Whittenburg Gerald E., Altus-Buller Martha. Income Tax Fundamentals

Подождите немного. Документ загружается.

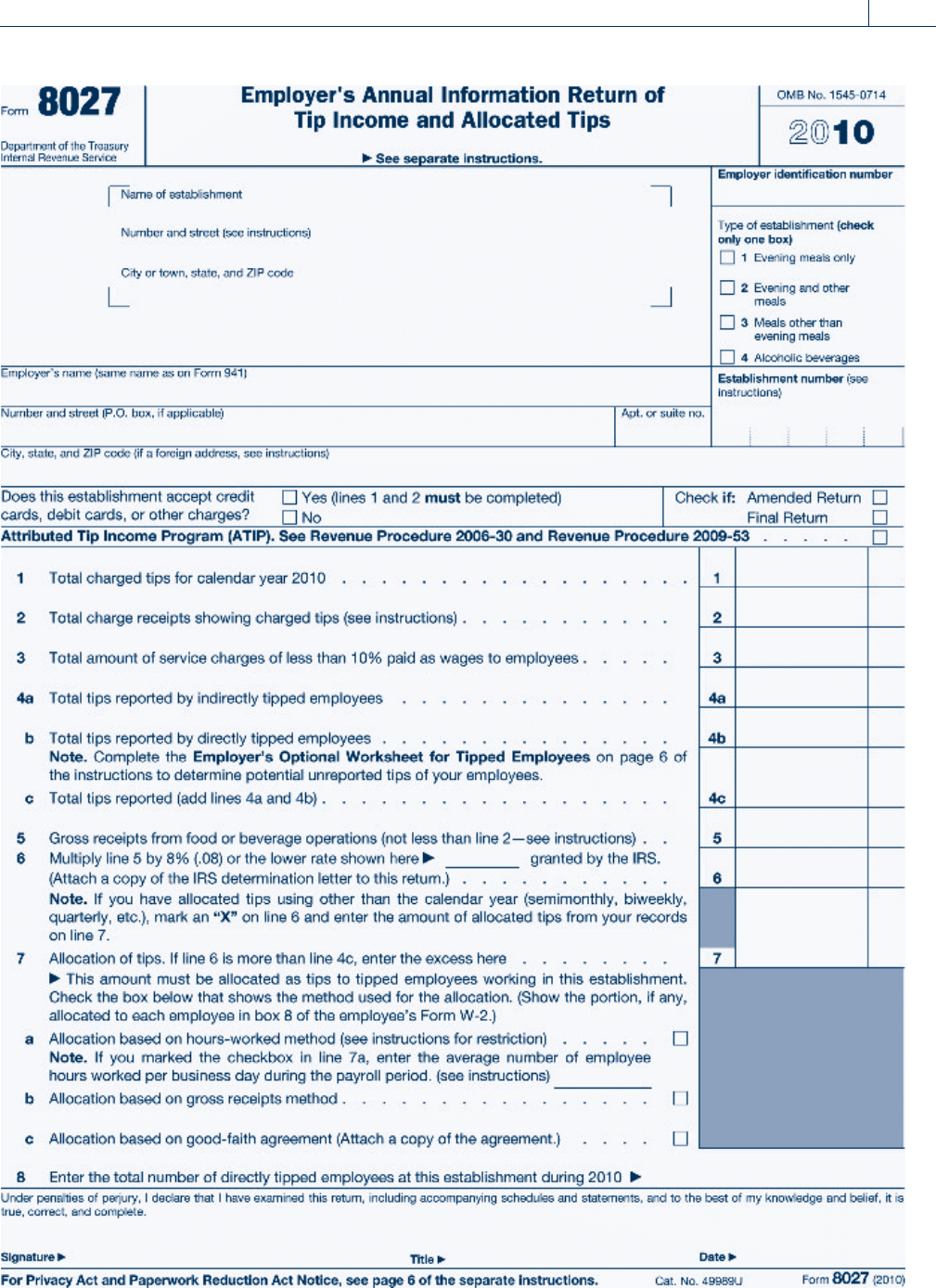

The allocation of tip income can be accomplished in one of four ways. The employer

may allocate the amount based on (1) gross receipts per employee, (2) hours worked by

each employee (available only to employers having fewer than the equivalent of twenty-

five full-time employees), (3) a good fa ith agreement as explained on Form 8027,

Employer’s Annual Information Return of Tip Income and Allocated Tips, or (4) the

new Attributed Tip Income Program (ATIP), which allows any reasonable method for

allocating tips to employees and may be elected in 2010 by checking a box at the beginning

of Form 8027. For a detailed explanation of the allocation process, see the instructions for

Form 8027. For more information on tip reporting in general, see the IRS Web site or a

tax research service.

Despite IRS efforts, tax cheating is on the rise. The Treasury Department esti-

mated that unreported income and other forms of cheating cost the govern-

ment $300 billion or more a year. Although there is disagreement about the

actual amount of tax cheating, experts agree it is a significant problem.

Backup Withholding

In some situations, individuals may be subject to backup withholding on payments such

as interest and dividends. The purpose of backup withholding is to ensure that income tax

is paid on income reported on Form 1099 (see Section 9.5). If backup withholding

applies, the payor (i.e., bank or insurance company) must withhold 28 percent of the

amount paid to the taxpayer. Payors are required to use backup withholding in the fol-

lowing cases:

1. The taxpayer does not give the payor his or her taxpayer identification number (e.g.,

Social Security number),

2. The taxpayer fails to certify that he or she is not subject to backup withholding,

3. The IRS informs the payor that the taxpayer gave an incorrect identification number, or

4. The IRS informs the payor to start withholding because the taxpayer has not reported

the income on his or her tax return.

EXAMPLE Barbra earned $2,000 in interest income from Cactus Savings Bank.

Barbra failed to certify that she was not subject to backup withhold-

ing. As a result, the bank must withhold taxes of $560 (28 percent of

$2,000) from the interest payments to Barbra. N

Taxpayers who give false information to avoid backup withholding are subject to a $500

civil penalty and a criminal penalty of up to $1,000 or up to 1 year of imprisonment, or both.

Self-Study Problem 9.1

For 2010, John earns $3,000 per month and has three dependent children. He

is divorce d and claims five allowances on his Form W-4. Calculate John’s with-

holding using:

1. The percentage method $ ____________

2. The wage bracket method $ ____________

Section 9.1

Withholding Methods 9-7

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 9.2

ESTIMATED PAYMENTS

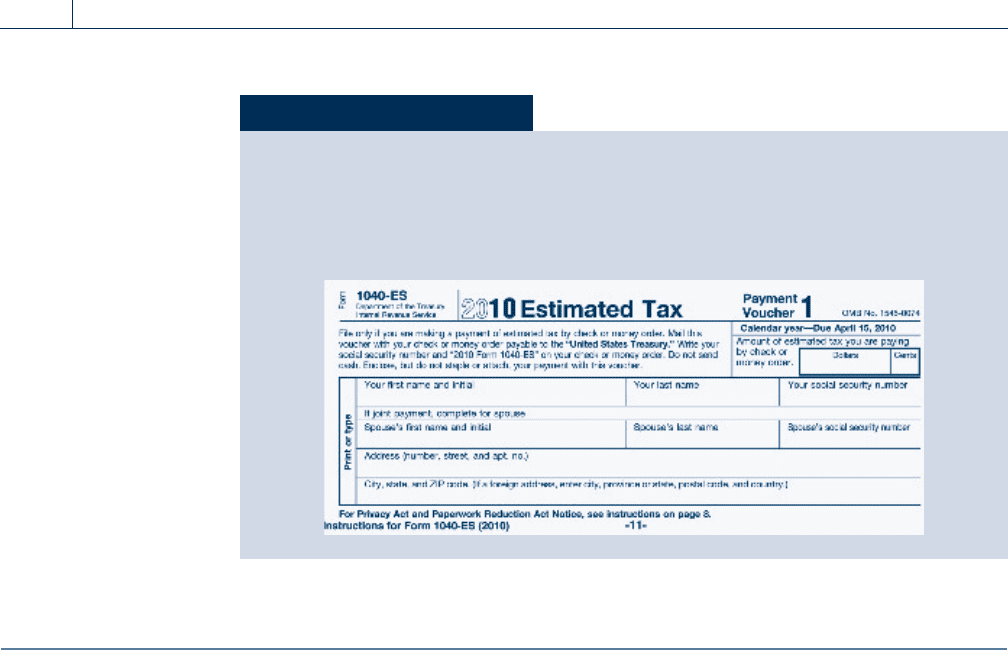

Self-employed taxpayers are not subject to withholding; however, they must make quar-

terly estimated tax payments. Taxpayers with large amounts of interest, dividends, and

other income not subject to withholding are also generally required to make estimated pay-

ments. Payments are made in four installments on April 15, June 15, and September 15 of the

tax year, and January 15 of the following year, based on the taxpayer’s estimate of the amount

of the tax liability for the year. A taxpayer with self-employment income must begin making

the payments when he or she first meets the filing requirements.

Never write out a check to the ‘‘IRS.’’ The IRS issues this warning every year,

because ‘‘IRS’’ may be easily changed to ‘‘MRS’’ plus an individual’s name if

the check falls into the wrong hands. Checks may be made payable to the U.S.

Treasury, as a reminder that the IRS is merely the collector of revenue for the

federal government.

Any individual taxpayer who has estimated tax for the year of $1,000 or more, after sub-

tracting withholding, a nd whose withholding does not equal or exceed the ‘‘required

annual payment,’’ must make quarterly estimated payments. The required annual payment

is the smallest of the following amounts:

1. Ninety percent of the tax shown on the current year’s return, or

2. One hundred percent of the tax shown on the preceding year’s return (such return

must cover a full 12 months), or

3. Ninety percent of the current-year tax determined by placing taxable income, alterna-

tive min imum taxable income, and adjusted self-employment income on an annual-

ized basis for each quarter.

A special rule applies to individuals with adjusted gross income in excess of $150,000 for

the previous year. These high-income taxpayers must pay 110 percent of 2010 tax for year

2011 estimated payments, instead of 100 percent, to meet the requirements in the second

exception above.

Estimated payments need not be paid if the estimated tax, after subtracting withholding,

can reasonably be expected to be less than $1,000. Therefore, employees who also have

self-employment income may avoid making estimated payments by filing a new Form

W-4 and increasing the amount of their withholding on their regular salary.

The IRS imposes a nondeductible pena lty on the amounts of any underpayments of esti-

mated tax. The penalty applies when any installment is less than the required annual pay-

ment divided by the number of installments that should have been made, which is usually

four. Form 2210, Underpayment of Estimated Tax by Individuals and Fiduciaries, is used

for the calculation of the penalty associated with the underpayment of estimated tax.

Good tax planning dictates that a taxpayer postpone payment of taxes as long as no pen-

alty is imposed. Unpaid taxes are equivalent to an interest-free loan from the government.

Therefore, taxpayers should base their estimated payments on the method which results in

the lowest amount of required quarterly or annual payment. For example, a taxpayer who

expects his tax liability to increase might base his estimated payments this year on the

amount of the tax liability for the prior year.

9-8 Chapter 9

Withholding, Estimated Payments, and Payroll Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

6,000

Kountry Kitchen

X

X

Kountry Kitchen

6,000

92,000

7,360

1,360

18

Section 9.2

Estimated Payments 9-9

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 9.3

THE FICA TAX

The Federal Insurance Contributions Act (FICA) imposed Social Security taxes. It was

passed by Congress in 1935 to provide benefits for qualified retired and disabled workers.

If a worker should die, it also provides the family of the worker with benefits. The Medicare

program for the elderly is also funded by FICA taxes.

FICA taxes have two parts, Social Security (old age, survivors, and disability insurance,

OASDI) and Medicare (hospital insurance). Employees and their employers are both

required to pay FICA taxes. Employers withhold a specified percentage of each employee’s

wages up to a maximum base amount, match the amount withheld with an equal amount,

and pay the total to the Social Security Administration.

For 2010, the Social Security (OASDI) tax rate is 6.2 percent and the Medicare tax rate is

1.45 percent each for employees and employers. The maximum wage subject to the Social

Security portion of the FICA tax is $106,800, and all wages are subject to the Medicare por-

tion of the FICA tax. The maximum amounts of Social Security to which the rates apply

have increased over the years.

Year Employee % Employer % Maximum Base

2007 6.20 6.20 $97,500 (Social Security)

1.45 1.45 Unlimited (Medicare)

2008 6.20 6.20 $102,000 (Social Security)

1.45 1.45 Unlimited (Medicare)

2009 6.20 6.20 $106,800 (Social Security)

1.45 1.45 Unlimited (Medicare)

2010 6.20 6.20 $106,800 (Social Security)

1.45 1.45 Unlimited (Medicare)

The original FICA tax in 1935 was 1 percent of the first $3,000 in earnings.

Self-Study Problem 9.2

Ray Adams (Social Security number 466-47-1131) estimates his required annual

payment for 2010 to be $7,560. He has a $510 overpayment of last year’s taxes

that he wishes to apply to the first quarter estimated tax payment for 2010.

Complete the first quarter voucher below for Ray for 2010 by assuming any

additional information, such as Ray’s address.

9-10 Chapter 9

Withholding, Estimated Payments, and Payroll Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Workers age 25 and over now receive an annual statement of Social Security ben-

efits about 3 months before their birth month. The statement provides estimates

of projected retirement, survivors’, and disability benefits. It also shows the work-

er’s Social Security earnings history, giving the worker an opportunity to correct

any errors or omissions.

Workers can also request an estimate of benefits at any time through the

Social Security Administration Web site (www.ssa.gov) or by mailing in Form

SSA-7004, which can be downloaded from the site. The advantage of making a

separate request is that workers can provide an exact retirement age as well as

an estimate of future earnings for use in making benefit projections. These pro-

jections may be more precise than those in the automatic annual statement.

(Source: Social Security Administration (www.ssa.gov))

EXAMPLE Katherine earns $21,500 for 2010. The FICA tax on her wages is calcu-

lated as follows:

Katherine: Soc. Sec. — 6.2% $21,500 $1,333.00

Medicare — 1.45% $21,500

311.75

Total employee FICA tax

$1,644.75

Katherine’s

employer: Soc. Sec. — 6.2% $21,500 $1,333.00

Medicare — 1.45% $21,500

311.75

Total employer FICA tax

$1,644.75

Total FICA tax

$3,289.50

N

EXAMPLE Sam is an employee of Serissa Company. His salary for 2010 is

$132,000. Sam’s portion of the FICA tax is calculated as follows:

Soc. Sec. — 6.2% $106,800 $6,621.60

Medicare — 1.45% $132,000

1,914.00

Total employee FICA tax

$8,535.60

The total combined FICA tax (employee’s and employer’s share) is

$17,071.20. N

According to the Congressional Budget Office, more than one-third of ho use-

holds pay mor e in FICA tax than in income tax. If the emplo yer share of FICA

is included, this number rises to 70 percent.

Overpayment of FICA Taxes

Taxpayers who work for more than one employer during the same tax year may pay more

than the maximum amount of FICA taxes. This occurs when the taxpayer’s total wages are

more than the maximum base amount(s) for the year. When this happens, the taxpayer

should compute the excess taxes paid, and report the excess on Form 1040 as an additional

payment against his or her tax liability.

Section 9.3

The FICA Tax 9-11

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

EXAMPLE Jerry worked for two employers during 2010. The first employer with-

held and paid FICA taxes on $70,000 of salary paid to Jerry, and the

second employer withheld and paid FICA taxes on $50,000 of salary

paid to Jerry. The amount of Jerry’s excess FICA taxes paid for 2010 is

computed as follows: 6.2% (Social Security rate) [$70,000 þ $50,000

$106,800 (maximum for Social Security portion of FICA tax)] ¼ $818.

Jerry receives a payment against his 2010 income tax liability equal

to the excess Social Security taxes of $818. No excess Medicare tax

has been paid, as there is no upper limit on Medicare wages. N

SECTION 9.4 FEDERAL TAX DEPOSIT SYSTEM

Employers must make periodic deposits of t he taxes that are withheld from employees’

wages. The frequency of the deposits depends on the total income tax withheld and the

total FICA taxes for all employees. Employers are either monthly depositors or semiweekly

depositors, depending on the total income taxes withheld from wages and FICA taxes

attributable to wages. Prior to the beginning of each calendar year, taxpayers are required

to determine which of the two deposit schedules they are required to use. If withholding

and FICA taxes of $100,000 or more are accumulated at any time during the year, the

depositor is subject to a special one-day deposit rule.

Monthly or semiweekly deposit status is determined by using a lookback period, consist-

ing of the four quarters beginning July 1 of the second preceding year and ending June 30

of the prior year. If the total income tax withheld from wages and FICA attributable to

wages for the four quarters in the lookback period is $50,000 or less, employers are

monthly depositors for the current year. Monthly depositors must make deposits of

employment taxes and taxes withheld by the fifteenth day of the month following the

month of withholding. New employers are automatically monthly depositors.

If the total income tax withheld from wages and FICA attributable to wages for the four

quarters in the lookback period is more than $50,000, the employer is a semiweekly depos-

itor for the current year. Taxes on payments made on Wednesday, Thursday, or Friday

must be deposited by the following Wednesday; taxes on payments made on the other

days of the week must be deposited by the following Friday. If a deposit is scheduled for

a day that is not a banking day, the deposit is considered to be made timely if it is made

by the close of the next banking day.

EXAMPLE Tom runs a small business with ten employees. During the lookback

period for the current year, the total withholding and FICA taxes

amounted to $15,600. Since this is less than $50,000, Tom is a monthly

depositor. His payroll tax deposits must be made by the fifteenth day

of the month following the month of withholding. N

Self-Study Problem 9.3

Debbie earns $120,000 in 2010. Calculate the total FICA tax that must be paid by:

Debbie: Soc. Sec. $ ____________

Medicare $ ____________

Debbie’s employer: Soc. Sec. $ ____________

Medicare $ ____________

Total FICA tax $ ____________

9-12 Chapter 9

Withholding, Estimated Payments, and Payroll Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Since 2006, nearly a million very small employers with employment tax liability of

$1,000 or less have been allowed to file and pay employment taxes just once a year, instead

of quarterly; for example, by January 31 of 2011 for 2010 employment taxes. Qualifying

small employers receive written notification from the IRS that they should file using a

Form 944 instead of the standard Form 9 41 used by most employers. The Form 944,

along with payment of tax, is due at the end of the month following the taxpayer’s year end.

Employer deposits are made to any commercial bank that is an authorized depository for

federal taxes. All national banks and many state banks are depositories. If the deposit is

mailed, it must have been mailed as of the second day before the due date to be considered

timely. Taxpayers should use registered or certified mail to document the mailing date.

Deposits may also be made by electronic funds transfer (EFT). Employers with tax deposits

exceeding certain dollar amounts and those who were required to make payments by EFTPS

(Electronic Federal Tax Payment System) in the previous year are required to make pay-

ments using EFTPS; failure to do so may subject the depositor to a 10 percent penalty.

Tax payments (monthly, semiweekly, or daily for large depositors) not made by EFTPS

must be accompanied by Form 8109 (Federal Tax Deposit Coupon). Generally, employers

must file Form 941, Employer’s Quarterly Federal Tax R eturn, which reports the federal

income taxes withheld from wages and the total FICA taxes attributable to wages paid dur-

ing each quarter. Form 941 must be accompanied by any payroll taxes not yet deposited for

the quarter. A special deposit rule allows small employers who accumulate less than $2,500

tax liability during a quarter to skip monthly payments and pay the entire amount of their

payroll taxes with their quarterly Form 941. Form 941 must be filed by the last day of the

month following the end of the quarter. For example, the first quarter Form 941, covering

the months of January through March, must be filed by April 30. The Form 941 e-file pro-

gram allows a taxpayer to electronically file Form 941 or Form 944.

The IRS plans to eliminate the use of federal tax deposit coupons and require

electronic filing and electronic tax deposits after 2010, exempting only small

employers paying less than $2,500 a quarter in employment taxes.

Self-Study Problem 9.4

For the first quarter of 2010, Rita O’Miya has two employees. The payroll infor-

mation for these two employees for the first quarter is as follows:

Mary Chris

January February March January February March

Gross wages $2,000 $2,000 $2,100 $1,000 $1,000 $1,500

Federal income

tax withheld

230 230 235 60 60 180

FICA tax

withheld

153 153 161 77 77 115

Rita deposited $750 on February 15, $750 on March 15, and $967 on April 15.

Using this information, complete Rita’s Form 941, on page 9-15, for the first

quarter of 2010.

Section 9.4

Federal Tax Deposit System 9-13

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

The President signed the Hiring Incentives to Restore Employment Act, or HIRE

Act, into law on March 18, 2010. The new law contains a brief payroll tax hol-

iday for employers of newly-hired workers and an employer credit for retained

workers hired during the payroll tax holiday.

Payroll Tax Holiday: Employers hiring previously unemployed or underem-

ployed new employees after February 3, 2010, and before January 1, 2011,

will not have to pay t he 6.2 percent employer portion of Social Security taxes

that would have been due for those employees for the period after March

18, 2010, and before January 1, 2011 . The newly-hired employees must

certify on Form W-11 that they were employed for no more than 40 hours in

the 60-day period ending on the date they began work in the new job. A recent

college graduate can qualify under this definition. The reduction in payroll

taxes will be made on the employer’s payroll tax return, Form 941, and will

not be claimed as a credit on the income tax return of the employer.

Credit for Retained Workers: Any worker who qualifies as a newly-hired

employee under the payroll tax holiday described above, and who is retained

by the employer for at least 52 weeks, may qualify the employer for a tax credit

of up to $1,000. Because the time period will not be met for any new hire until

sometime in the 2011 tax year, this credit will be claime d on 2011 income tax

returns only.

SECTION 9.5

EMPLOYER REPORTING REQUIREMENTS

On or before January 31 of the year following the calendar year of payment, an employer

must furnish to each employee two copies of the employee’s Wage and Tax Statement,

Form W-2, for the previous calendar year. If employment is terminated before the end

of the year and the employee requests a Form W-2, the employer must furnish the

Form W-2 within 30 days after the last wage payment is made or after the employee

request, whichever is later. Otherwise the general rule requiring the W-2 to be furnished

to the employee by January 31 applies. The original copy (Copy A) of all W-2 forms and

Form W-3 (Transmittal of Income and Tax Statements) must be filed with the Social

Security Administration by February 28 of the year following the calendar year of payment.

Copy B of Form W-2 is filed with the employee’s federal tax return. Employers retain

Copy D of Form W-2 for their records. Extra copies of Form W-2 are prepared for the

employee to use when filing state and local tax returns.

Form W-2 is used to report wages, tips, and other compensation paid to an employee.

Not all of the amounts included on a taxpayer’s Form W-2 are subject to income tax with-

holding. Among the items which must be reported on the employee’s Form W-2 are reim-

bursements for nonqualified moving expenses (a nonqualified moving expense is an

expense the employee cannot deduct for tax purposes), excess group-term life insurance

premiums, the value of noncash prizes and awards presented to individuals normally

paid on a commission basis, and certain reimbursements of travel and other ordinary

and necessary expenses. Special rules apply to the reimbursement of travel and other ordi-

nary and necessary employee business expenses.

If an employee is reimbursed for travel and other ordinary and necessary business

expenses, income and employment tax withholding m ay be required. If a reimbursement

payment is considered to have been made under an accountable plan, as discussed in Chap-

ter 4, the amount is excluded from the employee’s gross income and consequently is not

9-14 Chapter 9

Withholding, Estimated Payments, and Payroll Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Section 9.5

Employer Reporting Requirements 9-15

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

9-16 Chapter 9

Withholding, Estimated Payments, and Payroll Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.