Whittenburg Gerald E., Altus-Buller Martha. Income Tax Fundamentals

Подождите немного. Документ загружается.

the adjusted basis of the property plus Section 1245 recapture potential. Any gain recog-

nized in excess of the amount of ordinary income is a Section 1231 gain.

EXAMPLE On March 1, 2010, Melvin sells Section 1245 property, which was pur-

chased for $6,000 4 years ago. Melvin had claimed depreciation on

the property of $2,500, and sold the property for $5,000. The recap-

ture under Section 1245 is calculated below:

Section 1245 recapture potential $2,500

Adjusted basis ($6,000 $2,500) 3,500

Recomputed basis ($3,500 þ $2,500) 6,000

Gain realized ($5,000 $3,500) 1,500

The ordinary income is equal to the lesser of (1) $2,500, the recom-

puted basis ($6,000) less the adjusted basis ($3,500), or (2) $1,500, the

amount realized ($5,000) less the adjusted basis ($3,500). The entire

gain of $1,500 is ordinary income instead of a Section 1231 gain. N

EXAMPLE Assume the same facts as in the previous example, except that the

property is sold for $7,800. The recapture under Section 1245 is calcu-

lated below:

Section 1245 recapture potential $2,500

Adjusted basis ($6,000 $2,500) 3,500

Recomputed basis ($3,500 þ $2,500) 6,000

Gain realized ($7,800 $3,500) 4,300

The portion classifi ed as ordinary income is equal to the lesser of

(1) $2,500, the recomputed basis ( $6,000) less the adjusted basis

($3,500), or (2) $4,300, the amount realized ($7,800) less the adjusted

basis ($3,500). Of the $4,300 total gain, $2,500 is classified as ordinary

income and the remaining $1,800 ($4,300 $2,500) is a Section 1231

gain. N

Section 1250 Recapture

Section 1250 applies to the gain on the sale of real property, other than real property

included in the definition of Section 1245 property. The amount of Section 1250 recapture

potential is equal to the excess of d epreciation expense claimed over the life of the asset

under an accelerated method of depreciation over the amount of depreciation that

would have been allowed if the straigh t-line method of depreciation had been used. How-

ever, for commercial real property depreciated under accelerated methods under pre-1987

law, 100 percent of depreciation taken may be subject to recapture. If property is depreciated

using the straight-line method, there is no section 1250 recapture potential. Since the use of

the straight-line method is required for real property acquired after 1986, there will be no

Section 1250 recapture on the disposition of such property. In practice, Section 1250 recap-

ture is rarely seen.

‘‘Unrecaptured Depreciation’’ on Real Estate—25 Percent Rate

A special 25 percent tax rate applies to real property gains attributable to depreciation pre-

viously taken and not already recaptured under the Section 1250 or Section 1245 rules dis-

cussed above. Any remaining gain attributable to ‘‘unrecaptured depreciation’’ previously

Section 8.7

Depreciation Recapture 8-19

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

taken, including straight-line depreciation, is taxed at 25 percent rather than the long-term

capital gain rate of 15 percent. When the taxpayer’s ordinary tax rate is only 10 or 15 per-

cent, the depreciation recapture will be taxed at 10 or 15 percent to the extent of the

remaining amount in the 10 or 15 percent bracket and then at 25 percent. The application

of the 25 percent rate for ‘‘unrecaptured dep reciation’’ is frequently seen in practice

because it applies to every rental property which is first depreciated and then sold at a gain.

EXAMPLE Lew acquires an apartment building in 2001 for $300,000, and he sells

it in October 2010 for $500,000. The accumulated straight-line depreci-

ation on the building at the time of the sale is $50,000. Lew is in the

top tax bracket for ordinary income. Lew’s gain on the sale of the

property is $250,000 ($500,000 less adjusted basis of $250,000). $50,000

of the gain is attributable to unrecaptured depreciation and is taxed at

25 percent, while the remaining $200,000 gain is taxed at the 15 per-

cent long-term capital gain rate. N

SECTION 8.8

CAPITAL GAINS AND CASUALTY GAINS AND LOSSES

The treatment of c asualty gains and losses differs depending on whether the property

involved is personal-use, business, or investment property. Therefore, a taxpayer’s business

and investment casualty gains and losses are computed se parately from personal casualty

gains and losses.

Personal-Use Property Casualty Gains and Losses

Please note: The $100 floor discussed below may be changed to $500 by Congress during

the final weeks of 2010. Please see the ‘‘As We Go To Press’’ page and the Whittenburg

companion Web site for updated information.

In Chapter 5, the deduction of personal casualty losses as itemized deductions was dis-

cussed. Occasionally, taxpayers may have a gain from a casualty as a result of receiving an

insurance reimburse ment in an amount in excess of the basis of the property. In such a

case, the taxpayer must first determine the total casualty gains and total casualty losses,

after applying a $100 floor, but before the 10 percent of adjusted gross income limitation

for the year. The total gains and losses are then netted. If losses exceed gains, the excess

loss is treated as an itemized deduction on Schedule A, subject to the 10 percent of adjusted

gross income limitation. If, however, the casualty gains exceed the casualty losses, the taxpayer

must follow the general rules applicable to capital gains and losses. That is, all short-term

Self-Study Problem 8.7

A taxpayer acquired Section 1245 property at a cost of $12,000. The asset was

sold 10 years later for $6,000, and depreciation claimed on the asset was

$7,000. Calculate the following amounts:

1. Adjusted basis $ ____________

2. Recomputed basis $ ____________

3. Recomputed basis less the adjusted basis $ __________ __

4. Amount realized less adjusted basis (gain realized) $ ____________

5. Ordinary income under Section 1245 $ ____________

6. Section 1231 gain $ ____________

8-20 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

casualty gains and losses are netted, all long-term casualty gains and losses are netted, and the

resulting amounts are included with the taxpayer’s other capital gains or losses in determining

the taxpayer’s net capital gain or loss. When casualty gains exceed casualty losses for the year,

none of the casualty losses are subject to the 10 percent of adjusted gross income limitation.

EXAMPLE During 2010, Emily has the following casualties on personal-use

property.

Decrease in Fair

Market Value

Due to Casualty

Adjusted

Basis

Insurance

Reimbursement

Holding

Period

Automobile $5,000 $12,000 $4,000 2 years

Jewelry 7,000 3,000 7,000 9 years

Furniture 1,500 3,000 0 6 months

The properties were damaged as a result of separate casualties.

Step 1: Compute separate casualty gains and losses

Casualty

Gain or (Loss)

Automobile $5,000, lesser of adjusted basis or

decrease in fair market value, less

$4,000 insurance reimbursem ent,

less $100 floor

$ (900)

Jewelry $7,000 insurance reimbursement,

less $3,000 adjusted basis

4,000

Furniture $1,500, lesser of adjusted basis or

decrease in fair market value,

less $100 floor

(1,400)

Step 2: Net all personal casualty gains and losses

$(900) þ $4,000 þ $(1,400) ¼ $1,700 net casualty gain

Step 3: Determine treatment of casualty gains and losses

Since an overall gain results, the gain or loss on each item is

treated as a capital ga in or loss as follows:

Automobile—Long-term capital loss $ (900)

Jewelry—Long-term capital gain 4,000

Furniture—Short-term capital loss (1,400)

The capital gains and losses are combined with Emily’s other capital

gains and losses for the year. Since casualty gains exceeded casualty

losses for the year, the casualty losses recognized on the automobile

and the furniture are not subject to the 10 percent of adjusted gross

income limitation. N

The Ninth Circuit Court decided that a man’s payment to a woman to keep her

from revealing their extramarital affair was not a deductible casualty loss.

Section 8.8

Capital Gains and Casualty Gains and Losses 8-21

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Casualty Gains and Losses from Business or Investment Property

Gains and losses arising from a casualty or theft of property used in a trade or business or

held for investment are treated differently from gains and losses arising from a casualty or

theft of personal-use property. Business and investment property must be identified as a

capital asset, trade or business property subject to an allowance for depreciation, or ordi-

nary income property. The following rules apply to the treatment of business or investment

property:

1. Property held for 1 year or less—Gains from trade or business property (including

property used in the production of rental or royalty income) and gains from invest-

ment property are netted against losses from trade or business property, and the

resulting net gain or loss is treated as ordinary income or loss. Losses from invest-

ment property are separately considered.

2. Property held over 1 year—Gains and losses from trade or business property and

investment property are netted.

a. Net gain—If the result is a net gain, the net gain is included in the calculation of

the net Section 1231 gain or loss (the gains and losses are treated as Section 1231

gains and losses).

b. Net loss—If the result is a net loss, the gains and losses from business and invest-

ment property are excluded from Section 1231 treatment. The tax treatment of

the gains and losses depends on whether the property was used in the taxpayer’s

trade or business or held for investment. Gains and losses from business-use assets

are treated as ordinary income and ordinary losses, respectively.

If the taxpayer recognizes a gain as a result of a casualty, and the property involved is

depreciable property, the depreciation recapture provisions may cause all or a part of

the gain to be treated as ordinary income. A casualty involving business property is

included in the definition of an involuntary conversion, so that gain realized may be eligible

for deferral under the special involuntary conversion provisions discussed in Section 8.11 of

this chap ter. The interaction of Section 1231 and casualty gains and losses from business or

investment property is complex. Taxpayers should follow the instructions included with

Form 4684 and Form 4797. See the IRS Web site (www.irs.gov) for samples of these

forms and instructions.

EXAMPLE Two pieces of manufacturing equipment used by Robert in his busi-

ness are completely destroyed by fire. One of the pieces of equipment

had an adjusted basis of $5,000 ($11,000 original basis less $6,000

accumulated depreciation) and a fair market value of $3,000 on the

date of the fire. The other piece of equipment had an adjusted basis

of $7,000 ($18,000 original basis less $11,000 of accumulated deprecia-

tion) and a fair market value of $10,000. Robert receives $3,000 from

his insurance company to compensate him for the loss of the first

piece of equipment, and he receives $8,000 for the second piece of

equipment. As a result of the casualty, Robert’s casualty gain or loss is

calculated as follow s:

Item 1 Item 2

Insurance proceeds $ 3,000 $ 8,000

Basis of property

(5,000) (7,000)

Gain (loss)

$(2,000) $ 1,000

8-22 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

The netting of the business casualty gains and losses results in a

net loss; thus, the gains and losses are excluded from Section 1231

treatment. Since the loss on Item 1 represents a loss arising from an

asset used in the taxpayer’s business (not an asset held for invest-

ment), the loss is considered an ordinary loss. The $1,000 gain from

Item 2 is treated as ordinary income, Section 1245 recapture. N

SECTION 8.9

INSTALLMENT SALES

Some taxpayers sell property and do not receive payment immediately. Instead, they take a

note from the purchaser and receive payments over an extended period of time. It would be

a financial hardship to require those taxpayers to pay tax on all of the gain on the sale of the

property in the year of sale when they may not have received enough cash to cover the

taxes. To provide equity in such situations, Congress passed the installment sale provision.

The installment sale provision allows cash basis taxpayers to spread the ga in over the tax

years in which payments are received. On an installment sale, the taxable gain reported

each year is determined as follows:

Taxable gain ¼

Total gain realized on the sale

Contract price

Cash collections during the year

Taxpayers who receive payments over a period of time automatically report gain on the

installment method, unless they elect to report all the gain in the year of the sale. An elec-

tion to report all the gain in the year of sale is ma de by including all the gain in income for

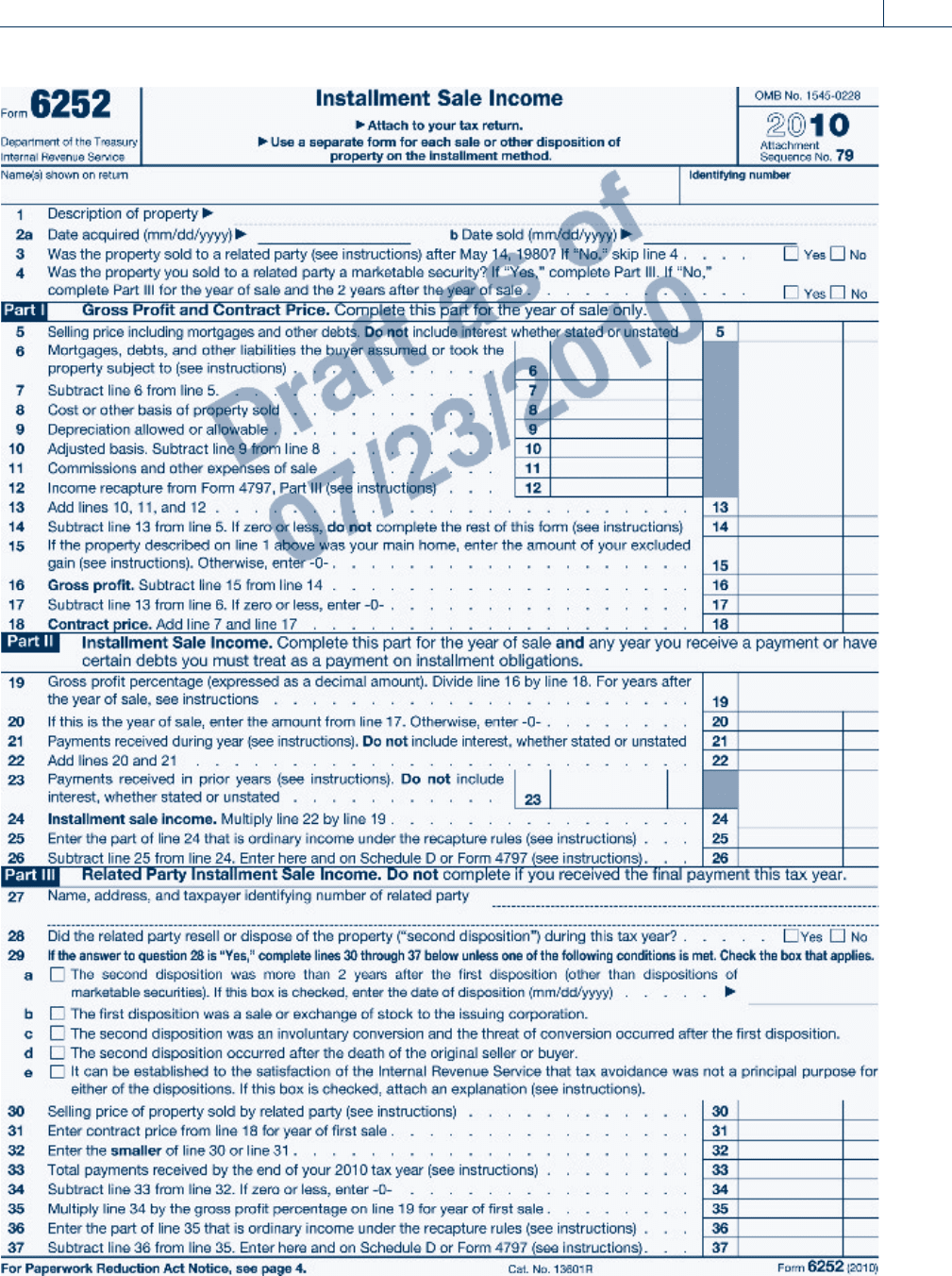

the year of the sale. Taxpayers use Form 6 252, Installment Sale Income, to report the

installment sale gain on their income tax returns.

EXAMPLE Howard Scripp sells land with an adjusted basis of $20,000 for $50,000.

He receives $10,000 in the year of sale, and the balance is payable at

$8,000 per year for 5 years, plus a reasonable amount of interest. If

Howard elects not to report under the installment method, the gain in

the year of sale would be calculated in the following manner:

Cash $ 10,000

Note at fair market value

40,000

Amount realized $ 50,000

Less: the land’s basis

(20,000)

Taxable gain

$ 30,000

N

Self-Study Problem 8.8

Jonathan has the following separate casualties during the year:

Decrease in Fair

Market Value

Adjusted

Basis

Insurance

Reimbursement

Holding

Period

Personal furniture $ 2,000 $ 3,000 $ 1,600 3 months

Personal jewelry 3,000 1,800 2,500 8 years

Business machinery 15,000 14,000 10,000 3 years

Calculate the amount and nature of Jonathan’s gains and losses as a result

of these casualties.

Section 8.9

Installment Sales 8-23

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

EXAMPLE If, instead, Howard reports the gain on the installment method, the

amount of the taxable gain in the year of sale is $6,000, which is cal-

culated below.

Taxable gain ¼

Total gain

Contract price

Cash collections

Taxable gain ¼

$30,000

$50,000

$10,000 ¼ $6,000

Howard must complete Form 6252 as illustrated on page 8-25.

If $8,000 is collected in the first year after the year of sale, the gain

in tha t year would be $4,800, as illustrated below.

Taxable gain ¼

$30,000

$50,000

$8,000 ¼ $4,800

Of course, any interest income received on the note is also included

in income as ordinary income. N

Complex installment sale rules apply to taxpayers who regularly sell real or personal

property and to taxpayers who sell certain business or rental real property. For example,

any recapture under Section 1245 or Section 1250 must be reported in full in the year

of sale, regardless of the taxpayer’s use of the installment method. Any remaining gain

may be reported under the installment method. In addition, certain limitations apply

where there is an installment sale between related parties.

The Contract Price

The contract price used in calculating the taxable gain is the amount the seller will ulti-

mately collect from the purchaser (other than interest). This amount is usually the sales

price of the property. However, the purchaser will occasionally assume the seller’s liability

on the property, in which case the contract price is computed by subtracting from the sell-

ing price any mortgage or notes assumed by the buyer. If the mortgage or notes assumed

by the buyer exceed the adjusted basis of the property, the excess is treated as a cash pay-

ment received in the year of sale and must be included in the contract price.

EXAMPLE Roger receives the following for an installment sale of real estate:

Cash $ 3,000

Roger’s mortgage assumed by the purchaser 9,00 0

Note payable to Roger from the purchaser

39,000

Selling price

$ 51,000

Roger’s total gain is computed as follows:

Selling price $ 51,000

Less: selling expenses

(1,500)

Amount realized 49,500

Less: Roger’s basis in the property

(30,000)

Total gain

$ 19,500

The contract price is $42,000 ($51,000 $9,000), and assuming the

$3,000 is the only cash received in the year of sale, the taxable gain

in the year of sale is $1,393 as shown below:

Taxable gain ¼

$19,500

$42,000

$3,000 ¼ $1,393 N

8-24 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Howard Scripp

Land

50,000

x

0

0

50,000

50,000

.60

0

0

0

10,000

10,000

6,000

6,000

20,000

20,000

20,000

30,000

30,000

0

Section 8.9

Installment Sales 8-25

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

8-26 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Taxpayers may wish to elect out of the installment treatment for a sale which

could qualify, and instead recognize all of the gain in the year of sale when they

have low income and expect that the gain would be taxed at a higher rate if

deferred to later years.

SECTION 8.10LIKE-KIND EXCHANGES

Although a taxpayer realizes a gain or loss on the sale or exchange of property, the rec-

ognition of the gain or loss may be deferred for tax purposes. One example of such a sit-

uation arises when a taxpayer exchanges property for other property of a like kind. Under

certain circumstances, the transaction may be nontaxable. To qualify as a nontaxable

exchange, the property exchanged must be held for productive use in a trade or business

or for investment. Property held for personal purposes, such as a taxpayer’s residence,

will not qualify for a like-kind exchange. When the exchange involves only qualified

like-kind property, no gain or loss is recognized. However, some exchanges include

cash or other property in addition to the like-kind property. Even when the exchange

is not solely for like-kind assets, the nontaxable treatment usually is not completely

lost.Gainisrecognizedinanamountequaltothelesserof(1)thegainrealizedor

(2) the ‘‘boot’’ received. Boot is money or the fair market value of other property received

in addition to the like-kind property. Relief from a liability is the same as receiving cash

and is treated as boot.

The basis of other property received as boot in an exc hange is its fair market value on

the date of the exchange. The basis of the like-kind property received is:

The basis of the like-kind property given up

þ Any boot paid

Any boot received

þ Any gain recognized

Basis of property received

The holding period for property acquired in a like-kind exchange includes the holding

period o f the property exchanged. For example, if long-term capital gain property is

exchanged today, the new property may be sold immediately, and the gain recognized

would be long-term capital gain.

Taxpayers must file Form 8824, Like-Kind Exchanges, to report the exchange of prop-

erty. This form must be completed even if no gain is recognized.

Self-Study Problem 8.9

Brian acquired a rental house in 1987 for a cost of $80,000. Straight-line depre-

ciation on the property of $26,000 has been claimed by Brian. In January 2010,

he sells the property for $120,000, receiving $20,000 cash on March 1 and the

buyer’s note for $100,000 at 10 percent interest. The note is payable at

$10,000 per year for 10 years, with the first payment to be received 1 year

after the date of sale. Calculate his taxable gain under the installment method

for the year of sale of the rental house.

Gain reporta ble in 2010 $ ____________

Section 8.10

Like-Kind Exchanges 8-27

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

EXAMPLE Janis and Kevin exchange real estate held as an investment. Janis gives

up property with an adjusted basis of $350,000 and a fair market value

of $560,000. The property is subject to a mortgage of $105,000 which

is assumed by Kevin. In return for this property, Janis receives from

Kevin property with a fair market value of $420,000 and cash of

$35,000. Kevin’s adjusted basis in the property he exchanges is $280,000.

1. Janis recognizes a gain of $140,000, equal to the lesser of the gain

realized or the boot received as calculated below.

Calculation of gain realized:

Fair market value of property received $420,000

Cash received 35,000

Liability assumed by Kevin

105,000

Total amount realized $560,000

Less: the adjusted basis of the property given up

(350,000)

Gain realized

$210,000

Calculation of boot received:

Cash received $ 35,000

Liability assumed by Kevin

105,000

Total boot received

$140,000

2. The basis of Janis’s property is calculated below.

Basis of the property given up $350,000

þ Boot paid 0

Boot received (140,000)

þ Gain recognized

140,000

Basis of the like-kind property received

$350,000

3. Kevin’s recognized gain is equal to the lesser of the gain realized

or the boot received. Since he received no boot, the recognized

gain is zero.

Calculation of gain realized:

Fair market value of the property received $560,000

Less: boot paid ($105,000 þ $35,000) (140,000)

Less: adjusted basis of property given up

(280,000)

Gain realized

$140,000

Boot received

$0

4. The basis of Kevin’s new property is calculated below.

Basis of the property given up $280,000

þ Boot paid 140,000

Boot received 0

þ Gain recognized

0

Basis of the property received

$420,000

N

Like-Kind Property

The term ‘‘like-kind property’’ does not include inventory, stocks, bonds, or other secur-

ities. A like-kind exchange must involve real estate for real estate, or personal property for

personal property of a like kind or class. Examples of different classes of personal property

8-28 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.