Blank L., Tarquin A. Engineering Economy (McGraw-Hill Series in Industrial Engineering and Management)

Подождите немного. Документ загружается.

SECTION 15.4

Cost Estimating Relationships: Factor Method

EXAMPLE

15.3

l'

The total design and construction cost for a digester to handle a flow rate

of

0

.5

million

gallons

per

day (MOD) was $1

.7

million in 2000. Estimate the cost today for a flow rate

of2.0

MOD. The exponent from Table

15-3

for the

MOD

range

of

0.2 to

40is

0.

14

.

The

cost index

in

2000

of

13l

ha

s been updated to 225 for this year.

Solution

Equation [15.2] estimates the

cost

of

the larger system in 2000, but it must be updated

by the cost ind

ex

to today

's

dollars. Equation

[J

5.3] perfonns both operations

at

once.

The estimated cost in current-value dollars is

c = 1 700

OOO(

2.0

)O

.1

4(

225 )

2 ' , 0.5

131

= 1,700,000(1.214)(1.718) = $3,546,178

15.4 COST ESTIMATING RELATIONSHIPS: FACTOR METHOD

Another widely used model for preliminary cost estimates

of

process plants is

called the

factor method. While the methods discussed above can be used to es-

timate the costs

of

major items

of

equipment, processes, and the total plant costs,

the factor method was developed specifically for total plant costs.

The

method

is

based on the premise that fairly reliable total plant costs can be obtained by

multiplying the cost

of

the major equipment by certain factors. Since major

equipment costs are readily available, rapid plant estimates are possible if the

appropriate factors are known. These factors are commonly referred to as Lang

factors after Hans

J.

Lang, who

fir

st proposed the method

in

1947.

In

its

si

mplest form, the factor method is expressed in the same form as the

unit method

[15.4]

where

C

T

= total plant cost

h = overall cost factor or sum

of

individual cost factors

C

E

= total cost

of

major equipment

The

h may be one overa

ll

cost factor or, more realistically, the sum

of

individual

cost components such as construction, maintenance, direct labor, materials, and

indirect cost elements. This follows the cost estimation approaches presented in

Figure

J

5-1.

In

hi

s original work, Lang showed that direct cost factors and indirect cost

factors can be combined into one overa

ll

factor for some types

of

plants as

follows: solid process plants, 3.

J 0; solid-fluid process plants, 3.63; and fluid

process plants, 4.74. These factors reveal that the total installed-plant cost is

many times the first cost

of

the major equipment.

505

506

CHAPTER

15

Cost Estimation and Indirect Cost Allocation

EXAMPLE

15.4

An engineer with Phillips Petroleum has learned that

an

expansion

of

the solid-fluid

process plant

is

expected to have a delivered equipment cost

of

$1.55 million.

If

the

overall cost factor for this type

of

plant

is

3.63, estimate the plant's total cost.

Solution

The total plant cost is estimated

by

Equation [15.4].

C

T

= 3

.6

3(1

,550,000)

= $5,626,500

Subsequent refinements

of

the factor method have led

to

the development

of

separate factors for direct and indirect cost components. Direct costs

as

discussed

in

Section

lS.l,

are specifically identifiable with a product, function, or process.

Indirect costs are not directly attributable

to

a single function, but are shared

by

several because they are necessary

to

perform the overall objective. Examples

of

indirect costs are general administration, computer services, quality, safety,

taxes, security, and a variety

of

support functions. The factors for both direct and

indirect costs are sometimes developed for use with delivered-equipment costs

and other times for installed-equipment costs. In this text, we assume that

all fac-

tors apply

to

delivered-equipment costs, unless otherwise specified.

For indirect costs, some

of

the factors apply to equipment costs only, while

others apply to the total direct cost. In the former case, the simplest procedure is

to

add the direct and indirect cost factors before multiplying

by

the delivered-

equipment cost. The overall cost factor

h.

can be written as

"

h.

= 1 + 'il;

[lS

.

S]

i= 1

where

I;

= factor for each cost component

i = 1

to

n components, including indirect cost

If

the indirect cost factor

is

applied to the total direct cost, only the direct cost

factors are added to obtain

h.

. Therefore, Equation [lS.4] is rewritten.

C

T

= l C

E

(

I +

~I;)

JO

+

J;)

[IS.6]

where

J;

= indirect cost factor

I;

= factors for direct cost components

Examples

IS.S

and IS.6 illustrate these equations.

EXAMPLE 15.5

~~

The delivered-equipment cost for a sma

ll

chemical process plant

is

expected to be

$2 million.

If

the direct cost factor is

1.61

a

nd

the indirect cost factor

is

0.25, determine

the total plant cost.

SECTION 15.4 Cost Estimating Rela

ti

onships: Factor Method

Solution

Since all factors apply

to

the delivered-equipment cost, they are added

to

obtain h, the

total cost factor

in

Eq

uation

lI5

.5

].

h = I +

1.61

+ 0.25 = 2.86

From Equation [15.4], the to

tal

plant cost is

C

T

= 2.86(2,000,000) = $5,720,000

EXAMPLE 15.6

An activated sludge wastewater treatment plant is expected

to

have the following

delivered-equipment

fir

st costs:

Equipment Cost

Prelimina

ry

tr

eat

ment

Primary treatment

Activated sludge

Clarification

Chlorination

Diges

ti

on

Vacuum

fi

ltration

Total cost

$30,000

40,000

18,000

57,000

31,000

70,000

27,000

$273,000

The

cost factor for the

in

sta

ll

ation

of

pip

in

g, concrete, steel, insulation, supports, etc., is

0.49.

The

con

st

ru

ction factor is 0.53, a

nd

the indirect cost factor

is

0.21 . Determine the

total plant cost

if

(a) all cost factors are app

li

ed

to

the cost

of

the delivered-equipment

and

(b)

th

e indirect cost factor is applied to the total direct cost.

Solution

(a) Total equipment cost is $273,000. Since both the direct and indirect cost

factors are applied

to

only the equipment cost, the overall cost factor from Equa-

tion [15.5] is

h = I + 0.49 + 0.53 + 0.21 = 2.23

The

total

pl

an

t cost is

C

r

= 2

.2

3(273,000) = $608,790

(b) Now the

tOlal

direct cost is calc

ul

ated first, and Equation [15.6] is used to esti-

mate the total plant cos

t.

"

h = 1 + IJ = 1 + 0.49 + 0.53 = 2.02

i= 1

C

T

= [273,000(2.02)](1.21) = $667,267

Comment

Note the decrease

in

estimated plant cost when the indirect cost is applied to the equip-

ment cost only

in

part (a). This illustrates the importance

of

determining exactly what

the factors apply

to

before they are used.

507

508

CHAPTER

15

Cost Estimation and Indirect Cost Allocation

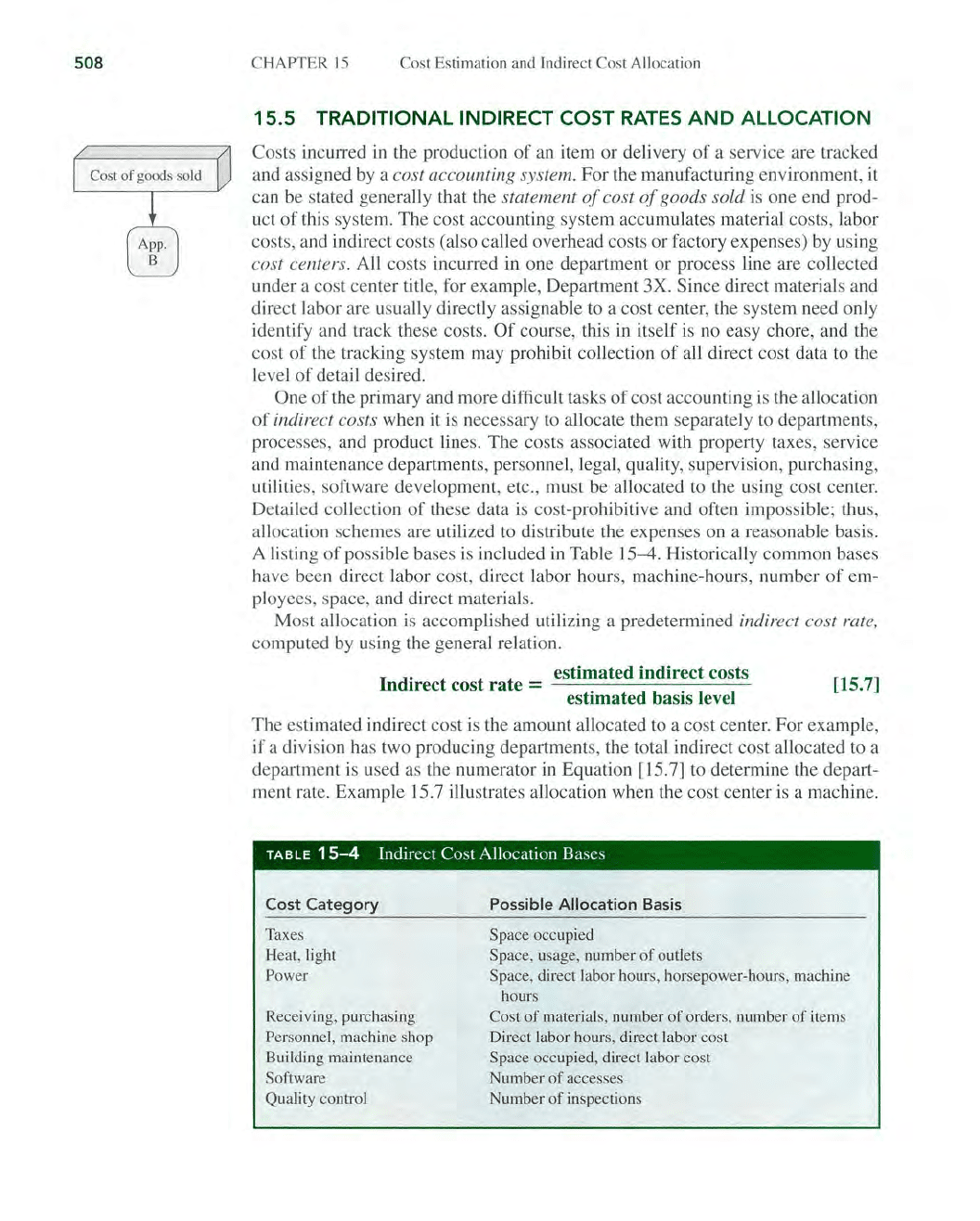

15.5 TRADITIONAL INDIRECT COST

RATES

AND

ALLOCATION

Costs incurred

in

the production

of

an item or delivery

of

a service are tracked

and assigned

by

a cost accounting system. For the manufacturing environment, it

can be stated generally that the

statement

of

cost

of

goods sold is one end prod-

uct

of

this system.

The

cost accounting system accumulates material costs, labor

costs, and indirect costs (also called overhead costs or factory expenses) by using

cost centers. All costs incurred in one department

or

process line are collected

under a cost center title, for

exam

ple, Department 3X. Since direct materials and

direct labor are usually directly assignable to a cost center, the system need only

identify and track these costs.

Of

course, this in itself is no easy chore, and the

cost

of

the tracking system may prohibit collection

of

all direct cost data

to th

e

level

of

detail desired.

One

of

the primary and more difficult tasks

of

cost accounting is the allocation

of

indirect costs when

it

is

necessary to allocate them separately to departments,

processes, and product lines. The costs associated with property taxes, service

and maintenance departments, personnel, legal, quality, supervision, purchasing,

utilities, software development, etc., must be allocated to the using cost center.

Detailed co

ll

ection

of

these data

is

cost-prohibitive and often impossible; thus,

allocation schemes are utilized to distribute the expenses on a reasonable basis.

A listing

of

possible bases is included

in

Table 15-4. Historically common bases

have been direct labor cost, direct labor hours, machine-hours, number

of

em-

ployees, space, and direct materials.

Most allocation is accomplished utilizing a predetermined

indirect cost rate,

computed by using the general relation.

I d

·

t t t estimated indirect costs

n lrec cos

ra

e =

estimated basis level

[15.7]

The

estimated indirect cost is the amount allocated to a cost center. For example,

if a division has two producing departments, the total indirect cost allocated to a

department

is

used as the numerator

in

Equation [15.7] to determine the depart-

ment rate. Example

15.7

illustrates allocation when the cost center is a machine.

TABLE

15-4

In

direct Cost A

ll

ocation Bases

Cost

Category

Taxes

Heat,

li

ght

Power

Receiving, purchasing

Personnel, machine shop

Building maintenance

Software

Quality control

Possible Allocation Basis

Space occupied

Space, usage, number

of

outlets

Space, direct labor hours, horsepower

-h

ours, machine

hOUTS

Cost

of

materials, number

of

orders, number

of

items

Direct labor hours, direct labor cost

Space occupied, direct labor cost

Number

of

accesses

Number

of

inspections

SECTION

15.5

Traditional Indirect Cost Rates and Allocation

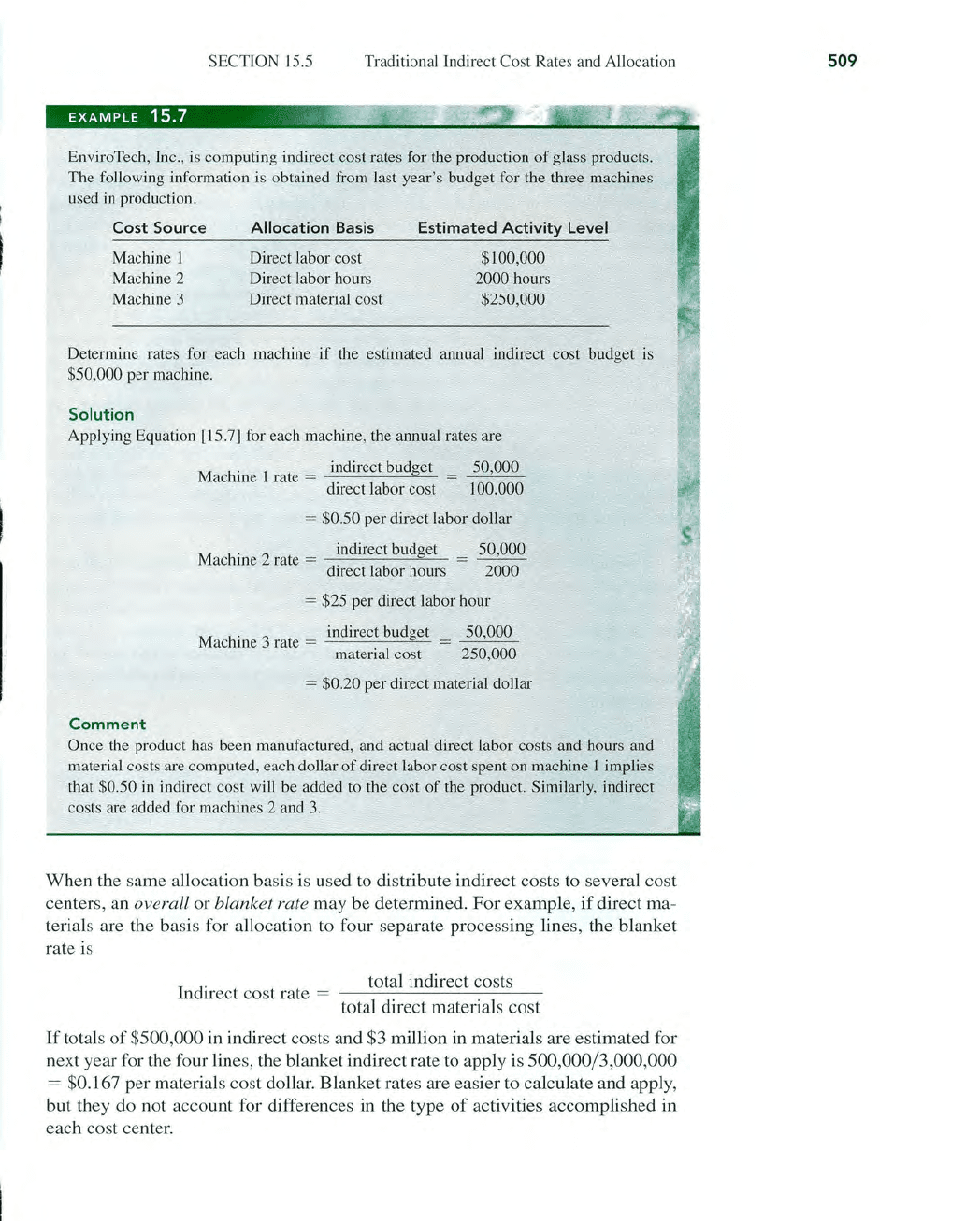

EXAMPLE

15.7

'1".

EnviroTech, Inc., is computing indirect cost rates for the production

of

glass products.

The following information is obtained from last year's bndget for the three machines

used

in

production.

Cost

Source

Allocation Basis

Estimated

Activity Level

Machine 1

Machine 2

Machine 3

Direct labor cost

Direct labor hours

Direct material cost

$100,000

2000

hours

$250,000

Determine rates for each machine

if

the estimated annual indirect cost budget is

$50,000

per

machine.

Solution

Applying Equation [15.7J for each machine, the annual rates are

Comment

M

h

· I

indirect budget

...:.

5...:.0,-",0..:..:00:.-

·

ac me rate = = -

direct labor cost 100,000

= $0.50 per direct labor dollar

M

h

·

2

_::ci

n:.:.;d

=i::.:r

e:...:c-,-t

..::.

b..::.u..::cdgQ.e:..:t_

ac me rate = .

dIrect labor hours

50,000

2000

=

$25

per direct labor hour

M

h

·

3 indirect

budgetS

,:...:0,-,-,0,,-0:...:0,-

ac me rate = = -

material cost 250,000

= $0.20 per direct material dollar

Once the product has been manufactured, and actual direct labor costs and hours and

material costs are computed, each dollar

of

direct labor cost spent on machine 1 implies

that

$0.50 in indirect cost will be added to the cost

of

the product. Similarly, indirect

costs are added for machines 2 and

3.

When the same allocation basis is used

to

distribute indirect costs to several cost

centers,

an

overall or blanket rate may be determined. For example, if direct ma-

terials are the basis for allocation

to

four separate processing lines, the blanket

rate is

Indirect cost rate

=

total indirect costs

total direct materials cost

If

totals

of

$500,000

in

indirect costs and

$3

million in materials are estimated for

next year for the four lines, the blanket indirect rate

to

apply

is

500,000/3,000,000

= $0.167 per materials cost dollar. Blanket rates are easier

to

calculate and apply,

but they do not account for differences in the type

of

activities accomplished in

each cost center.

509

510

CHAPTER

15

Cost Estimation and Indirect Cost Allocation

In most cases, machinery or processes add value to the end product at differ-

ent rates per unit or hour

of

use. For example, light machinery may contribute

less per hour than heavy, more expensive machinery. This

is

especially true when

advanced technology processing, for example, an automated manufacturing cell

is used along with traditional methods, for example, nonautomated finishing

equipment.

The

use

of

blanket or overall rates in these cases is not recommended

as the indirect cost will be incorrectly allocated.

The

lower-value-contribution

machinery will accumulate too much

of

the indirect cost.

The

approach to indi-

rect cost a

ll

ocation should be the application

of

different bases for different ma-

chines, activities, etc

.,

as

discussed earlier and illustrated in Example 15.7.

The

LIse

of

different, appropriate bases is often called the productive hour rate method

since the cost rate is determined based on the value added, not a uniform

or

blanket rate. Realization that more than one basis should be normally used

in

allocating indirect costs has led to the use

of

activity-based costing methods, as

di

scussed

in

the next section.

Once a period

of

time (month, quarter, or year) has passed, the indirect

cost rates are applied to determine the indirect cost

charge, which

is

then

added to direct costs. This results in the total cost

of

production, which is called

the cost

of

goods sold, or factory cost.

The

se costs are all accumulated by cost

center.

If

the total indirect cost budget is correct, the indirect costs charged to all cost

centers for the period

of

time should equal this budget amount. However, since

some

etTor in budgeting always exists, there will be overallocation or underallo-

cation relative to actual charges, which is termed

allocation variance. Experi-

ence

in

indirect cost estimation assists in reducing the variance at the end

of

th

e

accounting period. Example

15

.8

illustrates indirect cost allocation and variance

computation.

EXAM

PLE

15.8

~.,'

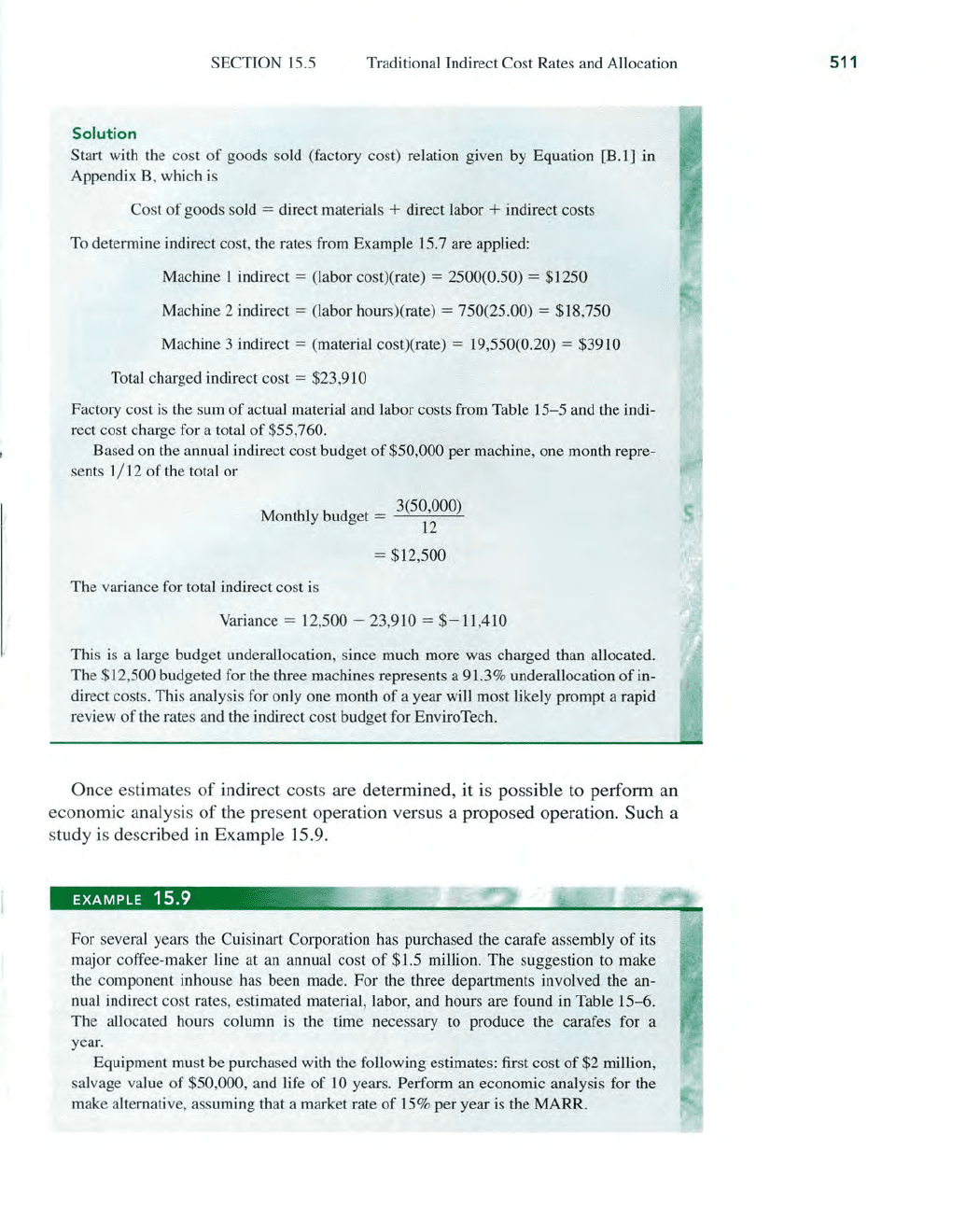

Since we determjned indirect cost rates for EnviroTech (Example 15.7), we can now

compute the total factory cost for a month.

Perform the computations using the data

in

Table 15-5. Also calculate the variance for indirect cost allocation for the month.

TABLE

15-5

Ac

tu

al Monthly Data 'Used for

In

direct Cost A

ll

ocation

Cost

So

u

rce

Mach

ine

Numbe

r A

ctual

C

os

t

Actu

al

Hours

Material

I $3,800

3

19

,550

Labor

1 2,500

650

2 3,200 750

3 2,800 720

SECTION 15.5 Traditional Indirect Cost Ra

te

s a

nd

Allocation

Solution

Start with the cost

of

goods so

ld

(factory cost) relation given

by

Equation [B.l] in

Appendix B, which is

Cost

of

goods so

ld

= direct mate

ri

als + direct labor + indirect costs

To

determine indirect cost, the rates from Example 15.7 are applied:

Mac

hin

e 1 indirect = (labor cost)(rate) = 2500(0.50) = $1250

Machine 2 indirect = (labor hours)(rate) = 750(25.00) = $18,750

Machine 3 indirect

= (material cost)(rate) = 19,550(0.20) = $3910

Total charged indirect cost

= $23,910

Factory cost is the sum

of

actual material and labor costs from Table

15

- 5 and the indi-

rect cost charge for a total

of

$55,760.

Ba

se

d

on

the annual indirect cost budget

of

$50,000 per machine, one month repre-

sents 1/

12

of

the total or

M thl b d

3(50,000)

on

y u get =

12

= $12,500

The variance for total indirect cost is

Variance

= 12,500 -

23

,910 =

$-11,410

This is a large budget underallocation, since much more was charged than allocated.

The

$12,500 budgeted for the three machines represents a 91.3% underallocation

of

in-

direct costs. T

hi

s analysis for only one month

of

a year will most likely prompt a rapid

review

of

th

e rates and the indirect cost budget for EnviroTech.

Once estimates

of

indirect costs are determined, it is possible to perform an

economic analysis

of

the present operation versus a proposed operation. Such a

study

is

described

in

Example

15

.

9.

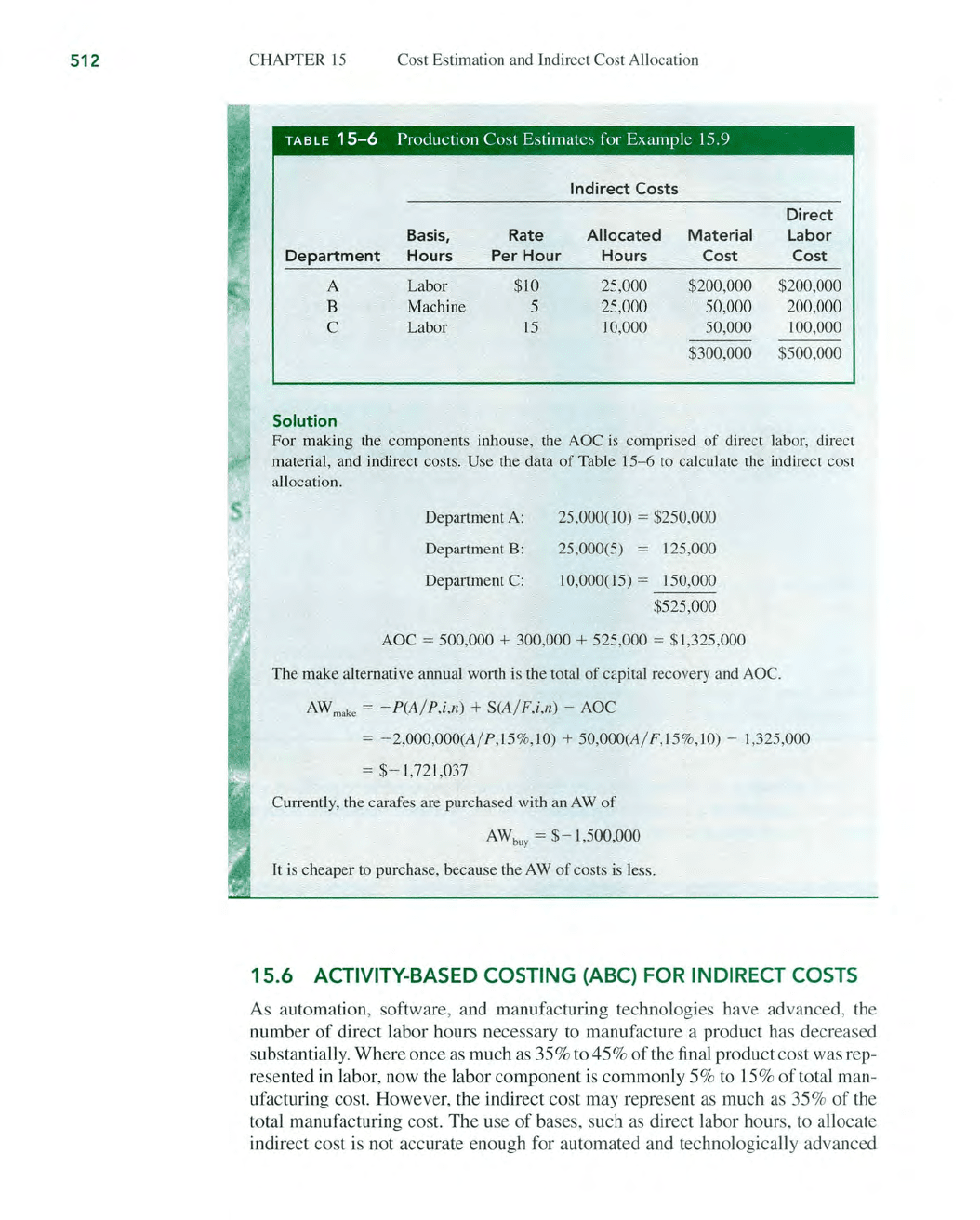

EXAMPLE

15.9

':.~'

For several yea

rs

the Cuisinart Corporation has purchased the carafe assembly

of

its

major coffee-maker line at

an

annual cost

of

$1.5 million. The suggestion

to

make

the compone

nt

inhouse has been made. For the three departments involved the an-

nu

al indirect cost rate

s,

estimated material, labor, and hours are found in Table 15-6.

The a

ll

ocated hours column is the time necessary

to

produce the carafes for a

yea

r.

Equipment must be purchased with the following estimates:

fir

st cost

of

$2 million,

salvage

va

lue of

$5

0,000, a

nd

life

of

10

years. Perform an economic analysis for the

make alternative, assuming that a market rate

of

15

% per year is the MARR.

511

512

CHAPTER

15

Cost Estimation a

nd

Indirect Cost

All

oca

ti

on

TABLE

15-6

Production Cost Estimates for Example 15.9

Indirect

Costs

Direct

Basis, Rate Allocated Material Labor

Department

Hours

Per

Hour Hours

Cost

Cost

A

Labor

$10

25,000 $200,000 $200,000

B

Machine 5 25,000 50,000 200,000

C

Labor

15

10,000 50,000

100

,000

$300,000

$500,000

Solution

For making the components inhouse, the AOC is comprised of direct labor, direct

material, and indirect costs. Use the data

of

Table 15-6

to

calculate the indirect cost

allocation.

Department

A:

Department B:

Department

C:

25

,000(10) = $250,000

25

,000(

5)

=

125

,000

10

,000(15) = 150,000

$525,000

AOC

= 500,000 + 300,000 + 525,000 =

$1

,325,000

The make alternative annual worth is the total

of

capital recovery a

nd

AOC.

AW

make

=

-P(A

/ P,i,n) +

S(A

/ F,i,n) - AOC

= -2,000,000(A/ P,l5%

,1O)

+ 50,000(A/ F,

15

%

,LO

) - 1,325,000

= $- 1,

721

,037

Currently, the carafes are purchased with an

AW

of

AW

buy

= $- 1,500,000

It is cheaper

to

purchase, because the

AW

of

costs is less.

15.6 ACTIVITY-BASED

COS

TING (ABC)

FOR

INDIRECT

COSTS

As automation, software, and manufacturing technologies have advanced, the

number

of

direct labor hours necessary to manufacture a product has decreased

substantially. Where once as much as 35% to 45%

of

the final product cost was rep-

resented in labor, now the labor component is commonly 5% to

15

%

of

total man-

ufacturing cost.

However

, the indirect cost may represent as much as 35%

of

the

total manufacturing cos

t.

The

use

of

base

s,

such as direct labor hour

s,

to allocate

indirect cost is not accurate enough for automated and technologica

ll

y advanced

SECTlON

15.

6 Activity-Based Costing (ABC) for Indirect Costs

environment

s.

This has led

to

the development

of

methods that supplement tradi-

tional cost allocations that rely upon one form or another

of

Equation [15.7]. Also,

allocation bases different from traditional ones are commonly utilized.

It is important from an engineering economy viewpoint to realize when tradi-

tional indirect cost allocation systems should be augmented with better method

s.

A product

th

at by traditional methods may have contributed a large portion to

profit may actually be a loser when indirect costs are allocated more correctly.

Compa

ni

es that have a wide variety

of

products and produce some

in

small lots

may find that traditional allocation methods have a tendency to underallocate the

indirect cost

to

small-lot products. This may indicate that they are profitable,

when

in

ac

tu

ality they are los

in

g money. Additionally, the productive hour rate

method, which uses different allocation bases dependent on the value added per

hour

of

operation, should be used, as discussed in Section 15.5.

An augmentation technique for indirect cost allocation

is

Activity-Based Cost-

ing,

or

ABC

for short. By design, its goal is to develop a cost center, called a cost

pool,

for each event, or activity, which acts

as

a cost driver. In other words, cost

drive

rs

actually drive the consumption

of

a shared resource and are charged

according

ly

. Cost pools are usually departments or

functions-purchasing,

in-

spection, maintenance, and information technology. Activities are events such

as

purchase orders, reworks, repairs, software activations, machine setups, material

movement, wait time, and engineering changes.

Some proponents

of

the ABC method recommend discarding the traditional

cost accounting methods

of

a company a

nd

utilizing

ABC

exclusively. This is not

a good approach, since ABC is not a complete cost system.

The

ABC method

provides in

fo

rmation that assists

in

cost control, while the traditional method em-

phasizes cost allocation and cost estimation.

The

two systems work well together

with the traditional methods allocating costs that have identifiable direct bases,

for example, direct labor.

The

ABC method can then be utilized to further allo-

cate support service costs us

in

g activity bases such as those mentioned above.

The ABC me

th

odology involves a two-step process:

1. Define cost pools. Usually these

are

support

functions.

2. Identify cost drivers. These help trace costs to the cost pools.

As an illustration, a company which produces an industrial laser has three pri-

mary support departments identified

as

cost pools

in

step

1:

A,

B, and

C.

The

annual support cost for the purchasing cost driver (step 2)

is

allocated to these

departments based on the number

of

purchase orders each department issues to

support its laser production functions. Example 15.10 illustrates the process

of

applying activity-based costing.

EXAMPLE

15.10

,'/

A multinational aerospace firm uses traditional methods to allocate manufacturing and

management support costs for its European division. However, accounts such

as

busi-

ne

ss travel have

hi

storically been allocated on the basis

of

the number

of

employees at

the plants

in

France, Italy, Germany, a

nd

Greece.

513

514

CHAPTER

15

Cost Estimation and Indirect Cost Allocation

The president recently stated that some product lines are likely generating much

more management travel than other

s.

The ABC system

is

chosen

to

augment the tradi-

tional method

to

more precisely allocate travel costs

to

major product lines at each pla

nt.

(a) First, assume that allocation of total observed travel expenses

of

$500,000

to

the

plants using a traditional basis

of

workforce size is sufficient.

If

total employ-

ment

of

29,100

is

distributed as follows, allocate the $500,000.

Paris,

France plant 12,500 employees

Florence, Italy plant

8,600 employees

Hamburg, Germany plant

Athen

s,

Greece plant

4,200 employees

3,800 employees

(b) Now, assume that corporate management wants

to

know more about travel expenses

based

on

product line, not merely plant location and workforce size. The ABC

method will be applied

to

allocate travel costs

to

major product lines. Annual plant

support budgets indicate that the following percentages are expended for travel:

Paris 5%

of

$2 million

Florence 15%

of

$500,000

Hamburg

Athens

17.5%

of

$1

million

30%

of

$500,000

Further, the study indicates that in 1 year a total

of

500 travel vouchers were

processed

by

the management

of

the major five product lines produced at the

four plant

s.

The distribution

is

as

follows:

Paris. Product lines

-l

and 2; number

of

vouchers-50

for line I, 25

for 2.

Florence. Product

lines-I

, 3, and 5; vouchers-

80

for line 1

,3

0 for 3, 30

for

5.

Hamburg. Product lines- I, 2 and 4; vouchers

-lOO

for Ii

ne

1,

25

for 2, 20

for 4.

Athens.

Product

line-5

;

vouchers-140

for line

5.

Use the ABC method to determine how the product lines drive travel costs at the

pl

ants.

Solution

(a) Equation [15.7] takes the form

of

a blanket ra

te

per employee.

travel budget

Indirect cost rate

= f

total work orce

$500,000

29,100 = $17.1821 per employee

Using this traditional basis

of

rate times workforce size results in a plant-by-

plant allocation.

Paris:

Florence:

Hamburg:

Athens:

$

17

.1821(12,500) =

$21

4,777

$147,766

$72,165

$65,292