart or Costco) purchase products in a condition ready

for sale to their customers — although the products have to be removed from

shipping containers, and a retailer does a little work making the products

presentable for sale and putting the products on display. Manufacturers don’t

have it so easy; their product costs have to be “manufactured” in the sense that

the accountants have to accumulate various production costs and compute

the cost per unit for every product manufactured. I focus on the special cost

concerns of manufacturers in the upcoming section “Assembling the Product

Cost of Manufacturers.”

226

Part III: Accounting in Managing a Business

17_246009 ch11.qxp 4/17/08 12:50 AM Page 226

227

Chapter 11: Cost Concepts and Conundrums

Accounting versus economic costs

Accountants focus mainly on

actual costs

(though they disagree regarding how exactly to

measure these costs). Actual costs are rooted

in the actual, or historical, transactions and

operations of a business. Accountants also

determine

budgeted costs

for businesses that

prepare budgets (see Chapter 10), and they

develop

standard costs

that serve as yardsticks

to compare with the actual costs of a business.

Other concepts of cost are found in economic

theory

.

You encounter a variety of economic

cost terms when reading

The Wall Street

Journal,

as well as in many business discus-

sions and deliberations. Don’t reveal your igno-

rance of the following cost terms:

Opportunity cost: The amount of income (or

other measurable benefit) given up when

you follow a better course of action. For

example, say that you quit your $50,000 job,

invest $200,000 to start a new business, and

end up netting $80,000 in your new business

for the year. Suppose also that you would

have earned 5 percent on the $200,000 (a

total of $10,000) if you’d kept the money in

whatever investment you took it from. So

you gave up a $50,000 salary and $10,000 in

investment income with your course of

action; your opportunity cost is $60,000.

Subtract that figure from what your actual

course of action netted you — $80,000 —

and you end up with a “real” economic

profit of $20,000. Your income is $20,000

better by starting your new business

according to economic theory.

Marginal cost: The

incremental,

out-of-

pocket outlay required for taking a particu-

lar course of action. Generally speaking, it’s

the same thing as a

variable

cost (see

“Fixed versus variable costs,” later in this

chapter). Marginal costs are important, but

in actual practice managers must recover

fixed (or nonmarginal) costs as well as mar-

ginal costs through sales revenue in order

to remain in business for any extent of time.

Marginal costs are most relevant for ana-

lyzing one-time ventures, which don’t last

over the long-term.

Replacement cost: The estimated amount it

would take today to purchase an asset that

the business already owns. The longer ago

an asset was acquired, the more likely its

current replacement cost is higher than its

original cost. Economists are of the opinion

that current replacement costs are relevant

in making rational economic decisions. For

insuring assets against fire, theft, and nat-

ural catastrophes, the current replacement

costs of the assets are clearly relevant.

Other than for insurance, however, replace-

ment costs are not on the front burners of

decision-making — except in situations in

which one alternative being seriously con-

sidered actually involves replacing assets.

Imputed cost: An ideal, or hypothetical, cost

number that is used as a benchmark or yard-

stick against which actual costs are com-

pared. Two examples are

standard costs

and

the

cost of capital.

Standard costs are set in

advance for the manufacture of products

during the coming period, and then actual

costs are compared against standard costs

to identify significant variances. The cost of

capital is the weighted average of the inter-

est rate on debt capital and a target rate of

return that should be earned on equity capi-

tal. The

economic value added

(EVA) method

compares a business’s cost of capital

against its actual return on capital, to deter-

mine whether the business did better or

worse than the benchmark.

For the most part, these types of cost aren’t

reflected in financial reports. I’ve included them

here to familiarize you with terms you’re likely

to see in the financial press and hear on finan-

cial talk shows. Business managers toss these

terms around a lot.

17_246009 ch11.qxp 4/17/08 12:50 AM Page 227

I cannot exaggerate the importance of correct product costs (for businesses

that sell products, of course). The total cost of goods (products) sold is the first,

and usually the largest, expense deducted from sales revenue in measur

ing profit.

The bottom-line profit amount reported in a business’s income statement depends

heavily on whether its product costs have been measured properly during that

period. Also, keep in mind that product cost is the value for the inventory asset

reported in the balance sheet of a business. (For a balance sheet example see

Figure 5-2.)

Direct versus indirect costs

You might say that the starting point for any sort of cost analysis, and particu-

larly for accounting for the product costs of manufacturers, is to clearly distin-

guish between direct and indirect costs. Direct costs are easy to match with a

process or product, whereas indirect costs are more distant and have to be

allocated to a process or product. Here are more details:

Direct costs: Can be clearly attributed to one product or product line, or

one source of sales revenue, or one organizational unit of the business,

or one specific operation in a process. An example of a direct cost in the

book publishing industry is the cost of the paper that a book is printed

on; this cost can be squarely attached to one particular phase of the

book production process.

Indirect costs: Are far removed from and cannot be naturally attached

to specific products, organizational units, or activities. A book pub-

lisher’s phone bill is a cost of doing business but can’t be tied down to

just one step in the book editorial and production process. The salary of

the purchasing officer who selects the paper for all the books is another

example of a cost that is indirect to the production of particular books.

Each business must determine a method of allocating indirect costs to dif-

ferent products, sources of sales revenue, organizational units, and so on.

Most allocation methods are far from perfect and, in the final analysis, end

up being arbitrary to one degree or another. Business managers should

always keep an eye on the allocation methods used for indirect costs and

take the cost figures produced by these methods with a grain of salt. If I

were called in as an expert witness in a court trial involving costs, the first

thing I’d do is critically analyze the allocation methods used by the busi-

ness for its indirect costs. If I were on the side of the defendant, I’d do my

best to defend the allocation methods. If I were on the side of the plaintiff,

I’d do my best to discredit the allocation methods — there are always

grounds for criticism.

228

Part III: Accounting in Managing a Business

17_246009 ch11.qxp 4/17/08 12:50 AM Page 228

The cost of filling the gas tank as I drive from Denver to San Diego and back

to consult with my coauthor and son, Tage, about the book we wrote

together, Small Business Financial Management Kit For Dummies (Wiley), is a

direct cost of making the trip. The annual auto license plate fee that I pay to

the state of Colorado is an indirect cost of the trip, although it is a direct cost

of having the car available during the year.

Fixed versus variable costs

If your business sells 100 more units of a certain item, some of your costs

increase accordingly, but others don’t budge one bit. This distinction

between variable and fixed costs is crucial:

Variable costs: Increase and decrease in proportion to changes in sales

or production level. Variable costs generally remain the same per unit of

product, or per unit of activity. Additional units manufactured or sold

cause variable costs to increase in concert. Fewer units manufactured or

sold result in variable costs going down in concert.

Fixed costs: Remain the same over a relatively broad range of sales volume

or production output. Fixed costs are like a dead weight on the business.

Its total fixed costs for the period are a hurdle it must overcome by selling

enough units at high enough margins per unit in order to avoid a loss and

move into the profit zone. (Chapter 9 explains the break-even point, which

is the level of sales needed to cover fixed costs for the period.)

Note: The distinction between variable and fixed costs is essential for under-

standing and analyzing profit behavior, which I explain in Chapter 9.

Relevant versus irrelevant costs

Not every cost is important to every decision a manager needs to make.

Hence the distinction between relevant and irrelevant costs:

Relevant costs: Costs that should be considered and included in your

analysis when deciding on a future course of action. Relevant costs are

future costs — costs that you would incur, or bring upon yourself, depend-

ing on which course of action you take. For example, say that you want to

increase the number of books that your business produces next year in

order to increase your sales revenue, but the cost of paper has just shot

up. Should you take the cost of paper into consideration? Absolutely —

that cost will affect your bottom-line profit and may negate any increase

in sales volume that you experience (unless you increase the sales

price). The cost of paper is a relevant cost.

229

Chapter 11: Cost Concepts and Conundrums

17_246009 ch11.qxp 4/17/08 12:50 AM Page 229