Blank L., Tarquin A. Engineering Economy (McGraw-Hill Series in Industrial Engineering and Management)

Подождите немного. Документ загружается.

The ch

apte

rs in this level

ex

t

end

the u

se

of

e

co

nomic

ev

al

uation

tools

into

real-world situ

at

ions. A large

pe

r

centage

of

eco

n

omi

c evaluations involve

ot

h

er

than

se

l

ect

ion

fr

om

new assets

or

pro

je

cts.

Probably

the

most

c

om-

monly

performed

evaluati

on

is

t

hat

of

replac

ing

or

retaining an i

n-place

asset. R

eplacement

analysis

app

lies the evaluation

tools

to

make

the

correct

econom

ic choice.

Often

the

eva

lu

atio

n involves ch

oosing

fr

om

independent

projects

unde

r

the

restriction of l

imited

capital

investme

nt. Th

is

requires a special

technique

that

is

based on the pr

evio

us ch

apters

.

Future estimates are

certainly

not

exact. Therefore, an

alternative

should

n

ot

be

se

lected on

th

e basis

of

fixed es

timate

s

only

. Breakev

en

analysis

ass

ists in

th

e eva

lu

ati

on

process of a ran

ge

of

est

imates

for

P,

A,

F,

i,

or

n,

an

d operating

va

ri

ab

les such

as

pro

duction level,

workfor

ce size,

design

cost, raw mate

ri

al cost, a

nd

sales p

ri

ce. Spreadsheets

speed

up

this

impor-

ta

nt

,

but

o

ft

en detailed, analysis tool.

Important

note:

If

asset

depreciation

and

taxes

are

to

be

considered

by

an

after-tax

analysis,

Chapters

16

and

17

should

be

covered

before

or

in

conjunction

with

these

chapters. See

the

Preface

for

options.

11

UJ

I

u

Replacement and

Retention Decisions

One

of

the

most

commonly

performed

engineering

economy

studies

is

that

of

replacement

or

retention

of

an asset

or

system

that

is

currently installed.

This differs

from

previous studies

where

all

the

alternatives are

new

. The

fundamental

question

answered

by

a

replacement

study

about

a currently

installed asset

or

system

is,

Should

it

be

replaced

now

or

later?

When

an

asset

is

currently

in

use

and

its

function

is

needed

in

the

future,

it

will

be

replaced

at

some

time

. So, in reality, a

replacement

study

answers

the

ques-

tion

of

when,

not

if,

to

replace.

A

replacement

study

is

usually

designed

to

first

make

the

economic

deci-

sion

to

retain

or

replace

now

.

If

the

decision

is

to

replace,

the

study

is

com-

plete.

If

the

decision

is

to

retain,

the

cost

estimates

and

decision

will

be

revisited each year

to

ensure

that

the

decision

to

retain

is

still

economically

correct. This

chapter

explains

how

to

perform

the

initial year

and

follow-on

year

replacement

studies.

A

replacement

study

is

an

application

of

the

AW

method

of

comparing

unequal-life

alternatives, first

introduced

in

Chapter

6.

In

a

replacement

study

with

no

specified

study

period,

the

AW

values are

determined

by

a

technique

of

cost

evaluation

called

the

economic

service life

(ESL)

analysis.

If a

study

period

is

specified,

the

replacement

study

procedure

is

different

from

that

used

when

no

study

period

is

set

. All

these

procedures

are

covered

in

this

chapter.

The

case

study

is

a real-world

replacement

analysis

involving

in-place

equipment

and possible

replacement

by

upgraded

equipment.

If

asset depreciation and taxes are

to

be

considered

in

an

after-tax

replacement

analysis, Chapters

16

and

17

should be covered before

or

in

conjunction

with

this chapter.

After-tax

replacement analysis

is

included

in

Section

17.7.

LEARNING OBJECTIVES

Purpose: Perform a replacement study

between

an

in-place asset

or

system and a

new

one

that

could replace it.

Basics

Economic service life

Replacement

study

Study period

This

chapter

will

help

you:

1.

Understand

the

fundamentals

and

terms

for

a

replacement

study

.

2.

Determine

the

econom

ic service

lif

e

of

an

asset

that

minimizes

the

total

AW

of

costs.

3. Perform a

replacement

study

between

the

defender

and

the

best

challenger.

4.

Understand

how

to

address several aspects

of

a

replacement

study

that

may

be

experienced.

5. Perform a

replacement

study

over

a

specified

number

of

years.

388 CHAPTER

II

Replacement and Retention Decisions

11.1 BASICS OF THE REPLACEMENT STUDY

The need for a replacement study can develop from several sources:

Reduced

performance.

Because

of

physical deterioration, the ability to per-

form at an expected level

of

reliability (being available and performing

correctly

when, needed) or productivity (performing at a given level

of

quality and quantity) is not present. This usually results in increased costs

of

operation, higher scrap and rework costs, lost sales, reduced quality, di-

minished safety, and larger maintenance expenses.

Altered

requirements.

New requirements

of

accuracy, speed, or other spec-

ifications cannot be met by the existing equipment or system.

Often the

choice is between complete replacement or enhancement through retro-

fitting or augmentation.

Obsolescence. International competition and rapidly changing technology

make currently used systems and assets perform acceptably but less pro-

ductively than equipment coming available. The ever-decreasing develop-

ment cycle time to bring new products to market is often the reason for

premature replacement studies, that is, studies performed before the esti-

mated useful or economic life is reached.

Replacement studies use some terminology that is new, yet closely related

to

terms

in

previous chapters.

Defender

and

challenger

are the names for two mutually exclusive alterna-

tives. The defender is the currently installed asset, and the challenger is the

potential replacement. A replacement study compares these two alterna-

tives. The challenger

is

the "best" challenger because it has been selected

as the one best challenger to possibly replace the defender. (This

is

the

same terminology used earlier for incremental

ROR

and B/C analysis of

two new alternatives.)

A W values are used as the primary economic measure

of

comparison between

the defender and challenger. The term

EUAC (equivalent uniform annual

cost) may be used in lieu

of

AW,

because often only costs are included

in

the

evaluation; revenues generated by the defender

or

challenger are assumed

to be equal. Since the equivalence calculations for

EUAC are exactly the

same as for A

W,

we use the term A W. Therefore, all values will be negati ve

when only costs are involved. Salvage value,

of

course,

is

an exception; it

is

a cash inflow and carries a plus sign.

Economic

service life (ESL) for an alternative is the

number

of

years at

which the lowest

AW

of

cost occurs. The equivalency calculations to deter-

mine

ESL

establish the life n for the best challenger, and it also establishes

the lowest cost life for the defender in a replacement study. (The next sec-

tion

of

this chapter explains how to find the

ESL

by hand and by computer

for any new or currently installed asset.)

Defender

first cost is the initial investment amount P used for the defender.

The

current

market

value (MV) is the correct estimate to use for P for the

SECTION

11.1

Basics

of

the Replacement Study

defender

in

a replacement study. The fair market value may be obtained

from professional appraisers, resellers, or liquidators who know the value

of

used assets.

The

estimated salvage value at the end

of

1 year becomes the

market value at the beginning

ofthe

next year, provided the estimates remain

correct

as

the years pass. It

is

incorrect to use the following as

MV

for the de-

fender first cost: trade-i n val ue that

does not represent

afair

market value, or

the depreciated book value taken from accounting records.

If

the defender

must be upgraded or augmented to make it equivalent to the challenger (in

speed, capacity, etc.), this cost is added to the

MV

to obtain the estimate

of

defender first cost. In the case

of

asset augmentation for the defender alterna-

tive, this separate asset and its estimates are included along with the installed

asset estimates to form the complete defender alternative. This alternative is

then compared with the challenger via a replacement study.

Challenger first cost

is

the amount

of

capital that must be recovered (amortized)

when replacing a defender with a challenger. This amount is almost always

equal to

P, the first cost

of

the challenger. On occasion, an unrealistically high

trade-

in

value may be offered for the defender compared to its fair market

value. In this event, the

net cash flow required for the challenger

is

reduced,

and this fact should be considered in the analysis. The correct amount to re-

cover and use in the economic analysis for the challenger

is

its first cost minus

the difference between the trade-in value (TIV) and market value (MV)

of

the

defender. In equation form, this

is

P - (TIV - MV). This amount represents

the actual cost to the company because it includes both the opportunity cost

(i.e., market value

of

the defender) and the out-of-pocket cost (i.e

.,

first

cost - trade-in) to acquire the challenger.

Of

course, when the trade-in and

market values are the same, the challenger

P value is used in all computations.

The

challenger first cost

is

the estimated initial investment necessary to ac-

quire and install

it.

Sometimes, an analyst or manager will attempt to increase

this first cost

by

an

amount equal to the unrecovered capital remaining in the de-

fender

as

shown on the accounting records for the asset. This is observed most

often when the defender

is

working well and in the early stages

of

its life, but

technological obsolescence, or some other reason, has forced consideration

of

a

replacement. This unrecovered capital amount is referred to as a

sunk cost. A

sunk cost must not be added to the challenger's first cost, because it will make the

challenger appear to be more costly than it is.

Sunk

costs

are

capital losses

and

cannot

be recovered in a replacement

study.

Sunk

costs

are

correctly handled in the

corporation's

income

statement

and

by tax law allowances.

A replacement study is performed most objectively

if

the analyst takes the

viewpoint

of

a consultant to the company or unit using the defender. In this way,

the perspective taken

is

that neither alternative is currently owned, and the ser-

vices provided

by

the defender could be purchased now with an "investment"

that is equal to its first cost (market value). This is indeed correct because

the market value will be a forgone opportunity

of

cash inflow if the question

389

390

CHAPTER

II

Replacement and Retention Decisions

"Replace

now?" is answered with a no. Therefore, the consultant's viewpoint is a

convenient way to allow the economic evaluation to be performed without bias

for either alternative .. This approach is also referred to as the outsider's viewpoint.

As mentioned in the introduction, a replacement study is an application

of

the

annual worth method. As such, the fundamental assumptions for a replacement

study parallel those

of

an AW analysis.

If

the planning horizon is unlimited, that

is, a study period is not specified, the assumptions are as follows:

1.

The

services provided are needed for the indefinite future.

2.

The

challenger is the best challenger available now and in the future to

replace the defender. When this challenger replaces the defender (now

or

later), it will be repeated for succeeding life cycles.

3. Cost estimates for every life cycle

of

the challenger will be the same.

As expected, none

of

these assumptions

is

precisely correct. We discussed this

previously for the AW method (and the

PW

method).

When

the intent

of

one

or

more

of

the assumptions becomes incorrect, the estimates for the alternatives must

be updated and a new replacement study conducted.

The

replacement procedure

discussed

in

Section 11.3 explains how to do this.

When

the planning horizon

is

limited to a specified study period, the assumptions above do not hold.

The

proce-

dure

of

Section

11.S

discusses how to perform the replacement study

in

this case.

EXAMPLE 11.1

The Arkansas Division

of

ADM, a large agricultural products corporation, purchased a

state-of-the-art ground-leveling system for rice field preparation 3 years ago for

$120,000. When purchased, it had

an

expected service

Hie

of

10

years,

an

estimated

salvage

of

$25,000 after

10

years, and AOC

of

$30,000. Current account book value

is

$80,000. The system

is

deteriorating rapidly; 3 more years

of

use and then salvaging

it

for $10,000 on the intemational used farm equipment network are now the expecta-

tions. The

AOC

is

averaging $30,000.

A substantially improved, laser-guided model is offered today for $100,000 with a

trade-in

of

$70,000 for the current system. The price goes

up

next week to $110,000

with a trade-in

of

$70,000. The ADM division engineer estimates the laser-guided

system

to

have a useful life

of

10

years, a salvage

of

$20,000, and

an

AOC

of

$20,000.

A $70,000 market value appraisal

of

the current system was made today.

If no further analysis

is

made

on

the estimates, state the correct values to include if

the replacement

study

is

performed today.

Solution

Take the consultant's viewpoint and use the most current estimates.

Defender

P = MY = $70,000

AOC

= $30,000

S

= $10,000

n = 3 years

Challeng

er

P = $100,000

AOC

= $20,000

S

= $20,000

n = 10 years

SECTION 11.2 Economic Service Life

The defender's original cost,

AOC, and salvage estimates, as well as its cnrrent book

value, are

all

irrelevant to the replacement study. Only the most current estimates

should be used. From the consultant's perspective, the services that the defender can

provide could be obtained at a cost equal to the defender market value of

$70,000.

Therefore, this

is

the first cost

of

the defender for the study. The other values are

as

shown.

11.2

ECONOMIC SERVICE

LIFE

Until now the estimated life n

of

an

alternative or asset has been stated.

In

real-

ity, the best life estimate to use

in

the economic analysis

is

not known initially.

When a replacement study or

an

analysis between new alternatives is performed,

the best value for n should be determined using current cost estimates. The best

life estimate

is

called the economic service life.

The

economic service life (ESL) is

the

number

of

years

n

at

which the

equivalent

uniform

annual

worth

(AW)

of

costs is

the

minimum,

consid-

ering

the

most

current

cost estimates

over

all possible

years

that

the asset

may provide a needed service.

The ESL

is

also referred

to

as

the economic life or minimum cost life. Once de-

termined, the ESL should be the estimated life for the asset used in

an

engineer-

ing economy study, if only economics are considered. When n years have passed,

the ESL indicates that the asset should be replaced to minimize overall costs. To

perform a replacement study correctly, it is important that the ESL

of

the chal-

lenger and ESL

of

the defender be determined, since their n values are usually

not preestablished.

The ESL

is

determined

by

calculating the total A W

of

costs

if

the asset is in

service 1 year, 2 years, 3 years, and so on, up

to

the last year the asset is consid-

ered useful. Total A W

of

costs is the sum

of

capital recovery (CR), which

is

the

AW

of

the initial investment and any salvage value, and the

AW

of

the estimated

annual operating cost

(AOC), that is,

Total AW =

-capital

recovery - AW

of

annual

operating

costs

=

-CR

-

AWofAOC

[11.1]

The

ESL

is

the n value

for

the smallest total A W

of

costs. (Remember: These

AW

values are cost estimates, so the

AW

values are negative numbers. There-

fore,

$-200

is

a lower cost than

$-500.)

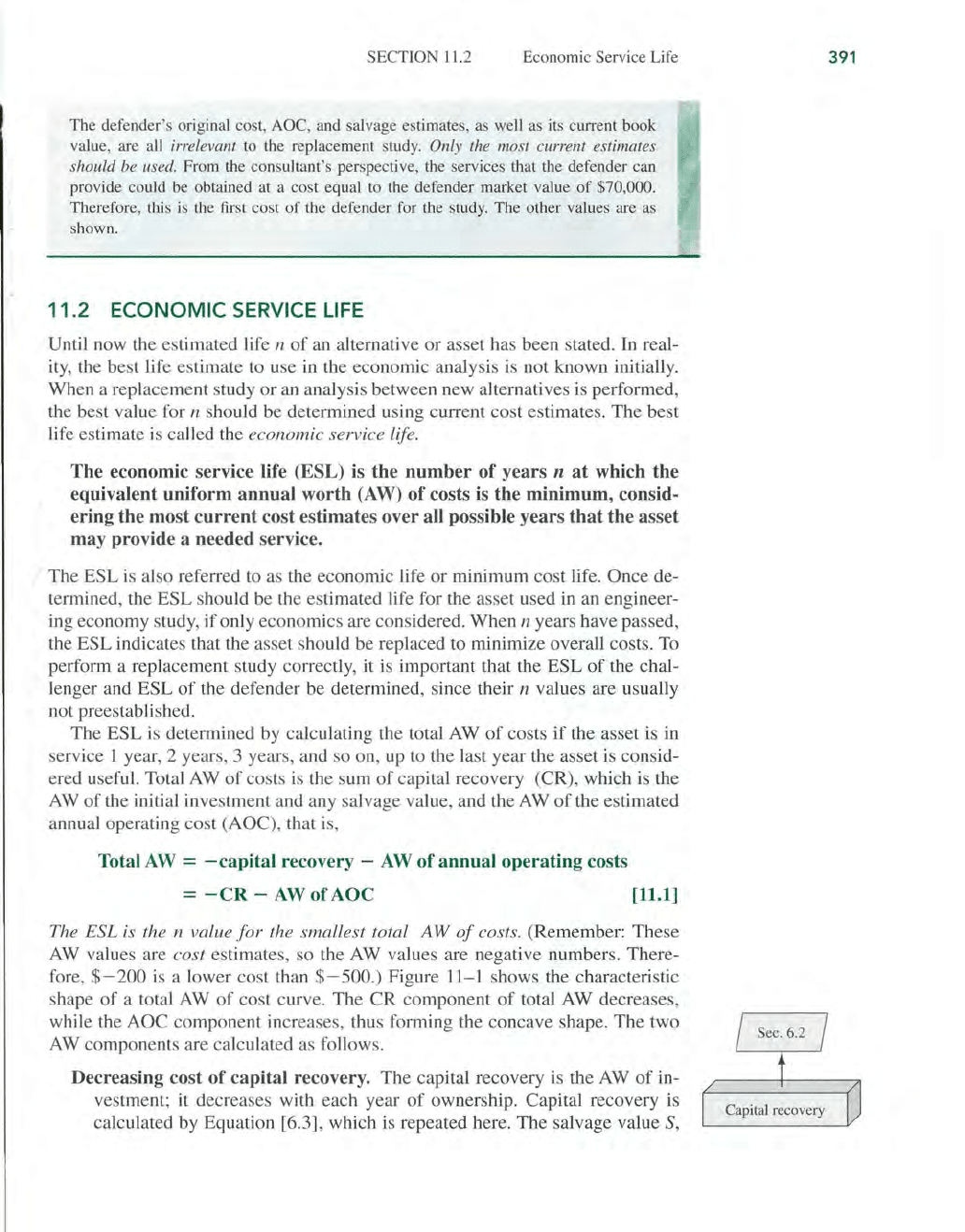

Figure 11-1 shows the characteristic

shape

of

a total

AW

of

cost curve. The CR component

of

total

AW

decreases,

while the

AOC component increases, thus forming the concave shape. The two

A W components are calculated as follows.

Decreasing cost

of

capital recovery. The capital recovery

is

the A W

of

in-

vestment; it decreases with each year

of

ownership. Capital recovery

is

calculated

by

Equation [6.3], which

is

repeated here. The salvage value

S,

391

Capital

recovery

392

Figure

11

-1

Annual worth curves

of

cost elements that

determine the economic

se

rvi

ce life.

m

E-Solve

CHAPTER

11

Larger

co

sts

Replacement and Retention Decisions

Economic

service

lif

e

Years

which usually decreases with time, is the estimated market value (MV) in

that year.

Capital recovery

= -

p(AI

P,i,n) +

S(AI

F,i,n)

[11.2]

Increasing cost

of

AW

of

AOC. Since the

AOC

estimates usually increase

over the years, the AW

of

AOC increases. To calculate the AW

of

the AOC

series for 1,

2,

3,

..

. years, determine the present worth

of

each AOC value

with the

PI

F factor, then redistribute this P value over the years

of

owner-

ship, using the

AlP

factor.

The complete equation for total A W

of

costs over k years is

TotalAW

k

=

-P(A

IP,i,k) +

SiA

IF,i,k) -

[:~AOC/P

I

F'i,j)}A

I

P'i'k)

[11.3]

where

P = initial investment or current market value

Sk

= salvage value or market value after k years

AOC) = annual operating cost for year j

(j

= 1 to

k)

The current MV

is

used for P when the asset is the defender, and the estimated

future MV values are substituted for the S values in years

1,2

, 3, .

..

.

To determine

ESL

by computer, the

PMT

function (with embedded NPV

functions

as

needed)

is

used repeatedly for each year to calculate capital recov-

ery and the

AW

of

AOe.

Their sum is the total AW for k years

of

ownership. The

PMT

function formats for the capital recovery and AOC components for each

year

k are as follows:

Capital recovery for the challenger:

PMT(i%,years,P, - MY

_in_yeack)

Capital recovery for the defender: PMT(i%,years,currencMV, -

MV

_in_yeack)

AW

of AOC:

-PMT(i%,years,NPV(i%,yeacCAOC:year

_k_AOC)+O)

SECTION 11.2

Economic Service Life

When the spreadsheet is developed, it

is

recommended that the

PMT

functions

in

year I be developed using cell-reference format, then drag down the function

through each column. A final column summing the two

PMT

results displays

total A W. Augmenting the table with an Excel

xy

scatter plot graphically displays

the cost curves

in

the general form

of

Figure 11-1, and the

ESL

is easily identi-

fied. Example

11

.2 illustrates

ESL

determination by hand and by computer.

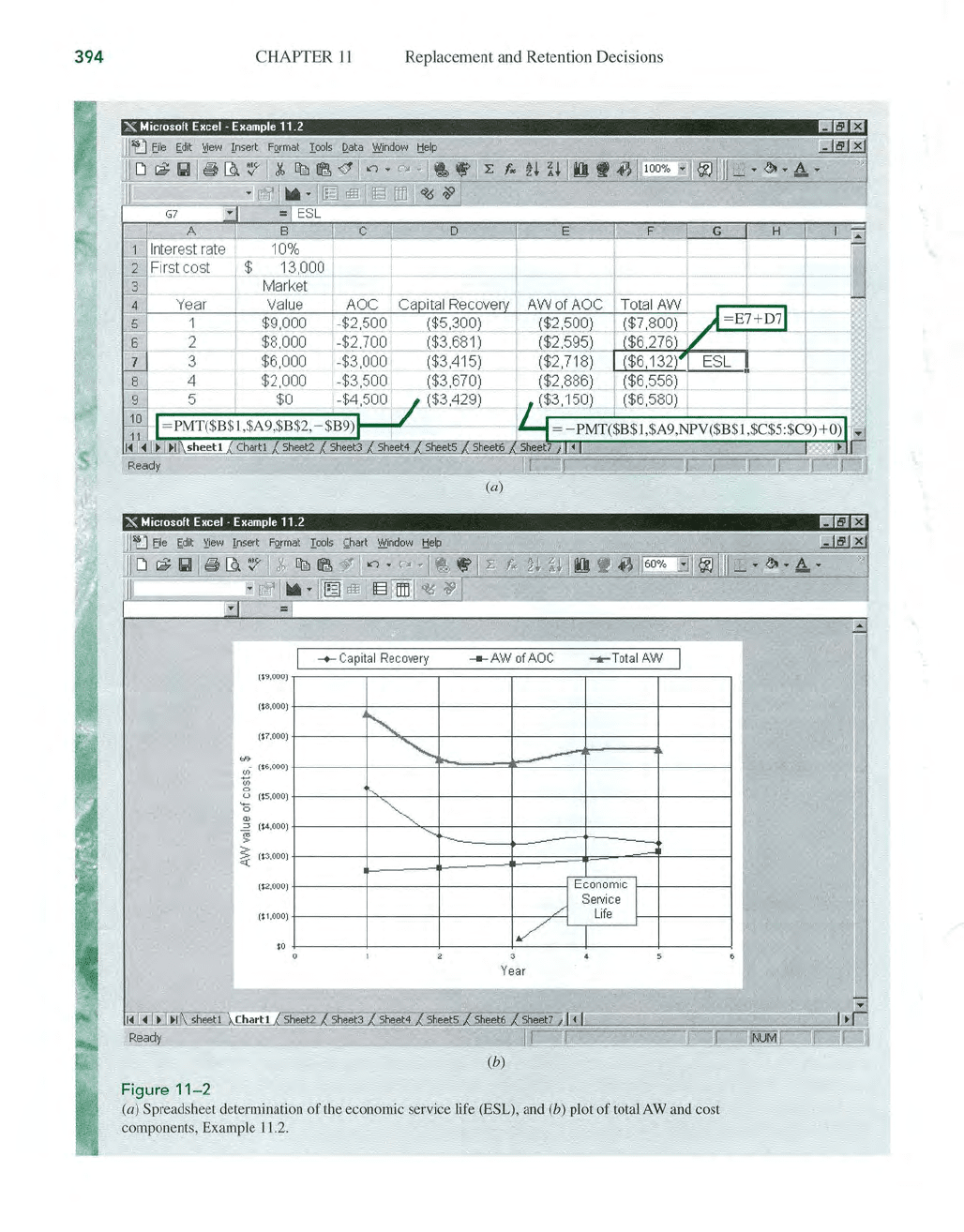

EXAM

PLE

11.2

:.~

A 3-year-o

ld

manufacturing process asset

is

being considered for early replacement. Its

cu

rrent market va

lu

e

is

$13,000. Estimated future market values and annual operating costs

for

the next 5 years are given

in

Table

II

-

I,

columns 2 and 3. What is the economic service

life

of

th

is defender if the interest rate is

10

% per year? Solve by hand and

by

computer.

TABLE

11-1

Computation

of

Economic Service Life

Capital

AWof

Total

Yearj

MVj

AOC

j

Recovery AOC

AW

k

(1

)

(2)

(3)

(4) (5)

(6)

= (4) + (5)

1

$9000

$

-2

500

$-5300 $-2500

$- 7800

2

8000

-2

700

-3

681

-2595

- 6276

3

6000

-3

000

-3

415

-2717

- 6132

4

2000

-3

500

-3

670

-2886

- 6556

5

0

- 4500

-3

429

-3150

- 6579

Solution by Hand

Equation [11.3 J is used to calculate total A W k for k = 1, 2,

...

, 5. Table 11-1, column 4,

shows the capi

tal

recovery for the $13,000 cun'ent market value

(j

=

0)

plus

10

% return.

Column 5 gives the equivalent

AW

of

AOC for k years. As an illustration, the comp

ut

ation

of

total

AW

for k = 3 from Equation [11.3J

is

Total

AW

3

= - P(A/P,i,3) +

MV

3

(A/

F,i,3) - [PW

of

AOC"AOC

2

,

and

AOC

3

J(A

/ P,i,3)

= -

13

,000(A/ P,

10

%,3) + 6000(A/ F,

1O

%,3) - [2500(P/ F,

1O

%,

1)

+ 2700(P/ F,

10

%,2) + 3000(P/F,JO%,3)](A/P,lO%,3)

=

-3415

- 2717 =

$-6132

A similar computat

ion

is

performed

fo

r each year I through

5.

The lowest equivalent cost

(numerically largest

AW

value) occurs at k = 3. Therefore, the defender ESL

is

n = 3 years,

and the

AW

value

is

$- 6132.

In

the replacement study, this

AW

will

be

compared with the

best challenger

AW

determined by a similar ESL analysis.

Solution by

Computer

See Figure

11

-2

for the spreadsheet and chart for this example. (This format

is

a template

for any ESL analysis; simply change the estimates and add rows for more years

.)

Contents

of

columns D and E are briefly described below. The PMT functions app

ly

the formats for

the defender

as

desclibed above. Cell tags show detailed cell-reference format for year

5.

The $

sy

mbols are

in

cluded for absolute cell referencing, needed when the entry is dragged

down through

th

e column.

393

m

E·Solve

394

Ready

Figure

11-2

CHAPTER

II

Replacement and Retention Decisions

-+-

C

apital

Re

covery

($9,

000

)

($

S

.ooO)

($

7,

000)

""

"

~

~-

($

6,

000

)

U

($

5,000)

'0

'"

..=e

($4.000)

'"

>

~

'-..,

r--~

~

($

3

,0

00)

($

2

.0

00)

($1.00

0)

10

(a)

__

AWofAOC

/

3

Year

(b)

~

__

TotalAW I

--'

Economic

SelYice

I

Life

(a) Spreadsheet determination

of

the economic service life (ESL), and (b) plot

of

total

AW

and cost

components,

Example 11.2.