Blank L., Tarquin A. Engineering Economy (McGraw-Hill Series in Industrial Engineering and Management)

Подождите немного. Документ загружается.

goes

to

office area employees. Be-

cause

of

this apparent imbalance in

expenditures, a split allocation

of

the

$200,200 amount is proposed: 80%

of

total dollars allocated via ABC

with the activities being the number

of accide

nts

occurring

in

generation

areas and the cost pool being

80%

of

the total safety program expendi-

tures; and

20%

of

the total dollars

using the traditional indirect cost

FE

REVIEW PROBLEMS

15.48 The cost

of

constructing a certain building

in 1999 was

$400,000. The ENR construc-

tion cost index was

6059 at that time.

If

the

ENR

index now is 6950, the cost

of

constructing a similar building is closest

to

(a) Less than $450,000

(b) $508,300

(c) $458,800

(d) More than $600,000

15.49

An

assembly line robot with a first

cost

of

$75,000

in

1995 had a cost

of

$89,750

in

2004.

If

the M&S equipment

cost index was

1027

in

1995 and the

robot cost increased exactly

in

propor-

tion

to

the index, the value

of

the index

in

2004 was closest

to

(a) Slightly less than 1250

(b)

1105.2

(c)

9]4

.6

(d)

Slightly more than 1400

CASE STUDY

State

CASE STUDY 525

allocation method with a basis of

number

of

office area employees. The

following data have been collected.

Number

of

Number

of

Employees

Accidents

Generation

Office

Generation

Office

Area Area

Area Area

Californ

ia

Arizona

300

200

600

300

405

20

125

10

15.50 A 50-horsepower turbine pump was pur-

chased for

$2100.

If

the exponent in the

cost capacity equation has a value

of

0.76, a 200-horsepower turbine could be

expected

to

cost about

Ca)

Less than $5000

(b)

$6020

Cc)

$5975

Cd)

More than $6100

15.51 The cost

of

a certain machine was

$15,000 in 2000 when the M&S equip-

ment cost index was 1092.

If

the current

index

is

] 164 and the exponent

in

the cost-

capacity equation had a value

of

0.65, the

cost now

of

a similar machine twice

as

large would be estimated to be about

(a) Less than $24,000

(b) $25,100

(c) $28,500

(d)

More than $30,000

TOTAL COST ESTIMATES FOR OPTIMIZING COAGULANT DOSAGE

Background

There are several processes involved

in

the treatment

of

drinking water, but three

of

the most important ones

are associated with removal

of

suspended matter,

which

is

known as turbidity. Turbidity removal is

brought about by adding chemicals that cause the

small suspended solids to clump together (coagula-

tion), forming larger particles

which can be removed

526

CHAPTER

15

Cost Estimation and Indirect Cost Allocation

through settling (sedimentation). The few particles that

remain after sedimentation are filtered out

in

sand, car-

bon, or coal filters

(fi

ltration).

In

general,

as

the dosage of chemicals is increased,

more

"clumping" occurs (up

to

a point), so there

is

increased removal

of

particles through the settling

process. This means that fewer particles have

to

be re-

moved through filtration, which obviously

meanS

that

the filter will not have to be cleaned

as

often through

backwashing. Thus, more chemicals mean less back-

wash water and vice versa. Since backwash water

and chemicals both have costs, a primary question is,

What amount

of

chemicals will result in the lowest

overall cost when the chemical coagulation and filtra-

tion processes are considered together?

Formulation

To

minimize the total cost associated with coagulation

a

nd

filtration, it is necessary to obtain the relationship

between

th

e chemical dosage and water turbidity after

coagulation and sedimentation, but before filtration.

This allows the chemical costs for different operating

strategies

to

be determined. This cost relationship,

derived using polynomi

al

regression analysis,

is

shown

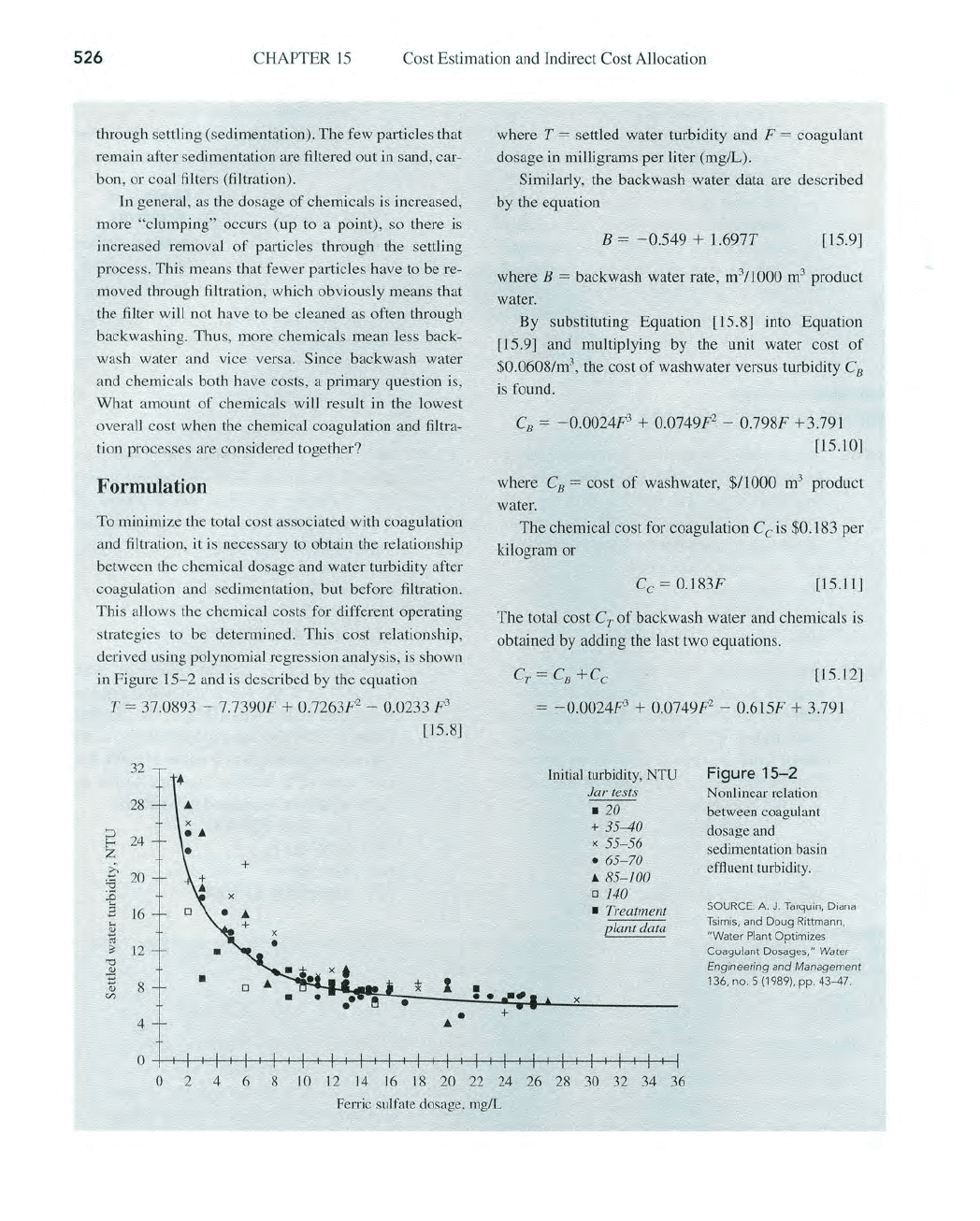

in Figure

15

-2

and

is

described by the equation

T = 37.0893 - 7.7390F + 0.7263F2 - 0.0233

F3

(15.8]

32

•

28

...

~

24

~

i'

+

~

20

x

'"

B

16

B

oj

~

12

"0

'"

'E

8

•

;l-

I

<I.l

CIl

•

4

...

•

•

••

where T = settled water turbidity and F = coagulant

dosage

in

milligrams per liter (mg/L).

SimilarlY, the backwash water data are described

by the equation

B =

-0.549

+ 1.697T

[15

.9

]

where

B = backwash water rate, m

3

/1000 m

3

product

water.

By substituting Equation [15.8] into Equation

[15.9] and multiplying by the unit water cost of

$0.0608/m

3

,

the cost

of

washwater versus turbidity C

s

is found.

C

s

= -0.0024F3 + 0.0749F

2

- 0.798F +3.791

[15.1

0]

where C

s

= cost

of

wash water, $/1000 m

3

product

water.

The chemical cost for coagulation

C

c

is $0.183 per

kilogram or

C

c

= 0.18

3F

[15.11]

The total cost

C

T

of

backwash water and chemicals

is

obtained

by

adding the last two equations.

-

+

(15.12]

=

-0.0024F3

+ 0.0749F

2

- 0.615F + 3.791

Initial turbidity, NTU

Jar tests

x

.20

+ 35-40

x 55-

56

• 65-70

...

85-100

o

140

• Treatment

plant data

Figure

15-2

Nonlinear relation

between coagulant

dosage and

sedimentation basin

effluent turbidity.

SOURCE:

A.

J. Tarquin, Diana

T5imis,

and

Doug

Rittmann,

"Water Plant Optimizes

Coagulant Dosages,

IJ

Water

Engineering and Management

136, no. 5 (1989). pp. 43-47.

o 2 4 6 8

10

12

14

16

18

20

22

24

26

28

30 32 34 36

Ferric sulfate dosage, mg/L

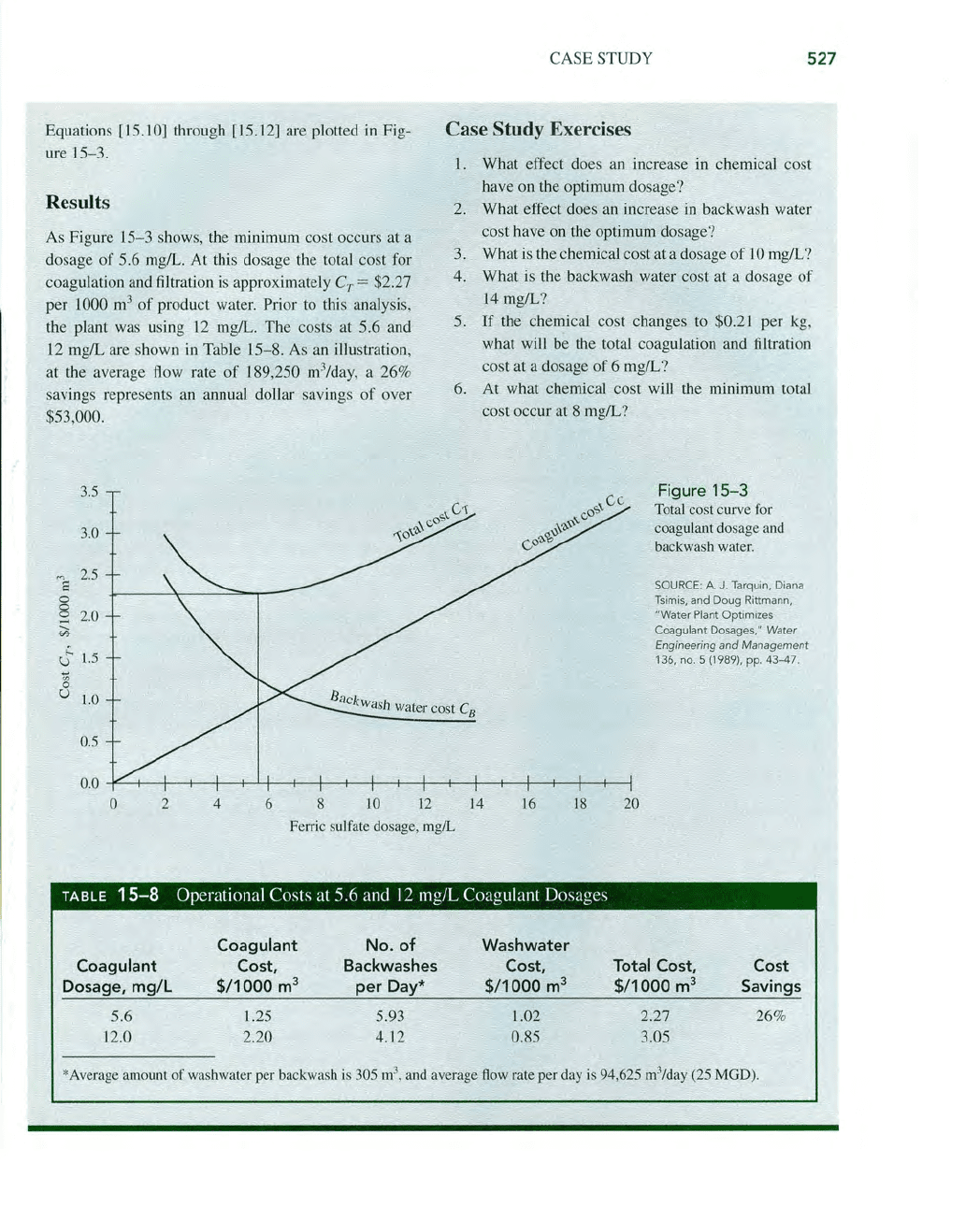

Equations [15.10] through [15.1

2]

are plotted

in

Fig-

ure

15

-

3.

Results

As

Figure

15

- 3 show

s,

the minimum cost occurs at a

dosage

of

5.6 mg/L. At this dosage the total cost for

coag

ul

ation and filtration is approximately C

T

= $2.27

per

1000 m

3

of product water. Prior to this analysis,

the plant was us

in

g 12 mg/L. The costs at 5.6 a

nd

12

mg/L are shown in Table

15

-

8.

As

an

illustra

ti

on,

at the average flow rate

of

189,250 m

3

/day, a 26%

savings represents

an

annual dollar savings

of

over

$53,000.

3.5

3.0

"'2

2.5

0

0

S

2.0

;;;.

.::,

1.5

U

u:

0

U

1.0

0.5

0.0

0

2

4

6 8

10

12

CASE STUDY

527

Case Study Exercises

1.

What effect does

an

increase in chemical cost

have on the optimum dosage?

2.

What effect does

an

increase in backwash water

cost have on the optimum dosage?

3.

What is the chemical cost at a dosage

of

10

mg/L?

4.

What is the backwash water cost at a dosage

of

14 mg/L?

5.

If

the chemical cost changes to $0.21 per kg,

what will be the total coagulation and filtration

cost at a dosage

of

6 mglL?

6. At what che

mi

cal cost will the minimum total

cost occur at 8 mg/L?

14

16

18 20

Figure

15-3

Total cost curve for

coag

ul

a

nt

dosage a

nd

backwash water.

SOURCE: A. J. Tarquin, Diana

Ts

imis, and D

oug

Ri

ttman

n,

"

Wa

te

r Plant

Op

timizes

Coagulant

Dosages," W

ate

r

Engineering

an

d Man

agemen

t

136, no. 5 (1989), pp. 4

3-47

.

Fe

rri

c sulfate dosage, mg/L

TABLE

15-8

Operational Costs at 5.6 and

12

mg/L Coagulant Dosages

Coagulant

No.

of

Washwater

Coagulant

Cost, Backwashes Cost,

Total Cost,

Cost

Dosage,

mg/L

$/1000

m

3

per

Day*

$/1000

m

3

$/1000

m

3

Savings

5.6 1.25 5.93 1.02 2.27

26%

12.0 2.20 4.12 0.85 3.05

* Average amount

of

washwater per backwash is 305 m

3

,

and average

fl

ow rate per day

is

94,625 m

3

/day (25 MGD).

528

CHAPTER 15

Cost Est

im

ation and Indirect Cost Allocation

CASE

STUDY

INDIRECT

COST

COMPARISON

OF

MEDICAL

EQUIPMENT

STERILIZATION

UNIT

The Product

Three years ago Medical Dynamics, a medical equip-

ment unit

of

Johnson and Sons,

In

c., initiated the man-

ufacture and sales

of

a portable sterilization unit

(Quik-Sterz) that can be placed

in

the hospital room

of

a patient. This unit sterilizes a

nd

makes available at the

beds

id

e some

of

the

reu

sa

bl

e

in

strumen

ts

that nurses

and doctors usua

ll

y obtain by walking to

or

having de-

livered from a centralized area. This new unit makes

the

in

struments available at the po

in

t a

nd

ti

me

of

use

for burn and severe wound patients who are in a regu-

lar patient room.

There are two models

of

Quik-Sterz sold. The stan-

dard version sells for $10.75, and a premium version

with customized trays and a battery backup system

se

ll

s for $29.75. The product has sold we

ll

to hospitals,

convalescent units, and nursing homes

at

the level

of

about I million units per year.

Cost Allocation Procedures

Medical Dyna

mi

cs has historically used an indirect

cost allocation system based upon direct hours to man-

uf

acture for

al

l its other product lines.

The

sa

me

was

app

li

ed when Quik-Sterz was priced. However, Arnie,

the person who perfOlmed the indirect cost

ana

lysis

and set the sales price, is no longer at the company, and

th

e deta

il

ed analysis is no longer available. Through

e-mail and telephone conversations, Arnie said the cur-

rent price was set at about 10% above dle total manu-

facturing cost determiJled 2 years ago, and that some

records were available in the design department

fil

es. A

search

of

these files revealed the manufacturing and

cost information

in

Table

15-9

.

It

is

clear from these

and o

th

er records

th

at

Arnie used traditional indirect

cost analysis based

on

dil"ect

labor hours to estimate the

total manufacturing costs

of

$9.73 p

er

unit for the stan-

dard model and

$27.07 per unit for

th

e premium model.

TABLE

15-9

Historical Records

of

Direct and Indirect Cost Analyses for Quik-Sterz

Ouick-Sterz Direct Cost (DC) Evaluation

Direct Labor, Direct Material,

Direct Labor,

Model

$/Unit*

$/Unit

Hours/Unit

Standa

rd

$ 5.00 $2.50 0.25

Pr

emium 10.

00

3.75 0

.5

0

Ouick-Sterz Indirect Cost (IDC) Evaluation

Direct Labor, Fraction IDC Allocated

Model

Hours/Unit Allocated IDC

0.25

I

$1.67 million

-

3

Standa

rd

Premium

0.50

2

3.33 million

3

*Average direct labor rate is $20 per hou

r.

Total Direct

Labor Hours

187,

500

125,000

Sales,

Units/Year

750,000

250,000

CASE

STUDY

529

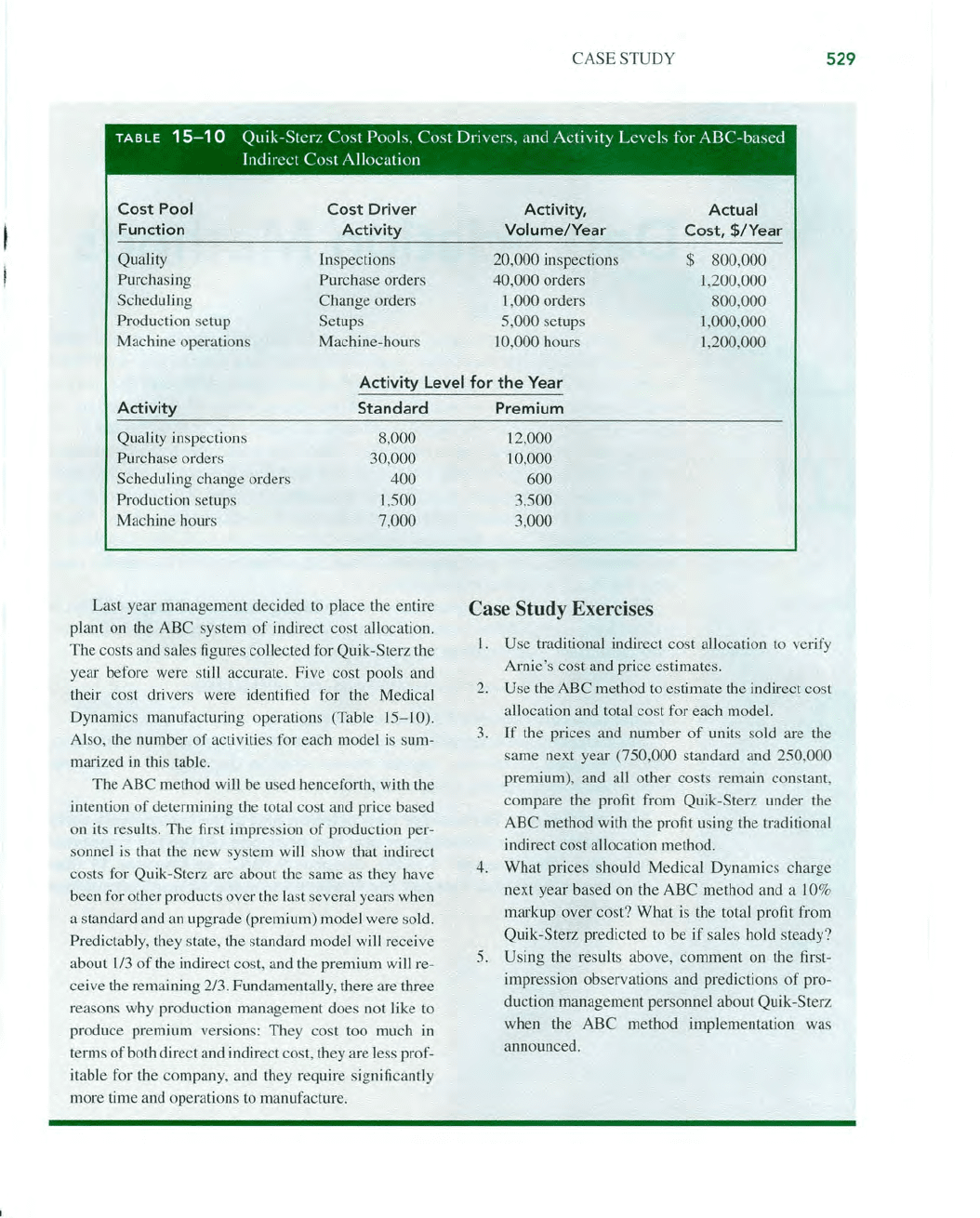

TABLE

15-10

Quik-Sterz

Cost

Pools.

Cos

t Drivers. and Activity Levels for ABC-based

Indirect Cost A

ll

oca

ti

on

Cost Pool

Function

Quality

Purchasing

Sche

duLin

g

Produc

ti

on

se

tup

Machine opera

ti

ons

Co

st

Driver

Activity

Inspections

Purchase orders

Change orders

Setups

Ma

chjne-hours

Activity,

Volume/Year

20,000 inspections

40,000 orders

1,000 orders

5,000 setups

10

,000 hours

Actual

Cost,

$/Year

$ 800,000

1,200,000

800,000

1,000,000

1,200,000

Activity

Activity Level for the Year

Standard Premium

Qua

li

ty

inspections

Purchase orders

Scheduling change orders

Produ

ct

ion

se

tups

Machine hours

8,000

30,000

400

1,500

7,000

La

st year management decided to place the entire

pJ

ant on the ABC system

of

indlrect cost alloca

ti

on.

The costs and sales

fi

gures

co

ll

ected for Quik-Sterz the

year before were still accurate. Five cost pools a

nd

th

eir cost drivers were

id

entified for the

Med

ical

Dynamics ma

nu

factur

in

g operations (Table

15

- 10).

Also,

th

e number

of

ac

ti

v

iti

es for each model is sum-

marized

in

this ta

bl

e.

The ABC me

th

od will be

lI

sed hen

cef

orth, with

th

e

inte

nti

on

of

determining the total cost aud price based

on i

ts

result

s.

The

fi

rst impression

of

production per-

so

nn

el is

th

at

th

e new system

wi

ll show

th

at indirect

costs for Quik-Sterz are about

th

e

sa

me as they have

been for other products over the l

ast

several years when

a standard and an upgrade (prem

iu

m) model were sold.

Predictabl

y,

they state, the standa

rd

model w

ill

receive

about

11

3 of

th

e indirect cost, a

nd

the premium

wi

ll

re-

ceive

th

e rema

in

ing 2/3. Fundamen

ta

lly, there are thr

ee

reasons why produc

ti

on management does not

li

ke

to

produce premium version

s:

They cost too much

in

terms of bo

th

djrect and indirect cost, they are less prof-

it

able for the company, and

th

ey require sig

nifi

cantly

more time and operations to manufacture.

12

,000

10,000

600

3,500

3,000

Case Study

Ex

ercises

1.

Use traditional indirect cost allocation to verify

Arnie's cost a

nd

pr

ice estimate

s.

2.

U

se

the ABC me

th

od to estimate the indlrect cost

a

ll

ocation and total cost for each model.

3.

If

th

e prices a

nd

number

of

units sold are the

same next year

(7

50,000 standard and 250,000

premium), and a

ll

other costs rema

in

constant,

compare the pro

fi

t from Quik-Sterz under the

A

BC

method with

th

e profit us

in

g the traditional

in

dl

rect cost allocation method.

4. What prices should Medical Dyna

mi

cs charge

next year based on the ABC method and a

10

%

markup over cost?

What

is the total profit from

Quik-Sterz predicted to be if sales hold steady?

5.

Us

ing the results above, comment on the first-

impression observations and predictions of pro-

duc

ti

on management perso

nn

el about Quik-Sterz

when the ABC method implementa

ti

on was

announced.

w

u

Depreciation Methods

The

capital

investments

of

a

corporation

in

tangible

assets-equipment,

computers,

vehicles,

buildings,

and

machinery-are

commonly

recovered

on

the

books

of

the

corporation

through

depreciation.

Although

the

depre-

ciation

amount

is

not

an actual cash flow,

the

process

of

depreciating

an

asset, also referred

to

as

capital recovery, accounts

for

the

decrease in

an

asset's value because

of

age, wear, and obsolescence. Even

though

an

asset

may

be

in

excellent

working

condition,

the

fact

that

it

is

worth

less

through

time

is

taken

into

account

in

economic

evaluation

studies.

An

introduction

to

the

classical

depreciation

methods

is

followed

by

a discussion

of

the

Modi-

fied

Accelerated

Cost

Recovery

System

(MACRS), which

is

the

standard in

the

United

States

for

tax

purposes

.

Other

countries

commonly

use

the

clas-

sical

methods

for

tax

computations.

Why

is

depreciation

important

to

engineering

economy?

Depreciation

is

a tax-allowed deduction

included

in

tax

calculations in virtually all industrial-

ized countries.

Depreciation

lowers

income

taxes via

the

relation

Taxes

= (income -

deductions)(tax

rate)

Income

taxes are discussed

further

in

Chapter

17.

This

chapter

concludes

with

an

introduction

to

two

methods

of

depletion,

which are used

to

recover

capital investments in

deposits

of

natural re-

sources such

as

minerals, ores,

and

timber.

Important

note:

To

consider depreciation and

after-tax

analysis early

in

a course, cover this

chapter

and

the

next

one (After-Tax Economic

Analysis)

after

Chapter

6 (AW),

Chapter

9 (B/C),

or

Chapter

11 (Re-

placement Analysis). Consult

the

Preface

for

more

options on subject

ordering.

LEARNING OBJECTIVES

Purpose: Use classical and

government-approved

methods

to

reduce

the

value

of

the

capital

investment

in

an asset

or

natural resource.

Depreciation terms

Straight line

Declining balance

Recovery period

Depletion

This

chapter

will

help

you:

1. Understand and use

the

basic

terminology

of

deprec

iation.

2.

App

ly

the

strai

ght

li

ne

model

of

depreciation.

3.

Apply

the

decl

ining balance and

double

declining

balance

mode

ls

of

deprec

iation.

4.

App

ly

th

e Modified Accelerat

ed

Cost

Recovery System

(M

AC

R

S)

of

dep

reciation f

or

U

.S.

corporation

s.

5. Select

the

recovery

per

i

od

of

an asset

for

MACRS

depreciation.

6.

Utilize

the

cost

dep

l

etion

and

percentage

depletion

methods

for

natural resource investments.

Chapter

Appendix

A

1.

Apply

the

sum-of-year

digits

method

of

depreciation.

A2.

Determine

when

to

switch from

one

depreciation

model

to

another

.

A3.

Compute

MACRS

deprec

iation rates

us

ing

depreciation

model

switching.

532 CHAPTER

16

Depreciation Methods

16

.1 DEPRECIATION TERMINOLOGY

Primary terms used

in

depreciation are defined here. Most terms are applicable to

corporations as well as individuals who own depreciable assets.

Depreciation

is

the reduction

in

value

of

an asset. The method used to depre-

ciate an asset is a way to account for the decreasing value

of

the asset

to

the

owner

and

to represent the diminishing value (amount)

of

the capital funds

invested

in

it. The annual depreciation amount

D/

does not represent

an

actual cash

flow,

nor does it necessarily reflect the actual usage pattern

of

the asset during ownership.

Book

depreciation

and

tax

depreciation

are terms used to describe the purpose

for reducing asset value. Depreciation may be performed for two reasons:

I. Use

by

a corporation

or

business for internal financial accounting.

This

is

book depreciation.

2.

Use

in

tax calculations per government regulations. This

is

tax depre-

ciation.

The methods applied for these two purposes

mayor

may not utilize the same

formulas, as is discussed later. Book depreciation indicates the reduced

in-

vestment

in

an asset based upon the usage pattern and expected useful life

of

the asset. There are classical, internationally accepted depreciation meth-

ods used to determine book depreciation: straight line, declining balance,

and the infrequently used sum-of-year digits method. The amount

of

tax de-

pr

eciation is important in

an

after-tax engineering economy study because

of

the following:

In

the

United

States

and

many

industrialized

countries,

the

annual

tax

depreciation

is

tax

deductible;

that

is,

it

is

subtracted

from

in-

come

when

calculating

the

amount

of

taxes

due

each

year. However,

the

tax

depreciation

amount

must

be

calculated

using a

government-

approved

method.

Tax depreciation may be calculated and referred to differently

in

countries

outside the

United States. For example,

in

Canada the equivalent

is

CCA

(capital cost allowance), which

is

calculated based on the undepreciated

val

ue

of

all corporate properties that form a particular class

of

assets, whereas

in

the

United States, depreciation may be determined for each asset separately.

Where allowed, tax depreciation

is

usually based on

an

accelerated

method, whereby the depreciation for the first years

of

use is larger than that

for later years. In the

United States, this method

is

called MACRS, as covered

in

later sections. In effect, accelerated methods defer some

of

the income tax

burden to later

in

the asset's life; they do not reduce the total tax burden.

First

cost or

unadjusted

basis

is

the delivered and installed cost

of

the asset

including purchase price, delivery and installation fees, and other deprecia-

ble direct costs incurred to prepare the asset for use. The term unadjusted

basis

B,

or simply basis,

is

used when the asset

is

new, with the term ad-

justed basis used after some depreciation has been charged.

SECTION

16.

I Depreciation Terminology

Book

value

represents the remaining, undepreciated capital investment on the

books after the total amount

of

depreciation charges to date have been sub-

tracted from the basis. The book value BV

r

is

usually determined at the end

of

each year, which

is

consistent with the end-of-year convention.

Recovery

period

is

the depreciable life n

of

the asset

in

years. Often there are

different n values for book and tax depreciation. Both

of

these values may

be different from the asset's estimated productive life.

Market

value, a term also used in replacement analysis, is the estimated

amount real izable if the asset were sold on the open market. Because

of

the

structure

of

depreciation laws, the book value and market value may be

substantially different. For example, a commercial building tends to in-

crease

in

market value, but the book value will decrease as depreciation

charges are taken. However, a computer workstation may have a market

value much lower than its book value due to rapidly changing technology.

Salvage

value

is

the estimated trade-in

or

market value at the end

of

the

asset's useful life. The salvage value, S expressed as an estimated dollar

amount

or

as a percentage

of

the first cost, may be positive, zero,

or

nega-

tive due to dismantling and carry-away costs.

Depreciation

rate

or

recovery

rate

is

the fraction

of

the first cost removed by

depreciation each year. This rate, denoted by

dl' may be the

same

each year,

which

is

called the straight-line rate,

or

different for each year

of

the

recovery period.

Personal

property,

one

of

the two types

of

property for which depreciation

is

allowed,

is

the income-producing, tangible possessions

of

a corporation

used to conduct business. Included is most manufacturing and service

industry

property-vehicles,

manufacturing equipment, materials handling

devices, computers and networking equipment, telephone equipment,

office furniture, refining process equipment, construction assets, and much

more.

Real

property

includes real estate and all

improvements-office

buildings,

manufacturing structures, test facilities, warehouses, apartments, and other

structures. Land

itself

is considered real property,

but

it is

not

depreciable.

Half-year

convention

assumes that assets are placed in service

or

disposed

of

in

midyear, regardless

of

when these events actually occur during the year.

This convention

is

utilized

in

this text and in most U.S.-approved tax de-

preciation methods. There are also midquarter and midmonth conventions.

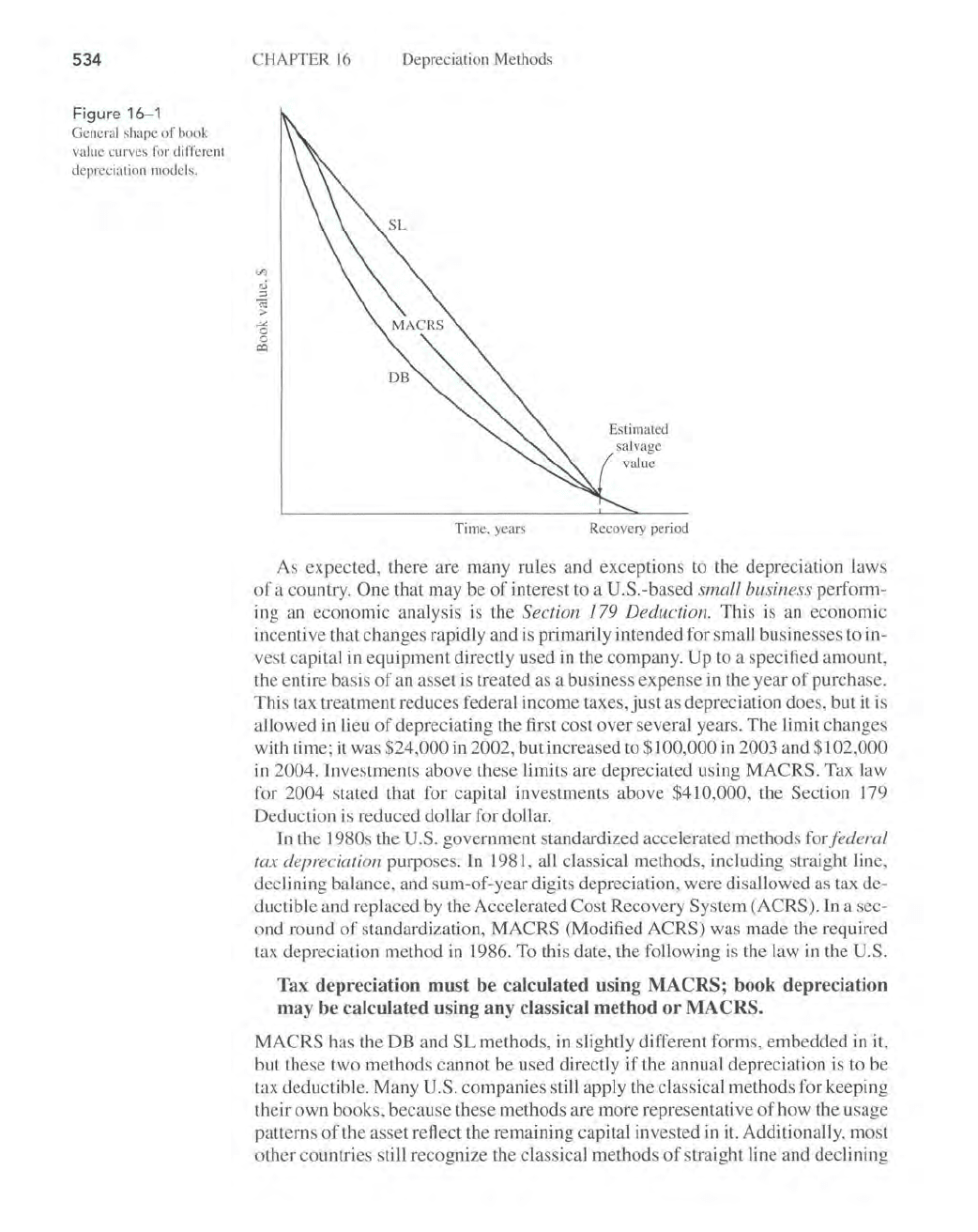

As

mentioned before, there are several models for depreciating assets. The

straight line (SL) model

is

used, historically and internationally. Accelerated

models, such as the declining balance (DB) model, decrease the book value to

zero (or to the salvage value) more rapidly than the straight line method, as

shown by the general book value curves in Figure 16-1.

For the classical

methods-straight

line, declining balance, and sum-oF-year dig-

its

(SYD)-there

are Excel functions available to determine annual depreciation.

Each function

is

introduced and illustrated as the method is explained. Since SYD

is applied less frequently,

it

is

summarized

in

the appendix to this chapter.

533

I Sec. J6A.1 I

534

Figure

16-1

General shape or book

value curv

es

for difTere

nt

depr

ec

iation model

s.

CHAP

TE

R 16

Depreciation Methods

-'"

o

o

co

Tim

e, years

Estimat

ed

s

al

vage

va

lue

R

ec

o

ve

ry period

As expected, there are many rules and exceptions to the depreciation laws

of

a country. One that may be

of

interest to a U.S.-based small busin.ess perform-

in

g an economic analysis

is

the Section 179 Deduction. This is an economic

incentive

th

at changes rapidly and

is

primarily intended for small businesses to in-

vest capital

in

equipment directly used in the company. Up to a specified amount,

th

e entire basis

of

an asset is treated as a business expense

in

th

e year

of

purchase.

This tax treatment reduces federal income taxes,

ju

st as depreciation does, but it is

allowed

in

lieu

of

depreciating the first cost over several years.

The

limit changes

with time; it was

$24,000 in 2002, but increased to $100,000 in 2003 and $102,000

in

2004. Investments above these limits are depreciated using MACRS. Tax law

for

2004 stated that for capital investments above $410,000, the Section 179

Deduction is reduced dollar for dollar.

In

the 1980s the U.S. government standardized accelerated methods

fo

rJ

ederal

tax de

pr

eciation purposes.

In

1981

, all classical methods, including straight line,

declining balance, and sum-of-year digits depreciation, were disallowed as tax de-

ductible and replaced

by

the Accelerated Cost Recovery System (ACRS). In a sec-

ond round

of

standardization, MACRS (Modified ACRS) was made the required

tax depreciation method in ] 986. To this date, the following is the law

in

the U.S.

Tax depreciation

must

be calculated using MACRS; book depreciation

may be calculated using

any

classical method

or

MACRS.

MACRS has the DB and

SL

methods,

in

slightly different forms, embedded in it,

but these two methods cannot be used directly

if

the annual depreciation

is

to be

tax deductible. Many

U.S. companies still apply the classical methods for keeping

th

eir own books, because these methods are more representative

of

how the usage

patte

rn

s of the asset re

fl

ect the remaining capital invested in

it.

Additionally, most

o

th

er countries still recognize the classical methods

of

straight line and declining