Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 14 Short-term asset management 375

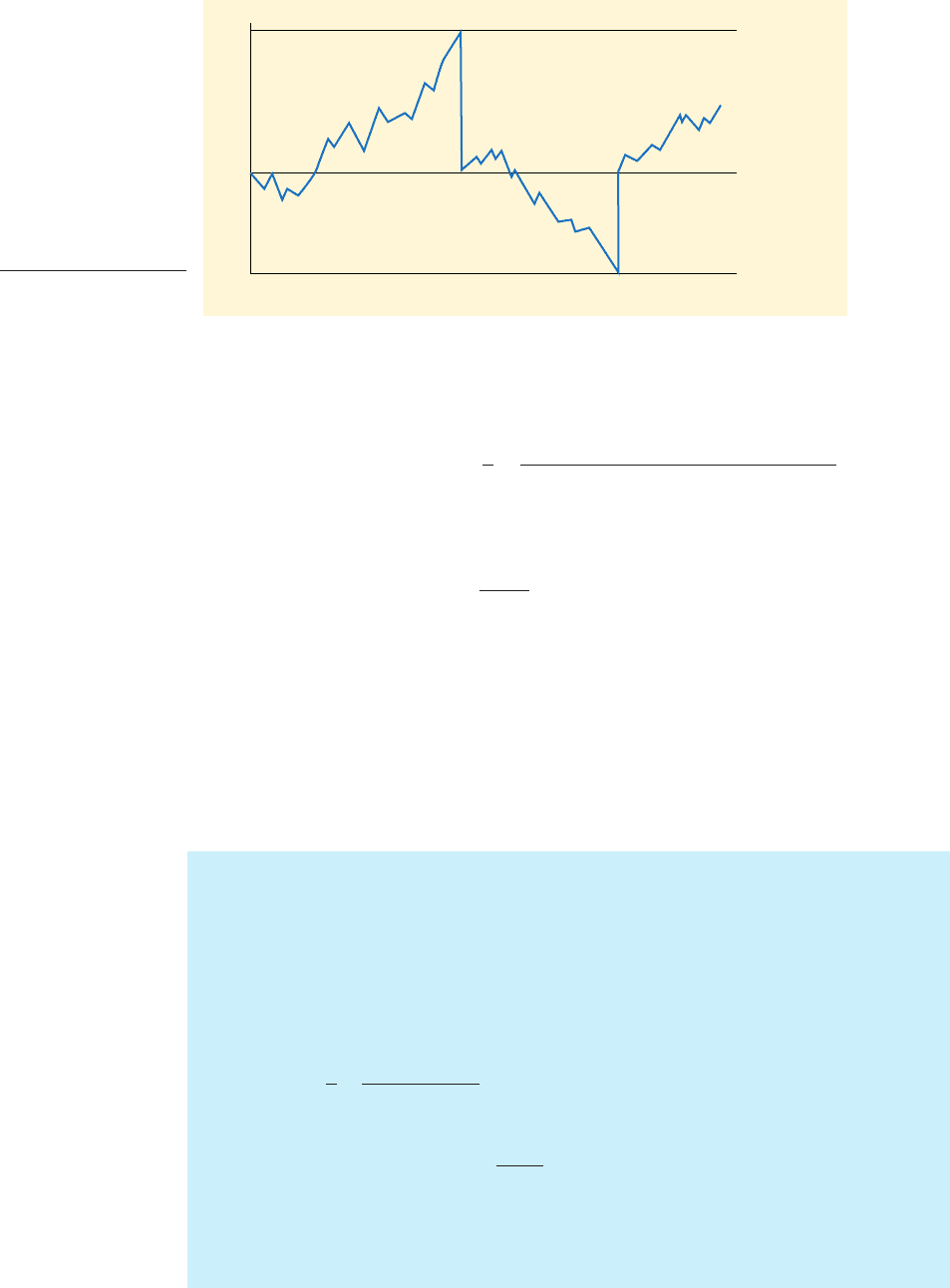

Time

Lower limit

Return point

Upper limit

Cash balance

Figure 14.5

Miller-Orr cash man-

agement model

In general, the limits will be wider apart when daily cash flows are highly variable,

transaction costs are high and interest on short-term investments is low. The Miller

and Orr formula for setting the limits is:

Range between upper

and lower limits

The cash balance does not return to a point mid-way between the upper and lower

limits. The return point is:

By having a return point below the mid-point between the two limits, the average cash

balance on which interest is charged is reduced.

The Baumol and Miller–Orr models are really two extremes: the former assumes

cash flows are constant, while the latter assumes they are unpredictable. In practice, an

experienced cash controller, using a detailed cash budget, should perform better than a

cash management model and should enable the company to operate on a lower cash

balance. The primary value of simple cash management models may be to evaluate

how much better the ‘hands-on’ expert can perform than the ‘hands-off’ control model.

Return point lower limit

range

3

3 a

3

4

transaction cost cash flow variance

interest rate

b

1>3

Example

The financial manager at Millor Ltd believes that cash flows are almost impossible to pre-

dict on a daily basis. She knows that a minimum cash balance of is required and

transferring money to or from the bank costs per transaction. Inspection of daily cash

flows over the past year suggests that the standard deviation is a day (i.e. million

variance). The interest rate is 0.03 per cent per day.

The Miller–Orr model specifies the range for the cash balance as below:

The decision rule is: if the cash balance reaches buy

of marketable securities. If the cash balance falls to sell of marketable secu-

rities for cash to return it to

£30,400.

£10,400£20,000,

ˇˇ £20,8001£51,200 £30,4002£51,200,

The return point lower limit

range

3

£30,400

The upper limit lower limit range 1£20,000 £31,2002 £51,200

Range 3 a

3

4

50 9,000,000

0.0003

b

0.3333

£31,200 approx.

£9£3,000

£50

£20,000

CFAI_C14.QXD 3/15/07 7:16 AM Page 375

.

Questions with

coloured numbers have solutions in Appendix B on page 706.

1 Specify the basic formula for calculating the cost of cash discounts.

2 What are the main differences in the assumptions underlying the Baumol and Miller–Orr cash models?

3 Hunslett Express Company specifies payment from its customers at the end of the month following delivery.

On average, customers take 70 days to pay. Sales total million per year and bad debts total per year.

The company plans to offer cash discounts for payment within 30 days. It is estimated that 50 per cent of

customers will take up the discount, but that the remaining customers will take 80 days to pay. The company

has an overdraft facility costing 13 per cent p.a. If the proposed scheme is introduced, bad debts will fall to

and savings in credit administration of p.a. are expected.

Should the company offer the new credit terms?

4 Salford Engineers Limited, a medium-sized manufacturing company, has discovered that it is holding 180

days’ stock while its main competitors are holding only 90 days’ stock.

Required

(a) Discuss what you consider to be the most important factors determining the optimum level of stock-

holding for the company.

(b) What action would you take if you were asked to investigate the reasons for Salford’s high level of stock?

(Certified Diploma)

5 Torrance Ltd was formed in 1988 to produce a new type of golf putter. The company sells the putter to whole-

salers and retailers and has an annual turnover of The following data relate to each putter produced:

£600,000.

£12,000£20,000

£40,000£8

QUESTIONS

376 Part IV Short-term financing and policies

Option

123

Increase in average collection period (days) 10 20 30

Increase in sales 30,000 45,000 50,000

1£s2

££

Selling price 36

Variable costs (18)

Fixed cost apportionment (6) (24)

Net profit 12

The cost of capital (before tax) of Torrance Ltd is estimated at 15 per cent.

Torrance Ltd believes it can expand sales of this new putter by offering customers a longer period in which

to pay. The average collection period of the company is currently 30 days. The company is considering three

options in order to increase sales. These are as follows:

Torrance Ltd is also reconsidering its policy towards trade creditors. In recent months, the company has

suffered from liquidity problems, which it believes can be alleviated by delaying payment to trade creditors.

Suppliers offer a 2.5 per cent discount if they are paid within 10 days of the invoice date. If they are not paid

within 10 days, suppliers expect the amount to be paid in full within 30 days. Torrance Ltd currently pays sup-

pliers at the end of the 10-day period in order to take advantage of the discounts. However, it is considering

delaying payment until either 30 or 45 days after the invoice date.

Required

(a) Prepare calculations to show which credit policy the company should offer its customers.

(b) Discuss the advantages and disadvantages of using trade credit as a source of finance.

(c) Prepare calculations to show the implicit annual interest cost associated with each proposal to delay pay-

ment to creditors. Discuss your findings.

(Certified Diploma)

CFAI_C14.QXD 3/15/07 7:16 AM Page 376

.

6 (a) Discuss:

(i) The significance of trade creditors in a firm’s working capital cycle, and

(ii) the dangers of over-reliance on trade credit as a source of finance.

(b) Keswick plc traditionally follows a highly aggressive working capital policy, with no long-term borrow-

ing. Key details from its recently compiled accounts appear below:

Chapter 14 Short-term asset management 377

December January February March April May

£000 £000 £000 £000 £000 £000

Expected sales 120 150 170 220 250 280

Purchases 156 180 195 160 150 160

Advertising 15 18 20 25 30 30

Rent 40 40

Rates 30

Wages 16 16 18 18 20 20

Sundry expenses 20 24 24 26 26 26

£m

Sales (all on credit) 10.00

Earnings before interest and tax (EBIT) 2.00

Interest payments for the year 0.50

Shareholders’ funds (comprising

million issued share capital, par value

25p, and million revenue reserves) 2.00

Debtors 0.40

Stocks 0.70

Trade creditors 1.50

Bank overdraft 3.00

£1

£1

A major supplier which accounts for 50 per cent of Keswick’s cost of sales is highly concerned about

Keswick’s policy of taking extended trade credit. The supplier offers Keswick the opportunity to pay for sup-

plies within 15 days in return for a discount of 5 per cent on the invoiced value.

Keswick holds no cash balances but is able to borrow on overdraft from its bank at 12 per cent. Tax on cor-

porate profit is paid at 33 per cent.

Required

Determine the costs and benefits to Keswick of making this arrangement with its supplier, and recommend

whether Keswick should accept the offer. Your answer should include the effects on:

■ The working capital cycle

■ Interest cover

■ Profits after tax

■ Earnings per share

■ Return on equity

■ Capital gearing

7 International Golf Ltd operates a large warehouse, selling golf equipment direct to the public by mail order

and to small retail outlets. The cash position of the company has caused some concern in recent months. At

the beginning of December 1993, there was an overdraft at the bank of The following data concern-

ing income and expenses has been collected in respect of the forthcoming six months:

£56,000.

The company also intends to purchase and pay for new motor vans in February at a cost of and to

pay taxation due on 1 March of

Sales to the public are on a cash basis and sales to retailers are on two months’ credit. Approximately 40 per

cent of sales are made to the public. Debtors at the beginning of December are 70 per cent of which

are in respect of November sales.

Purchases are on one month’s credit and, at the beginning of December, the trade creditors were

The purchases made in December, January and February are considered necessary to stock up for the sales

demand from March onwards.

Continued

£140,000.

£110,000,

£30,000.

£24,000

CFAI_C14.QXD 3/15/07 7:16 AM Page 377

.

All other expenses are paid in the month in which they are incurred. Sundry expenses include per

month for depreciation.

Required

(a) Explain the benefits to a business of preparing a cash flow forecast.

(b) Identify and discuss the costs to a business associated with:

(i) holding too much cash;

(ii) holding too little cash.

(c) Prepare a cash flow forecast for International Golf Ltd for the six months to 31 May 1994, which shows

the cash balance at the end of each month.

(d) State what problems International Golf Ltd is likely to face during the next six months and how these

might be dealt with. (Certified Diploma)

8 (a) The Treasurer of Ripley plc is contemplating a change in financial policy. At present, Ripley’s balance sheet

shows that fixed assets are of equal magnitude to the amount of long-term debt and equity financing. It is

proposed to take advantage of a recent fall in interest rates by replacing the long-term debt capital with an

overdraft. In addition, the Treasurer wants to speed up debtor collection by offering early payment dis-

counts to customers and to slow down the rate of payment to creditors.

As his assistant, you are required to write a brief memorandum to other Board members explaining

the rationales of the old and new policies and pinpointing the factors to be considered in making such a

switch of policy.

(b) Bramham plc, which currently has negligible cash holdings, expects to have to make a series of cash pay-

ments (P) of million over the forthcoming year. These will become due at a steady rate. It has two

alternative ways of meeting this liability.

Firstly, it can make periodic sales from existing holdings of short-term securities. According to

Bramham’s financial advisers, the most likely average percentage rate of return (i) on these securities is

12 per cent over the forthcoming year, although this estimate is highly uncertain. Whenever Bramham

sells securities, it incurs a transaction fee (T) of and places the proceeds on short-term deposit at 5 per

cent per annum interest until needed. The following formula specifies the optimal amount of cash raised

(Q) for each sale of securities:

The second policy involves taking a secured loan for the full million over one year at an interest

rate of 14 per cent based on the initial balance of the loan. The lender also imposes a flat arrangement fee

of which could be met out of existing balances. The sum borrowed would be placed in a notice

deposit at 9 per cent and drawn down at no cost as and when required.

Bramham’s Treasurer believes that cash balances will be run down at an even rate throughout the year.

Required

Advise Bramham as to the most beneficial cash management policy.

Note: ignore tax and the time-value of money in your answer.

(c) Discuss the limitations of the model of cash management used in part (b). (ACCA)

£5,000,

£1.5

Q

B

2 P T

i

£25,

£1.5

£8,000

378 Part IV Short-term financing and policies

1 Sound credit management can play an important role in the financial success of a business.

Required

(a) Explain the role of the credit manager within a business.

(b) Discuss the major factors a credit manager would consider when assessing the creditworthiness of a par-

ticular customer.

(c) Identify and discuss the major sources of information that may be used to evaluate the creditworthiness

of a commercial business.

(d) State the basis upon which any proposed changes in credit policy should be evaluated.

(Certified Diploma)

2 If you are based in a firm where credit management is important, apply the above question to your organisation.

Practical assignment

CFAI_C14.QXD 3/15/07 7:16 AM Page 378

.

Short- and medium-term finance

15

Learning objectives

This chapter aims to evaluate the advantages and disadvantages of the following means of

short- and medium-term finance:

■ Trade credit.

■ Bank finance.

■ Factoring and invoice discounting.

■ Bills of exchange and acceptance credits.

■ Hire purchase.

■ Leasing.

■ Financing foreign trade.

Particular attention is given to leasing in view of its importance as a method of financing the

acquisition of a wide range of assets.

Whom can you bank on?

Relationships between the banking system and the

business community are central to economic devel-

opment and progress. This is especially true for the

small firms that have to rely heavily on their banks

for support. However, some commercial banks do not

always enjoy easy relationships with their clients.

Over the years, banks have been criticised by small

firm pressure groups for a number of reasons, such as

insistence on ‘excessive’ level of security to back their

lending, tardiness in passing on interest rate reduc-

tions to customers, reluctance to advance longer-

term finance in loan form rather than via overdrafts,

although many of these criticisms are receding.

In response to such issues, the Federation of Private

Business conducts a biennial survey among its 25,000

members to gauge the quality of service provided by

their bankers. In its latest survey (December 2004), it

found a new problem – an increasing number of limited

liability firms having to put up personal assets to guar-

antee overdrafts with banks. This may have been in

response to an anticipated tightening of the regulations

connected with the Small Firms Loan Guarantee

Scheme (see below).

It also reported that despite recommendations by

the Office of Fair Trading that banks make it easier

for customers to switch accounts, few were doing so.

This was despite 40 per cent of firms surveyed that

banked with three leading high-street banks having

had cause to complain about the service received. In

its league table of bank performance (based on com-

petitiveness of interest rate and charges, knowledge

of industry, efficiency and reliability), smaller banks

outshone their larger brethren with Allied Irish Bank,

for the sixth time running, a clear winner.

The FPB argues the need for a specialist unit at the

Bank of England to monitor banking standards and to

offer protection to small businesses. Unsurprisingly, it

urged the reopening of the Bank’s Small Firms

Division (closed earlier in 2004) to address issues like

inconsistency in quality of service offered by the

commercial banks.

Source: Bank Report 2004, Federation of Private Businesses,

www.fpb.co.uk.

CFAI_C15.QXD 10/26/05 11:58 AM Page 379

.

380 Part IV Short-term financing and policies

15.1 INTRODUCTION

While banks have taken a number of steps to address the criticisms raised by their

detractors, many firms still find it difficult to arrange short-term finance, and many

remain critical of the banking system. (For news of developments in the field of finance

for small firms, see the website of the British Bankers Association: www.bba.org.uk.)

Despite such problems, the banks remain the most important source of external finance

for small- and medium-sized firms, providing 52 per cent of their external finance dur-

ing 2000–02. However, it is not only smaller firms that tend to rely on shorter-term

finance; firms of all sizes use these sources to varying degrees. For example, most large

companies arrange access to overdraft finance to tide them over temporary liquidity

shortages.

In this chapter, we examine the nature and characteristics of alternative sources of

finance, ranging from very short-term facilities (e.g. trade credit) to rather longer-term

ones (e.g. bank loans and finance leasing). Generally, we classify these under the head-

ing of short and medium term, although the distinction is somewhat arbitrary. For

example, lease finance can be used for varying time periods, ranging from a few weeks

(operating leases) to as long as 15 years in the case of some finance leases. In addition,

bank overdrafts are essentially short-term in nature, but are often used continuously

for lengthy periods.

15.2 TRADE CREDIT

Trade credit is finance obtained from suppliers of goods and services over the period

between delivery of goods (or provision of a service) and the subsequent settlement of

the account by the recipient. During this time, the company can enjoy the goods or

benefit from the service provided without having to pay up. Granting customers a

credit period is part of normal trading relationships throughout most of UK industry.

For this reason, it is sometimes called ‘spontaneous finance’. Additional features of

trade credit packages include the amount of credit that a company is allowed to

obtain, whether interest is paid on overdue accounts, and whether discounts are

offered for early payment.

A common way of expressing credit terms is as follows:

This means that the supplier will offer a 2 per cent discount for early settlement (in

this case, within 10 days); otherwise, it expects payment of the invoice in full within 30

days. As shown below, not to take a discount is often an expensive option. Moreover, a

very effective way of antagonising suppliers is to delay payment and attempt to claim

the discount.

The length of the trade credit period offered depends partly on the following factors:

■ Industry custom and practice. Terms of trade credit typically reflect traditional norms

built up over years of trading. Although these terms often vary between industries,

they are quite uniform within industries. Any supplier wanting to depart from the

industry norm has to compensate with some other product offering, say, speed of

delivery, to avoid losing sales.

■ Relative bargaining power. If the supplier has a large range of customers, none of

whom are crucial to it, and if the product is essential to buyers, the supplier has

great power to impose its own terms. This power is enhanced by lack of strong com-

petitors.

¿2>10: net 30¿

CFAI_C15.QXD 10/26/05 11:58 AM Page 380

.

Chapter 15 Short- and medium-term finance 381

Self-assessment activity 15.1

Trade credit is often called ‘spontaneous finance’ or ‘automatic finance’. Can you see why?

(Answer in Appendix A at the back of the book)

■ Type of product. Products that turn over rapidly are often sold on short credit terms

because they command small profit margins. Delay in settlement would severely

erode the margin.

A firm’s trade credit position is volatile, as it depends on which of its suppliers are

awaiting payment and for how much, and these factors change continuously with the

flow of business transactions. It is useful to express the average trade credit period in

days calculated as follows:

However, for the outside observer, this figure is only valid at the Balance Sheet date,

and even so, could have been ‘window-dressed’ by accelerated settlements immedi-

ately prior to drawing up the accounts. It is sometimes expressed in terms of total pur-

chases and sometimes, when data for purchases is unavailable, in terms of overall cost

of sales.

Creditor days

Trade creditors

Credit purchases

365

Because trade credit represents temporary borrowing from suppliers until invoices

are paid, it becomes an important method of financing investment in current assets.

Firms may be tempted to view trade creditors as a cheap source of finance although

statutory rights to claim interest on late payments now exist. Having a debtors’ col-

lection period shorter than the trade collection period may be taken as a sign of effi-

cient working capital management. However, trade credit is by no means free – it

carries both hidden and overt costs.

Excessive delay in settling invoices can undermine the stability of a business in a

number of ways. Existing suppliers may be unwilling to extend more credit until exist-

ing accounts are settled. They may start to assign lower priority to future orders placed

by the culprit, they may raise prices in the future or they may simply not supply at all.

In addition, if the firm acquires a reputation as a bad payer among the business com-

munity, its relationships with other suppliers may be soured.

Finally, by delaying payment of accounts due, the company may be passing up

valuable discounts, thus effectively increasing the cost of goods sold. This can be

shown with a simple example.

Martock plc is offered a discount of 2.5 per cent on an invoice of £100,000 by a major

supplier if it settles the account within 10 days, rather than taking the normal credit

period of 30 days. Martock, which has at present a zero cash balance, can borrow from

its bank at an interest rate of 15 per cent p.a. Should it borrow and exploit the discount,

or take the full credit period of 30 days?

If it takes the discount and pays on (but not before!) day 10, it will have to borrow

for an additional period of 20 days, since it

would have to settle anyway after 30 days. If it waits until day 30, the cost of settling

the bill is effectively the lost discount of By advancing payment, Martock is

borrowing for 20 days in order to save an interest rate over 20 days of

2.56 per cent. Expressed as an annual interest rate, this approximates to:

£2,500

£97,500

365

20

100 46.8%

£2,500,£97,500

£2,500.

197.5 per cent £100,0002 £97,500

CFAI_C15.QXD 10/26/05 11:58 AM Page 381

.

382 Part IV Short-term financing and policies

A more accurate solution can be obtained by compounding over the number of

20-day periods in a year (18.25). The true rate is:

As this compares very favourably with the 15 per cent cost of borrowing, Martock

should borrow in order to advance this payment.

During the recession of the early 1990s, there was widespread concern over the

tendency for more firms to delay payment of accounts. Larger firms have allegedly

exploited their industrial muscle by simultaneously spinning out their trade credit

periods while insisting on prompter payment from small firm customers. This prob-

lem led the UK Government in 1998 to introduce legislation for a statutory right to

demand interest on overdue accounts, initially for smaller companies only.

Until the passage of the Late Payments of Commercial Debts (Interest) Act in 1998,

interest could only be claimed on late debts if it was included in the contract, or if

awarded by a court. The Act enabled small businesses (50 or fewer employees) to

claim interest from large businesses and the public sector. From November 2000, they

were entitled to claim interest from other small businesses. From November 2002, any

business obtained the statutory right to claim interest from any other firm or from the

public sector.

Firms that suffer from late payment face a difficult choice – delay settlement to their

own suppliers or fall back on their banks for supplementary finance, via either over-

draft or loan facilities. We now consider bank lending.

311.02562

18.25

14 58.6%

15.3 BANK CREDIT FACILITIES

Major commercial banks extend a variety of credit facilities, ranging from short-term

overdrafts to long-term loans of varying terms. The interest rate generally increases

with the term of the advance, the actual rate being linked to the bank’s base rate, which

in turn depends on the base rate set by the national monetary authority (in the UK, the

Monetary Policy Committee of the Bank of England).

Self-assessment activity 15.2

What is the true annual interest rate paid when a firm delays payment under the following

credit terms: ‘ net 40’?

(Answer in Appendix A at the back of the book)

1

1

2

>15:

Self-assessment activity 15.3

What do you think are the main considerations a banker makes in assessing an application

for a loan or overdraft?

(Answer in Appendix A at the back of the book)

■ Overdrafts

The best-known form of bank finance is the overdraft, a facility available for specified

short-term periods such as six months or a year. This facility specifies a maximum

amount that the firm can draw upon either via direct cash withdrawals or in payments

by cheque to third parties. Interest is paid on the negative balance outstanding at

any time rather than the maximum advance agreed. Compared with many other

forms of finance, it is relatively inexpensive, with the interest cost set at some two to

CFAI_C15.QXD 10/26/05 11:58 AM Page 382

.

Chapter 15 Short- and medium-term finance 383

term loans

Loans made by a bank for a

specific period or term, usually

longer than a year

five percentage points above base rate, although most banks also levy an arrangement

fee (perhaps 1 per cent) of the maximum facility.

In principle, overdrafts are repayable at very short notice, even on demand, although

unless the company abuses the terms of the facility by exceeding the agreed overdraft

limit, the overdraft is unlikely to be called in. Besides, it is rarely in the best interests of

a bank to do this suddenly, as it could exert such severe financial pressure on the client

as to force it into liquidation.

Nevertheless, the bank retains the right to appoint a receiver if the client defaults on

the debt. In practice, well-behaved clients can roll forward overdrafts from period to

period. As a result, the overdraft effectively becomes a form of medium-term finance.

Even in these cases, it is wise policy not to use an overdraft to invest in long-term

assets that would be difficult to liquidate at short notice if the bank suddenly decided

to call in the debt.

To protect against risk of loss, the bank will usually demand that the overdraft be

secured against company assets, i.e. in the event of default, the receiver will reimburse

the bank out of the proceeds of selling these assets. Security can be in two forms: a

fixed charge, where the overdraft is secured against a specific asset, or a floating

charge, which offers security over all of the company’s assets, i.e. those with a ready

and stable second-hand market. A floating charge therefore ranks behind a fixed

charge in the queue for payment. For trading companies, overdrafts are often secured

against the inventory that the company purchases with the funds borrowed or even

against debtors. In this respect, the overdraft is ‘self-liquidating’ – it can be reduced as

the company sells goods and banks the proceeds.

Alternatively, and more to the liking of most bankers, overdrafts are secured against

property. However, this created problems in the recession of the early 1990s, when the

unprecedented collapse of property market prices often reduced the value of assets

upon which overdrafts were secured to below the balance outstanding. Many banks

made major provisions against the increasing likelihood of bad debts. In addition, they

incurred much ill-will by allegedly recalling overdrafts prematurely, thus exacerbating

the liquidity difficulties of their clients, already seriously affected by falling sales.

Many critics accused the banks of forcing many essentially sound companies out of

business.

■ Term loans

Term loans are loans for a year or longer. UK banks have traditionally been reluctant to

lend on a long-term basis, mainly because the bulk of their deposit liabilities are short-

term. In the event of unexpectedly high demand by the public to withdraw cash, this

could leave them vulnerable if they were unable to recall advances quickly from bor-

rowers. This low exposure to default risk is generally regarded as the reason why bank-

ing collapses are relatively uncommon in the UK.

However, because of criticism by a series of official reports on the financial system

and the advent of intensive competition from London branches of overseas banks, the

main UK banks are now far more willing to lend long-term. Term loans can be arranged

at variable or fixed rates of interest, although the interest cost is usually higher in the

latter case. For variable rate loans, the rate set may be two to five percentage points

above the bank’s base rate, depending on the credit rating of the client and the quality

of the assets offered as security. In addition, an arrangement fee is usually charged.

Self-assessment activity 15.4

Which are normally more expensive for firms – overdrafts or term loans? Why?

(Answer in Appendix A at the back of the book)

CFAI_C15.QXD 10/26/05 11:58 AM Page 383

.

384 Part IV Short-term financing and policies

Tailor-made facilities are available to some firms, with repayment terms designed

to suit their expected cash flow profiles. Sometimes, the bank may grant a ‘grace

period’ at the outset of the loan when no capital is repayable and interest may be

charged at a relatively low, but increasing, rate. This is particularly suitable for a

small, developing company trying to establish itself. Similarly, a balloon loan is

where increasing amounts of capital are repaid towards the end of the loan period,

whereas a bullet loan is where no capital is repaid until the very end of the loan

period.

In its Finance for Small Firms report in 1995, the Bank of England estimated that

fixed-term lending to small firms had overtaken overdraft finance, the proportion of

total lending in the form of term loans being 60 per cent, compared with 40 per cent

only two years previously. By 2003, the ratio of overdrafts to term lending had fall-

en to 23:77. (Finance for Small Firms is published annually and can be viewed at

www.bankofengland.co.uk.)

■ Revolving credit facilities (revolvers)

A term loan generally specifies an agreed payment profile and the amounts repaid can-

not normally be re-borrowed. A revolver allows the borrower to borrow, repay and re-

borrow over the life of the loan facility, rather like a continuous overdraft. Like an

overdraft, it is frequently secured on the borrower’s working capital, e.g. using debtors

and stocks as collateral, although very large firms may not be asked for any security.

The advantage of revolvers is the enhanced flexibility provided, i.e. funds can be reused

in a continuous credit line. The commitment by the bank thus ‘revolves’ – the borrow-

er can continue to ask for loans, subject to giving suitable notice, so long as the com-

mitted total is not exceeded. The fees charged include:

■ A front-end or facility fee for setting up the loan.

■ A commitment fee to compensate the bank for having to commit some of its loan

capacity by setting aside reserve assets to meet capital adequacy rules.

■ The interest cost, usually expressed as so many basis points (one )

above LIBOR, the rate at which London-based banks lend to each other.

In May 2004, the brewing firm SAB Miller plc announced a refinancing of an exist-

ing RCF. The new facility, for a total amount of $1 billion, would replace the group’s

existing $720 million facility. It was priced at a floating rate of LIBOR plus 32.5 basis

points.

■ Loan Guarantee Scheme (LGS)

The LGS was introduced in 1981 following the Report of the Committee to Review the

Functioning of Financial Institutions, set up to investigate the provision of finance to

business. The Committee pointed to the difficulty faced by smaller firms with little or

no track record in obtaining suitable longer-term finance.

Such firms are reluctant to release control by issuing equity, while investors are

reluctant to purchase equity owing to the risks involved, especially the difficulty of liq-

uidating their investment on acceptable terms. Firms may also have difficulty per-

suading banks of the inherent viability of their businesses, and are frequently unable

to offer sufficient and suitable security. Where banks do offer loan finance, it is often

on less advantageous terms than those extended to larger firms and less likely to be

augmented in times of difficult trading.

The LGS is financed by the Department of Trade and Industry. In its initial form, the

scheme was supposed to be self-financing. The government originally guaranteed

that, in the event of failure of a business, 80 per cent of the loan would be repaid to the

bp 0.01%

balloon loan

Where increasing amounts of

capital are repaid towards the

end of the loan period

bullet loan

Where no capital is repaid

until the very end of the loan

period

CFAI_C15.QXD 10/26/05 11:58 AM Page 384