Whittenburg Gerald E., Altus-Buller Martha. Income Tax Fundamentals

Подождите немного. Документ загружается.

Questions and Problems 8-69

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

8-70 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Student Name

Class/Section

Date

KEY NUMBER TAX RETURN SUMMARY

Chapter 8

Comprehensive Problem 1

Adjusted Gross Income (Line 37) ________________

Schedule D, Net Short-Term

Capital Gain or (Loss) (Line 7) ________________

Schedule D, Net Long-Term

Capital Gain or (Loss) (Line 15) ________________

Taxable Income (Line 43) ________________

Tax Overpaid (Line 73) ________________

Comprehensive Problem 2

Adjusted Gross Income (Line 37) ________________

Schedule D, Net Short-Term

Capital Gain or (Loss) (Line 7) ________________

Schedule D, Net Long-Term

Capital Gain or (Loss) (Line 15) ________________

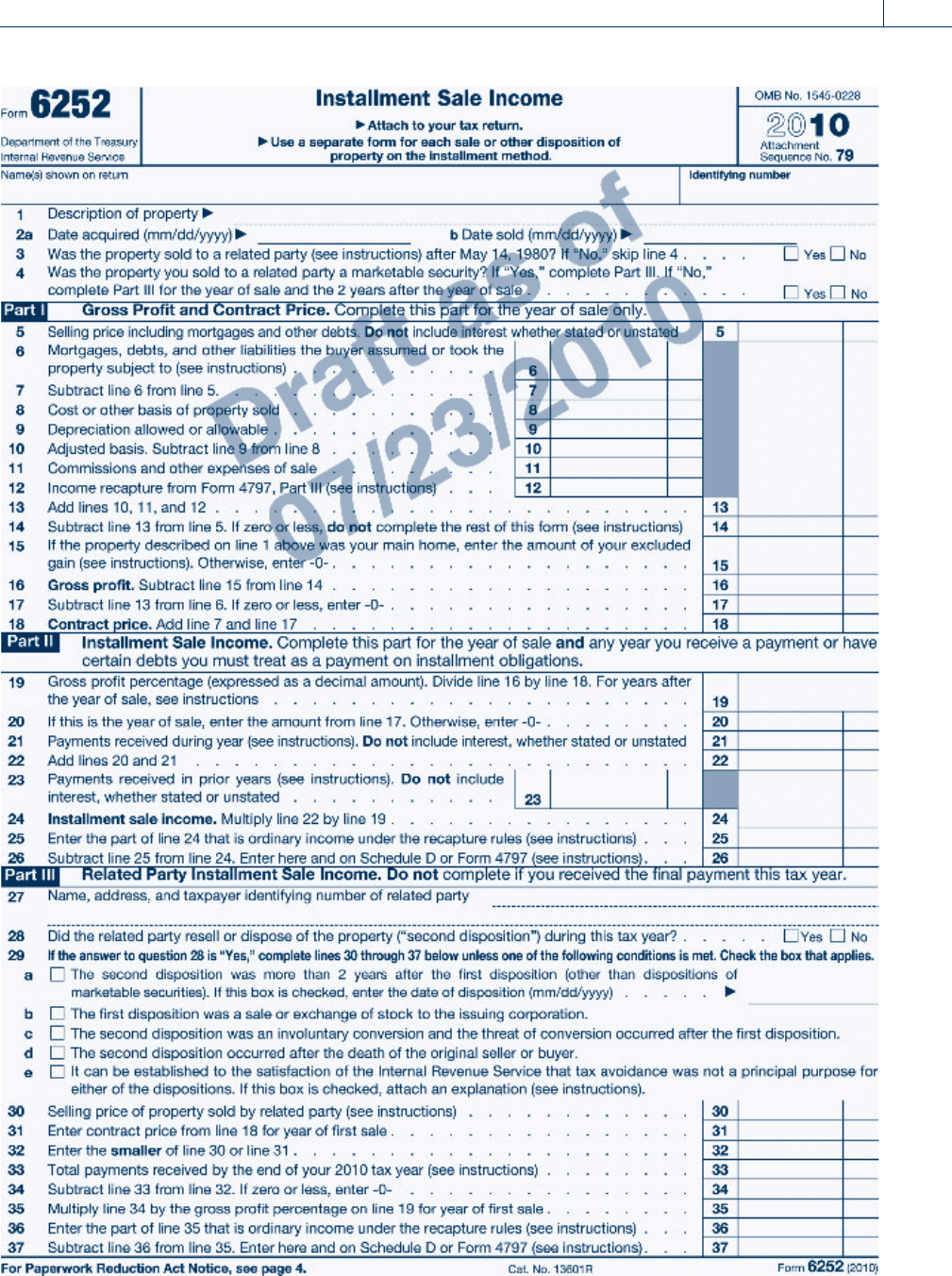

Form 6252, Installment Sale Income (Line 26) ________________

Tax Overpaid (Line 73) ________________

Questions and Problems 8-71

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

c

vgstudio/Shutterstock

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Chapter 9

Withholding, Estimated

Payments, and Payroll Taxes

LEARNING OBJECTIVES

.............................................. .........................

After completing this chapter, you should be able to:

LO 9.1 Compute the income tax withholding from employee

wages.

LO 9.2 Determine taxpayers’ quarterly estimated payments.

LO 9.3 Understand the FICA tax, the federal deposit system,

and employer payroll reporting.

LO 9.4 Calculate the self-employment tax (both Social Security

and Medicare portions) for self-employed taxpayers.

LO 9.5 Compute the amount of FUTA tax for an employer.

LO 9.6 Apply the special tax and reporting requirements for

household employees (the nanny tax).

Overview

This chapter focuses on the payment and reporting of income and other taxes by employ-

ers, employees, and self-employed taxpayers. Payroll and other tax topics covered include

withholding methods for employees, estimated payments, the FICA tax (Social Security

and Medicare taxes), the federal tax deposit system, and employer reporting requirements.

In addition, related taxes such as the self-employment (SE) tax, the Federal Unemployment

Tax Act (FUTA) tax, and the nanny tax are covered.

The FICA tax is a combined Social Security (6.2% up to the annual limit, $106,800 in

2010) and Medicare (1.45% with no limit) tax that is paid by both employees and employ-

ers. The tax is withheld from each employee’s paycheck, then the tax is matched by the

employer, and the total amount is remitted to the IRS.

The FUTA tax is unemployment insurance with a joint state and federal payment plan

to provide benefits for taxpayers when they b ecome unemployed. The FUTA tax is paid

only by employers, not employees.

Self-employed taxpayers do not have an employer to match their Social Security and

Medicare tax es, so they have to pay the full amount of the SE tax (15.3% in total up to

the $106,800 limit and then 2.9% with no limit). In many cases, the SE tax can exceed a

self-employed individual’s income tax.

9-1

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

The nanny tax is a reporting system for wages paid to household employees such as

babysitters, caretakers, cooks, drivers, gardeners, housekeepers, and maids who earn

more than an annual threshold amount.

Every working individual, whether an employee or self-employed, is affected by the

rules covered in this chapter.

SECTION 9.1

WITHHOLDING METHODS

Employers are required to withhold taxes from amounts paid to employees for wages, includ-

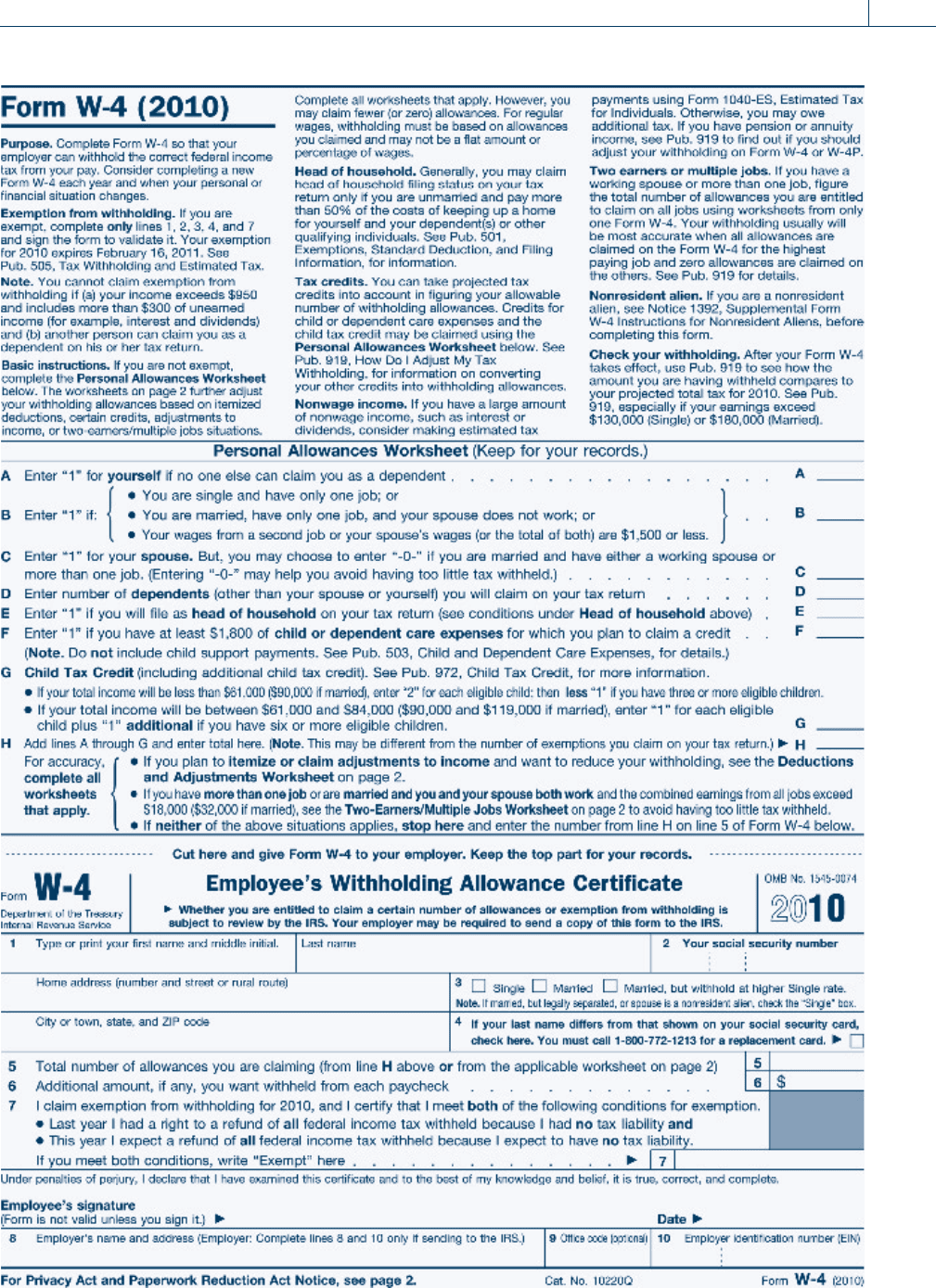

ing salaries, fees, bonuses, commissions, and vacation and retirement pay. Form W-4, show-

ing the filing status and the number of withholding allowances an employee is claiming, is

furnished to the employer by the employee. Form W-4 is the key to the amount of the

employee’s withholding for federal income taxes. Usually, employees claim the same number

of allowances on Form W-4 as the number of exemptions claimed on their federal tax

returns. Employees with alimony payments, a large amount of itemized deductions, or tax

credits may claim additional withholding allowances. Each additional withholding allowance

reduces annual withholding income by the value of one exemption. Form W-4 includes a

worksheet for calculating the number of additional allowances an employee should claim.

Some employee s want extra tax withheld from their wages; this may be authorized on

Form W-4. Also, exemption from withholding may be claimed on Form W-4 by employ-

ees who anticipate no federal tax liability for the current year. To be exempt from with-

holding, the employee must also have had no tax liability for the prior year. If an

employee does not complete Form W-4, the employer is required to withhold as if the

employee is single with no exemptions.

Single employees with only one job may claim one ‘‘special withholding allowance.’’

Married employees may also claim a ‘‘special withholding allowance’’ if one of the follow-

ing conditions exists:

1. The employee has only one job and his or her spouse does not work, or

2. Wages earned from the employee’s second job, or wages earned by his or her spouse,

or the total of both are $1,500 or less.

Employees with two or more jobs or employees with a spouse who also is employed must

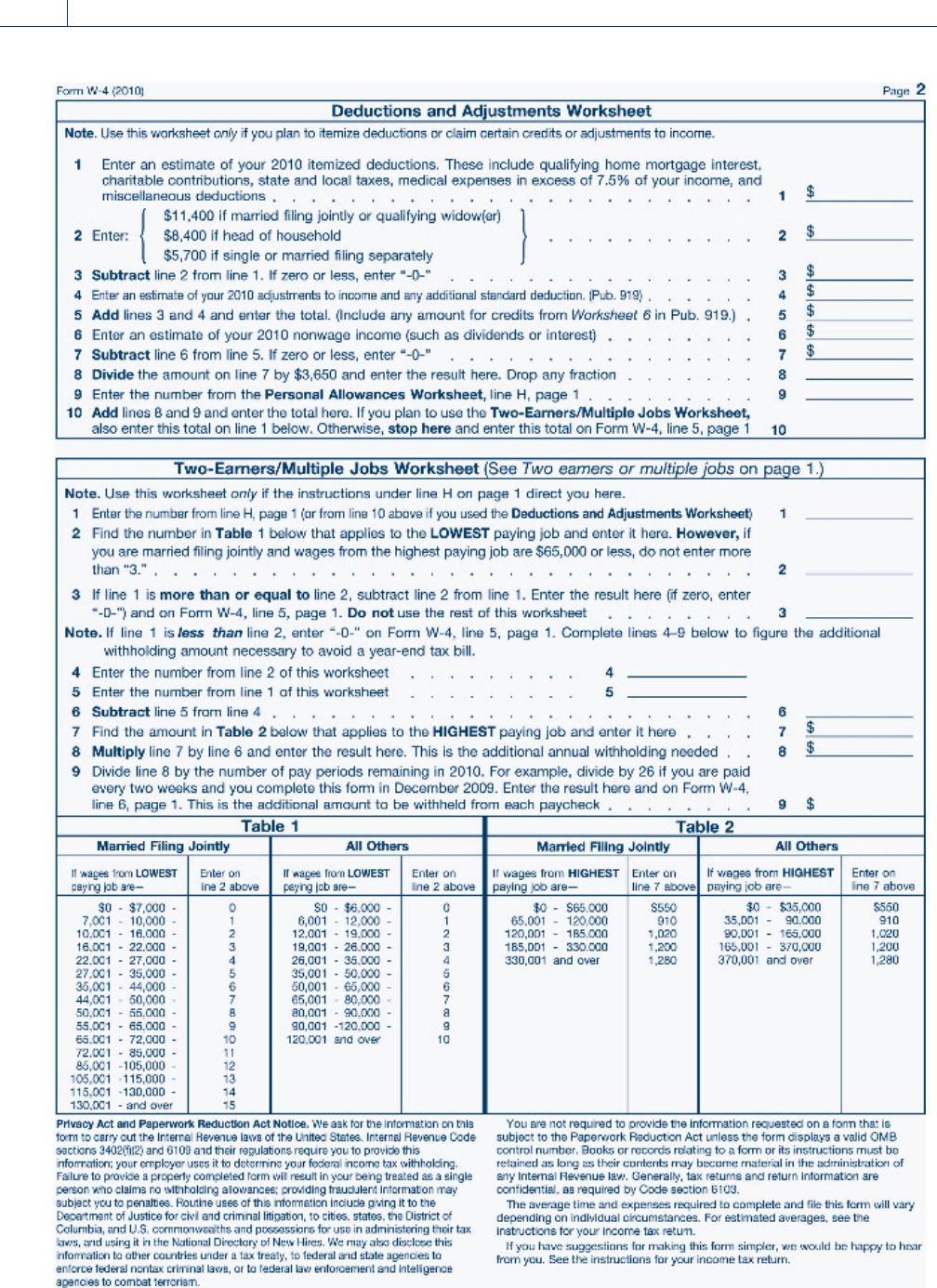

complete the ‘‘Two Earners/Multiple Jobs Worksheet’’ on page 2 of Form W-4.

Employees do not have to provide proof to their employers that they are e ntitled to

the number of allowances claimed on their Form W-4s. Prior to 2005, employers were

required to notify th e IRS if an emp loyee claimed more than ten allowances. New g uid-

lines require employers to submit copies of W-4s to the IRS only when directed to do so

by written notice. Where t here is significant underwithholding for a particular employee,

the IRS may require the employer to withhold income tax at a higher rate. Employees are

given the right to contest the IRS determination.

EXAMPLE Tom Barry earns $50,000 per year and his wife does not work. All of

Tom’s salary is from one job, and the Barrys have two dependent chil-

dren under 17. The Barrys estimate their itemized deductions to be

$13,500 for the year. Tom should claim nine withholding allowances

as illustrated on Form W-4 on pages 9-3 and 9-4. N

The former president of S print Corporation claimed approximately 300,000

exemptions connected to a complex tax shelter that eventually cost him his

job, according to the Wall Street Journal.

9-2 Chapter 9

Withholding, Estimated Payments, and Payroll Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

1

1

1

2

4

9

9

X

Tom Barry

Section 9.1

Withholding Methods 9-3

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

13,500

11,400

2,100

2,100

2,100

0

9

9

9-4 Chapter 9

Withholding, Estimated Payments, and Payroll Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

It pays to fill in Form W-4 correctly. When taxpayers have too much tax withheld,

they are giving the government an interest-free loan of the extra income tax

withholding until the ir tax return is filed and a refund is obtained. When tax-

payers have too little income tax withheld, they are subject to penalties for

underpayment of taxes (see Section 9.2).

Computing Withholding

The amount to be withheld by the employer is based on gross wages before deducting

Social Security taxes, pension payments, union dues, insurance, and other deductions. An

employer may elect to use any of several methods to determine the amount of

the withholding for each individual employee. Most commonly, withholding amounts are

determined by use of the percentage method or by use of wage bracket tables. To compute

the withholding amount under the percentage method, the employer should:

1. Multiply the number of allowances claimed by the employee (from the Form W-4)

by the allowance amount;

2. Subtract that amount from the employee’s gross wages for the pay period; and

3. Multiply the result in Step 2 by the percentage obtained from the tables in Appendix C

for the appropriate marital status.

The allowance amounts used in Step 1 for 2010 for various pay periods are from IR S

Publication 15, ‘‘Circular E, Employer’s Tax Guide.’’ All are based on the fact that in

2010, one allowance is $3,650.

Pay Period 2010 Allowance Amount

Daily (assumes 260 working days) $ 14.04

Weekly 70.19

Biweekly 140.38

Semimonthly 152.08

Monthly 304.17

Quarterly 912.50

Semiannually 1,825.00

Annually 3,650.00

EXAMPLE Sharon is married, and her pay is $2,250 per month. On her Form

W-4, Sharon claims married with a total of two allowances. The

amount of withholding for Sharon is calculated as follows:

1. Allowances amount (monthly) $ 304.17

Number of allowances claimed

2

Total

$ 608.34

2. Gross wages $2,250.00

Less: amount from above

(608.34)

Withholding income

$1,641.66

3. Withholding from percentage tables in Appendix C:

($1,642 $1,146) 10% ¼ $49.60 N

Section 9.1

Withholding Methods 9-5

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Under the second method of determining withholding, wage bracket tables are provided for

weekly, biweekly, semimonthly, monthly, and daily payroll periods for both married and single

taxpayers. The amount of withholding is obtained from the table for the appropriate payroll

period and marital status, and is based on the total wages and the number of withholding

allowances claimed. The monthly tables for married taxpayers are reproduced in Appendix C.

EXAMPLE Sharon’s withholding from the previous example may also be

obtained from the wage bracket tables in Appendix C. For a wage

payment of $2,250 with two allowances, on the married person’s

monthly payroll period table, the amount of the withholding is

found to be $51.00. N

Pension and Deferred Income

Withholding is also required on pension and other deferred income payments. Financial

institutions and corporations must withhold on the taxable part of pension, profit-sharing,

stock bonus, and individual retirement account payments. The rates used for withholding

vary depending on the nature of the payment, as described below:

1. Periodic payments (such as annuities): Rates are based on the taxpayer’s withholding

certificate as if the payments were additional wages.

2. Nonperiodic payments: The withholding is at a flat 10 percent rate, except for certain

distributions from qualified retirement plans, which have a required 20 percent rate.

See Chapter 3 for a discussion of withholding on rollover distributions.

EXAMPLE Adam is a retired college professor and receives a pension of $775

per month. The payor should withhold on the pension in the same

manner as if it were Adam’s salary. N

Tip Reporting

The receipt of tips is part of the vast economy of cash transactions which are underreported

or simply ignored as income by many taxpayers. To combat widespread underreporting of

tips in the food and beverage business, the IRS developed requirements for employees and

employers. Employees are generally required to report tips to their employers.

Then employers are generally required to report the amount of gross food and beverage

sales (other than carryout) to the IRS. If total reported tips are less than 8 percent

of sales, the employer must allocate among the employees the excess of 8 percent of gross

sales over the amount of tips reported to the employer by the employees. The employer is

not required to wit hhold income, Social Security, or Medicare tax on allocated tips, but

is required to collect those taxes on tips reported by employees.

EXAMPLE The Kountry Kitchen restaurant has eighteen tipped employees.

During the current reporting period, the restaurant has gross receipts

of $92,000. The employees report tip income of $6,000. Kountry

Kitchen must allocate tips of $1,360, determined as follows:

8% of $92,000 $ 7,360

Reported tips

(6,000)

Underreported tips

$ 1,360

The Kountry Kitchen restaurant must complete Form 8027,

Employer’s Annual Information Return of Tip Income and

Allocated Tips, as illustrated on page 9-9. N

9-6 Chapter 9

Withholding, Estimated Payments, and Payroll Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.