Whittenburg Gerald E., Altus-Buller Martha. Income Tax Fundamentals

Подождите немного. Документ загружается.

The net capital gain computation is illustrated with the following examples:

Example

Net LT Capital

Gain or (Loss)

Net ST Capital

Gain or (Loss)

Net Capital

Position

Taxable

LT Gain

Taxable

ST Gain

a. $10,000 $ 0 $ 10,000 $10,000 $ 0

b. 10,000 (4,000) 6,000 6,000 0

c. 0 20,000 20,000 0 20,000

d. 0 (20,000) (20,000) 0 0

e. 10,000 8,000 18,000 10,000 8,000

f. (8,000) 12,000 4,000 0 4,000

g. (8,000) (6,000) (14,000) 0 0

The rules for the taxation of capital gains are exceptionally complex, and a complete dis-

cussion of them is beyond the scope of the book. For more complete information on capital

gains and losses, see the current edition of West Federal Taxation: Individual Income Taxes.

SECTION 8.5NET CAPITAL LOSSES

Calculation of Net Capital Losses

The computation of an individual taxpayer’s net capital loss is accomplished in a manner

similar to the computation of a net capital gain. A net capital loss is incurred when the total

capital losses for the period exceed the total capital gains for the period.

EXAMPLE Connie has net long-term capital gains of $6,500 and a short-term

capital loss of $8,000. The net (short-term) capital loss is $1,500

($6,500 $8,000). N

EXAMPLE Delvin has net long-term capital losses of $8,000 and a short-term

capital gain of $4,500. The net (long-term) capital loss is $3,500

($4,500 $8,000). N

Treatment of Net Capital Losses

Individual taxpayers may deduct net capital losses against ordinary income in amounts up

to $3,000 per year. Unused capital losses in a particular year may be carried forward indef-

initely. Capital losses and capital loss carryovers first offset capital gains using the ordering

rules discussed on the next page. Any remaining net capital loss may be used to offset ordi-

nary income, subject to the $3,000 annual limitation.

Self-Study Problem 8.4

In October 2010, Jack, a single taxpayer, sold IBM stock for $12,000, which he

purchased 4 years ago for $4,000. He also sold GM stock for $14,000, which

cost $17,500 3 years ago, and he had a short-term capital loss of $1,800 on the

sale of land. If Jack’s other taxable income (salary) is $72,000, what is the

amount of Jack’s tax on these capital transactions?

$ ____________

Section 8.5

Net Capital Losses 8-9

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

EXAMPLE In 2010, Carter has a net long-term capital loss of $15,000 and other

taxable income for the year of $25,000. He may deduct $3,000 of the

loss against the $25,000 of other taxable income. The remaining capital

loss of $12,000 ($15,000 $3,000) is carried forward to future years. N

When unused capital losses are carried forward, they maintain their character as either

long-term or short-term. If a taxpayer has both net long-term losses and net short-te rm

losses in the same year, the net short-term losses are deducted first.

EXAMPLE Frances has a long-term capital loss of $7,000 and a $2,000 short-term

capital loss in 2010. For that year, Frances may deduct $3,000 in capital

losses, the $2,000 short-term capital loss and $1,000 of the long-term

capital loss. Her carryforward would be a $6,000 long-term capital loss.

If Frances has no capital gains or losses in 2011, she would deduct

$3,000 in long-term capital losses and carry forward $3,000 ($6,000

$3,000) to 2012. Assuming she has no other capital gains and losses,

the deduction of losses by year can be summarized as follows:

2010 2011 2012

Long-term capital loss $7,000 $6,000 $3,000

Short-term capital loss 2,000 0 0

Deduction 3,000 3,000 3,000

Long-term capital loss used 1,000 3,000 3,000

Carryforward, long-term capital loss 6,000 3,000 0 N

Taxpayers who have recognized a large capital loss during the year may wish to

sell stock or other property to generate enough capital gains prior to year-end to

use up all but $3,000 of the capital loss. This way, the capital loss in excess of

$3,000 will be used in the current period rather than carried forward, and the

capital gains will be fully she ltered from tax.

Personal Capital Losses

Losses from the sale of personal capital assets are not allowed for tax purposes. For

instance, the sale of a personal automobile at a loss or the sale of a per sonal residence at

a loss does not generate a tax-deductible capital loss for individual taxpayers.

EXAMPLE Rose moved to a nursing home in 2010 and sold both her personal

auto and her principal residence. She originally purchased her auto for

$20,000 and sold it for $10,000. She originally purchased her residence

for $125,000 and sold it for $100,000. The losses on these sales are not

tax-deductible to Rose because the assets were personal use assets. N

Ordering Rules for Capital Losses

When a taxpayer ends up with net capital losses, the losses offset capit al gains using the

following ordering rules:

Net short-term capital losses first reduce 28 percent gains, then 25 percent gains,

then regular long-term capital gains.

Net long-term capital losses first reduce 28 percent gains, then 25 percent gains,

then any short-term capital gains.

8-10 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

As with the ordering rules for capital gains, the ordering calculation may become quite

complex when different classes of capital assets are present. A detailed discussion is beyond

the scope of this text.

SECTION 8.6

SECTION 1231 GAINS AND LOSSES

Section 1231 assets are not capital assets (see Sectio n 8 .1), but they are given special tax

treatment. Gains on Section 1231 assets may be treated as long-term capital gain s, while

losses in some cases may be deducted as ordinary losses. Section 1231 assets include:

1. Depreciable or real property used in a trade or business;

2. Timber, coal, or domestic iron ore;

3. Livestock (not including poultry) held for draft, breeding, dairy, or sporting pur-

poses; and

4. Unharvested crops on land used in a trade or business.

Any property held 1 year or less, inventory and property held for sale to customers, and

copyrights, paintings, government publications, etc. are not Section 1231 property.

The calculation of net Section 1231 gains and losses is summarized as follows:

Net all Section 1231 gains and losses. If the gains exceed the losses, the excess is a

long-term capital gain. When the losses exceed the gains, all gains are treated as ordi-

nary income, and all losses are fully deductible as ordinary losses.

EXAMPLE Frank Harper had the following gai ns and losses during August of

2010:

Gain on the sale of land used in his business $ 9,500

Loss on the sale of a truck used in his business (2,100)

Assuming that all of the property was owned more than 12 months,

Frank’s gains and losses would be calculated as follows:

Gain on land $ 9,500

Loss on truck

(2,100)

Net Section 1231 gain

$ 7,400

The $7,400 gain would be treated as a long-term capit al gain and

would be reported on Schedule D of Form 1040. N

Self-Study Problem 8.5

During 2010, Gerry Appel, who is single, has the following stock transactions:

Description Date Acquired Date Sold Selling Price Cost Basis

IBM stock 06/21/03 08/15/10 $18,000 $12,500

GM stock 04/18/10 12/07/10 12,000 19,200

Pan Am stock 12/18/04 10/02/10 25,000 21,000

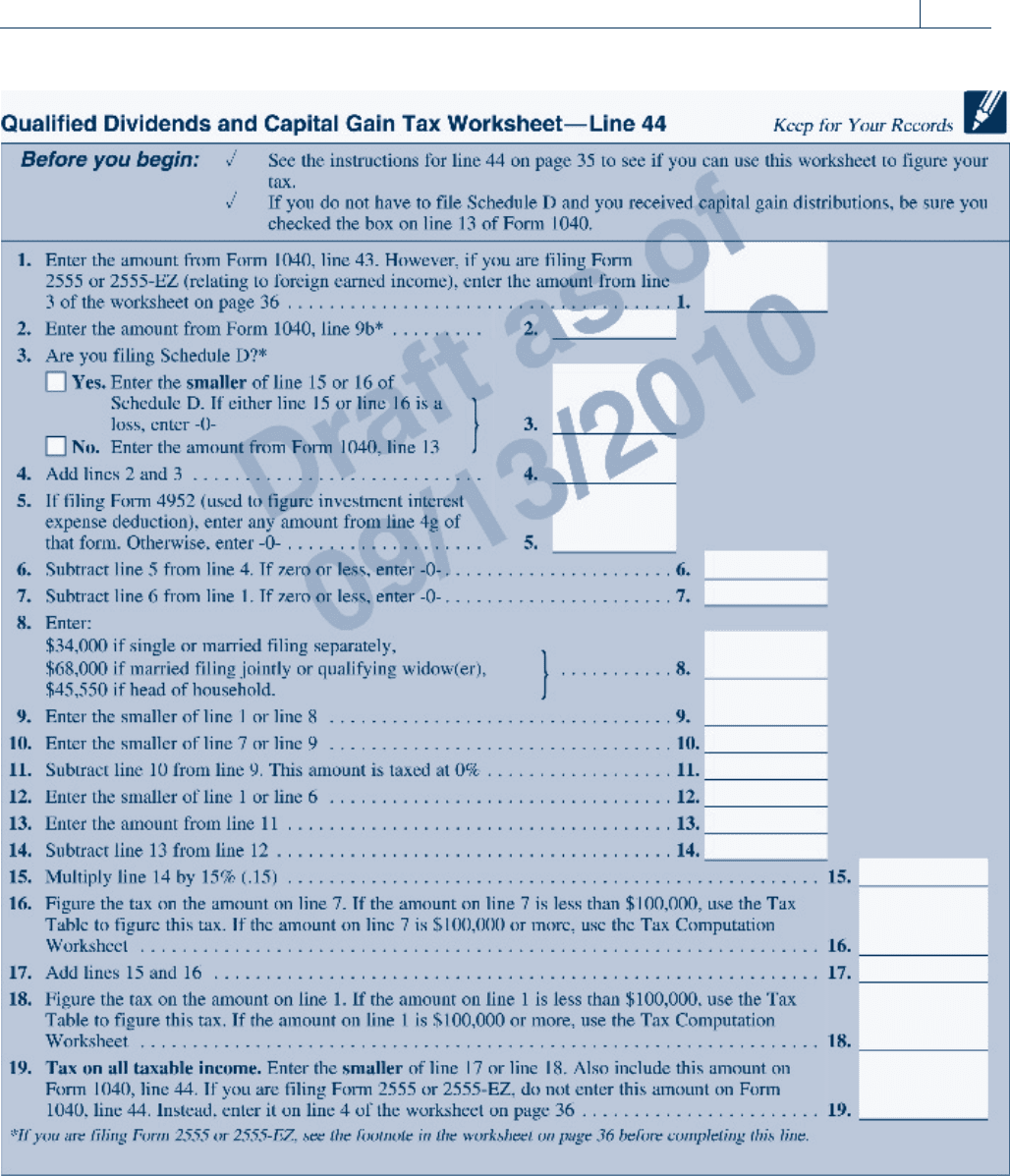

His taxable income is $59,000. Calculate Gerry’s net capital gain or loss and

tax liability using Schedule D of Form 1040, Parts I, II, and III, and the capital

gain tax worksheet on pages 8-13 to 8-15.

Section 8.6

Section 1231 Gains and Losses 8-11

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

SECTION 8.7

DEPRECIATION RECAPTURE

Since long-term capital gains traditionally have been taxed at a lower rate than ordinary

income, taxpayers have attempted to maximize the amount of income treated as capital

gain. Congress enacted depreciation recapture provisions to prevent taxpayers from con-

verting ordinary income into capital gains by claiming maximum depreciation deductions

over the life of the asset and then selling the asset and receiving capital gain treatment

on the resulting gain at sale. There are three major depreciation recapture provisions:

(1) Section 1245, which generally applies to personal property, (2) Section 1250, which

applies to real estate, and (3) ‘‘unrecaptured depreciation’’ previously taken on r eal estate

and taxed at the rate of 25 percent. The depreciation recapture provisions are extremely

complex. Only a brief overview of the general provisions contained in the law is presented

here.

Section 1245 Recapture

Under the provisions of Section 1245, any gain recognized on the disposition of a Section

1245 asset will be classified as ordinary income up to an amount equal to the depreciation

claimed after 1961. Any gain in excess of this amount is classified as Section 1231 gain. Sec-

tion 1245 property is:

Depreciable personal property

Livestock

Amortizable personal property such as patents, copyrights, leaseholds, and profes-

sional sports contracts

Elevators and escalators

Pollution control facilities, railroad grading and tunnel boring equipment, on-the-job

training, and child care facilities

Nonresidential real property (e.g., office buildings) acquired after 1980 but before

1987, on which accelerated ACRS depreciation was claimed

Section 1245 recapture potential is defined as the total depreciation claimed on Section

1245 property after 1961. The amount of ordinary income recognized upon the sale of an

asset under Section 1245 is equal to the lesser of (1) the recomputed basis less the adjusted

basis, or (2) the amount realized less the adjusted basis. The recomputed basis of an asset is

Self-Study Problem 8.6

Gary Farmer had the following Section 1231 gains and losses during the 2010

tax year:

1. Sold real estate acquired on December 3, 2002, at a cost of $24,000, for

$37,000 on January 5, 2010. The cost of selling the real estate was $500,

and there was no depreciation allowable or capital improvements made to

the asset over the life of the asset.

2. Sold a business computer with an adjusted basis of $20,700 that was

acquired on April 5, 2004. The computer was sold on May 2, 2010, for

$14,000, resulting in a $6,700 loss.

Gary’s employer identification number is 74-8976432. Use Form 4797 on

pages 8-17 and 8-18 to report the above gains and losses.

8-12 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Section 8.7

Depreciation Recapture 8-13

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

8-14 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Section 8.7

Depreciation Recapture 8-15

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

8-16 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Section 8.7

Depreciation Recapture 8-17

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

8-18 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.