Tracy John A. Accounting for Dummies

Подождите немного. Документ загружается.

Puffing Profit by Excessive Production

Whenever production output is higher than sales volume, be on guard.

Excessive production can puff up the profit figure. How? Until a product is sold,

the product cost goes in the inventory asset account rather than the cost of

goods sold expense account, meaning that the product cost is counted as a

positive number (an asset) rather than a negative number (an expense). Fixed

manufacturing overhead cost is included in product cost, which means that

this cost component goes into inventory and is held there until the products

are sold later. In short, when you overproduce, more of your total of fixed man-

ufacturing costs for the period is moved to the inventory asset account and

less is moved into cost of goods sold expense for the year.

You need to judge whether an inventory increase is justified. Be aware that

an unjustified increase may be evidence of profit manipulation or just good

old-fashioned management bungling. Either way, the day of reckoning will

come when the products are sold and the cost of inventory becomes cost of

goods sold expense — at which point the cost impacts the bottom line.

Shifting fixed manufacturing

costs to the future

The business represented in Figure 11-1 manufactured 10,000 more units than

it sold during the year. With variable manufacturing costs at $410 per unit,

the business expended $4.1 million more in variable manufacturing costs

than it would have if it had produced only the 110,000 units needed for its

sales volume. In other words, if the business had produced 10,000 fewer

units, its variable manufacturing costs would have been $4.1 million less —

that’s the nature of variable costs. In contrast, if the company had manufac-

tured 10,000 fewer units, its fixed manufacturing costs would not have been

any less — that’s the nature of fixed costs.

Of its $42 million total fixed manufacturing costs for the year, only $38.5 mil-

lion ended up in the cost of goods sold expense for the year ($350 burden

rate × 110,000 units sold). The other $3.5 million ended up in the inventory

asset account ($350 burden rate × 10,000 units inventory increase). The $3.5

million of fixed manufacturing costs that are absorbed by inventory is shifted

to the future. This amount will not be expensed (charged to cost of goods

sold expense) until the products are sold sometime in the future.

Shifting part of the fixed manufacturing cost for the year to the future may

seem to be accounting slight of hand. It has been argued that the entire

amount of fixed manufacturing costs should be expensed in the year that

240

Part III: Accounting in Managing a Business

17_246009 ch11.qxp 4/17/08 12:50 AM Page 240

these costs are recorded. (Only variable manufacturing costs would be

included in product cost for units going into the increase in inventory.)

Generally accepted accounting principles require that full product cost (variable

plus fixed manufacturing costs) be used for recording an increase in inventory.

However, as the example in Figure 11-1 shows, producing more than you sell

does boost profit.

Let me be very clear here: I’m not suggesting any hanky-panky in the example

shown in Figure 11-1. Producing 10,000 more units than sales volume during

the year looks — on the face of it — to be reasonable and not out of the ordi-

nary. Yet at the same time, it is naïve to ignore that the business did help its

pretax profit to the amount of $3.5 million by producing 10,000 more units than

it sold. If the business had produced only 110,000 units, equal to its sales volume

for the year, all its fixed manufacturing costs for the year would have gone into

cost of goods sold expense. The expense would have been $3.5 million higher,

and EBIT would have been that much lower.

Cranking up production output

Now let’s consider a more suspicious example. Suppose that the business

manufactured 150,000 units during the year and increased its inventory by

40,000 units. It may be a legitimate move if the business is anticipating a big

jump in sales next year. On the other hand, an inventory increase of 40,000

units in a year in which only 110,000 units were sold may be the result of a

serious overproduction mistake, and the larger inventory may not be needed

next year. In any case, Figure 11-2 shows what happens to production costs

and — more importantly — what happens to the profit lines at the higher

production output level.

The additional 30,000 units (over and above the 120,000 units manufactured

by the business in the original example) cost $410 per unit. (The precise cost

may be a little higher than $410 per unit because as you start crowding pro-

duction capacity, some variable costs per unit may increase a little.) The

business would need $12.3 million more for the additional 30,000 units of pro-

duction output:

$410 variable manufacturing cost per unit × 30,000

additional units produced = $12,300,000 additional

variable manufacturing costs invested in inventory

Again, its fixed manufacturing costs would not have increased, given the

nature of fixed costs. Fixed costs stay put until capacity is increased. Sales

volume, in this scenario, also remains the same.

241

Chapter 11: Cost Concepts and Conundrums

17_246009 ch11.qxp 4/17/08 12:50 AM Page 241

But check out the business’s EBIT in Figure 11-2: $23.65 million, compared with

$15.95 million in Figure 11-1 — a $7.7 million higher amount, even though sales

volume, sales prices, and operating costs all remain the same. Whoa! What’s

going on here? The simple answer is that the cost of goods sold expense is $7.7

million less than before. But how can cost of goods sold expense be less? The

business sells 110,000 units in both scenarios. And variable manufacturing

costs are $410 per unit in both cases.

Income Statement for Year

Sales volume 110,000 units

Totals

Sales revenue $1,400 $154,000,000

Cost of goods sold expense (690) (75,900,000)

Gross margin $710 $78,100,000

Variable operating expenses (300) (33,000,000)

Margin $410 $45,100,000

Fixed operating expenses (195) (21,450,000)

Earnings before interest and income tax (EBIT) $215 $23,650,000

Interest expense (2,750,000)

Earnings before income tax $20,900,000

Income tax expense (7,106,000)

Net income $13,794,000

Manufacturing Costs for Year

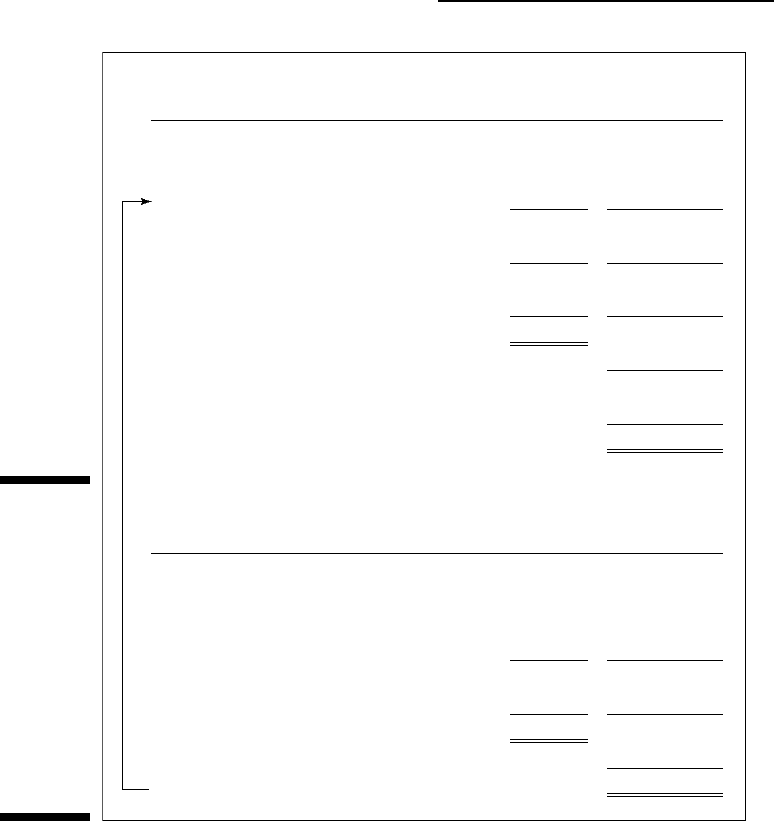

Production capacity 150,000 units

Actual output 150,000 units

Production Cost Components Per Unit

Per Unit

Totals

Raw materials $215 $32,250,000

Direct labor 125 18,750,000

Variable manufacturing overhead costs 70 10,500,000

Total variable manufacturing costs $410 $61,500,000

Fixed manufacturing overhead costs 280 42,000,000

Total manufacturing costs $690 $103,500,000

To 40,000 units inventory increase (27,600,000)

To 110,000 units sold $75,900,000

Figure 11-2:

Example in

which

production

output

greatly

exceeds

sales

volume for

the year,

thereby

boosting

profit for the

period.

242

Part III: Accounting in Managing a Business

17_246009 ch11.qxp 4/17/08 12:50 AM Page 242

The culprit is the burden rate component of product cost. In the Figure 11-1

example, total fixed manufacturing costs are spread over 120,000 units of

output, giving a $350 burden rate per unit. In the Figure 11-2 example, total

fixed manufacturing costs are spread over 150,000 units of output, giving a

much lower $280 burden rate, or $70 per unit less. The $70 lower burden rate

multiplied by the 110,000 units sold results in a $7.7 million lower cost of

goods sold expense for the period, a higher pretax profit of the same amount,

and a much improved bottom-line net income.

Being careful when production output

is out of kilter with sales volume

In the example shown in Figure 11-2, the business produced 150,000 units (full

capacity); therefore, its inventory asset absorbed $7.7 million of the company’s

fixed manufacturing costs for the year, and its cost of goods sold expense for

the year escaped this cost. But get this: Its inventory increased 40,000 units,

which is quite a large increase compared with the annual sales of 110,000 during

the year just ended. Who was responsible for the decision to go full blast and

produce up to production capacity? Do the managers really expect sales to jump

up enough next year to justify the much larger inventory level? If they prove to

be right, they’ll look brilliant. But if the output level was a mistake and sales do

not go up next year . . . they’ll have you-know-what to pay next year, even though

profit looks good this year. An experienced business manager knows to be on

guard when inventory takes such a big jump.

Summing up, the cost of goods sold expense of a manufacturer, and thus its

operating profit, is sensitive to a difference between its sales volume and pro-

duction output during the year. Manufacturing businesses do not generally

discuss or explain in their external financial reports to creditors and owners

why production output is different than sales volume for the year. Financial

report readers are pretty much on their own in interpreting the reasons for

and the effects of under- or over-producing products relative to actual sales

volume for the year. All I can tell you is to keep alert and keep in mind the

profit impact caused by a major disparity between a manufacturer’s produc-

tion output and sale levels for the year.

243

Chapter 11: Cost Concepts and Conundrums

17_246009 ch11.qxp 4/17/08 12:50 AM Page 243

244

Part III: Accounting in Managing a Business

17_246009 ch11.qxp 4/17/08 12:50 AM Page 244

Part IV

Preparing and

Using Financial

Reports

18_246009 pp04.qxp 4/17/08 12:03 AM Page 245

In this part . . .

F

inancial reports are like newspaper articles. A lot of

activity goes on behind the scenes that you may not

be aware of. In reading a financial report, you see only the

finished product. Chapter 12 gives the inside story of how

financial reports are put together.

Outside investors in a business — the owners who are not

on the inside managing the business — depend on its finan-

cial reports as their main source of information. Chapter 13

explains financial statement ratios that investors use for

interpreting profit performance and financial condition.

Serious investors must know these ratios.

The financial report is the end of the line for the outside

investors and lenders of a business. They can’t call the

business and ask for more information. But the financial

statements are just the starting point for the managers of

the business. Chapter 14 explains the more detailed and

highly confidential accounting information they need for

identifying problems and opportunities.

Chapter 15 explains the reasons for audits of financial

reports by independent CPAs. Investors and lenders defi-

nitely should read the auditor’s report, which is explained

in this chapter. The chapter also discusses the ugly topic

of accounting fraud. Unfortunately, some businesses resort

to accounting fraud, which is not only unethical but illegal.

18_246009 pp04.qxp 4/17/08 12:03 AM Page 246

Chapter 12

Getting a Financial Report

Ready for Release

In This Chapter

Keeping up-to-date on accounting and financial reporting standards

Assuring that disclosure is adequate

Nudging the numbers to make things look better

Comparing private and public businesses

Dealing with financial reports’ information overload

Looking at changes in owners’ equity

I

n Chapters 4, 5, and 6, I explain the three primary financial statements of a

business:

Income statement: Summarizes sales revenue and other income (if any)

and expenses and losses (if any) for the period. It ends with the bottom-

line profit for the period, which most commonly is called net income or

net earnings. (Inside a business this profit performance statement is

commonly called the Profit & Loss, or P&L, report.)

Balance sheet: Summarizes financial condition at the end of the period, con-

sisting of amounts for assets, liabilities, and owners’ equity at that instant in

time. (Its more formal name is the statement of financial condition.)

Statement of cash flows: Reports the cash increase or decrease during

the period from profit-making activities (revenue and expenses) and the

reasons this key figure is different than bottom-line net income. It also

summarizes other cash flows during the period from investing and

financing activities.

These three statements, plus the footnotes to the financials and other content,

are packaged into annual financial reports so a business’s investors, lenders,

and other interested parties can keep tabs on the business’s financial health. In

this chapter, I shine a light on the preparation process so you can recognize the

types of decisions that must be made before a financial report hits the streets.

19_246009 ch12.qxp 4/17/08 12:04 AM Page 247

Recognizing Management’s Role

Whether a business is a small private company or a large public corporation,

its annual financial report consists of

The three basic financial statements: income statement, balance sheet,

and statement of cash flows.

A statement of changes in owners’ equity (if needed). Although it’s

called a “statement,” this item is more properly described as a supple-

mentary schedule. It reports certain information regarding changes in

owners’ equity accounts during the year that is not included in its three

primary financial statements. (See “Statement of Changes in Owners’

Equity” later in the chapter.)

And more.

In deciding what “more” means, the business’s CEO and top lieutenants play

an essential role — which they (and outside investors and lenders) should

understand. The CEO does certain critical things before a financial report is

released to the outside world:

1. Confers with the company’s chief financial officer and controller

(chief accountant) to make sure that the latest accounting and finan-

cial reporting standards and requirements have been applied in its

financial report. (The president of a smaller private company may have

to consult with a CPA on these matters.) In recent years, we’ve seen a

high degree of flux in accounting and financial reporting standards and

requirements. The private sector Financial Accounting Standards Board

(FASB) and the governmental regulatory agency, the Securities and

Exchange Commission (SEC), have been very busy in recent years — to

say nothing of the federal Sarbanes-Oxley Act of 2002 and the creation of

the Public Company Accounting Oversight Board.

A business and its auditors cannot simply assume that the accounting

methods and financial reporting practices that have been used for many

years are still correct and adequate. A business must check carefully

whether it is in full compliance with current accounting standards and

financial reporting requirements.

2. Carefully reviews the disclosures in the financial report. The CEO and

financial officers of the business must make sure that the disclosures — all

information other than the financial statements — are adequate according

to financial reporting standards, and that all the disclosure elements are

truthful but, at the same time, not damaging to the business.

248

Part IV: Preparing and Using Financial Reports

19_246009 ch12.qxp 4/17/08 12:04 AM Page 248

This disclosure review can be compared with the notion of due diligence,

which is done to make certain that all relevant information is collected,

that the information is accurate and reliable, and that all relevant require-

ments and regulations are being complied with. This step is especially

important for public corporations whose securities (stock shares and

debt instruments) are traded on securities exchanges. Public businesses

fall under the jurisdiction of federal securities laws, which require very

technical and detailed filings with the SEC.

3. Considers whether the financial statement numbers need touching

up. The idea here is to smooth the jagged edges off the company’s year-

to-year profit gyrations or to improve the business’s short-term solvency

picture. Although this can be described as putting your thumb on the

scale, you can also argue that sometimes the scale is a little out of bal-

ance to begin with and the CEO should approve adjusting the financial

statements in order to make them jibe better with the normal circum-

stances of the business.

When I discuss the third step later in this chapter, I’m venturing into a gray area

that accountants don’t much like to talk about. Some topics are, shall I say,

rather delicate. The manager has to strike a balance between the interests of

the business on the one hand and the interests of the owners (investors) and

creditors of the business on the other. The best analogy I can think of is the

advertising done by a business. Advertising should be truthful, but, as I’m sure

you know, businesses have a lot of leeway regarding how to advertise their

products and have been known to engage in hyperbole. Managers exercise the

same freedoms in putting together their financial reports. Financial reports may

have some hype, and managers may put as much positive spin on bad news as

possible without making deceitful and deliberately misleading comments.

Keeping in Mind the Purpose

of Financial Reporting

Business managers, creditors, and investors read financial reports because these

reports provide information regarding how the business is doing and where it

stands financially. Indeed, these accounting reports are the only source of this

information! The top-level managers of a business, in reviewing the annual financial

report before releasing it outside the business, should keep in mind that a finan-

cial report is designed to answer certain basic financial questions:

Is the business making a profit or suffering a loss, and how much?

How do assets stack up against liabilities?

Where did the business get its capital, and is it making good use of the

money?

249

Chapter 12: Getting a Financial Report Ready for Release

19_246009 ch12.qxp 4/17/08 12:04 AM Page 249