Whittenburg Gerald E., Altus-Buller Martha. Income Tax Fundamentals

Подождите немного. Документ загружается.

required to be included on Form W-2, and no withholding is required. Alternatively, reim-

bursements of travel and other employee business expenses made under a nonaccountable

plan must be included as wages on Form W-2 and the amounts are subject to withholding.

Payments are considered made under a nonaccountable plan in the following circumstan-

ces: (1) the employee receives a reimbursement for expenses under an arrangement which

does not require the employee to account adequately to the employer, or the employee

receives advances under an arrangement which does not require the employee to return

amounts in excess of substantiated expenses; or (2) the employee receives amounts under

an arrangement that requires the employee to substantiate reimbursed expenses, but

the amounts are not substantiated within a reasonable period of time, or the employee

receives amounts under a plan which requires excess reimbursements to be returned to

the employer, but the employee does not return such excess amounts within a reasonable

period of time. In the first case, the entire amount paid under the expense account plan is

considered wages subject to withholding, where as under the circumstances described in the

second situation, on ly the amounts in excess of the substantiated expenses are subject to

withholding.

Every year the IRS releases a list of twelve scams, called by some the ‘‘we’ve

already seen it, so don’t try it’’ list, or ‘‘The Dirty Dozen.’’ The list includes off-

shore financial account misuse and frivolous arguments including ‘‘wages are

not income’’ and ‘‘paying taxes is voluntary.’’ Filling in a corrected wage form

(Form 4852, Substitute Form W-2) to change taxable wages to zero is a creative

additional item on the list.

Other Form W-2s

Gambling winnings are reported by the gambling establishment on Form W-2G. Amounts

that must be reported include certain winnings on horse and dog racing, jai alai, lotteries,

state-conducted lotteries, sweepstakes, wagering pools, bingo, keno, and slot machines. In

certain cases, withholding of income taxes is required. Form W-2Gs must be transmitted

to the taxpayer not later than January 31 of the year following the calendar year of pay-

ment, and to the IRS along with Form W-3G by February 28 of the year following the

calendar year of payment.

Information Returns

Taxpayers engaged in a t rade or business are required to file Form 1099 for each recip-

ient of certain payments made in the course of their trade or business. Where applica-

ble, federal income tax withheld with respect to the payment is also reported on F orm

1099. The common types of payments and the related Form 1099 are summarized in

Table 9.1.

Form 1099s must be mailed to the recipients by January 31 of the year following the

calendar year of payment. However, stockbrokers are allowed until February 15 of the

year following the calendar year of payment to provide Form 1099-B and other state-

ments. A separate Form 1096 must be used to transmit each type of 1099 to the appro-

priate IRS Service Center by February 28 of the year following the calendar year of

payment.

Section 9.5

Employer Reporting Requirements 9-17

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Court clerks must report to the IRS cash payments of bail exceeding $10,000

when it is posted in narcotics, racketeering, or money-laundering cases. The

payor s of large cash bai l am ounts mus t also be given a statement similar to a

1099 form at year-end.

TABLE 9.1

Form 1099s

Form Used For

1099-B Payments of proceeds from brokers

1099-DIV Dividend payments

1099-INT Interest payments

1099-MISC Miscellaneous payments

1099-R Pension, annuity, profit-sharing, retirement plan,

IRA, insurance contracts, etc.

1099-S Proceeds from real estate transactions

Self-Study Problem 9.5

Big Bank (P.O. Box 12344, San Diego, CA 92101; E.I.N. 95-1234567; California ID

800 4039 250 092) paid an employee, Mary Jones (6431 Gary Street, San Diego,

CA 92115), wages of $16,150 for 2010. The federal income tax withholding for

the year amounted to $2,422, and FICA withheld was $1,235.48 ($1,001.30 for

Social Security tax and $234.18 for Medicare tax). State income tax withheld

was $969.00. Mary’s FICA wages were the same as her total wages, and her

Social Security number is 464-74-1132.

a. Complete the following Form W-2 for Mary Jones from Big Bank.

9-18 Chapter 9

Withholding, Estimated Payments, and Payroll Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 9.6

SELF-EMPLOYMENT TAX

Self-employed individuals pay self-employment taxes instead of FICA taxes. Since these indi-

viduals have no employers, the entire tax is paid by the self-employed individuals. Like the

FICA taxes to which employees and their employers are subject, the self-employment tax

consists of two parts, Social Security Old Age, Survivors, and Disability Insurance

(OASDI) and Medicare (hospital insurance). For 2010, the Social Security (OASDI) tax

rate is 12.4 percent and the Medicare tax rate is 2.9 percent. The maximum base amount

of earnings subject to the Social Security portion of the FICA tax is $106,800. All earnings

are subject to the Medicare portion of the FICA tax. The self-employment tax rates and the

maximum base amounts for 4 years are illustrated in the following table:

Year Percentage Maximum Base

2007 12.40% $97,500 (Social Security)

2.90% Unlimited (Medicare)

2008 12.40% $102,000 (Social Security)

2.90% Unlimited (Medicare)

2009 12.40% $106,800 (Social Security)

2.90% Unlimited (Medicare)

2010 12.40% $106,800 (Social Security)

2.90% Unlimited (Medicare)

If an individual, subject to self-employment taxes, also receives wages subject to FICA taxes

during a tax year, the individual’s maximum base amount for self-employment taxes is reduced

by the amount of wages as both employee and employer have already paid FICA taxes on the

wages. Therefore, the total amount of earnings subject to both FICA and self-employment tax

for 2010 cannot exceed $106,800 for the Social Security portion of the tax. If net earnings

from self-employment are less than $400, no self-employment tax is payable.

The self-employment tax is imposed on net earnings of $400 or more from self-

employm ent. Net earnings from self-employment incl ude gross income from a trade

b.Mary also has a savings account at Big Bank, which paid her interest for

2010 of $461. Complete the following Form 1099-INT for Mary’s interest

income.

Self-Study Problem 9.5 (continued)

Section 9.6

Self-Employment Tax 9-19

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

or business less trade or business deductions, the distributive share of partnership income

from a trade or business, and net income earned as an independent contractor. Gains and

losses from property transactions, except inventory transactions, and other unearned income

are not considered self-employment income. In arriving at net earnings from self-employment

only for purposes of computing the self-employment tax, self-employed taxpayers are allowed

a deduction for AGI of one-half of the otherwise applicable self-employment tax. This deduc-

tion is determined by multiplying the net earnings from self-employment, before considering

this deduction, by one-half of the sum of the self-employment tax rates applicable for the tax

year. A shortcut to arriving at the self-employment income subject to self-employment tax is

to multiply the net earnings from self-employment by 92.35 percent. This shortcut is used on

Schedule SE as illustrated below. In addition, once the self-employment tax liability has been

determined, the taxpayer is allowed a deduction for income tax purposes equal to one-half of

the actual self-employment tax liability. For 2010 only, taxpayers are allowed to deduct health

insurance premiums to arrive at net earnings from self-employment.

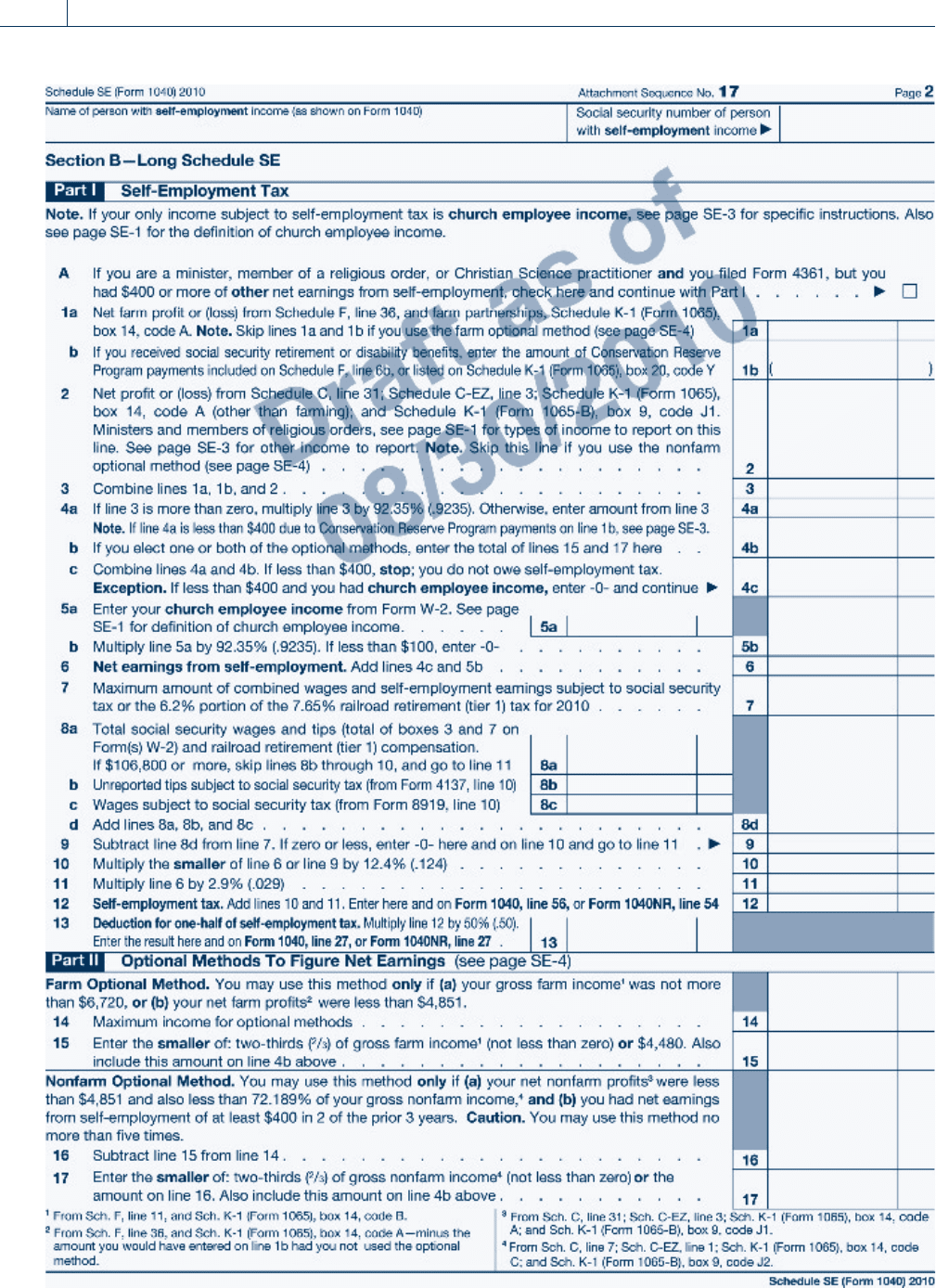

EXAMPLE Norman is a self-employed accountant in 2010. From his practice, Nor-

man earns $130,000, and has wages subject to FICA from a part-time

job of $9,100. Norman’s self-employment tax is calculated as follows:

Step 1:

Net earnings from self-

employment, before the self-

employment tax deduction

$130,000

92.35%

Tentative net earnings from

self-employment after deduc-

tion for self-employment tax

$120,055

Step 2:

Social Security Medicare

Maximum base for 2010 $106,800 Unlimited

Less: FICA wages

(9,100) Not Applicable

Maximum self-employment

tax base

$ 97,700 Unlimited

Lesser of net earnings from

self-employment after deduc-

tion for self-employment tax

or maximum base

$ 97,700 $120,055

Self-employment tax rate

12.4% 2.9%

Self-employment tax for 2010

$ 12,115 $ 3,482

Norman’s total self-employment tax for 2010 is $15,597 ($12,115 þ

$3,482). On his 2010 income tax return, Norman will report net earn-

ings from self-employment of $130,000, a deduction for adjusted

gross income of $7,799 (50 percent of $15,597), and s elf-employment

tax liability of $15,597. N

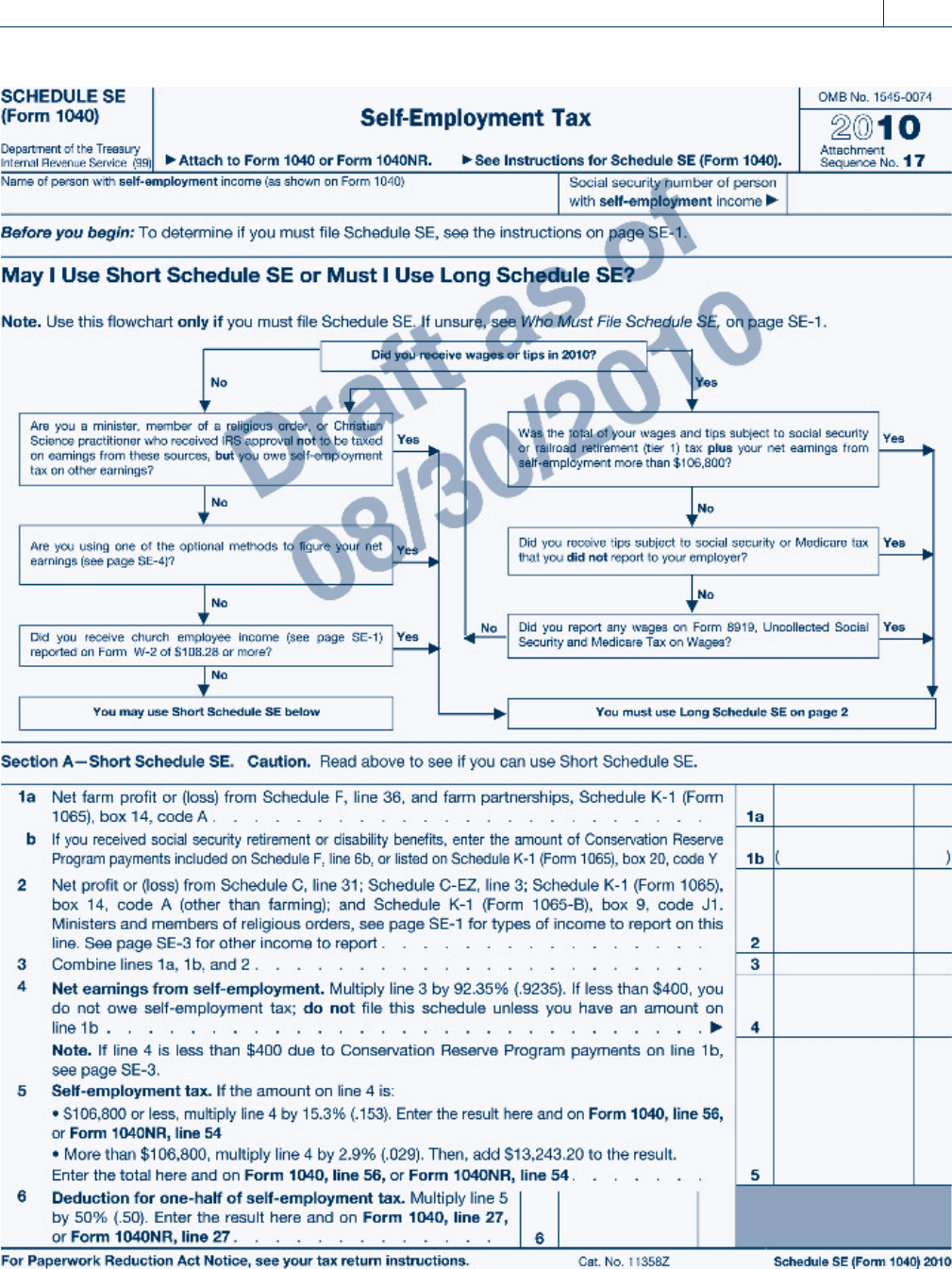

The calculation summarized here is done on page 2 of Schedule SE, Part I, and must be

included with a taxpayer’s Form 1040. Please see pages 9-21 and 9-22 for the same calcu-

lation on Schedule SE.

9-20 Chapter 9

Withholding, Estimated Payments, and Payroll Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Norman

Section 9.6

Self-Employment Tax 9-21

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

130,000

130,000

120,055

120,055

120,055

106,800

9,100

9,100

97,700

12,115

7,799

4,480

15,597

3,482

Norman

9-22 Chapter 9

Withholding, Estimated Payments, and Payroll Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Section 9.6

Self-Employment Tax 9-23

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

106,800

4,480

9-24 Chapter 9

Withholding, Estimated Payments, and Payroll Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 9.7THE FUTA TAX

The Federal Unemployment Tax Act (FUTA) instituted a tax that is not withheld from

employees’ wages, but instead is paid in full by employers. The federal tax rate is 6.2 percent

of an employee’s wages up to $7,000, but a credit is allowed for state unemployment taxes of

5.4 percent. Therefore, the effective federal tax rate is only .8 percent if the state also

assesses an unemployment tax.

EXAMPLE Karen has two employees in 2010, John, who earned $12,500 this

year, and Sue, who earned $5,100. The FUTA tax is calculated as

follows:

John’s wages, $12,500

(maximum $7,000)

$ 7,000

Sue’s wages

$ 5,100

Total FUTA wages $12,100

FUTA tax at .8%

$97

N

Employers report their Federal Unemployment Tax liability for the year on Form 940,

Employer’s Annual Federal Unemployment (FUTA) Tax Return. Like federal income tax

withholding and FICA taxes, federal unemployment taxes must be deposited by electronic

funds transfer or with a commercial bank that is a depository for federal taxes. A deposit is

required when the FUTA taxes for the quarter, plus any amount not yet deposited for the

prior quarter(s), exceed $500. If required, the depo sit must be made by the last day of

the first month after the end of each quarter.

EXAMPLE Ti Corporation’s federal unemployment tax liability for the first quar-

ter of 2010, after reduction by the credit for state unemployment

taxes, is $255; for the second quarter, $200; for the third quarter,

$75; and for the fourth quarter, $25. Ti Corporation must deposit

$530, the sum of the first, second, and third quarters’ liability, by

October 31, 2010. The remaining $25 may be either deposited or paid

with Form 940. N

Employers make the largest portion of unemployment tax payments to state govern-

ments that administer the federal-state program. Employers must pay all state unemploy-

ment taxes for the year by the due date of the federal Form 940 to get full credit for the

state taxes against FUTA.

Self-Study Problem 9.6

Robert Boyd is self-employed in 2010. His Schedule C net income is $27,450

for the year, and Robert also had a part-time job and earned $4,400 that

was subject to FICA tax. Robert receiv ed taxable dividends of $1,110 during

the year, and he had a capital gain on the sale of stock of $9,100. Calculate

Robert’s self-employment tax using Schedule SE of Form 1040 on pages 9-23

and 9-24.

Section 9.7

The FUTA Tax 9-25

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 9.8

THE NANNY TAX

Over the years, the taxation and reporting of household employees’ wages has caused many

problems for taxpayers and the IRS. The threshold for filing was low ($50 per quarter of

wages), and the tax forms to be completed were complex. As a result, many taxpayers

ignored the reporting of household workers’ wages and taxes. Congress addressed this

problem by enacting what are commonly referred to as the ‘‘nanny tax’’ provisions.

These provisions simplified the reporting process for employers of domestic household

workers.

Household employers are not required to pay FICA taxes on cash payments of less

than $1,700 paid to any household employee in a calendar year. If the cash payment to

any household employee is $1,700 or more in a calendar year, all the cash payments

(including the first $1,700) are subject to FICA and Medicare taxes (see Section 9.3).

The $1,700 threshold is indexed each year. Household employers must also withhold

income taxes if requested b y the employee and are required to pay FUTA tax (see Sec-

tion 9.7) if more than $1,000 in cash wages are paid to household employees during

any calendar quarter.

A taxpayer is a household employer if he or she hires workers to perform household

services, in or around the taxpayer’s home, that are subject to the ‘‘will and control’’ of

the taxpayer. Examples of household workers include:

Babysitters

Caretakers

Cooks

Drivers

Gardeners

Housekeepers

Maids

If the household worker has an employee-employer relationship with the taxpayer, it

does not matter if the worker is called something else, such as ‘‘independent contrac-

tor.’’ Also, it does not matter if the worker works full- or part-time. The household

employer is responsible for t he proper reporting, withholding, and payment of any

taxes due.

Self-Study Problem 9.7

The Rhus Company’s payroll information for 2010 is summarized as follows:

Quarter 1 Quarter 2 Quarter 3 Quarter 4

Gross earnings of employees $25,000 $30,000 $26,000 $32,000

Individual employee earnings

in excess of $7,000 None $ 4,000 $15,000 $20,000

Rhus Company (E.I.N. 94-0001112) pays California state unemployment tax.

The company makes the required deposits of both federal and state unemploy-

ment taxes on a timely basis. Complete the Rhus Company’s 2010 Form 940 on

pages 9-27 and 9-28, using the above information.

9-26 Chapter 9

Withholding, Estimated Payments, and Payroll Taxes

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.