Blank L., Tarquin A. Engineering Economy (McGraw-Hill Series in Industrial Engineering and Management)

Подождите немного. Документ загружается.

3. Finally, Kathy asked Bob to reevaluate the cash

flows for Homeworth at the

MARR

of

35%, but

using a reinvestment rate

of

45% to determine

if

the series is sti

ll

justified.

Case Study Exercises

1, 2, and 3. Answer the questions for Bob using

spreadsheets.

CASE

STUDY

275

4.

If

the

i'

approximating procedure Bob developed

is

not available, use the original cash flow data to

apply the basic net-investment procedure, and

answer Exercises 2 and

3, where c

is

35 and 45%,

respectively.

5. Kathy concluded from this exercise that any cash

flow series is economically

ju

stified for any rein-

vestment rate that is larger than the MARR. Is this

a correct conclusion? Explain why or why not.

LLI

I-

I

u

Rate

of

Return Analysis:

Multiple

Alternatives

This

chapter

presents

the

methods

by

which

two

or

more

alternatives

can

be

evaluated

using a rate

of

return

(ROR)

comparison

based

on

the

methods

of

the

previous

chapter.

The

ROR

evaluation

correctly

performed

will result in

the

same

selection

as

the

PW,

AW,

and

FW

analyses,

but

the

computational

procedure

is

considerably

different

for

ROR

evaluations

.

The

first

case

study

involv

es

multiple

options

for

a business

owned

for

many

years

by

one

person.

The

second

case

explores

nonconventional

cash

flow

series

with

multiple

rates

of

return

and

the

use

of

the

PW

method

in

this

situation.

LEARNING OBJECTIVES

Purpose: Select

the

best mutually exclusive alternative on

the

basis

of

rate

of

return analysis

of

incremental

cash

flows.

Why incremental analysis?

Incremental

cash

flows

Interpretation

Incremental ROR by

PW

Incremental ROR by

AW

Multiple

alternatives

Spreadsheets

This

chapter

will

help

you:

1. State

why

an incremental analysis

is

necessary

for

comparing

alternatives

by

the

ROR

method.

2.

Prepare a

tabulation

of

incremental

cash

flows

for

two

alternatives.

3.

Interpret

the

meaning

of

ROR

on

the

incremental

initial

investment.

4.

Select

the

better

of

two

alternatives using incremental

or

breakeven

ROR

analysis based on

present

worth.

5.

Select

the

better

of

two

alternatives using a

ROR

analysis

based

on

annual

worth.

6.

Select

the

best

of

multiple

alternatives using

an

in

crementa

l

ROR

analysis.

7.

Develop

spreadsheets

that

include

PW,

AW, and

ROR

evaluation

for

multiple,

different-life

alternatives.

278

Mutua

ll

y exc

lu

si

ve

Indepe

nd

ent projects

CH

APTER

8 Rate

of

Return Anal

ys

is: Multiple Alterna

ti

ve

s

8.1

WHY

INCREMENTAL ANALYSIS

IS

NECESSARY

Wh

en two or more mutually exclusive alternatives are

ev

aluated, engin

ee

ring

economy can

id

entify the one alternative that

is

the best economically. As we

have l

ea

rn

ed, the

PW

, AW, and FW techniques can be used to do so. Now the

pro

ce

dur

e for us

in

g

ROR

to identify the b

es

t is

pr

esented.

Le

t

's

assume that a

co

mpany uses a

MARR

of 16% per year, that the c

omp

any

has

$9

0,

000

available for investment, and that two alternatives (A and B) are

being eva

lu

ated. Alternative A requires an investment

of

$50,000 and has an

internal rate of return i

't.

of 35% per year. Alternative B requires $85,000 and has

an

i

;

~

of

29% per year. Intuitively we may conclude that the better alternative is

the one that has the larger return, A

in

this case.

How

ever, this is not necessarily

so. While A has the

hi

gher pro

ject

ed return, it requires an initial investment that

is much less than the total money available ($90,

000

).

Wh

at happens to the in-

vestment

ca

pital that is left

ove

r? It is

ge

nera

ll

y assumed that excess funds will

be

in

vested at

th

e compan

y's

MARR, as we learned

in

the previous

chapt

e

r.

Us

in

g t

hi

s assumption,

it

is possible to determine the consequences

of

the alter-

na

ti

ve

in

vestment

s.

If

alterna

ti

ve A is sel

ec

ted, $

50

,

000

will return 35% per yea

r.

The

$40

,000 l

ef

t

ove

r will be

in

vested at the

MARR

of 16% per year.

The

rate

of

return on the total capital available, then, will be the weighted average. Thus, if

a

lt

e

rn

ative A is sele

ct

ed,

Ove

ra

ll

ROR =

50

,

000

(0

.3

5) +

40

,

000

(0.

16

) = 26.6%

A 90,000

If alte

rn

a

ti

ve B is selected, $85,000 will be invested at 29% per year, and the

remaining $5000 will ea

rn

16% per year.

No

w the weighted average is

Ov

era

ll

ROR

= 85,

000

(0.29) +

5000

(0.16) = 28.3%

B 90,000

These calc

ul

a

ti

ons show that even though the i* for alterna

ti

ve A is

hi

gher,

a

lt

e

rn

a

ti

ve B presents the bett

er

ove

ra

ll

ROR

f

or

the $90,000.

If

either a PW

or AW comparison is conducted using the

MARR

of 16% per y

ea

r as i, alterna-

ti

ve B will be chosen.

This simple

exa

mple illustrates a major fact about the rate

of

return me

th

od

for

co

mpa

ri

ng alternatives:

Under

some circumstances, project

ROR

values do not provide the same

ranking

of

alternatives as do PW, A

W,

and

FW

analyses. This situation

does not occur if

we

conduct an incremental cash flow

ROR

analysis (dis-

cussed in the next section).

When independent proje

ct

s are

ev

aluated, no incremental analysis is neces-

sary between projects. Each project is

ev

aluated separately from others, and

more

th

an one

ca

n be selected.

Th

e

ref

ore, the only c

omp

arison is with the do-

nothing alternative for each project.

Th

e

ROR

can be used to accept or reje

ct

each independent project.

SECTIO 8.2

Calculation

of

In

cremental Cash Flows for ROR Analysis

TABLE

8-1 Format for Incremental Cash Flow Tabulation

Yea

r

o

A

lterna

ti

ve

A

(1 )

Cash Flow

Alternativ

e B

(2)

Incr

emen

ta

l

Cash Flow

(3) = (2) - (1)

8.2 CALCULATION OF INCREMENTAL CASH FLOWS

FOR

ROR

ANALYSIS

It

is

necessary to prepare an incremental cash flow tabulation between two alter-

natives

in

preparation for an incremental

ROR

analysis. A standardized format for

the tabulation will simplify this process.

The

column headings are shown in

Table

8-1.

If

the alternatives have equal lives, the year column will go from 0 to n.

If

the alternatives have unequal liv

es,

the year column will go from 0 to the

LCM

(least common multiple)

of

the two lives.

The

use

of

the

LCM

is necessary be-

cause incremental

ROR

analysis requires equal-service comparison between

alternatives. Therefore, all the assumptions and requirements developed earlier

apply for any incremental

ROR

evaluation. When the

LCM

of

lives is used, the

salvage value and reinvestment

in

each alternative are shown at appropriate time

s.

If

a planning period is defined, the cash flow tabulation is for the specified period.

Only for the purpose

of

simplification, use the convention that between two

alternatives, the one with the

larger initial investment will

be

regarded as alter-

native

B.

Then, for each year

in

Table

8-1,

Incremental cash flow = cash

flowB

- cash flow A

[8

.

1]

The initial investment and annual cash flows for each alternative (excluding the

salvage value)

occur

in

one

of

two patterns identified in Chapter

5:

Revenue alternative, where there are both negative and positive cash flows.

Service alternative, where all cash flow estimates are negative.

In either case, Equation

[8.1]

is

used to determine the incremental cash flow series

with the sign

of

each cash flow carefully determined.

The

next two examples

illustrate incremental cash flow tabulation

of

service alternatives

of

equal and

different live

s.

Later

examp

les treat revenue alternatives.

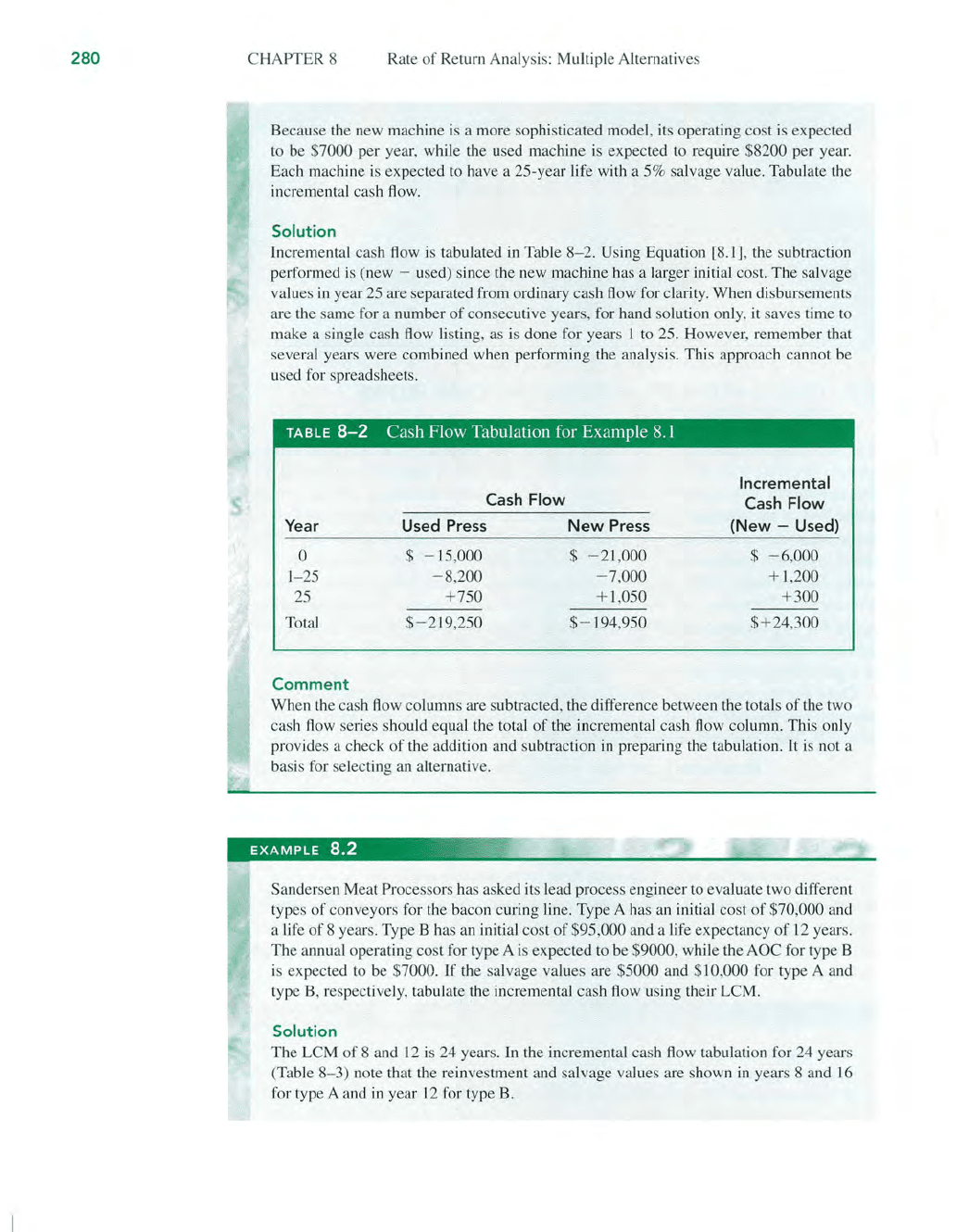

EXAMPLE

8.1 { ,

A tool and die company

in

Pittsburgh is considering the purchase

of

a dri

ll

press with

fuzzy-logic software to improve accuracy and reduce tool wear. The company has

the opportunity

to

buy a slightly used machine for $15,000 or a new one for $21,000.

279

I Sec.5.1 I

Revenue and

se

rvi

ce

280

CHAPTER 8 Rate

of

Return Analysis:

Mu

ltiple Alterna

ti

ves

Because

th

e new machine is a more sophisticated model, its operat

in

g cost is expected

to be

$7000 per year, while the used machine is expected to require $8200 per yea

r.

Each machine is expected

to

have a 25-year life with a 5% sa

lv

age va

lu

e.

Tabulate the

incremental cash

flow.

Solution

In

cremental cash flow is tabulated

in

Table

8-2.

Using Equation [8.1], the subtraction

perfo

rm

ed is (new - used) since the new machine has a larger initial cost. The salvage

va

lu

es

in

year 25 are separated from ordinary cash flow for clarity. When disbursements

are the same for a number

of

consecutive years, for hand solution onl

y,

it saves time to

make a single cash flow

li

sting,

as

is done for years l

to

25. However, remember

th

at

several years were combined when performing the analysis. This approach cannot be

used for spreadsheets.

TABLE

8-2

Cash Flow Tabulation for Example 8.1

Year

o

1

-2

5

25

Total

Comment

Cash Flow

Used Press

$ -

15

,000

-8,2

00

+ 750

$

-2

19

,2

50

New

Press

$ - 21,000

- 7,000

+ 1,050

$-

194,950

Incremental

Cash Flow

(New

- Used)

$ - 6,000

+ 1,200

+3

00

$+24,3

00

When

th

e cash

fl

ow columns are subtracted, the difference between the totals of the two

cash

flow

series should equal the total

of

the incremental cash

flow

column. This on

ly

provides a check of the addition and

su

btraction

in

preparing

th

e tabulation. It is not a

basis for select

in

g an alternative.

EXAMPLE

8.2

,.~

Sandersen Meat Processors has asked

it

s lead process engineer

to

evaluate two different

types

of

conveyors for the bacon curing line. Type A has

an

initial cost

of

$70,000 a

nd

a life

of

8 years. Type B has

an

initial cost

of

$95,000 and a life expectancy

of

12 years.

The annual operating cost for type A is expected

to

be

$9000, while the AOC for

ty

pe B

is

ex

pected

to

be $7000. If

th

e salvage values are $5000 and $

10

,000 for type A a

nd

type S,

re

spective

ly,

tabulate

th

e incremental cash flow us

in

g

th

e

ir

LCM.

Solution

The LCM

of

8 a

nd

12

is 24 years. In the

in

cremental cash flow tabulation for 24 years

(Ta

bl

e

8-3)

note that the reinvestment a

nd

salvage

va

lu

es are shown

in

years 8 and

16

for type A and

in

year

12

for type B.

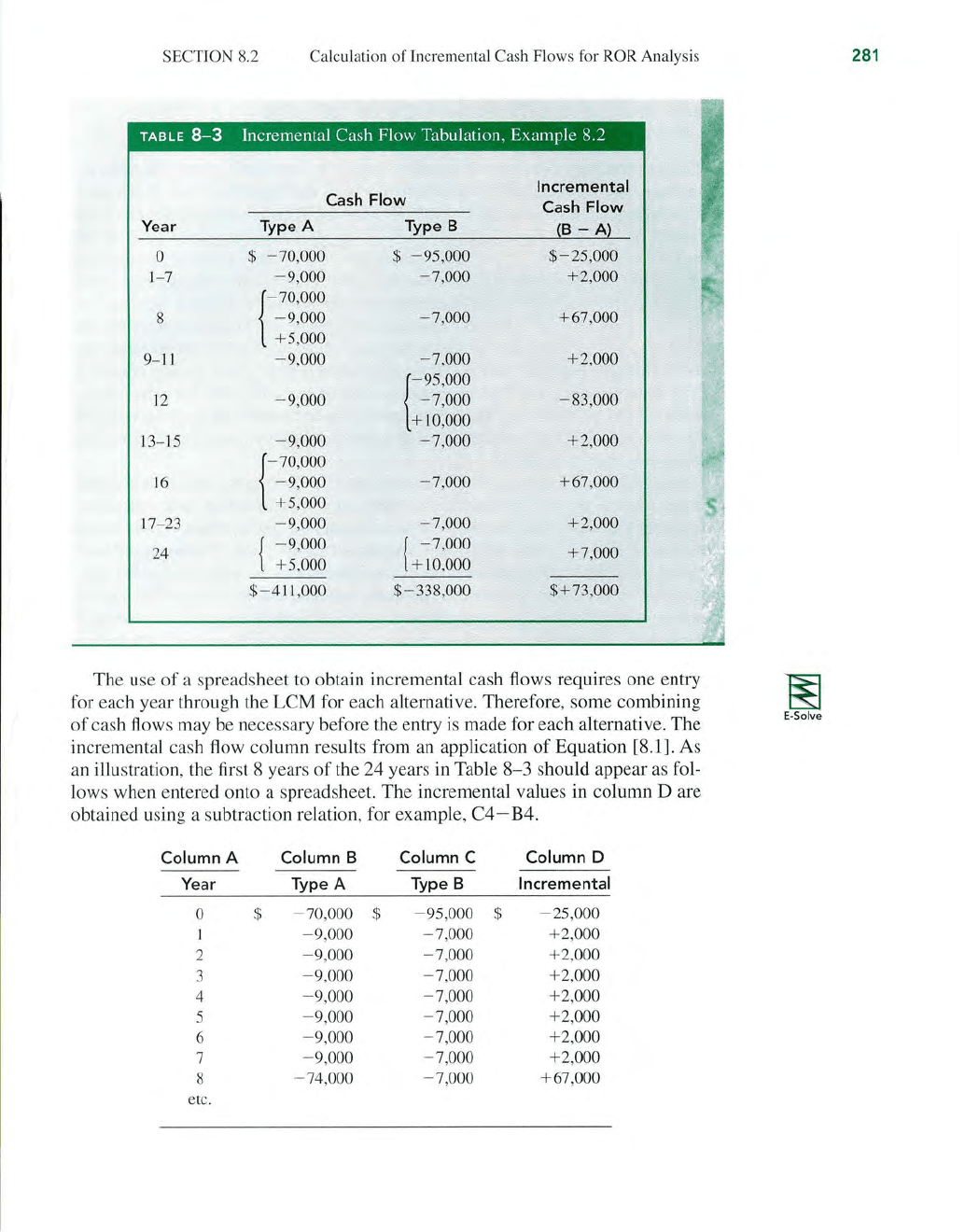

SECTI

ON

8

.2

Calculation of Incremental Cash Flows for ROR Analysis

TABLE

8-3

Incremental Cash Flow Tabulation, Example 8.2

Cash

Fl

ow

Incremental

Cash

Flow

Ye

ar

Type A

Type 8

(8

-

A}

0

$ - 70,000

$

- 95,000

$-2

5,000

1- 7

- 9,000

- 7,000

+2

,000

C

7O

,

OOO

8

- 9,000

- 7,000

+67,0

00

+ 5,000

9-

11

- 9,000

- 7,000

+2,000

C

95

,OOO

12

- 9,000

- 7,000 - 83,000

+10

,000

13

-

15

- 9,000

- 7,000

+2

,000

C

7O

,

OOO

16

- 9,000 - 7,000

+67

,000

+ 5,000

17

- 23

- 9,000 - 7,000 +2,000

24

- 9,000

{ - 7,000

+7,000

+ 5,000

+ 10,000

$- 411,000 $- 338,000

$+73

,000

The use

of

a spreadsheet to obtain incremental cash flows requires one entry

for each year through

th

e LCM for each alternative. Therefore, some combining

of cash flows may be necessa

ry

before the entry is made for each alternative. The

incremental cash

fl

ow column results from an application

of

Equation

[8

.1]. As

an illustration,

th

e first 8 years

of

the 24 years in Table

8-3

should appear

as

fol-

lows when entered onto a spreadsheet. The incremental values in column

Dare

obtained using a subtraction relation, for example,

C4-

B4.

Column A

Column B Column C Column D

Year Type A Type B

Incremental

0 $

- 70,000

$

-

95

,000

$

- 25,000

- 9,000

- 7,000

+ 2,000

2

- 9,000

- 7,000 + 2,000

3

- 9,000 - 7,000 + 2,000

4

- 9,000 - 7,000 + 2,000

5

-

9,

000 - 7,000 + 2,000

6

- 9,000

-7

,000 + 2,000

7

- 9,000

- 7,000

+2,000

8

- 74,000

- 7,000

+ 67,000

etc.

281

m

E-

So

l

ve

282

CHAPTER 8 Rate

of

Return Analysis: Multiple Alternatives

8.3 INTERPRETATION

OF

RATE

OF

RETURN

ON

THE EXTRA INVESTMENT

The

incremental cash flows

in

year 0

of

Tables 8- 2 and

8-3

reflect the extra in-

vestment or cost required

if

the alternative with the larger first cost is selected.

This

is

important in an incremental ROR analysis in order to determine the

ROR

earned on the extra funds expended for the larger-investment alternative.

If

the

incremental cash flows

of

the larger investment don'tjustify it, we must select the

cheaper one. In Example 8.1 the new drill press requires an extra investment

of

$6000 (Table

8-2)

.

If

the new machine

is

purchased, there will be a "savings"

of

$1200 per year for 25 years, plus an extra $300

in

year 25.

The

decision to buy the

used or new machine can be made on the basis

of

the profitability

of

investing the

extra

$6000 in the new machine.

If

the equivalent worth

of

the savings is greater

than the equivalent worth

of

the extra investment at the MARR, the extra invest-

ment should be made (i.e., the larger first-cost proposal should be accepted).

On

the other hand, if the extra investment

is

not justified

by

the savings, select the

lower-investment proposal.

It is important to recognize that the rationale for making the selection decision

is

the

same

as if only one alternative were under consideration, that alternative

being the one represented by the incremental cash flow series. When viewed in this

manner, it

is

obvious that unless this investment yields a rate

of

return equal to or

greater than the MARR, the extra investment should not be made. As further clar-

ification

of

this extra-investment rationale, consider the following:

The

rate

of

return attainable through the incremental cash flow is an alternative to investing at

the

MARR

. Section 8.1 states that any excess funds not invested in the alternative

are assumed to be invested at the MARR.

The

conclusion

is

clear:

If

the

rate

of

return

available through the incremental cash flow equals

or

exceeds the MARR, the alternative associated with the

extra

investment

should be selected.

Not only must the return on the extra investment meet or exceed the MARR,

but also the return on the investment that

is

common

to

both alternatives must meet

or exceed the MARR. Accordingly, before starting an incremental

ROR analysis,

it

is

advisable

to

determine the internal rate

of

return

i*

for each alternative.

(Of

course, this

is

much easier with evaluation by computer than by hand.) This can be

done only for revenue alternatives, because service alternatives have only cost

(negative) cash flows and no

i*

can be determined. The guideline

is

as

follows:

For

multiple revenue alternatives, calculate the internal

rate

of

return

i*

for each alternative,

and

eliminate all alternatives

that

have

an

i*

< MARR.

Compare

the remaining alternatives incrementally.

As an illustration,

if

the

MARR

= 15% and two alternatives have

i*

values

of

12

and

21

%, the 12% alternative can be eliminated from further consideration.

With only two alternatives, it

is

obvious that the second one

is

selected.

If

both

alternatives have i*

<

MARR

, no alternative

is

justified and the do-nothing alter-

native

is

the best economically. When three or more alternatives'are evaluated, it

SECTION

8.4

Rate

of

Return Eva

lu

ation Using PW: Incremental and Bre

akeve

n

is

usually worthwhile, but not required, to calculate

i*

for each alternative for

preliminary screening. Alternatives that

cannot

meet the

MARR

may be elimi-

nated from further evaluation using this option. This option is especially useful

when performing the analysis by computer.

The

IRR

function applied to each

alternative's cash flow

est

imates can quickly indicate unacceptable alternatives,

as demonstrated later

in

Section 8.6.

When independent projects are

eva

luated, there is no comparison on the extra

investment.

Th

e ROR value

is

used to accept all projects with i*

:::::

MARR,

assum-

ing there

is

no budget limitation.

For

examp

le, assume

MARR

= 10%, and three

independent projects are available with

ROR

values of:

it = 12%

i

~

= 9% it =

23

%

Projects A and C are selected, but B is not because

i~

'

<

MARR.

Example 8.8 in

Section 8.7 on spreadsh

ee

t applications illustrates selection from independent

projects using

ROR values.

8.4

RATE

OF RETURN EVALUATION USING

PW:

INCREMENTAL

AND

BREAKEVEN

In this section

we

discuss the primary approach to making mutually exclusive

alternative selections by the incremental

ROR

method. A PW-based relation like

Equation [7.1]

is

developed for the incremental cash flows.

Use

hand

or

com-

puter means to find

~i'~

-

A'

the internal

ROR

for the series. Placing

~

(delta) be-

fore

iJ

~

- A

distinguishes it from the ROR values it and

i~.

Since incremental ROR requires equal-service comparison, the

LCM

of

lives

must be used

in

the PW formu lation. Because

of

the reinvestment requirement for

PW

analysis for different-life assets, the incremental cash flow series may con-

tain several sign changes, indicating multiple

~i

*

values. Though incorrect, this

indication

is

usually neglected in actual practice.

The

correct approach

is

to es-

tablish the reinvestment rate c and follow the approach

of

Section 7.5. This means

that the unique composite rate

of

return

(~i')

for the incremental cash flow series

is determined.

These

three required

elements-incremental

cash flow series,

LCM, and multiple root

s-a

re the primary reaso

ns

that the

ROR

method is often

applied incorrectly

in

engineering economy analyses

of

multiple alternatives. As

stated earlier,

it

is always possible, and generally advisable, to use a

PW

or

AW

analysis at an established MARR

in

lieu

of

the ROR method when multiple rates

are indicated.

Th

e complete procedure by hand

or

computer

for an incremental

ROR

analy-

sis for two alternatives is as follows:

1.

Order the alternatives by initial investment

or

cost, starting with the smaller

one

, called

A.

The

one

with the larger initial investment

is

in the column

labeled B

in

Table 8-

1.

2. Develop the cash flow and incremental cash flow series using the

LCM

of

years, assuming reinvestment

in

alternatives.

3.

Draw an incremental cash flow diagram,

if

needed.

283

Q-Solv

284

Multiple-root tests

CHAPTER

8 Rate

of

Return Analysis: Multiple Alternatives

4. Count the number

of

sign changes in the incremental cash flow series to deter-

mine

if

multiple rates

of

return may be present.

If

necessary, use Norstrom's

criterion on the cumulative incremental cash flow series to determine

if

a

si

ngle positive root exists.

5.

Set up the

PW

equation for the incremental cash flows

in

the form

of

Equa-

tion [7.1], and determine

~i~~A

using trial and error by hand

or

spreadsheet

functions.

6. Select the economically better alternative as follows:

If

~i~~A

<

MARR,

select

alternative

A.

If

~i~~A

2':

MARR,

the

extra

investment is justified; select

alterna-

tive B.

If

the incremental i* is exactly equal to

or

very near the

MARR,

noneco-

nomic considerations will most likely be used to help

in

the selection

of

the

"best" alternative.

In

step 5,

if

trial and error

is

used to calculate the rate

of

return, time may be

saved

if

the

~i'~

~ A

value is bracketed, rather than approximated by a point value

using lin

ear

interpolation, provided that a single

ROR

value is not needed.

For

example

, if the

MARR

is

15

%

per

year and you have estab

li

shed that

~i~

~ A

is in

the

15

to 20% range, an exact value

is

not necessary to accept B since you al-

ready know that

~i~

~ A

2': MARR.

The

IRR function on a spreadsheet will normally determine

one

~i*

value.

Multiple guess va

lu

es

ca

n be input to find multiple roots

in

the range - 100%

to

00

for a nonconventional series, as illustrated

in

Examples 7.4 and 7.5.

If

this

is

not the case, to be correct, the indication

of

multiple roots

in

step 4 requires

that the net-investment procedure, Equation [7.6], be applied

in

step 5 to make

~i'

=

~i*

.

If

one

of

these multiple roots is the same as the expected reinvest-

ment rate c, this root can be used as the

ROR

value, and the net-investment pro-

cedure

is

not necessary. In this

case

only,

~i'

=

~i*

,

as concluded at the end

of

Section 7.5.

Tn

2000, Bell Atlantic and

GTE

merged to form a gia

nt

telecommunications corporation

named Verizon Communications. As expected, some equipment incompatibil.ities had to be

rectified, especia

ll

y for long distance and international wireless and video services.

One

item had two

suppliers-a

U.S. firm (A) and an Asian firm (B). Approximately 3000 units

of

this

equipment

were needed. Estimates for vendors A and B are given for each uni

t.

A ·8

Initial cost, $

- 8,000

-13,0

00

Annual costs, $

- 3,500 - 1

,6

00

Salvage value, $

0

2,000

Life, years

10

5