Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 13 Treasury Management and working capital policy 335

Whatever the risk management strategy, it is important that the treasurer explains

to senior management what has been done and what risk exposure remains.

■ Interest rate management

Every company is exposed to a degree of interest rate risk. This occurs when changes

in the interest rate affect a company’s profits and/or the value of its assets and liabili-

ties. The nature of the exposure depends on whether the company is a net borrower or

net investor.

The first form of interest rate risk is basis risk – the risk that the level of interest rates

will change. A second form of risk relates to changes in the yield curve over time. This

was discussed in Chapter 3 and refers to differences in short- and long-term interest

rates. The normal, positive yield curve arises where interest rates increase as the term

lengthens. In practice, however, the curve can be flat or even inverted.

Steps to manage interest rate exposure

The treasurer needs to understand the company’s interest rate risk exposure, how it is

likely to change over time and, where any of these exposures are compensating, how

they can be netted off against each other. The three-step process involves:

1 Identify the expected future cash flows that are exposed to interest rate fluctuations.

2 Specify those rates of interest beyond which steps must be taken to reduce exposure.

3 Reduce exposure by:

– Natural hedging – for example, an exposure to pay a rate of interest on a loan may

be partially offset by an investment linked to the same or a similar rate.

– Fixing the interest rate – loans can be taken out at a fixed rate rather than a float-

ing rate.

– Interest rate swaps. This is an arrangement whereby two parties agree to exchange

interest payments with each other over an agreed period. In other words, Company

A agrees to pay the interest on Company B’s loan, while Company B reciprocates

by paying the interest on Company A’s loan. Of course, what they are really

In every crisis, there’s risk and opportunity

The Chinese word for crisis (pronounced ‘Wegi’) is made from two words: risk (‘We’) and

opportunity (‘Gi’). Typical managers in the Western world tend to view a crisis as a major prob-

lem, but fail to identify the opportunities that such risks bring. However, the economic collapse

in many Far Eastern economies in the late 1990s suggests that they have invested heavily in

commercial opportunities with little regard for the risks. Business survival rests on seizing the

investment opportunity in risky markets, without jeopardising long-run corporate survival.

Korea’s crisis in 1998 was a little matter of virtually the total economy going bust. The IMF

had to step in to provide a $58 billion rescue package and help reschedule $22 billion of for-

eign debt. Korea had debt-burdened industrial companies, insolvent banks, growing unemploy-

ment and high interest rates, plus a massive amount of foreign borrowings. Total corporate

debt was twice the gross domestic product. Now that’s what you call a crisis!

The main reason why so many Korean banks were insolvent was the high level of bad

debts. Insufficient credit assessment was undertaken and major companies, with gearing levels

well beyond anything found in the UK, were encouraged to borrow even more, often investing

their new capital in dubious, high-risk ventures. Getting the balance between risk and oppor-

tunity wrong can turn a crisis into economic catastrophe.

CFAI_C13.QXD 10/26/05 11:42 AM Page 335

.

336 Part IV Short-term financing and policies

swapping is the different characteristics of the two loans. The most common char-

acteristic being exchanged is the fixed or variable interest rate, and this swap is

termed a plain vanilla or generic swap.

Heavy dependence upon short-term borrowing not only increases the risk of

insolvency from funding long-term assets with short-term borrowing, but also

exposes the company to short-term interest rate increases.

– Hedging contracts. The corporate treasurer has a variety of techniques available

to reduce interest rate risk, many of which have already been discussed. The

main methods are forward rate agreements (FRAs), interest rate futures, interest

rate options, interest rate swaps and more complex methods, such as options on

interest rate swaps (‘swaptions’). We are more concerned with the principles of

interest rate management than the detailed application. The following example

illustrates an approach to managing interest rates.

Managing interest rate risk at MedExpress Ltd

It was Karen Bailey’s first day as the financial controller of MedExpress Ltd, a fast-

growing business in the medical support industry. A quick look at the balance sheet

revealed that the company, although highly profitable, was heavily geared, with large

amounts of debt capital repayment due over the coming years. Interest rates had

changed little over the past two years, but opinions were divided over whether the

Bank of England would have to raise interest rates quite steeply in order to keep infla-

tion within prescribed government limits, or whether rates would hold, or even fall, to

stimulate exports currently suffering from the strength of sterling.

To Bailey’s surprise, the company had taken no steps to manage its exposure to inter-

est rate movements. Her first step was to identify the exposure to interest rate risk.

1 A million overdraft, with a variable interest rate, would have a significant

impact on profits and cash flow if the rate increased in the near future. If the inter-

est rate rise was dramatic, it could seriously affect cash flows and increase the risk

of liquidation.

2 The million fixed-rate long-term loan would become much less attractive if inter-

est rates fell. Paying unduly high interest rates adversely affects profitability.

3 million of the fixed rate loan would mature shortly and need replacing. The

company could choose to repay the loan at any time over the next two years. If rates

were expected to rise over that period, early redemption would be preferable.

As Bailey sought to get a grip on the interest rate exposure, she considered the fol-

lowing ways of managing interest rate risk:

(a) Interest rate mix. A mix of fixed and variable rate debt to reduce the effects of

unanticipated rate movements. She would need to give more thought to whether

the existing ratio of million variable/ million fixed rate was sufficiently well

balanced.

(b) Forward rate agreement (FRA). Some risk exposure could be eliminated by entering

into a forward rate agreement with the bank. This would lock the company into

borrowing at a future date at an agreed interest rate. Only the difference between

the agreed interest that would be paid at the forward rate and the actual loan inter-

est is transferred.

(c) Interest rate ‘cap’. It is possible to ‘cap’ the interest rate to remove the risk of a rate

rise. If the cap is set at 11 per cent, an upper limit is placed on the rate the compa-

ny pays for borrowing a specific sum. Unlike the FRA, if the rate falls, the compa-

ny does not have to compensate the bank.

(d) Interest rate futures. These contracts enable large interest rate exposures to be

hedged using relatively small outlays. They are similar in effect to FRAs, except

that the terms, the amounts and the periods are standardised.

£5£2

£1.8

£5

£2

CFAI_C13.QXD 10/26/05 11:42 AM Page 336

.

Chapter 13 Treasury Management and working capital policy 337

(e) Interest rate options. Also termed interest rate guarantees, these contracts grant the

buyer the right but not the obligation to deal at a specific interest rate at some

future date.

(f) Interest rate ‘swaps’. These occur where a company (usually very large firms) with

predominantly variable rate debt, worried about a rise in rates, ‘swaps’ or match-

es its debt with a company with predominantly fixed-rate debt concerned that

rates may fall. A bank usually acts as intermediary in the process, but it can be

through direct negotiations with another company. Each borrower will still remain

responsible for the original loan obligations incurred. Typically, firms continue to

pay the interest on their own loan and then, at the end of the agreed period, a cash

adjustment will be made between the two parties to the swap agreement. Interest

rate swaps can also involve exchanges in different currencies.

13.7 WORKING CAPITAL MANAGEMENT

The last main area of treasury management is the management of working capital,

including liquidity management. We devote the remainder of this chapter to working

capital policy and the following chapter to short-term asset management. Let us first

clarify the basic terms and ratios employed in working capital management.

Net working capital (or simply working capital) refers to current assets less current

liabilities – hence its alternative name of net current assets. Current assets include

cash, marketable securities, debtors and stock. Current liabilities are obligations that

are expected to be repaid within the year.

Working capital management refers to the financing, investment and control of net

current assets within policy guidelines. The treasurer acts as a steward of corporate

resources and needs to devise and operate clear and effective working capital policies.

Self-assessment activity 13.5

Define in your own words the main forms of derivatives – forwards, futures, swaps and options.

(Answer in Appendix A at the back of the book)

Not everyone likes derivatives

Warren Buffet, the so-called ‘Sage of Omaha’, has an excellent track record in managing

his investment vehicle, Berkshire Hathaway, having outperformed the S&P 500 index in 34

of the past 39 years (up to 2003). His success is based largely on sticking to firms that

produce simple basic products for which there is always likely to be a demand. ‘If you

don’t understand it, don’t invest in it’ is one of his mottos – he is famed for not investing

in technology stocks during the internet boom.

He is also very scathing about the relative freedom of companies and dealers to value

positions in swaps, options and other complex products whose prices are not listed on

exchanges, thus giving a potentially misleading picture of a firm’s true future liabilities.

According to Buffet, derivatives are ‘Weapons of Mass Financial Destruction’, time bombs

waiting to explode in the faces of the parties that deal in them, and for the whole econom-

ic system. Designed as risk management devices, he says they actually pose risks that cen-

tral banks and governments have so far found no effective way to control, or even monitor.

Source: Based on Warren Buffet’s annual letter to shareholders, as reported in an article in the Economist, 15 March 2003.

net working capital

Current assets less current

liabilities

CFAI_C13.QXD 10/26/05 11:42 AM Page 337

.

Liquidity management is the planned acquisition and utilisation of cash – or near

cash – resources to ensure that the company is in a position to meet its cash obligations

as they fall due. It requires close attention to cash forecasting and planning. If the

wheels of business are oiled by cash flow, the cash forecast, or cash budget, gauges

how much ‘oil’ is left in the can at any time. Any predicted cash shortfall may require

the raising of additional finance, disposal of fixed assets or tighter control over work-

ing capital requirements in order to avoid a liquidity crisis.

Various ratios are useful in assessing corporate liquidity, the following being the

most commonly employed:

1 The current ratio is the ratio of current assets to current liabilities. A high ratio (rel-

ative to the industry) would suggest that the firm is in a relatively liquid position.

However, if much of the current assets are in the form of raw materials and finished

stocks, this may not be the case.

2 The quick or ‘acid test’ ratio recognises that stocks may take many weeks to realise

in cash terms. Accordingly, it is computed by dividing current liabilities into current

assets excluding stock.

3 Days cash-on-hand ratio is found by dividing the cash and marketable securities by

projected daily cash operating expenses. As its name implies, it indicates the num-

ber of days the firm could meet its cash obligations, assuming that no further cash

is received during the period. Daily cash operating expenses should be based on

the projected cash flows from the cash budget, but a somewhat cruder approach is

to divide the annual cost of sales, plus selling, administrative and financing costs,

by 365.

338 Part IV Short-term financing and policies

liquidity management

Planning the acquisition and

utilisation of cash, i.e. cash

flow management

current ratio

Current assets divided by

current liabilities

quick/’acid test’ ratio

Current assets minus stocks,

divided by current liabilities

days cash-on-hand ratio

Cash and marketable securities

divided by daily cash operating

expenses.

Example: The General Eclectic Company (GEC)

The working capital of GEC is as follows:

Current assets

Stocks and contracts in progress 1,195

Debtors 1,572

Investments 400

Cash at bank and in hand 1,009

4,176

Less creditors due within one year (2,037

)

Net current assets 2,139

Notice that current assets are ranked in descending order of liquidity. The liquidity ratios

for GEC and the industry are:

GEC Industry average

Current ratio (4,176/2,037) 2.05 1.6

Acid test 1.46 1.2

GEC’s current and acid test ratios are both higher than the industry averages, reflecting

the company’s healthy liquidity position. But what would the position look like if the bil-

lion of cash were already committed, say, for major capital expenditure? If you recalculate

the current and acid test ratios, you will find that the liquidity position then falls below the

industry average.

£1

14,176 1,1952>2,037

£m

CFAI_C13.QXD 10/26/05 11:42 AM Page 338

.

Chapter 13 Treasury Management and working capital policy 339

13.8 PREDICTING CORPORATE FAILURE

Excessive levels of gearing are often responsible for corporate failure. However, very

highly geared companies do survive and, conversely, some low-geared companies fail.

This suggests that there are many other clues to the viability of a company, and it is not

enough simply to examine a single Balance Sheet ratio when attempting to predict

financial failure.

The Z-score method, developed by Altman (1968), attempts to balance out the rela-

tive importance of different financial indicators. This was based on examining the

financial characteristics of two samples of failed and surviving US companies to detect

which ratios were most important in discriminating between the two groups. For

example, were past failures characterised by low liquidity ratios? What other ratios

were important discriminators, and what was their relative importance?

Using a technique called discriminant analysis, the relative significance of each crit-

ical ratio can be expressed in an equation that generates a ‘Z-score’, a critical value

below which failed firms typically fall, and above which survivors are located. In gen-

eral terms, the equation is:

In this equation, a, b and c are constants derived from past observations and and

are two identified key discriminatory ratios.

A Z-score model using data for UK firms was developed by Marais (1982), an exten-

sion of which is currently used by the Datastream database. For Datastream, Marais

examined over 40 ratios before settling on four critical ones in his final model:

1

2

3

4

Other analysts, using different samples of firms, employ different ratios and weight-

ings in the equation for Z. In Marais’ model, the critical Z-value is zero. This does not

prove that an existing company displaying a Z-score of around zero is on the brink of

insolvency, merely that the firm is displaying characteristics similar to previous fail-

ures. Given that there are accounting policy differences between companies, it may be

more useful to look at changes in the Z-score over time. A declining Z-score suggests a

worsening financial condition, while an improving Z-score indicates strong corporate

financial management.

Corporate failure models, such as Z-scores, have their weaknesses (e.g. see Grice

and Ingram, 2001):

(a) ‘Failure’ is difficult to define. Usually its definition is wider than liquidation, but

all sorts of restructuring and rescue operations arise for a variety of reasons.

Stock

Sales

Stock Turnover:

All borrowing

Total capital employed less intangibles

Gearing:

Current assets less stocks

Current liabilities

Liquidity:

Pre-tax profit depreciation

Current liabilities

Profitability:

R

2

R

1

Z a bR

1

cR

2

Self-assessment activity 13.6

Which areas of treasury management would you say are most neglected by smaller firms?

(Answer in Appendix A at the back of the book)

CFAI_C13.QXD 10/26/05 11:42 AM Page 339

.

340 Part IV Short-term financing and policies

(b) All models are based on the past, when macroeconomic conditions were different

from the present.

(c) Companies employ different accounting policies, making comparison difficult.

Z-scoring is used primarily for credit risk assessment by banks and other financial

institutions, industrial companies and credit insurers. While it does not tell the whole

story behind the company’s prospects, it is widely regarded as an important indicator

of a company’s financial health and hence its credit status.

13.9 CASH OPERATING CYCLE

For a typical manufacturing firm, there are three primary activities affecting working

capital: purchasing materials, manufacturing the product and selling the product.

Because these activities are subject to uncertainty (delivery of materials may come

late, manufacturing problems may arise, sales may become sluggish, etc.), the cash

flows associated with them are also uncertain. If a firm is to maintain liquidity, it

needs to invest funds in working capital, and to ensure that the operating cycle is

properly controlled.

The cash operating cycle is the length of time between the firm’s cash payment for

purchases of material and labour, and cash receipts from the sale of goods. In other

words, it is the length of time the firm has funds tied up in working capital. This is cal-

culated as follows:

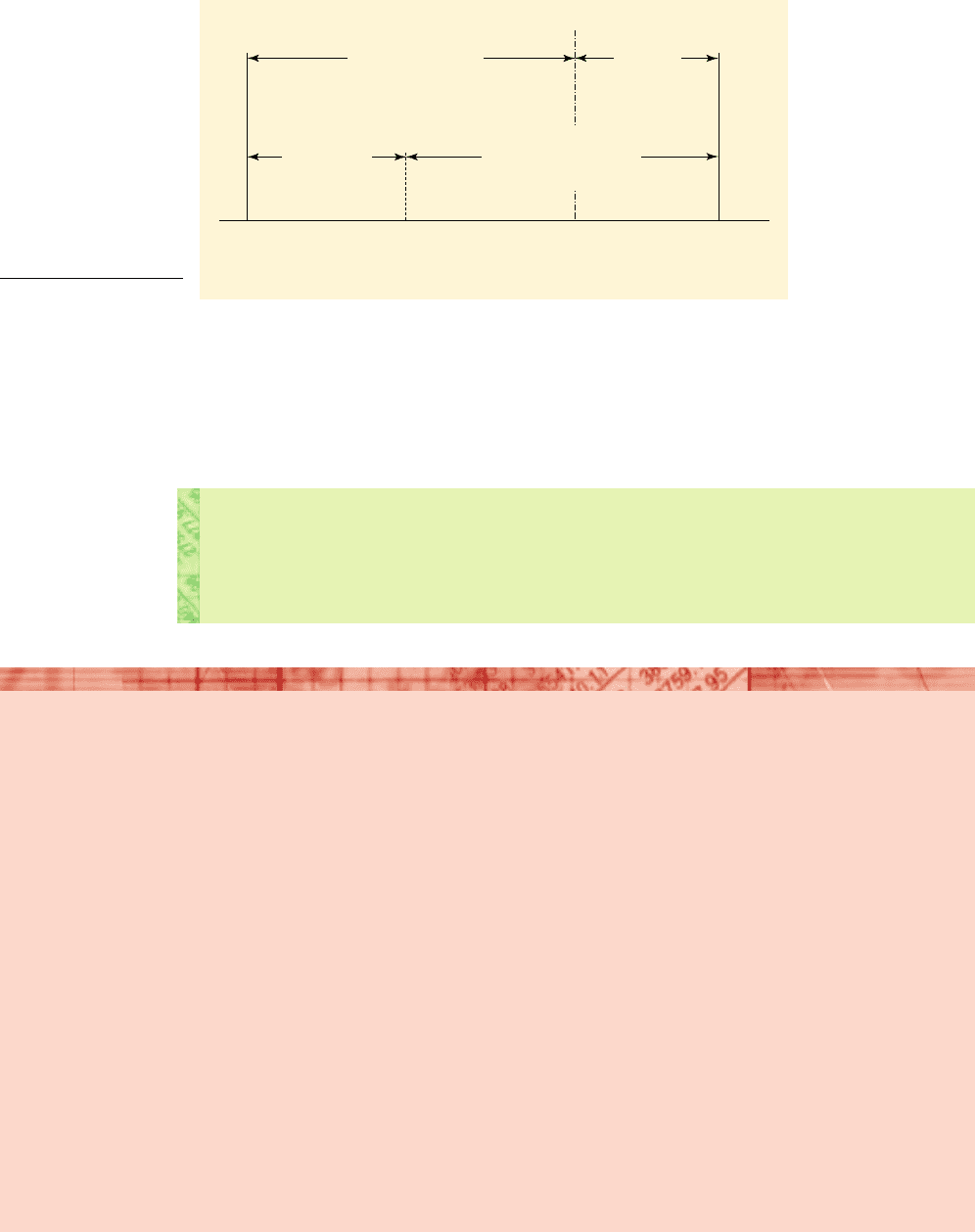

■ The cash operating cycle: Briggs plc

Briggs plc, a manufacturer of novelty toys, has the following working capital items in

its Balance Sheet at the start and end of its financial year:

Cash operating cycle stock period customer credit period

supplier credit period.

1 January 31 December

Stock

Debtors

Creditors

£4,500£3,000

£4,800£3,200

£6,500£5,500

Turnover for the year, all on credit, is and cost of sales is For how many

days is working capital tied up in each item? What is the cash operating cycle period?

Our first task is to calculate the turnover ratios for each:

To find the number of days each item is held in working capital, we divide the turnover

calculations into 365 days:

Creditors’ 1supplier credit2 period 365>8

45.6 days

Debtors 1customer credit2 period 365>12.5 29.2 days

Stock period 365>5

73 days

Creditors’ turnover

Cost of sales

Average creditors

£30,000

£3,750

8 times p.a.

Debtors’ turnover

Sales

Average debtors

£50,000

£4,000

12.5 times p.a.

Stock turnover

Cost of sales

Average stock

£30,000

£6,000

5 times p.a.

£30,000.£50,000

CFAI_C13.QXD 10/26/05 11:42 AM Page 340

.

Chapter 13 Treasury Management and working capital policy 341

The cash operating cycle is therefore:

This is illustrated in Figure 13.4.

173 29.2 45.62 56.6 days

Self-assessment activity 13.7

Explain why two firms in the same industry could have very different cash operating cycles.

What are the financial implications?

(Answer in Appendix A at the back of the book)

Stock conversion

period (73 days)

Customer

credit

period

(29 days)

Supplier credit

period

(46 days)

Materials

purchased

Cash paid

for

materials

Finished

goods

sold

Cash

received

from sales

Time

Cash conversion

cycle

(73 + 29 – 46 = 56 days)

Figure 13.4

Cash conversion cycle

Amazon spreads its risks

Has Jeff Bezos just made a big mistake?

Last week, the chairman of Amazon.com told securities

analysts that the company planned to start selling per-

sonal computers in the second half of 2001.

By traditional retailing logic, this is a bizarre mistake.

In the past, retailers have more often succeeded by con-

centrating on a small number of related product lines

than by trying to become generalists.

There is a simple reason for this: to sell something

effectively, you need to know a lot about the product.

Without this knowledge, you risk filling your shelves with

items that customers do not want.

In the early days of electronic commerce, it looked as

though these rules did not apply to online retailing.

Companies such as Amazon kept no inventories of the vast

majority of books they sold: only when your order came in

did they buy in the book you wanted from a wholesaler.

Thanks to the clever use of software, the process

happened so quickly that the book arrived within a few

days – just as fast as from a mail order retailer that was

a little slower off the mark in shipping its orders. And

this way of doing business had a marvellous advantage:

what accountants call a negative operating cycle.

Because the retailer got credit, it could sell the books to

customers and get paid before having to settle up with

its suppliers. Instead of sucking a flow of cash out of the

business, the products being sold provided working capi-

tal for other purposes.

As competition intensified, however, the customers

expected more reliable fulfilment. Thus Amazon, along

with everybody else, was forced to keep more items

in stock. That is why the company has ended up as

one of the larger operators of centralised inventory

in the US.

The attractions of the negative operating cycle are still

in place. Amazon can still receive payment for its sales

before paying its suppliers.

Source: Based on article by Tim Jackson, Financial Times, 12 June 2001.

CFAI_C13.QXD 10/26/05 11:42 AM Page 341

.

342 Part IV Short-term financing and policies

The treasury manager should ensure that the firm operates sound working capital poli-

cies. These policies cover such areas as the levels of cash and stock held, and the credit

terms granted to customers and agreed with suppliers. Successful implementation of

these policies influences the company’s expected future returns and associated risk,

which, in turn, influence shareholder value.

Failure to adopt sound working capital policies may jeopardise long-term growth

and even corporate survival. For example:

1 Failure to invest in working capital to expand production and sales may result in

lost orders and profits.

2 Failure to maintain current assets that can quickly be turned into cash can affect

corporate liquidity, damage the firm’s credit rating and increase borrowing costs.

3 Poor control over working capital is a major reason for overtrading problems,

discussed later in this chapter.

Typical questions arising in the working capital management field include the

following:

■ What should be the firm’s total level of investment in current assets?

■ What should be the level of investment for each type of current asset?

■ How should working capital be financed?

We now consider how firms establish and finance the levels of working capital

appropriate for their businesses, and how they impact on profitability and risk. The

level and nature of working capital within any organisation depend on a variety of fac-

tors, such as the following:

■ The industry within which the firm operates.

■ The type of products sold.

■ Whether products are manufactured or bought in.

■ Level of sales.

■ Stock and credit policies.

■ The efficiency with which working capital is managed.

We saw in Chapter 1 that the relationship between risk and the required financial

return is central to financial management. Investment in working capital is no excep-

tion. In establishing the planned level of working capital investment, management

should assess the level of liquidity risk it is prepared to accept, risk in the sense of the

possibility that the firm will not be able to meet its financial obligations as they fall

due. This is a further dimension of financial risk.

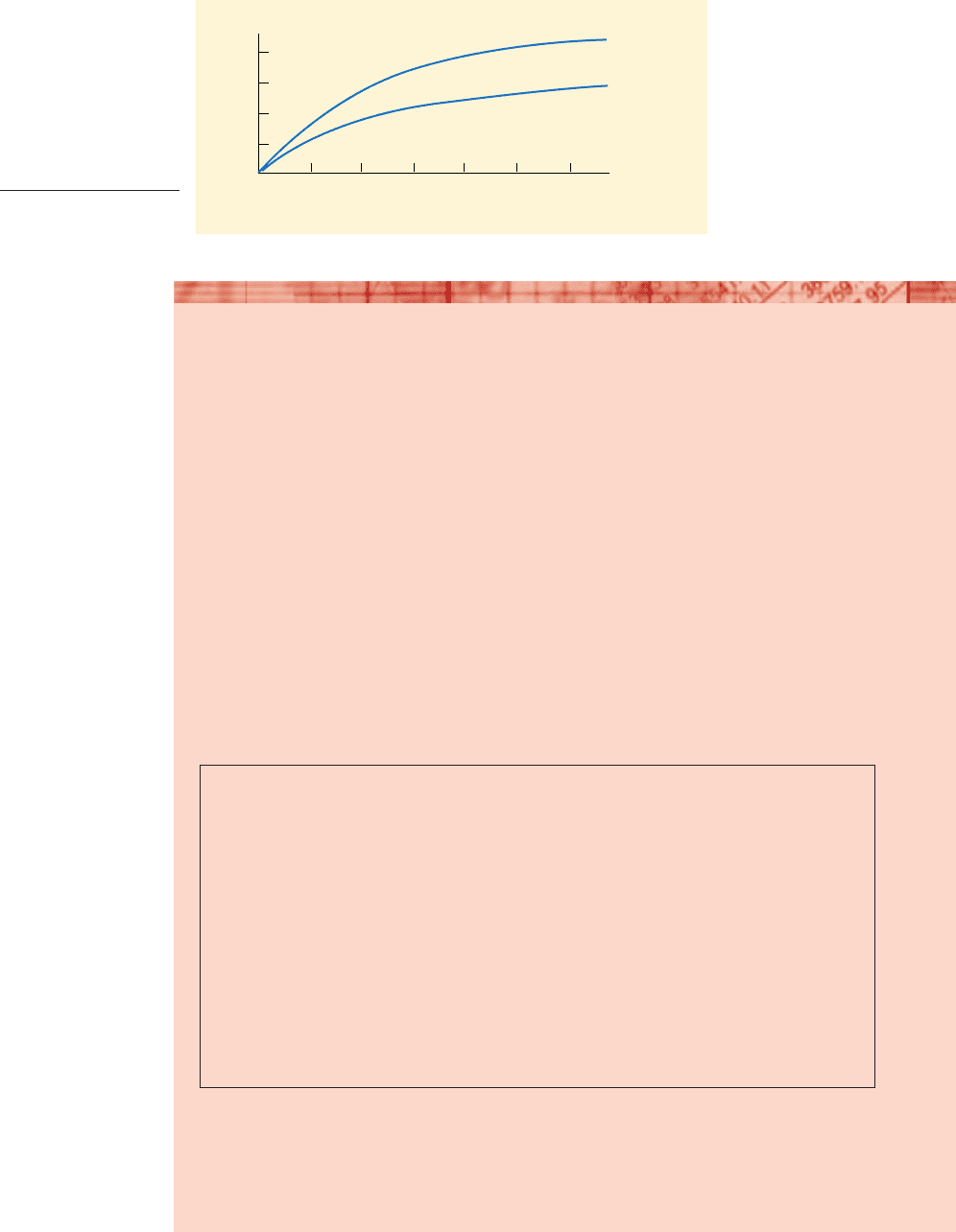

■ Working capital strategies: Helsinki plc

Helsinki plc, a dairy produce distributor, is considering which working capital policy it

should adopt.

Figure 13.5 shows the two working capital strategies under consideration. Notice

that both schedules are curvilinear, suggesting that economies of scale permit work-

ing capital to grow more slowly than sales. The firm operates with lower levels of

stock, debtors and cash under a more aggressive approach than under a more relaxed

strategy.

A relaxed, lower risk and more flexible policy for working capital means maintain-

ing a larger cash balance and investment in marketable securities that can quickly be

turned into cash, granting more generous customer credit terms and investing more

heavily in stock. This may attract more custom, but will usually lead to a reduction in

profitability for the business, given the high cost of tying up capital in relatively low

13.10 WORKING CAPITAL POLICY

CFAI_C13.QXD 10/26/05 11:42 AM Page 342

.

Chapter 13 Treasury Management and working capital policy 343

0 10 20 40 60 80 100

Sales (£)

Current assets (£m)

40

Relaxed

strategy

Aggressive

strategy

10

20

30

Figure 13.5

Helsinki plc working

capital strategies

e is for ‘efficiency’

In 2000, the big-three US car-makers, General Motors, Ford and DaimlerChrysler, joined forces

to develop a jointly-owned procurement exchange, in turn causing suppliers to worry about

pressures from manufacturers on component prices. In response, six of the largest parts sup-

pliers also combined to examine e-commerce initiatives in an effort to accelerate cost sav-

ings. Their aim was to improve supply-chain management and customer support, and

management of after-market activities.

The CEO of one supplier, Eaton, averred: ‘By working together on joint technology solu-

tions, we can avoid repetitive costs and establish common solutions that ultimately improve

effectiveness throughout the supply chain.’

Since 2000, the fears of suppliers that the manufacturers would reap the main benefits of

technology-driven procurement have receded, as the two sides now co-operate in a system

that has evolved from these early developments, namely the Covisint Communicate portal

service, that now serves more than 175,000 users from 20,000 companies. In particular, sup-

pliers to the automobile manufacturers are now able to use this service to procure their own

inputs more economically.

The following mini-case study is taken from Covisint’s website recording Ford’s experience.

The website also records the experience of Visteon, a parts supplier that was spun-off from

its parent, Ford, and found that it needed to rapidly develop a supplier portal and supplier

access management system to maintain competitiveness, and how it found the solution at

Covisint.

Source: Based on article by Nikki Tait, Financial Times, 4 June 2000, and Covisint website (www.covisint.com).

Ford

Ford already understood the value of a portal in working collaboratively with suppliers when it

chose to outsource the development and maintenance to Covisint. Covisint Communicate is

used to provide the Ford Supplier Portal which improves sharing of information and collaborative

business processes with suppliers. Covisint has provided these services to enable the Ford Supplier

Portal since 2001. Covisint Communicate helps Ford save on the cost of maintaining a supplier-

facing portal and frees valuable resources to direct their attention to improving business processes

with suppliers.

The Covisint Communicate service is used by Ford to securely share a large number of Ford-

specific applications with global supplier companies. In addition, Ford is able to maintain an

extensive library of updated documents and information that suppliers need to collaborate with

Ford. Covisint Communicate is available in seven languages and used by Ford and its suppliers

globally.

CFAI_C13.QXD 10/26/05 11:42 AM Page 343

.

344 Part IV Short-term financing and policies

A more aggressive working capital strategy is likely to improve the return on cap-

ital. In Helsinki’s case, the rate increases to 30 per cent. But this is achieved by

increasing liquidity risk. Net working capital falls to only million and the current

ratio to 1.3.

■ Working capital costs

Managing working capital involves a trade-off not only between risk and required

return, but also between costs that increase and costs that fall with the level of

investment. Costs that increase with additional investment are termed carrying

costs, while costs that fall with increases in investment are termed shortage costs.

These two types of cost may be found in most forms of current assets, but particu-

larly in stocks and cash.

The main form of carrying costs is opportunity costs associated with the cost of

financing the investment.

■ Financing costs: Bedford Auto-Vending Machine Company

The Bedford Auto-Vending Machine Company is considering how much to invest in

current assets. Two working capital policies are under investigation.

Relaxed policy ( ) Aggressive policy (

)

Stock 32 25

Debtors 28 22

Cash and marketable securities 12 –

72 47

It will be seen that the relaxed policy requires a further million investment in

working capital over and above that required for the aggressive policy. What is the

£25

£m£m

£5

profit-generating assets. Conversely, an aggressive policy should increase profitabili-

ty, while increasing the risk of failing to meet the firm’s financial obligations.

In Table 13.1, the relaxed working capital strategy involves a further million

investment in current assets. The additional stocks and more generous credit facilities

enable Helsinki’s management to attain an additional million sales with the aggres-

sive policy. This gives a 19.5 per cent return on capital employed and a secure current

ratio of 2.7.

£5

£20

carrying costs

Stock costs that increase with

the size of stock investment

shortage costs

Stock costs that reduce with

size of stock investment

Table 13.1

Helsinki plc: profitability

and risk of working capital

strategies

Relaxed (

)

Aggressive (

)

Current assets (CA) 40 20

Fixed assets 25 25

Total assets 65 45

Current liabilities (CL) (15) (15)

Capital employed (net assets) 50 30

Planned sales 65 60

Planned profit (15% of sales) 9.75 9.0

Return on capital employed 19.5% 30.0%

Net working capital

(CA – CL)

Current ratio (CA/CL) 2.7 1.3

£5 m£25 m

£m£m

CFAI_C13.QXD 10/26/05 11:42 AM Page 344