Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 15 Short- and medium-term finance 385

financial institution making the loan. The cost of meeting guarantees would be met by

borrowers paying to the government a premium of three percentage points above the

normal commercial rate applied by the bank. Loans were available for periods of two

to seven years. Losses on the scheme turned out much higher than anticipated, large-

ly, it was alleged, because banks contrived to shift existing shaky clients on to it. After

many modifications over the years, it now embodies the following features:

■ Firms apply for loans directly to banks and other lenders.

■ Applicants must demonstrate that they have applied for a conventional loan and

have been rejected for lack of security.

■ Only firms with less than 200 employees and annual turnovers no more than mil-

lion ( million for manufacturers) are eligible.

■ 75% per cent of the loan is guaranteed.

■ Loans are available for amounts between and (or for a firm

trading for two years already).

■ Borrowers pay a ‘normal commercial’ interest rate to the bank, plus a premium of

2.0 per cent p.a. on the outstanding amount of the loan.

■ Term of loan available from two to 10 years.

For updates on the LGS, see www.bba.org.uk and www.dti.gov.uk.

£250,000£100,000£5,000

£5

£3

15.4 INVOICE FINANCE

Some companies, which need to offer trade credit to customers for competitive reasons,

find that they need payment earlier than agreed in order to assist their own cash flow.

Institutions called factors, mainly subsidiaries of the major banks and members of the

Factors and Discounters Association (www.factors.org.uk), exist to help such compa-

nies. Factors do not always provide new finance, but can accelerate the cash conversion

cycle for client companies, allowing them to gain access to debtors more quickly than

if they waited for the normal trade credit period to unwind. The essence of both fac-

toring and invoice discounting is to use debtors (i.e. invoices) to provide security for

financing, hence the term ‘invoice finance’. Invoice finance thus includes both factoring

proper and invoice discounting.

Between 1993 and 2004, total invoice financing, measured by FDA clients’ turnover,

grew from £19 billion to £132 billion, 85 per cent of which was invoice discounting. In

2004, invoice discounting itself grew by 16 per cent from £97.5 billion to £113 billion.

■ Factoring

Factoring involves raising immediate cash based on the security of the company’s

debtors, thus accelerating payment from customers. A factor provides three main

services – sales administration, credit protection and provision of finance, commonly

80–85% of the value of approved invoices.

Sales administration

A factor assumes the various functions of sales ledger administration, ranging from

recording sales details to sending out invoices and reminders and collecting payment.

The benefits for the client are the cost savings from reducing in-house administration

and access to a more efficient, specialist debtor management team. This is particularly

valuable to a young fast-growing company, which may outgrow its administration

system and otherwise be exposed to the liquidity risks of overtrading. The fee for such

an administration service would lie typically in the range of 0.75–2.5 per cent of the

value of turnover handled, depending on whether credit protection against bad debt

losses is included.

factors

Organisations that offer

to purchase a firm’s debtors

for cash

CFAI_C15.QXD 10/26/05 11:58 AM Page 385

.

386 Part IV Short-term financing and policies

Credit protection

The factor may provide a credit evaluation service for clients, analysing customer char-

acteristics before deciding on their creditworthiness. When all risks are borne by the

factor, the service is termed ‘without recourse’, i.e. the factor has no ‘comeback’ on the

client if customers default. Where this applies, the factor requires total control of cred-

it approval, monitors customers’ payments and attempts to collect payment. This sug-

gests a possible problem with factoring – the intervention of the factor between the

factor’s client and the debtor company could endanger trading relationships and dam-

age goodwill. For this reason, some clients prefer to retain responsibility for collection

of problem debtors. This is known as ‘undisclosed factoring’. (In the case of ‘with

recourse’ factoring, the factor will call upon its client to reimburse the funds advanced

on an invoice relating to a delinquent account.)

Provision of finance

A factor will also advance funds to a client, based on a proportion, say 80 per cent, of

approved (i.e. reliable) invoices. For example, a company with sales on 30 day credit

terms from reliable customers of £500,000 per month would receive an advance of 80

per cent, i.e. £400,000 each month. The interest rate would be related to bank base rate,

probably slightly above the cost of an overdraft. The client would receive the balance

of the payment less interest and an administration charge, perhaps equal to 0.5 per cent

of turnover.

Although factors provide valuable services, companies are sometimes wary of

using them for reasons other than cost. Besides possible difficulties over collection

of payment, widespread knowledge that a company is using a factor may arouse

fears that the company is beset by cash flow problems. If so, its suppliers may impose

more stringent payment terms, thus negating the benefits provided by the factor.

Companies concerned by these risks may seek the more widely used but less compre-

hensive service of invoice discounting.

invoice discounting

Where a factor purchases

selected invoices from client

firm, without providing debt

collection or account adminis-

tration services

Self-assessment activity 15.5

Summarise the benefits of factoring for a small firm.

(Answer in Appendix A at the back of the book)

■ Invoice discounting

Although factors provide a range of services, a company seeking merely to improve its

cash flow is likely to use an invoice discounting facility. This involves the purchase of

selected invoices, sometimes just one, by the discounter. The discounter will advance

immediate cash up to 85 per cent of face value. It assumes no responsibility for the

administration of the accounts receivable, or the collection of the debts. The service is

totally confidential, the client’s debtors being unaware of the existence of the dis-

counter. It is therefore equivalent to the financing service provided by a factor, although

restricted to a narrower range of invoices. Invoice discounting business amounted to

over £67 billion in 2001.

Administration charges for this service are around 0.5 per cent of a client’s turnover.

It is more risky than factoring, since the client retains control of its credit policy.

Consequently, such facilities are usually confined to established companies with

turnovers above £1 million. Interest costs are usually 3–6 per cent above base rate,

although larger companies and those that arrange credit insurance may receive keen-

er terms.

CFAI_C15.QXD 10/26/05 11:58 AM Page 386

.

Chapter 15 Short- and medium-term finance 387

To view the offerings of a typical factor, visit the website of RBS Commercial Services

Ltd, a subsidiary of the Royal Bank of Scotland (www.rbcs.co.org).

15.5 USING THE MONEY MARKET: BILL FINANCE

A bill is often likened to a post-dated cheque or an IOU, as it represents a commitment

to pay out a specific sum of money after a specified period of time. Bills are traded on

the money market, which specialises in providing funds repayable over periods of less

than a year. The major players in the money market are the commercial banks, which

lend to each other, often overnight, to cover temporary cash shortages, at the London

Inter-Bank Offered Rate (LIBOR), and to the discount houses. The latter exist primarily

to deal in short-term bills issued by the government (Treasury Bills), local governments

and companies. They borrow on a very short-term basis from the commercial banks,

usually at a very keen interest rate, and use the proceeds to purchase bills, which they

may hold to maturity or sell at a profit in the money market.

A company can use two main types of bill to raise finance: a trade bill (Bill of

Exchange) or a bank bill (acceptance credit).

■ Bills of exchange

Bills of Exchange are generally trade-related, connected to specific trading transactions.

The trader purchasing goods draws up a bill stating a promise to repay at some future

date, and then conveys the bill to the supplier of the goods.

How invoice discounting works

At the beginning of February, Menston, plc sells goods for a total value of £300,000 to regu-

lar customers, but decides that it requires payment earlier than the agreed 30 day credit peri-

od for these invoices. A discounter agrees to finance 80 per cent of their face value, i.e.

£240,000. Interest is set at 13 per cent p.a. The invoices were due for payment in early March,

but were subsequently settled in mid-March, exactly 45 days after the initial transactions. The

service charge is set at 1 per cent. As usually applies, a special account is set up with a bank,

into which all payments are made. The sequence of cash flows is as follows:

February:

Menston receives cash advance of £240,000

Mid-March:

Customers pay up 300,000

Invoice discounter receives the full £300,000

Menston receives the balance less charges, i.e.

In effect, Menston has settled for a discount of per cent over 45 days

for early receipt of 80 per cent of the accounts payable. As there are about eight 45 day peri-

ods in a year, this corresponds to an annual interest rate of:

11.023

8

12 0.1995, i.e. 19.95%

£6,847>£300,000 2.3

Total receipts by Menston 1£240,000 £53,1532 £293,153

1£60,000 £6,8472 £53,153

Net receipts 120% £300,0002 £6,847

Total charges £6,847

Interest 113% £240,000 45>3652 £3,847

Service fee 1% £300,000 £3,000

CFAI_C15.QXD 10/26/05 11:58 AM Page 387

.

388 Part IV Short-term financing and policies

The supplier may then hold the bill until maturity or sell it in the market to a dis-

count house, if cash is required earlier. The terms of the bill usually include an

implicit interest charge, although no interest as such is paid, as the following exam-

ple indicates.

A trader wishes to acquire goods to the value of £1 million. He draws up a Bill of

Exchange, promising to pay £1 million in three months’ time. The bill is immediately

sold by the seller of the goods to a discount house, which pays out £975,000, i.e. a dis-

count of £25,000. If the discount house holds the bill to its maturity, it earns a profit of

£25,000. This is equivalent to an interest rate of over three

months, or in annual terms:

If the discount house can borrow at less than this rate, it stands to make a profit. If

interest rates fall, the discount house’s profit margin widens. Alternatively, the dis-

count house may sell the bill on the money market, its value rising as it nears maturi-

ty. The ultimate holder will present the bill to the trader, who assumes responsibility

for payment and, by this time, hopes to have sold the goods at a profit.

Bills of Exchange are drawn up for periods of 60–180 days, for values of at least

£75,000, reflecting interest rates based on LIBOR, but dependent on the riskiness of the

companies concerned and their respective credit ratings.

■ Acceptance credits

These are often called ‘bank bills’ – whereas trade Bills of Exchange are drawn on

the purchaser of goods by a supplier, an acceptance credit is drawn by a company

on a bank. Acceptance credits were originally developed by merchant banks, but all

large banks now offer this facility. The bank grants a credit facility whereby a client

company can draw bills (up to an agreed limit) that the bank will accept, i.e. agree

to honour, when presented for payment at a future specified date. The client com-

pany may not use the facility immediately, but may treat it as a standby to be used

when required, usually in minimum tranches of £250,000, over a period of up to

five years. Accepted bills are sold on the discount market by the bank on behalf of

the client company at a relatively ‘fine’, or low, discount. The company thus effec-

tively obtains finance from the purchaser of the discounted bills, using the name

and reputation of the accepting bank as security. It is thus a somewhat roundabout

way of one company lending to another, using the intermediary services of the

bank. Bank bills have a period to maturity of 30, 60, 90 or 180 days. At the maturi-

ty date, the bank can either ‘accept’ a new bill (i.e. effectively roll over the old one)

or receive the full value of the bill from the client’s account, using the funds to pay

the bearer of the bill. The cost to the client is the amount of discount on the bill plus

a fee payable to the bank of around 0.6 per cent. It is not unusual for banks to

require security for such facilities – the nature and type depending on the size and

credit standing of the client.

Acceptance credits have become increasingly popular in recent years. Among their

advantages are the following:

1 The ‘interest’ cost is relatively low, often below that of an overdraft, because the bills

are backed by a bank.

2 The cost involved with the bill is known when it is discounted, and is not affected

by subsequent interest rate changes, allowing greater accuracy in cash budgeting.

3 Acceptance credits can be negotiated for longer periods than overdrafts, thus offer-

ing more security to the borrower.

4 Unlike traditional bills of exchange, they are not tied to specific transactions.

11.02562

4

1 11.1064 12 0.1064, i.e. 10.64%

1£25,000>£975,0002 2.56%

CFAI_C15.QXD 10/26/05 11:58 AM Page 388

.

Chapter 15 Short- and medium-term finance 389

However, they are available only to large companies with sound credit ratings, and

they lack the flexibility of overdrafts, which a firm can reduce if it wishes to lower

interest costs.

■ Commercial paper (CP)

Another financial innovation imported from the USA that UK firms have been allowed

to use since 1986, CP is a means whereby the treasurer can circumvent the banking sys-

tem by issuing promissory notes – effectively IOUs – directly to large financial institu-

tions such as pension funds and insurance companies, or to corporates with temporary

excess liquidity.

CP is an example of disintermediation as it cuts out the banking intermediary as

middleman and thus avoids paying the spread on the difference between the bank’s

lending rate and the rate it pays depositors, i.e. it is cheaper. In addition, CP avoids

having to submit to the restrictive covenants that banks often impose on borrowers.

However, because it is unsecured, the ability to issue CP is confined to the largest firms

with the highest credit ratings, i.e. ‘blue chips’.

Specifically, to be allowed to issue CP, a firm must:

■ be listed on the London Stock Exchange

■ have net assets in excess of £50 million

■ issue CP that matures between 7 and 364 days (2–270 in the USA)

■ issue CP with a minimum denomination of £500,000.

Interest is not usually payable on CP – it has a maturity value greater than the amount lent,

the difference being the cost to the issuer. There is virtually no secondary market in CP.

disintermediation

Business-to-business lending

that eliminates the banking

intermediary

15.6 HIRE PURCHASE (HP)

With HP (also known as Asset Purchase), the user of the asset will eventually own it.

Small and medium-sized firms (SMEs) are particularly reliant on HP, which, although

often an expensive option, is readily available because the loan is secured on the asset

acquired. In 2003, HP together with leasing (see Section 15.7) accounted for 25 per cent

of all external finance for SMEs. HP of equipment by firms is very similar to HP by

consumers of durables such as washing machines. The equipment is purchased ini-

tially by specialist institutions called finance houses, most of which are subsidiaries

of commercial banks and members of the Finance and Leasing Association (FLA,

www.fla.org.uk). The hirer usually makes a down payment and then signs a commit-

ment to a series of (usually) monthly hire charges over a specified period, at the end

of which the legal title to the article passes to the user. The hire charge contains two

elements: an interest charge to reflect the borrowing of the capital involved; and a cap-

ital repayment element.

Two major advantages of HP are the avoidance of a major cash outlay at the outset

of the project and the immediate availability of the asset for use, although the user

assumes all the responsibilities of maintenance and insurance. However, if the user

fails to fulfil the payment schedule, the owner can repossess the asset. The user then

loses all title to the asset and obtains no credit for payments already made. HP tends

to be used by smaller and riskier firms. Because of the default risk, the contract peri-

od is invariably less than the asset lifespan, so that in the event of repossession, the

owner knows that it will hold a saleable asset with some working life remaining.

Conversely, over longer-term HP contracts, the owner is exposed to the risk of tech-

nological progress outdating the asset and reducing its marketability. As a result of

these considerations, HP is expensive.

CFAI_C15.QXD 10/26/05 11:58 AM Page 389

.

390 Part IV Short-term financing and policies

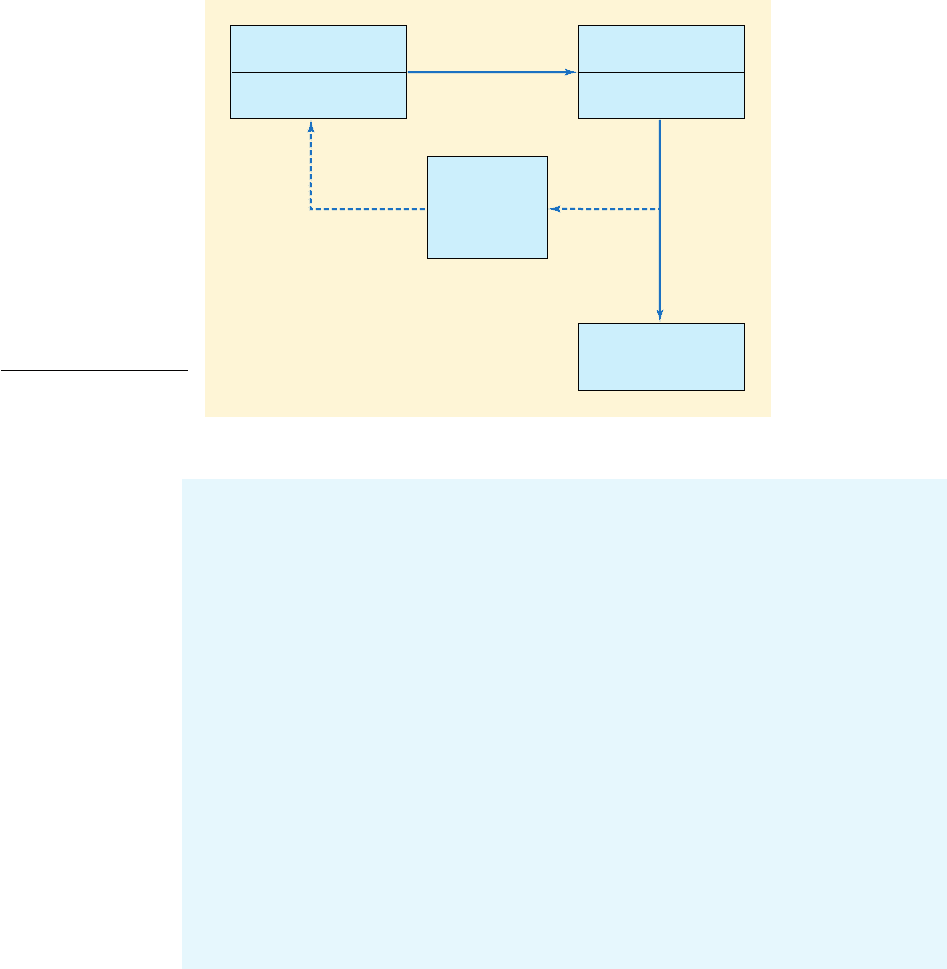

Asset

repossessed

if user

defaults

transfers

asset

to

user

Becomes the owner

when final payment

is made

User firm

contracts to make

a series of payments

Finance house

(HP company)

buys equipment

Figure 15.1

How hire purchase

works

An advantage of HP is that the user qualifies for tax relief on the interest element in

the repayment profile and also a writing-down allowance (WDA) on the capital

expenditure component (25 per cent reducing balance), based on the total cash price

of the asset. Table 15.1 shows the profile of tax reliefs for the Boston Builder’s exam-

ple, assuming tax is paid at 30 per cent, with no delay, and that the asset has a sale

value of £20,000 after four years, i.e. tax allowable depreciation is £100,000 over the

four-year lifespan of the asset.

Tax relief is of value only to profitable companies with taxable capacity. Many of the

smaller and higher-risk companies (often start-ups) that use HP are unable to exploit

the tax breaks, often making HP a very expensive form of finance.

How HP works

Boston Builders, wishing to obtain an earthmover using HP, contacts a manufacturer, which

arranges an HP contract with a finance house. The finance house buys the asset, which has

an expected useful life of four years, for £120,000 and arranges the following contract:

■ The asset will be purchased over three years but operated for four years.

■ A down payment of £20,000 is required.

■ Interest is charged at 15 per cent on the initial loan of

■ Capital will be repaid in three equal instalments.

Note that, even though the balance outstanding declines over the three-year period, inter-

est is applied to the initial loan of £100,000. The annual payments are thus:

Because the interest is paid in this way, the true interest rate is roughly double the quoted

rate. The annual interest charge of £15,000, applied to the average capital outstanding of

£50,000, yields an effective interest rate of per cent, although the

precise rate depends on the actual timing of payments.

1£15,000>£50,0002 30

Total £48,333 p.a. 1or £4,028 if paid monthly2

Capital˛˛ £100,000>3 £33,333 p.a.

Interest 115% £100,0002 £15,000 p.a.

£100,000.1£120,000 £20,0002

CFAI_C15.QXD 10/26/05 11:58 AM Page 390

.

Chapter 15 Short- and medium-term finance 391

15.7 LEASING

Self-assessment activity 15.6

What is the monthly payment on the following HP contract?

■ Total cost of

■

■

Interest

■ Hire

(Answer in Appendix A at the back of the book)

period 4 years

rate 10%

Down payment 30%

equipment £40,000

Table 15.1

Tax relief on 3-year HP

contract with 4-year

asset lifetime (£)

Year Interest WDA Total tax reliefs Tax saving @ 30%

1 15,000 30,000 45,000 13,500

2 15,000 22,500 37,500 11,250

3 15,000 16,875 31,875 9,562

4 – 30,625* 30,625 9,188

Totals 45,000 100,000 145,000 43,500

*Note: Year 4 allowable depreciation [Outlay less depreciation claimed for years 1–3 less

sale value]

£30,625

£120,000 £30,000 £22,500 £16,875 £20,000

Leasing resembles both HP and conventional borrowing, but deserves separate and

extensive analysis for two reasons. First, it is highly significant as a means of financing

fixed capital investment, having grown substantially since the 1970s. By 2003, over £25

billion in lease finance was provided to the UK business sector and UK public services,

accounting for over 25 per cent of all fixed capital investment (excluding property).

Second, it provides an example of the interaction between investment and financ-

ing decisions, and an opportunity to show how DCF principles can be applied to

financing as well as investment decisions.

■ What is leasing?

According to the International Accounting Standards Board:

A leasing transaction is a commercial arrangement whereby an equipment owner con-

veys the right to use the equipment in return for payment by the equipment user of a

specified rental over a pre-agreed period of time.

Thus, leasing is a way for companies to obtain the use of equipment when, for

varying reasons, they may wish to avoid acquiring it outright using other financing

methods. Leasing is a distinctive method of finance because it involves important

interactions between the investment and financing decisions.

■ How a lease works

Most leasing activity is undertaken by banking and similar institutions, such as HSBC

Equipment Finance (UK) Ltd. In addition, some manufacturers, such as IBM and John

CFAI_C15.QXD 10/26/05 11:58 AM Page 391

.

Deere, operate leasing companies to market their own products. A company wishing to

obtain the use of an asset (the lessee), such as an oil company wishing to lease a tanker,

or a Development Corporation wishing to lease property, will approach the leasing spe-

cialist (the lessor) with its requirements. The deal will involve the lessor purchasing the

tanker, or the site, and renting it to the lessee in return for a specified series of rental

payments over an agreed time period.

■ Types of lease

Where the agreed term of the lease approximates to the expected lifetime of the asset, the

lessee is clearly using the lease arrangement as an alternative form of finance to outright

acquisition. As a result, it avoids having to incur the perhaps substantial cash outlay

required at the outset of the project. Hence this type of lease is called a finance lease,

(or a capital lease or a full payout lease).

In the UK, it is important that the asset remains the legal property of the lessor, oth-

erwise certain tax advantages may be lost. At the expiration of the lease contract, the

two parties may negotiate a secondary lease, or the owner may otherwise dispose of

the asset. For assets with long lives, the lessor may ignore the potential resale value of

the asset when setting the rentals, since it is too distant in time to predict accurately.

Instead, the lessor may agree to reimburse the lessee with a proportion, often over

90 per cent (but never 100 per cent) of the resale value, an agreement known as a

rebate clause. Rebates are taxable in the hands of the lessee. Secondary leases are often

undertaken at nominal or ‘peppercorn’ rentals to reflect their bonus nature – the

owner will already have received back its outlay plus target profit once the contract

has reached its full term.

However, not all forms of lease operate over long time periods. The user may not

wish to incur the long-term contractual liability to pay rentals, especially if it wishes to

obtain the use of the asset only to perform a specific job, e.g. drilling equipment to bore

out a specific oil well. Lessors are willing to rent equipment to such firms on the basis

of an operating lease. This is usually job-specific and can be cancelled easily, whereas

cancellation of a finance lease usually involves financial penalties so severe that termi-

nation is rarely worthwhile. The lessor will hope to arrange a series of such contracts in

order to recover its capital outlay and achieve a profit. For this reason, the operating

lease is called a part payout lease. Unlike the finance lease, where the user bears the full

risks both of ‘downtime’ (inability to use the asset) and obsolescence, in an operating

lease, the owner incurs the brunt of these risks. To compensate for the risk of having a

yard full of idle and rusting equipment, the lessor will apply a rental that is higher per

unit of time than that for a financial lease, thus incorporating a risk premium.

Operating leases have another advantage for lessees. They are usually negotiated

on a ‘maintenance and insurance’ basis, whereby the owner undertakes to insure and

service the asset. This is normally the responsibility of the user in the case of the

finance lease, although the owner may actually perform the servicing functions for a

fee. The suitability of the operating lease for short-term projects explains its populari-

ty in the construction industry under the guise of plant hire, and for assets with a rapid

rate of technological advance such as photocopiers and computers. To compensate for

the risks of leasing out high-technology assets, lessors are sometimes able to protect

themselves by using specialist computer leasing insurers, although premium rates are

generally high.

■ The characteristics of a finance lease

Until 1984, UK companies were able to disguise their true indebtedness by undertak-

ing financial leases. Neither the asset acquired nor the contractual liability incurred

had to appear on the Balance Sheet, although the rental payment obligation had to be

392 Part IV Short-term financing and policies

capital lease/full payout

lease

A lease that transfers most of

the benefits and risks of own-

ership to the lessee

secondary lease

A second lease arranged to fol-

low the termination of the ini-

tial lease period

rebate clause

An arrangement whereby the

lessor pays a proportion of the

resale value of an asset to the

lessee

operating lease

A job-specific lease contract,

usually arranged for a short

period, during which the lessor

retains most of the benefits

and risks of ownership

part payout lease

A lease contract which recovers

a return lower than the capital

outlay made by the lessor

plant hire

Hiring of construction

equipment

the lessee

A firm that leases an asset

from a lessor

the lessor

A firm that acquires equip-

ment and other assets for leas-

ing out to firms wishing to use

such items in their operations

CFAI_C15.QXD 10/26/05 11:58 AM Page 392

.

Chapter 15 Short- and medium-term finance 393

stated in the notes to the accounts. To ensure that Balance Sheets would give a truer

picture of a company’s asset/liability position, the Accounting Standards Committee

issued SSAP 21, ‘Accounting for Leases and Hire Purchase’. This clarified the defini-

tion of a finance lease and issued instructions on how to account for leases.

Since the period of a finance lease usually matches the expected lifetime of an asset,

SSAP 21 defined a finance lease as one ‘that transfers substantially all the risks and

rewards of ownership to the lessee’. It assumes that such a transfer takes place if, at

the start of the lease, the present value of the lease amounts to 90 per cent or more of

the fair value of the asset (normally its cash price). Leases are also treated as financial

leases if they meet one or more of the following criteria:

1 At the end of the lease period, the lessee is given the option to buy the asset at a

price below its anticipated market value.

2 The lease period is no less than 75 per cent of the estimated working life of the asset.

3 Ownership of the asset can be transferred to the lessee at the end of the lease.

If, at the termination of a finance lease, the ownership of the asset does pass from

lessor to lessee, all previously exploited tax benefits will be clawed back by the Inland

Revenue.

The rules laid down for the accounting treatment of a finance lease are as follows:

1 The fair value is capitalised as a fixed asset in the Balance Sheet and is depreciated

over its useful life (or lease term, if shorter).

2 Rental payments are treated as comprising two elements – a finance charge and a

capital repayment. The finance charge is written off over the lease period at a con-

stant periodic rate.

3 The obligation to pay the capital element of the future rentals is recorded as a long-

term creditor in the Balance Sheet. At the outset of the lease period, the capital

element should equal the cash value of the asset.

4 Every year, the appropriate finance charge is recorded in the Profit and Loss

Account.

The International Accounting Standards Board is currently working on a project

to investigate the feasibility of aligning the accounting treatment of finance and

operating leases, i.e. to require that all leases are shown on the Balance Sheet (see

www.asb.org.uk for developments).

15.8 LEASE EVALUATION: A SIMPLE CASE

We now formally evaluate the decision of whether to lease or purchase an asset. We

begin by establishing the basic principles.

A lease requires a series of fixed rentals. This is a major appeal of a lease – the les-

see can predict with certainty its future lease payments, and budget accordingly.

Because leasing effectively offers fixed-rate finance, we examine the merits of a lease

against the yardstick of the cheapest alternative form of borrowing that would other-

wise be used to acquire the asset, normally a bank loan. In other words, leasing is an

alternative to borrowing at the risk-free rate (or, more realistically, the bank’s lending rate) in

order to buy the asset outright. Because leasing involves incurring a fixed liability, astute

lenders regard leases and debts as substitutes, so that an increase in the former should

lead to an exactly compensating decrease in the other. While this ‘one-for-one debt

displacement hypothesis’ is not universally accepted, we will assume that lenders

recognise leasing for what it is. The leasing decision then amounts to evaluating the

question: ‘Is it preferable to lease or borrow-to-buy?’

It follows that the appropriate rate of discount to use in lease evaluation is the lessee’s cost

of borrowing. This is shown in the following example.

CFAI_C15.QXD 10/26/05 11:58 AM Page 393

.

394 Part IV Short-term financing and policies

■ Lease evaluation: Hardup plc

Hardup plc wishes to lease an executive jet aircraft from Flush Ltd, the leasing sub-

sidiary of Moneybags Bank plc. The aircraft would otherwise cost £13.75 million to pur-

chase via a bank loan at a 12 per cent interest rate. Flush quotes an annual rental of

£5 million over three years, with the first instalment payable immediately, and the rest

annually thereafter. Should Hardup lease or borrow-to-buy? With a lease, Hardup

avoids the immediate cash outlay of £13.75 million, but loses out on any resale value

(unless there is a rebate clause).

We may assess the value of the lease on an incremental basis, by finding the NPV

of the decision to lease rather than borrow-to-buy, sometimes called the net advan-

tage of the lease (NAL). Table 15.2 sets out the relevant cash flows. For the purpos-

es of this simple example, tax has been ignored (we will see later that the tax

regulations have had an important bearing on the growth of leasing). We also ignore

any resale value.

The incremental cash flow profile shows that, by leasing, Hardup effectively obtains

net financing of £8.75 million in exchange for debt service costs of £5 million in each of

the following two years. (Notice that the timing of rental payments conflicts with our

usual assumption of year-end payments. The lease rentals are actually paid at the start

of Years 1, 2 and 3, respectively, which has negligible impact on the present value com-

putations, but could have important tax implications.) After allowing for the 12 per cent

cost of borrowing, the NPV of million indicates that the optimal form of financ-

ing arrangement is to obtain a lease from Flush. The same result could have been

obtained by separately discounting the two cash flow streams and choosing the one

with the lowest present value. This is simply a comparison between an outlay of £13.75

million and three payments of £5 million p.a. beginning now, with a present value of

£13.45 million, discounted at 12 per cent. For many purposes, the incremental layout is

easier and clearer: for example, it focuses attention directly on the relative merits of the

two options.

■ An alternative method of evaluation: the equivalent loan

Another approach to lease evaluation is to compare the purchase price of the asset con-

cerned with the equivalent loan, defined as the loan that would involve the same

schedule of interest and repayments as the profile of rentals required by the lessor. The

lease is adjudged worthwhile if the lease rental schedule provides more finance than

the loan that would be required to purchase the asset outright. The appeal of this

approach is that it emphasises the financing function of a lease. In the Hardup exam-

ple, the equivalent loan is the maximum loan at 12 per cent that could be supported by

a payment of £5 million now and two further payments of £5 million, after one and two

years respectively. To find the equivalent loan, we simply calculate the present value of

£0.30

Table 15.2

Hardup plc’s leasing

analysis

Year

Item of cash flow (£m) 0 1 2

Lease

Rentals

Buy

Outlay

Incremental cash flows

Present value at 12%

Net present

value £0.30 m

3.994.468.75

5.005.008.75

13.75

5.005.005.00

CFAI_C15.QXD 10/26/05 11:58 AM Page 394