Whittenburg Gerald E., Altus-Buller Martha. Income Tax Fundamentals

Подождите немного. Документ загружается.

are office furniture and equipment, airplanes, computers and peripheral equipment, trucks,

and automobiles. The exchange of office furniture for a computer, for inst ance, will not

qualify as a like-kind exchange. The like-kind exchange provision is not elective. Taxpayers

must use the provision if a transaction qualifies as a like-kind exchange, regardless of

whether the transaction results in a realized gain or a realized loss.

Tax planning for the sale of business automobiles can sometimes save significant

tax dollars. The luxury auto depreciation rules covered in Chapter 7 allow only

small amounts of depreciation on business autos, so the tax basis of business

automobiles may be much larger than the trade-in or direct sale value, especially

for expensive cars. The direct sale of a business auto will therefore often gener-

ate a deductible loss. An auto trade-in is generally treated as a mandatory like-

kind exchange, so the potential tax-deductible loss must be added to the basis of

the new vehicle and may not be deducted.

SECTION 8.11

INVOLUNTARY CONVERSIONS

Occasionally taxpayers are forced to dispose of property as a result of circumstances

beyond their control. At the election of the t axpayer, and provided certain conditions

are met, the gain on an involuntary conversion of property may be deferred. The provisions

require that the property must be replaced and the basis of the replacement property

reduced by the amount of the gain deferred. An involuntary conversion is defined as the

destruction of the taxpayer’s property in whole or in part, or loss of the property by

theft, seizure, requisition, or condemnation. Also, property sold pursuant to reclamation

laws, and livestock destroyed by disease or drought, are subject to the involuntary conver-

sion rules. To qualify for n onrecognition of gain, the taxpayer must obtain qualified

replacement property. The replacement p roperty must be ‘‘similar or related in service

or use.’’ This definition is narrower than the like-kind rule; the property must be very sim-

ilar to the property converted. Generally, a taxpayer has 2 years after the close of the tax

year in which a gain was realized to obtain replacement property.

A realized gain on the involuntary conversion of property occurs when the taxpayer

receives insurance proceeds or other payments in excess of his or her adjusted basis in

the converted property. Taxpayers need not recognize any gain if they completely reinvest

the proceeds or payments in qualified replacement property within the required time

period. If they do not reinvest the total amount of the payments received, they must rec-

ognize a gain equal to the amount of the payment not reinvested (but limited to the gain

realized). The basis of the replacement property is equal to the cost of the replacement

Self-Study Problem 8.10

During the current year, Daniel James exchanges a truck used in his business

for a new truck. Daniel’s basis in the truck is $18,000, and the truck is subject

to a liability of $8,000, which is assumed by the other party to the exchange.

Daniel receives a new truck that is worth $22,000. Calculate Daniel’s recog-

nized gain on the exchange and his basis in the new truck.

Recognized gain $ ____________

Basis in the new truck $ ____________

Section 8.11

Involuntary Conversions 8-29

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

property reduced by any gain not recognized on the transaction. The holding period of the

replacement property includes the period the original property was held.

EXAMPLE Tammy’s building, which has an adjusted basis of $50,000, is

destroyed by fire in 2010. In the same yea r, Tammy receives $100,000

of insurance proceeds for the loss. She has until December 31, 2012

(2 years after the end of the taxable year in which the gain is realized),

to acquire a replacement building. In 2011, Tammy replaces the build-

ing with a new building costing $80,000. Her realized gain on the

involuntary conversion is $50,000 ($100,000 $50,000), and the gain

recognized is $20,000, which is the $100,000 of cash received less the

amount reinvested ($80,000). The basis of the new building is $50,000

($80,000 $30,000), the cost of the new building less the portion of

the gain not recognized. N

The involuntary conversion provision applies only to gains, not to losses. The provision

must be elected by the taxpayer. In contrast, the like-kind exchange provision discussed

previously applies to both gains and losses and is not elective.

SECTION 8.12 SALE OF A PERSONAL RESIDENCE

Sales after May 6, 1997

For sales of a principal residence afte r May 6, 1997, the long-standing rollover rule (see

below) and the $125,000 exclusion for taxpayers over 55 years old were replaced by a

new g eneral exclusion. For gains on the sale of a person al reside nce after May 6, 1997, a

seller of any age who has owned and used a home as a principal residence for at least 2

of the last 5 years before the sale can exclude from income up to $250,000 of gain

($500,000 for joint return filers). In general, this exclusion can be used only once every

2 years. As under prior law, a personal residence includes single-family homes, mobile

homes, houseboats, condominiums, cooperative apartments, duplexes, or row houses.

EXAMPLE Joe, a single taxpayer, bought his home 22 years ago for $25,000. He

has lived in the home continuously since he purchased it. In Novem-

ber 2010, he sells his home for $300,000. Therefore, his realized gain

on the sale of his personal residence is $275,000 ($300,000 $25,000).

Joe’s taxable gain on this sale is $25,000, which is his total gain of

$275,000 less the exclusion of $250,000. N

Self-Study Problem 8.11

Sam’s store is destroyed in 2010 as a result of a flood. The store has an adjusted

basis of $70,000, and Sam receives insurance proceeds of $150,000 on the loss.

Sam invests $135,000 in a replacement store in 2011.

1. Calculate Sam’s recognized gain, assuming an election under the involuntary

conversion provision is made.

$ ____________

2. Calculate Sam’s basis in the replacement store. $ ____________

8-30 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

A seller otherwise qualified to exclude gain on a principal residence who fails to satisfy

the 2-year ownership and use requirements may calculate the amount of excluded gain by

prorating the exclusion amount if the residence sale is due to an employment-related move,

health, or unforeseen cir cumstances. Unforeseen circumstances include death, divorce or

separation, a change in employment that leaves the taxpayer unable to pay the mortgage,

multiple births from the same pregnancy, and becoming eligible for unemployment com-

pensation. The $250,000 or $500,000 exclusion amount is prorated by multiplying the

exclusion amount by the length of time the taxpayer owned and used the home divided

by 2 years.

EXAMPLE John is a single taxpayer who owns and uses his principal residence

for 1 year. He then sells the residence due to an employment-related

move at a $100,000 gain. Because he may exclude up to one half

(1 year divided by 2 years) of the $250,000 exclusion amount, or

$125,000, none of his gain is taxable. N

Married Taxpayers

Taxpayers who are mar ried and file a joint return for the year of sale may exclude up to

$500,000 of gain realized on the sale of a personal residence. The full $500,000 for a mar-

ried couple can be excluded if:

1. Either spouse owned the home for at least 2 of the 5 years before the sale,

2. Both spouses used the home as a principal residence for at least 2 of the last

5 years, and

3. Neither spouse has used the exclusion during the prior 2 years.

EXAMPLE Don and Dolly have been married for 20 years. At the time they were

married they purchased a home for $200,000 and have lived in the

home since their marriage. Don and Dolly sell their home for $800,000

and retire to Arizona. Their realized gain on the sale is $600,000

($800,000 $200,000), of which only $100,000 is taxable because of

the $500,000 exclusion. N

The $500,000 exclusion for married taxpayers has been extended to spouses who sell the

residence within 2 years of their spouse’s death, for sales after December 31, 2007.

Beginning in 2009, Congress has closed a loophole in the residence gain

exclusion laws, which has been used effectiv ely by some owners of multiple

rental properties. Under the residence gain exclusion laws in operation

prior to 2009, taxpayers with multiple rental properties could move into a

previously rented property every 2 years, reside in the property for the

required 2-year period, and then sell the property using the $250,000 or

$500,000 gain exclusion. Over a period of 10 years, a married couple could

theoretically exclude $2.5 million of taxable gain on five separate properties.

Beginning in 2009, taxpayers who rent their residence prior to their 2 years of

personal use are generally limited to an exclusion smaller than the full

$250,000 or $500,000 amounts. For details, examples, and exceptions to the

new law, visit www.irs.gov.

Section 8.12

Sale of a Personal Residence 8-31

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Sales before May 7, 1997

Please note: The law below no longer applies to sales of principal residences. However,

because many taxpayers still own residences with ‘‘rollover’’ basis determined under this

law, it is important to understand how the law operated.

For sales of a personal residence before May 7, 1997, taxpayers did not have to recognize

gain on the sale if they rolled the gain into a new house with a cost as high as the adjusted

sales price of the old residence. The adjusted sales price was the amount realized on the sale

less any qualified fixing-up expenses. Fixing-up expenses must have been incurred within 90

days prior to the date of sale and paid within 30 days after the date of sale. In addition, the

purchase of the new residence had to be within 2 years of the date of sale of the old resi-

dence to qualify for nonrecognition of the ga in. The adjusted basis of the new residence

was reduced by any gain not recognized on the sale of the old residence.

EXAMPLE Mary sold her personal residence for $60,000 in 1994 and paid selling

expenses of $3,600. Mary had fixing-up expenses of $1,400, and the

basis of her old residence was $40,000. If Mary purchased a new resi-

dence within 2 years for $85,000, her recognized gain and the basis

of the new residence was calculated as follows:

1. Sales price $60,000

Less: selling expenses

(3,600)

Amount realized $56,400

Adjusted basis of the old residence

(40,000)

Gain realized on the sale

$16,400

2. Amount realized $56,400

Less: fixing-up expenses

(1,400)

Adjusted sales price $55,000

Less: cost of the new residence

(85,000)

Gain recognized

$0

3. Gain realized $16,400

Less: gain recognized

(0)

Gain not recognized (deferred)

$16,400

4. Cost of the new residence $85,000

Less: gain deferred

(16,400)

Basis of the new residence

$68,600

N

EXAMPLE Assume instead that Mary paid only $50,000 for a new residence. The

gain and basis of the new residence are calculated as follows:

1. Adjusted sales price (from above) $ 55,000

Less: cost of new residence

(50,000)

Gain recognized

$ 5,000

2. Gain realized (from above example) $ 16,400

Less: gain recognized

(5,000)

Gain not recognized (deferred)

$ 11,400

3. Cost of the new residence $ 50,000

Less: gain deferred

(11,400)

Basis of the new residence

$ 38,600

N

8-32 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

The above calculations show that a taxpayer who sold one or more principal reside nces

over a period of years and ha s a ‘‘rollover’’ basis unde r the old law may have a principal

residence basis that is far lower than the cost of the taxpayer’s residence. Because the

new law does not require rollover treatment, taxpayers receive a fresh basis in a newly pur-

chased residence which is equal to the purchase price.

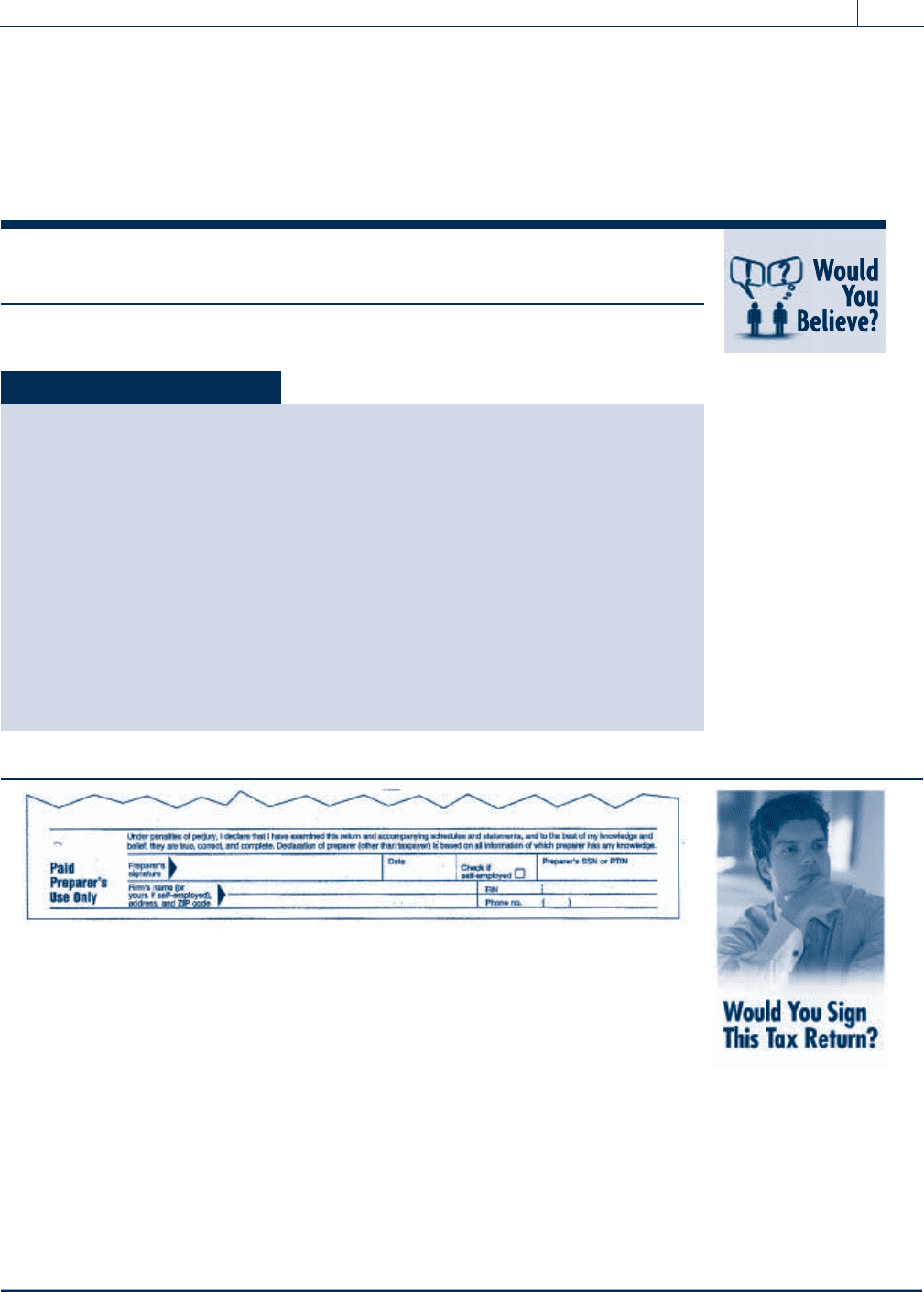

The IRS has ruled that in certain cases, a yacht may qualify as a taxpayer’s

principal residence.

Ivy Tower (age 45), a history professor at Coastal State University, recently

purchased a house near the beach. In the current year, she accepted an

offer from a buyer who wants to make the house into a B&B. She sold her

personal residence for a $100,000 gain. She owned the house 11 months as

of the date of sale. After the sale closed, she discovered that the $100,000 is

taxable as a short-term taxable gain (i.e., ordinary income) because she had

not lived there the 2 years required for exclusion of gain on the sale of a

residence. She is upset that she will have to pay substantial tax on the sale.

Her best friend’s husband is an M.D. who signed a letter that Ivy had to

move due to the dampness and humidity at the beach. She is not a regular

patient of the doctor and Ivy has no history of respiratory problems. Ivy

claims she meets the medical extraordinary circumstances exception and

therefore refuses to report the gain on her Form 1040. If Ivy were your tax

client, would you sign the Paid Preparer’s declaration (see example above)

on her return? Why or why not?

Self-Study Problem 8.12

Mike purchased a house 20 years ago for $30,000. He sells the house in Decem-

ber 2010 for $350,000. He has always lived in the house.

a. How much taxable gain does Mike have from the sale of his personal

residence?

$ ____________

b.Assume Mike married Mary 3 years ago and she has lived in the house since

their marriage. If they sell the house in December 2010 for $350,000, what is

their taxable gain on a joint tax return?

$ ____________

c. Assume Mike is not married and purchased the house only 1 year ago for

$200,000, and he sells the house for $350,000 due to an employment-related

move. What is Mike’s taxable gain?

$ ____________

Section 8.12

Sale of a Personal Residence 8-33

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

KEY POINTS

Learning Objectives Key Points

LO 8.1:

Define the term ‘‘capital asset’’

and the holding period for long-

term and short-term capital gains.

A capital asset is any property, whether or not used in a trade or business, except:

1) inventory, 2) depreciable property or real property used in a trade or business, 3) certain

copyrights, literary, musical, or artistic compositions, letters, or memorandums, 4) accounts

or notes receivable, and 5) certain U.S. government publications.

Assets excluded from the definition of a capital asset generate ordinary income or loss on

their disposition.

Assets must be held for more than 1 year for the gain or loss to be considered long-term.

A capital asset held 1 year or less results in a short-term capital gain or loss.

In calculating the holding period, the taxpayer excludes the date of acquisition and includes

the date of disposition.

LO 8.2:

Calculate the gain or loss on the

disposition of an asset.

The taxpayer’s gain or loss is calculated using the following formula: amount realized

adjusted basis ¼ gain or loss realized.

The amount realized from a sale or other disposition of property is equal to the sum of the

money received, plus the fair market value of other property received, less the costs paid to

transfer the property.

The adjusted basis of property ¼ the original basis þ capital improvements accumulated

depreciation.

In most cases, the original basis is the cost of the property at the date of acquisition, plus

any costs incidental to the purchase, such as title insurance, escrow fees, and inspection

fees.

Capital improvements are major expenditures for permanent improvements to or restoration

of the taxpayer’s property.

LO 8.3:

Compute the tax on long-term and

short-term capital assets.

Short-term capital gains are taxed as ordinary income, while there are various different

preferential long-term capital gains tax rates.

For 2010, net long-term capital gain may be subject to a 28 percent, 25 percent, 15 percent,

or 0 percent tax rate.

The 28 percent rate applies to gains on collectibles (e.g., stamps and coins), the 25 percent

rate applies to depreciation recapture on the disposition of certain Section 1250 assets, and

the 15 percent and 0 percent rates apply to all other net long-term gains.

Individual taxpayers may deduct net capital losses against ordinary income in amounts up

to $3,000 per year with any unused capital losses carried forward indefinitely.

When a taxpayer ends up with net capital losses, the losses offset capital gains as follows:

1) net short-term capital losses first reduce 28 percent gains, then 25 percent gains, then

regular long-term capital gains, and 2) net long-term capital losses first reduce 28 percent

gains, then 25 percent gains, then any short-term capital gains.

LO 8.4:

Understand the treatment of

Section 1231 assets and the

various recapture rules.

If net Section 1231 gains exceed the losses, the excess is a long-term capital gain. When

the net Section 1231 losses exceed the gains, all gains are treated as ordinary income, and

all losses are fully deductible as ordinary losses.

Section 1231 assets include 1) depreciable or real property used in a trade or business,

2) timber, coal, or domestic iron ore, 3) livestock (not including poultry) held for draft,

breeding, dairy, or sporting purposes, and 4) unharvested crops on land used in a trade or

business.

Depreciation recapture provisions are meant to prevent taxpayers from converting ordinary

income into capital gains by claiming maximum depreciation deductions over the life of the

asset and then selling the asset and receiving capital gain treatment on the resulting gain

at sale.

8-34 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Reinforce the tax information covered in this chapter by completing the

online interactive tutorials located at the Income Tax Fundamentals Web site:

www.cengagebrain.com.

Under Section 1245, any gain recognized on the disposition of a Section 1245 asset (gener-

ally personal property) will be classified as ordinary income up to an amount equal to the

depreciation claimed. Any gain in excess of depreciation taken is treated as Section 1231

gain.

Section 1250 real property recapture is the excess of depreciation expense claimed, using

an accelerated method of depreciation, over what would have been allowed if the straight-

line method were used for residential rental property, and 100 percent of accumulated

depreciation taken for commercial property.

Since the straight-line method is required for real property acquired after 1986, there will

be no Section 1250 recapture on the disposition of real property unless it was acquired

more than 20 years ago.

A special 25 percent tax rate applies to real property gains attributable to depreciation pre-

viously taken and not already recaptured under Section 1250 or Section 1245.

LO 8.5:

Know the general treatment of

casualty losses for both personal

and business purposes.

Taxpayers may have a gain from a casualty due to receipt of an insurance reimbursement

in excess of the basis of the property.

The taxpayer must first determine all personal casualty gains and losses (after applying

the $100 floor, but before the 10 percent of adjusted gross income limitation) for the

year.

The total casualty gains and losses are then netted, and if losses exceed gains, the excess

loss is treated as an itemized deduction on Schedule A, subject to the 10 percent of AGI

limitation.

If the casualty gains exceed the casualty losses, the taxpayer must follow the general rules

applicable to capital gains and losses.

Gains and losses arising from a casualty or theft of property used in a trade or business or

held for investment are treated differently than gains and losses from a casualty or theft of

personal-use property.

LO 8.6:

Understand the provisions allowing

deferral of gain on installment

sales, like-kind exchanges, involun-

tary conversions, and the gain

exclusion for personal residences.

On an installment sale, the taxable gain reported each year is determined as follows:

taxable gain equals total gain realized on the sale price, divided by the contract price, and

multiplied by the cash collections during the year.

To be a nontaxable like-kind exchange, the property exchanged must be held for use in a

trade or business or for investment and exchanged for property of a like-kind.

Like-kind gain is recognized in an amount equal to the lesser of 1) the gain realized or

2) the ‘‘boot’’ received. (Boot is money or the fair market value of other property received

in addition to the like-kind property.)

A realized gain on the involuntary conversion of property occurs when the taxpayer receives

insurance proceeds in excess of his or her adjusted basis.

Involuntary conversion gain is not recognized if the proceeds or payments are reinvested in

qualified replacement property within the required time period.

Taxpayers who have owned their personal residence and used it for at least 2 of the

5 years before the sale can exclude up to $250,000 of gain ($500,000 for joint return

filers).

Section 8.12

Sale of a Personal Residence 8-35

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

QUESTIONS and PROBLEMS

GROUP 1:

MULTIPLE CHOICE QUESTIONS

.............................................. .............................................. .

LO 8.1

1. All of the following assets are capital assets, except:

a. A personal automobile

b. IBM stock

c. Business in ventory

d. Personal furniture

e. An individual’s stamp collection

LO 8.1

2. Which of the following is a capital asset?

a. Account receivable

b. Copyright created by the taxpayer

c. Copyright (held by the writer)

d. Business inventory

e. A taxpayer’s residence

LO 8.2

3. Bob sells a stock investment for $45,000 cash, and the purchaser assumes Bob’s

$32,500 debt on the investment. The basis of Bob’s stock investment is $55,000.

What is the gain or loss realized on the sale?

a. $10,000 loss

b. $10,000 gain

c. $12,500 gain

d. $22,500 loss

e. $22,500 gain

LO 8.3

4. In 2010, the top tax rates are _____ percent on individual long-term capital gains on

sale of stock, and _____ percent on capital gains on sales of collectible items.

a. 10; 20

b. 15; 25

c. 15; 28

d. 25; 28

LO 8.3

5. In November 2010, Ben and Betty (married, filing jointly) have a long-term capital gain

of $50,000 on the sale of stock. They have no other capital gains and losses for the year.

Their ordinary income for the year after the standard deduction and personal exemptions

is $68,000, making their total taxable income for the year $118,000 ($68,000 þ $50,000).

In 2010, married taxpayers pay 10 percent on taxable income up to $16,750, 15 percent

on the next $51,250, and 25 percent on the next $69,300 of taxable income. What will be

their 2010 total tax liability assuming a tax of $9,363 on the $68,000 of ordinary income?

a. $9,363

b. $11,863

c. $16,863

d. $21,863

LO 8.3

6. Harold and Wanda (married filing jointly) have $30,000 ordinary income after the

standard deduction and personal exemptions, and $40,000 in unrecaptured

8-36 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

depreciation on the sale of rental property, for total taxable income of $70,000. For

2010, the 10 percent tax bra cket for married taxpayers filing jointly ends at $16,750,

the next $51,250 in taxable income is taxed at 15 percent, and 25 percent applies

to the next $69,300. What is Harold and Wanda’s tax? (Please use the percentages

given in this problem to calculate your answer.)

a. $7,315

b. $11,130

c. $9,863

d. $9,718

LO 8.3

7. In 2010, Tim, a single taxpayer, has ordinary income of $30,000. In addition, he has

$2,000 in short-term capital gains, long-term capital losses of $5,000, and long-term

capital gains of $4,000. What is Tim’s AGI for 2010?

a. $28,000

b. $30,000

c. $31,000

d. $32,000

LO 8.4

8. Which of the following is Section 1231 property?

a. A building used in a trade or business

b. Poultry used for egg production

c. Accounts receivable

d. Inventory

e. Paintings owned by the artist

LO 8.6

9. Pat sells real estate for $30,00 0 cash and a $120,000 5-year note. If her basis in the

property is $90,000 and she receives only the $30,000 down payment in the year of

sale, how much is Pat’s taxable gain in the year of sale using the installment sales

method?

a. $60,000

b. $30,000

c. $15,000

d. $12,000

e. $0

LO 8.6

10. Fred and Sarajane exchanged equipment in a qualifying like-kind exchange. Fred gives

up equipment with an adjusted basis of $14,000 (fair market value of $15,000) in

exchange for Sarajane’s equipment with a fair market value of $12,000 plus $3,000

cash. How much gain should Fred recognize on the exchange?

a. $3,000

b. $2,000

c. $1,000

d. $0

e. None of the above

LO 8.6

11. What is Sarajane’s basis in the equipment received in the exchange described in Ques-

tion 10, assuming her basis in the equipment given up was $12,000?

a. $0

b. $12,000

c. $14,000

d. $15,000

e. None of the above

Questions and Problems 8-37

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

LO 8.6

12. Oscar sells his residence of the last 10 years in January of 2010 for $190,000. Oscar’s

basis in the residence is $45,000, and his selling expenses are $11,000. If Oscar does

not buy a new residence, what is the taxable gain on the sale of his residence?

a. $145,000

b. $134,000

c. $45,000

d. $9,000

e. $0

LO 8.5

13. Virginia has a casualty gain of $5,000 and a casualty loss of $2,500, before reduction by

the $100 floor. The gain and loss were the result of two separate casualties, and both

properties were personal-u se assets. What is Virginia’s gain or loss as a result of these

casualties?

a. $5,000 capital gain and $2,500 capital loss

b. $5,000 capital gain and $2,400 itemized deduction, subject to the 10 percent of

adjusted gross income limitation

c. $5,000 capital gain and $2,500 itemized deduction, subject to the 10 percent of

adjusted gross income limitation

d. $5,000 capital gain and $2,400 capital loss

e. None of the above

LO 8.2

14. In 2010, Mary sells for $15,000 a machine used in her business. The property was pur-

chased on May 1, 2004, at a c ost of $12,500. Mary has claimed depreciation on the

machi ne of $4,750. What is the amount and natur e of Mary’s gain as a resu lt of the

sale of the machine?

a. $7,250 Section 1231 gain

b. $7,250 ordinary income under Section 1245

c. $2,500 ordinary income and $4,750 Section 1231 gain

d. $2,500 Section 1231 gain and $4,750 ordinary income under Section 1245

e. None of the above

LO 8.4

15. During 2010, Paul sells residential rental property for $300,000, which he acquired in

1992 for $150,000. Paul has claimed straight-line depreciation on the building of

$57,525. What is the amount and nature of Paul’s gain on the sale of the rental

property?

a. $207,525 Section 1231 gain

b. $150,000 Section 1231 gain, $57,525 ‘‘unrecaptured depreciation’’

c. $167,400 Section 1231 gain, $57,525 ordinary income

d. $190,125 Section 1231 gain, $17,400 ‘‘unrecaptured depreciation’’

e. None of the above

LO 8.4

16. Jeanie acquires an apartment building in 1991 for $260,000 and sells it for $500,000 in

2010. At the time of sale there is $78,000 of accumulated straight-line depreciation on

the apartment building. A ssuming Jeanie is in the highest tax bracket for ordinary

income, how much of her gain is taxed at 25 percent?

a. None

b. $240,000

c. $318,000

d. $162,000

e. $78,000

8-38 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.