Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 12 Identifying and valuing options 305

Self-assessment activity 12.2

You take out options contracts to sell a call and buy a put, both at the exercise price of

55p, exercisable one year hence. The cost of the put is 7p and the cost of the call is 1p.

The current share price is 44p and the risk-free interest rate is 10 per cent. What is the

present value of the exercise price?

(Answer in Appendix A at the back of the book)

■ Valuing a call

The following notation is employed with respect to valuing call options:

A number of formal statements can be made about call options:

1 Option prices cannot be negative. If the share price ends up below the exercise price

on the expiration date, the call option is worthless, but no further loss is created

beyond that of the initial premium paid. In mathematical terms:

(12.1)

This is the case where an option is ‘out of the money’ on expiry.

2 An option is worth on expiry the difference between the share price and the exercise price.

(12.2)

This is the case where an option is ‘in the money’ on expiry.

Thus far we have found the intrinsic values of the option – what it would be

worth were it about to expire. We have previously noted that options with some

time still to run will generally be worth more than the difference between current

share price and exercise price because the share price may rise further.

3 The maximum value of an option is the share price itself – it could never sell for more

than the underlying share price value.

(12.3)

The minimum value of a call today is equal to or greater than the current share

price less the exercise price:

(12.4)

But the exercise price is payable in the future. It was shown in the previous sec-

tion that the payoffs from a share are identical to the payoffs from buying a call

option, selling a put option and investing the remainder in a risk-free asset that

C

0

S

0

E

if

S

0

7 E

C

0

S

0

C

1

S

1

E

if

S

1

7 E

C

1

0

if

S

1

E

R

f

Risk-free interest rate

C

1

Value of call option on expiration date

C

0

Value of call option today

E Exercise price on the option

S

1

Share price at expiry date

S

0

Share price today

The net cash flow expected from investing in a put and a share is equivalent to that

to be expected from investing in a call and placing the present value of the sum nec-

essary to exercise the call in a risk-free investment. In both cases the investor will be

left with a sum equivalent to the exercise price if the share price is less than the exer-

cise price, and the value of the share if its price exceeds the exercise price.

CFAI_C12.QXD 3/15/07 7:21 AM Page 305

.

306 Part III Investment risk and return

400

350

300

250

200

150

100

50

0

700 800 900 1,000 1,100 1,200 1,300 1,400

In the money

At expiry

Lower limit

Before expiry

Exercise

price

Upper limit

Out of the money

A

B

C

Price of Bradford Option (p)

Share price (p)

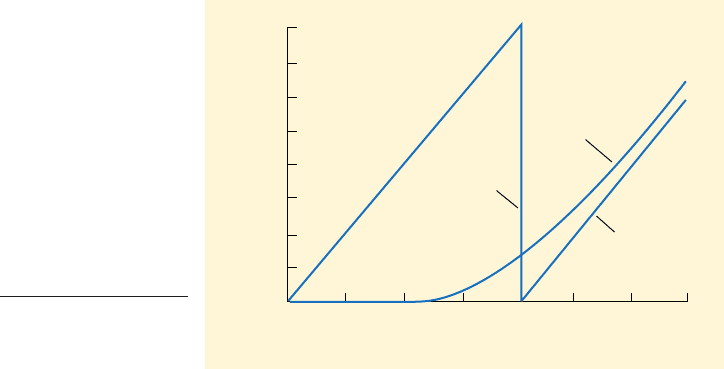

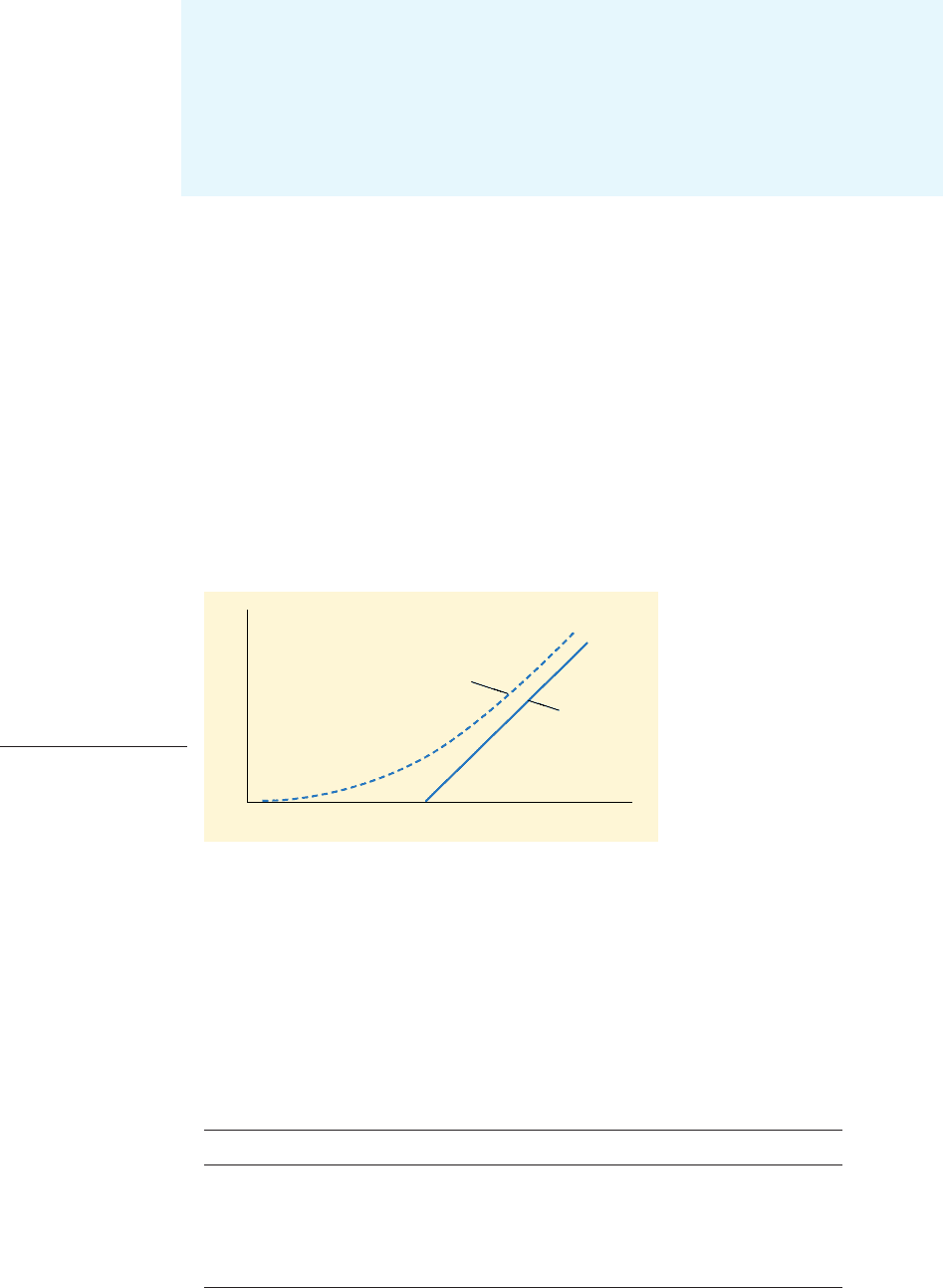

Figure 12.4

Option and share price

movements for

Bradford plc

yields the exercise price on the expiry date. In other words, we need to bring the

exercise price to its present value by discounting at the risk-free rate of interest. This

gives rise to the following revised statement.

4 The minimum value of an option is the difference between the share price and the present

value of the exercise price (or zero if greater).

(12.5)

The value of a call option can be observed in Figure 12.4. Bradford plc shares are

currently priced at 700p. The diagram shows how the value of an option to buy

Bradford shares at 1,100p moves with the share price. The upper limit to the option

price is the share price itself, and the lower limit is zero for share prices up to

1,100p, and the share price minus exercise price when share price moves above

1,100p. In fact, the actual option prices lie between these two extremes, on the

upward-sloping curve. The curve rises slowly at first, but then accelerates rapidly.

At point A on the curve, at the very start, the option is worthless. If the share

price for Bradford remained well below the exercise price, the option would remain

worthless. At point B, when the share price has rocketed to 1,400p, the option value

approximates the share price minus the present value of the exercise price. At point

C, the share price exactly equals the exercise price. If exercised today, the option

would be worthless. However, there may still be two months for the option to run,

in which time the share price could move up or down. In an efficient market, where

share prices follow a random walk, there is a 50 per cent chance that it will move

higher and an equal probability that it will go lower. If the share price falls, the

option will be worthless, but if it rises, the option will have some value. The value

placed on the option at point C depends largely on the likelihood of substantial

movements in share price. However, we can say that the higher the share price relative

to the exercise price, the safer the option (i.e. more valuable).

5 The value of a call option increases over time and as interest rates rise. Equation (12.4)

shows that the value of an option increases as the present value of the exercise

price falls. This reduction in present value occurs over time and/or with rises in

the interest rate.

6 The more risky the underlying share, the more valuable the option. This is because the

greater the variance of the underlying share price, the greater is the possibility that

prices will exceed the exercise price. But because option values cannot be negative

(i.e. the holder would not exercise the option), the ‘downside’ risk can be ignored.

C

0

S

0

3E>11 R

f

2

t

4

CFAI_C12.QXD 3/15/07 7:21 AM Page 306

.

Chapter 12 Identifying and valuing options 307

To summarise, the value of a call option is influenced by the following:

■ The share price. The higher the price of the share, the greater will be the value of an

option written on it.

■ The exercise price of the option. The lower the exercise price, the greater the value of

the call option.

■ The time to expiry of the option. As long as investors believe that the share price has a

chance of yielding a profit on the option, the option will have a positive value. So

the longer the time to expiry, the higher the option price.

■ The risk-free interest rate. As short-term interest rates rise, the value of a call option

also increases.

■ The volatility in the underlying share returns. The greater the volatility in share price,

the more likely it is that the exercise price will be exceeded and, hence, the option

value will rise.

■ Dividends. The price of a call option will normally fall with the share price as a share

goes ex-div (i.e. the next dividend is not received by the buyer).

A call option is therefore a contingent claim security that depends on the value and

riskiness of the underlying share on which it is written.

contingent claim security

Claim on a security whose

value depends on the value of

another asset

Self-assessment activity 12.3

Explain why option value increases with the volatility of the underlying share price. List

the factors that determine option value.

(Answer in Appendix A at the back of the book)

Best Worst

Share price 200p 50p

Less exercise price (125p) (125p)

Payoff 75p –

■ A simplified option-price model

Valuing options is a highly complex business, including a lot of mathematics or, for

most traders, a user-friendly software package. But we can introduce the valuation of

options by using a simple (if somewhat unrealistic) example. We argued earlier that it

is possible to replicate the payoffs from buying a share by purchasing a call option, sell-

ing a put option and placing the balance on deposit to earn a risk-free return over the

option period. This provides us with a method for valuing options.

Valuing a call option in Riskitt plc

In April, the share price of Riskitt plc is 100p. A three-month call option on the shares

with a July expiry date has an exercise price of 125p. With the current price well below

the exercise price it is clear that, for the option to have value, the share price must stand

a chance of increasing by at least 25p over the next quarter.

Assume that by the expiry date there is an equal chance that the share price will

have either soared to 200p or plummeted to 50p. There are no other possibilities.

Assume also that you can borrow at 12 per cent a year, or about 3 per cent a quarter.

What would be the payoff for a call option on one share in Riskitt?

CFAI_C12.QXD 3/15/07 7:21 AM Page 307

.

308 Part III Investment risk and return

Table 12.3

Valuing a call option in

Riskitt plc

Payoff in July if

Cash flow share price is

Strategy in April 200p 50p

£££

1 Buy 200 call options ? –

2 Buy 100 shares

Borrow

51.46 –

£

51.46>200 calls 25.73p, say 26pValue of call option

150

505048.54

50200100

150

You stand to make 75p if the share price does well, but nothing if it slips below the

exercise price. To work out how much you would be willing to pay for such an option,

we must replicate an investment in call options by a combination of investing in

Riskitt shares and borrowing.

Suppose we buy 200 call options. The payoffs in July will be zero if the share

price is only 50p and (i.e. ) if the share price is 200p. This is shown

in Table 12.3. Note that the cash flow we are trying to determine is the April premi-

um, represented by the question mark.

To replicate the call option cash flows, you adopt the second strategy in Table 12.3:

namely, buying 100 shares and borrowing sufficient cash to give identical cash flows

in July as the call option strategy. This means borrowing The net cash flows for

the two strategies are now the same in July whatever the share price. But the loan

repayment in July will include three months’ interest at 3 per cent for the quarter. The

initial sum borrowed in April would therefore be the present value of i.e.

Deducting this from the share price paid gives a net figure of

which must also be the April cash payment for 200 call options. The price for

one call option is therefore about 26p.

■ Black–Scholes pricing model

The above example took a highly simplified view of uncertainty, using only two possi-

ble share price outcomes. Black and Scholes (1973) combined the main determinants of

option values to develop a model of option pricing. Although its mathematics are

daunting, the model does have practical application. Every day, dealers in options use

it in specially programmed calculators to determine option prices.

For those who like a challenge, the complex mathematics of the Black–Scholes pric-

ing model are given in the appendix to this chapter. However, the key message is that

option pricing requires evaluation of five of the variables listed earlier: share price,

exercise price, risk-free rate of interest, time and share price volatility.

Acorn plc shares are currently worth 28p with a standard deviation of 30 per cent.

The risk-free rate of interest is 6 per cent. What is the value of a call option on Acorn

shares expiring in nine months and with an exercise price of 30p?

The fully-worked solution to this problem is given in the appendix to this chapter,

but we can identify here the five input variables:

Application of the Black–Scholes formula to the above data (see Appendix) gives a

value of the call option of 2.6p.

Share price volatility 1s2 30 per cent

Time to expiry 1t2 nine months

Risk-free rate 1k2 6 per cent p.a.

Exercise price 1E2 30p

Share price 1S2 28p

£51.46,

£50>1.03 £48.54.

£50,

£50

£50.

200 75p£150

CFAI_C12.QXD 3/15/07 7:21 AM Page 308

.

Chapter 12 Identifying and valuing options 309

Black–Scholes option pricing formula

Value of call option (C) is:

where

N(d) is the value of the cumulative distribution function for a standardised normal

random variable and is the present value of the exercise price continuously dis-

counted.

A simplified Black–Scholes formula can be used as an approximation for options

less than one year:

This formula emphasises the impact of volatility and time to expiry on the option

price.

Applying the above to the previous example we derive a slightly higher option

price:

Although the model is complex, the valuation equation derived from the model is

quite straightforward to use, and is widely employed in practice. Four of the five vari-

ables on which it is based are observable: the only non-observable variable, the volatil-

ity or standard deviation of the return on the underlying asset, is generally estimated

from historical data.

The Black–Scholes model is based on the following assumptions:

(a) there are no transactions costs or taxes;

(b) the expected risk free rate of interest is constant for the period of the option life;

(c) the market operates continuously;

(d) share prices change smoothly over time – there are no jumps or discontinuities in

the price series;

(e) the standard deviation of the distribution of returns on the share is known;

(f) the share pays no dividends during the life of the option; and

(g) the option may only be exercised at expiry of the call (i.e. a European-type option).

The assumptions on which the model is based are clearly quite restrictive. However,

as these assumptions are consistent with mainstream theorising in finance, the model

integrates well into the general body of finance theory. And of more practical impor-

tance the model appears to be quite robust: it is feasible to relax many assumptions

and incorporate more ‘real world’ features into the model without changing its over-

all character.

C 0.398 0.320.75

28 2.9p

C

S

1

22

s1t

e

tk

d

2

d

1

st

1>2

d

1

ln1S>E2 tk

st

1>2

st

1>2

2

C SN1d

1

2 EN1d

2

2e

tk

12.4 APPLICATION OF OPTION THEORY TO CORPORATE FINANCE

Option theory has implications going far beyond the valuation of traded share options.

It offers a powerful tool for understanding various other contractual arrangements in

finance. Here are some examples:

1 Share warrants, giving the holder the option to buy shares directly from the compa-

ny at a fixed exercise price for a given period of time.

CFAI_C12.QXD 3/15/07 7:21 AM Page 309

.

310 Part III Investment risk and return

2 Convertible loan stock, giving the holder a combination of a straight loan or bond and

a call option. On exercising the option, the holder exchanges the loan for a fixed

number of shares in the company.

3 Loan stock can have a call option attached, giving the company the right to repur-

chase the stock before maturity.

4 Executive share option schemes are share options issued to company executives as

incentives to pursue shareholder goals.

5 Insurance and loan guarantees are a form of put option. An insurance claim is the

exercise of an option. Government loan guarantees are a form of insurance. The

government, in effect, provides a put option to the holders of risky bonds so that, if

the borrowers default, the bond-holders can exercise their option by seeking reim-

bursement from the government. Underwriting a share issue is a similar type of

option.

6 Currency and interest rate options are discussed in later chapters as ways of hedging

or speculating on currency or interest rate movements.

7 Underwriting a new issue of shares when underwriters must take up any shares not

subscribed for by investors.

Two further forms of option are equity options and capital investment options, dis-

cussed in subsequent sections.

■ Equity as a call option on a company’s assets: Reckless Ltd

Option-like features are found in financially geared companies. Equity is, in effect, a call

option on the company’s assets.

Reckless Ltd has a single million debenture in issue, which is due for repayment

in one year. The directors, on behalf of the shareholders, can either pay off the loan at

the year end, thereby having no prior claim on the firm’s assets, or default on the

debenture. If they default, the debenture-holders will take charge of the assets or

recover the million owing to them.

In such a situation, the shareholders of Reckless have a call option on the compa-

ny’s assets with an exercise price of million. They can exercise the option by repay-

ing the loan, or they can allow the option to lapse by defaulting on the loan. Their

choice depends on the value of the company’s assets. If they are worth more than

million, the option is ‘in the money’ and the loan should be repaid. If the option is ‘out

of the money’, because the assets are worth less than million, option theory argues

that shareholders would prefer the company to default or enter liquidation. This

option-like feature arises because companies have limited liability status, effectively

protecting shareholders from having to make good any losses.

£1

£1

£1

£1

£1

Derivatives: a double-edged sword

Three years ago, Jackie Brown, a housewife from

Leicestershire who trained as a market researcher,

became a full-time day trader in investment derivatives.

Ms Brown is one of the many private investors who

have been drawn by the flexibility of derivatives, which

allow buyers – usually for a small consideration – to

gain exposure to the performance of an underlying

share, index or security without physically owning it.

Derivatives are the proverbial double-edged sword.

They enable investors to isolate certain risks, such as

interest rate risk or credit risk. Investors can then either

increase risk or hedge it out of their portfolios altogether.

Unlike buying a share or an asset, these instruments

allow investors to go short – sell stock they do not

own – in order to profit on falling markets. The danger

is that investors can lose more than their original stake.

CFAI_C12.QXD 3/15/07 7:21 AM Page 310

.

Chapter 12 Identifying and valuing options 311

12.5 CAPITAL INVESTMENT OPTIONS

We can now apply option theory to capital budgeting. Capital investment options (some-

times termed real options) are option-like features found in capital budgeting decisions.

While discounted cash flow techniques are very useful tools of analysis, they are gener-

ally more suited to financial assets, because they assume that assets are held rather than

managed. The main difference between evaluating financial assets and real assets is that

investors in, say, shares, are generally passive. Unless they have a fair degree of control,

they can only monitor performance and decide whether to hold or sell their shares.

Corporate managers, on the other hand, play a far more active role in achieving the

planned net present value on a capital project. When a project is slipping behind fore-

cast they can take action to try to achieve the original NPV target. In other words, they

can create options – actions to mitigate losses or exploit new opportunities presented

by capital investments. Managerial flexibility to adapt its future actions creates an

asymmetry in the NPV probability distribution that increases the investment project’s

value by improving the upside potential while limiting downside losses.

We will consider three types of option: the abandonment option, the timing option

and strategic investment options.

■ Abandonment option

Major investment decisions involve heavy capital commitments and are largely

irreversible: once the initial capital expenditure is incurred, management cannot turn the

clock back and do it differently. The costs associated with divestment are usually very

high. Most capital projects divested early will realise little more than scrap value. In the

case of a nuclear power plant, the decommissioning cost could be phenomenal. Because

management is committing large sums of money in pursuit of higher, but uncertain,

payoffs, the option to abandon, without incurring enormous costs if things look grim,

can be very valuable. Any project that permits management to extract value when things

go bad has an embedded put option. To ignore this is to undervalue the project.

real options

Options to invest in real assets

such as capital projects

option to abandon

Choice to allow an option to

expire. With a capital invest-

ment, abandonment should

take place where the value for

which an asset can be sold

exceeds the present value of

its future benefits from contin-

uing its operations

Example: Cardiff Components Ltd

Cardiff Components Ltd is considering building a new plant to produce components for the

nuclear defence industry. Proposal A is to build a custom-designed plant using the latest tech-

nology, but applicable only to nuclear defence contracts. A less profitable scheme, Proposal B,

is to build a plant using standard machine tools, giving greater flexibility in application.

Continued

Not surprisingly, derivatives have been vilified in some

quarters and beatified in others. But whatever investors

think about them, these tools are becoming impossible

to ignore and are fast becoming a part of ordinary

investors’ everyday life.

There are many hidden risks in the derivatives market,

warn experts. Warren Buffett, the investment guru who

is famous for his down-to-earth attitude to investing,

memorably billed them ‘weapons of mass destruction’.

His warning reverberated around the market and was

echoed by many others who worry that derivatives mar-

kets are opaque and standards of reporting are lax.

Investors often do not know who the end acquirer of

the risk is and how much accumulated exposure to one

type of risk he might have.

Anyone hoping to delve into spread betting, covered

warrants or options, should take heed. As veteran mar-

ket watchers always say: Do not buy what you do not

understand, beware of who you are dealing with, and

know that betting with derivatives is seductive but

dangerous.

As Mr Buffett says, it is ‘like hell – easy to enter and

almost impossible to exit’.

Source: Based on Kate Burgess, Financial Times, 25 October 2003.

CFAI_C12.QXD 3/15/07 7:21 AM Page 311

.

312 Part III Investment risk and return

■ Timing option

The Cardiff Components example not only introduces an abandonment option, it also

raises the timing option. Management may have viewed the investment as a ‘now or

never’ opportunity, arguing that in highly competitive markets there is no scope for

delay. However, most project decisions have three possible outcomes – accept, reject or

defer until economic and other conditions improve. In effect, this amounts to viewing

the decision as a call option that is about to expire on the new plant, the capital invest-

ment outlay being the exercise price. If a positive NPV is expected, the option will be

exercised; otherwise the option lapses and no investment is made.

The option to defer the decision by one year, until the outcome of the general elec-

tion is known, makes obvious sense. This may look something like the curved line in

Figure 12.5.

timing option

The option to invest now or

defer the decision until condi-

tions are more favourable

Now or never

investment

Investment

postponed

one year

Value of option to invest

Negative 0 Positive Project NPV

Figure 12.5

The value of the

options to delay

investments: Cardiff

Components Ltd

The outcome of a general election to be held one year hence has a major impact on the

decision. If the current government is returned to office, its commitment to nuclear

defence is likely to give rise to new orders, making Proposal A the better choice. If the cur-

rent opposition party is elected, its commitment to run down the nuclear defence indus-

try would make Proposal B the better course of action. Proposal B has, in effect, a put

option attached to it, giving the flexibility to abandon the proposed operation in favour of

some other activity.

Share call option Real call option

Current value of share Present value of expected cash flows

Exercise price Investment cost

Time to expiry Time until investment opportunity disappears

Share price uncertainty Project value uncertainty

Risk-free interest rate Risk-free interest rate

An immediate investment would yield either a negative NPV – in which case it

would not be taken up – or a positive NPV. Delaying the decision by a year to gain valu-

able new information (the curved broken line) is a more valuable option. Managements

sometimes delay taking up apparently wealth-creating opportunities because they

believe that the option to wait and gather new information is sufficiently valuable.

Investment as a call option

The five main variables in pricing a share call option can be applied to capital invest-

ment (or real) call options.

CFAI_C12.QXD 3/15/07 7:21 AM Page 312

.

Chapter 12 Identifying and valuing options 313

■ Strategic investment options

Certain investment decisions give rise to follow-on opportunities that are wealth-creating.

New technology investment, involving large-scale research and development, is par-

ticularly difficult to evaluate. Managers refer to the high level of intangible benefits

associated with such decisions. What they really mean is that these investments offer

further investment opportunities (e.g. greater flexibility), but that, at this stage, the pre-

cise form of such opportunities cannot be quantified.

follow-on opportunities

Options that arise following a

course of action

Table 12.4 Harlequin plc: call option valuation

Initial project (£000)

Cost of investment (400)

PV of cash inflows 375

Net present value (25)

Follow-on-project in Year 4

Cost of investment (1320)

PV of cash inflows 1320

Net present value in Year 4 –

Main factors in valuing the call option:

1 Asset value PV of cash flows at Year 4 discounted to Year 0

2 Exercise price

3 Risk-free discount rate

4 Time period

5 Asset volatility

Continued

standard deviation of 30%

4 years

10%

£1.32 m

cost of follow-on project

£0.636 m

£1.32 m>11.22

4

Example: Strategic options in Harlequin plc

Harlequin plc has developed a new form of mobile phone, using the latest technology. It is

considering whether to enter this market by investing in equipment costing to assem-

ble and then market the product in the north of England during the first four years. (Most of

the product parts will be bought in.) The expected net present value from this initial project,

however, is – The strategic case for such an investment is that by the end of the pro-

ject’s life sufficient expertise would have been developed to launch an improved product on a

larger scale to be distributed throughout Europe. The cost of the second project in four years’

time is estimated at Although there is a reasonable chance of fairly high payoffs,

the expected net present value suggests this project will do little more than break even.

‘Obviously, with the two projects combining to produce a negative NPV, the whole idea

should be scrapped,’ remarked the finance director.

Gary Owen, a recent MBA graduate, was less sure that this was the right course of action.

He reckoned that the second project was a kind of call option, the initial cost being the exer-

cise price and the present value of its future stream of benefits being equivalent to the option’s

underlying share price. The risks for the two projects looked to be in line with the variability

of the company’s share price, which had a standard deviation of 30 per cent a year.

If, by the end of Year 4, the second project did not suggest a positive NPV, the company

could walk away from the decision, the option would lapse and the cost to the company

would be the negative NPV on the first project (the option premium). But it could

be a winner, and only ‘upside’ risk is considered with call options.

Gary knew that Harlequin’s discount rate for such projects was 20 per cent and the risk-

free interest rate was 10 per cent. Table 12.4 shows his estimation of the main elements to

be considered.

£25,000

£1.32 million.

£25,000.

£400,000

CFAI_C12.QXD 3/15/07 7:21 AM Page 313

.

314 Part III Investment risk and return

12.6 WHY CONVENTIONAL NPV MAY NOT TELL THE WHOLE STORY

Earlier chapters have rehearsed the theoretical argument that capital projects that offer

positive net present values, when discounted at the risk-adjusted discount rate, should

be accepted. In Chapter 7 we raised a number of practical shortcomings with discount-

ed cash flow approaches; here we introduce an important theoretical point.

We have noted that orthodox capital projects analysis adopts a ‘now or never’ men-

tality. But the timing option reminds us that a ‘wait and see’ approach can add value.

Whenever a company makes an investment decision it also surrenders a call option –

the right to invest in the same asset at some later date. Such waiting may be passive,

waiting for the right economic and market conditions, or active, where management

seeks to gather project-related information to reduce uncertainty (further product tri-

als, competitor reaction, etc.). Hence, the true NPV of a project being undertaken today

should include the values of various options associated with the decision:

If the total is positive, the project creates wealth. This is why firms frequently defer

apparently wealth-creating projects or accept apparently uneconomic projects. Senior

managers recognise that investment ideas often have wider strategic implications, are

irreversible and improve with age.

Real options are particularly important in investment decisions when the conven-

tional NPV analysis suggests that the project is ‘marginal’, uncertainty is high and

there is value in retaining flexibility. In such cases, the conventional NPV will almost

always understate the true value.

True NPV

NPV of

basic

project

NPV of

abandonment

option

NPV of

follow-on

projects

NPV of

option

to wait

Gary Owen then entered these variables into a computer model. He found that the pres-

ent value of the four-year call option to invest in the follow-on project, with an exercise

price of million, was worth around This is because there is a chance that the

project could be really profitable, but the company will not know whether this is likely until

the outcome of the first project is known. The high degree of risk in the second project actu-

ally increases the value of the call option. It seems, therefore, that the initial project launch,

which creates an option value of for a ‘premium’ of (negative NPV) may

make economic as well as strategic sense.

£25,000£75,000

£75,000.£1.32

Such valuation calculations applied to strategic investment options raise as many

questions as they answer. For example, how much of the risk for the follow-on project

is dependent upon the outcome of the initial project? But option pricing does offer

insights into the problem of valuing ‘intangibles’ in capital budgeting, particularly

where they create options not otherwise available to the firm.

Eurotunnel considers all its options

The idea of a road tunnel under the Channel is a legacy

of Baroness Thatcher’s 11-year reign as the prime minister

who got the first tunnel built.

So keen was she on the idea, she insisted Eurotunnel be

contractually obliged to submit a feasibility study by

2000, or lose an exclusive option over the second link.

Continued

MINI CASE

CFAI_C12.QXD 3/15/07 7:21 AM Page 314