Blank L., Tarquin A. Engineering Economy (McGraw-Hill Series in Industrial Engineering and Management)

Подождите немного. Документ загружается.

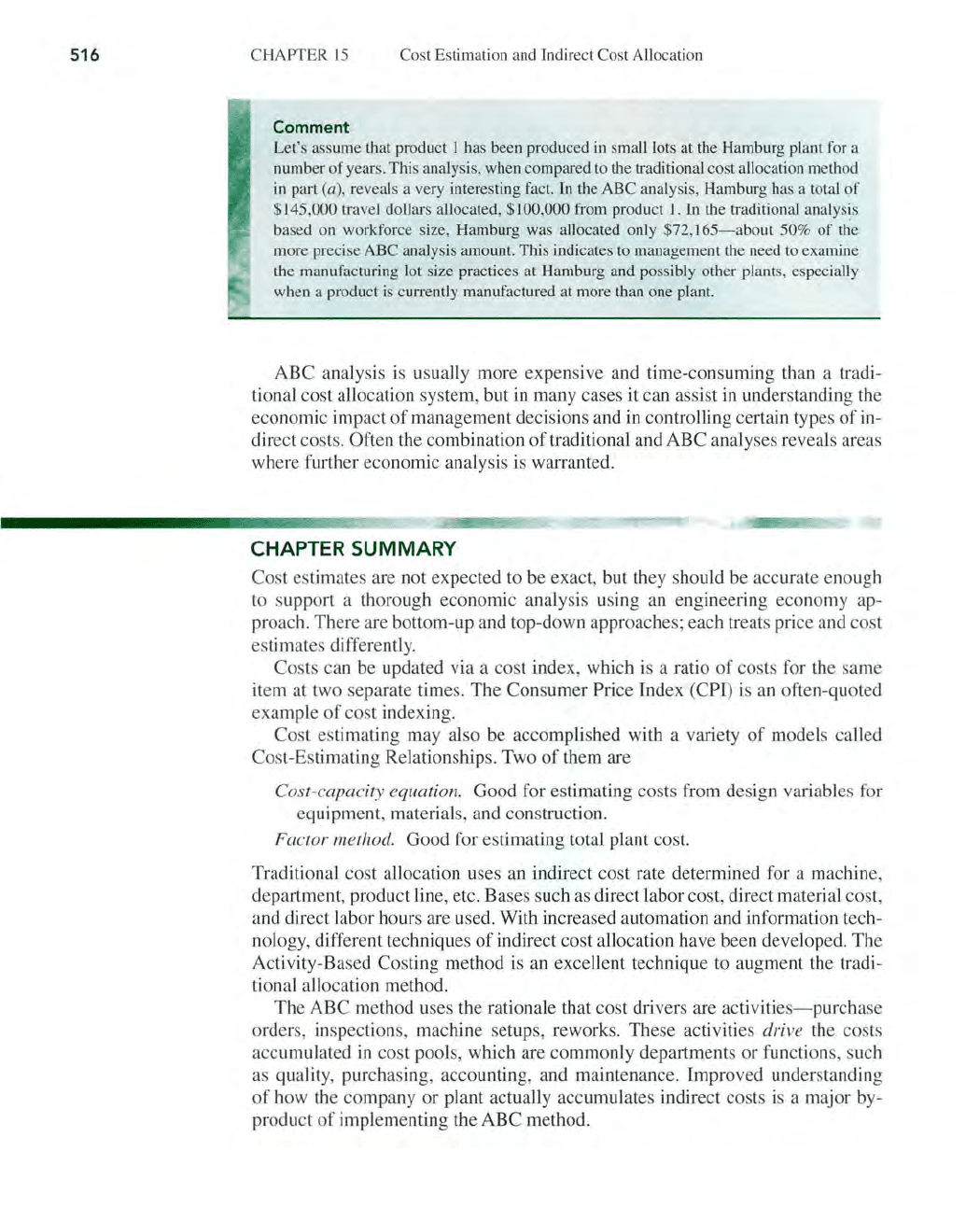

SECTION 15.6 Activity-Based Costing (ABC) for Indirect Costs

(b) The ABC method is more involved since it requires the definition

of

the cost

pool and

it

s size (step

I)

and the allocation

to

product lines using the cost driver

(step 2). The by-plant amounts will be different from those

in

part (a) since com-

pletely different bases are being applied.

Step

1. The cost pool is travel activity, and the size

of

the cost pool is deter-

mined from the percentages

of

each plant's support budget devoted

to

travel. Using the travel expense information in the problem state-

ment, a total cost pool

of

$500,000 is

to

be allocated

to

the five prod-

uct line

s.

This number

is

determined from the percent-of-budget data

as

follows:

0.05(2,000,000) +

...

+ 0.30(500,000) = $500,000

Step

2. The cost driver for the ABC method is the number

of

travel vouchers

submitted

by

the management unit responsible for each product line

at each plant. The allocation will be to the products directly, not

to

the plants. However, the travel allocation to the plants can be deter-

mined afterward since we know what product lines are produced at

each plant. For the cost driver

of

travel vouchers, the format

of

Equa-

tion [15.7] can be used to determine

an

ABC allocation rate.

total travel cost pool

ABC a

ll

ocation per travel voucher =

----------'---

total number

of

vonchers

$500,000

500

= $1000 per voucher

Table

15

- 7 summarizes the vouchers and allocation

by

product line

a

nd

by

city. Product 1 ($230,000) and product 5 ($170,000) drive the

travel costs based

on

the ABC analysis. Comparison

of

the by-plant

totals

in

Table

15-7

with the respective totals

in

part (a) indicates a

s

ub

stantial difference in the amounts allocated, especially to Paris,

Hamburg, and Athens. This comparison verifies the president's suspi-

cion that product lines, not plants, drive travel requirements.

TABLE

15-7

ABC Allocation

of

Travel Cost ($ in Thousands),

Example 15.10

Product

Line

2

3 4

5

Total

Paris 50 25

75

Florence

80 30 30 140

Hamburg

100

25

20

145

Athens

140 140

--

Total $230

$50 $30 $20 $170 $500

515

516

CHAPTER

15

Cost Estimation and Indirect Cost Allocation

Comment

Let's assume that product I has been produced

in

small lots at the Hamburg plant for a

number

of

years. This analysis, when compared to the traditional cost a

llo

cation method

in

part (a), reveals a very interesting fact. In the ABC analysis, Hamburg has a total

of

$145,000 travel dollars allocated, $100,000 from product

I.

In the traditional analysis

based on workforce size, Hamburg was allocated only $72,

165-about

50% of the

more precise ABC analysis amount. This indicates

to

management the need to examine

the manufacturing lot size practices at Hamburg and possibly other plants, especia

ll

y

when a product

is

currently manufactured at more than one plant.

ABC analysis

is

usually more expensive and time-consuming than a tradi-

tional cost allocation system, but in many cases it can assist in understanding the

economic impact

of

management decisions and in controlling certain types

of

in-

direct costs. Often the combination

of

traditional and ABC analyses reveals areas

where further economic analysis is warranted.

CHAPTER SUMMARY

Cost estimates are not expected to be exact, but they should be accurate enough

to support a thorough economic analysis using an engineeting economy ap-

proach. There are bottom-up and top-down approaches; each treats price and cost

estimates differently.

Costs can be updated via a cost index, which is a ratio

of

costs for the same

item at two separate times. The Consumer

Price Index (CPI) is an often-quoted

example

of

cost indexing.

Cost estimating may also be accomplished with a variety

of

models called

Cost-Estimating Relationships. Two

of

them are

Cost-capacity equ.ation. Good for estimating costs from design variables for

equipment, materials, and construction.

Factor method. Good for estimating total plant cost.

Traditional cost allocation uses an indirect cost rate determined for a machine,

department, product line, etc. Bases such

as

direct labor cost, direct material cost,

and direct labor hours are used. With increased automation and information tech-

nology, different techniques

of

indirect cost allocation have been developed. The

Activity-Based Costing method is an exce

ll

ent technique to augment the tradi-

tional allocation method.

The ABC method uses the rationale that cost drivers are

activities-purchase

orders, inspections, machine setups, reworks. These activities drive the costs

accumulated

in

cost pools, which are commonly departments or functions, such

as quality, purchasing, accounting, and maintenance. Improved understanding

of

how the company or plant actually accumulates indirect costs is a major by-

product

of

implementing the ABC method.

PROBLEMS

Cost Estimation Approaches

15.1 List three elements

of

the following

costs for a new computer integrated

manufacturing system.

(a) First cost

of

equipment

(b) AOC

15.2 Identify a primary difference between

the bottom-up and design-to-cost ap-

proaches to cost estimation.

15

.3 Identify each

of

the following costs as-

sociated with owning an automobile as

direct

or

indirect. Assume a direct cost

of

ownership

is

one that keeps the car in

your possession and running to provide

you transportation at the time that you

want

it.

If

you are undecided, state the

conditions under which the cost is direct

and indirect.

(a) Gasoline

(b) Highway toll fee

(c) Cost

of

repairs after a serious

collision

(d)

Annual inspection fee

(e)

Federal gasoline tax

(f)

Monthly loan payment

15.4 Estimate the cost

of

purchasing a subur-

ban

lot, constructing a house, and fur-

nishing the house, using the following

unit cost estimates:

Size

of

property: 100 X 150 feet

House approximate size: 6 rooms,

50 X

46

feet with 75% livable space

Price

of

property

in

the suburban area:

$2.50

per

square foot

Average cost

of

construction: $125 per

usable square foot

Furniture and appointments:

$3000 per

room

15

.5 Two people developed first-cut cost

estimates to construct a new

J

30

,000-

PROBLEMS

517

square-foot building on a university cam-

pus.

Person A applied a general-purpose

per unit cost estimate

of

$120 per square

foot for the estimate. Individual B was

more specific; she used the area estimates

and per unit cost factors shown below.

What

are the cost estimates developed by

the two people?

How

do they compare?

Percent

Cost

per

Type

of

Usage

of

Area

Square

Foot, $

Classroom

30

125

Laboratory

40

185

Offices

30

110

Furnishings-

labs

25

150

Furnishings-all

other

75

25

Cost Indexes

15

.6

The

cost

of

a standard cooling system

in

1995 was $78,000.

If

the M&S equip-

ment cost index applies, what will be the

estimated cost for a similar system when

the index

is

1200?

15.7

Use

the ENR construction cost index to

determine the cost

of

constructing a sec-

tion

of

highway similar to one built

in

1995 at a cost

of

$2.3 million. Use the

most current index value from the

ENR

website.

15.8

On the website containing the ENR con-

struction cost index (enr.construction.

com), two indexes are

reported-the

construction cost index and the building

cost index. Locate the section that ex-

plains their use and discuss the differ-

ence between the two indexes and under

what conditions each one is appropriate

to make cost estimates.

15

.9

If

the cost

of

a certain piece

of

equip-

ment was

$20,000 when the M&S index

was 915.1, what was the index value

518 CHAPTER

IS

Cost Estimation

and

Indirect Cost Allocation

when the

same

equipment was estimated

to cost

$30

,

000

?

15

.

10

(a) Estimate the value

of

the ENR con-

struction cost index for the year 2002 by

using the average (compound) percent-

age change

in

its value between 1990 and

2000 to predict the 2002 value. (b) How

much difference is there between the

estimated and historical

2002 values?

15.11 A particular type

of

labor

cost

index had

a value

of

720

in

1985 and 1315

in

2004.

If the labor cost for constructing a

building was $1.6 million

in

2004,

what

would the labor cost have been

in

1985?

15.12 Use the ENR construction cost index

(Table

15-2)

to update a cost

of

$325,000

in

1990 to a 2004 figure.

15.13 Chemical processing plant

equipment

was newly purchased

in

1998 at a

cost

of

$2

.5 million. Similar

equipment

was

purchased

in

1994 at another site and

again

in

2002

at a third site.

The

plant en-

gineer

wants to

know

the

compound

rate

of

cost

growth

over

the time span

of

the

three purchases.

Determine

this annual

rate.

The

CE

plant

cost

index applies.

15

.14 If a person makes 1990 the base year

with an index value equal to 100 for the

CE

plant cost index (Table

15-2),

what

is

the projected value

of

the index in

(a) 2002 and (b) current calendar month?

(Hint:

Use

the index website to find the

most current index value.)

15.

15

Determine the average (compound) per-

centage increase per year between 1990

and 2002 for the

CE

plant cost index.

15.16 Estimate the value

of

the

M&S

equip-

ment

cost

index

in

2005 if it was 1068.3

in

1999 and it increases by 2% per year.

15

.17 A mass spectrometer can be purchased for

$60,000 today.

The

owner

of

a mineral

analysis laboratory expects the cost to

increase exactly by the equipment

inflation rate over the next

10

years.

(a)

The

inflation rate

is

estimated to be

2% per year for the next 3 years and 5%

per year thereafter.

How

much will the

spectrometer cost

10

years from now

if

the

lab's

MARR

is 10% per year? (b)

If

the

appl icable equipment cost index is at 1203

now, what will it be

10

years from now?

Cost-Estimating Relationships

15.18

What

is the fundamental difference be-

tween estimating a cost using a

CER

and

a cost index?

15

.

19

The cost

of

a high-q uali

ty

250-horsepower

compressor was $] 3,000 when recently

purchased. What would

a450-

horsepower

compressor be expected to cost?

15.20 Janus Co. purchased a 100-horsepower

centrifugal pump and associated gear last

year for

$20

,000. Two additional pump

systems are needed at other plant sites,

one

rated at 200 horsepower and the

other at 75 horsepower. (a) Estimate the

cost

ofthe

two new pumps. (b)

If

the 200-

horsepower

pump

is delayed for 3 years,

estimate its future cost provided the cost

index is expected to rise 20% from its

current value

of

185

over

these years.

15.

21

The

cost for implementing a manufac-

turing process that has a capacity

of

6000 units

per

day was $550,000.

If

the

cost

for a plant with a capacity

of

100,000 units

per

day was $3 million,

what is the value

of

the exponent

in

the

cost-capacity equation?

15.22

The

estimated cost for a multitube cycl

one

system with a capacity

of

60,000 cubic

feet per minute is

$450,000. (a) [f the

$200,000 actual cost for a 35,000 cubic

feet per minute system was inserted into

the cost-capacity equation, what value

of

the exponent in the estimation equation

was used?

(b) What can be concluded

about the economy

of

scale

of

the costs

between the two systems?

15

.23 The cost for construction

of

a desulfuriza-

tion system for flue gas from utility boil-

ers at a 600-megawatt plant was estimated

to be

$250 million.

If

a smaller plant has a

costof$55

million and the exponent in the

cost-capacity equation is

0.67, what was

the size

of

the smaller plant that served

as

the basis for the cost projection?

15

.24

The

net annual operating cost for a filtra-

tion plant treating water for a semicon-

ductor fabrication line was estimated to

be $1.5 million

per

year. The estimate

was based on the

$200,000 per year cost

of

a I-MGD plant.

If

the exponent in the

cost-capacity equation is

0.80, what was

the size

of

the larger plant?

15

.

25

In the year 2002, new technology

IP

tele-

phony equipment was installed

atthe

IDS

Building headquarters at a total cost

of

$1

million. In the same year, an estimate

was made that a system with 3 times the

capacity would be needed

in

2 years, that

economies

of

scale and technological de-

velopment warranted a cost-capacity ex-

ponent

of

0.2, and that a 10% increase in

the cost index would be sufficient. In fact,

a 3

X capacity system was installed

in

2004 at a cost

of

$2 million, and the cost

index had gone up by 25%

in

stead

of

the

anticipated

10

%. (a) What is the differ-

ence between the estimate made in

2002

and the actual 2004 cost? (b) What value

of

the cost-capacity equation exponent

should have been used to correctly esti-

mate the actual $2 million cost?

15

.26 Estimate the cost in 2002

of

processing

equipment if the cost

of

a unit one-half

its size was

$50,000

in

1998.

The

expo-

nent

111

the cost-capacity equation

is

0.24. Use the tabulated CE plant cost

index to update the cost.

15.27 E timate the cost in

2002

of

a 1000-

horsepower steam turbine air compressor

if a 200-horsepower unit cost

$160,000

in

1995.

The

exponent

in

the cost-capacity

PROBLEMS

519

equation

is

0.35.

The

equipment cost

index increased by 35% between the two

years.

15

.28 In 1990, a 1O,000-square-meter facility

was constructed at a food processing

plant

in

Chicago for in-process handling

at a cost

of

$220,000. In 2002, an engi-

neer was asked to estimate the cost

of

a

similar structure, but for

5000 square

meters

in

a new plant in London. What

was the

2002 estimate

if

the six-tenths

model was applied?

15.29

The

equipment cost for phosphorus re-

moval from wastewater at a 50-MGD

plant will be $16 million.

If

the overall

cost factor for this type

of

plant

is

2.97,

what

is

the total plant cost expected

to be?

15

.30

The

delivered-equipment cost for a fab-

ric filter particulate collection system

is

$1.6 mjllion.

The

direct cost factor is

1.52, and the indirect cost factor

is

0.31 .

Estimate the total plant cost if the indi-

rect cost factor applies

(a) to delivered

equipment cost only and

(b) to the total

direct cost.

15.31 During major expansion

In

1994,

Douwalla' a Import Company developed

a new processing line for which the

delivered-equipment cost was $1.75 mil-

lion. Now,

11

years later, the board

of

directors has decided to expand into new

markets and expects to build the current

version

of

the same line. Estimate the

cost

if

the following factors are applica-

ble: Construction cost factor

is

0.20, in-

stallation cost factor is

0.50, indirect cost

factor applied against equipment is 0.25,

and the total plant cost index has risen

from 2509 to 3713 over the years.

15.32 Josephina

is

an engineer on temporary

assignment at a refining operation

111

Seaside. She has reviewed a cost esti-

mate for

$450,000, which covers some

520

CHAPTER

15

Cost Estimation and Indirect Cost

Al

location

new processing equipment for the ethyl-

ene line.

The

eq

ui

pment itself is estimated

at

$250,000 with a construction cost fac-

tor

of

0.30 and an insta

ll

ation cost factor

of

0.30. No indirect cost factor is listed,

but she knows from other sites that indi-

rect cost is a sizable amount that increases

the

total direct cost

of

the line's equip-

ment.

(a)

If

the indirect cost factor should

be

0.40, detennine whether the current es-

timate includes a factor comparable to

th

is val ue. ( b) Determi ne the cost estimate

if the

0.40 indirect cost factor

is

used.

Indir

ect Cost Allocation

15.33 Direct labor hours are used as the alloca-

tion basis for indirect costs per quarter. A

total amount

of

$450,000

is

to be allo-

cated at each plant

in

each quarter.

(a) Determine the indirect cost rates

for the Humboldt plant for each

quarter if each type

of

machining is

allocated

50%

of

the indirect cost.

(b) Determine the blanket rate for

Ql

for Humboldt. Calculate the

amount

of

indirect cost charged to

light machining only using this

blanket quarterly rate, and the

amount charged using the rate de-

termined in part

(a).

If

the rate that

is

sensitive to the type

of

machin-

ing

is

correct, by how much

is

light

machining overcharged or under-

charged when the blanket rate is

used?

(c) Determine the blanket indirect cost

rate for the Concourse plant for

each quart

er.

Machini

ng

Humboldt

Concourse

Direct

Labor

Hours

Qua

r

te

r Q1

Heavy

2000

1000

Light

800

800

Qua

r

ter

Q2

Heavy

1500

800

Light

1500

2000

15

.

34

A department has four processing lines,

each one considered a separate cost

center for indirect cost allocation pur-

poses. Machine operating hours are used

as

the allocation basis for all lines. A

total

of

$500,000 is allocated to the de-

partment for next year.

Use the data col-

lected this year to determine the indirect

cost rate for each line.

C

os

t Indir

ect

Cos

t

Estimate

d

C

ente

r

Allocat

ed

, $

Opera

t

in

g Hours

50,000 600

2 100,000 200

3

150,000

800

4 200,000 1200

15

.35 Dirk, the department manager

of

Chassis

Fabrication, has obtained from finance

and accounting the records that indicate

indirect cost allocation rates and the ac-

tual indirect charges for the prior 3 months

and their estimates for this month and

next month (September and October).

The

basis

of

allocation is not indicated.

The

finance and accounting manager

says there

is

no record

of

the basis used.

However, he tells Dirk to not be con-

cerned about the total allocation because

the rate is now constant at

$1

.25 a

nd

lower than previous rates.

I

nd

i

rect

Cos

t,

$

Mon

th

Rate

All

o

cate

d C

harge

d

June

1.50 20,000 22,000

July

1.33

34,000

38

,000

August 1.37

35

,000 35,000

September

1.25

36,000

October 1.25 36,250

During his evaluation, Dirk finds this ad-

ditional information from departmental

and accounting records.

Direct

Labor

Material

Dept

.

Space,

Month

Hours

Cost,

$

Cost,

$

Square

Feet

June 13,330

53,000 54,000 20,000

July 6,400

25,560

46,000

20,000

August

6,400 25,560

57.000

29

,000

September

6,400 27,200

63

,000 29,000

October

8,000 33,200

65

,000

29,000

(a)

For

each month, determine the allo-

cation basi

s,

and (b)

co

mment on the

statement

of

the finance and accounting

man

age

r that the rate is n

ow

constant

and lower than previous rates.

15.36 A manufacturer serving the sea transport

industry has five department

s.

Indirect

cost allocations for 1 month are detailed

below, along with space assigned, direct

labor hours, and direct labor costs for

each department that directly manufac-

tures rad

ar

and sonar equipment.

Actual

Data

for

1

Month

Indirect

Space,

Cost

Square

Direct

Labor

Department

Allocation, $

Feet

Hours

Cost,

$

Housing

20,000 10,000 480

31,680

Subassemblies 45,000 18,000

1,000

10

3,250

Final

assemb

ly

10

,000

10

,000 600

12,460

Test

in

g

15

,000 1,200

Engineering 19,000 2,000

Determine the ma

nuf

acturing depart-

ment a

ll

ocation rates for redistributing

th

e indir

ect

cost allocation for testing

a

nd

engineering ($34,000) to the

ot

her

departments.

Use

the following bases to

determine the rates: (a) space, (b) direct

labor hours, and (c) direct labor costs.

15.37

For

Problem

15

.3

6, determine the actual

indirect cost charges, us

in

g the rates de-

termined. For actual charges, use bases

of

dir

ect

labor hours for the hous

in

g a

nd

sub-

assemb

li

es departments and dir

ec

t labor

cost for the final assembly department.

15.38

PROBLEMS

521

Use the individual cost center rates

in

Problem

15

.3

4 to compute (a) the actual

indirect cost charges and a

ll

ocation var

i-

ances for each line and (b) the total for a

ll

lines.

The

actual hours credited to each

center are as follows: 1 has

700 hours;

2 has

350

hour

s;

3 has 650 hours; 4 has

1400 hour

s.

15.39 Indirect

cost

rates and bases for six pro-

ducing departments at Haycrow Indus-

tries are

li

sted below. (a)

Use

them to

distribute indir

ec

t

cost

s to the depart-

ments. (b)

Determine

the a

ll

ocat

ion

variance relative to a total indir

ect

cost

allocation

budget

of

$800,000.

Direct

Direct

Depart-

Allocation

Labor

Labor Machine

ment

Basis* Rate, $ Hours

Cost,

$

Hours

OLH

2.

50 5,000 20,000

3,500

2

MH

0.95 5,000

35

,000

25,000

3 OLe

1.

25

10

,500 44,

100

5,000

4 OLe 5.

75

12,000 84,000 40,000

5

OLe 3.45

10,200 54,700 10,200

6

DLH

0.75

19

,000

69

,000

60,500

*OLH = direct labor hour

s;

MH

= machine hours;

OLe

=

direct labor cos

t.

15.40 A new plant

manager

has b

ee

n assigned

to Haycrow Industries. This individual

has reviewed the information conta

in

ed

in the table

in

Problem 15.39 and deter-

mined that

it

is too complex to have more

than one indirect cost allocation basi

s.

The

sel

ec

ted basis is dir

ect

labor cost.

Therefore, for this year, the

si

mple

ave

r-

age

of

the

DLC

rates in departments 3, 4,

and 5 will be used to calculate actual

in

-

dir

ec

t charges. Determine the amount

of

charges for a

ll

six departments and the

total variance relative to the indirect cost

a

ll

ocation budget

of

$800,000.

15.41 Tocomo Industries serves the sea trans-

port industry. Indirect cost allocations for

1 month are detailed, along with space

assigned, direct labor hours, and dir

ect

522

CHAPTER

15

Cost Estimation and Indirect Cost Allocation

labor costs for the three departments that

directly manufacture radar and sonar

equipment. (For reference, this is the

same

information presented in Problem

15.36, but you do not need to have

worked it to complete this problem.)

In

direct

Cost

Actual

Data

for

1

Month

Space,

Direct

Labor

Square

De

partm

e

nt

Allocation, $

Feet

Hours

Cost,

$

Housing

20,000

10

,000 480

31

,680

Subassemblies

45,000

18

,000

1,000

103,250

Final assembly 10,000

10

,000

600

12,460

Te

sting

15,000 1,200

Engineering

19,000 2,000

The

company presently makes all the

components required by the housing de-

partment.

The

company

is

considering

buying rather than making these compo-

nents. An outside contractor has offered

to make the items for

$87,500 per month.

(a)

If

the costs for housing for the partic-

ular month shown are considered

good estimates for an engineering

economy study, and if$41

,000 worth

of

materials

is

charged to housing, do

a comparison

of

the make-versus-

buy alternatives. Assume that the

housing department's share

of

the

testing and engi neering departments'

costs is a

total

of

$3500 per month.

(b) A third alternative for the company

is

to purchase new equipment for the

housing department and continue to

make the components. The machin-

ery will cost

$375,

000

and will have

a 5-year life, no salvage value, and a

monthly operating cost

of

$5000.

This purchase

is

expected to re-

duce monthly costs in testing and

engineering by

$2000 and $3000,

respectively, and also reduce

monthly direct labor hours to

200

and monthly direct labor costs to

$20,000 for the housing department.

The

redistribution

of

the indirect

costs from testing and engineering

to the three production departments

is on the basis

of

direct labor hours.

If

other costs remain the same, com-

pare three costs: the present cost

of

making the components, the esti-

mated cost

if

the new equipment is

purchased, and the outside contrac-

tor cost. Select the most economic

alternative. A market

MARR

of

12 %

per year, compounded monthly, is

used for capital investments.

15.42 A corporation operates three plants in one

state. They all manufacture the same lines

of

precision and high-pressure fittings

of

a

wide variety for the oil, gas, and chemical

processing industries. The corporate of-

fices market and ship the finished products.

Additionally, the three sites share the same

support services for purchasing, comput-

ing, design engineering, process engineer-

ing, human resources, safety, and many

other functions, the costs for which are dis-

tributed annually to the three plants as an

indirect cost allocation. This allocation re-

duces the total plant income as determined

by the finance department.

One

ofthe

pli-

mary measures

of

performance for each

plant manager is the plant's net income

contribution to corporate income. There-

fore, the annual indirect cost allocation is a

direct reduction to the plant's bottom line.

For

the last 5 years a total

of

$10 mil-

lion

per

year has been allocated to the

three plants on the basis

of

direct labor

hours (DLH), which have the following

annual averages.

Pla

nt

A C

DLH per year 200,000 1,800,000

Employment and

DLH

have been rela-

tively constant over the 5-year period.

Therefore, the indirect cost allocation is

determined by using a rate known by

each plant manager.

I d

· total indirect costs

n (rect cost rate

= D

total

LH

$10 million

2.1

million

= $4.762

per

DLH

Hi

stor

ically, the oldest plant, A, has set the

standard for plant capacity per year.

It

is

500 units per day for each 200,000 direct

labor hours, which is exactly the capacity

of

plant

A.

Thus, at 250 days per work-

year, the capacity for each plant that is

used by the corporate office

is

as follows:

Plant

ABC

Capacity, units/year

1,125,000

The

manager

of

plant B has been diligent

about quality

improvement

, minimizing

scrap and rework, worker incentives, etc.

He

believes the standard

ofDLH

for indi-

rect allocation is not representative

of

plant B when

compared

with the statistics

for number shipped from plants A and C.

(a) Allocate the

$10

million indirect

cost on the basis

of

DLH

.

(b) Plant A manager has proposed that

a new blanket indir

ect

cost rate

using the basis

of

total output ca-

pacity

of

the corporation

in

units

per year be used. Determine this

rate and allocate the

$1

0 million in-

direct

cost

on this basis.

(c) Records indicate that the number

of

quality-checked units shipped in the

last 2 years has averaged 100,000

for plant A, 60,000 for B, and

900,000 for C. Plant B manager is

convinced his plant is, and will con-

tinue to be, allocated more indirect

cost than it should be,

in

part based

on the fact that plant B consistently

ships a higher percentage

of

its ca-

pacity than plants A and C.

He

will

propose that an incentive be devel-

oped to ship a number

of

quality-

checked units as close as possible

to the capacity

of

each plant.

The

PROBLEMS

523

allocation formula will use the rate

based on plant capacity from part (b)

but modified by a dimensionless

ratio that measures the actual output

relative to plant capacity.

Indirect cost allocation

(rate )(plant capacity)

actual output/plant capacity

Determine the allocation by plant

using this method, and compare it

with the allocated amounts deter-

mined by the previous two methods.

ABC Method

15.43

Use

Equation [15.7] and the bases listed

in

Table

15-4

to explain why a decrease

in direct labor hours, coupled with an

increase in indirect labor hours due to

automation on a production line, may

require the use

of

new bases to allocate

indirect costs.

15.44

If

the traditional method

of

indirect cost

allocation assists

in estimating the cost to

produce a unit

of

product, what does the

ABC

method often assist with concern-

ing the cost to produce a unit

of

product?

15.45 SNTTA Travel distributes food costs for its

four hotel sites in Europe based on the size

of

the budget.

For

this year, in round num-

bers, the budgets and allocation

of

$1

mil-

lion indirect costs for food are disuibuted

at the rate

of

10%

of

total hotel budget.

Site

A B

C D

Budget,

$ 2 million 3 million 4 million I million

Allocation,

$ 200,000 300,000 400,000 100,000

(a)

Use

the

ABC

allocation method

with a

cost

pool

of

$1

million

in

food costs.

The

activity is the num-

ber

of

guests during the year.

S~e

I A I B I C I D

Guests 3500 4000 8000 1000

524

CHAPTER

15

Cost Estimation and Indirect Cost Allocation

(b) Again use the ABC method, but

now the activity

is

the number

of

guest-nights. The average number

of

lodging-nights for guests at each

site

is

as follows:

Site D

Length

of

stay, nights 4.75

(c) Comment on the distribution

of

food costs, using the two methods.

Identify any other activities (cost

drivers) that might be considered for

the ABC approach that may reflect a

realistic allocation

of

indirect costs.

(d)

If

a new distribution scheme for the

$1

million total indirect cost is in-

stituted (that is, other than the

10%

of

total hotel budget), explain the

difference

it

will make in the final

actual amounts charged in parts

(a) and (b). Will it make a differ-

ence

in

the allocation variances if,

for example, the distribution is

30%

to budgets

of

$3 million or more

and only

20% to budgets

of

less

than $3 million per year?

15.46 Indirect costs are allocated each calen-

dar quarter to three processing lines,

using direct labor hours as the basis.

New automated equipment has de-

creased direct labor and the time to pro-

duce a unit significantly, so the di vision

manager plans to use cycle time

per

unit

produced as the basis. However, the

manager wants, initially, to determine

what the allocation would have been

had the cycle time been the basis prior

to the automation.

Use the data below

to determine the allocation rate and ac-

tual indirect charges for the three

different situations,

if

the amount to be

allocated in an average quarter is

$400,000.

Comment

on changes in the

amount

of

actual charged indirect cost

per processing line.

Processing Line

10

11

12

Direct labor hours

20,000 12,700

18

,600

per quarter

Cycle time per unit

3.9

17.0 24.8

now, seconds

Cycle time per unit

13

.0

55.8 28.5

previously, seconds

15.47 This problem consists

of

three parts that

build upon each other.

The

object is to

compare and comment upon the amount

of

indirect cost allocated to the electricity-

generating facilities located

in

two states

for the different situations described

in

each part.

(a) Historically,

Mesa

Power Author-

ity has allocated the indirect costs

associated with its employee safety

program to its plants in California

and Arizona based on the number

of

employees. Information to allo-

cate a

$200,200 budget for this

year follows:

State

California

Arizona

Workforce Size

900

500

(b) The head

of

the department

of

accounting recommends that the

traditional method be abandoned

and that activity-based costing be

used to allocate the

$200,200, using

expenditures on the safety program

as

the cost pool and the number

of

accidents as the activities which

dri ve the costs. Accident statistics

indicate the following for the year.

(c)

State

California

Arizona

Number

of

Accidents

425

135

Further study indicates that 80%

of

the safety program indirect costs

is

expended for employees

in

genera-

tion areas, and the remaining

20%