Whittenburg Gerald E., Altus-Buller Martha. Income Tax Fundamentals

Подождите немного. Документ загружается.

LO 8.6

17. Jim, a single taxpayer, bought his home 20 years ago for $25,000. He has lived in the

home continuously since he purchased it. In 2010, he sells his home for $200,000.

What is Jim’s taxable gain on the sale?

a. $0

b. $50,000

c. $125,000

d. $175,000

LO 8.6

18. Susan, a single taxpayer, bought her hom e 25 years ago for $30,000. She has lived in

the home continuously since she purchased it. In 2010, she sells her home for

$300,000. What is Susan’s taxable gain on the sale?

a. $0

b. $20,000

c. $250,000

d. $270,000

LO 8.6

19. Kevin purchased a house 20 years ago for $100,000 and he has always lived in the

house. Three years ago Kevin married Karen, and she has lived in the house since

their marriage. If they sell Kevin’s house in December 2010 for $425,000, what is

their taxable gain on a joint tax return?

a. $0

b. $75,000

c. $125,000

d. $250,000

LO 8.6

20. Gene purchased a house 18 months ago for $350,000. If Gene sells his house due to

unforeseen circumstances for $550,000 after living in it for the full 18 months, what

is his taxable gain?

a. $0

b. $12,500

c. $50,000

d. $200,000

GROUP 2:

PROBLEMS

.............................................. .............................................. .

LO 8.1

LO 8.2

1. Martin sells a stock investment for $25,000 on August 2, 2010. Martin’s adjusted basis

in the stock is $14,000.

a. If Martin acquired the stock on November 15, 2009, calculate the amount and the

nature of the gain or loss.

$ ____________

b. If Martin had acquired the stock on September 11, 2008, calculate the amount and

nature of the gain or loss.

$ ____________

LO 8.2

LO 8.6

2. Elvin, 45 years of age, sells his residence in 2010. He receives $30,000 in cash, and the

buyer assumes his $105,000 mortgage. Elvin also pays $6,500 in commissions and

transfer costs.

a. Calculate the amount realized on the sale.

$ ____________

Questions and Problems 8-39

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

b. If the residence was acquired in 1986, and its adjusted basis is $75,000, calculate the

amount and nature of the taxable gain on the sale (assuming he does not purchase a

new residence).

$ ____________

LO 8.2 3. Jocasta owns an apartment complex that she purchased 6 years ago for $750,000. Jocasta

has made $40,000 of capital improvements on the complex, and her depreciation claimed

on the building to date is $150,000. Calculate Jocasta’s adjusted basis in the building.

$ ____________

LO 8.2 4. Chrissy receives 200 shares of Chevron Texaco stock as a gift from her father. The

stock cost her father $8,500 10 years ago and is worth $10,000 at the date of the gift.

a. If the stock is sold for $12,500, calculate the amount of the gain or loss on the sale.

$ ____________

b. If the stock is sold for $4,600, calculate the amount of the gain or loss on the sale.

$ ____________

LO 8.1

LO 8.2

LO 8.3

5. During 2010, Tom sold Sears stock for $10,000. The stock was purchased 4 years ago

for $13,000. Tom also sold Ford Motor Co. bonds for $35,000. The bonds were pur-

chased 2 months ago for $30,000. Home Depot stock, purchased 2 years ago for

$1,000, was so ld by Tom for $1,500. Calculate Tom’s net gain or loss, and indicate

the nature of the gain or loss.

$ ____________

LO 8.3 6. In 2010, Michael has net short-term capital losses of $2,0 00, a net long-term capital

loss of $45,000, and other ordinary taxable income of $45,000.

a. Calculate the amount of Michael’s deduction for capital losses for 2010.

$ ____________

b. Calculate the amount and nature of his capital loss carryforward.

$ ____________

c. For how long may Michael carry forward the unused loss?

____________

LO 8.1

LO 8.2

LO 8.3

7. Karim Depak has the following stock transactions during 2010:

Stock

Date

Purchased Date Sold

Sales

Price

Cost

Basis

4,000 shares Green Co. 06/04/02 08/05/10 $12,000 $ 4,000

500 shares Gold Co. 02/12/10 09/05/10 54,000 58,000

5,000 shares Blue Co. 02/04/03 10/08/10 18,000 22,000

None of the stock is qualified small business stock. Calculate Ka rim’s net capita l

gain or loss using Schedule D of Form 1040 on pages 8-41 and 8-42.

LO 8.2

LO 8.4

8. Frank Willingham has the following transactions during the year:

Sale of office equipment on March 15 that cost $20,000 when purchased on July 1,

2005. Frank has claimed $5,000 in depreciation and sells the asset for $13,000 with no

selling costs.

Sale of land on April 19 for $120,000. The land cost $130,000 when purchased on

February 1, 2002. Frank’s selling costs are $5,000.

Assume there were no capital improvements on either business asset sold.

Frank’s Social Security number is 924-56-5783. Complete Form 4797 on pages

8-43 and 8-44 to report the above gains or losses.

8-40 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Questions and Problems 8-41

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

8-42 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Questions and Problems 8-43

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

8-44 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

Questions and Problems 8-45

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

8-46 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

LO 8.2

LO 8.6

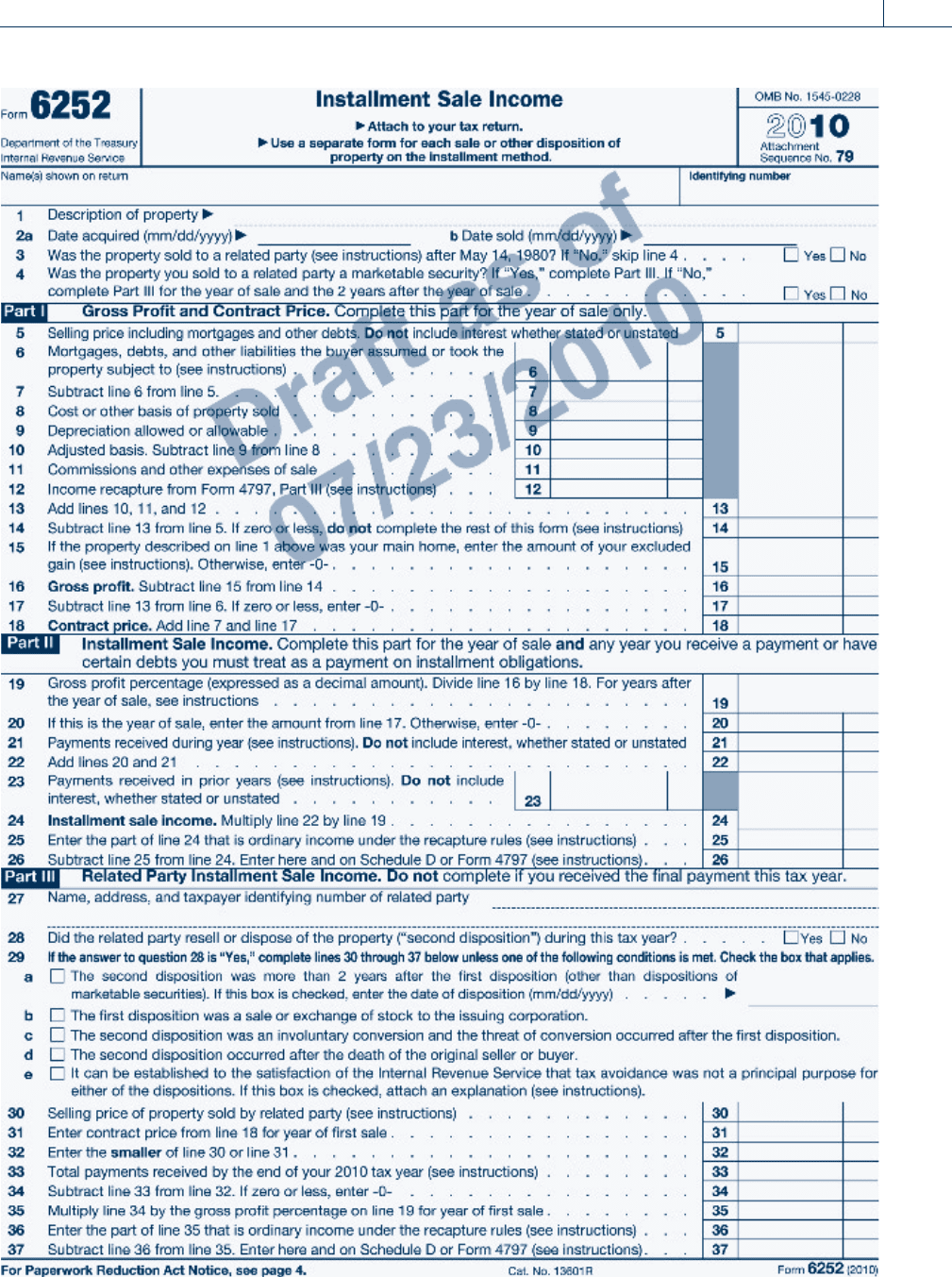

9. Steve Drake sells a rental house on January 1, 2010, and receives $130,000 cash and a

note for $55,000 at 10 percent interest. The purchaser also assumes the mortgage on

the property of $45,000. Steve’s adjusted basis in the house on the date of sale is

$152,500, and he collects only the $130,000 down payment in the year of sale.

a. If Steve elects to recognize the total gain on the property in the year of sale, calcu-

late the taxable gain.

$ ____________

b. Assuming Steve uses the installment sale method, complete Form 6252 on page 8-45

for the year of the sale.

c. Assuming Steve collects $5,000 (not including interest) of the note principal in the

year following the year of sale, calculate the amount of income recognized under

the installment sale method.

$ ____________

LO 8.6 10. Carey exchanges real estate for other real estate in a qualifying like-kind exchange.

Carey’s basis in the real estate given up is $110,000, and the property has a fair market

value of $170,000. In exchange for her property, Carey receives real estate with a fair

market value of $100,000 and cash of $20,000. In addition, the other party to the

exchange assumes a mortgage loan on Carey’s property of $50,000.

a. Calculate Carey’s recognized gain, if any, on the exchange.

$ ____________

b. Calculate Carey’s basis in the property received. $ ____________

LO 8.6 11. Teresa’s manufacturing plant is destroyed by fi re. The plant has an adjusted basis of

$260,000, and Teresa receives insurance proceeds of $400,000 for the loss. Teresa

reinvests $425,000 in a replacement plant.

a. Calculate Teresa’s recognized gain if she elects to utilize the involuntary conversion

provision. $ ____________

b. Calculate Teresa’s basis in the new plant. $ ____________

LO 8.2

LO 8.6

12. Larry Gaines, age 42, sells his personal residence on November 12, 2010, for $144,000. He

lived in the house for 7 years. The expenses of the sale are $10,500, and he has made capital

improvements of $5,500. Larry’s cost basis in his residence is $84,000. On November 30,

2010, Larry purchases and occupies a new residence at a cost of $148,000. Calculate Larry’s

realized gain, recognized gain, and the adjusted basis of his new residence.

a. Realized gain $ ____________

b. Recognized gain $ ____________

c. Adjusted basis of new residence $ ____________

LO 8.4 13. William sold Section 1245 property for $25,000 in 2010. The property cost $35,000 when

it was purchased 5 years ago. The depreciation claimed on the property was $16,000.

a. Calculate the adjusted basis of the property. $ ____________

b. Calculate the recomp uted basis of the property. $ ____________

c. Calculate the amount of ordinary income under Section 1245. $ ____________

d. Calculate the Section 1231 gain. $ ____________

LO 8.5 14. An office machine used by Josie in her accounting business was completely destroyed

by fire. The adjusted basis of the machine was $7,500 (original basis of $12,500 less

accumulated depreciation of $5,000). The machine was not insured. Calculate the

amount and nature of Josie’s gain or loss as a result of this casualty.

Amount of gain or loss $ __________ __

Nature ____________

Questions and Problems 8-47

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.

LO 8.5 15. Rebecca recognizes a $6,400 casualty loss, before any limitations, as a result of the

complete destruction of personal-use property. She also receives $1,200 of insurance

proceeds for the destruction of a second item of personal-use property which was dam-

aged in a separate casualty. The damaged property had a fair market value before the

casualty of $2,000 and after the casualty of $700 . The adjusted basis of the property

was $500. Determine the amount and nature of Rebecca’s gain or loss as a result of

these casualties.

Amount of gain or loss $ __________ __

Nature ____________

LO 8.6 16. On July 1, 2010, Ted, age 73 and single, sells his personal residence of the last 30 years

for $365,000. Ted’s basis in his residence is $35,000. The expenses associated with the

sale of his home total $20,000. On December 15, 2010, Ted purchases and occupies a

new residence at a cost of $175,000. Calculate Ted’s realized gain, recognized gain,

and the adjusted basis of his new residence.

Realized gain $ ____________

Recognized gain $ ____________

Adjusted basis of the new residence $ ____________

17. You have a problem and need a full-text copy of the Code Section 1033. Go to the U.S.

House of Representatives’ Web sit e (www.hou se.gov) and click on the ‘‘Acc ess the

United States Code’’ link. The Intern al Revenue Code is Title 26. Use the search

page to find Section 1033 and print out a copy of Se ction 1033(a), ‘‘General Rule.’’ Do

not print the entire Section 1033.

18. Go to the IRS Web site (www.irs.gov) and redo Problem 9 (Chapter 8, Group 2) using

the most recent interactive ‘‘Fill-in Forms’’ Form 6252, Installment Sale Income. Print

out the completed Form 6252.

GROUP 3:

COMPREHENSIVE PROBLEMS

.............................................. .............................................. .

1. Robert Ramos (age 36) is a single taxpayer, living at 8765 Bay Dr., Monterey, CA

93940. His Social Security number is 976-23-5132. Robert’s earnings and income

tax withhold ing as the manager of a local supermarket store for 2010 are:

Earnings from the Vons Market $68,000

Federal income tax withheld 14,800

State income tax withheld 2,300

Robert’s other income includes qualifying dividends on Arizona Public Service

stock of $3,600 and interest on a savings account at Bank of America of $5,885.

During the year, Robert paid the following amounts (all of which can be

substantiated):

Home mortgage interest $10,500

Credit card interest 550

Auto loan interest 1,700

8-48 Chapter 8

Capital Gains and Losses

Copyright 2010 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s).

Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.