Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 14 Short-term asset management 355

Customer credit mission and goals for Makebelieve Ltd

Mission: To maintain and protect a portfolio of high-quality accounts receivable and to develop

sound credit policies and administer credit operations in a manner that increases sales, con-

tributes to profits, aids customer loyalty and improves shareholder value.

Goals:

1 To restrict monthly debtors to 45 days.

2 To achieve agreed monthly cash collection targets.

3 To limit overdue debts to 30 per cent of sales.

4 To limit bad debts to 1 per cent of sales.

5 To resolve credit-related customer queries within 3 days.

6 To improve the relationship between the credit function and major customers through

regular contact and visits.

7 To convert 20 per cent of existing customers to direct debit in the year.

4 Efficiency. Information asymmetry exists between buyer and seller. The buyer does

not know whether the product delivered is of the quality ordered until it has been

thoroughly inspected. The credit period therefore provides a valuable inspection

and verification period. Many companies deliver to customers on a daily basis.

Trade credit is therefore a convenient means for separating the delivery of goods

from the payment of deliveries.

The aims of trade credit management are the following:

■ To safeguard the firm’s investment in debtors.

■ To maximise operational cash flows by assessing customer credit risks, agreeing

appropriate terms and collecting payments in accordance with these terms.

The level of debtors in a company will depend on its terms of sale, credit screening,

cash discounts offered and cash collection procedures.

Effective debtor control policy requires careful consideration of the following:

■ Credit period.

■ Credit standards.

■ Cost of cash discounts.

■ Collection policy.

Each of these are discussed in the following section.

While the main responsibility for setting credit policy lies within financial manage-

ment, other functions should be involved, particularly marketing. However, all too often,

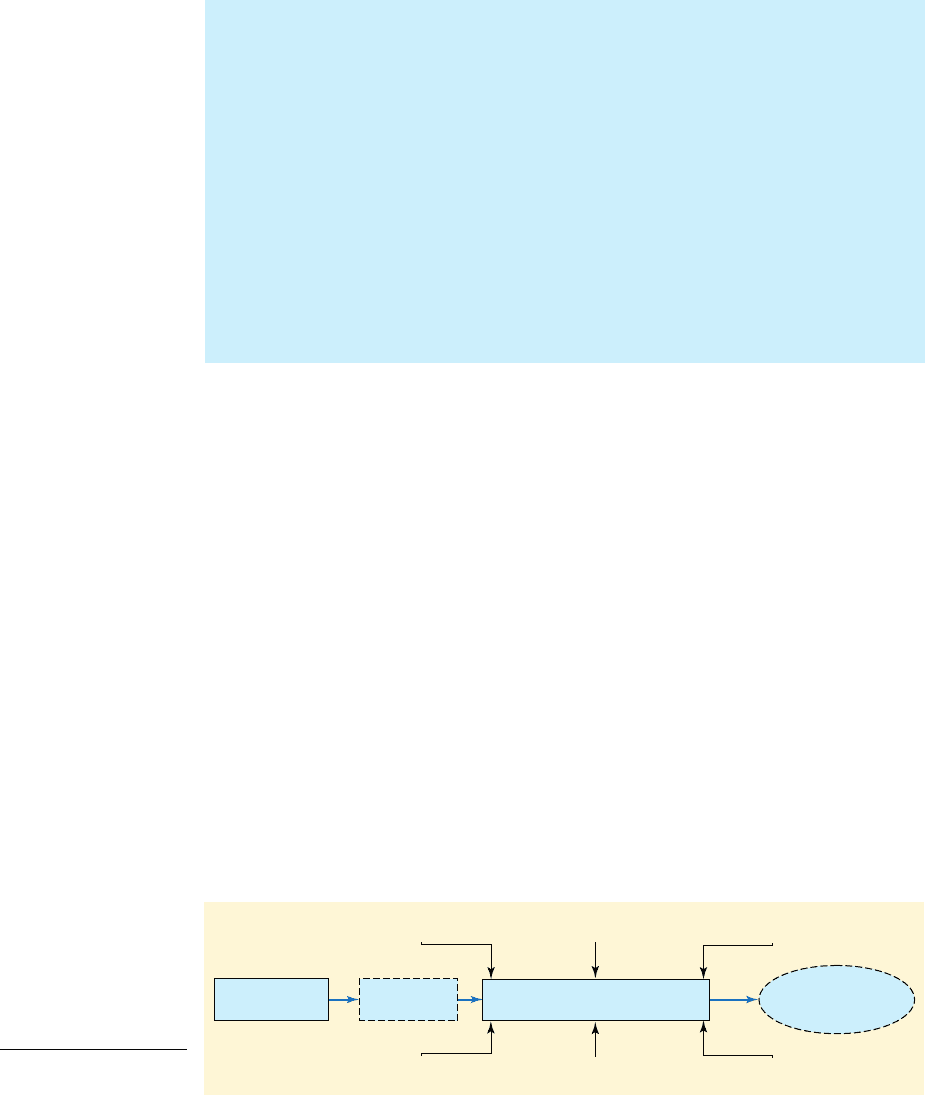

this collaboration is lacking. The credit management process is shown in Figure 14.1.

Reporting

Risk-reduction methods

Credit screening

Credit management

performance

Monitoring receivables

Credit granting

Credit policy

Credit mission

and goal

Cash collection

Credit management process

Figure 14.1

The credit manage-

ment process

CFAI_C14.QXD 3/15/07 7:16 AM Page 355

.

356 Part IV Short-term financing and policies

■ Credit period

The main factors influencing the period of credit granted to customers are:

1 The normal terms of trade for the industry. It is difficult to operate a trade credit poli-

cy where the period offered is considerably below the normal expectation for the

industry unless the company has another clear competitive advantage, such as a

recognised better quality product.

2 The importance of trade credit as a marketing tool. Determining the optimum credit

period requires the finance manager to identify the point where the costs of

increased credit are matched by the profits made on the increased sales generated

by the additional credit. The more vital the perception of credit as a marketing tool,

the longer the likely period of credit offered.

3 The individual credit ratings of customers. Most firms operate regular credit terms for

good-quality customers and specific credit terms for higher-risk customers. The

credit quality of customers is based on the credit standards addressed in the worked

example in Section 14.3.

Credit limits should be set for each customer based on their credit-worthiness. The

firm should consider:

1 Customer payment record: is the customer a prompt payer?

2 Financial signals: is there evidence of the customer running up losses or having liq-

uidity problems?

Very high-risk customers may be reviewed monthly and have to pay, in full or part,

with order. Other customers may be granted credit on the basis of percentage of annu-

al purchases.

credit limits

The maximum amount of

credit that a firm is willing to

extend to a customer

Commonly quoted trade credit terms

■ Cash before delivery (CBD)

■ Cash on delivery (COD)

■ Invoice terms (e.g. 2/10, net 30). A two-stage payment term giving a 2 per cent cash dis-

count for payment within 10 days, otherwise the net amount is due after 30 days.

■ Consignment sales – pay for goods when used or sold.

■ Periodic statement – payment by a specific date for all invoices up to a cut-off date.

■ Seasonal dating – payments due at specific dates to match the buyer’s seasonal income.

■ Credit standards

We have noted that granting trade credit is partly a marketing exercise designed to

increase sales. However, at the individual customer level, it is essentially a credit assess-

ment and control exercise. In this sense, extending trade credit is no different from a

bank granting a loan to a customer. The risk of granting trade credit can be seen when

we consider the effect on profit of customer default. If a company sells a product for

with a 10 per cent net margin, which subsequently becomes a bad debt, the busi-

ness must make ten similar sales to good customers simply to recover the bad

debt incurred.

Credit assessment should involve the following:

1 Prior experience with the particular customer. The credit extended and payment

experience in the past is a useful guide, but it may relate to a time when the cus-

tomer was not experiencing financial difficulty. Even so, it is wise to have more

rigorous procedures for assessing new accounts.

£1,000

£1,000

CFAI_C14.QXD 3/15/07 7:16 AM Page 356

.

Chapter 14 Short-term asset management 357

2 Analysis of the customer’s accounts and credit reports. Profit and Loss Accounts

and Balance Sheets are available from the company’s registered office, but can more

easily be taken from computer databases. Credit reports include:

(a) Bank references

(b) Trade references expressing the views of other businesses trading with the

customer

(c) Credit bureau reports. Credit-reporting agencies (such as Dun & Bradstreet)

provide data and credit ratings that can be used in credit analysis. It is common

practice for firms to offer credit agencies full disclosure of financial and trading

information in order to gain a good rating. From an assessment of the cus-

tomer’s creditworthiness, it is possible to establish appropriate credit rules cov-

ering the terms of sale:

(i) the maximum period of credit granted;

(ii) the maximum amount of credit;

(iii) the payment terms, including any discounts for early payment and

interest charges on overdue accounts.

The businesses most vulnerable to late payment are often those that do least to vet

their customers. According to the Confederation of British Industry, many small firms

fail to chase their late payers with any degree of urgency, partly because their credit

management systems are not good enough to support such activity.

In evaluating customer creditworthiness, it is useful to remember the five Cs of

credit: capacity, character, capital, collateral and conditions.

1 Capacity – does the customer have the capacity to repay the debt within the required

period? This may require examination of the past payment record of the customer.

2 Character – will the customer make a serious effort to repay the debt in accordance

with the terms agreed? Bank and trade references will be useful here.

3 Capital – what is the financial health of the customer? Is the firm profitable and liq-

uid? Is it borrowing beyond its means? Financial accounts and credit agency reports

will help here.

4 Collateral – should some form of security be required in return for extending credit

facilities? Alternatively, should part payment in advance or retention of title be

specified?

5 Conditions – what are the normal terms for the industry? Are our main competitors

offering more generous terms?

■ Cash discounts

The longer a customer’s account remains unpaid, the greater the risk that it will never

be paid. But the cost of financing late payments is often greater than the cost of bad

debts. Surveys suggest that customers, on average, take 30 days’ extra credit beyond

the payment terms.

Cash discounts are financial inducements for customers to pay accounts promptly.

Such discounts can be very costly.

Example: Yorko plc

Yorko plc offers terms of trade which are ‘2/10 net 30’. This means that a 2 per cent dis-

count is offered for all accounts settled within ten days, otherwise payment in full is to be

made in 30 days. A 2 per cent discount may not seem much until one realises that it is given

for a payment in advance of just 20 days (i.e. ). The annualised cost is actually over

37 per cent, calculated by the formula below:

Continued

30 10

CFAI_C14.QXD 3/15/07 7:16 AM Page 357

.

358 Part IV Short-term financing and policies

Self-assessment activity 14.1

A survey of large UK companies (Pike et al., 1998) found that the normal credit period

granted was 30 days, but the average credit period taken by customers was 46 days. Only

20 per cent of firms offered prompt payment cash discounts, with the most common terms

being per cent/net 30 days. For a company offering those terms, what would be the

effective interest rate for granting cash discounts assuming that firms would otherwise pay

within 46 days?

(Answer in Appendix A at the back of the book)

2

1

2

■ Credit collection policy

A good credit collection policy is one in which procedures are clearly defined and cus-

tomers know the rules. Debtors who are experiencing financial difficulties will always

try to delay payment to companies with poor or relaxed collection procedures. The sup-

plier who insists on payment in accordance with agreed terms, and who is prepared to

cut off supplies or take action to recover overdue debts, is most likely to be paid in full

and on time.

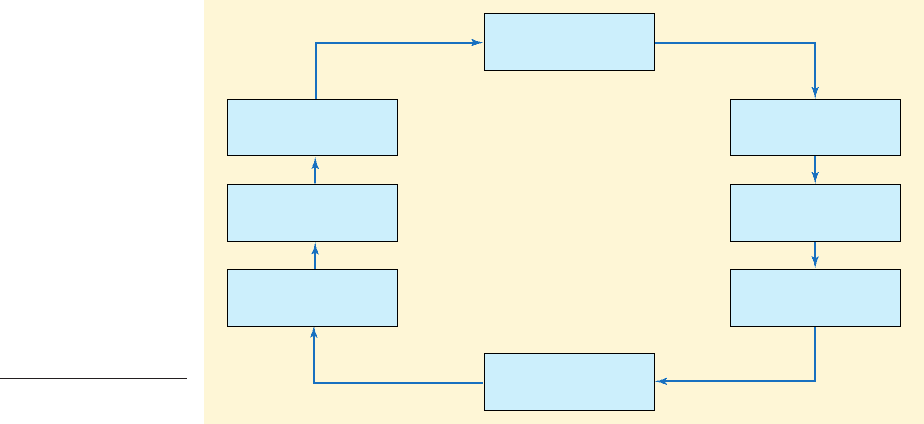

Figure 14.2 shows the debt collection cycle, starting with the customer order and

ending with the cash received. Any speeding up of the order will reduce the required

working capital. Late payment by major customers often has a knock-on effect

throughout the supply chain. For example, if a customer of company A pays its debts

The cost of a discount

In the Yorko example, the annualised cost of forgoing the cash discount is:

A more precise calculation is to find the effective annual rate of return. We have already

calculated for Yorko the two elements:

This expression of the cost is greater than in the first calculation because it assumes com-

pound rather than simple interest which is more accurate.

Where such generous terms are available, it probably makes sense for customers to opt

for the discount even if it means borrowing, as long as the cost of finance is clearly below

the annualised cost of discount. So why should firms offer such inducements? First, early

payment can significantly improve cash flow and reduce bad debt risk. Second, cash dis-

counts can encourage new customers who are attracted by the discounts. However, the

financial manager should be aware of the true cost of such discounts and be able to justify

why terms should be offered costing more than the cost of capital.

Effective annual interest rate 11.02042

18.25

1 44%

Number of 20-day periods a year 365>20 18.25 periods

Cost of discount 2>1100 22 0.0204% per 20-day period

37.23%

0.0204 18.25

Cost

2

1100 22

365

130 102

Cost of cash discount

Discount %

1100 discount %2

365

1Final date discount period2

CFAI_C14.QXD 3/15/07 7:16 AM Page 358

.

Chapter 14 Short-term asset management 359

60 days late, this may force Company A to pay its bills late to Company B, which might

create sufficient cash flow pressures for B to go out of business.

It is a sad fact that firms usually only run out of cash once. Second chances are rare

when it comes to cash failure. So getting on top of the credit screening and control

process is vital. Smaller businesses often complain that some larger companies take an

unduly long time to settle their accounts. There is a real problem in British industry

that far too much time and energy has to be devoted to chasing debts, for no apparent

net gain to the business community. The CBI has introduced a Code of Practice, Prompt

Payers – In Good Company, where firms agree to pay within the agreed payment terms.

Businesses have a statutory right to charge larger customers interest on overdue

accounts. The interest rate is set high (currently, Bank of England base rate )

because most firms must finance late payment from bank overdrafts.

CBI prompt payment code

This states that a responsible company should:

■ Have a clear, consistent policy of paying bills in accordance with contract.

■ Ensure that the finance and purchasing departments are both aware of this policy

and adhere to it.

■ Agree payment terms at the outset of a deal and stick to them.

■ Not extend or alter payment terms without prior agreement.

■ Provide suppliers with clear guidance on payment procedures.

■ Ensure that there is a system for dealing quickly with complaints and disputes, and

advise suppliers without delay when invoices are contested.

The CBI has joined forces with other interested parties (e.g. the DTI, the British Chambers

of Commerce, the British Bankers Association, the Institute of Credit Management) to

form the Better Payment Practice Group, which provides a set of best practice guidelines

for both buyers and sellers. Its website (www.payontime.co.uk) gives a listing of the aver-

age payment times of public companies to enable small suppliers, in particular, to moni-

tor and compare the payment practices of these firms. Most listed firms state their

payment policy in their annual reports.

For example, Corus plc, the steel-making firm, declares its policy as to ‘establish

payment terms with suppliers when agreeing transactions, and to despatch cheques

by the due date.’ In 2003, it made purchases of million, and its accounts showed

trade creditors of million at year-end, down from million in 2002. This£1,047£986

£7,253

8%

Customer

receives invoice

Cash received

Reminder

Credit screening

and terms agreed

Goods delivered

Invoice raised

Customer receives

statement

Customer

places order

Figure 14.2

Ordering and debt

collection cycle

CFAI_C14.QXD 3/15/07 7:16 AM Page 359

.

360 Part IV Short-term financing and policies

implied an average payment period on credit purchases of 51 days. Corus claimed to

have nil days purchases outstanding (i.e. in arrears) ‘based on the average daily

amount invoiced by suppliers during the year’.

■ Using debtors as security

The financing of trade debtors may involve either the assignment of debts (invoice dis-

counting) or the selling of debts (factoring). With invoice discounting, the risk of default

on the trade debtors pledged remains with the borrower. Factoring, on the other hand,

can be and usually is ‘without recourse’, i.e. the factor bears the loss in the event of a bad

debt. Factors provide a wide range of services, the most common of which are as follows:

1 Advancing cash against invoices. Up to 80 per cent of the value of invoices can typ-

ically be obtained; repayments (together with interest on the advances) are paid

from the subsequent cash collected from debtors.

The subtle art of getting paid: late payment

Some small businesses develop creative ways to pursue customers who are paying their bills

late.

An antique fireplace shop in north London until recently kept on call a 6ft 3in ex-con

who had two fingers missing on his left hand and halitosis. His job was simple: to persuade

defaulting customers to pay up by going to their workplace and sitting quietly, but

unpleasantly, in the lobby. He seldom had to stay long before the promised cheque

appeared.

Another small businessman, this time in advertising, was owed money by a smart furniture shop.

He took the afternoon off to stand in the customer’s doorway telling people coming in that they

would be ripped off. He had his cheque within an hour.

Neither approach would feature in a business school textbook on credit management, but

both were effective. One spent money on paying someone to chase the debt, the other judged it

an effective use of his time to do it himself. Both related to a simple business problem: staying

afloat when customers delay paying invoices as long as possible.

Each year, 10,000 UK businesses fail because their invoices are paid late, according to Dun &

Bradstreet, the credit management consultancy. Out of billion owed to UK small businesses

last year, billion was paid after the due date.Yet few small businesses make use of legislation

that penalises late payers, and most believe the law can be of little help when withholding payment

appears to be becoming the norm. As an economic downturn approaches the situation is bound to

deteriorate.

To address this, the Late Payment of Commercial Debts (Interest) Act 1998 allows creditors to add

interest to unpaid invoices without having to go to court. A European Community directive, for which

the UK consultation period ends on Friday, would allow companies to claim compensation as well as

interest from late paying customers.

Trade credit is a loan to your customer, yet customer/supplier contracts can be surprisingly

vague on the terms of payment. There are three steps to managing trade credit:

■ Sell the payment terms at the same time as you sell the product, agree those terms and get

to know the person who actually signs the cheque.

■ Eliminate ‘own goals’ such as delivering the product late or sending an invoice that does not

match the delivery note.

■ Be prepared to ask for the money you are owed. Big companies, which are organised, will

introduce interest on overdue accounts automatically. Small companies will not have the

resources to chase up interest payments.

Source: Based on article in Financial Times, 26 April 2001.

£6.8

£17

CFAI_C14.QXD 3/15/07 7:16 AM Page 360

.

Chapter 14 Short-term asset management 361

Self-assessment activity 14.2

What are the main elements in a firm’s credit policy?

(Answer in Appendix A at the back of the book)

14.3 WORKED EXAMPLE: PICKLES LTD

Pickles Ltd produces a single product sold throughout the UK. Its profit analysis is

given below:

Per unit

Selling price 40

Variable costs (36)

Fixed cost apportionment (3) (39)

Net profit per unit 1

££

£000

New business 1,200

New debtors 300

Additional stocks 400

Additional creditors (200)

Required increase in working capital 500

Increase in operating profit 120

Less financing cost (50)

Net profit increase 70

1£500,000 10%2

1£1.2 m 10%2

1£1.2 m 3>122

1£4.8 m 25%2

2 Insurance against bad debts.

3 Administration of the credit control functions. This involves sending out invoices,

maintaining the sales ledger and collecting payments.

We return to this topic in Chapter 15.

Pickles has an annual turnover of million and an average collection period for

debtors of one month. It has conducted a study on entering new European markets

and believes that this would produce an additional 25 per cent of sales, but the new

business would require three months’ credit. Stocks and creditors would rise by

and respectively. The cost of financing any increase in working cap-

ital is 10 per cent.

Operating profit before finance costs increases as a result of the new business by

Sales increase

Contribution/sales ratio

Increase in

The question of whether profits increase as a result of the expansion into European

markets very much rests on whether the existing UK customers also demand more

favourable terms.

1 Assuming only new customers take three months’ credit

profit £120,000

140 362>40 10%

125% £4.8 m2 £1.2 m

£120,000:

£200,000£400,000

£4.8

CFAI_C14.QXD 3/15/07 7:16 AM Page 361

.

362 Part IV Short-term financing and policies

£000

Sales 6,000

New debtors level 1,500

Less existing debtors (400)

1,100

Additional stocks 400

Additional creditors (200)

Additional working capital 1,300

Operating profit increase (as above) 120

Less financing cost (130)

Net profit reduction after financing costs (10)

110% £1.3 m2

11>12 £4.8 m2

13>12 £6 m2

1£4.8 m £1.2 m2

Thus net profits increase by But what happens if existing customers

demand the same credit terms?

2 Assuming existing customers take three months’ credit

£70,000.

14.4 INVENTORY MANAGEMENT

Inventory, or stock, may be classified into the following:

1 Pre-production inventory – stocks of raw materials and bought-in parts.

2 In-process inventory – work-in-progress at various stages of the production process.

3 Finished goods inventory – manufactured goods ready for sale.

In most cases, finished goods will convert most rapidly into cash; but where cus-

tomer tastes change rapidly, such as in the fashion trade, this stock can also be the most

risky.

Inventory is the least liquid of current assets. It is therefore vital to manage it in such

a way that it can be converted from raw material to work-in-progress and finished

goods as quickly as possible.

Stock is carried for two reasons:

1 Business is uncertain. Consumer demand and production requirements are difficult

to forecast, and suppliers may not always be reliable in meeting delivery require-

ments. The cost of being out-of-stock, in terms of lost sales, profits and goodwill, is

generally very high.

2 Economies in ordering. Every business needs to determine its economic order quan-

tity for its main stock items.

Inventory control is an important topic for both production management and finan-

cial management, which should work closely to establish an inventory policy that

meets customers’ requirements while operating at optimum stock levels. It should

avoid the twin evils of overstocking and understocking.

Overstocking results in the following:

■ An unduly high level of working capital investment.

■ Additional storage space requirements and greater handling and insurance costs.

■ Possible deterioration and increased obsolescence risk.

Understocking reduces the working capital required, but can lead to out-of-stock situ-

ations (‘stockouts’) with orders unfulfilled, idle machines and underemployed workers.

After charging the cost of finance on additional debtors, stocks and creditors, the

extra business does not increase profits.

CFAI_C14.QXD 3/15/07 7:16 AM Page 362

.

Chapter 14 Short-term asset management 363

In the past, carrying higher than necessary stocks has been a way of compensat-

ing for inefficient production and distribution or poor forecasting. But in today’s

highly competitive global markets, with Japanese and other overseas businesses

operating efficient production schedules and minimal stock levels, European com-

panies have been forced to examine their inventory management processes more

closely.

■ Approaches to inventory management

There is now a whole variety of methods for improving stock control, some simple, oth-

ers more sophisticated, using computer software. We will limit our discussion to three

forms of stock control:

1 ‘Broad-brush’ approaches.

2 Economic order quantity models.

3 Computer-based material requirements and just-in-time methods.

Broad-brush approaches

A simple, but useful, starting point is to consider the total stock position using the num-

ber of days’ stock ratio:

Consider the stock levels of two companies, based on latest accounts (Table 14.1)

U-Save, a discount supermarket chain, carries only finished stocks. Its generic strategy –

to be the lowest-cost grocery retailer – requires tight control over its ordering, deliver-

ies and stocks. Its stockholding period is 22 days, which means that stock will proba-

bly be turned into cash before the invoice for the goods is paid. By contrast, a major

diversified producer like Unicom has very significant raw material stocks and a stock-

holding period which is double that of U-Save.

While such cross-industry comparisons are interesting, U-Save will want to com-

pare its stockholding period against Tesco and other competitors to see whether it is

more efficient in its inventory control processes.

Major companies may well have thousands of items in stock. How should they

determine the appropriate level of inventory control for each item? A simple stock

classification, often called the ABC system, can help identify how closely stock items

should be controlled. It divides a company’s inventory into three groups according to

importance to sales value, with high-value stocks requiring the highest stock control

attention.

ABC stock classification in Boris plc

An analysis of stock items in Boris plc revealed the following:

Number of days’ stock

Average stock

Cost of sales

365

Table 14.1

Total inventory levels

and stockholding

periods

U-Save (£m) Unicom (£m)

Raw materials — 1,380

Work-in-progress — 175

Finished goods 148 1,894

Total stock 148 3,449

Cost of sales 2,403 25,926

Days’ stock 22.5 48.5

ABC system

A system of stock manage-

ment that prioritises items

accounting for greatest stock

value

CFAI_C14.QXD 3/15/07 7:16 AM Page 363

.

364 Part IV Short-term financing and policies

Short-term financing and policies

Category Stock items (%) Stock value (%)

A12 72

B38 18

C50 10

100 100

Category A stock items have only 12 per cent of the total number of items in stock,

but account for 72 per cent of stock value. It was decided that these items required a

considerable degree of stock control attention, regular forecasting and monitoring,

carefully assessed economic order quantities and an appropriate level of buffer stocks.

Category B stock items cover 38 per cent of total items, but only 18 per cent of stock

value. The inventory policy for these items would be less sophisticated; forecasting

would be simpler and less frequent.

Category C, which covers half the stock items but only 10 per cent of stock value,

requires much simpler treatment, with few stock records and less regular monitoring.

For example, stocks of nuts and bolts might simply require that an ample supply is

always on hand.

Economic order quantity models

The costs of holding high levels of stocks include the interest lost in tying up capital in

such assets, the costs of storing, insuring, managing and protecting stock from pilfer-

age, deterioration, etc., and obsolescence costs. Against this, there are costs involved in

holding low levels of stock or running out of stock:

1 Loss of goodwill from failure to deliver by the date specified by customers.

2 Lost production and disruption due to essential items being unavailable.

3 More frequent re-order costs (buyer’s and storekeeper’s time, telephone, postage,

invoice-processing costs, etc.).

A variety of stock management models have been developed to help managers

determine the optimal level of stock that balances holding costs against shortage costs.

One way of addressing the issue is to determine the economic order quantity (EOQ)

for the stock required.

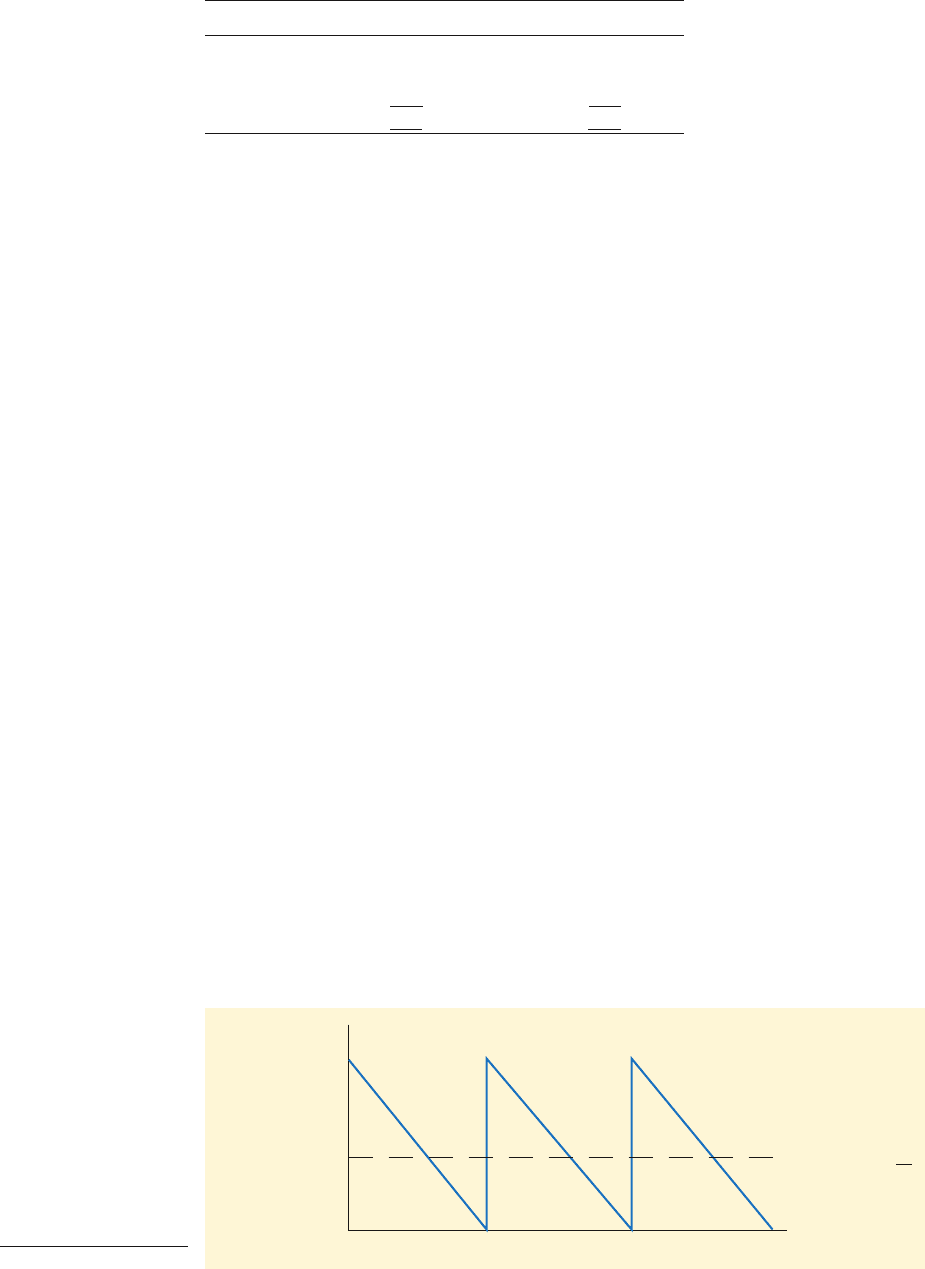

Every firm should operate a clear stock control policy, which specifies for its main

items the timing of stock replenishments, re-order quantities, safety stock levels and

the implications of being out of stock. Figure 14.3 depicts the inventory cycle for a sim-

ple stock control model. It assumes a single product, immediate stock replenishment,

constant usage and certainty.

Average stock =

Q

Time0

Order quantity,

Q

2

Figure 14.3

The inventory cycle

CFAI_C14.QXD 3/15/07 7:16 AM Page 364