Tracy John A. Accounting for Dummies

Подождите немного. Документ загружается.

Irrelevant (or sunk) costs: Costs that should be disregarded when deciding

on a future course of action; if brought into the analysis, these costs could

cause you to make the wrong decision. An irrelevant cost is a vestige of the

past — that money is gone. For this reason, irrelevant costs are also called

sunk costs. For example, suppose that your supervisor tells you to expect a

slew of new hires next week. All your staff members use computers now,

but you have a bunch of typewriters gathering dust in the supply room.

Should you consider the cost paid for those typewriters in your decision to

buy computers for all the new hires? Absolutely not — that cost should

have been written off and is no match for the cost you’d pay in productivity

(and morale) for new employees who are forced to use typewriters.

Generally speaking, fixed costs are irrelevant when deciding on a future course

of action, assuming that they’re truly fixed and can’t be increased or decreased

over the short term. Most variable costs are relevant because they depend

on which alternative is selected.

Although fixed costs themselves are usually irrelevant in decision making, these

costs often indicate something about a business’s capacity — how much building

space it has, how many machine-hours are available for use, how many hours of

labor can be worked, and so on. Managers have to figure out the best way to uti-

lize these capacities. For example, suppose your retail business pays an annual

building rent of $200,000, which is a fixed cost (unless the rental contract with the

landlord has a rent escalation clause based on sales revenue). The rent, which

gives the business the legal right to occupy the building, provides 15,000 square

feet of retail and storage space. You should figure out which sales mix of products

will generate the highest total margin — equal to total sales revenue less total

variable costs of making the sales, including the costs of the goods sold and all

variable costs driven by sales revenue and sales volume.

Actual, budgeted, and standard costs

The actual costs a business incurs may differ (though we hope not significantly)

from its budgeted and standard costs:

Actual costs: Historical costs, based on actual transactions and operations

for the period just ended, or going back to earlier periods. Financial state-

ment accounting is mainly (though not entirely) based on a business’s

actual transactions and operations; the basic approach to determining

annual profit is to record the financial effects of actual transactions and

allocate historical costs to the periods benefited by the costs.

Budgeted costs: Future costs, for transactions and operations expected

to take place over the coming period, based on forecasts and established

goals. Fixed costs are budgeted differently than variable costs. For example,

if sales volume is forecast to increase by 10 percent, variable costs will

definitely increase accordingly, but fixed costs may or may not need to be

230

Part III: Accounting in Managing a Business

17_246009 ch11.qxp 4/17/08 12:50 AM Page 230

increased to accommodate the volume increase. In Chapter 10, I explain

the budgeting process and budgeted financial statements.

Standard costs: Costs, primarily in the area of manufacturing, that are

carefully engineered based on detailed analysis of operations and forecast

costs for each component or step in an operation. Developing standard costs

for variable production costs is relatively straightforward because most are

direct costs. In contrast, most fixed costs are indirect, and standard costs for

fixed costs are necessarily based on more arbitrary methods (see “Direct

versus indirect costs,” earlier in this chapter). Note: Some variable costs

are indirect and have to be allocated to specific products in order to come

up with a full (total) standard cost of the product.

Product versus period costs

Some costs are linked to particular products, and others are not:

Product costs: Manufacturing costs attached directly or allocated to

particular products. The cost is recorded in the inventory asset account

and stays in that asset account until the product is sold, at which time

the cost goes into the cost of goods sold expense account. (See Chapters 4

and 5 for more about these accounts; also, see Chapter 7 for alternative

methods for selecting which product costs are first charged to the cost of

goods sold expense.)

For example, the cost of a new Ford Focus sitting on a car dealer’s show-

room floor is a product cost. The dealer keeps the cost in the inventory

asset account until you buy the car, at which point the dealer charges

the cost to the cost of goods sold expense.

Period costs: Costs that are not attached to particular products. These

costs do not spend time in the “waiting room” of inventory. Period costs

are recorded as expenses immediately; unlike product costs, period costs

don’t pass through the inventory account first. Advertising costs, for

example, are accounted for as period costs and recorded immediately in

an expense account. Also, research and development costs are treated as

period costs (with some exceptions).

Separating product costs and period costs is particularly important for

manufacturing businesses, as you find out in the following section.

231

Chapter 11: Cost Concepts and Conundrums

17_246009 ch11.qxp 4/17/08 12:50 AM Page 231

Assembling the Product Cost

of Manufacturers

Businesses that manufacture products have several additional cost problems

to deal with, compared with retailers and distributors. I use the term manufac-

ture in the broadest sense: Automobile makers assemble cars, beer companies

brew beer, automobile gasoline companies refine oil, DuPont makes products

through chemical synthesis, and so on. Retailers (also called merchandisers)

and distributors, on the other hand, buy products in a condition ready for

resale to the end consumer. For example, Levi Strauss manufactures clothing,

and Macy’s is a retailer that buys from Levi Strauss and sells the clothes to the

public. The following sections describe costs unique to manufacturers.

Minding manufacturing costs

Manufacturing costs consist of four basic types:

Raw materials (also called direct materials): What a manufacturer buys

from other companies to use in the production of its own products. For

example, General Motors buys tires from Goodyear (or other tire manu-

facturers) that then become part of GM’s cars.

Direct labor: The employees who work on the production line.

Variable overhead: Indirect production costs that increase or decrease as

the quantity produced increases or decreases. An example is the cost of

electricity that runs the production equipment: You pay for the electricity

for the whole plant, not machine by machine, so you can’t attach this cost

to one particular part of the process. But if you increase or decrease the

use of those machines, the electricity cost increases or decreases accord-

ingly. (In contrast, the monthly utility bill for a company’s office and sales

space probably is fixed for all practical purposes.)

Fixed overhead: Indirect production costs that do not increase or

decrease as the quantity produced increases or decreases. These fixed

costs remain the same over a fairly broad range of production output

levels (see “Fixed versus variable costs,” earlier in this chapter). Three

significant fixed manufacturing costs are

• Salaries for certain production employees who don’t work directly

on the production line, such as a vice president, safety inspectors,

security guards, accountants, and shipping and receiving workers.

• Depreciation of production buildings, equipment, and other manu-

facturing fixed assets.

• Occupancy costs, such as building insurance, property taxes, and

heating and lighting charges.

232

Part III: Accounting in Managing a Business

17_246009 ch11.qxp 4/17/08 12:50 AM Page 232

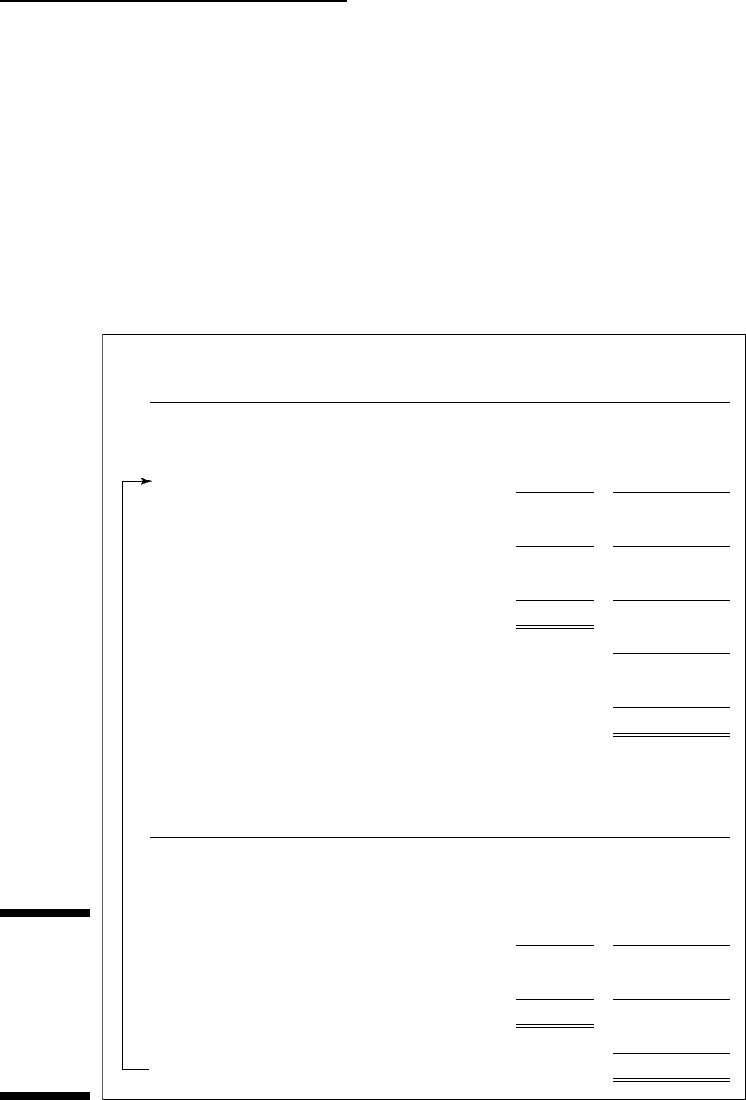

Figure 11-1 presents an annual income statement for a manufacturer and

includes information about its manufacturing costs for the year. The cost of

goods sold expense depends directly on the product cost from the summary

of manufacturing costs that appears below the income statement. A business

may manufacture 100 or 1,000 different products, or even more, and the busi-

ness must prepare a summary of manufacturing costs for each product. To

keep our example easy to follow (but still realistic), Figure 11-1 presents a sce-

nario for a one-product manufacturer. The multi-product manufacturer has

some additional accounting problems, but I can’t provide that level of detail

here. This example illustrates the fundamental accounting problems and

methods of all manufacturers.

Income Statement for Year

Sales volume 110,000 units

Per Unit

Per Unit

Totals

Sales revenue $1,400 $154,000,000

Cost of goods sold expense (760) (83,600,000)

Gross margin $640 $70,400,000

Variable operating expenses (300) (33,000,000)

Margin $340 $37,400,000

Fixed operating expenses (195) (21,450,000)

Earnings before interest and income tax (EBIT) $145 $15,950,000

Interest expense (2,750,000)

Earnings before income tax $13,200,000

Income tax expense (4,488,000)

Net income $8,712,000

Manufacturing Costs for Year

Production capacity 150,000 units

Actual output 120,000 units

Production Cost Components

Totals

Raw materials $215 $25,800,000

Direct labor 125 15,000,000

Variable manufacturing overhead costs 70 8,400,000

Total variable manufacturing costs $410 $49,200,000

Fixed manufacturing overhead costs 350 42,000,000

Total manufacturing costs $760 $91,200,000

To 10,000 units inventory increase (7,600,000)

To 110,000 units sold $83,600,000

Figure 11-1:

Example for

determining

the product

cost of

a manu-

facturer.

233

Chapter 11: Cost Concepts and Conundrums

17_246009 ch11.qxp 4/17/08 12:50 AM Page 233

The information in the manufacturing costs summary below the income

statement (see Figure 11-1) is highly confidential and for management eyes

only. Competitors would love to know this information. A company may

enjoy a significant cost advantage over its competitors and definitely does

not want its cost data to get into their hands.

Classifying costs properly

Two vexing issues rear their ugly heads in determining product cost for a

manufacturer:

Drawing a bright line between manufacturing costs and non-

manufacturing operating costs: The key difference here is that manufac-

turing costs are categorized as product costs, whereas non-manufacturing

operating costs are categorized as period costs (refer to “Product versus

period costs,” earlier in this chapter). In calculating product costs, you

include only manufacturing costs and not other costs. Period costs are

recorded right away as expenses — either in variable operating expenses

or fixed operating expenses (see Figure 11-1). Here are some examples of

each type of cost:

• Wages paid to production line workers are a clear-cut example of a

manufacturing cost.

• Salaries paid to salespeople are a marketing cost and are not part

of product cost; marketing costs are treated as period costs, which

means they are recorded immediately to expense of the period.

• Depreciation on production equipment is a manufacturing cost,

but depreciation on the warehouse in which products are stored

after being manufactured is a period cost.

• Moving the raw materials and partially-completed products through

the production process is a manufacturing cost, but transporting the

finished products from the warehouse to customers is a period cost.

The accumulation of direct and indirect production costs starts at the

beginning of the manufacturing process and stops at the end of the produc-

tion line. In other words, product cost stops at the end of the production

line — every cost up to that point should be included as a manufacturing

cost.

If you misclassify some manufacturing costs as operating costs, your

product cost calculation will be too low (see the following section,

“Calculating product cost”). Also, the Internal Revenue Service may come

knocking at your door if it suspects that you deliberately (or even inno-

cently) misclassified manufacturing costs as non-manufacturing costs in

order to minimize your taxable income.

234

Part III: Accounting in Managing a Business

17_246009 ch11.qxp 4/17/08 12:50 AM Page 234

Allocating indirect costs among different products: Indirect manufac-

turing costs must be allocated among the products produced during

the period. The full product cost includes both direct and indirect

manufacturing costs. Creating a completely satisfactory allocation

method is difficult; the process ends up being somewhat arbitrary, but

it must be done to determine product cost. Managers should understand

how indirect manufacturing costs are allocated among products (and,

for that matter, how indirect non-manufacturing costs are allocated

among organizational units and profit centers). Managers should also

keep in mind that every allocation method is arbitrary and that a different

allocation method may be just as convincing. (See the sidebar “Allocating

indirect costs is as simple as ABC — not!”)

235

Chapter 11: Cost Concepts and Conundrums

Allocating indirect costs is

as simple as ABC — not!

Accountants for manufacturers have developed

many methods and schemes for allocating indi-

rect overhead costs, most of which are based

on a common denominator of production activ-

ity, such as direct labor hours or machine hours.

A different method has received a lot of press

recently:

activity-based costing

(ABC).

With the ABC method, you identify each sup-

porting activity in the production process and

collect costs into a separate pool for each iden-

tified activity. Then you develop a

measure

for

each activity — for example, the measure for the

engineering department may be hours, and the

measure for the maintenance department may

be square feet. You use the activity measures as

cost drivers

to allocate costs to products.

The idea is that the engineering department

doesn’t come cheap; including the cost of their

slide rules and pocket protectors, as well as their

salaries and benefits, the total cost per hour for

those engineers could be $200 or more. The logic

of the ABC cost-allocation method is that the

engineering cost per hour should be allocated on

the basis of the number of hours (the driver)

required by each product. So if Product A needs

200 hours of the engineering department’s time

and Product B is a simple product that needs only

20 hours of engineering, you allocate ten times as

much of the engineering cost to Product A. In

similar fashion, suppose the cost of the mainte-

nance department is $20 per square foot per year.

If Product C uses twice as much floor space as

Product D, it would be charged with twice as

much maintenance cost.

The ABC method has received much praise for

being better than traditional allocation methods,

especially for management decision making.

But keep in mind that this method still requires

rather arbitrary definitions of cost drivers, and

having too many different cost drivers, each

with its own pool of costs, is not too practical.

Cost allocation always involves arbitrary meth-

ods. Managers should be aware of which meth-

ods are being used and should challenge a

method if they think that it’s misleading and

should be replaced with a better (though still

somewhat arbitrary) method. I don’t mean to put

too fine a point on this, but cost allocation

essentially boils down to a “my arbitrary method

is better than your arbitrary method” argument.

17_246009 ch11.qxp 4/17/08 12:50 AM Page 235

Calculating product cost

The basic equation for calculating product cost is as follows (using the exam-

ple of the manufacturer given in Figure 11-1):

$91,200,000 total manufacturing costs ÷ 120,000 units

production output = $760 product cost per unit

Looks pretty straightforward, doesn’t it? Well, the equation itself may be

simple, but the accuracy of the results depends directly on the accuracy of

your manufacturing cost numbers. The business example we’re using in this

chapter manufactures just one product. Even so, a single manufacturing

process can be fairly complex, with hundreds or thousands of steps and

operations. In the real world, where businesses produce multiple products,

your accounting systems must be very complex and extraordinarily detailed

to keep accurate track of all direct and indirect (allocated) manufacturing

costs.

In our example, the business manufactured 120,000 units and sold 110,000

units during the year, and its product cost per unit is $760. The 110,000 total

units sold during the year is multiplied by the $760 product cost to compute

the $83.6 million cost of goods sold expense, which is deducted against the

company’s revenue from selling 110,000 units during the year. The company’s

total manufacturing costs for the year were $91.2 million, which is $7.6 mil-

lion more than the cost of goods sold expense. The remainder of the total

annual manufacturing costs is recorded as an increase in the company’s

inventory asset account, to recognize that 10,000 units manufactured this

year are awaiting sale in the future. In Figure 11-1, note that the $760 product

cost per unit is applied both to the 110,000 units sold and to the 10,000 units

added to inventory.

Note: The product cost per unit for our example business is determined for

the entire year. In actual practice, manufacturers calculate their product

costs monthly or quarterly. The computation process is the same, but the

frequency of doing the computation varies from business to business.

Product costs likely will vary each successive period the costs are deter-

mined. Because the product costs vary from period to period, the business

must choose which cost of goods sold and inventory cost method to use. (If

product cost happened to remain absolutely flat and constant period to

period, the different methods would yield the same results.) Chapter 7

explains the alternative accounting methods for determining cost of goods

sold expense and inventory cost value.

236

Part III: Accounting in Managing a Business

17_246009 ch11.qxp 4/17/08 12:50 AM Page 236

Examining fixed manufacturing

costs and production capacity

Product cost consists of two very distinct components: variable manufacturing

costs and fixed manufacturing costs. In Figure 11-1, note that the company’s

variable manufacturing costs are $410 per unit, and its fixed manufacturing

costs are $350 per unit. Now, what if the business had manufactured ten more

units? Its total variable manufacturing costs would have been $4,100 higher.

The actual number of units produced drives variable costs, so even one more

unit would have caused the variable costs to increase. But the company’s total

fixed costs would have been the same if it had produced ten more units, or

10,000 more units for that matter. Variable manufacturing costs are bought on a

per-unit basis, as it were, whereas fixed manufacturing costs are bought in bulk

for the whole period.

Fixed manufacturing costs are needed to provide production capacity — the

people and physical resources needed to manufacture products — for the

period. After the business has the production plant and people in place for

the year, its fixed manufacturing costs cannot be easily scaled down. The

business is stuck with these costs over the short run. It has to make the best

use it can from its production capacity.

Production capacity is a critical concept for business managers to stay focused

on. You need to plan your production capacity well ahead of time because you

need plenty of lead-time to assemble the right people, equipment, land, and

buildings. When you have the necessary production capacity in place, you want

to make sure that you’re making optimal use of that capacity. The fixed costs of

production capacity remain the same even as production output increases or

decreases, so you may as well make optimal use of the capacity provided by

those fixed costs. For example, you’re recording the same depreciation amount

on your machinery regardless of how you actually use those machines, so you

should be sure to optimize the use of those machines (within limits, of course —

overworking the machines to the point where they break down won’t do you

much good).

The burden rate

The fixed cost component of product cost is called the burden rate. In our man-

ufacturing example, the burden rate is computed as follows (see Figure 11-1

for data):

$42,000,000 fixed manufacturing costs for period ÷

120,000 units production output for period =

$350 burden rate

Note that the burden rate depends on the number divided into total fixed

manufacturing costs for the period — that is, the production output for the

period.

237

Chapter 11: Cost Concepts and Conundrums

17_246009 ch11.qxp 4/17/08 12:50 AM Page 237

Now, here’s a very important twist on my example: Suppose the company

had manufactured only 110,000 units during the period — equal exactly to

the quantity sold during the year. Its variable manufacturing cost per unit

would have been the same, or $410 per unit. But its burden rate would have

been $381.82 per unit (computed by dividing the $42 million total fixed manu-

facturing costs by the 110,000 units production output). Each unit sold, there-

fore, would have cost $31.82 more simply because the company produced

fewer units. (The burden rate is $381.82 at the 110,000 output level but only

$350 at the 120,000 output level.)

If only 110,000 units were produced, the company’s product cost would have

been $791.82 ($410 variable costs plus the $381.82 burden rate). The com-

pany’s cost of goods sold, therefore, would have been $3.5 million higher for

the year ($31.82 higher product cost × 110,000 units sold). This rather signifi-

cant increase in its cost of goods sold expense is caused by the company pro-

ducing fewer units, even though it produced all the units that it needed for

sales during the year. The same total amount of fixed manufacturing costs is

spread over fewer units of production output.

Idle capacity

The production capacity of the business example in Figure 11-1 is 150,000 units

for the year. However, this business produced only 120,000 units during the

year, which is 30,000 units fewer than it could have. In other words, it operated

at 80 percent of production capacity, which is 20 percent idle capacity:

120,000 units output ÷ 150,000 units capacity =

80% utilization, or 20% idle capacity

This rate of idle capacity isn’t unusual — the average U.S. manufacturing

plant normally operates at 80 to 85 percent of its production capacity.

The effects of increasing inventory

Looking back at the numbers shown in Figure 11-1, the company’s cost of

goods sold benefited from the fact that it produced 10,000 more units than it

sold during the year. These 10,000 units absorbed $3.5 million of its total

fixed manufacturing costs for the year, and until the units are sold this $3.5

million stays in the inventory asset account (along with the variable manufac-

turing costs, of course). It’s entirely possible that the higher production level

was justified — to have more units on hand for sales growth next year. But

production output can get out of hand, as I discuss in the following section,

“Puffing Profit by Excessive Production.”

238

Part III: Accounting in Managing a Business

17_246009 ch11.qxp 4/17/08 12:50 AM Page 238

Managers (and investors as well) should understand the inventory increase

effects caused by manufacturing more units than are sold during the year. In the

example shown in Figure 11-1, the cost of goods sold expense escaped $3.5 million

of fixed manufacturing costs because the company produced 10,000 more

units than it sold during the year, thus pushing down the burden rate. The

company’s cost of goods sold expense would have been $3.5 million higher if

it had produced just the number of units it sold during the year. The lower

output level would have increased cost of goods sold expense and would

have caused a $3.5 million drop in gross margin and earnings before income

tax. Indeed, earnings before income tax would have been 27 percent lower

($3.5 million ÷ $13.2 million = 27 percent decrease).

239

Chapter 11: Cost Concepts and Conundrums

The actual costs/actual output method

and when not to use it

The product cost calculation for the business

example shown in Figure 11-1 is based on the

actual cost/actual output method,

in which you

take your actual costs — which may have been

higher or lower than the budgeted costs for the

year — and divide by the actual output for the year.

The actual costs/actual output method is appro-

priate in most situations. However, this method

is not appropriate and would have to be modi-

fied in two extreme situations:

Manufacturing costs are grossly excessive

or wasteful due to inefficient production

operations: For example, suppose that the

business represented in Figure 11-1 had to

throw away $1.2 million of raw materials

during the year. The $1.2 million should be

removed from the calculation of the raw

material cost per unit. Instead, you treat it as

a period cost — meaning that you take it

directly into expense. Then the cost of goods

sold expense would be based on $750 per

unit instead of $760, which lowers this

expense by $1.1 million (based on the 110,000

units sold). But you still have to record the

$1.2 million expense for wasted raw materi-

als, so EBIT would be $100,000 lower.

Production output is significantly less than

normal capacity utilization: Suppose that the

Figure 11-1 business produced only 75,000

units during the year but still sold 110,000

units because it was working off a large

inventory carryover from the year before.

Then its production output would be 50 per-

cent instead of 80 percent of capacity. In a

sense, the business wasted half of its pro-

duction capacity, and you can argue that half

of its fixed manufacturing costs should be

charged directly to expense on the income

statement and not included in the calculation

of product cost.

17_246009 ch11.qxp 4/17/08 12:50 AM Page 239