Hull J.C. Risk management and Financial institutions

Подождите немного. Документ загружается.

Financial Products and How They Are Used for Hedging 51

2.7. Suppose you write a put contract with a strike price of $40 and an

expiration date in three months. The current stock price is $41 and the

contract is on 100 shares. What have you committed yourself to? How

much could you gain or lose?

2.8. What is the difference between the over-the-counter market and the

exchange-traded market? Which of the two markets do the following trade

in: (a) a forward contract, (b) a futures contract, (c) an option, (d) a swap,

and (e) an exotic option?

2.9. You would like to speculate on a rise in the price of a certain stock. The

current stock price is $29, and a three-month call with a strike of $30 costs

$2.90. You have $5,800 to invest. Identify two alternative strategies, one

involving an investment in the stock and the other involving investment in

the option. What are the potential gains and losses from each?

2.10. Suppose that you own 5,000 shares worth $25 each. How can put options

be used to provide you with insurance against a decline in the value of

your holding over the next four months?

2.11. When first issued, a stock provides funds for a company. Is the same true

of a stock option? Discuss.

2.12. Suppose that a March call option to buy a share for $50 costs $2.50 and is

held until March. Under what circumstances will the holder of the option

make a profit? Under what circumstances will the option be exercised?

2.13. Suppose that a June put option to sell a share for $60 costs $4 and is held

until June. Under what circumstances will the seller of the option (i.e., the

party with the short position) make a profit? Under what circumstances

will the option be exercised?

2.14. A company knows that it is due to receive a certain amount of a foreign

currency in four months. What type of option contract is appropriate for

hedging?

2.15. A United States company expects to have to pay 1 million Canadian

dollars in six months. Explain how the exchange rate risk can be hedged

using (a) a forward contract and (b) an option.

2.16. In the 1980s, Bankers Trust developed index currency option notes

(ICONs). These are bonds in which the amount received by the holder

at maturity varies with a foreign exchange rate. One example was its trade

with the Long Term Credit Bank of Japan. The ICON specified that if the

yen/US dollar exchange rate, S

T

, is greater than 169 yen per dollar at

maturity (in 1995), the holder of the bond receives $1,000. If it is less than

169 yen per dollar, the amount received by the holder of the bond is

52

Chapter 2

When the exchange rate is below 84.5, nothing is received by the holder at

maturity. Show that this ICON is a combination of a regular bond and two

options.

2.17. Suppose that USD/GBP spot and forward exchange rates are as follows:

Spot 1.6080

90-day forward 1.6056

180-day forward 1.6018

What opportunities are open to an arbitrageur in the following situations:

(a) a 180-day European call option to buy £1 for $1.57 costs 2 cents and

(b) a 90-day European put option to sell £1 for $1.64 costs 2 cents?

2.18. A company has money invested at 5% for five years. It wishes to use the

swap quotes in Table 2.5 to convert its investment to a floating-rate

investment. Explain how it can do this.

2.19. A company has borrowed money for five years at 7%. Explain how it can

use the quotes in Table 2.5 to convert this to a floating-rate liability.

2.20. A company has a has a floating-rate liability that costs LIBOR plus 1%.

Explain how it can use the quotes in Table 2.5 to convert this to a three-

year fixed-rate liability.

2.21. A corn farmer argues: "I do not use futures contracts for hedging. My real

risk is not the price of corn. It is that my whole crop gets wiped out by the

weather." Discuss this viewpoint. Should the farmer estimate his or her

expected production of corn and hedge to try to lock in a price for

expected production?

2.22. An airline executive has argued: "There is no point in our hedging the

price of jet fuel. There is just as much chance that we will lose from doing

this as that we will gain." Discuss the executive's viewpoint.

2.23. The standard deviation of monthly changes in the spot price of live cattle

is (in cents per pound) 1.2. The standard deviation of monthly changes in

the futures price of live cattle for the closest contract is 1.4. The correlation

between the futures price changes and the spot price changes is 0.7. It is

now October 15. A beef producer is committed to purchasing 200,000

pounds of live cattle on November 15. The producer wants to use the

December live-cattle futures contracts to hedge its risk. Each contract is

for the delivery of 40,000 pounds of cattle. What strategy should the beef

producer follow?

2.24. Why is the cost of an Asian basket put option to Microsoft considerably

less than the cost of a portfolio of put options, one for each currency and

each maturity (see Business Snapshot 2.3.)?

Financial Products and How They Are Used for Hedging 53

ASSIGNMENT QUESTIONS

2.25. The current price of a stock is $94, and three-month European call options

with a strike price of $95 currently sell for $4.70. An investor who feels

that the price of the stock will increase is trying to decide between buying

100 shares and buying 2,000 call options (= 20 contracts). Both strategies

involve an investment of $9,400. What advice would you give? How high

does the stock price have to rise for the option strategy to be more

profitable?

2.26. A bond issued by Standard Oil worked as follows. The holder received no

interest. At the bond's maturity the company promised to pay $1,000 plus

an additional amount based on the price of oil at that time. The additional

amount was equal to the product of 170 and the excess (if any) of the price

of a barrel of oil at maturity over $25. The maximum additional amount

paid was $2,550 (which corresponds to a price of $40 per barrel). Show

that the bond is a combination of a regular bond, a long position in call

options on oil with a strike price of $25, and a short position in call

options on oil with a strike price of $40.

2.27. The price of gold is currently $500 per ounce. The forward price for

delivery in one year is $700. An arbitrageur can borrow money at 10%

per annum. What should the arbitrageur do? Assume that the cost of

storing gold is zero and that gold provides no income.

2.28. A company's investments earn LIBOR minus 0.5%. Explain how it can

use the quotes in Table 2.5 to convert the investments to (a) 3-year,

(b) 5-year, and (c) 10-year fixed-rate investments.

2.29. What position is equivalent to a long forward contract to buy an asset at

K on a. certain date and a long position in a European put option to sell it

for K on that date.

2.30. Estimate the interest rate paid by P&G on the 5/30 swap in Business

Snapshot 2.2 if (a) the CP rate is 6.5% and the Treasury yield curve is flat

at 6% and (b) the CP rate is 7.5% and the Treasury yield curve is flat at

7% with semiannual compounding.

2.31. It is July 16. A company has a portfolio of stocks worth $100 million. The

beta of the portfolio is 1.2. The company would like to use the CME

December futures contract on the S&P 500 to change the beta of the

portfolio to 0.5 during the period July 16 to November 16. The index is

currently 1,000, and each contract is on $250 times the index, (a) What

position should the company take? (b) Suppose that the company changes

its mind and decides to increase the beta of the portfolio from 1.2 to 1.5.

What position in futures contracts should it take?

How Traders

Manage Their

Exposures

The trading function within a financial institution is referred to as the front

office; the part of the financial institution that is concerned with the overall

level of the risks being taken, capital adequacy, and regulatory compliance

is referred to as the middle office; the record keeping function is referred to

as the back office. As explained in Chapter 1, there are two levels within a

financial institution at which trading risks are managed. First, the front

office hedges risks by ensuring that exposures to individual market vari-

ables are not too great. Second, the middle office aggregates the exposures

of all traders to determine whether the total risk is acceptable. In this

chapter we focus on the hedging activities of the front office. In later

chapters we will consider how risks are aggregated in the middle office.

This chapter explains what are termed the "Greek letters", or simply

the "Greeks". Each of the Greeks measures a different aspect of the risk

in a trading position. Traders calculate their Greeks at the end of each day

and are required to take action if the internal risk limits of the financial

institution they work for are exceeded. Failure to take this action is liable

to lead to immediate dismissal.

3.1 DELTA

Imagine that you are a trader working for a US bank and responsible for

all trades involving gold. The current price of gold is $500 per ounce.

56 Chapter 3

Table 3.1 Summary of gold portfolio.

Table 3.1 shows a summary of your portfolio (known as your "book").

How can you manage your risks?

The value of your portfolio is currently $117,000. One way of investi-

gating the risks you face is to revalue the portfolio on the assumption that

there is a small increase in the price of gold from $500 per ounce to

$500.10 per ounce. Suppose that the new value of the portfolio is

$116,900. A $0.10 increase in the price of gold decreases the value of

your portfolio by $100. The sensitivity of the portfolio to the price of

gold is therefore

This is referred to as the delta of the portfolio. The portfolio loses value

at a rate of $1,000 per $1 increase in the price of gold. Similarly, it gains

value at a rate of $1,000 per $1 decrease in the price of gold.

In general, the delta of a portfolio with respect to a market variable is

where is a small change in the value of the variable and is the

resultant change in the value of the portfolio. Using calculus terminology,

delta is the partial derivative of the portfolio value with respect to the

value of the variable:

In our example the trader can eliminate the delta exposure by buying

1,000 ounces of gold. This is because the delta of a position in 1,000 ounces

of gold is 1,000. (The position gains value at the rate of $1,000 per $1

Position

Spot gold

Forward Contracts

Futures Contracts

Swaps

Options

Exotics

Total

Value ($)

180,000

-60,000

2,000

80,000

-110,000

25,000

117,000

How Traders Manage Their Exposures 57

increase in the price of gold.) When this trade is combined with the existing

portfolio, the resultant portfolio has a delta of zero. Such a portfolio is

referred to as a delta-neutral portfolio.

Linear Products

A linear product is a product whose value at any given time is linearly

dependent on the value of the underlying asset price (see Figure 3.1).

Forward contracts, futures contracts, and swaps are linear products;

options are not.

A linear product can be hedged relatively easily. Consider, for example,

a US bank that enters into a forward contract with a corporate client

where it agrees to sell the client 1 million euros at a certain exchange rate

in one year. Assume that the euro interest rate is 4% with annual

compounding. This means that the present value of 1 million euros in

one year is 961,538 euros. The bank can hedge its risk by borrowing

enough dollars to buy 961,538 euros today and then investing the euros

for one year at 4%. The bank knows that it will have the 1 million euros it

needs to deliver in one year and it knows what its costs will be.

When the bank enters into the opposite transaction and agrees to buy

1 million euros in one year it must hedge by shorting 961,538 euros. It

Figure 3.1 A linear product

58

Chapter 3

does this by borrowing the euros today at 4% and immediately converting

them to US dollars. The 1 million euros received in one year are used to

repay the loan.

Shorting assets to hedge forward contracts is not always easy. Gold is

an interesting case in point. Financial institutions often find that they

enter into very large forward contracts to buy gold from gold producers.

This means that they need to borrow large quantities of gold to create a

short position for hedging. As outlined in Business Snapshot 3.1, central

banks are the source of the borrowed gold.

Nonlinear Products

Options and most structured products are nonlinear products. The

relationship between the value of the product and the value of the

underlying market variable at any given time is nonlinear. This non-

linearity makes them more difficult to hedge.

Business Snapshot 3.1 Hedging by Gold Mining Companies

It is natural for a gold mining company to consider hedging against changes

in the price of gold. Typically it takes several years to extract all the gold from

a mine. Once a gold mining company decides to go ahead with production at

a particular mine, it has a big exposure to the price of gold. Indeed, a mine

that looks profitable at the outset could become unprofitable if the price of

gold plunges.

Gold mining companies are careful to explain their hedging strategies to

potential shareholders. Some gold mining companies do not hedge. They tend

to attract shareholders who buy gold stocks because they want to benefit

when the price of gold increases and are prepared to accept the risk of a loss

from a decrease in the price of gold. Other companies choose to hedge. They

estimate the number of ounces they will produce each month for the next few

years and enter into short futures or forward contracts to lock in the price

that will be received.

Suppose you are Goldman Sachs and have just entered into a forward

contract with a gold mining company where you agree to buy a large amount

of gold at a fixed price. How do you hedge your risk? The answer is that you

borrow gold from a central bank and sell it at the current market price. (The

central banks of many countries hold large amounts of gold.) At the end of

the life of the forward contract, you buy gold from the gold mining company

under the terms of the forward contract and use it to repay the central bank.

The central bank charges a fee (perhaps 1.5% per annum) known as the gold

lease rate for lending its gold in this way.

How Traders Manage Their Exposures 59

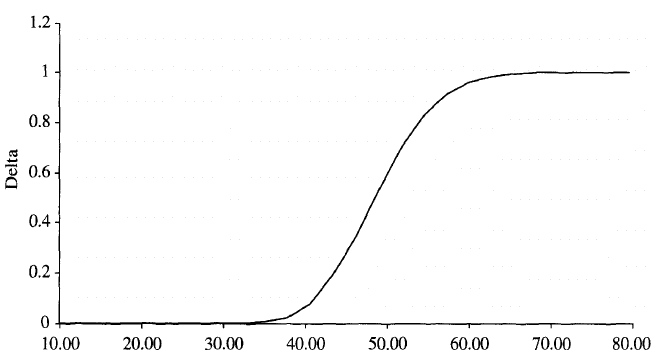

Asset price

Figure 3.2 Value of option as a function of stock price.

Consider as an example a trader who sells 100,000 European call

options on a non-dividend-Paying stock when

1. The stock price is $49.

2. The strike price is $50.

3. The risk-free interest rate is 5%.

4. The stock price volatility is 20% per annum.

5. The time to option maturity is 20 weeks.

We suppose that the amount received for the options is $300,000 and that

the trader has no other positions dependent on the stock.

The value of one option as a function of the underlying stock price is

shown in Figure 3.2. The delta of one option changes with the stock price

in the way shown in Figure 3.3.

1

At the time of the trade, the value of an

option to buy one share of the stock is $2.40 and the delta of the option is

0.522. Because the trader is short 100,000 options, the value of the

trader's portfolio is -$240,000 and the delta of the portfolio is

—52,200. The trader can feel pleased that the options have been sold

for $60,000 more than their theoretical value, but is faced with the

problem of hedging the risk in the position.

The portfolio can be made delta neutral immediately after the trade by

1

Figures 3.2 and 3.3 were produced with the DerivaGem software, which can be

downloaded from the author's website. The Black-Scholes (analytic) model is used.

60 Chapter 3

Asset price

Figure 3.3 Delta of option as a function of stock price.

buying 52,200 shares of the underlying stock. If there is a small decrease

(increase) in the stock price, the gain (loss) on the option position should

be offset by the loss (gain) on the shares. For example, if the stock price

increases from $49 to $49.10, then the value of the options will decrease by

52,200 x 0.1 = $5,220 while that of the shares will increase by this amount.

In the case of linear products, once the hedge has been set up, it does

not need to be changed. This is not the case for nonlinear products. To

preserve delta neutrality, the hedge has to be adjusted periodically. This is

known as rebalancing.

Tables 3.2 and 3.3 provide two examples of how rebalancing might

work in our example. Rebalancing is assumed to be done weekly. As

mentioned, the initial value of delta for a single option is 0.522 and the

delta of the portfolio is —52,200. This means that, as soon as the option is

written, $2,557,800 must be borrowed to buy 52,200 shares at a price of

$49. The rate of interest is 5%. An interest cost of approximately $2,500 is

therefore incurred in the first week.

In Table 3.2 the stock price falls by the end of the first week to $48.12.

The delta declines to 0.458. A long position in 45,800 shares is now

required to hedge the option position. A total of 6,400 (i.e., 52,200 -

45,800) shares is therefore sold to maintain the delta neutrality of the

hedge. The strategy realizes $308,000 in cash, and the cumulative borrow-

ings at the end of Week 1 are reduced to $2,252,300. During the second

week, the stock price reduces to $47.37 and delta declines again. This

How Traders Manage Their Exposures 61

Table 3.2 Simulation of delta hedging. Option closes in the money and cost of

hedging is $263,300.

Week

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

Stock

price

49.00

48.12

47.37

50.25

51.75

53.12

53.00

51.87

51.38

53.00

49.88

48.50

49.88

50.37

52.13

51.88

52.87

54.87

54.62

55.87

57.25

Delta

0.522

0.458

0.400

0.596

0.693

0.774

0.771

0.706

0.674

0.787

0.550

0.413

0.542

0.591

0.768

0.759

0.865

0.978

0.990

1.000

1.000

Shares

purchased

52,200

(6,400)

(5,800)

19,600

9,700

8,100

(300)

(6,500)

(3,200)

11,300

(23,700)

(13,700)

12,900

4,900

17,700

(900)

10,600

11,300

1,200

1,000

0

Cost of shares

purchased

($000)

2,557.8

(308.0)

(274.7)

984.9

502.0

430.3

(15.9)

(337.2)

(164.4)

598.9

(1,182.2)

(664.4)

643.5

246.8

922.7

(46.7)

560.4

620.0

65.5

55.9

0.0

Cumulative cash

outflow

($000)

2,557.8

2,252.3

1,979.8

2,966.6

3,471.5

3,905.1

3,893.0

3,559.5

3,398.5

4,000.7

2,822.3

2,160.6

2,806.2

3,055.7

3,981.3

3,938.4

4,502.6

5,126.9

5,197.3

5,258.2

5,263.3

Interest

cost

($000)

2.5

2.2

1.9

2.9

3.3

3.8

3.7

3.4

3.3

3.8

2.7

2.1

2.7

2.9

3.8

3.8

4.3

4.9

5.0

5.1

leads to 5,800 shares being sold at the end of the second week. During the

third week, the stock price increases to over $50 and delta increases. This

leads to 19,600 shares being purchased at the end of the third week.

Toward the end of the life of the option, it becomes apparent that the

option will be exercised and delta approaches 1.0. By Week 20, therefore,

the hedger owns 100,000 shares. The hedger receives $5 million (i.e.,

100,000 x $50) for these shares when the option is exercised so that

the total cost of writing the option and hedging it is $263,300.

Table 3.3 illustrates an alternative sequence of events where the option

closes out of the money. As it becomes clear that the option will not be

exercised, delta approaches zero. By Week 20 the hedger therefore has no

Position in the underlying stock. The total costs incurred are $256,600.