Blank L., Tarquin A. Engineering Economy (McGraw-Hill Series in Industrial Engineering and Management)

Подождите немного. Документ загружается.

LEARNING OBJECTIVES

Purpose:

Make

cost estimates and include

the

dimension

of

indirect cost allocation

in

an

engineering economy study.

Approaches

Cost indexes

Cost-capacity equations

Factor

method

Indirect cost rates and allocation

ABC allocation

This

chapter

will

help you learn

to

:

1.

Describe different

approaches

to

cost

estimation.

2. Use a

cost

index

to

estimate

present

cost

based

on

historic

data.

3.

Estimate

the

cost

of

a

component,

system,

or

plant

by using

a cost-capacity

equation

.

4. Estimate

total plant

cost

using

the

factor

method.

5. Allocate indirect

costs

using traditional indirect

cost

rates.

6.

Allocate indirect

costs

using

the

Activity-Based

Costing

(ABC)

method

.

496

CHAPTER

15

Cost

Estimation and Indirect

Cost

Allocation

15.1 UNDERSTANDING

HOW

COST ESTIMATION

IS

ACCOMPLISHED

Cost estimation

is

a major activity performed

in

the initial stages

of

virtually every

effort

in

industry, business, and government.

In

general, most cost estimates are

developed for eith

er

a project

or

a system; however, combinations

of

these are

very common. A project usually involves physical items, such as a building,

bridge, manufacturing plant, and offshore drilling platform, to name

just

a few. A

system

is

usually an operational design that involves processes, software, and

other nonphysical items. Examples might be a purchase order system, a software

package, and an Internet-based remote-control system. Additionally the cost esti-

mates are usually made for the initial development

of

the project

or

system, with

the life-cycle costs

of

maintenance and upgrade estimated as a percentage

of

first

cost.

Of

course, many projects will have major elements that are not physical, so

esti mates

of

both types

must

be

developed.

For

example, consider a computer net-

work system.

There

would be no operational system

if

only the computer hard-

ware plus wire and wireless connectors were estimated; it is equally important to

estimate the software, personnel, and maintenance costs.

Much

of

the discussion

that follows concentrates on physical-based projects. However, the logic

is

widely

applicable to cost estimation for project and system designs.

Thus far virtually all cash flow estimates

in

the examples, problems, and exer-

cises

of

this text were stated

or

assumed to

beknown.

In

real-world practice, the cash

flows for costs and revenues must be estimated prior to the evaluation

of

a project

or

comparison

of

alternatives. We concentrate on cost estimation because costs are the

primary values estimated for the economic analysis. Revenue estimates utilized by

eng

in

eers are usually developed in marketing, sales, and other departments.

Costs are comprised

of

direct costs and indirect costs. Normally direct costs

are estimated with some detail, then the indirect costs are added using standard

rates and factors. However, direct costs in many industries, including manufac-

turing and assembly settings, have

become

a small percentage

of

overall product

cost, while indirect costs have become much larger. Accordingly, many industrial

settings require

some

estimating for indirect costs as well. Indirect cost alloca-

tion

is

discussed

in

detail in later sections

of

this chapter. Primarily, direct costs

are discussed here.

Because cost estimation is a complex activity, the following questions form a

structure for

our

discussion.

•

•

•

What cost components must be estimated?

What approach to cost estimation will be applied?

How accurate should the estimates be?

What

estimation techniques will be utilized?

Costs to Estimate

If

a project revolves around a single piece

of

equipment, for

example, an industrial robot, the cost components will be signifi

cant

ly

simpler

and fewer than the

co

mponents for a complete system such as the manufacturing

a

nd

testing line for a new product. Therefore, it

is

important to know up front how

much the cost estima

ti

on task will involve. Examples

of

cost components are the

SECTION

15.1

Understanding How Cost Estimation Is Accomplished

first cost P and the annual operating cost (AOC), also

ca

lled the

M&O

costs (main-

tenance and operat

in

g)

of

equipment. Each

component

will have several cost ele-

ments, some that are directly estimated, others that require examination

of

records

of

similar projects, and sti

ll

others that must be modeled using an estimation tech-

nique. Listed below are sample elements

of

the first cost and AOC components.

First cost component

P:

Elements:

Equipment

cost

Del i very charges

Installation cost

Insurance coverage

Initial training

of

personnel for equipment use

Delivered-equipment cost

is

the sum

of

the first two elements; installed-equipment

cost adds the third element. Capital recovery (CR) for the first cost is determined

using the

MARR

and the

AI

P factor over the estimated life

of

the equipment.

AOe

component, a part

of

the equivalent annual cost

A:

Elements: Direct labor cost for operating personnel

Direct materials

Maintenance (daily, periodic, repairs, etc.)

Rework and rebuild

Some

of

these elements, such as equipment cost, can be determined with high

accuracy; others, such as maintenance costs, are harder to estimate. When costs for

an entire system must be estimated, the number

of

cost components and elements

is likely to be

in

the hundreds.

It

is then necessary to prioritize the estimation tasks.

For familiar projects (houses, office buildings, highways, and some chemical

plants) there are standard cost estimation packages available

in

paper or software

form. For example, state highway departments utilize software packages that

prompt for the correct

cost

components (bridges, pavement, cut-and-fill profiles,

etc.) and estimate costs with time-proven, built-in relations. Once these compo-

nents are estimated, exceptions for the specific project are added. However, there

are no "canned" software packages for a large percentage

of

industrial, business,

and public sector cost estimation jobs.

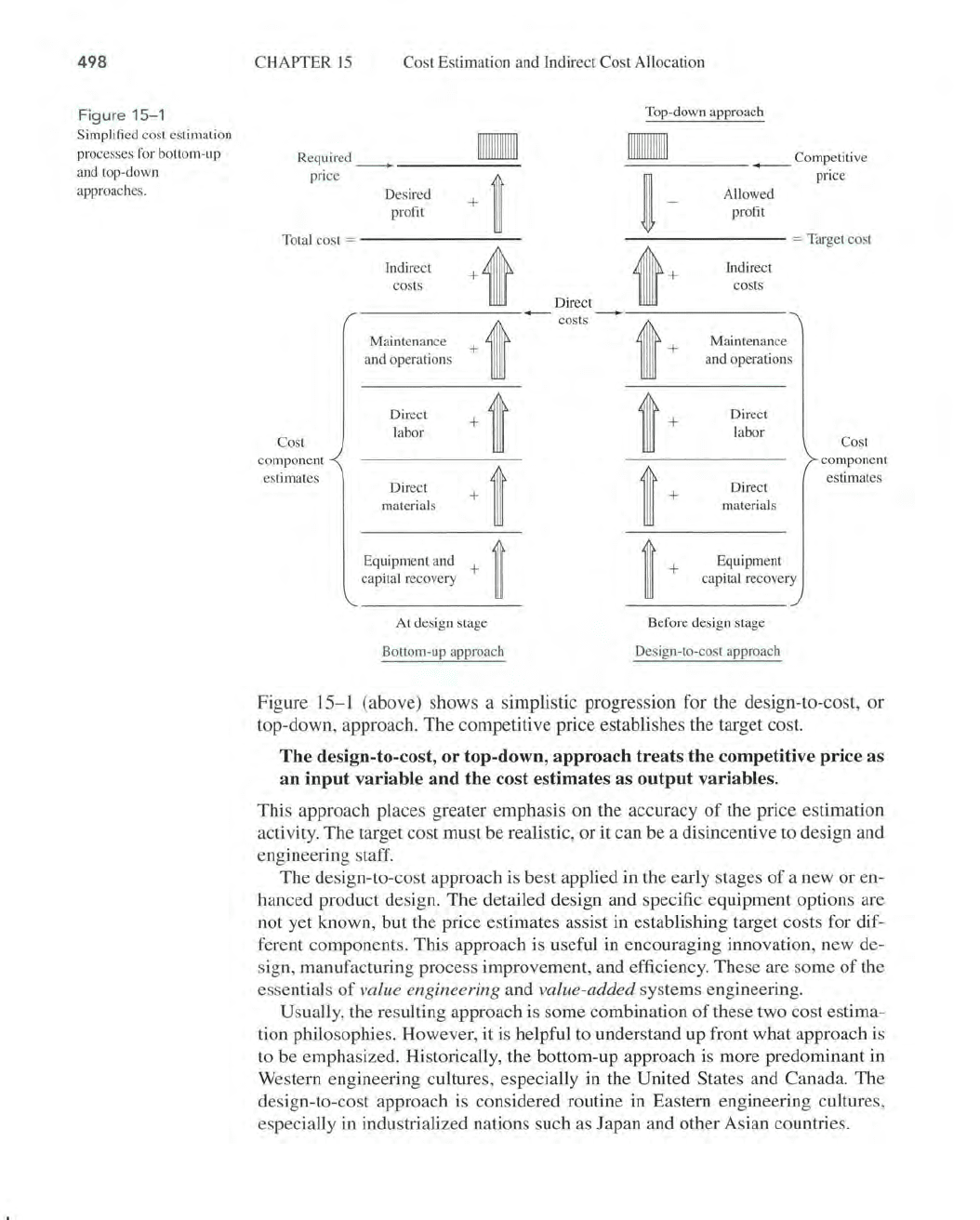

Cost Estimation Approach Traditionally

in

industry, business, and the public

sector, a "bottom-up" approach to cost estimation is applied.

For

a simple rendi-

tion

of

this approach, see Figure 15-1 (left).

The

progression

is

as follows: cost

components and their elements are identified, cost elements are estimated, and

estimates are summed to obtain total direct cost.

The

price

is

then determined by

adding indirect costs and the profit margin, which is usually a percentage

of

the

total cost. This approach works we

ll

when competition

is

not the dominant fac-

tor

in

pricing the product

or

service.

The

bottom-up

approach

treats

the

required

price

as

an

output

variable

and

the

cost

estimates

as

input

variables.

497

498

Figure 15-1

Simplified cost estimation

processes for bottom-

up

and top-down

approaches.

CHAPTER 15 Cost Estimation and Indirect Cost Allocation

Top-down approach

Require

d_

•

•

_ Competitive

pnce

i

~

price

Desired

+

-

A

ll

owed

profit

profit

Total cost

=

=

Target cost

In

direct

+it

it+

Indirect

costs

costs

Direct

~

costs

Maintenance

+t

t+

Maintenance

and operations a

nd

opera

ti

ons

Direct

+t

t+

Direct

labor

labor

Cost

Cost

compone

nt

t t

compone

nt

estimates

Direct

estimates

Direct

+ +

mate

ri

als

materials

Equipment a

nd

capital recove

ry

+

~ ~

+

Equipment

cap

it

al recove

ry

At design stage

Before design stage

Bo

tt

om-up approach

Design-to-cost approach

Figure

15

- 1 (above) shows a simplistic progression for the design-to-cost, or

top-down, approach. The competitive price establishes the target cost.

The

design-to-cost,

or

top-down,

approach

treats the competitive price as

an

input

variable

and

the cost estimates as

output

variables.

This approach places greater emphasis on the accuracy

of

the price estimation

activity. The target cost

mu

st be rea

li

stic, or it can be a disincentive

to

design and

engineering staff.

The design-to-cost approach is best applied in the early stages

of

a new or en-

hanced product design. The detailed design and specific equipment options are

not yet known, but the price estimates assist in establishing target costs for

di

f-

ferent components. This approach

is

useful in encouraging innovation, new de-

sign, manufacturing process improvement, and efficiency. These are some

of

the

essentials

of

va

lue engineering and value-add

ed

systems engineering.

Usually, the resulting approach is some combination

of

these two cost estima-

tion philosophies. However, it is helpful

to

understand up front what approach is

to

be emphasized. Historically, the bottom-up approach is more predominant

in

Western engineering cultures, especially in the United States and Canada. The

design-to-cost approach is considered routine in Eastern engineering cultures,

especia

ll

y

in

industria

li

zed nations such

as

Japan and other Asian countries.

SECTION 15.2 Cost Indexes

Accuracy

oj

the Estimates No cost estimates are expected to be exact; how-

ever, they are expected to be reasonable and accurate enough to support eco-

nomic scrutiny.

The

accuracy required increases as the project progresses from

preliminary design to detailed design and on to

economic

evaluation. Cost esti-

mates made before and during the preliminary design stage are expected to be

good "first-cut" esti

mates

that serve as input to the project budget. Estimation

techniques, such as the unit method, are applicable at this stage.

The

unit method

is

a popular, very pre]jminary estimation technique.

The

total

estimated cost

is

obtained by multiplying the number

of

units by a per unit cost

factor. Sample cost factors are

Cost

of

automobile operation per mile, including fuel, insurance, wear and

tear (e.g., 34.5 cents per mile)

Cost

of

house construction per livable square foot (e.g.,

$150

per square foot)

Cost

of

buried electrical cable per mile

Cost per parking space in a parking garage

Cost

of

constructing a standard-width suburban street

per

mile

Instances

of

the unit method are evident

in

everyday business activities.

If

house

construction costs average

$150

per square foot, a pre]jminary

cost

estimate for

a 2000-square-foot

home

is $300,000.

If

car

travel is expensed at $0.345 per

mile, a 200-mile business trip should cost approximately

$70

for the car.

When utilized at early and conceptual design stages, the estimates above are

often referred to as order-oJ-magni tude estimates. At the detai led design stage, cost

estimates are expected to be accurate enough to support economic evaluation for a

go-no go decision. Every project setting has its own characteristics, but a range on

estimates

of

::!:::5%

to::!:::

15%

of

actual costs

is

expected at the detailed design stage.

Cost Estimation Techniques

Methods

such as expert opinion and comparison

with comparable installations serve as excellent estimators.

The

use

of

cost in-

dexes bases the present

cost

estimate on past cost experiences, with inflation

considered. Models such as cost-capacity equations and the Jactor method are

simple mathematical techniques applied at the preliminary design stage.

These

cost-estimating relationships (eER) are presented in the following sections.

There are many additional methods discussed

in

the handbooks and pub]jcations

of

different industry and business sectors.

15.2

COST INDEXES

A cost index

is

a ratio

of

the cost

of

something today to its cost sometime in the past.

As such, the index

is

a dimensionless number that shows the relative cost change

over time.

One

such index that most people are familiar with is the Consumer Price

Index (CPI), which shows the relationship between present and past costs for many

of

the things that "typical" consumers must buy. This index includes such items as

rent, food, transportation, and certain services.

Other indexes track the costs

of

equipment, and goods and services that are more pertinent to the engineering dis-

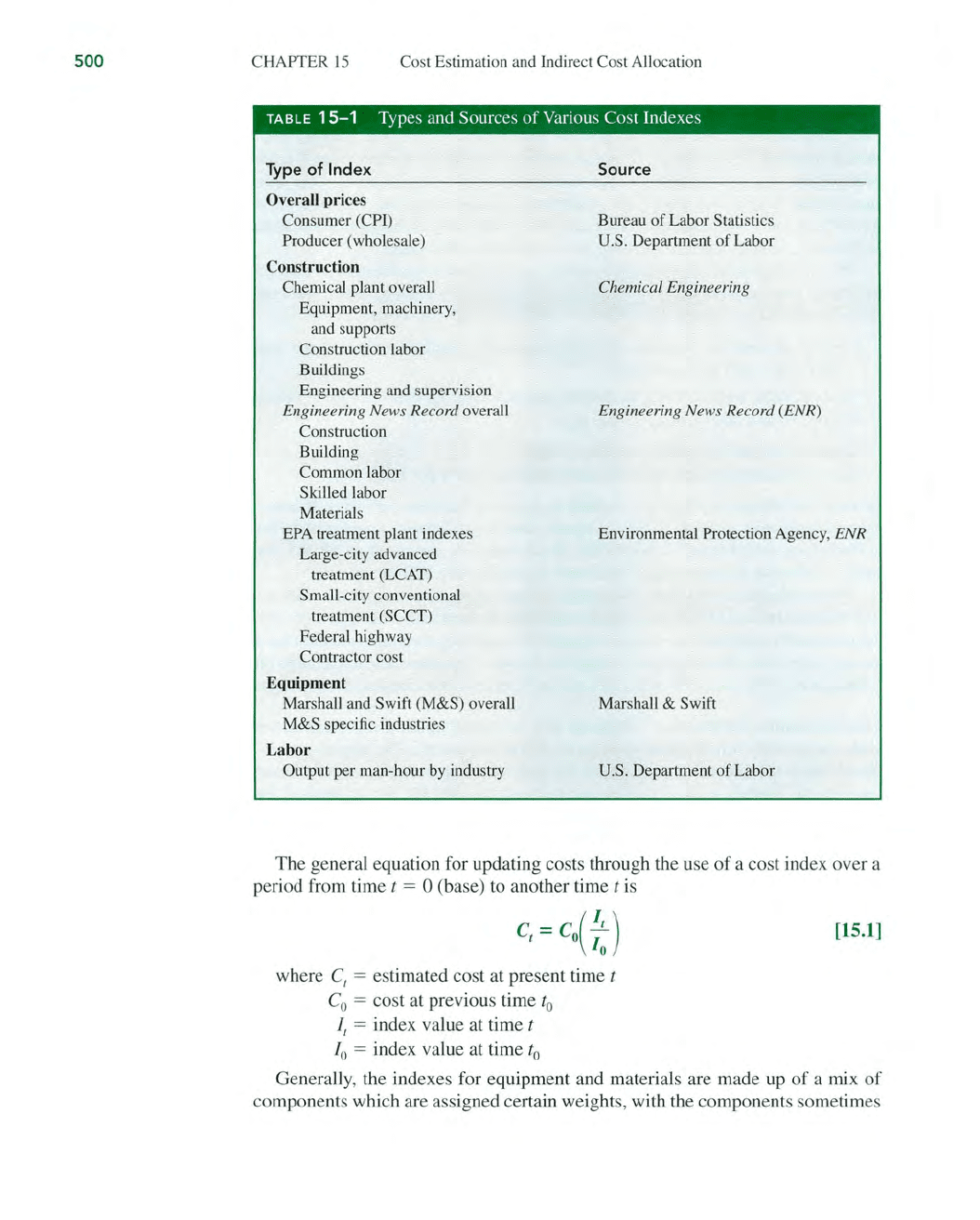

ciplines. Table 15-1

is

a listing

of

some

of

the more common indexes.

499

500

CHAPTER

15

Cost Estimation and Indirect Cost Allocation

TABLE

15-1

Types and Sources

of

Various Cost Indexes

Type of Index

Overa

ll

prices

Consumer (CPI)

Producer (wholesale)

Construction

Chemical plant overall

Equipment, machinery,

and supports

Construction labor

Buildings

Engineering and supervision

Engineering News Record overall

Construction

Building

Common labor

Skilled labor

Materials

Source

Bureau

of

Labor Statistics

U.S. Department

of

Labor

Chemical Engineering

Engineering News Record (ENR)

EPA treatment plant indexes

Large-city advanced

treatment (LCAT)

Small-city conventional

treatment

(SCCT)

Federal highway

Contractor cost

Environmental Protection Agency, ENR

Eq

ui

pment

Marshall and Swift (M&S) overall

M&S specific industries

Labor

Output per man-hour by industry

Marshall &

Swift

U.S.

Department

of

Labor

The general equation for updating costs through the use

of

a cost index over a

period from time

t = 0 (base) to another time

tis

C = C

(~)

t 0 I

o

[15.1]

where C, = estimated cost at present time t

Co = cost at previous time

to

I, = index value at time t

10

= index value at time

to

Generally, the indexes for equipment and materials are made up

of

a mix

of

components which are assigned certain weights, with the components sometimes

SECTION

15

.2

Cost I

nd

exes

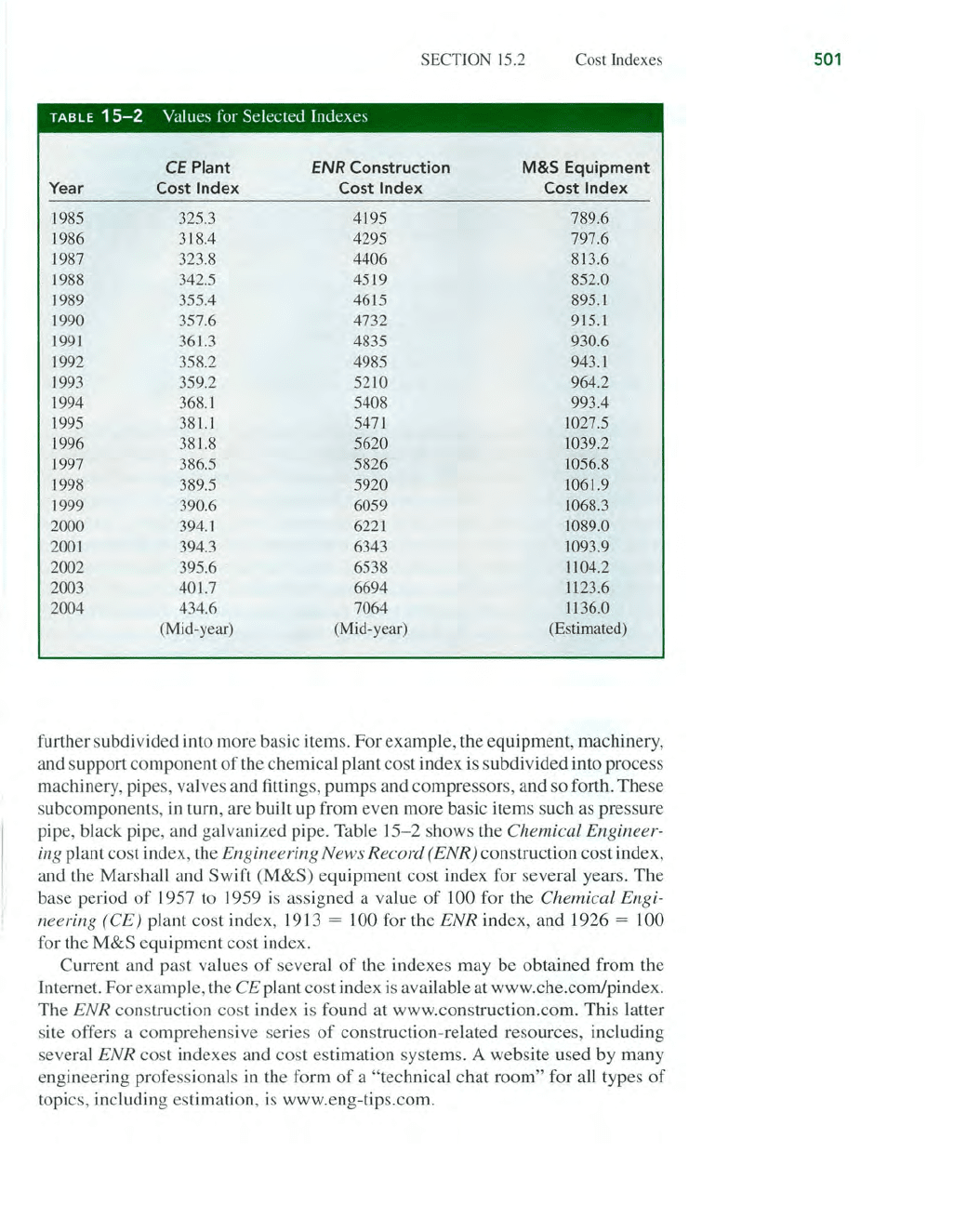

TABLE

15-2

Va

lu

es

fo

r Selected Indexes

CE

Plant

ENR

Construction

M&S

Equi

pment

Year Cost Index Cost Index Cost Index

1985

325.3 41

95

789.6

1986 318.4 4295 797.6

1987 323.8 4406

813.6

1988

342.5 4519 852.0

1989

355.4 4615 895.1

1990

357.6 4732 915.1

1991

361

.3

4835 930.6

199

2 358.2 4985 943.1

J993 359.2 5210

964.2

1994 368.1 5408

993.4

1995 381.l 5471

1027.5

1996 381.8

5620 1039.2

1997 386.5

5826 1056.8

J998 389.5

5920 106

1.

9

1999

390.6

6059

1068.3

2000 394.1 6221 1089.0

2001 394.3 6343 1093.9

2002 395.6 6538

1104.2

2003

40

1.

7 6694

1123.6

2004 434.6 7064

1136.0

(Mid-year) (Mid-year)

(Estimated)

further subdi vided into more basic item

s.

For

example, the equipment, machinery,

and support

co

mponent

ofthe

chemical plant

cost

index is subdi vided into process

machinery, pipes, va

lv

es and fittings,

pump

s and compressors, and so forth.

The

se

sub

co

mponents,

in

turn, are built up from even more basic items such as pressure

pipe, black pipe, and galvanized pipe. Table

15-2

shows the Chemical Engineer-

ing

plant

cost

index, the Engineering News Record (ENR) construction cost index,

and

th

e Marshall and Swift (M&S)

equipment

cost index for several year

s.

The

base period

of

1957 to 1959 is assigned a value

of

100 for the Chemical Engi-

neering (CE)

plant cost index, 1913 = 100 for the

ENR

index, and 1926 = 100

for the

M&S

equipment cost index.

Current and past values

of

several

of

the indexes

may

be

obta

ined from the

Internet.

For

example, the

CE

plant cost index is available at www.che.comJpindex.

The

EN

R

co

nstru

ct

ion cost index is found at

www.construction.com.This

latt

er

site offers a

co

mprehensive series

of

construction-related resources, including

several

ENR

cost indexes and cost estimation system

s.

A website used by many

en

gi

n

ee

ring professionals in the form

of

a "technical

chat

room" for all types

of

topics, including estimation, is www.eng-tips.com.

501

502

CHAPTER

15

Cost Estimation and Indirect Cost Allocation

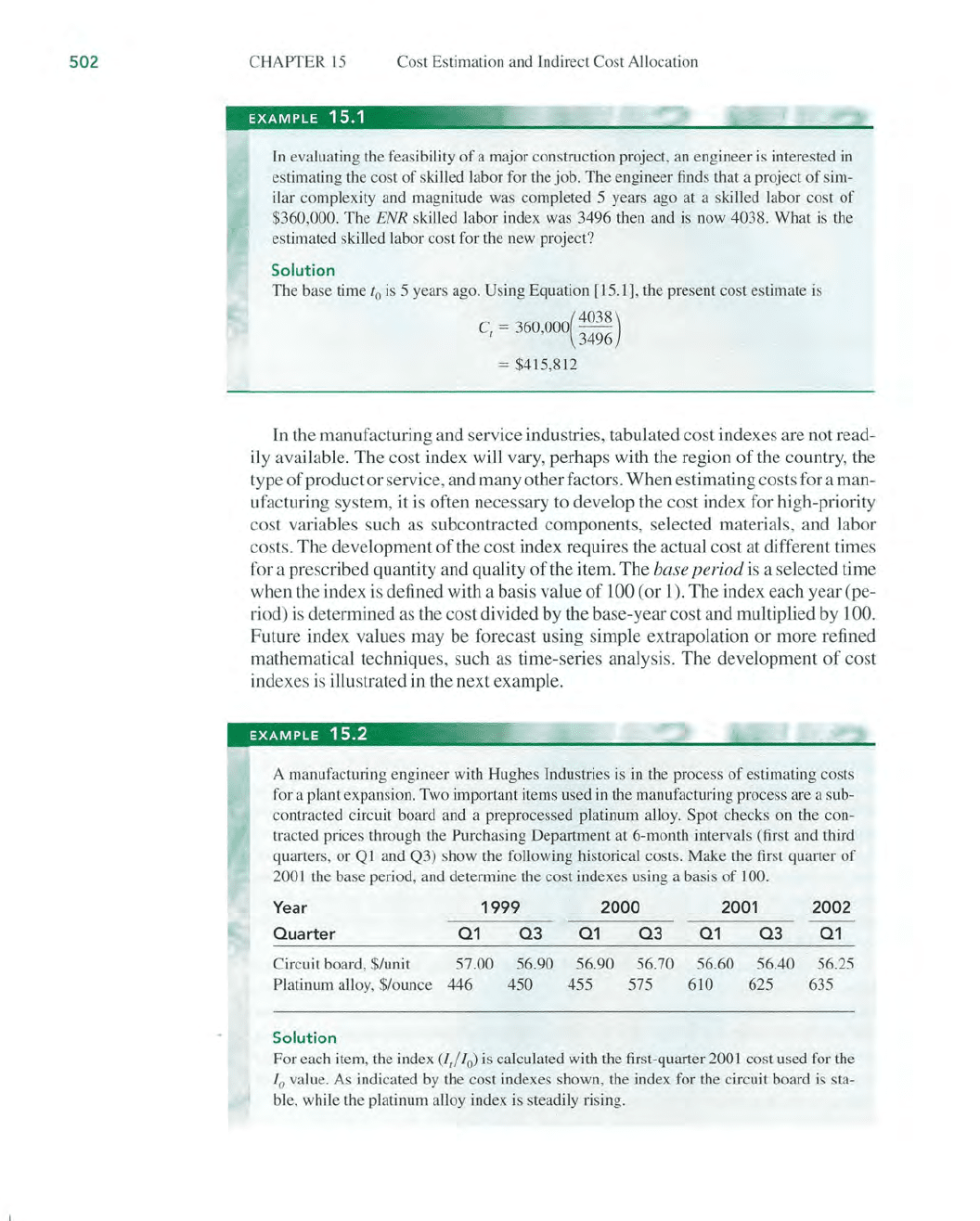

In

eva

lu

ating the feasibility

of

a major construction project, an engineer

is

interested

in

estimating the cost

of

skilled labor for the job.

The

engineer finds that a project

of

sim-

ilar complexity and magnitude was completed 5 years ago at a skilled labor cost

of

$360,000.

The

ENR

skilled labor index was 3496 then and

is

now 4038. What

is

the

estimated skilled labor cost for the new project?

Solution

The

base time 10

is

5 years ago. Using Equation [J5.1], the present cost estimate is

C

=

360000(4038)

f ' 3496

= $415,812

In the manufacturing and service industries, tabulated cost indexes are not read-

ily available. The cost index will vary, perhaps with the region

of

the country, the

type

of

product

or

serv

ic

e, and many other factors.

When

estimating costs for a man-

ufacturing system, it is often necessary to develop the cost index for high-priority

cost variables such as subcontracted components, selected materials, and labor

costs.

The

development

of

the cost index requires the actual cost at different

ti

mes

for a prescribed quantity and quality

of

the item. The base period is a selected time

when the index

is

defined with a basis value

of

100 (or 1

).

The

index each year (pe-

riod)

is

determjned as the cost divided by the base-year cost and multiplied by 100.

Future index values may be forecast using simple extrapolation

or

more refined

mathematical techniques, such as time-series analysis. The development

of

cost

indexes

is

illustrated in the next example.

EXAMPLE

15.2

'-.

A manufacturing engineer with Hughes Industries

is

in the process

of

estimating costs

for a plant expansion. Two important items used

in

the manufacturing process are a sub-

contracted circuit board and a preprocessed platinum alloy. Spot checks on the co

n-

tracted prices through the Purchasing Department at 6-month intervals (first and third

quarters, or Q

I and Q3) show the following historical costs. Make the first quarter

of

2001 the base period, and determine the cost indexes us

in

g a basis

of

100.

Year 1999 2000 2001 2002

Ouarter

01

03

01

03

01

03

01

CiJ'cuit board, $/unit 57.00 56.90 56.90 56.70 56.60 56.40 56.25

Platinum alloy, $Iounce 446 450 455 575 610 625 635

Solution

For each item, the index

(1

,/

/

0

)

is

calc

ul

ated with the first-quarter

200

1 cost used for the

10 value. As indicated by the cost indexes shown, the index for the circuit board is sta-

ble, while the platinum a

ll

oy index is steadily

ri

sing.

SECTION

15

.3 Cost-Estimating Relationships: Cost-Capacity Equations

Year

Quarter

Q1

1999

Q3

2000

Q1

2001

Q3

Q1

Q3

2002

Q1

Circuit board cost i.ndex

Platin

um

a

ll

oy cost index

100.71 100.53 100.53 100.17 100.00 99.

65

99.38

73.11 73.77 74.59 94.26

100.00 102.46 104.10

Comment

Use

of

the cost index for forecasting costs sho

ul

d be performed with a good under-

standing

of

the vari

ab

le itself. The cost index

of

the platinum a

ll

oy

is

rising, but plat-

inum

is

much more susceptible to economic market trends and conditions than the

circuit board cost. Accordingly, cost indexes are often more reliable to estimate present

and short-term future costs.

Cost indexes are sensitive over time to technological change. The predefined

quantity and quality used to obtain cost values may be difficult to retain through

time, so

"index creep" may occur. Updating

of

the index and its definition

is

nec-

essary when identifiable changes occur.

15.3

COST-ESTIMATING RELATIONSHIPS:

COST-CAPACITY EQUATIONS

Design variables (speed, weight, thrust, physical size, etc.) for plants, equipment,

and construction are determined

in

the early design stages. Cost-estimating rela-

tionships (CER) use these design variables to predict costs. Thus, a

CE

R is

generically different from the cost index method, because the index

is

based on

the cost history

of

a defined quantity and quality

of

a variable.

One

of

the most widely used

CER

models

is

a cost-capacity equation. As the

name implies, an equation relates the cost

of

a component, system, or plant to its

capacity. This is also known as the

power law and sizing model. Since many cost-

capacity equations plot as a straight line on log-log paper, a common form

is

where

C\

= cost at capacity Q\

C

2

= cost at capacity Q

2

x = correlating exponent

[15.2]

The value

of

the exponent for various components, systems, or entire plants can

be obtained or derived from a number

of

SOUfces,

including Plant Design and

Economics for Chemical Engineers, Preliminary

Plant Design in Chemical En-

gineering,

Ch

emical Engineers' Handbook, technicaljoumals (especially

Ch

em-

ical Engineering),

the U.S. Environmental Protection Agency, professional or

trade organization

s,

consulting firms, handbooks, and equipment companies.

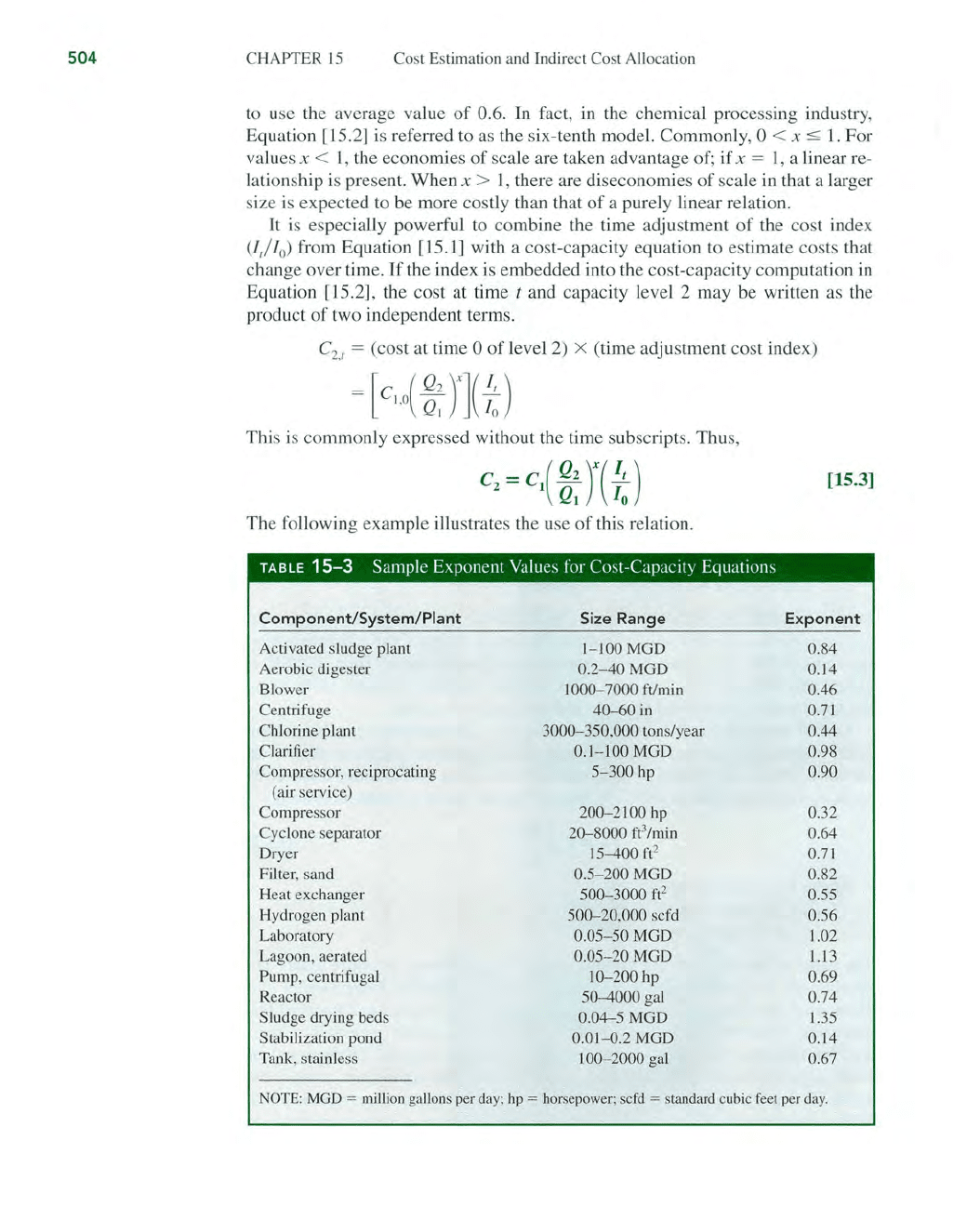

Table

15-3

is

a partial listing

of

typical values

of

the exponent

fOf

various units.

When an exponent value for a partic

ul

ar unit is not known, it

is

common practice

503

504

CHAPTER

15

Cost

Estimation and Indirect Cost Allocation

to use the average value

of

0.6. In fact,

in

the chemical processing industry,

Equation [15.2] is refelTed to as the six-tenth model. Commonly,

0 <

x:::;

1.

For

values

x <

1,

the economies

of

scale are taken advantage of; if x =

1,

a linear re-

lationship

is

present. When x >

1,

there are diseconomies

of

scale

in

that a larger

size is expected to be more costly than that

of

a purely linear relation.

It

is especially powerful to combine the time adjustment

of

the cost index

(1

,/

1

0

)

from Equation [15.1] with a cost-capacity equation to estimate costs that

change over time.

If

the index is embedded into the cost-capacity computation

in

Equation [15.2], the cost at time t and capacity level 2 may be written as the

product

of

two independent terms.

C

2.t

= (cost at time 0

of

level 2) X (time adjustment cost index)

This

is

commonly expressed without the time subscripts. Thus,

[15.3]

The following example illustrates the use

of

this relation.

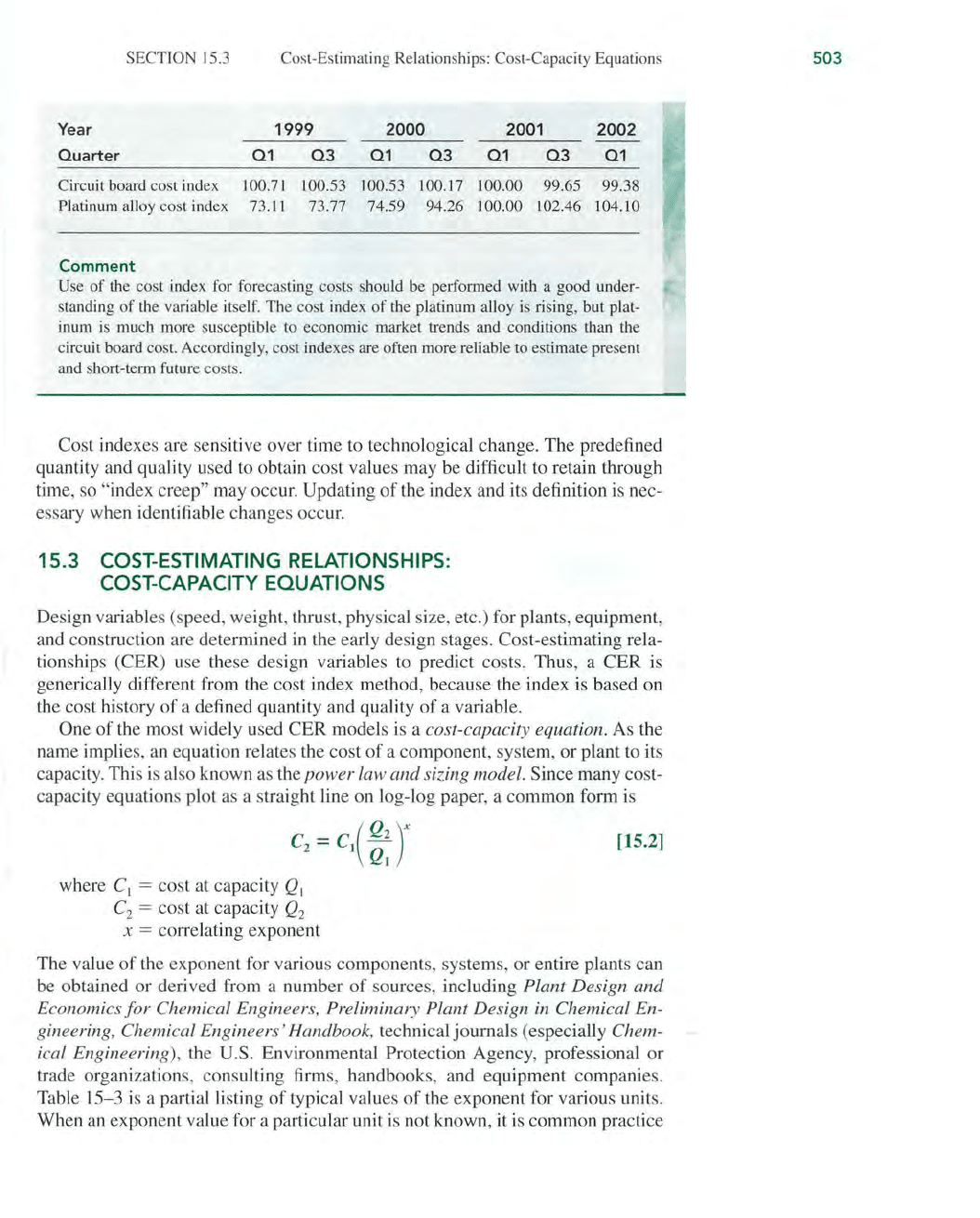

TABLE

15-3

Sample Exponent

Va

lu

es for Cost-Capacity E

qu

at

ions

C

omponent/S

y

stem/

Plant Size R

ange

Ex

pon

ent

Activated sludge

plant

l-lOOMGD

0.84

Aerobic digester

0.2-40MGD

0.14

Blower

1000-7000 ft/min 0.46

Centrifuge

40-60

in

0.71

Chlorine plant

3000-350,000

tons/year 0.44

Clarifier

0.1-100

MGD

0.98

Compressor, reciprocating

5-300

hp 0.90

(air service)

Compressor

200-2100

hp 0.32

Cyclone separator

20-8000

fe/min

0.64

Dryer

15-400

ft

2

0.71

Filter, sand 0.

5-200MGD

0.82

Heat

exchanger

500-3000

ft

2

0.55

Hydrogen plant

500-20,000

scfd

0.56

Laboratory

0.05-50MGD

1.02

Lagoon, aerated

0.05-20MGD

1.13

Pump

, centrifugal

10-200

hp

0.69

Reactor

50-4000

gal 0.74

Sludge drying beds

0.04-5MGD

1.35

Stabilization pond

0.01-0.2

MGD

0.14

Tank, stainless JOO-2000 gal 0.67

NOTE: MGD = million gallons per day; hp = horsepower; scfd = standard cubic feet per day.