Pike Robert, Neal Bill. Corporate finance and investment: decisions and strategy

Подождите немного. Документ загружается.

.

Chapter 14 Short-term asset management 365

The total cost is:

Algebraically,

where Q is the quantity ordered, C is the cost of placing an order, H is the cost of hold-

ing a unit of stock for one year and A is the annual usage of stock.

The economic order quantity is that quantity which minimises the total cost. We

examined a similar cost function when we discussed total working capital investment

in the previous chapter.

At its simplest, the economic order quantity (EOQ) can be calculated as follows:*

EOQ

B

2AC

H

Total cost a

C

Q

Ab a

Q

2

Hb

Total cost Ordering costs Holding costs

Self-assessment activity 14.3

What do you understand by carrying costs and ordering costs? How do they fit into the

economic order quantity formula?

(Answer in Appendix A at the back of the book)

EOQ example: Ivan plc

Ivan plc uses 2,000 units of stock item KPR each year. The cost of holding a single item

for a year is and the cost of placing each order is The current order quantity is

200 units, but the company is considering changing to batches of 400. Is this the opti-

mum re-order quantity?

Using the cost equation above:

The minimum total cost is achieved by ordering 300 units.

This is confirmed as the most economic order quantity by the EOQ model:

Each order will be placed for 300 units, which implies that orders will be placed

every 55 days (i.e. ).300>2,000 365

300 units

EOQ

B

2 2000 £45

£2

290,000

Total cost for 300 a

£45

300

2,000b a

300

2

£2b £600

Total cost for 400 a

£45

400

2,000b a

400

2

£2b £625

Total cost for 200 a

£45

200

2,000b a

200

2

£2b £650

£45.£2

*Mathematically, the EOQ is the value of Q that minimises the sum of ordering and holding costs.

This is found by the technique of differentiation.

CFAI_C14.QXD 3/15/07 7:16 AM Page 365

.

366 Part IV Short-term financing and policies

This simple model has two important limitations:

1 Demand, and therefore stock usage, may be seasonal. Hence the constant usage rate

for stock assumed here may be unrealistic. Alternatively, demand may be difficult

to predict, which necessitates holding safety or buffer stocks, and calls for a modi-

fication of the model.

2 Only the more easily quantifiable costs are included. Many of the other costs

referred to earlier (lost goodwill, lost production, etc.) should also be considered.

We have so far assumed that stocks are used up at a constant rate and are replen-

ished when the old level falls to zero. A stockout occurs when a firm is unable to deliv-

er a product due to the lack of a specific inventory item. It is therefore tempting for

firms to hold large levels of safety stocks to reduce this risk. In effect, this is a form of

just-in-case management, as opposed to just-in-time management (see below).

Holding costs will rise through carrying safety stocks, but costs associated with

stockouts will fall. The level of safety stock will be affected by management’s ability to

forecast stock usage and lead time replenishment. Lead time is the delay between

ordering and arrival of stock. Each stock item requires a re-order point to be set to

cover safety stocks and lead time. The re-order point will be:

In words, the re-order point (R) equals the lead time (L) times the weekly stock

demand (W) plus the average safety stock (S).

Returning to the example of Ivan plc, if the stock item under consideration has a

three week re-order lead time and an average level of safety stocks is set at 40 units,

we can determine the re-order point, assuming a 50-week working year.

In practice, rarely is demand uniform, and usage and lead times are uncertain.

Determining the optimal stock levels and order quantities under conditions of uncer-

tainty requires probabilistic inventory control models, which are beyond the scope of

this book. However, the fundamental point remains that determining the optimal

stock level involves balancing the expected costs of ordering and stockouts against the

cost of holding additional stocks.

Materials requirement planning (MRP)

MRP is a computer-based planning system for scheduling stock replenishment, ensur-

ing that adequate materials are always available for production purposes. Raw materi-

als are determined from production schedules and lead times for replenishment. MRP

can greatly reduce stockholding costs where the finished product requires a multi-stage

production process with a large number of components and sub-assemblies, such as in

motor car manufacture.

MRPII is a more comprehensive manufacturing resource planning system, which

integrates all the resource requirements of the company. In addition to stocks, it also

encompasses labour and machine requirements.

Just-in-time

In recent times, managers in some manufacturing firms have been aiming for ‘stockless

production’ and just-in-time (JIT) deliveries. JIT aims for an ‘ideal’ level of zero stocks,

but with no hold-ups due to stock shortages. Materials and parts are delivered from

suppliers just before they are needed, and products are manufactured just before they

are needed for sale to customers. Where such an operation is successful, the consequent

160 units

3

2,000

50

40

R LW S

R LW S

safety/buffer stocks

Stocks held as insurance

against stock-outs (shortages)

stockout

Where a firm is unable to

deliver due to shortage of

stock

CFAI_C14.QXD 3/15/07 7:16 AM Page 366

.

Chapter 14 Short-term asset management 367

reduction in inventory and the cash operating cycle can be very considerable. Indeed,

trade creditors can virtually match the current asset investment, thus enabling the busi-

ness to operate with the minimum of working capital.

While it focuses on minimising stock levels, JIT forms part of a total quality pro-

duction programme and rarely works well in isolation. A number of conditions are

necessary for JIT to operate successfully:

■ Strong links and shared information with suppliers and customers.

■ Satisfied customers.

■ A quality production process in a ‘right-first-time’ culture.

■ Computerised ordering and inventory tracking systems.

■ Smooth movement of materials from process to process.

Suppliers are typically located close to the manufacturer, making regular (often

daily) deliveries in small quantities. They are tightly managed and deliver quality

assured components to meet agreed production schedules.

JIT was first introduced by Toyota in 1981, using the famous Kanban (card) system.

Cards are attached to component containers to monitor the flow of production through

the factory, then are returned to signal the need for more supplies. It is particularly suit-

ed to high-volume products where assembly line schedules operate continuously.

The main benefits of JIT, experienced by a growing number of companies, are:

1 Drastically reduced stock levels with commensurate savings in storage space, staff

and financing costs.

2 A ‘right-first-time’ culture.

3 Reduced stock defects.

4 Increased productivity.

14.5 CASH MANAGEMENT

Throughout this book, we have emphasised the importance of cash – rather than profit –

in financial management. We now consider why cash has such a vital role to play, and

how cash flow forecasts are prepared and used to help manage businesses operating in

uncertain environments.

■ Why hold cash?

The word cash is something of a misnomer. While some ‘cash’ will be in the form of

notes and coins, or bank accounts giving immediate access, much will be invested in

short-term bank deposits.

Why should a company hold sums of money in cash or short-term deposits when

the return is often quite low? There are a number of reasons why companies hold cash

balances:

1 Transactions motive. Day-to-day cash inflows and outflows do not match perfectly;

cash serves as a buffer to ensure that transactions occur at the appropriate time.

Cash balances are particularly important where the patterns of cash inflows and

outflows differ greatly, e.g. where business is highly seasonal.

2 Precautionary motive. Cash flows are often difficult to predict. Cash balances are

required to cater for unanticipated cash disbursements.

3 Speculative motive. Cash allows the business to be highly flexible and to exploit

wealth-creating opportunities more easily. Large cash balances are common

among acquisitive companies where a cash alternative to a takeover bid is

required.

4 Compensation balances motive. Banks provide a range of financial services, many of

which are ‘free’ as long as the company keeps a positive bank balance.

CFAI_C14.QXD 3/15/07 7:16 AM Page 367

.

368 Part IV Short-term financing and policies

Surplus cash is not always reinvested immediately in the business. The cash – or

near cash – balance in some companies can be far greater than that required for nor-

mal trading purposes. The financial press publishes the main types of short-term

financial investment opportunities available to companies, showing the relationship

between maturity and interest rates.

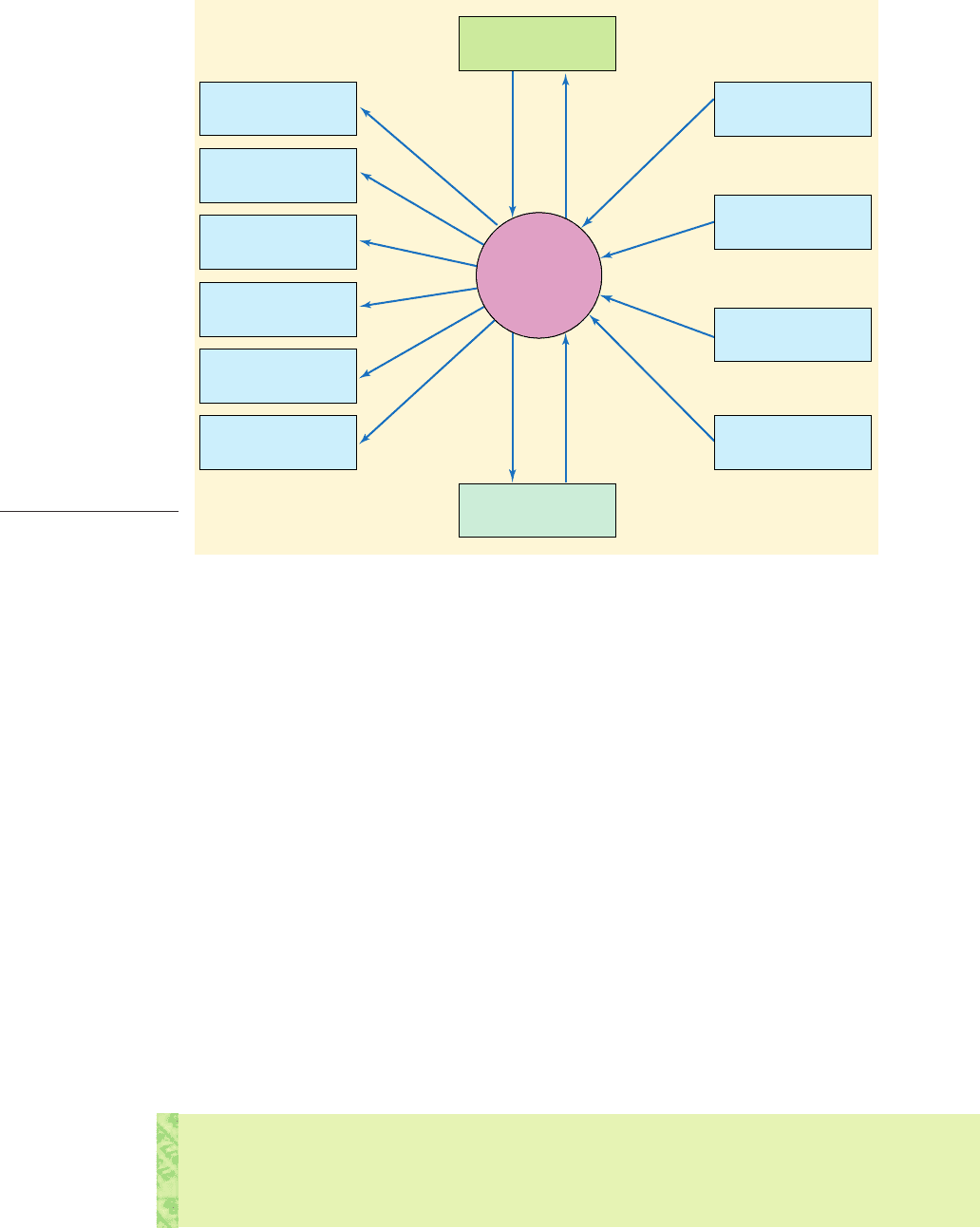

Figure 14.4 illustrates the pivotal role played by cash in a typical firm. The cash bal-

ance is the result of the interactions of various activities with stakeholders.

■ Operating activities – cash from customers less payments to employees and suppliers.

■ Servicing finance – dividends and interest on loans.

■ Taxation – Corporation Tax and VAT.

■ Investing activities – purchase and sale of fixed assets.

■ Financing activities – new finance from shareholders and bondholders, and loan

repayments.

The cash balance is restored to its appropriate level by short-term bank borrowing

or repayment and the sale or purchase of marketable securities. The financial manag-

er should therefore project the firm’s ability to finance its operations and to manage

corporate cash flow.

Capital equipment

manufacturers

Suppliers

Employees

Government

Shareholders

Bondholders

Banks

Cash

Balance

Marketable

securities

Customers

Government

Shareholders

Bondholders

Figure 14.4

Cash flow activity for

main stakeholders

Self-assessment activity 14.4

What are the main motives for holding cash?

(Answer in Appendix A at the back of the book)

CFAI_C14.QXD 3/15/07 7:16 AM Page 368

.

Chapter 14 Short-term asset management 369

Even in well-diversified firms, it makes sense to centralise cash management:

1 It allows the treasurer to operate on a larger scale, which should lead to more com-

petitive interest rates and lower staffing costs.

2 Specialist staff can be employed to work in cash management.

3 Negative cash flows from one operating unit may be offset by positive cash flows

from others, thus avoiding additional financing and loan-raising costs. This may

well mean that the overall level of cash required to cover unanticipated cash short-

falls is reduced.

4 Banking operations become faster and more efficient, giving rise to advantageous

banking arrangements.

■ Cash flow statements

In 1991, the Accounting Standards Board in the UK issued a standard (FRS1) requiring

companies to present a cash flow statement within their published accounts. The inten-

tion was to move away from over-reliance on profits.

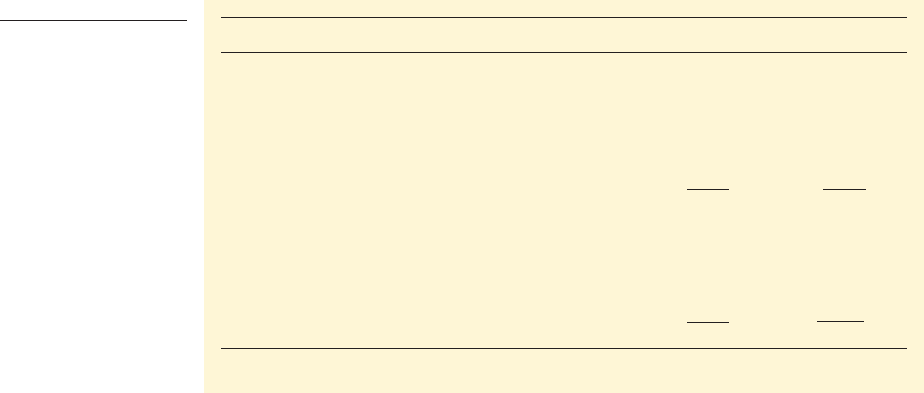

A summarised cash flow statement for the chocolate manufacturer and retailer,

Thorntons plc, is given in Table 14.2. The starting point in the statement is the compa-

ny’s ability to generate cash from its operations. A shareholder reading the cash flow

statement can identify the reasons for the change in cash position over the year.

For 2004, Thorntons achieved a positive cash flow of before financing.

However, the requirement to repay loans resulted in a decrease in cash in the year of

■ Cash flow forecasting

The cash flow forecast, or cash budget, is the primary tool in short-term financial plan-

ning. It helps identify short-term financial requirements and surpluses based on the

firm’s budgeted activities. Cash budgeting is a continuous activity with budgets being

rolled forward, usually in weeks or months, over time.

Preparation of the cash budget involves four distinct stages:

1 Forecast the anticipated cash inflows. The main source of cash is usually sales, and the

sales forecast will therefore be the primary data source. Sales can be divided into

£2,453.

£6,765,000

Table 14.2

Thorntons plc consoli-

dated cash flow

statement

Year ended 26 June: 2004 2003

Cash flow from operating activities 18,132 24,860

Returns on investment and servicing of finance (2,825) (3,225)

Taxation (1,627) (2,727)

Capital expenditure and financial investment (2,492) (2,337)

Equity dividends paid (4,423) (4,422)

Cash inflow (outflow) before use of liquid (6,765) (12,149)

resources and financing

Management of liquid resources (500) (1,792)

Financing

Issue of shares 90 —

(Decrease)/increase in debt (9,808) (11,132)

Decrease/increase in cash in the period (2,453) (2,809)

Source: Thorntons plc, Annual Report, 2004 (www.Thorntons.com).

£000£000

CFAI_C14.QXD 3/15/07 7:16 AM Page 369

.

cash sales and credit sales, the timing of the cash flow arising from the latter depend-

ing on the agreed credit terms. Thus, for example, the sales forecast for January

would appear as a cash receipt in March if all sales were on credit terms of 60 days.

Other cash inflows might be income from investments, cash from disposal of fixed

assets, etc.

2 Forecast the anticipated cash outflows. The main payment is generally the payment of

trade purchases. Once again, the credit period taken must be allowed for. Other

cash outflows include wages and salaries, administrative costs, taxation, capital

expenditure and dividends.

3 Compare the anticipated cash inflows and outflows to determine the net cash flow

for each period.

4 Calculate the cumulative cash flow for each period by adding the opening cash bal-

ance to the net cash flow for the period.

■ Float

The ‘cash at bank’ position shown in a company’s books will not usually be the same

as that shown on the bank statement. Float is the money arising from the time lag

between posting a cheque and it being cleared by the bank.

Float management in Marcus Ltd

On 1 July, the bank statement and cash account in the ledger of Marcus Ltd both show

The company pays suppliers by cheque and receives cheques from

suppliers for The net cash balance in the accounts is therefore

But the bank position is still The cheques from

customers will take three days to clear and the cheques paid will take more like 6–8

days to clear, including postal delay and time taken to pay in the cheque.

The cash controller must, therefore, regularly reconcile the two positions, but also

manage the float by recognising that the actual cleared bank balance, upon which

interest is calculated, is likely to be somewhat higher than the balance in the company’s

accounts. If Marcus can get its customers to pay by direct debit, this will speed up the

banking process and further improve the bank position.

Another method of speeding up collections is concentration banking, where cus-

tomers in a geographical area pay a local branch office rather than head office. The

cheque is then deposited in the local bank branch. Where both the customer and the

company have local banks, this can reduce both postal and clearing time.

Electronic funds transfer has certain benefits over cheque payment by post. Cost

savings arise from the reduction in administration effort, time and postage. The trans-

fer is instantaneous, which means that cash can stay in the company’s bank account

longer. The main disadvantage is that ‘the cheque is in the post’ excuse can no longer

be employed. If payment is made on the same day as the cheque used to be posted, it

impacts on the bank account quicker and results in more interest charges. BACS

(Bankers’ Automated Clearing Services) enables computerised funds transfers

between banks. Corporate customers can use BACS, particularly for payment of

salaries, by providing details of payments. Payment is made in two days. For large

payments, same day clearance can be made through CHAPS (Clearing House

Automated Payment System).

£40,000.£20,000 £15,0002 £35,000.

1£40,000

ˇ£15,000.

£20,000£40,000.

370 Part IV Short-term financing and policies

direct debit

An automatic payment from a

customer’s bank account pre-

arranged with the bank by

both trading partners

concentration banking

Where customers in a geo-

graphical area pay bills to a

local branch office rather than

to the head office

electronic funds transfer

Instantaneous transfer of

money from a debtor’s bank

account to a creditor

14.6 WORKED EXAMPLE: MANGLE LTD

Mangle Ltd produces a single product – a manually operated spindryer. It plans to

increase production and sales during the first half of next year; the plans for the next

eight months are shown in Table 14.3.

CFAI_C14.QXD 3/15/07 7:16 AM Page 370

.

Chapter 14 Short-term asset management 371

Table 14.3

Mangle Ltd: production

and sales

Month Production Sales

November 70 70

December 80 80

January 100 80

February 120 100

March 120 120

April 140 130

May 150 140

June 150 160

Table 14.4

Mangle Ltd: cash budget

for six months to June

(

£

)

Jan. Feb. Mar. Apr. May June

Inflows

Receipts from cash sales 3,200 4,000 4,800 5,200 5,600 7,040

Receipts from debtors 4,200 4,800 4,800 6,000 7,200 7,800

(A) 7,400 8,800 9,600 11,200 12,800 14,840

Outflows

Payments to creditors 2,000 2,400 2,400 2,800 3,000 3,000

Variable costs 3,000 3,600 3,600 4,200 4,500 4,500

Fixed costs 1,800 1,800 1,800 1,800 2,200 2,200

Advertising 2,000 2,000

Capital expenditure 10,000

Dividend 1,000

(B) 8,800 17,800 9,800 8,800 10,700 9,700

Net cash surplus (deficit)

in month (1,400) (9,000) (200) 2,400 2,100 5,140

Opening cash balance 2,000 600 (8,400) (8,600) (6,200) (4,100)

Closing cash balance 600 (8,400) (8,600) (6,200) (4,100) 1,040

1A B2

The selling price is with an anticipated price increase to in June. Raw

materials cost per unit; wages and other variable costs are per unit. Other fixed

costs are a month, rising to from May onwards. Forty per cent of sales

are for cash, the remainder being paid in full 60 days following delivery. Material pur-

chases are paid one month after delivery and are held in stock one month before enter-

ing production. Wages and variable and fixed costs are paid in the month of

production.

A new machine costing is to be purchased in February to cope with the

planned expansion of demand. An advertising campaign is also to be launched,

involving payments of in January and March. The directors plan to pay a divi-

dend of in May. On 1 January the firm expects to have in the bank. How

will the cash position appear over the following six months?

Table 14.4 reveals that the first step is to determine the sales revenue each month.

Forty per cent of sales are for cash and are therefore received in the selling month,

while the remaining 60 per cent are received two months after the month of sale.

Purchases are made in the month prior to entering production, but because a

month’s credit is taken, the payment to creditors is in the same month as production.

After including all cash flows, the net cash flow for each of the six months shows

that, in the first three months, Mangle Ltd has a negative cash flow, and a negative

cash balance for the February to May period. The company may decide that this is a

£2,000£1,000

£2,000

£10,000

£2,200£1,800

£30£20

£110£100,

CFAI_C14.QXD 3/15/07 7:16 AM Page 371

.

372 Part IV Short-term financing and policies

seasonal business and that it is acceptable to operate with such monthly cash flow fig-

ures. In this case, the firm should seek to negotiate a loan to cover the shortfall.

However, it would do well to consider ways of minimising the monthly deficits. For

example, could cash receipts from debtors be collected more quickly? Could payment

of creditors be deferred for a few weeks? Could the price increase be brought for-

ward? Could payment terms on the capital equipment be extended over a longer

period, possibly by leasing the equipment? The cash budget allows finance managers

to consider such questions well ahead of events. Frequently, forward planning avoids

the need to raise external finance through astute management of working capital.

14.7 CASH MANAGEMENT MODELS

We have already examined inventory control models. Cash is, in many ways, simply a

form of inventory, the stock of cash required to enable a business to operate effectively.

William Baumol (1952) recognised the similarity between cash and inventory for

control purposes, particularly when the bank balance is simply a draw-down account.

This is when a firm has a cash balance upon which it draws steadily, and which it

replenishes to the original balance at some point before running out (see the sawtooth

diagram for stock in Figure 14.3). Any surplus cash is invested in interest-bearing

short-term securities.

In this case, the economic order quantity (EOQ) model can be employed, where

EOQ represents the short-term securities to be sold to replenish the balance.

Recall that the equation is:

where C now represents the transaction cost for selling securities, H is the holding cost

of cash (i.e. the interest rate) and A is the annual cash disbursements.

EOQ

B

2CA

H

Self-assessment activity 14.5

As interest rates increase, it obviously becomes more attractive to transfer smaller quantities.

Try reworking the Bizarre problem assuming a doubling of the interest rate to 12 per cent p.a.

(Answer in Appendix A at the back of the book)

Cash management model for Bizarre plc

The treasurer of Bizarre plc, a company specialising in unusual gifts for eccentric business

managers (a rapidly growing market), has a sizeable sum invested in short-term invest-

ments, earning 6 per cent interest. Every time she sells investments to top up the bank bal-

ance the transaction cost is Monthly cash payments are around How often

and by how much should she transfer money to the bank account?

The EOQ model gives an indication of the most economic amount of cash to be drawn

each time:

The frequency with which the treasurer will transfer cash is

a year, or approximately weekly.

1£2.4 million>£45,0002 53 times

B

a

2 £2,400,000 £25

0.06

b £44,721, say £45,000

EOQ

B

a

2 annual cash payments cost of selling securities

annual interest rate

b

£200,000.£25.

CFAI_C14.QXD 3/15/07 7:16 AM Page 372

.

Chapter 14 Short-term asset management 373

The above cash management model works quite well when daily cash drawings on

the bank account are uniform. This is rarely the pattern of actual cash flows in business.

Cash flows go up and down in what often appears a fairly random manner. Miller and

Orr (1966) suggested that, instead of assuming a constant rate of cash payment, per-

haps we should assume that daily balances cannot be predicted – they meander in a

random fashion. This is further discussed in the Appendix to this chapter.

■ Short-term investment

When the cash budget indicates a cash surplus, the financial manager needs to consid-

er opportunities for short-term investment. Any cash surplus beyond the immediate

needs should be put to work, even if just invested overnight. The following considera-

tions should be made in assessing how to invest short-term cash surpluses:

1 The length of time for which the funds are available.

2 The amount of funds available.

3 The return offered on the investment in relation to the investment involved.

4 The risks associated with calling in the investment early (e.g. the need to give three

months’ notice to avoid losing the interest).

5 The ease of realisation.

Examples of short-term investment opportunities are as follows:

■ Treasury Bills – issued by the Bank of England and guaranteed by the UK govern-

ment. No interest as such is paid, but they are issued at a discount and redeemed at

par after 91 days. At any time, the bills can be sold on the money market.

■ Bank deposits – a wide range of financial instruments is available from banks, but the

more established investment opportunities are:

(a) term deposits, where for a fixed period (usually from one month to six years)

a fixed rate is given. For shorter periods (typically up to three months), the

interest may be at a variable rate based on money market rates

(b) Certificates of Deposit, issued by the banks at a fixed interest rate for a fixed

term (usually between three months and five years), but which can be sold on

the money market at any time.

■ Money market accounts – most major financial institutions offer schemes for invest-

ment in the money market at variable rates of interest (e.g. treasury accounts).

SUMMARY

The management of working capital is a key element in financial management, not

least because, for most firms, current assets represent a major proportion of their total

investment. Working capital policy is concerned with determining the total amount

and the composition of a firm’s current assets and current liabilities.

Key points

■ An effective debtor control policy should cover the credit period, credit standard,

cost of cash discounts and collection policy.

■ Credit terms should reflect the customer’s credit rating, normal terms of the indus-

try and the extent to which the firm wishes to use credit as a marketing tool.

■ In evaluating customer credit worthiness, remember the five Cs: capacity, charac-

ter, capital, collateral and conditions.

Continued

CFAI_C14.QXD 3/15/07 7:16 AM Page 373

.

374 Part IV Short-term financing and policies

Further reading

Pike et al. (1998) report findings on trade credit management in large companies.

Brigham and Gapenski (1996) and Brealey, Myers and Allen (2005) provide fuller discussions on

the issues addressed in this chapter. Sartoris and Hill (1981) provide a present value approach to

credit evaluation. The pioneering work on cash management models is found in Baumol (1952)

and Miller and Orr (1966).

Useful websites

Better Payments Practice Group: www.payontime.co.uk

Credit checks: www.checkit.co.uk

Companies House: www.companieshouse.co.uk

Dun & Bradstreet: www.dnb.com

■ Trade debtors can be used to raise finance through invoice discounting and fac-

toring.

■ Inventory management involves determining the level of stock to be held, when

to place orders and how many units to order at a time.

■ Inventory costs can be classified into carrying or holding costs, which increase as

the level of stock rises, and shortage costs (or stockout costs and ordering costs),

which fall as stock levels increase.

■ A variety of economic order quantity models is available for determining the

order quantity that will minimise total inventory cost. The basic model is:

where C is the cost of placing an order, A is the annual usage of stock and H is

the cost of holding a unit of stock for one year.

■ The cash flow forecast, or cash budget, is a vital tool in short-term financial

planning.

■ Cash management models (e.g. Baumol and Miller–Orr models) are useful in set-

ting limits that trigger cash adjustment.

EOQ

A

2AC

H

APPENDIX

MILLER–ORR CASH MANAGEMENT MODEL

When daily cash flows are very difficult to predict, it may be sensible to assume that the

pattern of cash flows is random. This gives rise to the cash position shown in Figure 14.5.

Rather than decide how often to transfer cash into the account, the treasurer sets upper

and lower limits that trigger cash adjustments, sending the balance back to the return

point by selling short-term investments. The diagram prompts two questions:

1 How are the limits set?

2 Why isn’t the return point midway between the two?

CFAI_C14.QXD 3/15/07 7:16 AM Page 374