Whittenburg Gerald E., Altus-Buller Martha. Income Tax Fundamentals

Подождите немного. Документ загружается.

Student Name

Class/Section

Date

KEY NUMBER TAX RETURN SUMMARY

Chapter 7

Comprehensive Problem 1

Schedule C, Gross Income (Line 7) ________________

Form 4562, Depreciation on

7-year Property (Line 19c) ________________

Schedule C, Depreciation (Line 13) ________________

Schedule C, Total Expenses (Line 28) ________________

Schedule C, Net Profit or Loss (Line 31) ________________

Comprehensive Problem 2

Adjusted Gross Income (Line 37) ________________

Itemized Deductions (Line 40) ________________

Exemptions (Line 42) ________________

Tax Liability (Line 60) ________________

Tax Overpaid (Line 73) ________________

Questions and Problems 7-51

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

c

Ryan McVay/Getty Images, Inc.

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Chapter 8

Capital Gains and Losses

LEARNING OBJECTIVES

.............................................. .........................

After completing this chapter, you should be able to:

LO 8.1 Define the term ‘‘capital asset’’ and the holding period for

long-term and short-term capital gains.

LO 8.2 Calculate the gain or loss on the disposition of an asset.

LO 8.3 Compute the tax on long-term and short-term capital assets.

LO 8.4 Understand the treatment of Section 1231 assets and the

various recapture rules.

LO 8.5 Know the general treatment of casualty losses for both

personal and business purposes.

LO 8.6 Understand the provisions allowing deferral of gain on

installment sales, like-kind exchanges, involuntary conver-

sions, and the gain exclusion for personal residences.

Overview

This chapter covers the reporting and taxability of gains and losses from the sale of capital

and non-capital assets. Different tax rates apply to different gains depending on the type of

asset sold and the tax bracket of the taxpayer. Some gains may be deferred into future years

or even excluded from income. Losses may be fully deductible, partly deductible, or non-

deductible depending on the type of transaction.

In general, gains and losses realized are recognized for tax purposes unless there is a tax

provision that specifically allows for a different treatment. Transactions covered in this

chapter include:

1. Section 1231 (business) gains and losses

2. Capital loss netting and carryovers

3. Depreciation recapture on business assets

4. Casualty gains and losses

5. Installment sales

6. Like-kind exchanges

7. Involuntary conversions, and

8. Sales of personal residences.

Capital gains and losses are generally reported on Schedule D, many business asset sale

transactions are reported on Form 4797, and installment sales are reported on Form 6252.

Filled-in examples of each of these forms are provided.

8-1

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 8.1

WHAT IS A CAPITAL ASSET?

When taxpayers dispose of property, they must calculate any gain or loss on the transaction

and report the gain or loss on their tax returns. The gain or loss realized is equal to the

difference between the amount realized on the sale or exchange of the p roperty and the

taxpayer’s adjusted basis in the property. How gains and losses are reported is dependent

on the nature of the property and the length of time the property has been owned. Gains

and losses on the sale of capital assets are known as capital gains and losses and are classi-

fied as either short-term or long-term. For a gain on the sale of a capital asset to be clas-

sified as a lon g-term capital gain, the taxpayer must h ave held the asset for the required

holding period.

The tax law defines a capital asset as any property, whether or not used in a trade o r

business, other than:

1. Stock in trade, inventory, or property held primarily for sale to customers in the

ordinary course of a trade or business;

2. Depreciable property or real property used in a trade or business (Section 1231

assets);

3. Copyrights, literary, musical, or artistic compositions, letters or memorandums, or

similar property if the property is created by the taxpayer;

4. Accounts or notes receivable; and

5. Certain U.S. government publications.

The definition of a capital asset is a definition by exception. All property owned by a

taxpayer, other than property specifically noted as an ex ception, is a capital asset.

Depreciable property and re al estate used in a trade or business are referred to as Sec-

tion 1231 assets and will be discussed later in this chapter since special rules apply to

such assets.

Self-Study Problem 8.1

Indicate, by circling your answer, whether each of the following properti es is

or is not a capital asset.

Property Capital Asset?

1. Shoes held by a shoe store Yes No

2. A taxpayer’s personal residence Yes No

3. A painting held by the artist Yes No

4. Accounts receivable of a dentist Yes No

5. A copyright purchased from a company Yes No

6. A truck used in the taxpayer’s business Yes No

7. IBM stock owned by an investor Yes No

8. AT&T bonds owned by an investor Yes No

9. Land held as an investment Yes No

10. A taxpayer’s television Yes No

11. Automobiles for sale owned by a car dealer Yes No

12. A taxpayer’s sailboat Yes No

8-2 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 8.2

HOLDING PERIOD

Assets must be held for more than 1 year for the gain or loss to be considered long-term.

A capital asset sold before it is owned for the required holding period results in short-term

capital gain or loss. A net short-term capital gain is treated as ordinary income for tax pur-

poses. In calculating the holding period, the taxpayer excludes the date of acquisition and

includes the date of disposition.

EXAMPLE Glen purchased stock as an investment on March 27, 2010. The first

day the stock may be sold for long-term capital gain treatment is

March 28, 2011. N

To satisfy the long-term holding period requirement, a capital asset acquired on the last

day of a month mus t not be disposed of before the first day of the thirteenth month fol-

lowing the month of purchase.

EXAMPLE If Elwood purchases a painting on March 31, 2010, the first day the

painting may be sold for long-term capital gain treatment is April 1,

2011. N

SECTION 8.3

CALCULATION OF GAIN OR LOSS

A taxpayer must calculate his or her amount realized and the adjusted basis of property sold

or exchanged to arrive at the amount of the gain or loss realized on the disposition. The

taxpayer’s gain or loss is calculated using the following formula:

Amount realized Adjusted basis ¼ Gain or loss realized

Sale or Exchange

The realization of a gain or loss requires the ‘‘sale or exchange’’ of an asset. The term ‘‘sale

or exchange’’ is not defined in the tax law, but a sale generally requires the receip t of money

or the relief from liabilities in exchange for property, and an exchange is the transfer of

ownership of one property for another property .

EXAMPLE Maggie sells stock for $8,500 that she purchased 2 years ago for

$6,000. Magg ie’s adjusted basis in the stock is its cost, $6,000; there-

fore, she realizes a long-term capital gain of $2,500 ($8,500 $6,000)

on the sale. N

Self-Study Problem 8.2

Indicate whether a gain or loss realized in each of the following situations

would be long-term or short-term by putting an ‘‘X’’ in the appropriate blank.

Date Acquired Date Sold Long-Term Short-Term

1. October 16, 2009 May 30, 2010 ____________ ____________

2. May 2, 2009 October 12, 2010 ____________ ____________

3. July 18, 2009 July 18, 2010 ____________ ____________

4. August 31, 2008 March 1, 2010 ____________ ____________

Section 8.3

Calculation of Gain or Loss 8-3

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

EXAMPLE Art owns a home which has increased in value during 2010. If Art

does not sell the home, there is no realized gain in 2010. N

Amount Realized

The amount realized from a sale or other disposition of property is equal to the sum of the

money received, plus the fair market value of other property received, less the costs paid to

transfer the property. If the taxpayer is relieved of a liability, the amount of the liability is

added to the amount realized.

EXAMPLE In 2010, Ted sells real estate held as an investment for $75,000 in

cash, and the buyer assumes the mortgage on the property of

$120,000. Ted pays real estate commissions and other transfer costs

of $11,000. The amount realized on the sale is calculated as:

Cash received $ 75,000

Liabilities transferred

120,000

Total sales price 195,000

Less: tran sfer costs

(11,000)

Amount realized

$184,000

N

Adjusted Basis

The adjusted basis of property is equal to the original basis adjusted by adding capital

(major) improvem ents and deducting de preciation allowed or allowable, as illustrated by

the following formula:

Adjusted basis ¼ Original basis þ Capital improvements Accumulated depreciation

The original basis is usually the cost of the property at the date of acquisition, plus any

costs inci dental to the purchase, such as title insurance, escrow fees, and inspection fees.

Capital improvements are major expenditures for permanent improvements to or restora-

tion of the taxpayer’s property. These expenditures include amounts which result in an

increase in the value of the taxpayer’s property or substantially increase the useful life of

the property, as well as amounts which are spent to adapt property to a new use. For exam-

ple, architect fees paid to plan an addition to a building, as well as the cost of the additio n,

must be added to the original basis of the asset as capital improvements. Ordinary repairs

and maintenance expenditures are not capital expenditures.

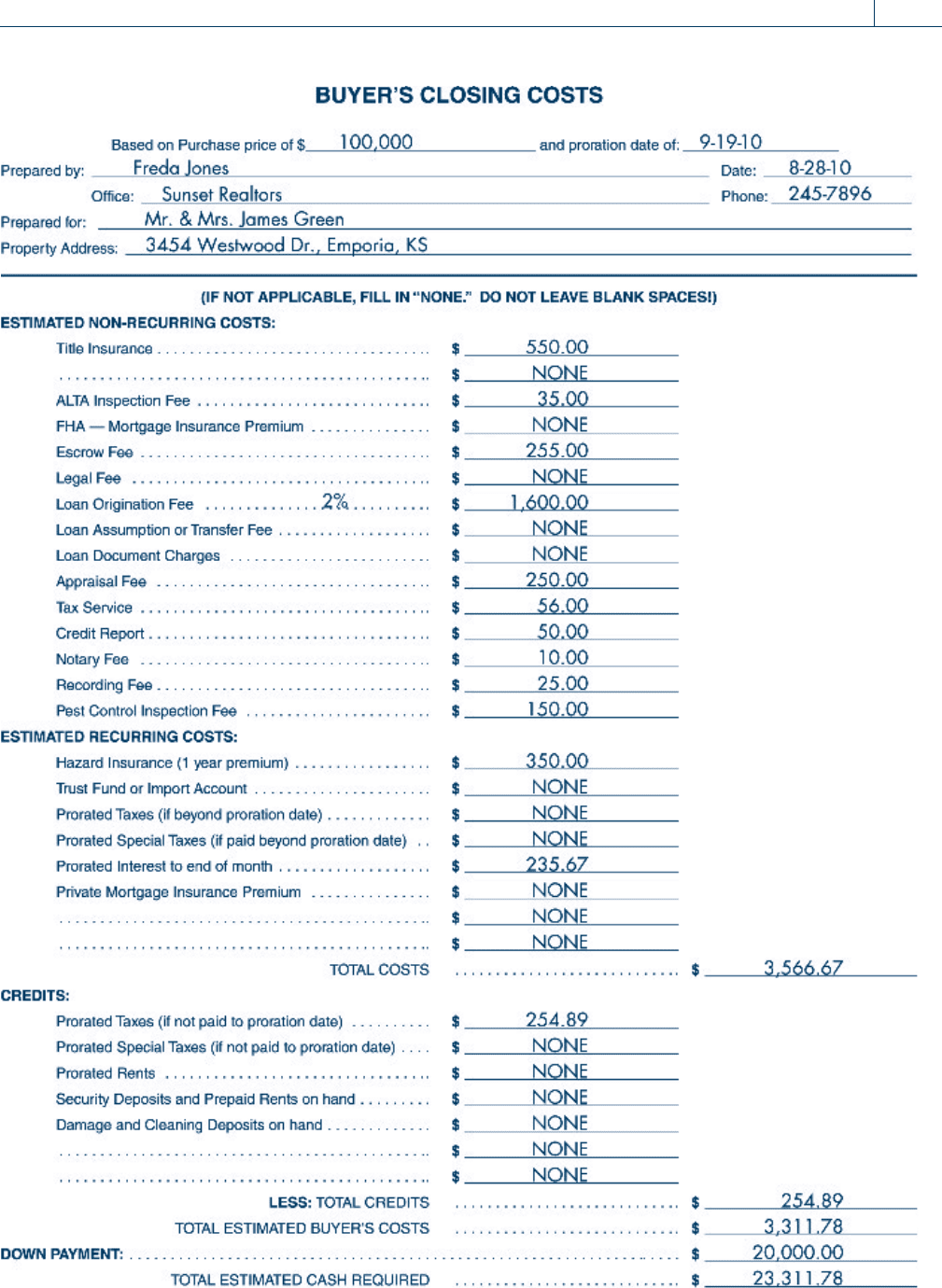

EXAMPLE James and his wife purchased a house on September 19, 2010. Their

closing statement for the purchase is illustrated on page 8-5. Their

original tax basis in the house is equal to the purchase price of

$100,000 plus the incidental costs of title insurance, inspection fee,

escrow fee, appraisal fee, tax service, credit report, notary fee, record-

ing fee, and pest control inspection fee. Therefore, their original basis

is $101,381 ($100,000 þ $550 þ $35 þ $255 þ $250 þ $56 þ $50 þ

$10 þ $25 þ $150). The loan origination fee represents ‘‘points’’ on

the mortgage loan. If the house is their principal residence, the points

are deductible as interest in the year of payment. The prorated inter-

est and taxes affect their deductions for interest and taxes, as

described in Chapter 5. The insurance is a nondeductible personal

expense, assuming the house is their personal residence. N

8-4 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Section 8.3

Calculation of Gain or Loss 8-5

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

EXAMPLE Paul acquired a rental house 4 years ago for $91,000. Depreciation

claimed on the house for the 4 years totals $14,000. Paul installed a

new roof at a cost of $2,500. The adjusted basis of the house is

$79,500, as calculated below:

Adjusted basis

depreciation

¼ Original basis þ Capital improvements Accumulated

¼ $91,000 þ $2,500 $14,000

¼ $79,500 N

If property is received from a decedent (as an inheritance), the original basis is equal to

the fair market value at the decedent’s date of death. (This may not apply to large in her-

itances in 2010.) For property acquired as a gift, the amount of the donee’s basis depends

on whether the property is sold for a gain or a loss by the donee. If a gain results from the

disposition of the property, the donee’s basis is equal to the donor’s basis. If the disposition

of the property results in a loss, the donee’s basis is equal to the lesser of the donor’s basis

or the fair market value of the property at the date of the gift. When property acquired by

gift is disposed of at an amount between the basis for gain and the basis for loss, no gain or

loss is recognized. Note that the basis for gain and the basis for loss will be different only

where the gifted property has a fair market value, on the date of the gift, that is less than the

donor’s adjusted basis in the property.

Taxpayer errors in rep orting the adjusted basis of stock and other property sold

are common. A Government Accountability Office (GAO) report estimated that

over one-third of individuals with securities transactions failed to report capital

gains and losses accurately. The GAO suggested Congress consider requiring

broker s to report adjust ed basis to both taxpayers and the IRS. On October 3,

2008, Congress passed a law which requires brokers to report basis for some

sales made as early as 2011.

EXAMPLE Ron received AT&T stock upon the death of his grandfather. The stock

cost his grandfather $6,000 40 years ago and was worth $97,000 at the

date of his grandfather’s death. Ron’s basis in the stock is $97,000. N

EXAMPLE Jane received a gift of stock from her mother. The stock cost her mother

$9,000 5 years ago and was worth $6,500 on the date of the gift. If the

stock is sold by Jane for $12,000, her gain would be $3,000 ($12,000

$9,000). However, if the stock is sold for $5,000, the loss would be only

$1,500 ($5,000 $6,500). If the stock is sold for an amount between

$6,500 and $9,000, no gain or loss is recognized on the sale. N

Self-Study Problem 8.3

Supply the missing information in the following blanks:

Original Cost

Accumulated

Depreciation

Capital

Improvements Adjusted Basis

1. $15,000 $5,000 $1,000 $_________

2. 15,000 8,000 _________ 9,000

3. 30,000 _________ 2,000 17,000

4. _________ 9,000 4,000 18,000

8-6 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 8.4

NET CAPITAL GAINS

The capital gains rates shown below are for 2010. After 2010, these capital

gains rates will ‘‘sunset,’’ and as we go to press, we do not know what the

rates will be for 2011. In 2011, we may see a reversion to higher rates in effect

a decade ago as is currently scheduled under the law. It is also possible that

Congress will pass new laws with a completely new set of rates, or it is possible

that Congress will extend the 2010 rates for another year.

In recent years, the tax rates on long- and short-term capital gains have become com-

plex. Short-term capital gains are taxed as ordinary income, while there are various differ-

ent preferential long-term capital gains tax rates. The 2010 capital gains tax r ates are as

follows:

Capital Gains and Applicable Tax Rates

Type of

Capital Gain*

For Taxpayers in

10%–15% Brackets

For Taxpayers in 25% and

Above Brackets

Short-term Taxed at ordinary income rates Taxed at ordinary income r ates

Long-term** 0% 15%

Unrecaptured

Section 1250

Gain (Deprecia-

tion recapture

on real estate—

See Section 8.7)

Taxed at ordinary income rates

for taxpayers in the 10% and

15% brackets

Taxed at 25% for taxpayers in

the 25% and higher brackets

* For gains on collectibles (artwork, coins, gems, stamps, etc.), the tax rate is capped at

28% for taxpayers in the 28% and higher tax brackets.

** The 0% and 15% tax rates are scheduled to remain in effect through 2010.

EXAMPLE In 2010, Pedro and Paula’s (married , f iling jointly) only long-term

capital gain is $30,000 from the sale of stock. Their noncapital ordi-

nary income (salary, interest, etc.) is $82,000, putting them in the

25 percent ordinary tax bracket. Pedro and Paula would pay the

tax shown in the tax tables on the $82,000. The $30,000 would be

taxed at the 15 percent preferential long-term capital gain rate.

Thus, the tax on the gain from the stock would be $4,500 (15%

$30,000). N

EXAMPLE In October 2010, Frank and Fran (married, filing jointly) have a long-

term capital gain of $30,000 on the sale of stock. They have no other

capital gains or losses for the year. Their ordinary income after the

standard deduction and exemptions for the year is $13,000, making

their total taxable income for the year $43,000 ($13,000 þ $30,000).

In 2010, married-filing-jointly taxpayers pay 10 percent on taxable

income up to $16,750 and 15 percent on taxable income from

Section 8.4

Net Capital Gains 8-7

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

$16,750 up to $68,000. The capital gains rate used for Frank and

Fran would be selected based on their income in the 10 percent and

15 percent ordinary income brackets, that is, a 0 percent long-term

capital gains rate would apply.

For purposes of illustration, their total tax liability would be calcu-

lated as follows:

Tax on ordinary income $13,000 10% ¼ $1,300

Tax on capital gains $30,000 0% ¼

0

Total tax

$1,300

Tax on ordinary income up to $100,000 is taken from the tax

tables, and in the tables, amounts are calculated based on the mid-

point of ranges, not exact numbers. The tax table shows $1,303 as tax

on $13, 000, slightly different from the example. In practice, the

amounts from the tax tables would be used. N

Ordering Rules for Capital Gains

Since there are multiple kinds of capital gains on which to calculate tax, an ordering system

is necessary to know which capital gains to tax at what rates. The various kinds of gains are

included in taxable income in the following order:

1. Short-term capital gains

2. Unrecaptured Section 1250 gains on real estate

3. Gains on collectibles

4. Long-term capital gains

If taxpayers (or tax practitioners) have several different types of capital gains that interact

with each other, the calculation may become very complex. A good tax preparation com-

puter program will provide the calculation along with supporting worksheets for review.

Calculation of a Net Capital Position

If a taxpayer has a ‘‘net capital gain’’ (net long-term capital gain in excess of net short-term

capital loss), the gain is subject to a preferential tax rate as discussed above. Thus, a tax-

payer has to net multiple long-term and short-term capital transactions that take place dur-

ing a year to calculate tax liability. In calculating a taxpayer’s net capital gain or net capital

loss, the following procedure is followed:

1. Capital gains and losses are classified into two groups, long-term and short-term.

2. Long-term capital gains are offset by long-term capital losses, resulting in either a

net long-term capital gain or a net long-term capital loss.

3. Short-term capital gains are offset by short-term capital losses, resulting in a net

short-term capital gain or a net short-term capital loss.

4. If Step 2 above results in a net long-term capital gain, it is offset by any net short-

term capital loss (Step 3), resulting in either a net capital gain (net long-term capital

gain exceeds net short-term capital loss) or a net short-term capital loss (net short-

term capital loss exceeds net long-term capital gain). If Step 2 above results in a net

long-term capital loss, it is offset against any net short-term capital gain (Step 3),

resulting in either a net long-term capital loss (net long-term capital loss exceeds net

short-term capital gain) or ordinary income (net short-term capital gain exceeds net

long-term capital loss).

8-8 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.