Hull J.C. Risk management and Financial institutions

Подождите немного. Документ загружается.

20

Chapter 1

one by one (risk decomposition) rather than relying solely on risk

diversification. They also allow banks to buy protection against the

overall level of defaults in the economy. We discuss credit derivatives in

Chapter 13.

1.5 THE MANAGEMENT OF NET INTEREST INCOME

As mentioned earlier net interest income is the excess of interest received

over interest paid. It is the role of the asset/liability management function

to ensure that fluctuations in net interest income are minimal. In this

section we explain how it does this.

To illustrate how fluctuations in net interest income could occur,

consider a simple situation where a bank offers consumers a one-year

and a five-year deposit rate as well as a one-year and five-year mortgage

rate. The rates are shown in Table 1.6. We make the simplifying assump-

tion that market participants expect the one-year interest rate for future

time periods to equal the one-year rates prevailing in the market today.

Loosely speaking, this means that the market considers interest rate

increases to be just as likely as interest rate decreases. As a result the rates

in Table 1.6 are "fair", in that they reflect the market's expectations.

Investing money for one year and reinvesting for four further one-year

periods gives the same expected overall return as a single five-year

investment. Similarly, borrowing money for one year and refinancing each

year for the next four years leads to the same expected financing costs as a

single five-year loan.

Now suppose you have money to deposit and agree with the prevailing

view that interest rate increases are just as likely as interest rate decreases.

Would you choose to deposit your money for one year at 3% per annum

or for five years at 3% per annum? The chances are that you would

choose one year because this gives you more financial flexibility. It ties up

your funds for a shorter period of time.

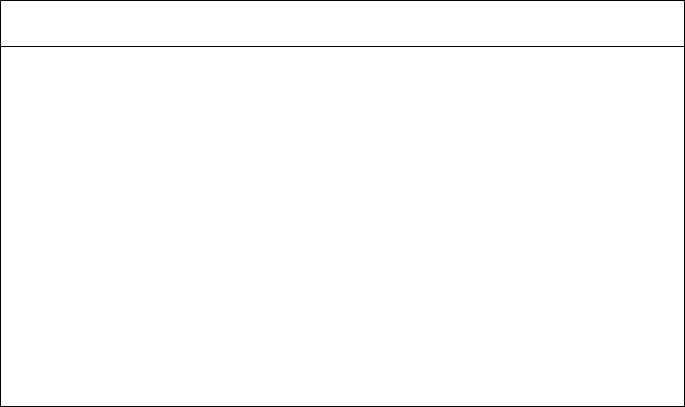

Table 1.6 Example of rates offered by a bank to

its customers.

Maturity

(years)

1

5

Deposit

rate

3%

3%

Mortgage

rate

6%

6%

Introduction

21

Now suppose that you want a mortgage. Again you agree with the

prevailing view that interest rate increases are just as likely as interest rate

decreases. Would you choose a one-year mortgage at 6% or a five-year

mortgage at 6%? The chances are that you would choose a five-year

mortgage because it fixes your borrowing rate for the next five years and

subjects you to less refinancing risk.

When the bank posts the rates shown in Table 1.6, it is likely to find

that the majority of its depositors opt for one-year maturities and the

majority of its customers seeking mortgages opt for five-year maturities.

This creates an asset/liability mismatch for the bank and subjects its net

interest income to risks. There is no problem if interest rates fall. The

bank will find itself financing the five-year 6% mortgages with deposits

that cost less than 3% and net interest income will increase. However, if

rates rise, the deposits that are financing these 6% mortgages will cost

more than 3% and net interest income will decline. A 3% rise in interest

rates would reduce the net interest income to zero.

It is the job of the asset/liability management group to ensure that the

maturities of the assets on which interest is earned and the maturities of the

liabilities on which interest is paid are matched. One way to do this in our

example is to increase the five-year rate on both deposits and mortgages.

For example, we could move to the situation in Table 1.7 where the five-

year deposit rate is 4% and the five-year mortgage rate 7%. This would

make five-year deposits relatively more attractive and one-year mortgages

relatively more attractive. Some customers who chose one-year deposits

when the rates were as in Table 1.6 will switch to five-year deposits when

rates are as in Table 1.7. Some customers who chose five-year mortgages

when the rates were as in Table 1.6 will choose one-year mortgages. This

may lead to the maturities of assets and liabilities being matched. If there is

still an imbalance with depositors tending to choose a one-year maturity

and borrowers a five-year maturity, five-year deposit and mortgage rates

could be increased even further. Eventually the imbalance will disappear.

The net result of all banks behaving in the way we have just described is

Table 1.7 Five-year rates are increased in an attempt

to match maturities of assets and liabilities.

Maturity

(years)

1

5

Deposit

rate

3%

4%

Mortgage

rate

6%

7%

22

Chapter 1

that long-term rates tend to be higher than those predicted by expected

future short-term rates. This phenomenon is referred to as liquidity

preference theory. It leads to long-term rates being higher than short-term

rates most of the time. Even when the market expects a small decline in

short-term rates, liquidity preference theory is likely to cause long-term

rates to be higher than short-term rates.

Many banks now have sophisticated systems for monitoring the deci-

sions being made by customers so that, when they detect small differences

between the maturities of the assets and liabilities being chosen, they can

fine-tune the rates they offer. Sometimes derivatives such as interest rate

swaps are also used to manage their exposure. The result is that net interest

income is very stable and does not lead to significant risks. However, as

indicated in Business Snapshot 1.2, this has not always been the case.

SUMMARY

An important general principle in finance is that there is a trade-off

between risk and return. Higher expected returns can usually be achieved

only by taking higher risks. Investors should not, in theory, be concerned

with risks they can diversify away. The extra return they demand should

be for the amount of nondiversifiable systematic risk they are bearing.

For companies, investment decisions are more complicated. Compan-

ies are not in general as well diversified as investors and survival is an

Business Snapshot 1.2 Expensive Failures of Financial Institutions in the US

Throughout the 1960s, 1970s, and 1980s, Savings and Loans (S&Ls) in the

United States failed to manage interest rate risk well. They tended to take

short-term deposits and make long-term fixed-rate mortgages. As a result they

were seriously hurt by interest rate increases in 1966, 1969 70, 1974. and the

killer in 1979-82. S&Ls were protected by government guarantees. Over 1,700

failed in the 1980s. A major reason for the failures was their inadequate

interest rate risk management. The total cost to the US taxpayer of the failures

has been estimated to be between $100 and $500 billion.

The largest bank failure in the US, Contintental Illinois, can also be

attributed to a failure to manage interest rale risks well. During the period

1980 to 1983 its assets (i.e., loans) with maturities over a year totaled between

$7 billion and $8 billion, whereas its liabilities (i.e., deposits) with maturities

over a year were between $1.4 billion and $2.5 billion. Continental failed in

1984 and was the subject of an expensive government bailout.

Introduction

23

important and legitimate objective. Both financing and investment

decisions should be taken so that the possibility of financial distress

is low.

This is because financial distress leads to what are known as bank-

ruptcy costs. These costs arise from the nature of the bankruptcy process

and almost invariably lead to a reduction in shareholder value over and

above the reduction that took place as a result of the adverse events

leading to bankruptcy.

Banks must manage the risks they face carefully. Equity capital is

typically about 5% of assets and profit before taxes is often less than

1% of assets. Large trading losses, an economic downturn leading to a

sharp rise in loan losses, or other unexpected events can lead to an

erosion of equity capital and put the bank in a precarious position.

Regulators have become increasingly active in ensuring that the capital

a bank keeps is commensurate with the risks it takes.

Two general approaches to risk management are risk decomposition

and risk aggregation. Risk decomposition involves managing risks one

by one. Risk aggregation involves relying on the power of diversification

to reduce risks. Banks use both approaches to manage market risks.

Credit risks have traditionally been managed using risk aggregation, but

with the advent of credit derivatives the risk decomposition approach

can be used.

A bank's net interest income is the excess of the interest earned over the

interest paid. There are now well established asset/liability management

procedures to ensure that this remains roughly constant from year to year.

These involve adjusting the rates offered to customers to ensure that the

maturities of assets and liabilities are matched.

FURTHER READING

Markowitz, H. "Portfolio Selection," Journal of Finance, 1, 1 (March 1952),

77-91.

Ross, S. "The Arbitrage Theory of Capital Asset Pricing," Journal of Economic

Theory, 13 (December 1976), 343-362.

Sharpe, W. "Capital Asset Prices: A Theory of Market Equilibrium," Journal of

Finance, September 1964, 425-442.

Smith, C. W., and R. M. Stulz, "The Determinants of a Firm's Hedging Policy,"

Journal of Financial and Quantitative Analysis, 20 (1985), 391-406.

Stulz, R. M., Risk Management and Derivatives. Southwestern, 2003.

24 Chapter 1

QUESTIONS AND PROBLEMS (Answers at End of Book)

1.1. An investment has probabilities 0.1, 0.2, 0.35, 0.25, and 0.1 of giving

returns equal to 40%, 30%, 15%, -5% and -15%. What is the expected

return and the standard deviation of returns?

1.2. Suppose that there are two investments with the same probability dis-

tribution of returns as in Problem 1.1. The correlation between the

returns is 0.15. What is the expected return and standard deviation of

return from a portfolio where money is divided equally between the

investments.

1.3. For the two investments considered in Figure 1.2 and Table 1.2, what are

the alternative risk/return combinations if the correlation is (a) 0.3, (b) 1.0,

and (c) -1.0.

1.4. What is the difference between systematic and nonsystematic risk? Which

is more important to an equity investor? Which can lead to the bankruptcy

of a corporation?

1.5. Outline the arguments leading to the conclusion that all investors should

choose the same portfolio of risky investments. What are the key

assumptions?

1.6. The expected return on the market portfolio is 12% and the risk-free rate

is 6%. What is the expected return on an investment with a beta of (a) 0.2,

(b) 0.5, and (c) 1.4?

1.7. "Arbitrage pricing theory is an extension of the capital asset pricing

model." Explain this statement.

1.8. "The capital structure decision of a company is a trade-off between

bankruptcy costs and the tax advantages of debt." Explain this statement.

1.9. A bank's operational risk is the risk of large losses because of employee

fraud, natural disasters, litigation, etc. It will be discussed in Chapter 14. Is

operational risk best handled by risk decomposition or risk aggregation.

1.10. A bank's profit next year will be normally distributed with a mean of 0.6%

of assets and a standard deviation of 1.5% of assets. The bank's equity is

4% of assets. What is the probability that the bank will have a positive

equity at the end of the year? Ignore taxes.

1.11. Why do you think that banks are regulated to ensure that they do not take

too much risk but most other companies (e.g., those in manufacturing and

retailing) are not?

1.12. Explain carefully the risks faced by Continental Illinois in the 1980 to 1983

period based on the data in Business Snapshot 1.2.

1.13. Explain carefully why interest rate risks contributed to the expensive S&L

failures in the United States.

Introduction

25

1.14. Suppose that a bank has $5 billion of one-year loans and $20 billion of

five-year loans. These are financed by $15 billion of one-year deposits and

$10 billion of five-year deposits. Explain the impact on the bank's net

interest income of interest rates increasing by 1 % every year for the next

three years.

1.15. List the bankruptcy costs incurred by the company in Business Snap-

shot 1.1.

ASSIGNMENT QUESTIONS

1.16. Suppose that one investment has a mean return of 8% and a standard

deviation of return of 14%. Another investment has a mean return of 12%

and a standard deviation of return of 20%. The correlation between the

returns is 0.3. Produce a chart similar to Figure 1.2 showing alternative

risk/return combinations from the two investments.

1.17. Which items on a DLC's income statement in Table 1.4 are most likely to

be affected by (a) credit risk, (b) market risk, and (c) operational risk.

1.18. A bank estimates that its profit next year is normally distributed with a

mean of 0.8% of assets and the standard deviation of 2% of assets. How

much equity (as a percent of assets) does the company need to be (a) 99%

and (b) 99.9% sure that it will have positive equity at the end of the year.

Ignore taxes.

1.19. Suppose that a bank has $10 billion of one-year loans and $30 billion of

five-year loans. These are financed by $35 billion of one-year deposits and

$5 billion of five-year deposits. The bank has equity totaling $2 billion and

its return on equity is currently 12%. Estimate what change in the interest

rates next year would lead to the bank's return on equity being reduced to

zero. Assume that the bank is subject to a tax rate of 30%.

1.20. Explain why long-term rates are higher than short-term rates most of the

time. Under what circumstances would you expect long-term rates to be

lower than short-term rates?

Financial Products

and How They Are

Used for Hedging

Companies trade a variety of financial instruments to manage their risks.

Some of these instruments are referred to as standard or "plain vanilla"

products. Most forward contracts, futures contracts, swaps, and options

fall into this category. Others are designed to meet the particular needs of

a corporate treasurer. These are referred to as "exotics" or structured

products. This chapter describes the instruments and how they trade. It

discusses the circumstances when a company should hedge, how much

hedging it should do, and what instruments should be used.

2.1 THE MARKETS

There are two types of markets in which financial instruments trade.

These are known as the exchange-traded market and the over-the-counter

(or OTC) market.

Exchange-Traded Markets

Exchanges have been used to trade financial products for many years.

Some exchanges such as the New York Stock Exchange (NYSE) focus on

the trading of stocks. Others such as the Chicago Board of Trade (CBOT)

and the Chicago Board Options Exchange (CBOE) are concerned with

the trading of derivatives such as futures and options.

28

Chapter 2

The role of the exchange is to define the contracts that trade and

organize trading so that market participants can be sure that the trades

they agree to will be honored. Traditionally individuals have met at the

exchange and agreed on the prices for trades, often by using an elaborate

system of hand signals. Exchanges are increasingly moving to electronic

trading. This involves traders entering their desired trades at a keyboard

and a computer being used to match buyers and sellers. Not everyone

agrees that the shift to electronic trading is desirable. Electronic trading is

less physically demanding than traditional floor trading. However, traders

do not have the opportunity to attempt to predict short-term market

trends from the behavior and body language of other traders.

Sometimes trading is facilitated with market makers. These are indi-

viduals who are always prepared to quote both a bid price (the price at

which they are prepared to buy) and an offer price (the price at which they

are prepared to sell). Typically the exchange will specify an upper bound

for the spread between a market maker's bid and offer prices.

Over-the-Counter Markets

The over-the-counter market is an important alternative to exchanges. It

is a telephone- and computer-linked network of traders who work for

financial institutions, large corporations, or fund managers. Financial

institutions often act as market makers for the more commonly traded

instruments.

Telephone conversations in the over-the-counter market are usually

taped. If there is a dispute over what was agreed, the tapes are replayed

to resolve the issue. Trades in the over-the-counter market are typically

much larger than trades in the exchange-traded market. A key advantage

of the over-the-counter market is that the terms of a contract do not have

to be those specified by an exchange. Market participants are free to

negotiate any mutually attractive deal. A disadvantage is that there is

usually some credit risk in an over-the-counter trade (i.e., there is a small

risk that the contract will not be honored). Exchanges have organized

themselves to eliminate virtually all credit risk.

2.2 WHEN TO HEDGE

Most nonfinancial companies have no particular skills or expertise in

predicting variables such as interest rates, exchange rates, and commod-

ity prices. It makes sense for them to hedge the risks associated with

Financial Products and How They Are Used for Hedging 29

these variables as they arise. The companies can then focus on their main

activities. By hedging, they avoid unpleasant surprises such as a foreign

exchange loss or a sharp rise in the price of a commodity that has to be

purchased.

It can be argued that companies need not hedge because the company's

shareholders can implement their own hedging programs, deciding which

of the company's risks to keep and which to get rid of. However this

assumes—unrealistically—that a company's shareholders have as much

information about the risks faced by the company as the company's

management. It also ignores the bankruptcy costs arguments in

Section 1.2.

Hedging and Competitors

It is not always correct for a company to choose to hedge. If hedging is

not the norm in a certain industry, it can be dangerous for one company

to choose to be different from all others. Competitive pressures within the

industry may be such that the prices of the goods and services produced

by the industry fluctuate to reflect raw material costs, interest rates,

exchange rates, and so on. A company that does not hedge can expect

its profit margins to be roughly constant. However, a company that does

hedge can expect its profit margins to fluctuate!

To illustrate this point, consider two manufacturers of gold jewelry,

SafeandSure Company and TakeaChance Company. We assume that

most companies in the industry do not hedge against movements in the

price of gold and that TakeaChance Company is no exception. However,

SafeandSure Company has decided to be different from its competitors

and to use futures contracts to lock in the price it will pay for gold over

the next 18 months.

If the price of gold goes up, economic pressures will tend to lead to a

corresponding increase in the wholesale price of the jewelry, so that

TakeaChance Company's profit margin is unaffected. By contrast,

SafeandSure Company's profit margin will increase after the effects of

the hedge have been taken into account. If the price of gold goes down,

economic pressures will tend to lead to a corresponding decrease in the

wholesale price of the jewelry. Again, TakeaChance Company's profit

margin is unaffected. However, SafeandSure Company's profit margin

goes down. In extreme conditions, SafeandSure Company's profit margin

could become negative as a result of the "hedging" carried out! This

example is summarized in Table 2.1.

30

Chapter 2

The example emphasizes the importance of looking at the big picture

when hedging. All the implications of changes in commodity prices,

interest rates, and exchange rates on a company's profitability should

be taken into account in the design of a hedging strategy.

2.3 THE "PLAIN VANILLA" PRODUCTS

In this section we review the products that most commonly trade in

financial markets. We focus on those that involve stocks, currencies,

commodities, and interest rates. Less traditional products such as credit

derivatives, weather derivatives, energy derivatives, and insurance deriva-

tives are covered in later chapters. *

Long and Short Positions in Assets

The simplest type of trade is the purchase or sale of an asset. Examples of

such trades are:

1. The purchase of 100 IBM shares

2. The sale of 1 million British pounds

3. The purchase of 1000 ounces of gold

4. The sale of $1 million worth of bonds issued by General Motors

The first of these trades would typically be done on an exchange; the

other three would be done in the over-the-counter market. The trades are

sometimes referred to as spot contracts because they lead to almost

immediate "on the spot" delivery of the asset.

Short Sales

In some markets it is possible to sell an asset that you do not own with

the intention of buying it back later. This is referred to as shorting the

asset. We will illustrate how it works by considering a short sale of shares

of a stock.

Change in

gold price

Increase

Decrease

Effect on price

of gold jewelry

Increase

Decrease

Effect on profits

of TakeaChance Co.

None

None

Effect on profits

of SafeandSure Co.

Increase

Decrease

Table 2.1 Danger in hedging when competitors do not.